Financial Analysis and Decision-Making Report for Trustlis Ltd

VerifiedAdded on 2020/01/16

|14

|4198

|101

Report

AI Summary

This report provides a comprehensive analysis of financial management, focusing on the case of Trustlis Ltd. It begins by exploring various sources of finance, including equity capital, debentures, bank loans, leasing, and angel investors, along with their implications. The report then delves into the costs of different financing options and the importance of financial planning, covering income, cash flow, capital, and investment strategies. Key needs of decision-makers, such as organizational size, business nature, and cost of capital, are examined. Furthermore, the report assesses the impact of finance on financial statements, including sales, expenses, and borrowing costs, and includes a cash flow projection for a specific period. The report concludes by emphasizing the importance of effective financial resource management for business growth and sustainability.

Managing Financial Resources and

Decisions

Decisions

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Introduction......................................................................................................................................3

TASK 1............................................................................................................................................3

1.1.................................................................................................................................................3

1.2.................................................................................................................................................4

1.3.................................................................................................................................................4

TASK 2............................................................................................................................................5

2.3.................................................................................................................................................6

2.4.................................................................................................................................................7

TASK 3............................................................................................................................................7

3.1.................................................................................................................................................7

3.2.................................................................................................................................................8

3.3 ................................................................................................................................................9

TASK 4..........................................................................................................................................10

4.1 ..............................................................................................................................................10

4.2...............................................................................................................................................10

4.3...............................................................................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

2

Introduction......................................................................................................................................3

TASK 1............................................................................................................................................3

1.1.................................................................................................................................................3

1.2.................................................................................................................................................4

1.3.................................................................................................................................................4

TASK 2............................................................................................................................................5

2.3.................................................................................................................................................6

2.4.................................................................................................................................................7

TASK 3............................................................................................................................................7

3.1.................................................................................................................................................7

3.2.................................................................................................................................................8

3.3 ................................................................................................................................................9

TASK 4..........................................................................................................................................10

4.1 ..............................................................................................................................................10

4.2...............................................................................................................................................10

4.3...............................................................................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

2

INTRODUCTION

Finance is all about money management and it plays a crucial role in fabrication of a new

business concern. It includes two aspects that are Procurement of funds and Effective Utilization

of funds. This leads an organization to identify its opportunities and grow in the competitive

market. This research report is based on evaluation of financing options for Trustlis Ltd. Further,

financial performance for Dixons Plc is evaluated through the report. This report also includes

the sources of finance available for any start up and what are its implications within the business.

Evaluating the performance of the business and financial decisions which are to be taken are also

discussed in this report.

TASK 1

1.1

The sources of finance available for expansion of business operation of Trustlis Ltd are listed

underneath in detail. Equity capital: The organisation can issue equity capital to raise funds for expansion of

operations. Acquisition of funds by way of equity capital do provide voting rights.

However, it does not set any fixed obligation for regular payments. The equity capital is

always suitable to acquire funds for expansion of operations. Issue of debentures: The organization can issue corporate bonds or debentures so as to

raise capital for long term. It helps in acquisition of funds at reasonable cost of capital.

Bank Loans- The firm can take loan from the bank at a certain rate of interest. This is

considered as one of the most flexible sources of finance but the applier need to agree

upon certain terms and conditions of the bank (Rostamkalaei, and Freel, 2016).

Leasing- It is another option for acquiring capital asset, an agreement between the two

parties that is lessor and lessee is done. Lessor is the possessor of the capital asset and

permits the lessee to utilize it for the agreed period. The payment is made under the terms

of the lease and for a specified period of time. The lessee is responsible for the upkeep

and maintenance of the leased asset.

Angel investors- The persons which are retired and wealthy and are willing to invest in

any other firm in which they are already specialized in the past act as angels. These

3

Finance is all about money management and it plays a crucial role in fabrication of a new

business concern. It includes two aspects that are Procurement of funds and Effective Utilization

of funds. This leads an organization to identify its opportunities and grow in the competitive

market. This research report is based on evaluation of financing options for Trustlis Ltd. Further,

financial performance for Dixons Plc is evaluated through the report. This report also includes

the sources of finance available for any start up and what are its implications within the business.

Evaluating the performance of the business and financial decisions which are to be taken are also

discussed in this report.

TASK 1

1.1

The sources of finance available for expansion of business operation of Trustlis Ltd are listed

underneath in detail. Equity capital: The organisation can issue equity capital to raise funds for expansion of

operations. Acquisition of funds by way of equity capital do provide voting rights.

However, it does not set any fixed obligation for regular payments. The equity capital is

always suitable to acquire funds for expansion of operations. Issue of debentures: The organization can issue corporate bonds or debentures so as to

raise capital for long term. It helps in acquisition of funds at reasonable cost of capital.

Bank Loans- The firm can take loan from the bank at a certain rate of interest. This is

considered as one of the most flexible sources of finance but the applier need to agree

upon certain terms and conditions of the bank (Rostamkalaei, and Freel, 2016).

Leasing- It is another option for acquiring capital asset, an agreement between the two

parties that is lessor and lessee is done. Lessor is the possessor of the capital asset and

permits the lessee to utilize it for the agreed period. The payment is made under the terms

of the lease and for a specified period of time. The lessee is responsible for the upkeep

and maintenance of the leased asset.

Angel investors- The persons which are retired and wealthy and are willing to invest in

any other firm in which they are already specialized in the past act as angels. These

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

angels give advice and contribute their experiences so the new set up can work efficiently

(Source of finance, 2014).

1.2

Implications of different source of financing are-

At the time of investing, one thing which should be kept in mind is that this money of

family and friends should be used cautiously. They do not charge any interest and returns for it.

But it should be returned as early as possible so it does not affect the relations. For establishing

the business as soon as possible, it needs to acquire assets more quickly. This can be done by

acquiring assets from hire seller and then purchaser can earn profit by selling it at high cost to the

other party by purchasing that asset in future (Quattrone, 2016). The only thing that he has to

keep in mind is that, paying all the installments at their due dates else these assets can be ceased

any time by the vendor. This will provide him assistance for making a systematic business plan.

The angels are already experienced in this so they can even help in getting a good staff of

trainees and employees. Although, the angels would charge a high amount of interest but it

would help in earning higher profits in the future. This would act as a best source of finance and

it would provide assistance for forming the new business in a well designed way which will

result in reducing the complications.

1.3

Appropriate sources of finance suitable for a business project are-

Equity capital: The organisation is raising funds for expanding operations which

demands capital for long run. Henceforth, the equity capital is considered to be suitable

option. The financing option does not raise set a fixed obligation for interest payments.

Further, no liability is set for re-payment of amount in long term. They share voting

rights and proportion of profits into extended operations of the business.

Business angel financing- Being new in the market and least knowledge, Trustlis Ltd.

should avail the option of angel financing as it will provide him a better assistance.

Selecting this option will set him free from making payments of interest and installments

on time. Also it will help him in reducing the complications in the future. Business

Angels are free to make decisions quickly as there is no requirement of personal assets. It

4

(Source of finance, 2014).

1.2

Implications of different source of financing are-

At the time of investing, one thing which should be kept in mind is that this money of

family and friends should be used cautiously. They do not charge any interest and returns for it.

But it should be returned as early as possible so it does not affect the relations. For establishing

the business as soon as possible, it needs to acquire assets more quickly. This can be done by

acquiring assets from hire seller and then purchaser can earn profit by selling it at high cost to the

other party by purchasing that asset in future (Quattrone, 2016). The only thing that he has to

keep in mind is that, paying all the installments at their due dates else these assets can be ceased

any time by the vendor. This will provide him assistance for making a systematic business plan.

The angels are already experienced in this so they can even help in getting a good staff of

trainees and employees. Although, the angels would charge a high amount of interest but it

would help in earning higher profits in the future. This would act as a best source of finance and

it would provide assistance for forming the new business in a well designed way which will

result in reducing the complications.

1.3

Appropriate sources of finance suitable for a business project are-

Equity capital: The organisation is raising funds for expanding operations which

demands capital for long run. Henceforth, the equity capital is considered to be suitable

option. The financing option does not raise set a fixed obligation for interest payments.

Further, no liability is set for re-payment of amount in long term. They share voting

rights and proportion of profits into extended operations of the business.

Business angel financing- Being new in the market and least knowledge, Trustlis Ltd.

should avail the option of angel financing as it will provide him a better assistance.

Selecting this option will set him free from making payments of interest and installments

on time. Also it will help him in reducing the complications in the future. Business

Angels are free to make decisions quickly as there is no requirement of personal assets. It

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

will also help in getting a trained staff for the salon (Miller, Steier and Breton‐Miller.

2016).

TASK 2

2.1

The costs of various sources of finance are to be incurred by the owner. There are

sufficient funds available with the possessor for investing it personally. So Trustlis Ltd. does not

required to bear any cost for this as these are his personal savings but needs to effectively utilize

his money. Further, as he is purchasing assets from hire purchaser he needs to pay a fixed

amount of interest on it along with installments for a specified time and he has to take care of

discharging this responsibility. Along with that, he has to make a down payment at the time of

agreement. As he is also using business angel source of finance they would demand higher

returns on it. Trustlis Ltd. is going to take loan therefore he also needs to pay interest and

installment for that loan also (Damodaran, 2016). So, the major responsibility of the Trustlis Ltd.

is to manage the funds available with him along with completing his duties of making the

payments for the limited time period and to pay taxes in additional as he is in the service sector

and service tax is also required to be paid. Trustlis Ltd. will have to face some problems but once

he creates goodwill of the firm by providing better services then it would result in higher returns

and growth. Then later on, the firm will provide with the good earnings (Mahmoud, 2016).

2.2

Financial planning is important because it helps to determine the short term and long term

financial goals which help in creating a balanced plan to meet this content. Income-Through effective planning, it becomes easier to manage the income. Managing

income helps in knowing that what amount should be used for paying taxes, meeting

monthly expenditures and even it leads to savings. Cash flow- Continuously checks on the expenses and spending leads to easier

management of cash (Quattrone, 2016). Capital- As there is inflow of cash in the firm, it leads to increase in capital. Family security- It provides security to family as insurance policies and coverage also

form a part of the financial planning process.

5

2016).

TASK 2

2.1

The costs of various sources of finance are to be incurred by the owner. There are

sufficient funds available with the possessor for investing it personally. So Trustlis Ltd. does not

required to bear any cost for this as these are his personal savings but needs to effectively utilize

his money. Further, as he is purchasing assets from hire purchaser he needs to pay a fixed

amount of interest on it along with installments for a specified time and he has to take care of

discharging this responsibility. Along with that, he has to make a down payment at the time of

agreement. As he is also using business angel source of finance they would demand higher

returns on it. Trustlis Ltd. is going to take loan therefore he also needs to pay interest and

installment for that loan also (Damodaran, 2016). So, the major responsibility of the Trustlis Ltd.

is to manage the funds available with him along with completing his duties of making the

payments for the limited time period and to pay taxes in additional as he is in the service sector

and service tax is also required to be paid. Trustlis Ltd. will have to face some problems but once

he creates goodwill of the firm by providing better services then it would result in higher returns

and growth. Then later on, the firm will provide with the good earnings (Mahmoud, 2016).

2.2

Financial planning is important because it helps to determine the short term and long term

financial goals which help in creating a balanced plan to meet this content. Income-Through effective planning, it becomes easier to manage the income. Managing

income helps in knowing that what amount should be used for paying taxes, meeting

monthly expenditures and even it leads to savings. Cash flow- Continuously checks on the expenses and spending leads to easier

management of cash (Quattrone, 2016). Capital- As there is inflow of cash in the firm, it leads to increase in capital. Family security- It provides security to family as insurance policies and coverage also

form a part of the financial planning process.

5

Investment- If the right investment is made then it would lead to more and more returns

and thus result in profit increase. This helps in fulfilling all personal as well as business

needs. Standard of living- A good planning can prove to be beneficial at the difficult times. Savings- This savings are very useful at the time of emergency. Some investments with

high liquidity are even required to meet the day to day expenses. Ongoing advices- Financial advisor by assessing the current financial situations can

prepare a customized plan which helps in achieving the long term goals (McPherson. and

Pincus.2016.).

Assets-Most of the assets come along with the liabilities attached to it so the relationship

between the financial advisors should be maintained so that he helps in reducing the

burden in the future.

2.3

The important needs of the decision makers are as follows-

Size of the organisation- It is very important to know the size of the organization

as it helps in further planning and the steps to be taken. Size of the company helps

in deciding that what all sort of funds are available and how much more is

required and what are the sources possible in case of extra needs.

Nature of the business- Nature of the business helps in deciding that what are its

requirements relating to the staff, machines and whether it will be able to sustain

in the market for long time (Miller, Steier and Breton‐Miller, 2016.).

Cost of capital – Owner of Trustlis Ltd. should be well in managing the

expenditures of the company as well as have enough liquidity to meet out those

expenditures and pay the instalment on due basis along with interest, taxes etc. He

should take the advice from the angel who will guide him in managing the funds

and get some savings for himself also.

2.4

There are many things that are to be taken into account while considering the impact of

finance on financial statements such as the sales, collection of money, expenses cost, cost of

6

and thus result in profit increase. This helps in fulfilling all personal as well as business

needs. Standard of living- A good planning can prove to be beneficial at the difficult times. Savings- This savings are very useful at the time of emergency. Some investments with

high liquidity are even required to meet the day to day expenses. Ongoing advices- Financial advisor by assessing the current financial situations can

prepare a customized plan which helps in achieving the long term goals (McPherson. and

Pincus.2016.).

Assets-Most of the assets come along with the liabilities attached to it so the relationship

between the financial advisors should be maintained so that he helps in reducing the

burden in the future.

2.3

The important needs of the decision makers are as follows-

Size of the organisation- It is very important to know the size of the organization

as it helps in further planning and the steps to be taken. Size of the company helps

in deciding that what all sort of funds are available and how much more is

required and what are the sources possible in case of extra needs.

Nature of the business- Nature of the business helps in deciding that what are its

requirements relating to the staff, machines and whether it will be able to sustain

in the market for long time (Miller, Steier and Breton‐Miller, 2016.).

Cost of capital – Owner of Trustlis Ltd. should be well in managing the

expenditures of the company as well as have enough liquidity to meet out those

expenditures and pay the instalment on due basis along with interest, taxes etc. He

should take the advice from the angel who will guide him in managing the funds

and get some savings for himself also.

2.4

There are many things that are to be taken into account while considering the impact of

finance on financial statements such as the sales, collection of money, expenses cost, cost of

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

borrowings, payment of principal instalments etc. When sales increase, it leads to increase in

revenue in the income statement and affects the profit as well. Therefore, for making the sales

good Trustlis Ltd. 's owner by hiring good trainees are required to provide better and better

services. So the customers get satisfied with the services and avail the services next time also. It

would affect the owner's fund as well as the performance of the business. Efficient performance

will attract the new customers also as the existing customer will recommend others to go there

and avail those services (Mahmoud, 2016.). Further, in future if there is a need of business loan

then the financial statements would be analysed and checked by the lender if it creates a negative

effect then it would impact the financial decisions of the company. Lenders usually are interested

to invest in the business that has good financial numbers (Rostamkalaei and Freel, 2016).

TASK 3

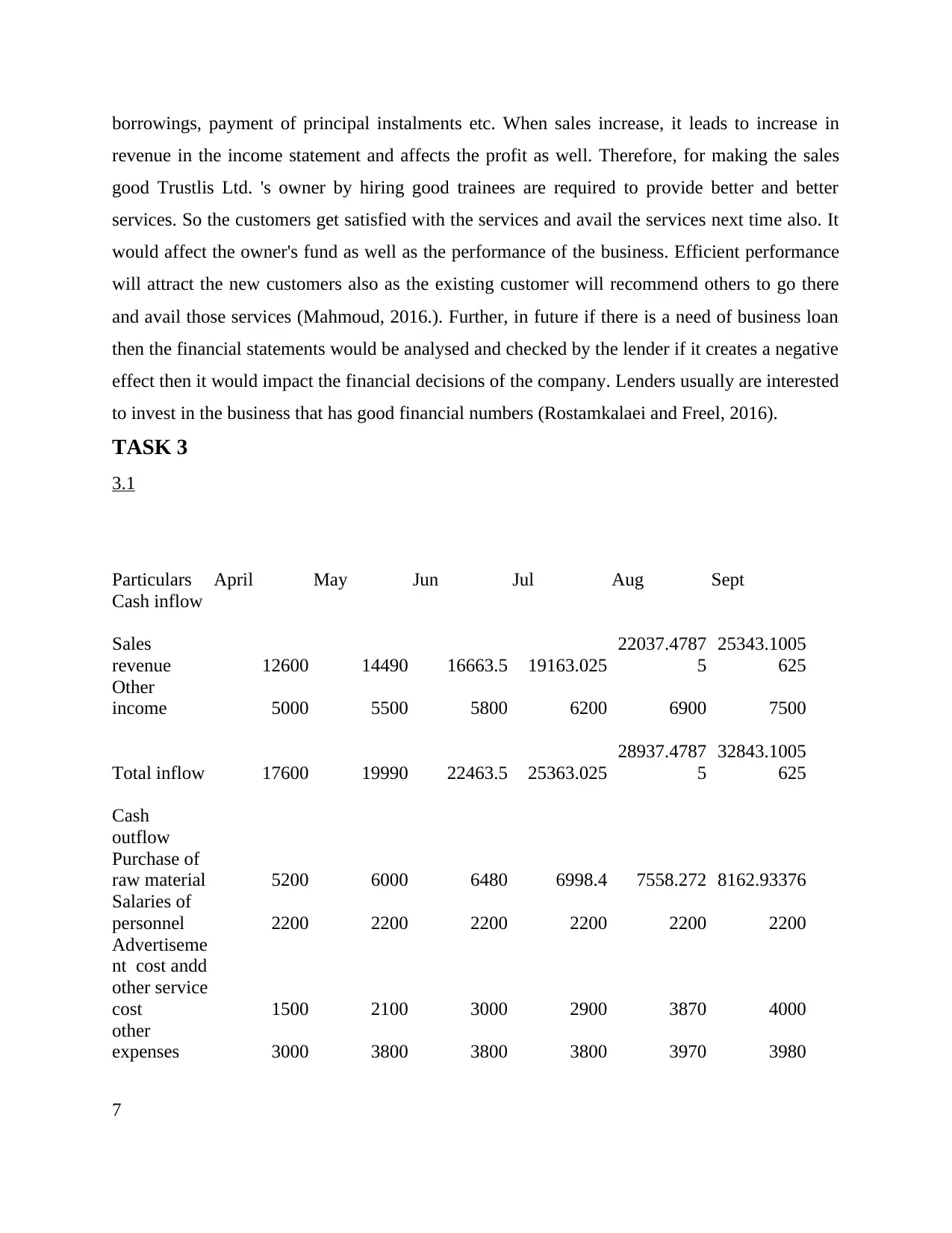

3.1

Particulars April May Jun Jul Aug Sept

Cash inflow

Sales

revenue 12600 14490 16663.5 19163.025

22037.4787

5

25343.1005

625

Other

income 5000 5500 5800 6200 6900 7500

Total inflow 17600 19990 22463.5 25363.025

28937.4787

5

32843.1005

625

Cash

outflow

Purchase of

raw material 5200 6000 6480 6998.4 7558.272 8162.93376

Salaries of

personnel 2200 2200 2200 2200 2200 2200

Advertiseme

nt cost andd

other service

cost 1500 2100 3000 2900 3870 4000

other

expenses 3000 3800 3800 3800 3970 3980

7

revenue in the income statement and affects the profit as well. Therefore, for making the sales

good Trustlis Ltd. 's owner by hiring good trainees are required to provide better and better

services. So the customers get satisfied with the services and avail the services next time also. It

would affect the owner's fund as well as the performance of the business. Efficient performance

will attract the new customers also as the existing customer will recommend others to go there

and avail those services (Mahmoud, 2016.). Further, in future if there is a need of business loan

then the financial statements would be analysed and checked by the lender if it creates a negative

effect then it would impact the financial decisions of the company. Lenders usually are interested

to invest in the business that has good financial numbers (Rostamkalaei and Freel, 2016).

TASK 3

3.1

Particulars April May Jun Jul Aug Sept

Cash inflow

Sales

revenue 12600 14490 16663.5 19163.025

22037.4787

5

25343.1005

625

Other

income 5000 5500 5800 6200 6900 7500

Total inflow 17600 19990 22463.5 25363.025

28937.4787

5

32843.1005

625

Cash

outflow

Purchase of

raw material 5200 6000 6480 6998.4 7558.272 8162.93376

Salaries of

personnel 2200 2200 2200 2200 2200 2200

Advertiseme

nt cost andd

other service

cost 1500 2100 3000 2900 3870 4000

other

expenses 3000 3800 3800 3800 3970 3980

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Total cash

outflow 11900 14100 15480 15898.4 17598.272

18342.9337

6

Cash

deficit /

surplus 5700 5890 6983.5 9464.625

11339.2067

5

14500.1668

025

opening

cash balance 12000 17700 23590 30573.5 40038.125

51377.3317

5

Closing cash

balance 17700 23590 30573.5 40038.125

51377.3317

5

65877.4985

525

As per the budget, sales has increased year by year which means performance of business

is good and its making profits yearly. Other incomes of the firm are also increasing representing

better returns in future also. On the other hand, company is also able to manage the daily

expenditures and paying the staff salaries on time. It has also been seen that firm is continuously

advertising and providing schemes also to create a reputation among the customers (Hopper and

Bui, 2016). Cash surplus is there may be the firm is providing better facilities to the customers

which have resulted in increase in sales proportionately. It also reveals that firm is operating

efficiently and is able to manage the expenses without incurring any extra cost.

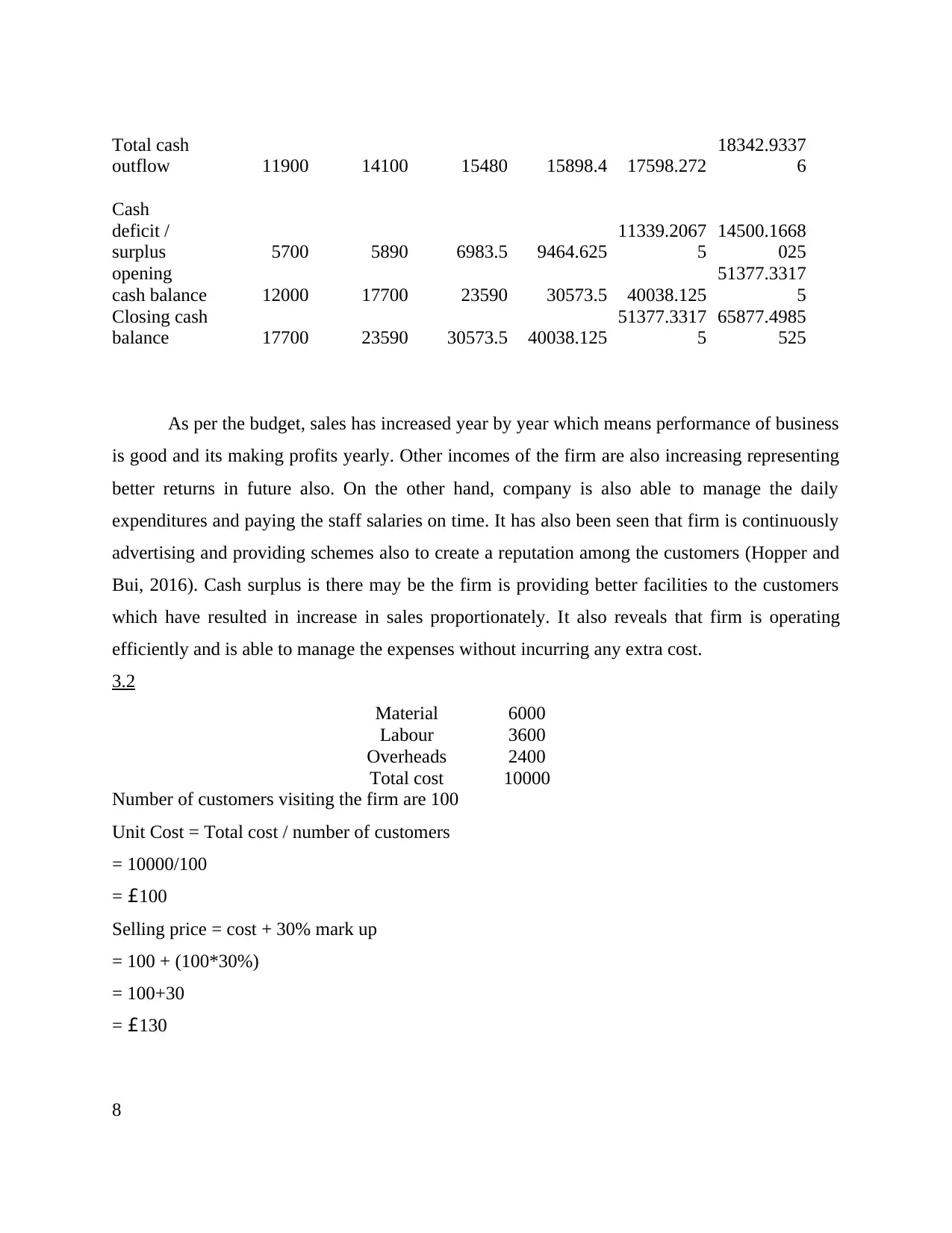

3.2

Material 6000

Labour 3600

Overheads 2400

Total cost 10000

Number of customers visiting the firm are 100

Unit Cost = Total cost / number of customers

= 10000/100

= £100

Selling price = cost + 30% mark up

= 100 + (100*30%)

= 100+30

= £130

8

outflow 11900 14100 15480 15898.4 17598.272

18342.9337

6

Cash

deficit /

surplus 5700 5890 6983.5 9464.625

11339.2067

5

14500.1668

025

opening

cash balance 12000 17700 23590 30573.5 40038.125

51377.3317

5

Closing cash

balance 17700 23590 30573.5 40038.125

51377.3317

5

65877.4985

525

As per the budget, sales has increased year by year which means performance of business

is good and its making profits yearly. Other incomes of the firm are also increasing representing

better returns in future also. On the other hand, company is also able to manage the daily

expenditures and paying the staff salaries on time. It has also been seen that firm is continuously

advertising and providing schemes also to create a reputation among the customers (Hopper and

Bui, 2016). Cash surplus is there may be the firm is providing better facilities to the customers

which have resulted in increase in sales proportionately. It also reveals that firm is operating

efficiently and is able to manage the expenses without incurring any extra cost.

3.2

Material 6000

Labour 3600

Overheads 2400

Total cost 10000

Number of customers visiting the firm are 100

Unit Cost = Total cost / number of customers

= 10000/100

= £100

Selling price = cost + 30% mark up

= 100 + (100*30%)

= 100+30

= £130

8

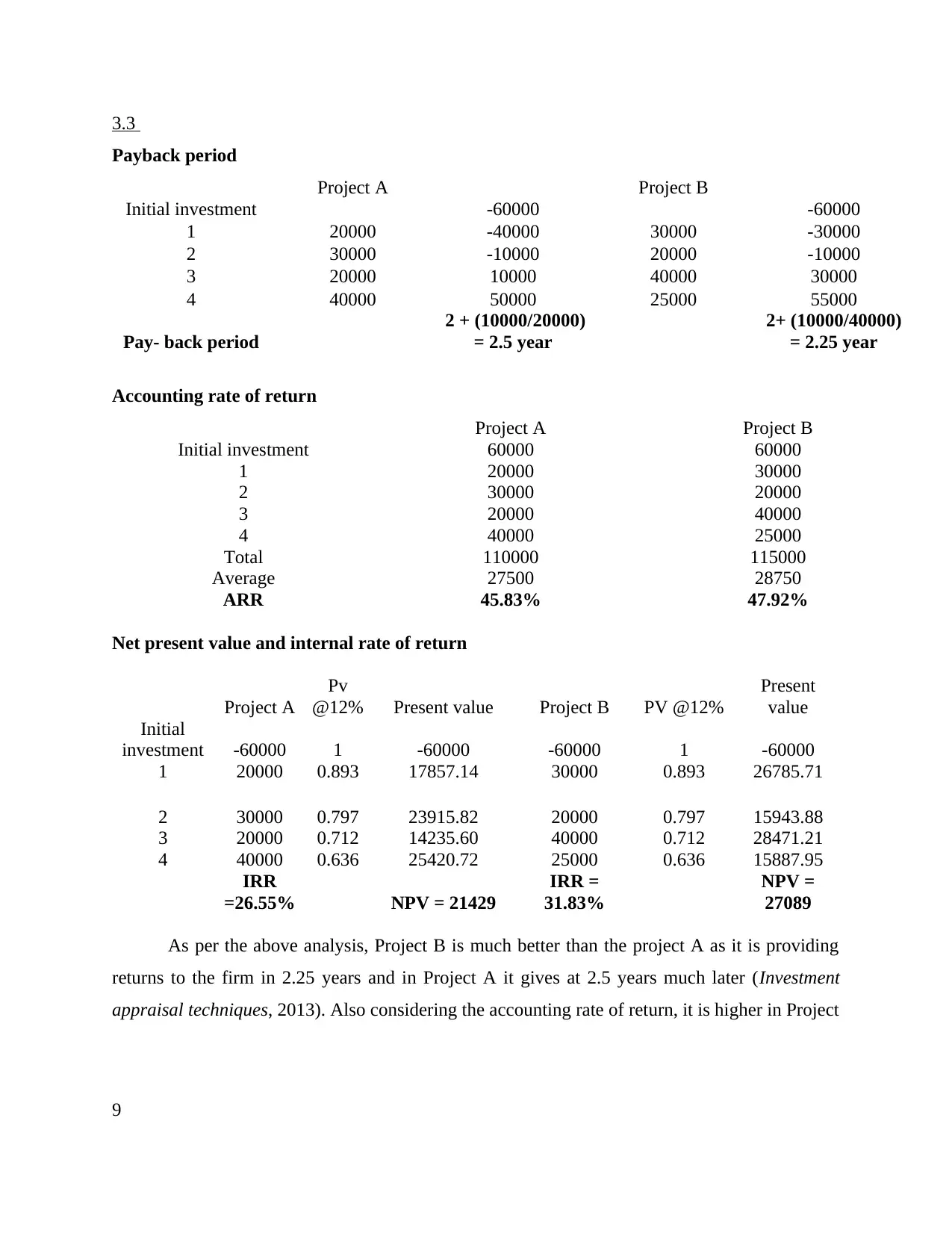

3.3

Payback period

Project A Project B

Initial investment -60000 -60000

1 20000 -40000 30000 -30000

2 30000 -10000 20000 -10000

3 20000 10000 40000 30000

4 40000 50000 25000 55000

Pay- back period

2 + (10000/20000)

= 2.5 year

2+ (10000/40000)

= 2.25 year

Accounting rate of return

Project A Project B

Initial investment 60000 60000

1 20000 30000

2 30000 20000

3 20000 40000

4 40000 25000

Total 110000 115000

Average 27500 28750

ARR 45.83% 47.92%

Net present value and internal rate of return

Project A

Pv

@12% Present value Project B PV @12%

Present

value

Initial

investment -60000 1 -60000 -60000 1 -60000

1 20000 0.893 17857.14 30000 0.893 26785.71

2 30000 0.797 23915.82 20000 0.797 15943.88

3 20000 0.712 14235.60 40000 0.712 28471.21

4 40000 0.636 25420.72 25000 0.636 15887.95

IRR

=26.55% NPV = 21429

IRR =

31.83%

NPV =

27089

As per the above analysis, Project B is much better than the project A as it is providing

returns to the firm in 2.25 years and in Project A it gives at 2.5 years much later (Investment

appraisal techniques, 2013). Also considering the accounting rate of return, it is higher in Project

9

Payback period

Project A Project B

Initial investment -60000 -60000

1 20000 -40000 30000 -30000

2 30000 -10000 20000 -10000

3 20000 10000 40000 30000

4 40000 50000 25000 55000

Pay- back period

2 + (10000/20000)

= 2.5 year

2+ (10000/40000)

= 2.25 year

Accounting rate of return

Project A Project B

Initial investment 60000 60000

1 20000 30000

2 30000 20000

3 20000 40000

4 40000 25000

Total 110000 115000

Average 27500 28750

ARR 45.83% 47.92%

Net present value and internal rate of return

Project A

Pv

@12% Present value Project B PV @12%

Present

value

Initial

investment -60000 1 -60000 -60000 1 -60000

1 20000 0.893 17857.14 30000 0.893 26785.71

2 30000 0.797 23915.82 20000 0.797 15943.88

3 20000 0.712 14235.60 40000 0.712 28471.21

4 40000 0.636 25420.72 25000 0.636 15887.95

IRR

=26.55% NPV = 21429

IRR =

31.83%

NPV =

27089

As per the above analysis, Project B is much better than the project A as it is providing

returns to the firm in 2.25 years and in Project A it gives at 2.5 years much later (Investment

appraisal techniques, 2013). Also considering the accounting rate of return, it is higher in Project

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

B which is 47.92% and internal rate of return is also higher in B which is 31.83% as compared to

the project A. So the company should adopt the project B (Filip, 2016).

TASK 4

4.1

The main types of financial statements are-

Balance Sheet- This statement discloses the financial position of any company on a particular

date. It includes - Assets- The things which are owned by the company are assets .It may be either tangible

or intangible like plants and machinery, equipments, patent and copyright. Liabilities-The thing which the company owes to the others are liabilities it may be either

creditors, bank loans etc (Goel, 2016). Equity- The things which remains in the business after the assets which are used to pay

off of its outstanding liabilities. In other words, difference between assets and liabilities is

called equity.

Income Statement- This shows the financial performance of the business in terms of profit or

loss over a specified period of time. It is also known as a profit and loss statement. Further it

includes the income and expenses which are earned and met by the company.

Cash flow statements- This statement reveals that what all types of activities resulted in the

inflow and outflow of cash. So that the firm is able to meet out its working capital expenses and

maintain the amount of liquidity (Crosby and Henneberry, 2016).

Statement of changes in equity- The amount of retained earnings can be revealed by this

statement only that what is left after the payment of all liabilities, interests and dividends. It also

derives the effects of change in any accounting policy or any corrections in the accounting error.

4.2

Different accounts are maintained by the different size of the firm. A sole trader

maintains only the Profit and loss statement, Balance Sheet and mainly Cash book to reveal the

performance of his firms. Though these statements are not mandatory to prepare but it helps in

knowing the profit and loss at the end. This assists in decision making in the future (Bromwich

and Scapens, 2016). On the other hand, partnership firm’s capital accounts are maintained along

with a balance sheet to perceive the share of every partner in the firm as well as their drawings

10

the project A. So the company should adopt the project B (Filip, 2016).

TASK 4

4.1

The main types of financial statements are-

Balance Sheet- This statement discloses the financial position of any company on a particular

date. It includes - Assets- The things which are owned by the company are assets .It may be either tangible

or intangible like plants and machinery, equipments, patent and copyright. Liabilities-The thing which the company owes to the others are liabilities it may be either

creditors, bank loans etc (Goel, 2016). Equity- The things which remains in the business after the assets which are used to pay

off of its outstanding liabilities. In other words, difference between assets and liabilities is

called equity.

Income Statement- This shows the financial performance of the business in terms of profit or

loss over a specified period of time. It is also known as a profit and loss statement. Further it

includes the income and expenses which are earned and met by the company.

Cash flow statements- This statement reveals that what all types of activities resulted in the

inflow and outflow of cash. So that the firm is able to meet out its working capital expenses and

maintain the amount of liquidity (Crosby and Henneberry, 2016).

Statement of changes in equity- The amount of retained earnings can be revealed by this

statement only that what is left after the payment of all liabilities, interests and dividends. It also

derives the effects of change in any accounting policy or any corrections in the accounting error.

4.2

Different accounts are maintained by the different size of the firm. A sole trader

maintains only the Profit and loss statement, Balance Sheet and mainly Cash book to reveal the

performance of his firms. Though these statements are not mandatory to prepare but it helps in

knowing the profit and loss at the end. This assists in decision making in the future (Bromwich

and Scapens, 2016). On the other hand, partnership firm’s capital accounts are maintained along

with a balance sheet to perceive the share of every partner in the firm as well as their drawings

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

and additional capital introduced by them. Partnership Act 1932 applies in case of disputes and

conflicts in the firm of partners (Culkin, Murzacheva and Davis, 2016). The companies are

required to maintain all the financial statements and these statements are to be prepared by

following all the rules and acts applicable to the company. Formats are specified by the

Companies Act 2013 and rules of International Financial Reporting System and standards are to

be followed (Damodaran. 2016). In case, if these guidelines are not followed than the company is

required to specifically mention the reasons for not complying with that.

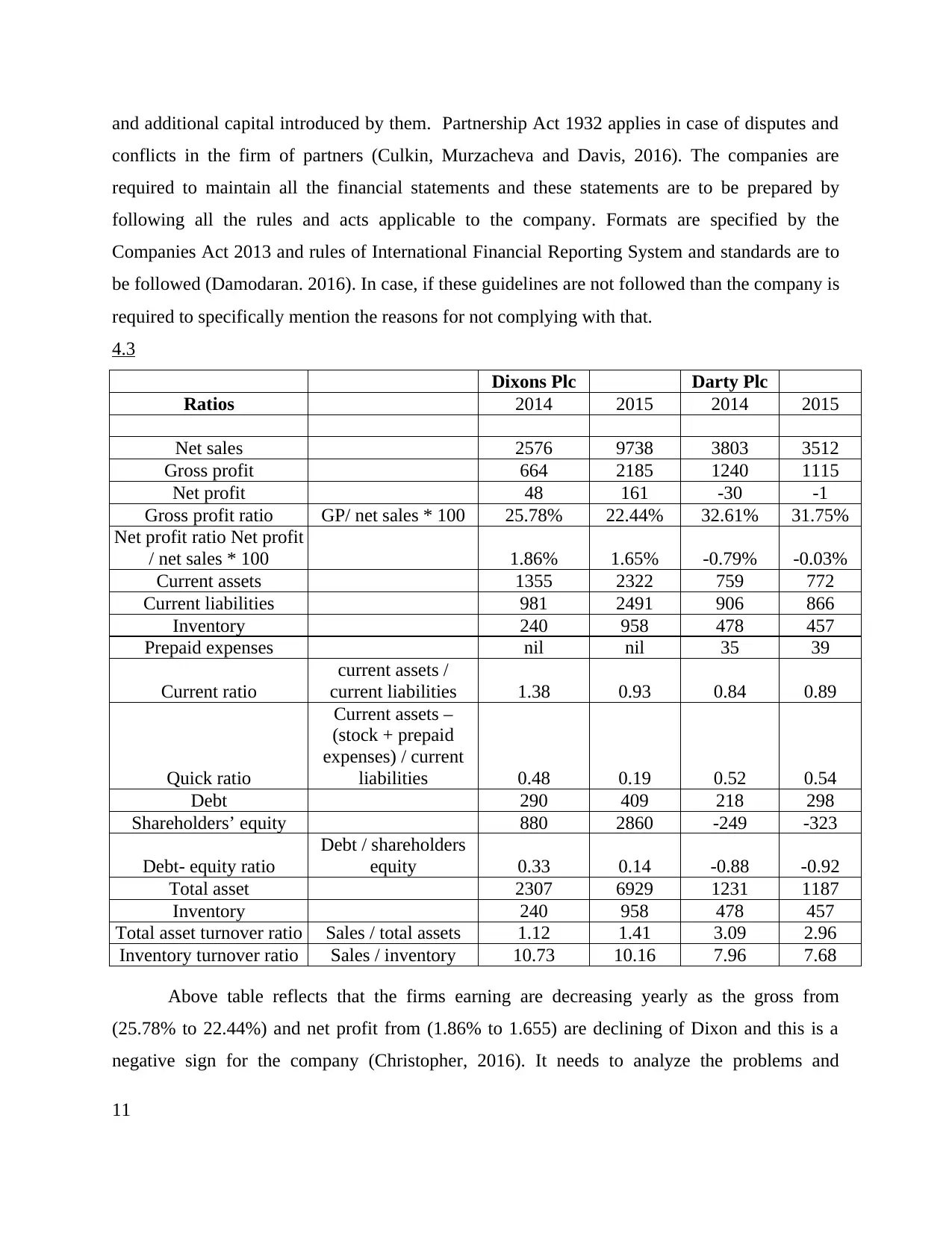

4.3

Dixons Plc Darty Plc

Ratios 2014 2015 2014 2015

Net sales 2576 9738 3803 3512

Gross profit 664 2185 1240 1115

Net profit 48 161 -30 -1

Gross profit ratio GP/ net sales * 100 25.78% 22.44% 32.61% 31.75%

Net profit ratio Net profit

/ net sales * 100 1.86% 1.65% -0.79% -0.03%

Current assets 1355 2322 759 772

Current liabilities 981 2491 906 866

Inventory 240 958 478 457

Prepaid expenses nil nil 35 39

Current ratio

current assets /

current liabilities 1.38 0.93 0.84 0.89

Quick ratio

Current assets –

(stock + prepaid

expenses) / current

liabilities 0.48 0.19 0.52 0.54

Debt 290 409 218 298

Shareholders’ equity 880 2860 -249 -323

Debt- equity ratio

Debt / shareholders

equity 0.33 0.14 -0.88 -0.92

Total asset 2307 6929 1231 1187

Inventory 240 958 478 457

Total asset turnover ratio Sales / total assets 1.12 1.41 3.09 2.96

Inventory turnover ratio Sales / inventory 10.73 10.16 7.96 7.68

Above table reflects that the firms earning are decreasing yearly as the gross from

(25.78% to 22.44%) and net profit from (1.86% to 1.655) are declining of Dixon and this is a

negative sign for the company (Christopher, 2016). It needs to analyze the problems and

11

conflicts in the firm of partners (Culkin, Murzacheva and Davis, 2016). The companies are

required to maintain all the financial statements and these statements are to be prepared by

following all the rules and acts applicable to the company. Formats are specified by the

Companies Act 2013 and rules of International Financial Reporting System and standards are to

be followed (Damodaran. 2016). In case, if these guidelines are not followed than the company is

required to specifically mention the reasons for not complying with that.

4.3

Dixons Plc Darty Plc

Ratios 2014 2015 2014 2015

Net sales 2576 9738 3803 3512

Gross profit 664 2185 1240 1115

Net profit 48 161 -30 -1

Gross profit ratio GP/ net sales * 100 25.78% 22.44% 32.61% 31.75%

Net profit ratio Net profit

/ net sales * 100 1.86% 1.65% -0.79% -0.03%

Current assets 1355 2322 759 772

Current liabilities 981 2491 906 866

Inventory 240 958 478 457

Prepaid expenses nil nil 35 39

Current ratio

current assets /

current liabilities 1.38 0.93 0.84 0.89

Quick ratio

Current assets –

(stock + prepaid

expenses) / current

liabilities 0.48 0.19 0.52 0.54

Debt 290 409 218 298

Shareholders’ equity 880 2860 -249 -323

Debt- equity ratio

Debt / shareholders

equity 0.33 0.14 -0.88 -0.92

Total asset 2307 6929 1231 1187

Inventory 240 958 478 457

Total asset turnover ratio Sales / total assets 1.12 1.41 3.09 2.96

Inventory turnover ratio Sales / inventory 10.73 10.16 7.96 7.68

Above table reflects that the firms earning are decreasing yearly as the gross from

(25.78% to 22.44%) and net profit from (1.86% to 1.655) are declining of Dixon and this is a

negative sign for the company (Christopher, 2016). It needs to analyze the problems and

11

implement the renewed plans and policies to maintain its position in the market. Dixon's current

assets are although increasing at high velocity but at the same time its current liabilities are

increasing more than its assets. It is an alarming situation for the Dixon otherwise soon it will be

dissolved. Comparing with Dixon and Darty the performance of Darty is better than that as its

profits (from 32.61% to 31.75%) and current assets (from 759 to 772) are decreasing but not at a

higher rate (Burger, 2016).

CONCLUSION

From the above report it is concluded that for the smooth functioning of any business at

its initial stage, proper planning is to be done This report includes availability of sources of

finance for expansion of operations by Trustlis ltd. Moreover, report identified that project B is

considered best because in this, there is a possibility of greater return in the future. Further,

financial performance analysis concluded that Darty Plc is performing much well as compare to

Dixons Carphone Plc.

12

assets are although increasing at high velocity but at the same time its current liabilities are

increasing more than its assets. It is an alarming situation for the Dixon otherwise soon it will be

dissolved. Comparing with Dixon and Darty the performance of Darty is better than that as its

profits (from 32.61% to 31.75%) and current assets (from 759 to 772) are decreasing but not at a

higher rate (Burger, 2016).

CONCLUSION

From the above report it is concluded that for the smooth functioning of any business at

its initial stage, proper planning is to be done This report includes availability of sources of

finance for expansion of operations by Trustlis ltd. Moreover, report identified that project B is

considered best because in this, there is a possibility of greater return in the future. Further,

financial performance analysis concluded that Darty Plc is performing much well as compare to

Dixons Carphone Plc.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.