Financial Resource Management: Analysis and Report for Business

VerifiedAdded on 2020/01/07

|17

|5129

|469

Report

AI Summary

This report provides a comprehensive overview of financial resource management, encompassing key aspects such as sources of finance, implications of financing, and the evaluation of appropriate financing options for a business. The report delves into the cost of finance, the importance of financial planning, and the information needs of both internal and external decision-makers. It further explores the impact of finance on financial statements, including a detailed analysis of cash budgeting and the calculation of unit costs, along with effective pricing strategies. Investment appraisal techniques are also discussed, alongside a comparison of main financial statements, their purposes, contents, and the interpretation of these statements using various ratios. The report aims to provide a clear understanding of financial resource management within a business context.

MANAGING FINANCIAL

RESOURCES

RESOURCES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

MANAGING FINANCIAL RESOURCES.....................................................................................1

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

1.1 The sources of finance available to a business......................................................................3

1.2 Implication of sources of finance..........................................................................................4

1.3 Evaluation of appropriate sources of finance for a business ................................................4

2.1 Cost of sources of finance ....................................................................................................5

2.2Importance of financial planning and how it is undertaken ..................................................6

2.3The information needs of internal and external decision makers..........................................7

2.4 Impact of finance on financial statement..............................................................................7

3.1 Cash budget for cited organisation........................................................................................8

3.2 Calculation of unit cost along with the making of effective pricing decisions.....................8

3.3 Different investment appraisal techniques for the organisation..........................................10

TASK 2..........................................................................................................................................12

4.1Main financial statement with their purpose, contents and makers.....................................12

4.2Comparison between different financial statement .............................................................13

4.3Interpreatation of financial statement by using different ratios and comparison.................13

CONCLUSION ..............................................................................................................14

REFERENCES..............................................................................................................................15

MANAGING FINANCIAL RESOURCES.....................................................................................1

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

1.1 The sources of finance available to a business......................................................................3

1.2 Implication of sources of finance..........................................................................................4

1.3 Evaluation of appropriate sources of finance for a business ................................................4

2.1 Cost of sources of finance ....................................................................................................5

2.2Importance of financial planning and how it is undertaken ..................................................6

2.3The information needs of internal and external decision makers..........................................7

2.4 Impact of finance on financial statement..............................................................................7

3.1 Cash budget for cited organisation........................................................................................8

3.2 Calculation of unit cost along with the making of effective pricing decisions.....................8

3.3 Different investment appraisal techniques for the organisation..........................................10

TASK 2..........................................................................................................................................12

4.1Main financial statement with their purpose, contents and makers.....................................12

4.2Comparison between different financial statement .............................................................13

4.3Interpreatation of financial statement by using different ratios and comparison.................13

CONCLUSION ..............................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

Financial resources are the basic elements which helps a firm to operate their daily and

routine operations. Firm uses its shares in the market and number of people buy such shares and

pay some money to the company. Such shareholders are the financial resource of the company.

The term financial resource is made with the combination of two words: financial which is in the

form of money and the other one is resources which means the way. So, by the term financial

resources means the way through which money enters in the business. Money is a basic need of a

business and proper allocation of resources is compulsory. For this purpose entity have to

prepare budget in which all the operations which are related with the business is mentioned. This

helps in making the decision of the business effective and helps in made a positive impact of

such decisions on the organisation. All such factors are going to discussed in this report with

more evaluation with the help of taking the example of Sainsbury with its budget.

TASK 1

1.1 The sources of finance available to a business

Business Loan: Business loan is a traditional but still popular source as a funding option

for start-ups and retained equity is an additional advantage (Zhu and et. al., 2010). Even the

government support in the availability of these kind of loans to small business firms. Banks also

provide long-term kind of finance for start-ups. The bank states the fixed period in which the

amount is to be paid back, the rate of interest and amount of repayments. The banks usually asks

for some security for the loan from the start-ups, and these security generally are in form of the

entrepreneur's personal guarantee. These form of funds are good for investing finance in fixed

assets and are usually at a lower rate of interest.

Outside Investors (Share Capital): One of the main source of investment in a start-up

are family and friends of the entrepreneur. Opinions of either of them may sometimes differ in

case of the influence of the one who came out with the idea and how strong it is. Investments of

an average amount for a longer period may depend on the individual's encouragement towards

the entrepreneur whom he personally know. May be they are ready to invest but not interested in

participating in the daily operation of the business.

Business Angels: Angel investors are professional investors and the amount they

generally invest in a start-up may differ from £10k - £750k. Angels are experts in proven

Financial resources are the basic elements which helps a firm to operate their daily and

routine operations. Firm uses its shares in the market and number of people buy such shares and

pay some money to the company. Such shareholders are the financial resource of the company.

The term financial resource is made with the combination of two words: financial which is in the

form of money and the other one is resources which means the way. So, by the term financial

resources means the way through which money enters in the business. Money is a basic need of a

business and proper allocation of resources is compulsory. For this purpose entity have to

prepare budget in which all the operations which are related with the business is mentioned. This

helps in making the decision of the business effective and helps in made a positive impact of

such decisions on the organisation. All such factors are going to discussed in this report with

more evaluation with the help of taking the example of Sainsbury with its budget.

TASK 1

1.1 The sources of finance available to a business

Business Loan: Business loan is a traditional but still popular source as a funding option

for start-ups and retained equity is an additional advantage (Zhu and et. al., 2010). Even the

government support in the availability of these kind of loans to small business firms. Banks also

provide long-term kind of finance for start-ups. The bank states the fixed period in which the

amount is to be paid back, the rate of interest and amount of repayments. The banks usually asks

for some security for the loan from the start-ups, and these security generally are in form of the

entrepreneur's personal guarantee. These form of funds are good for investing finance in fixed

assets and are usually at a lower rate of interest.

Outside Investors (Share Capital): One of the main source of investment in a start-up

are family and friends of the entrepreneur. Opinions of either of them may sometimes differ in

case of the influence of the one who came out with the idea and how strong it is. Investments of

an average amount for a longer period may depend on the individual's encouragement towards

the entrepreneur whom he personally know. May be they are ready to invest but not interested in

participating in the daily operation of the business.

Business Angels: Angel investors are professional investors and the amount they

generally invest in a start-up may differ from £10k - £750k. Angels are experts in proven

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

entrepreneurship and tend to invest in businesses with huge growth prospects (Surroca, Tribó

and Waddock, 2010). Their part of investment either comes out of their already settled

business or selling their own business.

1.2 Implication of sources of finance

Loans: Debenture loans, usually secured against asset of the entrepreneur or investor.

The sources of loans usually charges variable or fixed rate of interest on the amount loaned. This

makes the entrepreneur unable to send the asset without the priority of the lenders agreement

(Kusumasari, Alam and Siddiqui, 2010). And in case, the shareholder or the

entrepreneur fails to pay the loan within the given time period, the cost will be repaid even it

may result in a loss by the sale of the asset assigned as security against the loan.

Venture Capital: The source of finance best for a newly started business firm at its early

stages. High level of risks are predictable in the way if this source of finance is owned. But also

the possible potentials seem are big too. The venture capitalists generally look for a share in the

firm's equity and it can be the biggest part of the risk. They often look for a strong return for their

investment. Venture capitals are mostly being acknowledged by the shareholders and

entrepreneurs for their important presence while in the running of the business to prove the value

of themselves.

Credit from Suppliers: Supplier credits are issued for 30 days or more. Maximum

amount of time can be taken by a company to get the money utilized very well and pay back

within the interim period so that they could finance other things (Rockey and Collins,

2010). This method should be considered cautious to make sure that the invoice is been paid on

time. Otherwise, the firm might end up upsetting the supplier and the future working

relationship will be jeopardised.

1.3 Evaluation of appropriate sources of finance for a business

There are two types of sources in the sources of finance for a

business. They are:

External sources, and

Internal sources.

The sources of fund included in external sources are:

Loans

and Waddock, 2010). Their part of investment either comes out of their already settled

business or selling their own business.

1.2 Implication of sources of finance

Loans: Debenture loans, usually secured against asset of the entrepreneur or investor.

The sources of loans usually charges variable or fixed rate of interest on the amount loaned. This

makes the entrepreneur unable to send the asset without the priority of the lenders agreement

(Kusumasari, Alam and Siddiqui, 2010). And in case, the shareholder or the

entrepreneur fails to pay the loan within the given time period, the cost will be repaid even it

may result in a loss by the sale of the asset assigned as security against the loan.

Venture Capital: The source of finance best for a newly started business firm at its early

stages. High level of risks are predictable in the way if this source of finance is owned. But also

the possible potentials seem are big too. The venture capitalists generally look for a share in the

firm's equity and it can be the biggest part of the risk. They often look for a strong return for their

investment. Venture capitals are mostly being acknowledged by the shareholders and

entrepreneurs for their important presence while in the running of the business to prove the value

of themselves.

Credit from Suppliers: Supplier credits are issued for 30 days or more. Maximum

amount of time can be taken by a company to get the money utilized very well and pay back

within the interim period so that they could finance other things (Rockey and Collins,

2010). This method should be considered cautious to make sure that the invoice is been paid on

time. Otherwise, the firm might end up upsetting the supplier and the future working

relationship will be jeopardised.

1.3 Evaluation of appropriate sources of finance for a business

There are two types of sources in the sources of finance for a

business. They are:

External sources, and

Internal sources.

The sources of fund included in external sources are:

Loans

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Overdrafts

Debentures

Shareholders

Factoring Debts

The sources of finance that comes under internal sources are:

Profits

Sale of assets

Reduced working capital

External sources of finance is flexible and the source is generally for

long terms and thus it can cover the flexibility of the monthly payment

interval. Even this source is quick. Sources like overdrafts are easy to

manage and quick as the cash flow takes place easy in the format (Swayne,

Duncan and Ginter, 2012). In case of internal sources of fund raising, there

are certain advantages of no paper works needed to be done and the

payment to be made to self has no interest to be paid on it. And there is no

need of payment from the profits, as the amount raised in the period of

establishment was made by the own capability of the entrepreneur.

The profit for the entrepreneur is much more than the good money

paid to the customer at higher rates. The money value of share may go up

and up in the stock market and increases in terms of profit. The shares

could be easily sold in the share market. The equity share issued could

increase the capital and is not paid back. The company is not liable of the

issue payment of the dividend, given for making profit.

2.1 Cost of sources of finance

The cost is the amount the entity must pay to raise the finance for

starting the business. Cost of capital is a term referring to the cost

paid by an organization to raise the funds. Bond issuing and loans

from banks can be a part of this (Snell, Morris and Bohlander, 2015).

It is generally presented in form of an annual percentage.

Debentures

Shareholders

Factoring Debts

The sources of finance that comes under internal sources are:

Profits

Sale of assets

Reduced working capital

External sources of finance is flexible and the source is generally for

long terms and thus it can cover the flexibility of the monthly payment

interval. Even this source is quick. Sources like overdrafts are easy to

manage and quick as the cash flow takes place easy in the format (Swayne,

Duncan and Ginter, 2012). In case of internal sources of fund raising, there

are certain advantages of no paper works needed to be done and the

payment to be made to self has no interest to be paid on it. And there is no

need of payment from the profits, as the amount raised in the period of

establishment was made by the own capability of the entrepreneur.

The profit for the entrepreneur is much more than the good money

paid to the customer at higher rates. The money value of share may go up

and up in the stock market and increases in terms of profit. The shares

could be easily sold in the share market. The equity share issued could

increase the capital and is not paid back. The company is not liable of the

issue payment of the dividend, given for making profit.

2.1 Cost of sources of finance

The cost is the amount the entity must pay to raise the finance for

starting the business. Cost of capital is a term referring to the cost

paid by an organization to raise the funds. Bond issuing and loans

from banks can be a part of this (Snell, Morris and Bohlander, 2015).

It is generally presented in form of an annual percentage.

The contributed weight of every source of capital by the total funding

proportion it provides is known as weighted average cost of capital

(WACC). WACC also appears as an annual percentage.

The amount paid by the debtor to secure a loan and the fund to be

used that includes maintenance of accounts, cost of finance,

origination of loan and other expenses related to the loan are referred

to as cost of borrowing. Cost of borrowing is measured as amounts, in

the currency of nation where the company is situated.

The amount an organization pays as an overall average rate on all its

debts are called as cost of debt. Cost of debt is appeared as annual

percentage.

The returns produced by the demands of the stock market investors

who are bearing the risk of being owners are called as cost of

equity(COE). Usually, COE is to be appeared as an annual percentage.

Cost of funds can be defined as the payment the financial institutions

made as the interest cost for the use of money (Renz, 2016). Appears

as an annual percentage.

Regionally divided rate of an established Cost of funds are known as

cost of funds index (COFI). Also appears as an annual percentage.

2.2Importance of financial planning and how it is undertaken

The short and long term life goals of an organization can only be

cleared by creating a financial plan. It is a step which is very crucial in

mapping out the financial future of the organization. It is much easy to

make decisions related to finance and keep focused on the organizational

objectives.

Financial management makes it possible to manage the income of the

organization more effectively. Management of the income helps in

understanding the amount of money needed in the future for tax

payments and other monthly expenditures.

proportion it provides is known as weighted average cost of capital

(WACC). WACC also appears as an annual percentage.

The amount paid by the debtor to secure a loan and the fund to be

used that includes maintenance of accounts, cost of finance,

origination of loan and other expenses related to the loan are referred

to as cost of borrowing. Cost of borrowing is measured as amounts, in

the currency of nation where the company is situated.

The amount an organization pays as an overall average rate on all its

debts are called as cost of debt. Cost of debt is appeared as annual

percentage.

The returns produced by the demands of the stock market investors

who are bearing the risk of being owners are called as cost of

equity(COE). Usually, COE is to be appeared as an annual percentage.

Cost of funds can be defined as the payment the financial institutions

made as the interest cost for the use of money (Renz, 2016). Appears

as an annual percentage.

Regionally divided rate of an established Cost of funds are known as

cost of funds index (COFI). Also appears as an annual percentage.

2.2Importance of financial planning and how it is undertaken

The short and long term life goals of an organization can only be

cleared by creating a financial plan. It is a step which is very crucial in

mapping out the financial future of the organization. It is much easy to

make decisions related to finance and keep focused on the organizational

objectives.

Financial management makes it possible to manage the income of the

organization more effectively. Management of the income helps in

understanding the amount of money needed in the future for tax

payments and other monthly expenditures.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial management supports in the increase in cash flow by

monitoring the organizations pattern of expenditure (Broadbent and

Cullen, 2012). Planning of taxes, prudent spending and budgeting

carefully is going to help the company more hard to earn money.

Increase in cash flow is followed by an increase in capital. Thus,

allowing the organization to think of investments to create progress in

you financial well being.

An appropriate financial plan gives importance to the entrepreneur's

personal situations and objectives. It also takes care of the risks

tolerated by him.

A good financial plan could help in saving and saving can help them

prove beneficial in difficult times (Surroca, Tribó and Waddock,

2010). It can also include the company's insurance coverage so that

any lost income shall be replaced under its care of.

Understanding the finance and its related surroundings can achieve

the financial goals that are measured during the decision making

process. It can help the company's budget attain a completely new

approach and suggest to improve control over financial lifestyle of

the organization.

2.3The information needs of internal and external decision makers

The organizational information of a company are communicated to the

external users generally in the form of financial statements (Zhu and et. al.,

2010). The financial statement's purpose is to provide the various need of

users in need of the market related information of the organization in order

to assist them create a better and effective set of financial decisions.

The information may contain the recording , classification and

transactions summarized and events in such a manner that it would help the

users to assess the performance financially and position of the entity. As

soon as the events and transactions are identified, they are recorded and

the classification is done, so as to summarize it in a manner that could help

monitoring the organizations pattern of expenditure (Broadbent and

Cullen, 2012). Planning of taxes, prudent spending and budgeting

carefully is going to help the company more hard to earn money.

Increase in cash flow is followed by an increase in capital. Thus,

allowing the organization to think of investments to create progress in

you financial well being.

An appropriate financial plan gives importance to the entrepreneur's

personal situations and objectives. It also takes care of the risks

tolerated by him.

A good financial plan could help in saving and saving can help them

prove beneficial in difficult times (Surroca, Tribó and Waddock,

2010). It can also include the company's insurance coverage so that

any lost income shall be replaced under its care of.

Understanding the finance and its related surroundings can achieve

the financial goals that are measured during the decision making

process. It can help the company's budget attain a completely new

approach and suggest to improve control over financial lifestyle of

the organization.

2.3The information needs of internal and external decision makers

The organizational information of a company are communicated to the

external users generally in the form of financial statements (Zhu and et. al.,

2010). The financial statement's purpose is to provide the various need of

users in need of the market related information of the organization in order

to assist them create a better and effective set of financial decisions.

The information may contain the recording , classification and

transactions summarized and events in such a manner that it would help the

users to assess the performance financially and position of the entity. As

soon as the events and transactions are identified, they are recorded and

the classification is done, so as to summarize it in a manner that could help

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the user of the organizational and accounting information to determine the

nature and the effects of those transaction a events.

2.4 Impact of finance on financial statement

Finance is a necessary element which helps in preparing all the financial statement. These

statements are generally prepared with the aim of examine the growth of the company,

investment of the firm etc. All such things are mentioned and can be clearly understandable to

the company shareholders with the help of financial statement. Without any fiscal activity an

entity will not be able to prepare their financial statement. For better understanding of the firm

whole year activities as well as their routine activities preparation of this evidence is compulsory.

If company is going to present their financial statement to the owners of the company which are

shareholders then it made a positive impact over on them and their investment can increase with

the help of this.

Profit and loss statement: A p/l statement helps in summarising the revenue, cost and expenses

of the company which are generally incur during the entire year. This helps in clear

understanding of all the detriment which are related with the business.

Balance sheet:A balance sheet is a summary of all the company total assets, liabilities and

shareholders equity. It helps to the investors to examine and monitor out what the company owes

and owns in the near future. This is a helpful factor because it also helps in the lucid

understanding of all the records which taken place during an accounting year(Aras, Aybars and

Kutlu, 2010).

Whenever any kind of financial transaction take place it become compulsory for an

organisation or a proprietor to record it in financial statement. So whenever any activity took

place it affect the fiscal evidence of a company. Hence by recording all the transactions in

corrective manner made a positive impact on a business as well as on its financial statement also.

If a business entity have good finance position in their financial statement then it promotes in

providing a true image of their organisation. Moreover it also create easiness in taking the

decision by their investors. Hence with the help of above mentioned statement it provides in

taking beneficial decision for a business related operations.

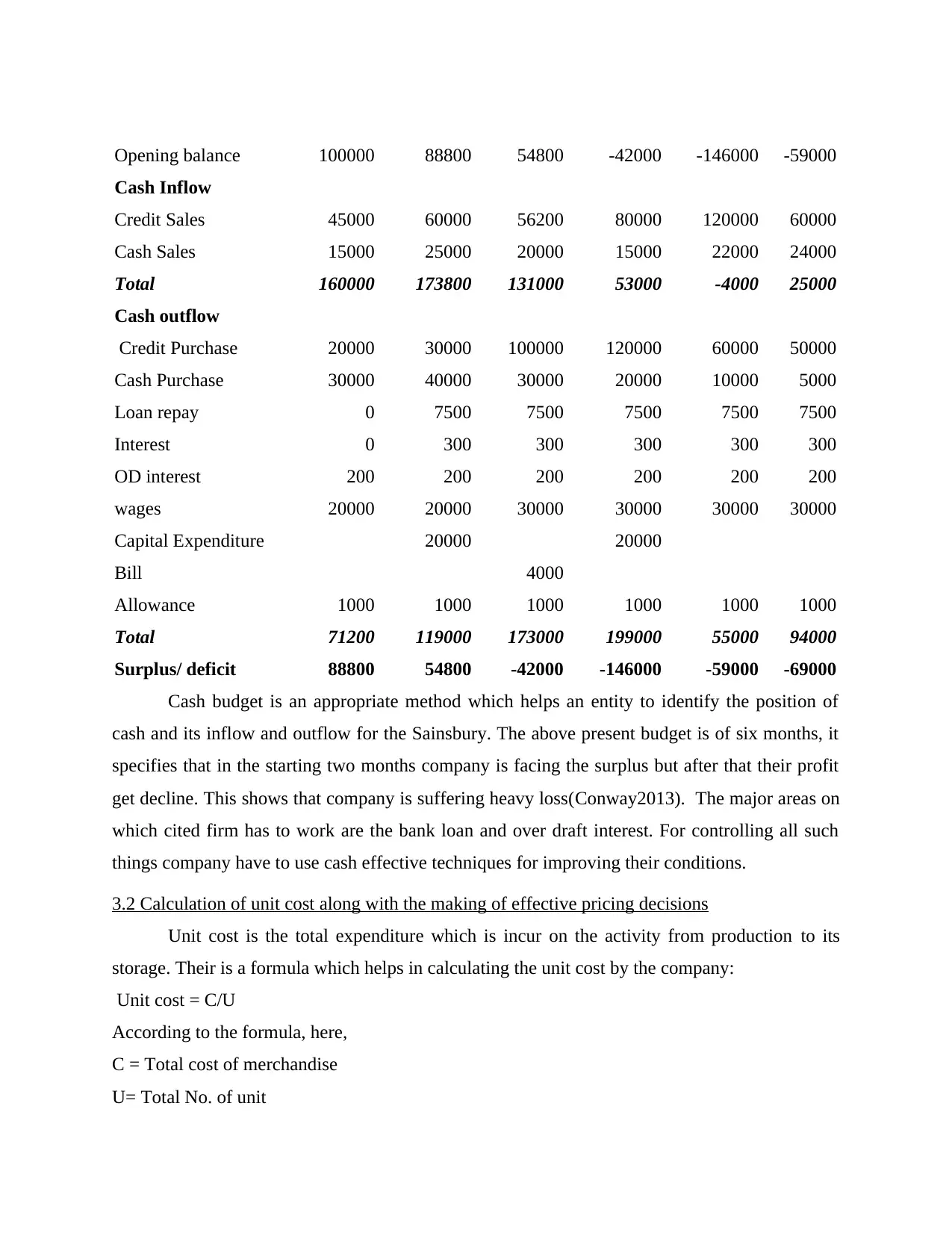

3.1 Cash budget for cited organisation

Table 1: Budget for J Siansbury PLC for six months

Particular January February March April May June

nature and the effects of those transaction a events.

2.4 Impact of finance on financial statement

Finance is a necessary element which helps in preparing all the financial statement. These

statements are generally prepared with the aim of examine the growth of the company,

investment of the firm etc. All such things are mentioned and can be clearly understandable to

the company shareholders with the help of financial statement. Without any fiscal activity an

entity will not be able to prepare their financial statement. For better understanding of the firm

whole year activities as well as their routine activities preparation of this evidence is compulsory.

If company is going to present their financial statement to the owners of the company which are

shareholders then it made a positive impact over on them and their investment can increase with

the help of this.

Profit and loss statement: A p/l statement helps in summarising the revenue, cost and expenses

of the company which are generally incur during the entire year. This helps in clear

understanding of all the detriment which are related with the business.

Balance sheet:A balance sheet is a summary of all the company total assets, liabilities and

shareholders equity. It helps to the investors to examine and monitor out what the company owes

and owns in the near future. This is a helpful factor because it also helps in the lucid

understanding of all the records which taken place during an accounting year(Aras, Aybars and

Kutlu, 2010).

Whenever any kind of financial transaction take place it become compulsory for an

organisation or a proprietor to record it in financial statement. So whenever any activity took

place it affect the fiscal evidence of a company. Hence by recording all the transactions in

corrective manner made a positive impact on a business as well as on its financial statement also.

If a business entity have good finance position in their financial statement then it promotes in

providing a true image of their organisation. Moreover it also create easiness in taking the

decision by their investors. Hence with the help of above mentioned statement it provides in

taking beneficial decision for a business related operations.

3.1 Cash budget for cited organisation

Table 1: Budget for J Siansbury PLC for six months

Particular January February March April May June

Opening balance 100000 88800 54800 -42000 -146000 -59000

Cash Inflow

Credit Sales 45000 60000 56200 80000 120000 60000

Cash Sales 15000 25000 20000 15000 22000 24000

Total 160000 173800 131000 53000 -4000 25000

Cash outflow

Credit Purchase 20000 30000 100000 120000 60000 50000

Cash Purchase 30000 40000 30000 20000 10000 5000

Loan repay 0 7500 7500 7500 7500 7500

Interest 0 300 300 300 300 300

OD interest 200 200 200 200 200 200

wages 20000 20000 30000 30000 30000 30000

Capital Expenditure 20000 20000

Bill 4000

Allowance 1000 1000 1000 1000 1000 1000

Total 71200 119000 173000 199000 55000 94000

Surplus/ deficit 88800 54800 -42000 -146000 -59000 -69000

Cash budget is an appropriate method which helps an entity to identify the position of

cash and its inflow and outflow for the Sainsbury. The above present budget is of six months, it

specifies that in the starting two months company is facing the surplus but after that their profit

get decline. This shows that company is suffering heavy loss(Conway2013). The major areas on

which cited firm has to work are the bank loan and over draft interest. For controlling all such

things company have to use cash effective techniques for improving their conditions.

3.2 Calculation of unit cost along with the making of effective pricing decisions

Unit cost is the total expenditure which is incur on the activity from production to its

storage. Their is a formula which helps in calculating the unit cost by the company:

Unit cost = C/U

According to the formula, here,

C = Total cost of merchandise

U= Total No. of unit

Cash Inflow

Credit Sales 45000 60000 56200 80000 120000 60000

Cash Sales 15000 25000 20000 15000 22000 24000

Total 160000 173800 131000 53000 -4000 25000

Cash outflow

Credit Purchase 20000 30000 100000 120000 60000 50000

Cash Purchase 30000 40000 30000 20000 10000 5000

Loan repay 0 7500 7500 7500 7500 7500

Interest 0 300 300 300 300 300

OD interest 200 200 200 200 200 200

wages 20000 20000 30000 30000 30000 30000

Capital Expenditure 20000 20000

Bill 4000

Allowance 1000 1000 1000 1000 1000 1000

Total 71200 119000 173000 199000 55000 94000

Surplus/ deficit 88800 54800 -42000 -146000 -59000 -69000

Cash budget is an appropriate method which helps an entity to identify the position of

cash and its inflow and outflow for the Sainsbury. The above present budget is of six months, it

specifies that in the starting two months company is facing the surplus but after that their profit

get decline. This shows that company is suffering heavy loss(Conway2013). The major areas on

which cited firm has to work are the bank loan and over draft interest. For controlling all such

things company have to use cash effective techniques for improving their conditions.

3.2 Calculation of unit cost along with the making of effective pricing decisions

Unit cost is the total expenditure which is incur on the activity from production to its

storage. Their is a formula which helps in calculating the unit cost by the company:

Unit cost = C/U

According to the formula, here,

C = Total cost of merchandise

U= Total No. of unit

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

In any workplace there are mainly three types of cost which are:

a) Fixed cost

b) Direct labour cost

c) Direct material cost

According to these types types, fixed cost is a such type of cost which do not get vary and

keep remain fixed. Company produce any quantity but the fixed cost remains the same(Farmeret.

And et. al., 2012).

Direct labour cost is directly paid to the labours which helps in making the merchandise.

This cost is generally paid directly to the workers or employees who are a part of the

organisation.

Direct material cost is simple in understand. It is same as direct labour cost but

not properly. This cost is paid in the purchasing of raw material and while making of the goods.

All such expenses are also includes in this concept which suddenly arises.

Now lets simplifies these definitions in the form of calculation. Sainsbury cost

calculation is as follow for the month of August. Let assume that total unit production is £6000

and direct material cost, direct labour cost and fixed cost are £ 10,000, £ 12,000 and £

14,000 . Along with the profit margin of 10%. So, the calculation of this concept is as follow:

Unit cost = C/U

= (£ 10,000+£ 12,000+£ 14,000)/ £6000

= £ 6 units.

Now another concept is if company added profit margin then selling price of the product

is get calculated.

Profit = £6* 10% = £0.6

Selling price = unit cost + profit

SP = £6+ £0.6

SP = £6.06.

Hence, profit of the company is 10% and the total unit production is £ 6 units. Then selling price

of the goods become £6.06. Another factor which can get concluded by this calculation is

company profit is £0.6.

So company have to set their price which is £6.06. This can only calculated with the help

of using formula. Company have to take their pricing decisions on the basis of such factors of

a) Fixed cost

b) Direct labour cost

c) Direct material cost

According to these types types, fixed cost is a such type of cost which do not get vary and

keep remain fixed. Company produce any quantity but the fixed cost remains the same(Farmeret.

And et. al., 2012).

Direct labour cost is directly paid to the labours which helps in making the merchandise.

This cost is generally paid directly to the workers or employees who are a part of the

organisation.

Direct material cost is simple in understand. It is same as direct labour cost but

not properly. This cost is paid in the purchasing of raw material and while making of the goods.

All such expenses are also includes in this concept which suddenly arises.

Now lets simplifies these definitions in the form of calculation. Sainsbury cost

calculation is as follow for the month of August. Let assume that total unit production is £6000

and direct material cost, direct labour cost and fixed cost are £ 10,000, £ 12,000 and £

14,000 . Along with the profit margin of 10%. So, the calculation of this concept is as follow:

Unit cost = C/U

= (£ 10,000+£ 12,000+£ 14,000)/ £6000

= £ 6 units.

Now another concept is if company added profit margin then selling price of the product

is get calculated.

Profit = £6* 10% = £0.6

Selling price = unit cost + profit

SP = £6+ £0.6

SP = £6.06.

Hence, profit of the company is 10% and the total unit production is £ 6 units. Then selling price

of the goods become £6.06. Another factor which can get concluded by this calculation is

company profit is £0.6.

So company have to set their price which is £6.06. This can only calculated with the help

of using formula. Company have to take their pricing decisions on the basis of such factors of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

cost which are fixed cost, direct labour cost and direct material cost. These elements are get

included by the firm to make their price(Singer et. al., 2011).

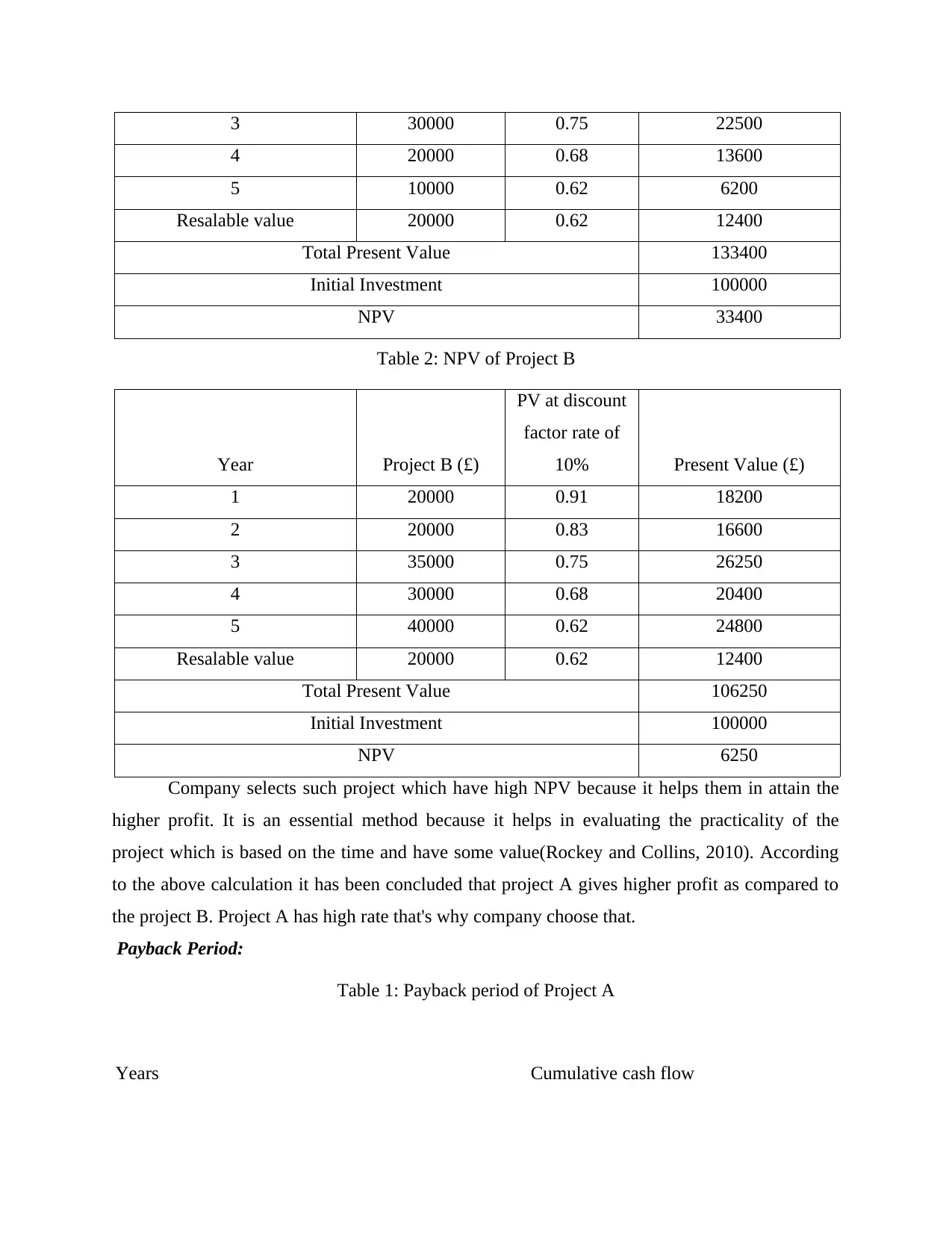

3.3 Different investment appraisal techniques for the organisation

Investment appraisal techniques are used by the firm top find out the appropriate project

in which company want to invest their money. This technique is helpful because it helps in

selecting a best project from numerous numbers. Some famous techniques of the investment

appraisals are:

1. Net present value

2. Accounting rate of return

3. Payback period

4. Internal rate of return

These approaches are used by the firm to find out the best project from group of task.

Calculation of new present value and payback period are as follow:

Year Project A

(£)

Project B

(£)

1

2

3

4

5

Salvage value

Initial Investment

50000

40000

30000

20000

10000

20000

100000

20000

25000

40000

50000

60000

20000

100000

Net Present Value:

Table 1: NPV of Project A

Year Project A (£)

PV at discount

factor rate of

10% Present Value (£)

1 50000 0.91 45500

2 40000 0.83 33200

included by the firm to make their price(Singer et. al., 2011).

3.3 Different investment appraisal techniques for the organisation

Investment appraisal techniques are used by the firm top find out the appropriate project

in which company want to invest their money. This technique is helpful because it helps in

selecting a best project from numerous numbers. Some famous techniques of the investment

appraisals are:

1. Net present value

2. Accounting rate of return

3. Payback period

4. Internal rate of return

These approaches are used by the firm to find out the best project from group of task.

Calculation of new present value and payback period are as follow:

Year Project A

(£)

Project B

(£)

1

2

3

4

5

Salvage value

Initial Investment

50000

40000

30000

20000

10000

20000

100000

20000

25000

40000

50000

60000

20000

100000

Net Present Value:

Table 1: NPV of Project A

Year Project A (£)

PV at discount

factor rate of

10% Present Value (£)

1 50000 0.91 45500

2 40000 0.83 33200

3 30000 0.75 22500

4 20000 0.68 13600

5 10000 0.62 6200

Resalable value 20000 0.62 12400

Total Present Value 133400

Initial Investment 100000

NPV 33400

Table 2: NPV of Project B

Year Project B (£)

PV at discount

factor rate of

10% Present Value (£)

1 20000 0.91 18200

2 20000 0.83 16600

3 35000 0.75 26250

4 30000 0.68 20400

5 40000 0.62 24800

Resalable value 20000 0.62 12400

Total Present Value 106250

Initial Investment 100000

NPV 6250

Company selects such project which have high NPV because it helps them in attain the

higher profit. It is an essential method because it helps in evaluating the practicality of the

project which is based on the time and have some value(Rockey and Collins, 2010). According

to the above calculation it has been concluded that project A gives higher profit as compared to

the project B. Project A has high rate that's why company choose that.

Payback Period:

Table 1: Payback period of Project A

Years Cumulative cash flow

4 20000 0.68 13600

5 10000 0.62 6200

Resalable value 20000 0.62 12400

Total Present Value 133400

Initial Investment 100000

NPV 33400

Table 2: NPV of Project B

Year Project B (£)

PV at discount

factor rate of

10% Present Value (£)

1 20000 0.91 18200

2 20000 0.83 16600

3 35000 0.75 26250

4 30000 0.68 20400

5 40000 0.62 24800

Resalable value 20000 0.62 12400

Total Present Value 106250

Initial Investment 100000

NPV 6250

Company selects such project which have high NPV because it helps them in attain the

higher profit. It is an essential method because it helps in evaluating the practicality of the

project which is based on the time and have some value(Rockey and Collins, 2010). According

to the above calculation it has been concluded that project A gives higher profit as compared to

the project B. Project A has high rate that's why company choose that.

Payback Period:

Table 1: Payback period of Project A

Years Cumulative cash flow

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.