FINA6000: Case Study on Australian IPOs and Finance Management

VerifiedAdded on 2023/03/30

|21

|2982

|273

Case Study

AI Summary

This case study examines the efficiency of Initial Public Offerings (IPOs) conducted in Australia from 2007 to 2013, focusing on three companies: iSelect, Sandon Capital Investments, and Virtus Health. The analysis assesses the funds raised, their intended uses, and the actual outcomes, including debt reduction and capital expansion. The study evaluates the returns generated on the first day of trading, identifying levels of underpricing, and calculates the cost of capital post-IPO for each company. Furthermore, it explores the IPO activity in Australia, correlating it with capital market conditions and providing a detailed comparison of returns for the selected IPOs over a five-year period. The findings highlight the impact of market dynamics on IPO success and the importance of understanding underpricing and cost of capital in financial decision-making.

Running head: MANAGING FINANCE

Managing Finance

Name of the Student:

Name of the University:

Authors Note:

Managing Finance

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGING FINANCE

1

Table of Contents

Introduction:...............................................................................................................................2

Answer to a:...............................................................................................................................2

Answer to b:...............................................................................................................................3

Answer to c:...............................................................................................................................4

Answer to d:...............................................................................................................................6

Answer to e:...............................................................................................................................7

Answer to f:................................................................................................................................9

Conclusion:..............................................................................................................................14

References and Bibliography:..................................................................................................15

1

Table of Contents

Introduction:...............................................................................................................................2

Answer to a:...............................................................................................................................2

Answer to b:...............................................................................................................................3

Answer to c:...............................................................................................................................4

Answer to d:...............................................................................................................................6

Answer to e:...............................................................................................................................7

Answer to f:................................................................................................................................9

Conclusion:..............................................................................................................................14

References and Bibliography:..................................................................................................15

MANAGING FINANCE

2

Introduction:

The aim of the assessment is to detect efficiency of the IPOs that has been conducted

in Australia over the period of time. There is adequate analysis conducted on the overall IPOs

which tissue during 2013 whose main purpose was to acquire the required level of funding

support their future expansion and debt combination. Moreover, the assessment evaluates the

overall returns that have been generated by the initial public offering during the first day of

trade. In addition, this relevant comparison of the first day return is relatively conducted to

identify the levels of underpricing which is present within the initial public offerings of

organization. Further evaluation has been conducted on the overall value of cost of capital

that has already changed for the organizations after the initial public offering. Lastly,

adequate measures are taken to provide information about the IPO activity in Australia and

relevant returns that has been provided by the three selected IPO during five financial years..

Answer to a:

Company

Name

Industry Date

of

IPO

Amount

intended to

raise

Amount

actually

raised

The purpose of the funds

iSelect health

insurance

Jun-

13

$215m $215m The main purpose of the fund

acquisition it to reduce debt and

increase acquisition of

additional capital funding’s

Sandon

Capital

Investments

Diversified

financial

Dec-

13

$100m $100m The fund acquisition is

conducted to increase the

relevant fund, which might help

in minimising the risk exposure

2

Introduction:

The aim of the assessment is to detect efficiency of the IPOs that has been conducted

in Australia over the period of time. There is adequate analysis conducted on the overall IPOs

which tissue during 2013 whose main purpose was to acquire the required level of funding

support their future expansion and debt combination. Moreover, the assessment evaluates the

overall returns that have been generated by the initial public offering during the first day of

trade. In addition, this relevant comparison of the first day return is relatively conducted to

identify the levels of underpricing which is present within the initial public offerings of

organization. Further evaluation has been conducted on the overall value of cost of capital

that has already changed for the organizations after the initial public offering. Lastly,

adequate measures are taken to provide information about the IPO activity in Australia and

relevant returns that has been provided by the three selected IPO during five financial years..

Answer to a:

Company

Name

Industry Date

of

IPO

Amount

intended to

raise

Amount

actually

raised

The purpose of the funds

iSelect health

insurance

Jun-

13

$215m $215m The main purpose of the fund

acquisition it to reduce debt and

increase acquisition of

additional capital funding’s

Sandon

Capital

Investments

Diversified

financial

Dec-

13

$100m $100m The fund acquisition is

conducted to increase the

relevant fund, which might help

in minimising the risk exposure

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGING FINANCE

3

of the organisation

Virtus Health Healthcare

Equipment

Jun-

13

$346.5m $346.5m The IPO funding is required by

the organisation for minimising

the exposure of debt in their

capital requirements

The companies initiating the IPO structure has adequately gather all the relevant

funding for their operational needs. The purpose of the funds have been meet adequately, as

all the three companies were able to gather the relevant funding from their share issue.

Company iSelect

Sandon Capital

Investments Virtus Health

Industry

health

insurance Diversified financial

Healthcare

Equipment

Date of IPO 6/1/2013 12/1/2013 6/1/2013

Amount Raised $215m $100m $346.5m

Offer price $215m $100m $346.5m

Offer price 1.85 0.9835 5.68

Closing price on first day of

trading 1.55 0.95 6.28

Return on first day of trading -16.22% -3.41% 10.56%

Answer to b:

iSelect 2014

Growth(retention) 15.0%

Closing price 1.385

Dividend 0.0786

Cost of capital 20.7%

Sandon Capital

Investments 2014

Growth(retention) 5.0%

Closing price 0.945

Dividend 0.17

Cost of capital 22.76%

3

of the organisation

Virtus Health Healthcare

Equipment

Jun-

13

$346.5m $346.5m The IPO funding is required by

the organisation for minimising

the exposure of debt in their

capital requirements

The companies initiating the IPO structure has adequately gather all the relevant

funding for their operational needs. The purpose of the funds have been meet adequately, as

all the three companies were able to gather the relevant funding from their share issue.

Company iSelect

Sandon Capital

Investments Virtus Health

Industry

health

insurance Diversified financial

Healthcare

Equipment

Date of IPO 6/1/2013 12/1/2013 6/1/2013

Amount Raised $215m $100m $346.5m

Offer price $215m $100m $346.5m

Offer price 1.85 0.9835 5.68

Closing price on first day of

trading 1.55 0.95 6.28

Return on first day of trading -16.22% -3.41% 10.56%

Answer to b:

iSelect 2014

Growth(retention) 15.0%

Closing price 1.385

Dividend 0.0786

Cost of capital 20.7%

Sandon Capital

Investments 2014

Growth(retention) 5.0%

Closing price 0.945

Dividend 0.17

Cost of capital 22.76%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGING FINANCE

4

Virtus Health 2014

Growth(retention) 16.0%

Closing price 8.31

Dividend 0.095

Cost of capital 17.1%

The above calculations shed light on the overall cost of capital for all the three

companies that have initiated the initial public offering during the financial year 2013. The

cost of capital has been derived during 2014 by adequately identifying all the relevant values

from the annual report. The analysis directly indicates that cost of capital of the organization

was relatively zero, as the companies were not trading shares in the capital market, which is

the main reason why the actual cost of the capital is not derived. From the analysis, it could

be identified that the dividend anticipated by the organization with the growth conditions is a

relatively helpful in detecting the cost of capital for each organization. The detection of the

cost of capital would eventually allow the investors to identify the level of returns that needs

to be provided by the companies during the financial year. The range of cost of capital is

derived from the relevant growth conditions that are anticipated by the organization for its

future dividends. Therefore, it could be understood that the overall cost of capital for each

IPO is directly related to financial benefits that would be provided by the organization to the

shareholders (Au.finance.yahoo.com, 2019).

Answer to c:

Company iSelect

Sandon Capital

Investments Virtus Health

Industry

health

insurance Diversified financial

Healthcare

Equipment

Date of IPO 6/1/2013 12/1/2013 6/1/2013

Amount Raised $215m $100m $346.5m

Offer amount $215m $100m $346.5m

Offer price 1.85 0.9835 5.68

Closing price on first day of 1.55 0.95 6.28

4

Virtus Health 2014

Growth(retention) 16.0%

Closing price 8.31

Dividend 0.095

Cost of capital 17.1%

The above calculations shed light on the overall cost of capital for all the three

companies that have initiated the initial public offering during the financial year 2013. The

cost of capital has been derived during 2014 by adequately identifying all the relevant values

from the annual report. The analysis directly indicates that cost of capital of the organization

was relatively zero, as the companies were not trading shares in the capital market, which is

the main reason why the actual cost of the capital is not derived. From the analysis, it could

be identified that the dividend anticipated by the organization with the growth conditions is a

relatively helpful in detecting the cost of capital for each organization. The detection of the

cost of capital would eventually allow the investors to identify the level of returns that needs

to be provided by the companies during the financial year. The range of cost of capital is

derived from the relevant growth conditions that are anticipated by the organization for its

future dividends. Therefore, it could be understood that the overall cost of capital for each

IPO is directly related to financial benefits that would be provided by the organization to the

shareholders (Au.finance.yahoo.com, 2019).

Answer to c:

Company iSelect

Sandon Capital

Investments Virtus Health

Industry

health

insurance Diversified financial

Healthcare

Equipment

Date of IPO 6/1/2013 12/1/2013 6/1/2013

Amount Raised $215m $100m $346.5m

Offer amount $215m $100m $346.5m

Offer price 1.85 0.9835 5.68

Closing price on first day of 1.55 0.95 6.28

MANAGING FINANCE

5

trading

Return on first day of trading -16.22% -3.41% 10.56%

Underpricing is a relevant concern for major organizations, as they are not able to

identify the level of Capital that would be generated from the overall initial public offering.

The underpricing measure directly impact the overall price of the organization, as investors

are focused on reducing the offer price of an organization to effectively generate higher

returns on the first day of trade. The above calculations and directly indicated that only the

IPO of Virtus Health was subject to underpricing method, as it generated a return of 10.56%

in the first day of trade. Hence, underpricing is present under different industries, which led

to the underpricing of Virtus Health IPO, as calculated in the above table. This mainly

indicated that the actual valuation of the company was higher, as the investors used the

underpricing method to reduce the initial public offering price of the organization. This is the

main reason why the overall returns on the first day of trade is relatively higher. The negative

impact of underpricing is relevantly present throughout the industry, as relevant research has

been conducted on the Australian market, which indicates that more than 33% of the IPOs

that are conducted during the year are underpriced. The confirmation is relevantly provided

from the analysis of the above table, where one of the three IPOs was affected by

underpricing effect (Asx.com.au, 2019).

5

trading

Return on first day of trading -16.22% -3.41% 10.56%

Underpricing is a relevant concern for major organizations, as they are not able to

identify the level of Capital that would be generated from the overall initial public offering.

The underpricing measure directly impact the overall price of the organization, as investors

are focused on reducing the offer price of an organization to effectively generate higher

returns on the first day of trade. The above calculations and directly indicated that only the

IPO of Virtus Health was subject to underpricing method, as it generated a return of 10.56%

in the first day of trade. Hence, underpricing is present under different industries, which led

to the underpricing of Virtus Health IPO, as calculated in the above table. This mainly

indicated that the actual valuation of the company was higher, as the investors used the

underpricing method to reduce the initial public offering price of the organization. This is the

main reason why the overall returns on the first day of trade is relatively higher. The negative

impact of underpricing is relevantly present throughout the industry, as relevant research has

been conducted on the Australian market, which indicates that more than 33% of the IPOs

that are conducted during the year are underpriced. The confirmation is relevantly provided

from the analysis of the above table, where one of the three IPOs was affected by

underpricing effect (Asx.com.au, 2019).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGING FINANCE

6

Answer to d:

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

-100.00%

-50.00%

0.00%

50.00%

100.00%

150.00%

Return Activity of IPO Return ALL Ordinary Index

Yea

r ALL Ordinary Index

Activity of

IPO Return

2007 6,416.7 260.0 ALL Ordinary Index Activity of IPO

2008 3,659.3 75.0 -42.97% -71.15%

2009 4,882.7 42.0 33.43% -44.00%

2010 4,846.9 99.0 -0.73% 135.71%

2011 4,111.0 105.0 -15.18% 6.06%

2012 4,664.6 51.0 13.47% -51.43%

2013 5,353.1 61.0 14.76% 19.61%

2014 5,388.6 73.0 0.66% 19.67%

2015 5,344.6 97.0 -0.82% 32.88%

2016 5,719.1 94.0 7.01% -3.09%

2017 6,167.3 115.0 7.84% 22.34%

The above table provides information about the IPO activity that has been derived

from different sources of Deloitte. From the relevant analysis, it could be identified that the

IPO activity is directly related to the overall financial performance of the capital market.

From the analysis, it could be identified that the before the financial crisis IPO was relatively

at its peak where 260 companies conducted the first public offering. However, the negative

impact of the financial crisis on the capital market has directly reduced due to the low

6

Answer to d:

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

-100.00%

-50.00%

0.00%

50.00%

100.00%

150.00%

Return Activity of IPO Return ALL Ordinary Index

Yea

r ALL Ordinary Index

Activity of

IPO Return

2007 6,416.7 260.0 ALL Ordinary Index Activity of IPO

2008 3,659.3 75.0 -42.97% -71.15%

2009 4,882.7 42.0 33.43% -44.00%

2010 4,846.9 99.0 -0.73% 135.71%

2011 4,111.0 105.0 -15.18% 6.06%

2012 4,664.6 51.0 13.47% -51.43%

2013 5,353.1 61.0 14.76% 19.61%

2014 5,388.6 73.0 0.66% 19.67%

2015 5,344.6 97.0 -0.82% 32.88%

2016 5,719.1 94.0 7.01% -3.09%

2017 6,167.3 115.0 7.84% 22.34%

The above table provides information about the IPO activity that has been derived

from different sources of Deloitte. From the relevant analysis, it could be identified that the

IPO activity is directly related to the overall financial performance of the capital market.

From the analysis, it could be identified that the before the financial crisis IPO was relatively

at its peak where 260 companies conducted the first public offering. However, the negative

impact of the financial crisis on the capital market has directly reduced due to the low

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGING FINANCE

7

performance of the capital market. The initial public offerings in Australia are directly related

to its capital market conditions, where relevant decline in the capital market performance is

directly reflected on the number of |IPOs conducted during the year. The progress of the

financial crisis started to increase, which is the level of IPOs conducted each year.

Nevertheless, the short recession occurred during 2012 negatively affected the overall IPOs

in the country, as a capital market was not performing adequately. Hence, it could be

identified that after the 2013 the IPOs in Australia started to increase gradually, due to the

improvements that was achieved by its capital market. Thus, it could be understood that the

company wait for the capital market to perform well before imitating their IPO, as it helps

them to complete the process successfully and acquire the required funding from their public

offerings (Indoorskydiveaustralia.com.au, 2013).

Answer to e:

Return without dividends

Date

All Ordinary

Index

Virtus

Health Ltd

Sandon Capital

Investments Ltd

iSelect

Ltd

30-06-2013 5.45% 10.23% -5.88%

31-07-2013 1.78% 4.78% -11.25%

31-08-2013 1.80% 10.60% -11.27%

30-09-2013 3.88% 0.73% 3.97%

31-10-2013 -1.96% 6.02% -6.87%

30-11-2013 0.73% -0.68% 18.44%

31-12-2013 -2.76% -4.92% -2.02% -4.15%

31-01-2014 4.04% -5.66% 0.00% -21.66%

28-02-2014 -0.23% -7.14% 0.53% 5.07%

31-03-2014 1.25% 1.92% 0.00% -1.32%

30-04-2014 0.05% 11.32% 3.78% 8.00%

31-05-2014 -1.68% -1.21% -4.15% -5.35%

30-06-2014 4.48% -3.80% 4.76% 7.39%

31-07-2014 0.03% -0.64% 3.11% -2.02%

31-08-2014 -5.83% -0.38% -5.96% 16.94%

30-09-2014 3.93% -4.12% -3.65% -3.18%

31-10-2014 -3.76% -6.31% 7.51% -6.57%

30-11-2014 1.71% 12.46% -7.99% 0.39%

7

performance of the capital market. The initial public offerings in Australia are directly related

to its capital market conditions, where relevant decline in the capital market performance is

directly reflected on the number of |IPOs conducted during the year. The progress of the

financial crisis started to increase, which is the level of IPOs conducted each year.

Nevertheless, the short recession occurred during 2012 negatively affected the overall IPOs

in the country, as a capital market was not performing adequately. Hence, it could be

identified that after the 2013 the IPOs in Australia started to increase gradually, due to the

improvements that was achieved by its capital market. Thus, it could be understood that the

company wait for the capital market to perform well before imitating their IPO, as it helps

them to complete the process successfully and acquire the required funding from their public

offerings (Indoorskydiveaustralia.com.au, 2013).

Answer to e:

Return without dividends

Date

All Ordinary

Index

Virtus

Health Ltd

Sandon Capital

Investments Ltd

iSelect

Ltd

30-06-2013 5.45% 10.23% -5.88%

31-07-2013 1.78% 4.78% -11.25%

31-08-2013 1.80% 10.60% -11.27%

30-09-2013 3.88% 0.73% 3.97%

31-10-2013 -1.96% 6.02% -6.87%

30-11-2013 0.73% -0.68% 18.44%

31-12-2013 -2.76% -4.92% -2.02% -4.15%

31-01-2014 4.04% -5.66% 0.00% -21.66%

28-02-2014 -0.23% -7.14% 0.53% 5.07%

31-03-2014 1.25% 1.92% 0.00% -1.32%

30-04-2014 0.05% 11.32% 3.78% 8.00%

31-05-2014 -1.68% -1.21% -4.15% -5.35%

30-06-2014 4.48% -3.80% 4.76% 7.39%

31-07-2014 0.03% -0.64% 3.11% -2.02%

31-08-2014 -5.83% -0.38% -5.96% 16.94%

30-09-2014 3.93% -4.12% -3.65% -3.18%

31-10-2014 -3.76% -6.31% 7.51% -6.57%

30-11-2014 1.71% 12.46% -7.99% 0.39%

MANAGING FINANCE

8

31-12-2014 3.02% 2.29% 9.06% -5.06%

31-01-2015 6.25% -2.24% -0.03% 20.08%

28-02-2015 -0.62% -6.62% -8.78% 1.37%

31-03-2015 -1.50% 4.23% 4.95% 2.69%

30-04-2015 0.02% 1.57% 4.93% 2.95%

31-05-2015 -5.61% -30.80% -13.68% -8.28%

30-06-2015 4.23% 0.00% 4.05% 22.22%

31-07-2015 -8.09% -4.10% 0.00% -17.61%

31-08-2015 -3.13% 5.44% -1.11% 3.79%

30-09-2015 4.55% 16.21% 7.49% -0.33%

31-10-2015 -1.33% 2.69% -10.11% -11.67%

30-11-2015 2.42% 0.31% -1.16% -14.72%

31-12-2015 -5.39% -2.62% 13.53% -20.35%

31-01-2016 -2.15% -5.06% -11.40% -1.67%

29-02-2016 4.12% 4.16% -0.58% 16.38%

31-03-2016 3.19% 7.99% 9.72% 11.17%

30-04-2016 2.48% 4.88% -12.61% -4.37%

31-05-2016 -2.52% -3.10% -1.84% 13.70%

30-06-2016 6.28% 12.52% 24.21% 4.42%

31-07-2016 -2.03% 5.30% -8.42% 11.15%

31-08-2016 -0.08% -5.41% -0.55% 28.72%

30-09-2016 -2.22% -9.48% -0.55% -2.15%

31-10-2016 1.85% -17.36% 7.22% 5.77%

30-11-2016 3.94% 8.33% 6.75% -1.82%

31-12-2016 -0.77% -18.11% -4.86% -7.94%

31-01-2017 1.52% 5.87% 12.24% 11.78%

28-02-2017 2.48% 6.84% -2.73% 1.80%

31-03-2017 0.74% 0.69% -6.50% 0.51%

30-04-2017 -3.13% -3.61% -6.04% 5.53%

31-05-2017 0.05% -4.10% 0.00% -4.29%

30-06-2017 0.17% 4.28% 3.19% 3.98%

31-07-2017 0.04% 3.39% 2.58% -19.14%

31-08-2017 -0.54% -3.79% 1.22% -5.33%

30-09-2017 4.03% -1.79% -1.70% -0.31%

31-10-2017 0.79% -5.11% 0.00% -10.34%

30-11-2017 2.39% 1.15% 1.77% 0.35%

31-12-2017 -0.34% -0.38% -1.24% -9.06%

31-01-2018 -0.48% 10.11% 0.00% -7.28%

28-02-2018 -4.06% -6.24% 0.04% -15.70%

31-03-2018 3.45% 4.44% 1.47% -44.12%

30-04-2018 0.85% -2.12% -4.46% 9.65%

31-05-2018 2.71% 3.98% 3.03% 30.40%

Average 0.51% 0.13% 0.28% -0.37%

8

31-12-2014 3.02% 2.29% 9.06% -5.06%

31-01-2015 6.25% -2.24% -0.03% 20.08%

28-02-2015 -0.62% -6.62% -8.78% 1.37%

31-03-2015 -1.50% 4.23% 4.95% 2.69%

30-04-2015 0.02% 1.57% 4.93% 2.95%

31-05-2015 -5.61% -30.80% -13.68% -8.28%

30-06-2015 4.23% 0.00% 4.05% 22.22%

31-07-2015 -8.09% -4.10% 0.00% -17.61%

31-08-2015 -3.13% 5.44% -1.11% 3.79%

30-09-2015 4.55% 16.21% 7.49% -0.33%

31-10-2015 -1.33% 2.69% -10.11% -11.67%

30-11-2015 2.42% 0.31% -1.16% -14.72%

31-12-2015 -5.39% -2.62% 13.53% -20.35%

31-01-2016 -2.15% -5.06% -11.40% -1.67%

29-02-2016 4.12% 4.16% -0.58% 16.38%

31-03-2016 3.19% 7.99% 9.72% 11.17%

30-04-2016 2.48% 4.88% -12.61% -4.37%

31-05-2016 -2.52% -3.10% -1.84% 13.70%

30-06-2016 6.28% 12.52% 24.21% 4.42%

31-07-2016 -2.03% 5.30% -8.42% 11.15%

31-08-2016 -0.08% -5.41% -0.55% 28.72%

30-09-2016 -2.22% -9.48% -0.55% -2.15%

31-10-2016 1.85% -17.36% 7.22% 5.77%

30-11-2016 3.94% 8.33% 6.75% -1.82%

31-12-2016 -0.77% -18.11% -4.86% -7.94%

31-01-2017 1.52% 5.87% 12.24% 11.78%

28-02-2017 2.48% 6.84% -2.73% 1.80%

31-03-2017 0.74% 0.69% -6.50% 0.51%

30-04-2017 -3.13% -3.61% -6.04% 5.53%

31-05-2017 0.05% -4.10% 0.00% -4.29%

30-06-2017 0.17% 4.28% 3.19% 3.98%

31-07-2017 0.04% 3.39% 2.58% -19.14%

31-08-2017 -0.54% -3.79% 1.22% -5.33%

30-09-2017 4.03% -1.79% -1.70% -0.31%

31-10-2017 0.79% -5.11% 0.00% -10.34%

30-11-2017 2.39% 1.15% 1.77% 0.35%

31-12-2017 -0.34% -0.38% -1.24% -9.06%

31-01-2018 -0.48% 10.11% 0.00% -7.28%

28-02-2018 -4.06% -6.24% 0.04% -15.70%

31-03-2018 3.45% 4.44% 1.47% -44.12%

30-04-2018 0.85% -2.12% -4.46% 9.65%

31-05-2018 2.71% 3.98% 3.03% 30.40%

Average 0.51% 0.13% 0.28% -0.37%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGING FINANCE

9

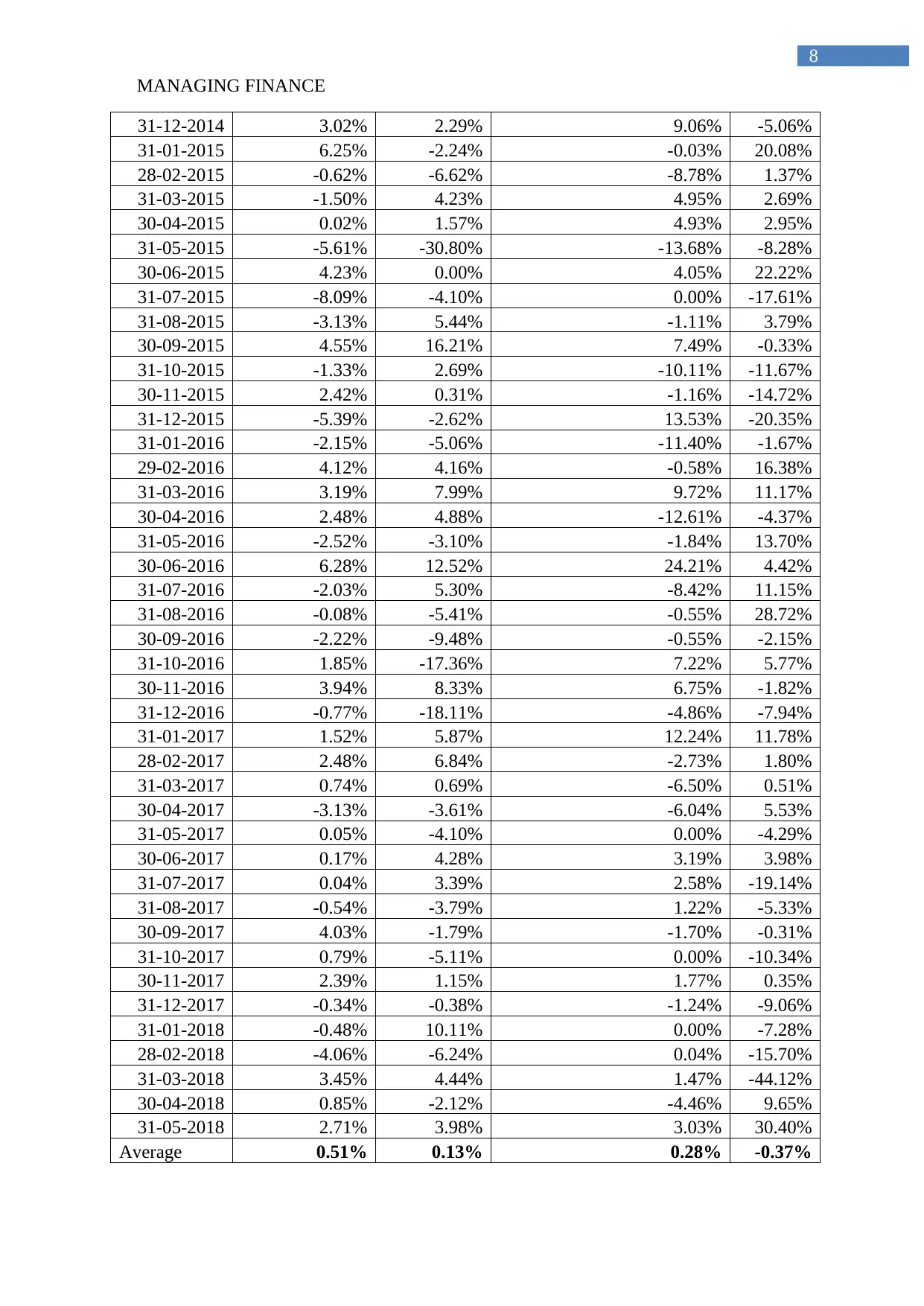

The above calculations directly provide information about the average returns that is

generated by all index and three IPOs for the next five years after their public offerings. From

the relevant analysis, it can be identified that the average returns of the market was not

breached by any of the IPOs that was taken into consideration and is depicted in the above

table. This indicates that the company's return did not outperform the Australian capital

market, which relatively depicts about the low growth capability of the IPOs

(Au.finance.yahoo.com, 2019).

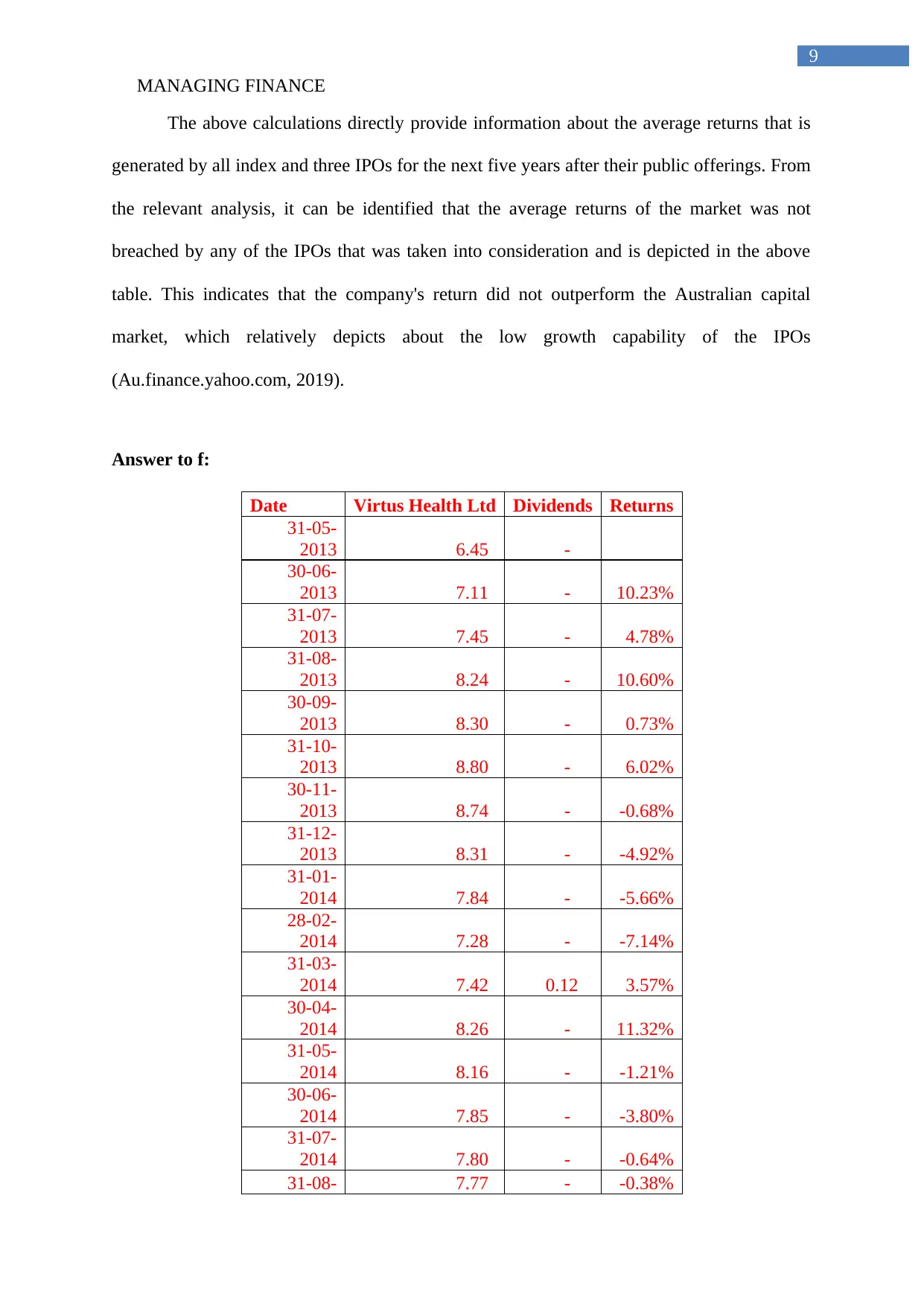

Answer to f:

Date Virtus Health Ltd Dividends Returns

31-05-

2013 6.45 -

30-06-

2013 7.11 - 10.23%

31-07-

2013 7.45 - 4.78%

31-08-

2013 8.24 - 10.60%

30-09-

2013 8.30 - 0.73%

31-10-

2013 8.80 - 6.02%

30-11-

2013 8.74 - -0.68%

31-12-

2013 8.31 - -4.92%

31-01-

2014 7.84 - -5.66%

28-02-

2014 7.28 - -7.14%

31-03-

2014 7.42 0.12 3.57%

30-04-

2014 8.26 - 11.32%

31-05-

2014 8.16 - -1.21%

30-06-

2014 7.85 - -3.80%

31-07-

2014 7.80 - -0.64%

31-08- 7.77 - -0.38%

9

The above calculations directly provide information about the average returns that is

generated by all index and three IPOs for the next five years after their public offerings. From

the relevant analysis, it can be identified that the average returns of the market was not

breached by any of the IPOs that was taken into consideration and is depicted in the above

table. This indicates that the company's return did not outperform the Australian capital

market, which relatively depicts about the low growth capability of the IPOs

(Au.finance.yahoo.com, 2019).

Answer to f:

Date Virtus Health Ltd Dividends Returns

31-05-

2013 6.45 -

30-06-

2013 7.11 - 10.23%

31-07-

2013 7.45 - 4.78%

31-08-

2013 8.24 - 10.60%

30-09-

2013 8.30 - 0.73%

31-10-

2013 8.80 - 6.02%

30-11-

2013 8.74 - -0.68%

31-12-

2013 8.31 - -4.92%

31-01-

2014 7.84 - -5.66%

28-02-

2014 7.28 - -7.14%

31-03-

2014 7.42 0.12 3.57%

30-04-

2014 8.26 - 11.32%

31-05-

2014 8.16 - -1.21%

30-06-

2014 7.85 - -3.80%

31-07-

2014 7.80 - -0.64%

31-08- 7.77 - -0.38%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGING FINANCE

10

2014

30-09-

2014 7.45 0.14 -2.32%

31-10-

2014 6.98 - -6.31%

30-11-

2014 7.85 - 12.46%

31-12-

2014 8.03 - 2.29%

31-01-

2015 7.85 - -2.24%

28-02-

2015 7.33 - -6.62%

31-03-

2015 7.64 0.13 6.00%

30-04-

2015 7.76 - 1.57%

31-05-

2015 5.37 - -30.80%

30-06-

2015 5.37 - 0.00%

31-07-

2015 5.15 - -4.10%

31-08-

2015 5.43 - 5.44%

30-09-

2015 6.31 0.14 18.78%

31-10-

2015 6.48 - 2.69%

30-11-

2015 6.50 - 0.31%

31-12-

2015 6.33 - -2.62%

31-01-

2016 6.01 - -5.06%

29-02-

2016 6.26 - 4.16%

31-03-

2016 6.76 0.14 10.22%

30-04-

2016 7.09 - 4.88%

31-05-

2016 6.87 - -3.10%

30-06-

2016 7.73 - 12.52%

31-07-

2016 8.14 - 5.30%

31-08-

2016 7.70 - -5.41%

10

2014

30-09-

2014 7.45 0.14 -2.32%

31-10-

2014 6.98 - -6.31%

30-11-

2014 7.85 - 12.46%

31-12-

2014 8.03 - 2.29%

31-01-

2015 7.85 - -2.24%

28-02-

2015 7.33 - -6.62%

31-03-

2015 7.64 0.13 6.00%

30-04-

2015 7.76 - 1.57%

31-05-

2015 5.37 - -30.80%

30-06-

2015 5.37 - 0.00%

31-07-

2015 5.15 - -4.10%

31-08-

2015 5.43 - 5.44%

30-09-

2015 6.31 0.14 18.78%

31-10-

2015 6.48 - 2.69%

30-11-

2015 6.50 - 0.31%

31-12-

2015 6.33 - -2.62%

31-01-

2016 6.01 - -5.06%

29-02-

2016 6.26 - 4.16%

31-03-

2016 6.76 0.14 10.22%

30-04-

2016 7.09 - 4.88%

31-05-

2016 6.87 - -3.10%

30-06-

2016 7.73 - 12.52%

31-07-

2016 8.14 - 5.30%

31-08-

2016 7.70 - -5.41%

MANAGING FINANCE

11

30-09-

2016 6.97 0.15 -7.53%

31-10-

2016 5.76 - -17.36%

30-11-

2016 6.24 - 8.33%

31-12-

2016 5.11 - -18.11%

31-01-

2017 5.41 - 5.87%

28-02-

2017 5.78 - 6.84%

31-03-

2017 5.82 0.13 2.94%

30-04-

2017 5.61 - -3.61%

31-05-

2017 5.38 - -4.10%

30-06-

2017 5.61 - 4.28%

31-07-

2017 5.80 - 3.39%

31-08-

2017 5.58 - -3.79%

30-09-

2017 5.48 0.12 0.36%

31-10-

2017 5.20 - -5.11%

30-11-

2017 5.26 - 1.15%

31-12-

2017 5.24 - -0.38%

31-01-

2018 5.77 - 10.11%

28-02-

2018 5.41 - -6.24%

31-03-

2018 5.65 0.14 7.02%

30-04-

2018 5.53 - -2.12%

31-05-

2018 5.75 - 3.98%

Average 0.45%

Date Sandon Capital Investments Ltd Dividends Returns

30-11-

2013 0.96 -

31-12- 0.95 - -2.02%

11

30-09-

2016 6.97 0.15 -7.53%

31-10-

2016 5.76 - -17.36%

30-11-

2016 6.24 - 8.33%

31-12-

2016 5.11 - -18.11%

31-01-

2017 5.41 - 5.87%

28-02-

2017 5.78 - 6.84%

31-03-

2017 5.82 0.13 2.94%

30-04-

2017 5.61 - -3.61%

31-05-

2017 5.38 - -4.10%

30-06-

2017 5.61 - 4.28%

31-07-

2017 5.80 - 3.39%

31-08-

2017 5.58 - -3.79%

30-09-

2017 5.48 0.12 0.36%

31-10-

2017 5.20 - -5.11%

30-11-

2017 5.26 - 1.15%

31-12-

2017 5.24 - -0.38%

31-01-

2018 5.77 - 10.11%

28-02-

2018 5.41 - -6.24%

31-03-

2018 5.65 0.14 7.02%

30-04-

2018 5.53 - -2.12%

31-05-

2018 5.75 - 3.98%

Average 0.45%

Date Sandon Capital Investments Ltd Dividends Returns

30-11-

2013 0.96 -

31-12- 0.95 - -2.02%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.