Financial Resource Management and Decision Making for PQR LTD

VerifiedAdded on 2020/02/03

|17

|4794

|75

Report

AI Summary

This report examines the financial resource management and decision-making processes for PQR LTD, a new venture seeking capital. It explores various sources of finance, including debentures, capital markets, and bank borrowings, evaluating their implications and costs. The report assesses the importance of financial planning, analyzes cash budgets, and calculates unit costs for pricing decisions. It also includes an analysis of financial statements, comparing formats and interpreting financial ratios. The report concludes with recommendations for PQR LTD's financial strategies, emphasizing the significance of informed decision-making to ensure the company's growth and sustainability. The report provides a comprehensive overview of the financial aspects involved in starting and managing a business, highlighting the critical role of financial planning and resource allocation.

MANAGING FINANCIAL

RESOURCES AND

DECISIONS

RESOURCES AND

DECISIONS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

AC 1.1 Sources of finance..........................................................................................................3

A.C. 1.2 Assessment of implications of financial sources..........................................................4

AC 1.3 Evaluation of appropriate source of finance...................................................................5

AC 2.1 Assessment of cost of sources of finance.......................................................................6

AC 2.2 importance of financial planning....................................................................................7

AC 2.3 Types of information needs for decision makers............................................................7

AC.2.4 Impact of finance on financial statements......................................................................8

AC 3.1 analysing cash budget and decision for business proposal.............................................8

AC 3.2 unit cost calculations and pricing decisions...................................................................9

AC 3.3 financial appraisal...........................................................................................................9

TASK 2..........................................................................................................................................10

A.C 4.1 Financial statements....................................................................................................10

AC 4.2 Comparison of formats of financial statements............................................................12

AC 4.3 Interpretation of financial ratios ..................................................................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

AC 1.1 Sources of finance..........................................................................................................3

A.C. 1.2 Assessment of implications of financial sources..........................................................4

AC 1.3 Evaluation of appropriate source of finance...................................................................5

AC 2.1 Assessment of cost of sources of finance.......................................................................6

AC 2.2 importance of financial planning....................................................................................7

AC 2.3 Types of information needs for decision makers............................................................7

AC.2.4 Impact of finance on financial statements......................................................................8

AC 3.1 analysing cash budget and decision for business proposal.............................................8

AC 3.2 unit cost calculations and pricing decisions...................................................................9

AC 3.3 financial appraisal...........................................................................................................9

TASK 2..........................................................................................................................................10

A.C 4.1 Financial statements....................................................................................................10

AC 4.2 Comparison of formats of financial statements............................................................12

AC 4.3 Interpretation of financial ratios ..................................................................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................15

INTRODUCTION

It is very important for a business to manage its financial resources and take such

decisions that helps in the growth of business and helps it expand. The sustainability of business

is another important aspect. The financial decisions are very critical in nature and they are to be

taken after thorough critical assessment of the sources of finance. It is the science of money

management. Managing financial resources and taking relevant decisions is what an entrepreneur

has to do. In this report the company PQR LTD. Is a new venture and they want to raise capital

from the market. So this report includes all the aspects that the entrepreneur has to look before

proposing a business proposal( Bierman, and midt 2012). They has to make a plan by keeping in

mind the objective of profit maximisation. This report further includes the analysis of cash

budget and comparison of financial ratios with the importance of finance on financial

statements.

TASK 1

AC 1.1 Sources of finance

An entrepreneur wants to launch a business proposal for which he has £ 20000 for

investing purpose as capital but he needs to borrow £ 280000 for making a bid of

£300000. for this they have to raise funds from the capital market and they

are a newly set up company. It is true that business are more profitable if

there is more risk involves(Brown Evans and Moser 2010). There are

various sources of finance that they are considering for raising the capital

for their proposal. These resources are available at various costs and they

have to decide which will be beneficial for the. The sources available to

them could be external as well as internal .

External sources available are :

Debentures: these are the fund borrowed from the public and

contains a written acknowledgement. It comprises of terms and

conditions regarding its interest payment and repayment of debt.

Capital market: the another way to raise capital from the market is

by issuing its shares in the market or by issuing right shares to the

existing shareholders at a comparatively low prices than the market

It is very important for a business to manage its financial resources and take such

decisions that helps in the growth of business and helps it expand. The sustainability of business

is another important aspect. The financial decisions are very critical in nature and they are to be

taken after thorough critical assessment of the sources of finance. It is the science of money

management. Managing financial resources and taking relevant decisions is what an entrepreneur

has to do. In this report the company PQR LTD. Is a new venture and they want to raise capital

from the market. So this report includes all the aspects that the entrepreneur has to look before

proposing a business proposal( Bierman, and midt 2012). They has to make a plan by keeping in

mind the objective of profit maximisation. This report further includes the analysis of cash

budget and comparison of financial ratios with the importance of finance on financial

statements.

TASK 1

AC 1.1 Sources of finance

An entrepreneur wants to launch a business proposal for which he has £ 20000 for

investing purpose as capital but he needs to borrow £ 280000 for making a bid of

£300000. for this they have to raise funds from the capital market and they

are a newly set up company. It is true that business are more profitable if

there is more risk involves(Brown Evans and Moser 2010). There are

various sources of finance that they are considering for raising the capital

for their proposal. These resources are available at various costs and they

have to decide which will be beneficial for the. The sources available to

them could be external as well as internal .

External sources available are :

Debentures: these are the fund borrowed from the public and

contains a written acknowledgement. It comprises of terms and

conditions regarding its interest payment and repayment of debt.

Capital market: the another way to raise capital from the market is

by issuing its shares in the market or by issuing right shares to the

existing shareholders at a comparatively low prices than the market

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

price. They can raise it by either preference shares or by equity

shares.

Bank borrowings: the company can avail the option of borrowing

from banks directly. They have to go under certain formalities and can

get the loan required.

Bank overdraft: It allows the company to withdraw funds even if the

balance of their account is zero. It will lead to higher rate of interest.

Franchising: It helps the business to so the operations by lending

their name to other party and they run the business(Ezzamel Robson

and Stapleton 2012). It costs them less.

Internal sources

Retained Earnings: these are the earnings of the owners of the

business and these are not spend and are invested back in the

business for further investment purposes.

A.C. 1.2 Assessment of implications of financial sources.

The financial sources are available to the business but they all have various benefits and

certain limitations attached to them. The implications has a great impact on the working of the

business as they need to be selected very carefully. If the financial sources are not taken with

proper evaluation they can hinder the operations of business. Here in this case scenario the

entrepreneur wants to raise funds of £ 280000. the company has to critically evaluate the pros

and cons of every source. As if he gets the fund from debentures or from bank borrowings he has

to go for various legal proceedings and fixed repayment period. Etc. there are some implications

attached to it and these may be in the form of legal(Gervais Heaton and Odean 2011),

financial, dilution of control and bankruptcy.

Sources Legal Financial Bankruptcy Dilution of

control

Shares The voting rights

are not available

with them.

The repayment is

not the concerned

issue but they are

obligatory to give

In case of

bankruptcy the

preference

shareholders are

Control is not

diluted

shares.

Bank borrowings: the company can avail the option of borrowing

from banks directly. They have to go under certain formalities and can

get the loan required.

Bank overdraft: It allows the company to withdraw funds even if the

balance of their account is zero. It will lead to higher rate of interest.

Franchising: It helps the business to so the operations by lending

their name to other party and they run the business(Ezzamel Robson

and Stapleton 2012). It costs them less.

Internal sources

Retained Earnings: these are the earnings of the owners of the

business and these are not spend and are invested back in the

business for further investment purposes.

A.C. 1.2 Assessment of implications of financial sources.

The financial sources are available to the business but they all have various benefits and

certain limitations attached to them. The implications has a great impact on the working of the

business as they need to be selected very carefully. If the financial sources are not taken with

proper evaluation they can hinder the operations of business. Here in this case scenario the

entrepreneur wants to raise funds of £ 280000. the company has to critically evaluate the pros

and cons of every source. As if he gets the fund from debentures or from bank borrowings he has

to go for various legal proceedings and fixed repayment period. Etc. there are some implications

attached to it and these may be in the form of legal(Gervais Heaton and Odean 2011),

financial, dilution of control and bankruptcy.

Sources Legal Financial Bankruptcy Dilution of

control

Shares The voting rights

are not available

with them.

The repayment is

not the concerned

issue but they are

obligatory to give

In case of

bankruptcy the

preference

shareholders are

Control is not

diluted

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

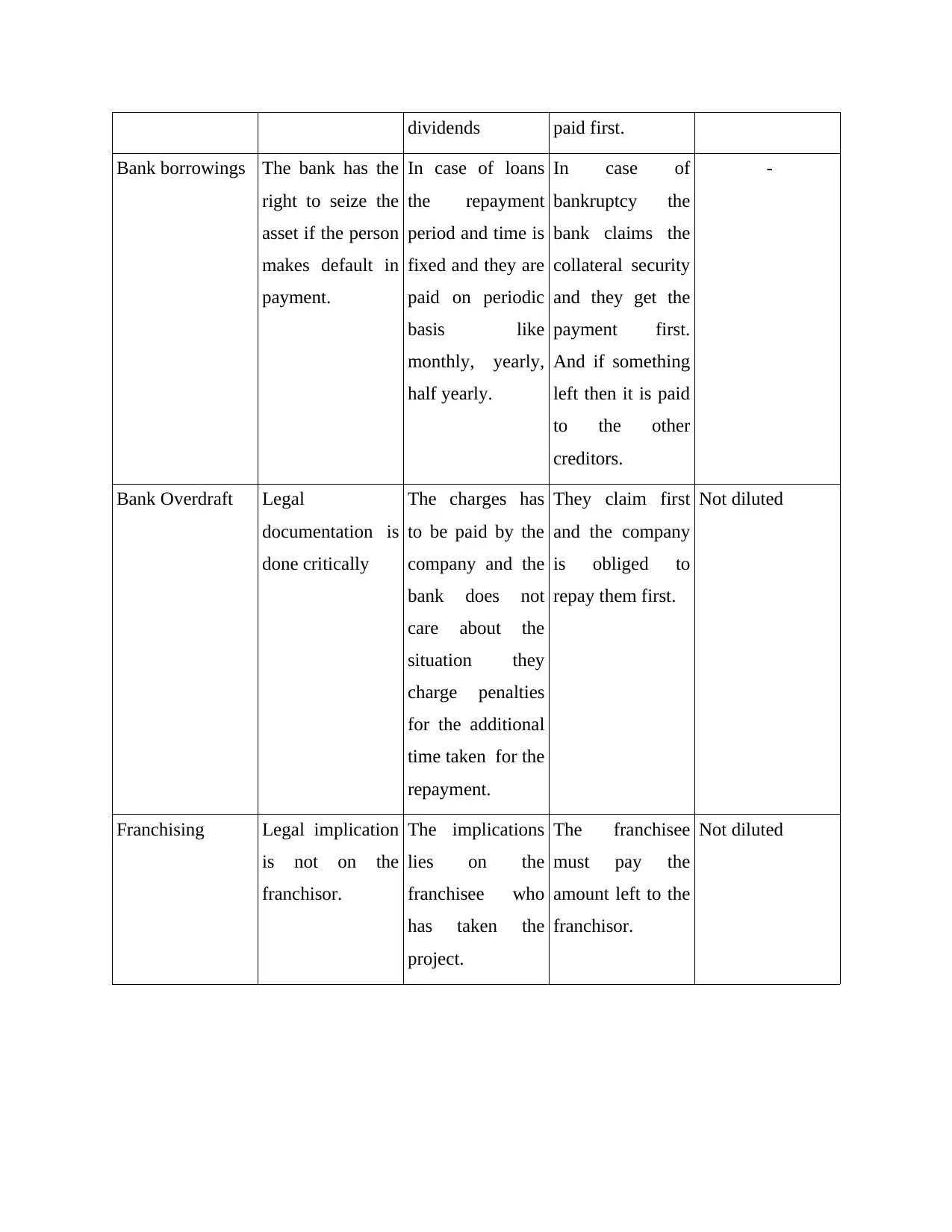

dividends paid first.

Bank borrowings The bank has the

right to seize the

asset if the person

makes default in

payment.

In case of loans

the repayment

period and time is

fixed and they are

paid on periodic

basis like

monthly, yearly,

half yearly.

In case of

bankruptcy the

bank claims the

collateral security

and they get the

payment first.

And if something

left then it is paid

to the other

creditors.

-

Bank Overdraft Legal

documentation is

done critically

The charges has

to be paid by the

company and the

bank does not

care about the

situation they

charge penalties

for the additional

time taken for the

repayment.

They claim first

and the company

is obliged to

repay them first.

Not diluted

Franchising Legal implication

is not on the

franchisor.

The implications

lies on the

franchisee who

has taken the

project.

The franchisee

must pay the

amount left to the

franchisor.

Not diluted

Bank borrowings The bank has the

right to seize the

asset if the person

makes default in

payment.

In case of loans

the repayment

period and time is

fixed and they are

paid on periodic

basis like

monthly, yearly,

half yearly.

In case of

bankruptcy the

bank claims the

collateral security

and they get the

payment first.

And if something

left then it is paid

to the other

creditors.

-

Bank Overdraft Legal

documentation is

done critically

The charges has

to be paid by the

company and the

bank does not

care about the

situation they

charge penalties

for the additional

time taken for the

repayment.

They claim first

and the company

is obliged to

repay them first.

Not diluted

Franchising Legal implication

is not on the

franchisor.

The implications

lies on the

franchisee who

has taken the

project.

The franchisee

must pay the

amount left to the

franchisor.

Not diluted

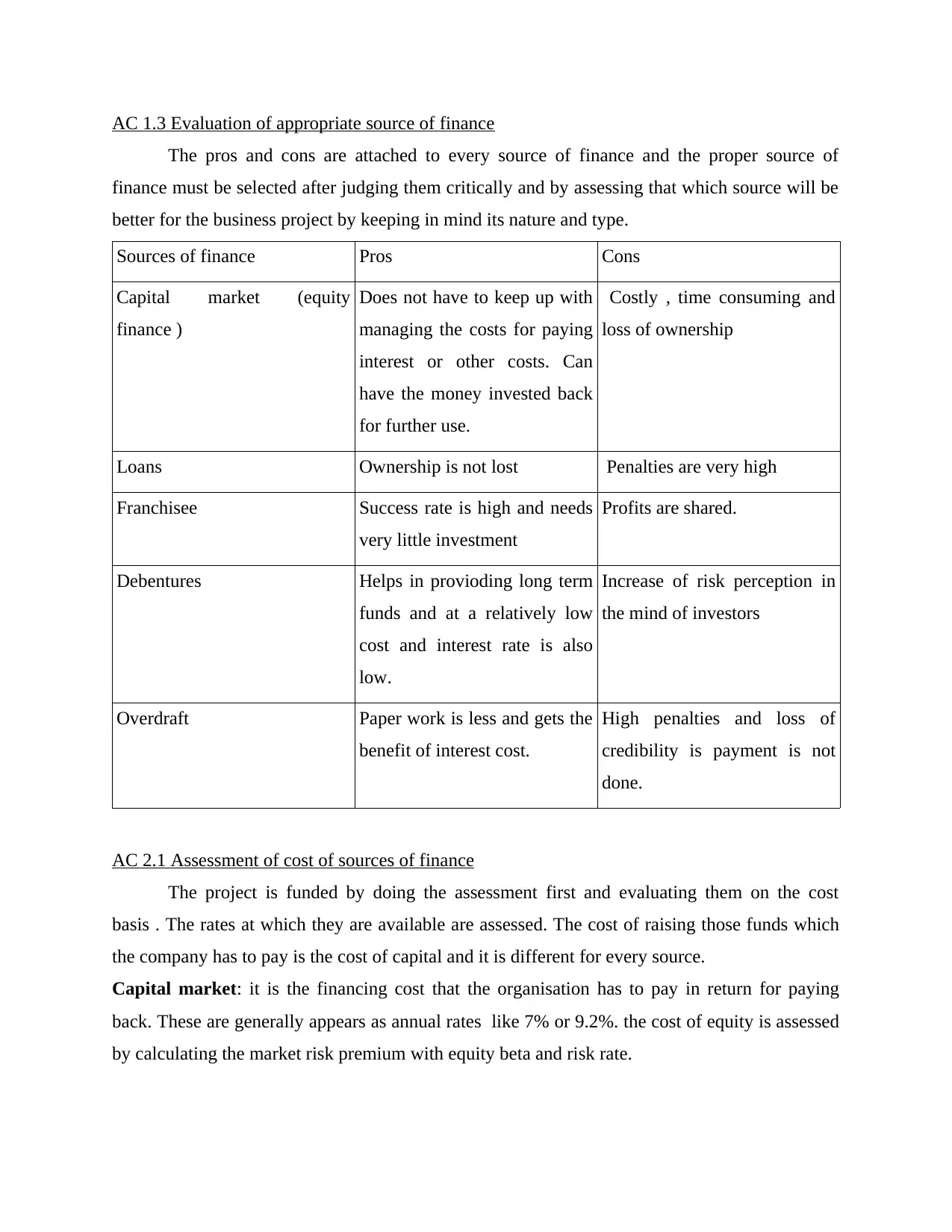

AC 1.3 Evaluation of appropriate source of finance

The pros and cons are attached to every source of finance and the proper source of

finance must be selected after judging them critically and by assessing that which source will be

better for the business project by keeping in mind its nature and type.

Sources of finance Pros Cons

Capital market (equity

finance )

Does not have to keep up with

managing the costs for paying

interest or other costs. Can

have the money invested back

for further use.

Costly , time consuming and

loss of ownership

Loans Ownership is not lost Penalties are very high

Franchisee Success rate is high and needs

very little investment

Profits are shared.

Debentures Helps in provioding long term

funds and at a relatively low

cost and interest rate is also

low.

Increase of risk perception in

the mind of investors

Overdraft Paper work is less and gets the

benefit of interest cost.

High penalties and loss of

credibility is payment is not

done.

AC 2.1 Assessment of cost of sources of finance

The project is funded by doing the assessment first and evaluating them on the cost

basis . The rates at which they are available are assessed. The cost of raising those funds which

the company has to pay is the cost of capital and it is different for every source.

Capital market: it is the financing cost that the organisation has to pay in return for paying

back. These are generally appears as annual rates like 7% or 9.2%. the cost of equity is assessed

by calculating the market risk premium with equity beta and risk rate.

The pros and cons are attached to every source of finance and the proper source of

finance must be selected after judging them critically and by assessing that which source will be

better for the business project by keeping in mind its nature and type.

Sources of finance Pros Cons

Capital market (equity

finance )

Does not have to keep up with

managing the costs for paying

interest or other costs. Can

have the money invested back

for further use.

Costly , time consuming and

loss of ownership

Loans Ownership is not lost Penalties are very high

Franchisee Success rate is high and needs

very little investment

Profits are shared.

Debentures Helps in provioding long term

funds and at a relatively low

cost and interest rate is also

low.

Increase of risk perception in

the mind of investors

Overdraft Paper work is less and gets the

benefit of interest cost.

High penalties and loss of

credibility is payment is not

done.

AC 2.1 Assessment of cost of sources of finance

The project is funded by doing the assessment first and evaluating them on the cost

basis . The rates at which they are available are assessed. The cost of raising those funds which

the company has to pay is the cost of capital and it is different for every source.

Capital market: it is the financing cost that the organisation has to pay in return for paying

back. These are generally appears as annual rates like 7% or 9.2%. the cost of equity is assessed

by calculating the market risk premium with equity beta and risk rate.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Debentures: It includes the cost of interests. The cost is assessed by calculating the cost of

borrowing and the debenture cost in this market is around 7.5%.

Bank Overdraft : The HSBC has allowed the facility of overdraft to some of its customers and

they charge high interest rate for this facility(Hope and Fraser 2013). The customers are

offered to take loan even if the bank account has zero balance and they are given the relaxation

to pay later. The penalty rate is 13%

Bank Borrowings: The business proposal can be funded from the bank borrowings and these are

available at HSBC from 11 % - 18.4 % the advantage of getting borrowed from bank is that the

company will get tax benefits.

Franchise : The cost of franchisee is very low as compared to the other sources. They need to

just start the business as all the set up needed is already ready.

AC 2.2 importance of financial planning

A financial plan is the situation of an investor's current and future. It is made by

predicting the future state of the investor by evaluating current financial state. It is the process

that helps in forming the objectives and policies and regulation that will help in improving the

financial position of the company and they include adequate financial policies(Joyce, 2011).

The importance of finance planning are:

the funds required are ensured.

If the plan is there then it will help in balancing the inflow and outflow of cash .

It helps the business to make long term objectives and helps to sustain the business.

It helps in maintaining certainty in situations and market trends and helps in expansion.

It helps in coping up with uncertainties and coming out of the situations that are creating

hindrance.

Appropriate financial planning helps a business to be stable and ensure profit

maximisation.

AC 2.3 Types of information needs for decision makers.

There are various types of information that the internal and external decision makers

need. There are certain decision makers which check the viability of the project and managers

have to give the information to them. These decision makers are:

Government: the government needs to know the status of business as they are concern

with the taxation policies, what steps they are taking for the benefit of the society. what CSR

borrowing and the debenture cost in this market is around 7.5%.

Bank Overdraft : The HSBC has allowed the facility of overdraft to some of its customers and

they charge high interest rate for this facility(Hope and Fraser 2013). The customers are

offered to take loan even if the bank account has zero balance and they are given the relaxation

to pay later. The penalty rate is 13%

Bank Borrowings: The business proposal can be funded from the bank borrowings and these are

available at HSBC from 11 % - 18.4 % the advantage of getting borrowed from bank is that the

company will get tax benefits.

Franchise : The cost of franchisee is very low as compared to the other sources. They need to

just start the business as all the set up needed is already ready.

AC 2.2 importance of financial planning

A financial plan is the situation of an investor's current and future. It is made by

predicting the future state of the investor by evaluating current financial state. It is the process

that helps in forming the objectives and policies and regulation that will help in improving the

financial position of the company and they include adequate financial policies(Joyce, 2011).

The importance of finance planning are:

the funds required are ensured.

If the plan is there then it will help in balancing the inflow and outflow of cash .

It helps the business to make long term objectives and helps to sustain the business.

It helps in maintaining certainty in situations and market trends and helps in expansion.

It helps in coping up with uncertainties and coming out of the situations that are creating

hindrance.

Appropriate financial planning helps a business to be stable and ensure profit

maximisation.

AC 2.3 Types of information needs for decision makers.

There are various types of information that the internal and external decision makers

need. There are certain decision makers which check the viability of the project and managers

have to give the information to them. These decision makers are:

Government: the government needs to know the status of business as they are concern

with the taxation policies, what steps they are taking for the benefit of the society. what CSR

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

issues they are addressing(Kilfoyle and Richardson 2011) , though the government is not

related to the business but they need information on this.

Stockholders: they are the owner of the company so they need to know the financial

position of the company to take the decisions relevant for the company. They t6ake the financial

decisions of the company.

Creditors: they need the financial information to know that the loan taken by the firm

will be re payed or not. What is their financial conditions.

Suppliers: they need to know the information regarding the raw materials and products.

Employees: the employees of the organisation needs to know the current position of the

company they are working in .

AC.2.4 Impact of finance on financial statements

The source of finance that is choose for the business proposal id bank borrowings (loan)

as the company is new so they cant issue debentures. They can easily take loans and pay interest

on them. The amount of loan will have a impact on the balance sheet of the company. it will

create the risk profile of business and the analyst and investor depends upon. It will increase the

liabilities side of the balance sheet(Lee Johnson and Joyce 2012). The loan indicates an

external liability in the business. The EMI the company pays will have an impact in income

statement as interest payment.

If the company raise capital from other sources say suppose from equity then it will increase the

shareholders fund and will occur on liabilities side. the impact can be measured by the change of

market shares price.

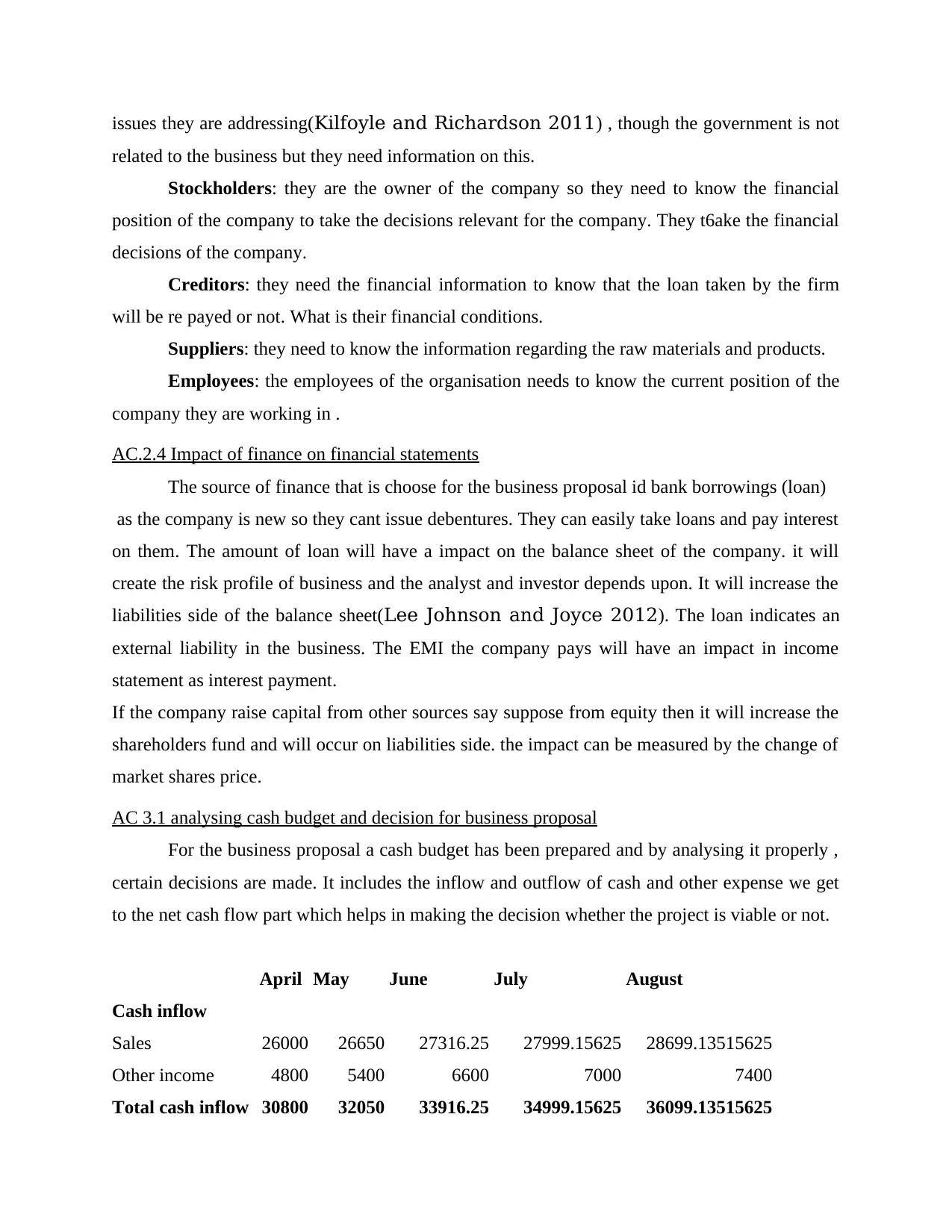

AC 3.1 analysing cash budget and decision for business proposal

For the business proposal a cash budget has been prepared and by analysing it properly ,

certain decisions are made. It includes the inflow and outflow of cash and other expense we get

to the net cash flow part which helps in making the decision whether the project is viable or not.

April May June July August

Cash inflow

Sales 26000 26650 27316.25 27999.15625 28699.13515625

Other income 4800 5400 6600 7000 7400

Total cash inflow 30800 32050 33916.25 34999.15625 36099.13515625

related to the business but they need information on this.

Stockholders: they are the owner of the company so they need to know the financial

position of the company to take the decisions relevant for the company. They t6ake the financial

decisions of the company.

Creditors: they need the financial information to know that the loan taken by the firm

will be re payed or not. What is their financial conditions.

Suppliers: they need to know the information regarding the raw materials and products.

Employees: the employees of the organisation needs to know the current position of the

company they are working in .

AC.2.4 Impact of finance on financial statements

The source of finance that is choose for the business proposal id bank borrowings (loan)

as the company is new so they cant issue debentures. They can easily take loans and pay interest

on them. The amount of loan will have a impact on the balance sheet of the company. it will

create the risk profile of business and the analyst and investor depends upon. It will increase the

liabilities side of the balance sheet(Lee Johnson and Joyce 2012). The loan indicates an

external liability in the business. The EMI the company pays will have an impact in income

statement as interest payment.

If the company raise capital from other sources say suppose from equity then it will increase the

shareholders fund and will occur on liabilities side. the impact can be measured by the change of

market shares price.

AC 3.1 analysing cash budget and decision for business proposal

For the business proposal a cash budget has been prepared and by analysing it properly ,

certain decisions are made. It includes the inflow and outflow of cash and other expense we get

to the net cash flow part which helps in making the decision whether the project is viable or not.

April May June July August

Cash inflow

Sales 26000 26650 27316.25 27999.15625 28699.13515625

Other income 4800 5400 6600 7000 7400

Total cash inflow 30800 32050 33916.25 34999.15625 36099.13515625

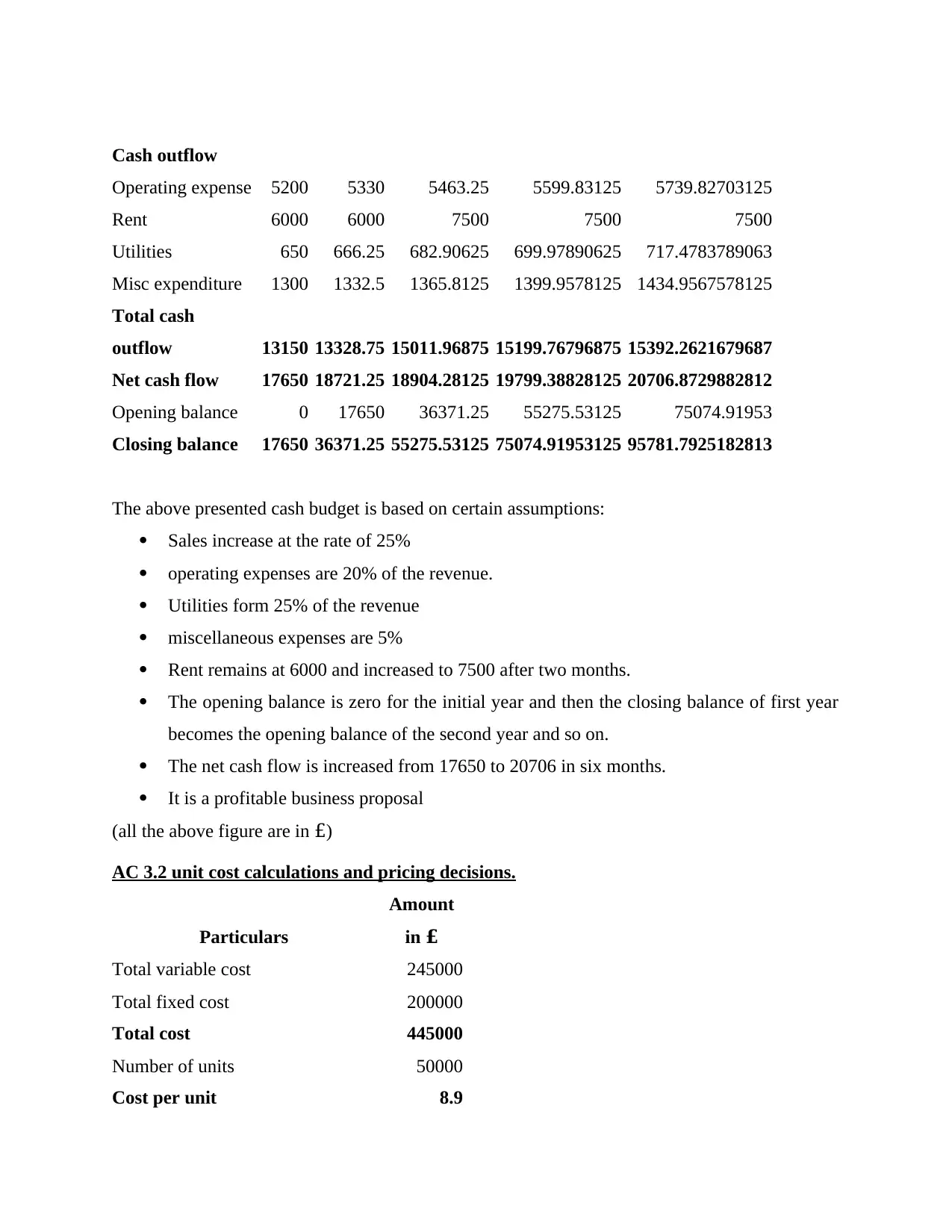

Cash outflow

Operating expense 5200 5330 5463.25 5599.83125 5739.82703125

Rent 6000 6000 7500 7500 7500

Utilities 650 666.25 682.90625 699.97890625 717.4783789063

Misc expenditure 1300 1332.5 1365.8125 1399.9578125 1434.9567578125

Total cash

outflow 13150 13328.75 15011.96875 15199.76796875 15392.2621679687

Net cash flow 17650 18721.25 18904.28125 19799.38828125 20706.8729882812

Opening balance 0 17650 36371.25 55275.53125 75074.91953

Closing balance 17650 36371.25 55275.53125 75074.91953125 95781.7925182813

The above presented cash budget is based on certain assumptions:

Sales increase at the rate of 25%

operating expenses are 20% of the revenue.

Utilities form 25% of the revenue

miscellaneous expenses are 5%

Rent remains at 6000 and increased to 7500 after two months.

The opening balance is zero for the initial year and then the closing balance of first year

becomes the opening balance of the second year and so on.

The net cash flow is increased from 17650 to 20706 in six months.

It is a profitable business proposal

(all the above figure are in £)

AC 3.2 unit cost calculations and pricing decisions.

Particulars

Amount

in £

Total variable cost 245000

Total fixed cost 200000

Total cost 445000

Number of units 50000

Cost per unit 8.9

Operating expense 5200 5330 5463.25 5599.83125 5739.82703125

Rent 6000 6000 7500 7500 7500

Utilities 650 666.25 682.90625 699.97890625 717.4783789063

Misc expenditure 1300 1332.5 1365.8125 1399.9578125 1434.9567578125

Total cash

outflow 13150 13328.75 15011.96875 15199.76796875 15392.2621679687

Net cash flow 17650 18721.25 18904.28125 19799.38828125 20706.8729882812

Opening balance 0 17650 36371.25 55275.53125 75074.91953

Closing balance 17650 36371.25 55275.53125 75074.91953125 95781.7925182813

The above presented cash budget is based on certain assumptions:

Sales increase at the rate of 25%

operating expenses are 20% of the revenue.

Utilities form 25% of the revenue

miscellaneous expenses are 5%

Rent remains at 6000 and increased to 7500 after two months.

The opening balance is zero for the initial year and then the closing balance of first year

becomes the opening balance of the second year and so on.

The net cash flow is increased from 17650 to 20706 in six months.

It is a profitable business proposal

(all the above figure are in £)

AC 3.2 unit cost calculations and pricing decisions.

Particulars

Amount

in £

Total variable cost 245000

Total fixed cost 200000

Total cost 445000

Number of units 50000

Cost per unit 8.9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

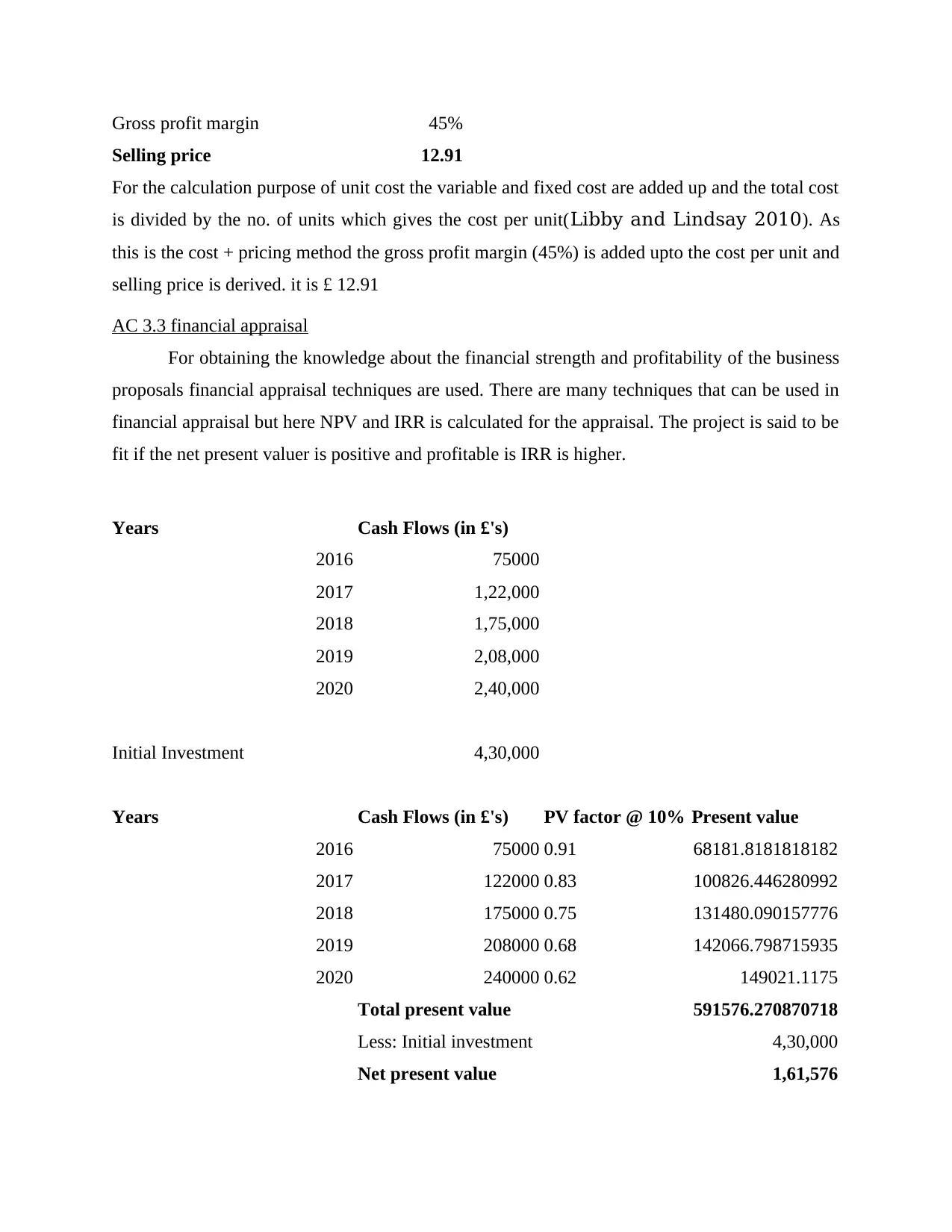

Gross profit margin 45%

Selling price 12.91

For the calculation purpose of unit cost the variable and fixed cost are added up and the total cost

is divided by the no. of units which gives the cost per unit(Libby and Lindsay 2010). As

this is the cost + pricing method the gross profit margin (45%) is added upto the cost per unit and

selling price is derived. it is £ 12.91

AC 3.3 financial appraisal

For obtaining the knowledge about the financial strength and profitability of the business

proposals financial appraisal techniques are used. There are many techniques that can be used in

financial appraisal but here NPV and IRR is calculated for the appraisal. The project is said to be

fit if the net present valuer is positive and profitable is IRR is higher.

Years Cash Flows (in £'s)

2016 75000

2017 1,22,000

2018 1,75,000

2019 2,08,000

2020 2,40,000

Initial Investment 4,30,000

Years Cash Flows (in £'s) PV factor @ 10% Present value

2016 75000 0.91 68181.8181818182

2017 122000 0.83 100826.446280992

2018 175000 0.75 131480.090157776

2019 208000 0.68 142066.798715935

2020 240000 0.62 149021.1175

Total present value 591576.270870718

Less: Initial investment 4,30,000

Net present value 1,61,576

Selling price 12.91

For the calculation purpose of unit cost the variable and fixed cost are added up and the total cost

is divided by the no. of units which gives the cost per unit(Libby and Lindsay 2010). As

this is the cost + pricing method the gross profit margin (45%) is added upto the cost per unit and

selling price is derived. it is £ 12.91

AC 3.3 financial appraisal

For obtaining the knowledge about the financial strength and profitability of the business

proposals financial appraisal techniques are used. There are many techniques that can be used in

financial appraisal but here NPV and IRR is calculated for the appraisal. The project is said to be

fit if the net present valuer is positive and profitable is IRR is higher.

Years Cash Flows (in £'s)

2016 75000

2017 1,22,000

2018 1,75,000

2019 2,08,000

2020 2,40,000

Initial Investment 4,30,000

Years Cash Flows (in £'s) PV factor @ 10% Present value

2016 75000 0.91 68181.8181818182

2017 122000 0.83 100826.446280992

2018 175000 0.75 131480.090157776

2019 208000 0.68 142066.798715935

2020 240000 0.62 149021.1175

Total present value 591576.270870718

Less: Initial investment 4,30,000

Net present value 1,61,576

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

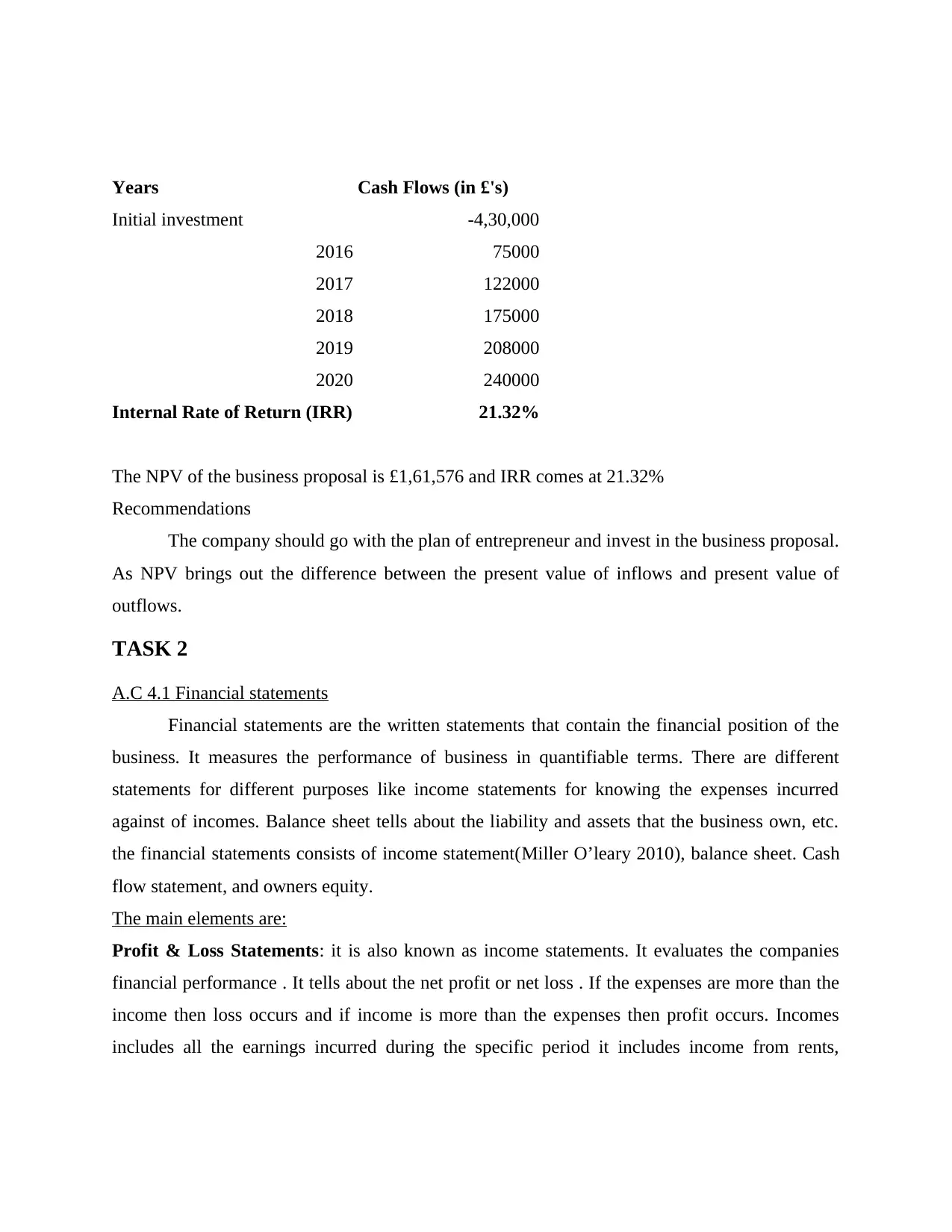

Years Cash Flows (in £'s)

Initial investment -4,30,000

2016 75000

2017 122000

2018 175000

2019 208000

2020 240000

Internal Rate of Return (IRR) 21.32%

The NPV of the business proposal is £1,61,576 and IRR comes at 21.32%

Recommendations

The company should go with the plan of entrepreneur and invest in the business proposal.

As NPV brings out the difference between the present value of inflows and present value of

outflows.

TASK 2

A.C 4.1 Financial statements

Financial statements are the written statements that contain the financial position of the

business. It measures the performance of business in quantifiable terms. There are different

statements for different purposes like income statements for knowing the expenses incurred

against of incomes. Balance sheet tells about the liability and assets that the business own, etc.

the financial statements consists of income statement(Miller O’leary 2010), balance sheet. Cash

flow statement, and owners equity.

The main elements are:

Profit & Loss Statements: it is also known as income statements. It evaluates the companies

financial performance . It tells about the net profit or net loss . If the expenses are more than the

income then loss occurs and if income is more than the expenses then profit occurs. Incomes

includes all the earnings incurred during the specific period it includes income from rents,

Initial investment -4,30,000

2016 75000

2017 122000

2018 175000

2019 208000

2020 240000

Internal Rate of Return (IRR) 21.32%

The NPV of the business proposal is £1,61,576 and IRR comes at 21.32%

Recommendations

The company should go with the plan of entrepreneur and invest in the business proposal.

As NPV brings out the difference between the present value of inflows and present value of

outflows.

TASK 2

A.C 4.1 Financial statements

Financial statements are the written statements that contain the financial position of the

business. It measures the performance of business in quantifiable terms. There are different

statements for different purposes like income statements for knowing the expenses incurred

against of incomes. Balance sheet tells about the liability and assets that the business own, etc.

the financial statements consists of income statement(Miller O’leary 2010), balance sheet. Cash

flow statement, and owners equity.

The main elements are:

Profit & Loss Statements: it is also known as income statements. It evaluates the companies

financial performance . It tells about the net profit or net loss . If the expenses are more than the

income then loss occurs and if income is more than the expenses then profit occurs. Incomes

includes all the earnings incurred during the specific period it includes income from rents,

interests etc. expenses are included that is incurred in that particular period and it includes bank

charges, wages taxes etc.

Balance Sheet: It comprises of liabilities and assets. Liabilities are something that the business

owe to and assets are the things that they own(Phillips and Costa 2010), balance sheet is the

summary of the business . Assets includes current asset as well as fixed asset. Current assets are

those that can be converted into liquid form and fixed assets are not easily convertible. These

includes buildings, lands, machineries plant etc. and current assets includes inventories, whereas

liabilities are also divided into two categories on the basis of short term and long term. Long

term are the liabilities which remains for the period of more than one year and short term are

paid off within a year.

Cash Flow Statements: this is made for tracking the inflows and outflows of cash. It keeps a

check on the firm and tells that whether the company is able to manage the funds or not. It has to

keep the balance between inflow and outflow of funds and helps in taking the decisions

regarding cash management. The cash flow operates on the basis of operating activities in which

day to day operations are included(Sintomer Herzberg and Röcke 2011). Then investing

activities are recorded that includes inflow and outflow of investing activities like purchase and

sale of assets. Then at last financing activities are taken care of which includes inflow and

outflow of cash from the issue of shares and redemptions. At last the ending amount of cash flow

should be equal to cash in hand.

Statements Of Changes In Equity:

Owners detailed earnings are stated in this statement.

The financial statements are used by many people.

Government: They needed financial statements of the company to know whether they are

abiding by the rules and regulations and following the company standards(Truong Partington

and, Peat 2010). They wanted to know what they are doing for the society.

Competitors: The financial statements are useful for the competitors to know about their

position and their pricing techniques, so that they can make their prices accordingly. By doing

backward calculations prices can be calculated. And annual reports may guide along the way

from where raw materials are gathered.

Customers: The customers who want to invest in their shares need to study the annual reports of

the company and then make a decision whether to invest in it or not.

charges, wages taxes etc.

Balance Sheet: It comprises of liabilities and assets. Liabilities are something that the business

owe to and assets are the things that they own(Phillips and Costa 2010), balance sheet is the

summary of the business . Assets includes current asset as well as fixed asset. Current assets are

those that can be converted into liquid form and fixed assets are not easily convertible. These

includes buildings, lands, machineries plant etc. and current assets includes inventories, whereas

liabilities are also divided into two categories on the basis of short term and long term. Long

term are the liabilities which remains for the period of more than one year and short term are

paid off within a year.

Cash Flow Statements: this is made for tracking the inflows and outflows of cash. It keeps a

check on the firm and tells that whether the company is able to manage the funds or not. It has to

keep the balance between inflow and outflow of funds and helps in taking the decisions

regarding cash management. The cash flow operates on the basis of operating activities in which

day to day operations are included(Sintomer Herzberg and Röcke 2011). Then investing

activities are recorded that includes inflow and outflow of investing activities like purchase and

sale of assets. Then at last financing activities are taken care of which includes inflow and

outflow of cash from the issue of shares and redemptions. At last the ending amount of cash flow

should be equal to cash in hand.

Statements Of Changes In Equity:

Owners detailed earnings are stated in this statement.

The financial statements are used by many people.

Government: They needed financial statements of the company to know whether they are

abiding by the rules and regulations and following the company standards(Truong Partington

and, Peat 2010). They wanted to know what they are doing for the society.

Competitors: The financial statements are useful for the competitors to know about their

position and their pricing techniques, so that they can make their prices accordingly. By doing

backward calculations prices can be calculated. And annual reports may guide along the way

from where raw materials are gathered.

Customers: The customers who want to invest in their shares need to study the annual reports of

the company and then make a decision whether to invest in it or not.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.