Comprehensive Report: Financial Resources and Decision-Making Analysis

VerifiedAdded on 2020/02/17

|14

|3673

|31

Report

AI Summary

This report provides a comprehensive analysis of financial resource management and decision-making for a business. It begins by exploring various sources of finance, including bank loans, retained earnings, venture capital, equity, and debentures, along with their implications on the business. The report then delves into the importance of financial planning, including budgeting and the information needs of decision-makers. A detailed cash budget is prepared and interpreted, followed by the computation of unit costs. Project evaluation methods, such as payback period, average rate of return (ARR), and net present value (NPV), are applied to assess investment opportunities. Finally, the report examines financial statements, including format and ratio analysis to assess the financial performance of the business. The report concludes with a summary of the key findings and recommendations for effective financial management.

MANAGING FINANCIAL

RESOURCES AND DECISIONS

1

RESOURCES AND DECISIONS

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

1.1 Finance sources for business firms........................................................................................3

1.2 Implications of finance sources.............................................................................................4

1.3 Appropriate source of finance................................................................................................5

TASK 2 ...........................................................................................................................................5

2.1 Cost of source of finance.......................................................................................................5

2.2 Importance of financial planning for firms............................................................................5

2.3 Information needs of decision makers...................................................................................6

2.4 Impact of finance on the financial statements........................................................................6

TASK 3............................................................................................................................................7

3.1 Cash budget for Clariton........................................................................................................7

3.2 Computation of unit cost.......................................................................................................8

3.3 Project evaluation method .....................................................................................................9

TASK 4..........................................................................................................................................10

4.1 Financial statements.............................................................................................................10

4.2 Format of financial statements ............................................................................................11

4.3 Ratio analysis.......................................................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INDEX OF TABLES

Table 1 Preparation of cash budget..................................................................................................7

Table 2 Per unit cost calculation......................................................................................................8

Table 3: Calculation of payback period...........................................................................................9

Table 4: Calculation of ARR...........................................................................................................9

Table 5: Calculation of NPV..........................................................................................................10

Table 6: Ratio analysis...................................................................................................................11

2

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

1.1 Finance sources for business firms........................................................................................3

1.2 Implications of finance sources.............................................................................................4

1.3 Appropriate source of finance................................................................................................5

TASK 2 ...........................................................................................................................................5

2.1 Cost of source of finance.......................................................................................................5

2.2 Importance of financial planning for firms............................................................................5

2.3 Information needs of decision makers...................................................................................6

2.4 Impact of finance on the financial statements........................................................................6

TASK 3............................................................................................................................................7

3.1 Cash budget for Clariton........................................................................................................7

3.2 Computation of unit cost.......................................................................................................8

3.3 Project evaluation method .....................................................................................................9

TASK 4..........................................................................................................................................10

4.1 Financial statements.............................................................................................................10

4.2 Format of financial statements ............................................................................................11

4.3 Ratio analysis.......................................................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INDEX OF TABLES

Table 1 Preparation of cash budget..................................................................................................7

Table 2 Per unit cost calculation......................................................................................................8

Table 3: Calculation of payback period...........................................................................................9

Table 4: Calculation of ARR...........................................................................................................9

Table 5: Calculation of NPV..........................................................................................................10

Table 6: Ratio analysis...................................................................................................................11

2

INTRODUCTION

Finance is the one of the important factor that heavily influence business performance of

any firm. In the current report, varied finance sources and there implications on business are

discussed in detail. Along with this, budget is prepare and and interpretation about same is made.

Project evaluation methods are applied on cash flows and best one is selected for the firm. In end

section ratio analysis is done and comments are made on performance.

TASK 1

1.1 Finance sources for business firms

There are two sort of business firms namely unincorporated and incorporated business.

There is difference between both sort of business firms. Unincorporated business refers to the

sole trader and partnership business. Whereas, incorporated business refers to the company.

Sources of finance for both are given below.

Unincorporated business Bank loan: Bank loan is the source of finance which comes in debt category (Raheman

and et.al., 2010). In order to meet long and short term finance need bank loan is usually

taken by the business firms. Retained earning: It is a portion of sales value which remain as residual amount after

paying all expenses out of cash inflow amount.

Incorporated business Venture capital: It is a long term source of finance in which VC company buy shares of

any other firm and in return latter entity receive cash in its business. Thus, it is attractive

source of finance. Equity: Similar to VC equity is also long term source of finance. Firm need to obtain

prior approval from stock exchange in order to issue shares in the market (Wilmott,

2013).

Debenture: Debenture is similar to bank loan and only difference between both is that

in case of former one assets are not mortgaged but in latter case specific asset is

mortgaged. Interest is paid to creditor on debt amount.

3

Finance is the one of the important factor that heavily influence business performance of

any firm. In the current report, varied finance sources and there implications on business are

discussed in detail. Along with this, budget is prepare and and interpretation about same is made.

Project evaluation methods are applied on cash flows and best one is selected for the firm. In end

section ratio analysis is done and comments are made on performance.

TASK 1

1.1 Finance sources for business firms

There are two sort of business firms namely unincorporated and incorporated business.

There is difference between both sort of business firms. Unincorporated business refers to the

sole trader and partnership business. Whereas, incorporated business refers to the company.

Sources of finance for both are given below.

Unincorporated business Bank loan: Bank loan is the source of finance which comes in debt category (Raheman

and et.al., 2010). In order to meet long and short term finance need bank loan is usually

taken by the business firms. Retained earning: It is a portion of sales value which remain as residual amount after

paying all expenses out of cash inflow amount.

Incorporated business Venture capital: It is a long term source of finance in which VC company buy shares of

any other firm and in return latter entity receive cash in its business. Thus, it is attractive

source of finance. Equity: Similar to VC equity is also long term source of finance. Firm need to obtain

prior approval from stock exchange in order to issue shares in the market (Wilmott,

2013).

Debenture: Debenture is similar to bank loan and only difference between both is that

in case of former one assets are not mortgaged but in latter case specific asset is

mortgaged. Interest is paid to creditor on debt amount.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

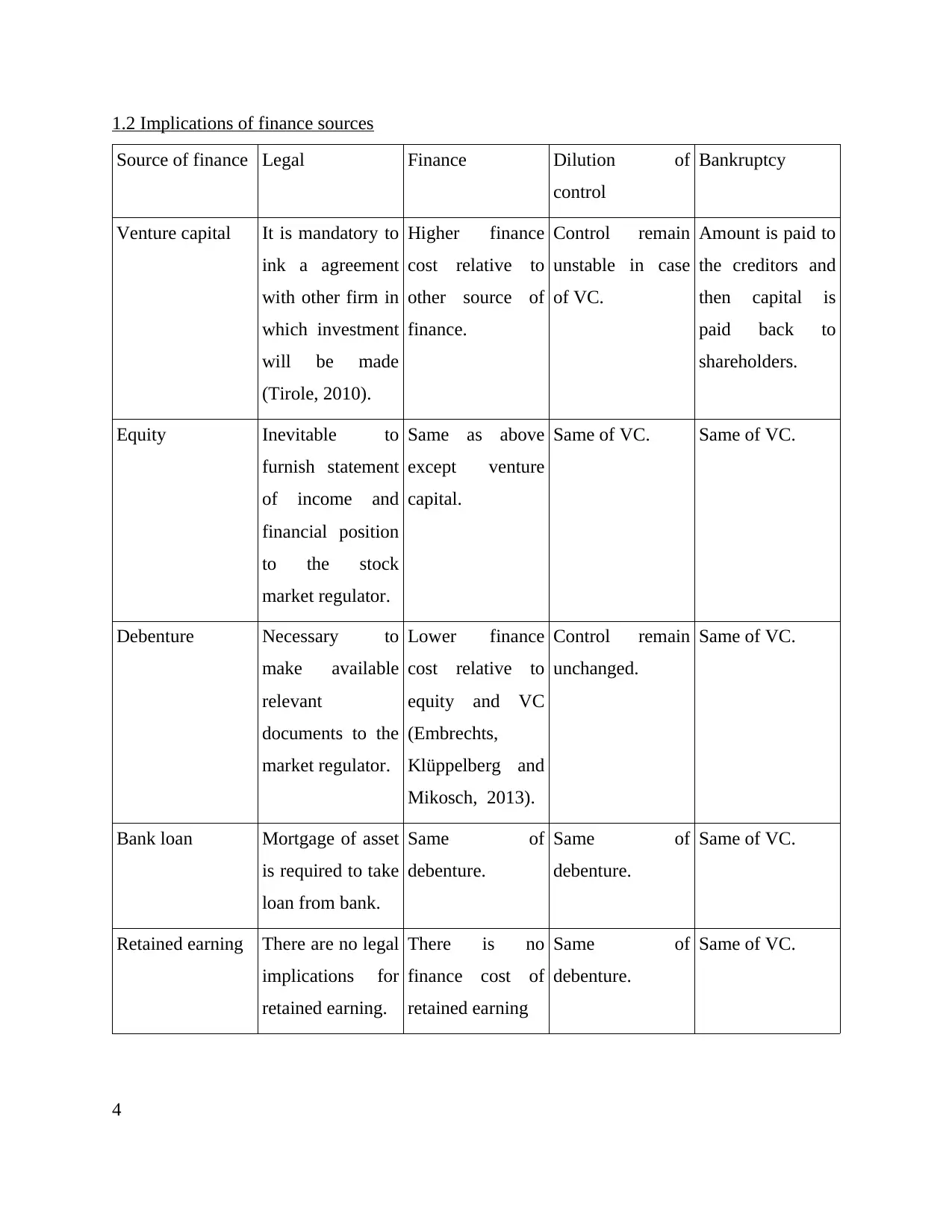

1.2 Implications of finance sources

Source of finance Legal Finance Dilution of

control

Bankruptcy

Venture capital It is mandatory to

ink a agreement

with other firm in

which investment

will be made

(Tirole, 2010).

Higher finance

cost relative to

other source of

finance.

Control remain

unstable in case

of VC.

Amount is paid to

the creditors and

then capital is

paid back to

shareholders.

Equity Inevitable to

furnish statement

of income and

financial position

to the stock

market regulator.

Same as above

except venture

capital.

Same of VC. Same of VC.

Debenture Necessary to

make available

relevant

documents to the

market regulator.

Lower finance

cost relative to

equity and VC

(Embrechts,

Klüppelberg and

Mikosch, 2013).

Control remain

unchanged.

Same of VC.

Bank loan Mortgage of asset

is required to take

loan from bank.

Same of

debenture.

Same of

debenture.

Same of VC.

Retained earning There are no legal

implications for

retained earning.

There is no

finance cost of

retained earning

Same of

debenture.

Same of VC.

4

Source of finance Legal Finance Dilution of

control

Bankruptcy

Venture capital It is mandatory to

ink a agreement

with other firm in

which investment

will be made

(Tirole, 2010).

Higher finance

cost relative to

other source of

finance.

Control remain

unstable in case

of VC.

Amount is paid to

the creditors and

then capital is

paid back to

shareholders.

Equity Inevitable to

furnish statement

of income and

financial position

to the stock

market regulator.

Same as above

except venture

capital.

Same of VC. Same of VC.

Debenture Necessary to

make available

relevant

documents to the

market regulator.

Lower finance

cost relative to

equity and VC

(Embrechts,

Klüppelberg and

Mikosch, 2013).

Control remain

unchanged.

Same of VC.

Bank loan Mortgage of asset

is required to take

loan from bank.

Same of

debenture.

Same of

debenture.

Same of VC.

Retained earning There are no legal

implications for

retained earning.

There is no

finance cost of

retained earning

Same of

debenture.

Same of VC.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1.3 Appropriate source of finance

Debt is the appropriate source of finance for the Clariton in comparison to other source of

finance. This is because small percentage of interest is charged on the bank loan amount by the

business firms. Moreover, Directors of Clariton will be able to make business decisions

independently and without any person interference. Thus, on this ground debt seems appropriate

source of finance for the business firm (Brigham and Ehrhardt, 2013). Venture capital and equity

both are not assumed for the relevant firm because there cost is so high and decision making

power of the Directors also get reduced. Hence, in order to prevent this situation debt is

considered appropriate one for the business firm. Retained earning is the best option that firm

currently having because there is no cost of retained earning. Hence, bank loan and retained

earning is considered best source of finance.

TASK 2

2.1 Cost of source of finance Dividend: In case of venture capital and equity dividend is paid to the investors for the

investment they make in the specific company. Thus, dividend is considered as cost of

finance of both venture capital and equity. In case of VC company have to pay seating

fee to the former entity. Due to this reason cost of equity and venture capital is

considered high. Interest: Banks and other creditors charged a interest on the debt amount that is payable

by the business firm. Bank loan may be taken at stable or non stable interest rate. In case

of non stable interest rate finance cost get changed regularly (Lo, Wong and Firth, 2010).

Tax:Tax is payable by the business firm in case it declared dividend to the shareholders.

Relaxation in tax payment is give only when funds were raised by the business firm

through bank loan or debenture.

2.2 Importance of financial planning for firms

Importance of financial planning is explained below. Budgeting: Budget is prepared by taken in to account entire financial plan. In the

financial plan allocation of cash is already done and same is followed to allot cash

amount to different expenditures in the budget. Thus, it can be said that financial

planning have significance for the firms.

5

Debt is the appropriate source of finance for the Clariton in comparison to other source of

finance. This is because small percentage of interest is charged on the bank loan amount by the

business firms. Moreover, Directors of Clariton will be able to make business decisions

independently and without any person interference. Thus, on this ground debt seems appropriate

source of finance for the business firm (Brigham and Ehrhardt, 2013). Venture capital and equity

both are not assumed for the relevant firm because there cost is so high and decision making

power of the Directors also get reduced. Hence, in order to prevent this situation debt is

considered appropriate one for the business firm. Retained earning is the best option that firm

currently having because there is no cost of retained earning. Hence, bank loan and retained

earning is considered best source of finance.

TASK 2

2.1 Cost of source of finance Dividend: In case of venture capital and equity dividend is paid to the investors for the

investment they make in the specific company. Thus, dividend is considered as cost of

finance of both venture capital and equity. In case of VC company have to pay seating

fee to the former entity. Due to this reason cost of equity and venture capital is

considered high. Interest: Banks and other creditors charged a interest on the debt amount that is payable

by the business firm. Bank loan may be taken at stable or non stable interest rate. In case

of non stable interest rate finance cost get changed regularly (Lo, Wong and Firth, 2010).

Tax:Tax is payable by the business firm in case it declared dividend to the shareholders.

Relaxation in tax payment is give only when funds were raised by the business firm

through bank loan or debenture.

2.2 Importance of financial planning for firms

Importance of financial planning is explained below. Budgeting: Budget is prepared by taken in to account entire financial plan. In the

financial plan allocation of cash is already done and same is followed to allot cash

amount to different expenditures in the budget. Thus, it can be said that financial

planning have significance for the firms.

5

Implication of failure to finance adequately: Most of the business firms have limited

amount of cash in their business and they failed to make best use of same. It is the

financial plan that help firms in making best use of cash in the business (Sarumathi and

Mohan, 2011). Thus, financial plan ensured that business firm will not financed

inadequately.

Over trading: Due to over trading of goods some times receivables increased at rapid

pace in the business. They get converted in to bad debts with passage of time period.

Financial plan ensure that less amount of debtors will be bad debt. This happened

because in financial plan amount of sales that will be done on credit basis is determined

earlier.

2.3 Information needs of decision makers

Information needs of varied decision makers is given below. Partners: Partners require an income statement and balance sheet of the other firm in

order to make acquisition related decisions. They are already aware about their business

performance and due to this reason does not need their firm financial statements. Apart

from this, partners also need business related information of company which they wants

to acquire in order to make business decisions. Venture capitalist:Venture capitalist needed financial statements of Clariton and other

business firm. This is because return of VC firm depends on the performance and

business conditions given and faced by the Clariton and other business firm. Thus, it can

be said that venture capital needed lots of information related to both firms.

Finance broker:Finance broker require an information related to the amount that of debt

that is already taken by the firm from the market (Krätke, 2010). On this basis they can

access current burden of finance cost on the firm and can identify whether they will

receive fee amount on time from Clariton.

2.4 Impact of finance on the financial statements

Finance have great impact on the firm financial statements. This is because if any

company issues shares in the market then in that case shareholder equity will increase. At same

time cash amount in the asset side of balance sheet will increase. In any case if dividend is paid

to the shareholders then in that situation profit amount will declined by some percentage. On

6

amount of cash in their business and they failed to make best use of same. It is the

financial plan that help firms in making best use of cash in the business (Sarumathi and

Mohan, 2011). Thus, financial plan ensured that business firm will not financed

inadequately.

Over trading: Due to over trading of goods some times receivables increased at rapid

pace in the business. They get converted in to bad debts with passage of time period.

Financial plan ensure that less amount of debtors will be bad debt. This happened

because in financial plan amount of sales that will be done on credit basis is determined

earlier.

2.3 Information needs of decision makers

Information needs of varied decision makers is given below. Partners: Partners require an income statement and balance sheet of the other firm in

order to make acquisition related decisions. They are already aware about their business

performance and due to this reason does not need their firm financial statements. Apart

from this, partners also need business related information of company which they wants

to acquire in order to make business decisions. Venture capitalist:Venture capitalist needed financial statements of Clariton and other

business firm. This is because return of VC firm depends on the performance and

business conditions given and faced by the Clariton and other business firm. Thus, it can

be said that venture capital needed lots of information related to both firms.

Finance broker:Finance broker require an information related to the amount that of debt

that is already taken by the firm from the market (Krätke, 2010). On this basis they can

access current burden of finance cost on the firm and can identify whether they will

receive fee amount on time from Clariton.

2.4 Impact of finance on the financial statements

Finance have great impact on the firm financial statements. This is because if any

company issues shares in the market then in that case shareholder equity will increase. At same

time cash amount in the asset side of balance sheet will increase. In any case if dividend is paid

to the shareholders then in that situation profit amount will declined by some percentage. On

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

other hand, if business operations are funded through bank loan then in that condition also bank

loan amount will be increased and in same time asset side of balance sheet will elevate (Chandra,

2011). Interest that is paid annually will be recorded in statement of income and by this value

profit will slightly reduced in the business. It can be said that different sources of finance heavily

affects financial statements of the business firm.

TASK 3

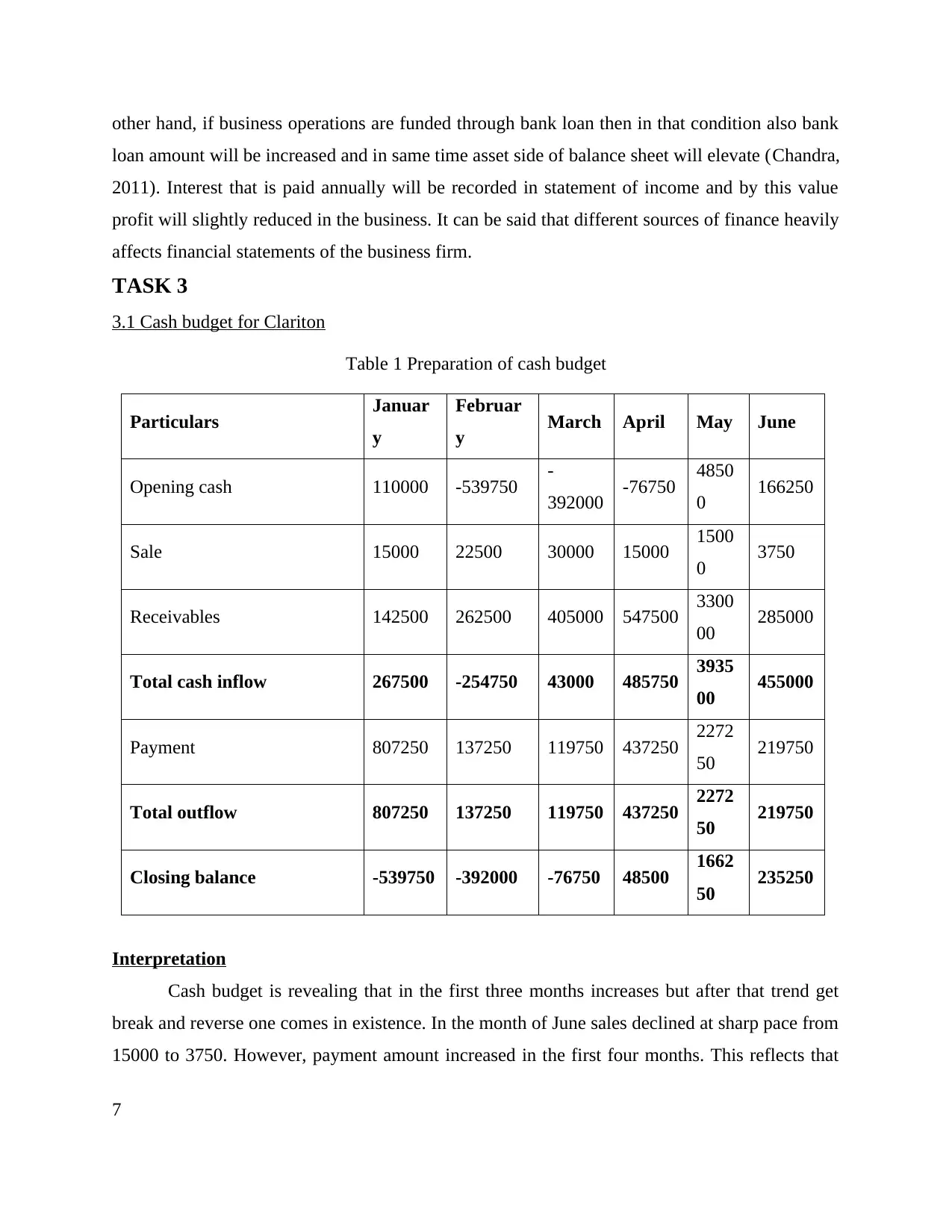

3.1 Cash budget for Clariton

Table 1 Preparation of cash budget

Particulars Januar

y

Februar

y March April May June

Opening cash 110000 -539750 -

392000 -76750 4850

0 166250

Sale 15000 22500 30000 15000 1500

0 3750

Receivables 142500 262500 405000 547500 3300

00 285000

Total cash inflow 267500 -254750 43000 485750 3935

00 455000

Payment 807250 137250 119750 437250 2272

50 219750

Total outflow 807250 137250 119750 437250 2272

50 219750

Closing balance -539750 -392000 -76750 48500 1662

50 235250

Interpretation

Cash budget is revealing that in the first three months increases but after that trend get

break and reverse one comes in existence. In the month of June sales declined at sharp pace from

15000 to 3750. However, payment amount increased in the first four months. This reflects that

7

loan amount will be increased and in same time asset side of balance sheet will elevate (Chandra,

2011). Interest that is paid annually will be recorded in statement of income and by this value

profit will slightly reduced in the business. It can be said that different sources of finance heavily

affects financial statements of the business firm.

TASK 3

3.1 Cash budget for Clariton

Table 1 Preparation of cash budget

Particulars Januar

y

Februar

y March April May June

Opening cash 110000 -539750 -

392000 -76750 4850

0 166250

Sale 15000 22500 30000 15000 1500

0 3750

Receivables 142500 262500 405000 547500 3300

00 285000

Total cash inflow 267500 -254750 43000 485750 3935

00 455000

Payment 807250 137250 119750 437250 2272

50 219750

Total outflow 807250 137250 119750 437250 2272

50 219750

Closing balance -539750 -392000 -76750 48500 1662

50 235250

Interpretation

Cash budget is revealing that in the first three months increases but after that trend get

break and reverse one comes in existence. In the month of June sales declined at sharp pace from

15000 to 3750. However, payment amount increased in the first four months. This reflects that

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

with increase in sales payments also increased. In the month of May and June decline comes in

the payment value. Hence, it can be said that with increase in sales payment increase or vice

verse. This reflects that budget is prepared in appropriate manner. Due to high amount of

payment relative to sales value closing balance is negative and it slowly become positive from

the month of April. Effective use of surplus cash must be made by the business firm and in this

regard it must allocate 60%,20% and 20% of cash surplus among operating activities, to meet

working capital needs and to make investment in shares. In this way best use of cash can be

done in the business.

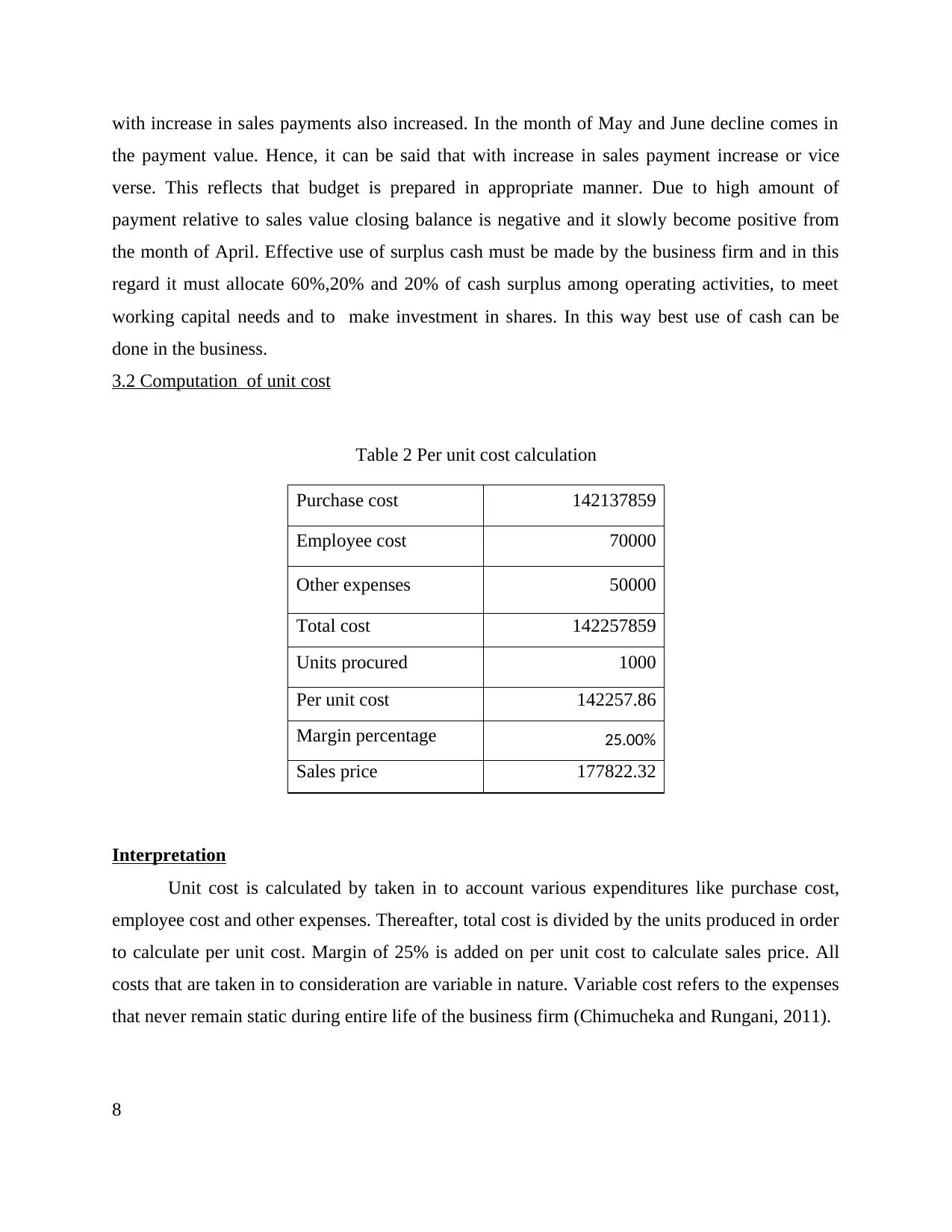

3.2 Computation of unit cost

Table 2 Per unit cost calculation

Purchase cost 142137859

Employee cost 70000

Other expenses 50000

Total cost 142257859

Units procured 1000

Per unit cost 142257.86

Margin percentage 25.00%

Sales price 177822.32

Interpretation

Unit cost is calculated by taken in to account various expenditures like purchase cost,

employee cost and other expenses. Thereafter, total cost is divided by the units produced in order

to calculate per unit cost. Margin of 25% is added on per unit cost to calculate sales price. All

costs that are taken in to consideration are variable in nature. Variable cost refers to the expenses

that never remain static during entire life of the business firm (Chimucheka and Rungani, 2011).

8

the payment value. Hence, it can be said that with increase in sales payment increase or vice

verse. This reflects that budget is prepared in appropriate manner. Due to high amount of

payment relative to sales value closing balance is negative and it slowly become positive from

the month of April. Effective use of surplus cash must be made by the business firm and in this

regard it must allocate 60%,20% and 20% of cash surplus among operating activities, to meet

working capital needs and to make investment in shares. In this way best use of cash can be

done in the business.

3.2 Computation of unit cost

Table 2 Per unit cost calculation

Purchase cost 142137859

Employee cost 70000

Other expenses 50000

Total cost 142257859

Units procured 1000

Per unit cost 142257.86

Margin percentage 25.00%

Sales price 177822.32

Interpretation

Unit cost is calculated by taken in to account various expenditures like purchase cost,

employee cost and other expenses. Thereafter, total cost is divided by the units produced in order

to calculate per unit cost. Margin of 25% is added on per unit cost to calculate sales price. All

costs that are taken in to consideration are variable in nature. Variable cost refers to the expenses

that never remain static during entire life of the business firm (Chimucheka and Rungani, 2011).

8

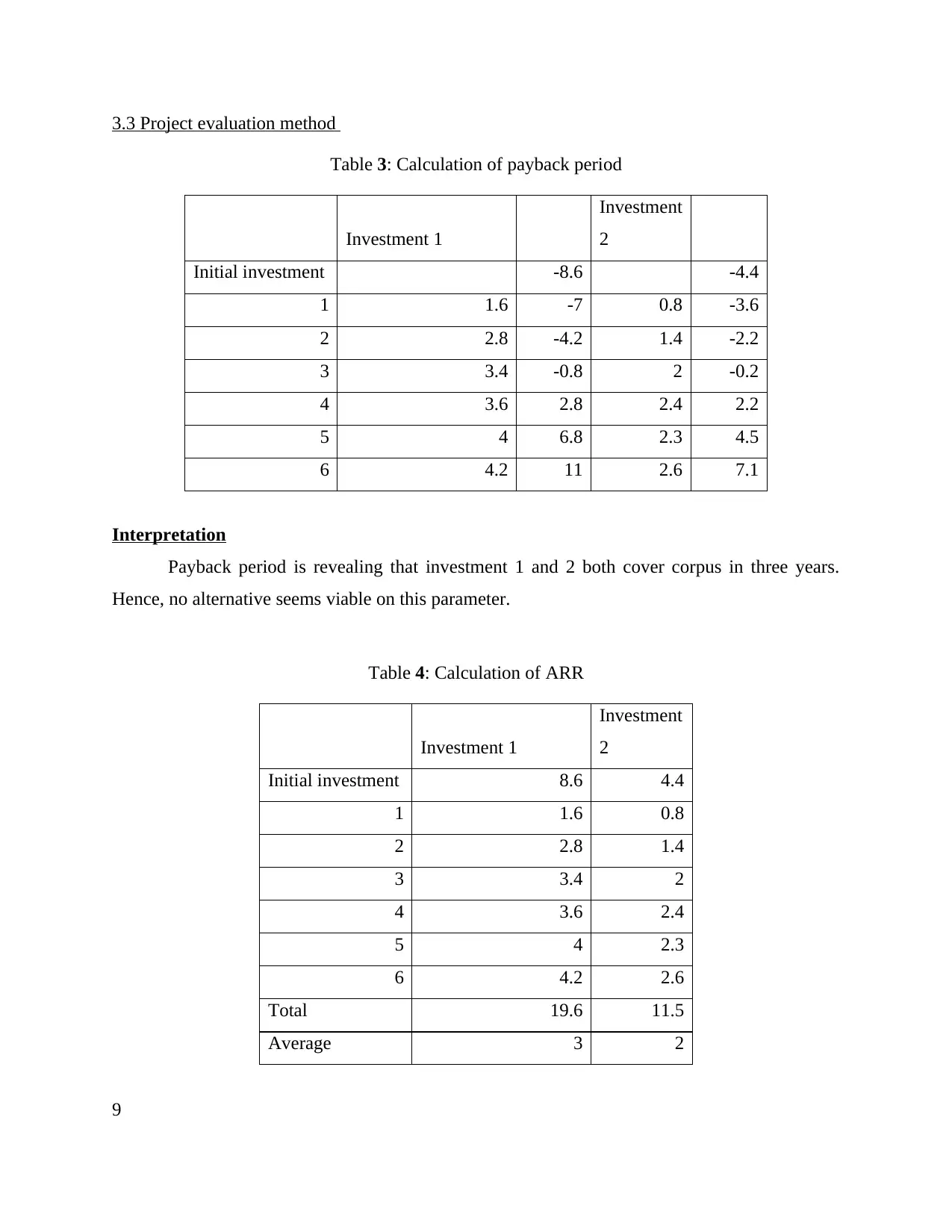

3.3 Project evaluation method

Table 3: Calculation of payback period

Investment 1

Investment

2

Initial investment -8.6 -4.4

1 1.6 -7 0.8 -3.6

2 2.8 -4.2 1.4 -2.2

3 3.4 -0.8 2 -0.2

4 3.6 2.8 2.4 2.2

5 4 6.8 2.3 4.5

6 4.2 11 2.6 7.1

Interpretation

Payback period is revealing that investment 1 and 2 both cover corpus in three years.

Hence, no alternative seems viable on this parameter.

Table 4: Calculation of ARR

Investment 1

Investment

2

Initial investment 8.6 4.4

1 1.6 0.8

2 2.8 1.4

3 3.4 2

4 3.6 2.4

5 4 2.3

6 4.2 2.6

Total 19.6 11.5

Average 3 2

9

Table 3: Calculation of payback period

Investment 1

Investment

2

Initial investment -8.6 -4.4

1 1.6 -7 0.8 -3.6

2 2.8 -4.2 1.4 -2.2

3 3.4 -0.8 2 -0.2

4 3.6 2.8 2.4 2.2

5 4 6.8 2.3 4.5

6 4.2 11 2.6 7.1

Interpretation

Payback period is revealing that investment 1 and 2 both cover corpus in three years.

Hence, no alternative seems viable on this parameter.

Table 4: Calculation of ARR

Investment 1

Investment

2

Initial investment 8.6 4.4

1 1.6 0.8

2 2.8 1.4

3 3.4 2

4 3.6 2.4

5 4 2.3

6 4.2 2.6

Total 19.6 11.5

Average 3 2

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

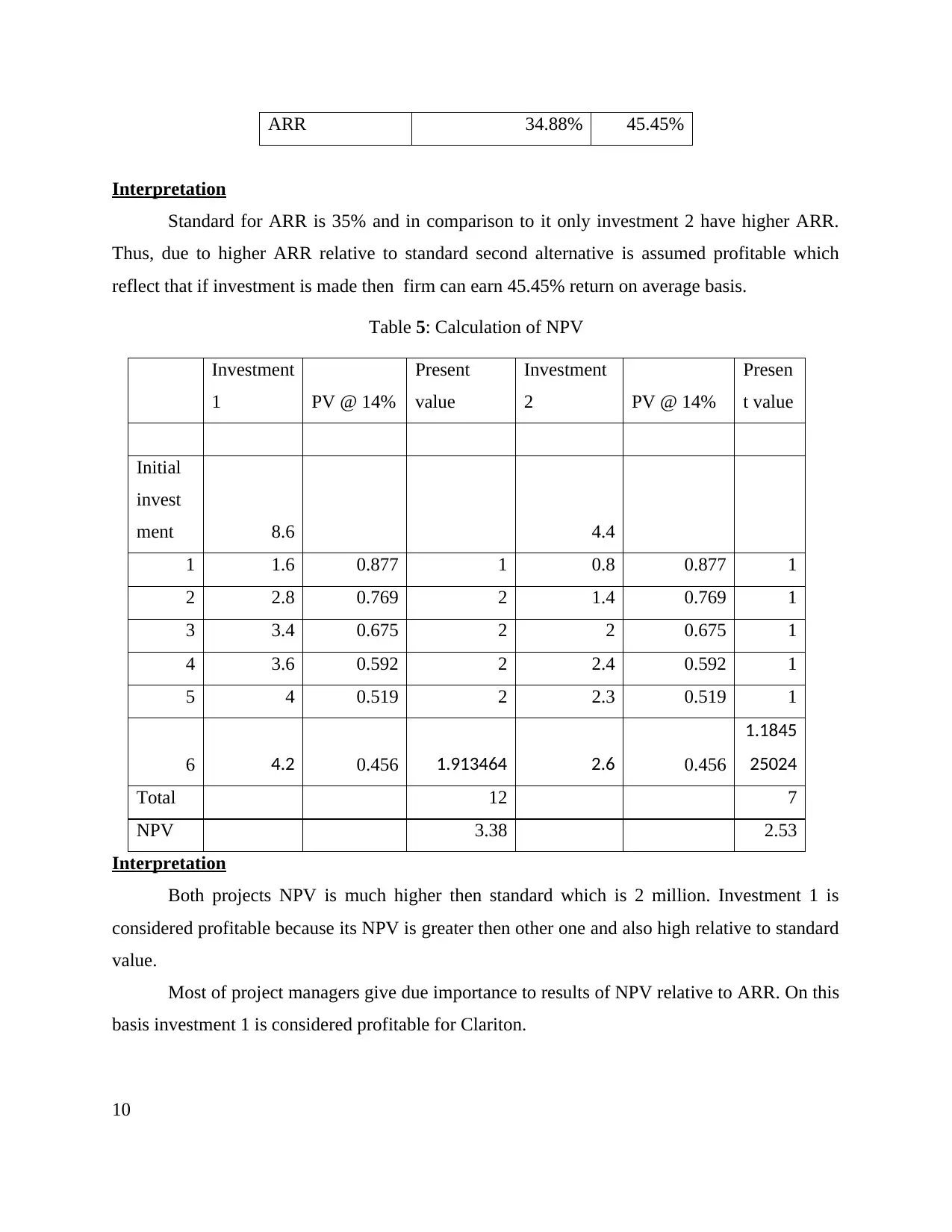

ARR 34.88% 45.45%

Interpretation

Standard for ARR is 35% and in comparison to it only investment 2 have higher ARR.

Thus, due to higher ARR relative to standard second alternative is assumed profitable which

reflect that if investment is made then firm can earn 45.45% return on average basis.

Table 5: Calculation of NPV

Investment

1 PV @ 14%

Present

value

Investment

2 PV @ 14%

Presen

t value

Initial

invest

ment 8.6 4.4

1 1.6 0.877 1 0.8 0.877 1

2 2.8 0.769 2 1.4 0.769 1

3 3.4 0.675 2 2 0.675 1

4 3.6 0.592 2 2.4 0.592 1

5 4 0.519 2 2.3 0.519 1

6 4.2 0.456 1.913464 2.6 0.456

1.1845

25024

Total 12 7

NPV 3.38 2.53

Interpretation

Both projects NPV is much higher then standard which is 2 million. Investment 1 is

considered profitable because its NPV is greater then other one and also high relative to standard

value.

Most of project managers give due importance to results of NPV relative to ARR. On this

basis investment 1 is considered profitable for Clariton.

10

Interpretation

Standard for ARR is 35% and in comparison to it only investment 2 have higher ARR.

Thus, due to higher ARR relative to standard second alternative is assumed profitable which

reflect that if investment is made then firm can earn 45.45% return on average basis.

Table 5: Calculation of NPV

Investment

1 PV @ 14%

Present

value

Investment

2 PV @ 14%

Presen

t value

Initial

invest

ment 8.6 4.4

1 1.6 0.877 1 0.8 0.877 1

2 2.8 0.769 2 1.4 0.769 1

3 3.4 0.675 2 2 0.675 1

4 3.6 0.592 2 2.4 0.592 1

5 4 0.519 2 2.3 0.519 1

6 4.2 0.456 1.913464 2.6 0.456

1.1845

25024

Total 12 7

NPV 3.38 2.53

Interpretation

Both projects NPV is much higher then standard which is 2 million. Investment 1 is

considered profitable because its NPV is greater then other one and also high relative to standard

value.

Most of project managers give due importance to results of NPV relative to ARR. On this

basis investment 1 is considered profitable for Clariton.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 4

4.1 Financial statements Statement of income: This statement indicate the revenue gained and expenditure made

by the firm in its business during a year (Fracassi, 2016). Cost control strategy is

prepared on the basis of input provided by income statement. Statement of financial position: This statement indicate the assets and liability value at

end of year. Varied areas where attention needed is identified by using this statement. Statement of cash flows: This statement is prepared to find out sources from which cash

inflow happen and places where same invested resultant amount of cash and equivalent

inn business (Fayol, 2016). This statement help one in preparing strong cash management

strategy. Statement of equity:: It reveal the overall change that happened in the value of equity

during a year. This statement is prepared by every company in its business.

Notes on financial statements: It indicate the values that are taken in to consideration to

calculate final value of specific element of income statement and balance sheet.

4.2 Format of financial statements

There is huge difference in the financial statements of the sole traders, partners and

company. As per rules every company have to follow IFRS and GAAP in order to prepare its

financial statements. Whereas, in case of sole trader and partnership same rules does not applied.

In partnership assets, liability, profit and loss are shared among partners but in case of company

same thing does not happened (Ireland, Paul and Dujardin, 2011). Thus, it can be said there is a

difference in the financial statements of the company, sole trader and company. In case of

company each and every item is put in the specific category all things are presented in detail but

in case of sole trader and partners same does not happened. These are the basic difference

between the format of financial statement of business firms.

4.3 Ratio analysis

Table 6: Ratio analysis

2016 2015

Gross profit 178 175

11

4.1 Financial statements Statement of income: This statement indicate the revenue gained and expenditure made

by the firm in its business during a year (Fracassi, 2016). Cost control strategy is

prepared on the basis of input provided by income statement. Statement of financial position: This statement indicate the assets and liability value at

end of year. Varied areas where attention needed is identified by using this statement. Statement of cash flows: This statement is prepared to find out sources from which cash

inflow happen and places where same invested resultant amount of cash and equivalent

inn business (Fayol, 2016). This statement help one in preparing strong cash management

strategy. Statement of equity:: It reveal the overall change that happened in the value of equity

during a year. This statement is prepared by every company in its business.

Notes on financial statements: It indicate the values that are taken in to consideration to

calculate final value of specific element of income statement and balance sheet.

4.2 Format of financial statements

There is huge difference in the financial statements of the sole traders, partners and

company. As per rules every company have to follow IFRS and GAAP in order to prepare its

financial statements. Whereas, in case of sole trader and partnership same rules does not applied.

In partnership assets, liability, profit and loss are shared among partners but in case of company

same thing does not happened (Ireland, Paul and Dujardin, 2011). Thus, it can be said there is a

difference in the financial statements of the company, sole trader and company. In case of

company each and every item is put in the specific category all things are presented in detail but

in case of sole trader and partners same does not happened. These are the basic difference

between the format of financial statement of business firms.

4.3 Ratio analysis

Table 6: Ratio analysis

2016 2015

Gross profit 178 175

11

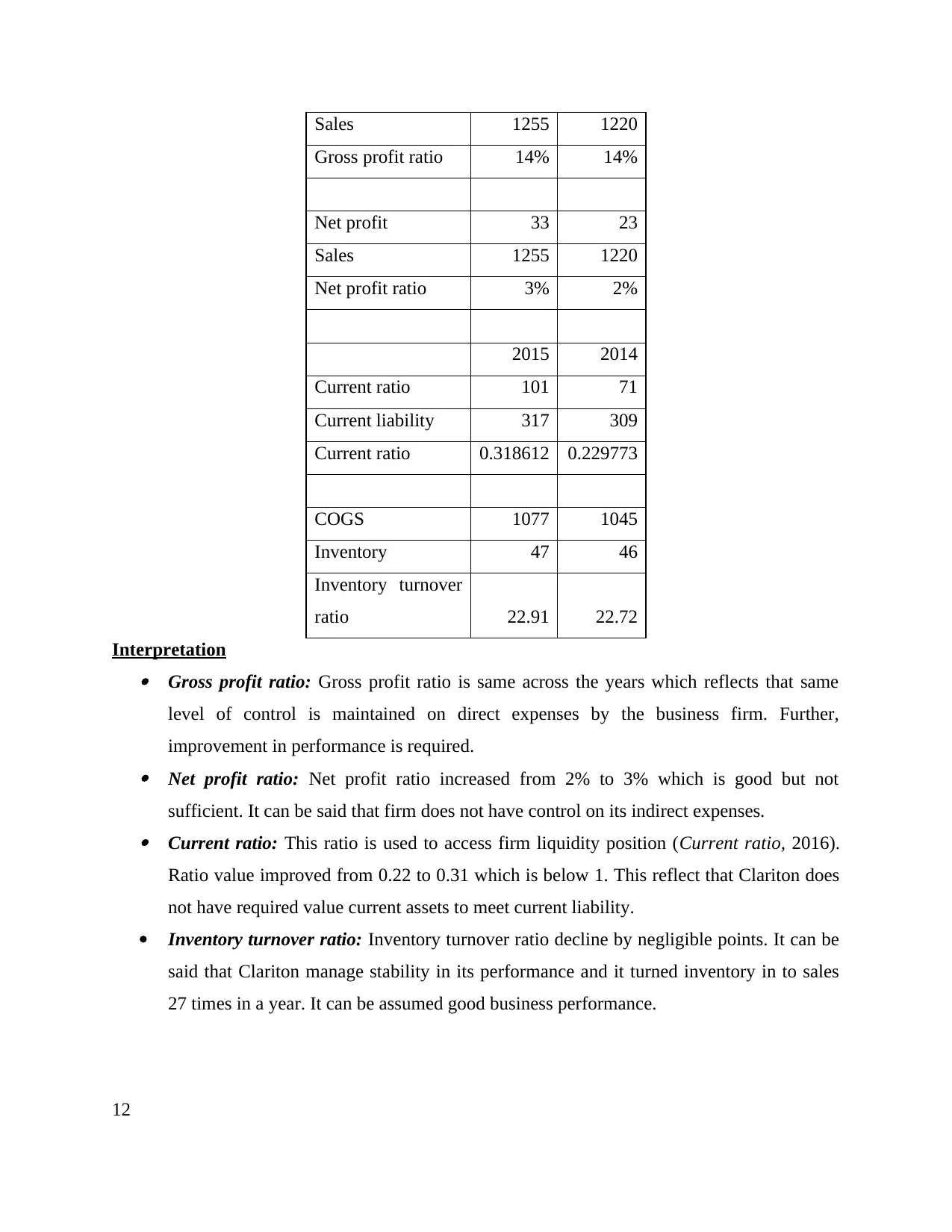

Sales 1255 1220

Gross profit ratio 14% 14%

Net profit 33 23

Sales 1255 1220

Net profit ratio 3% 2%

2015 2014

Current ratio 101 71

Current liability 317 309

Current ratio 0.318612 0.229773

COGS 1077 1045

Inventory 47 46

Inventory turnover

ratio 22.91 22.72

Interpretation Gross profit ratio: Gross profit ratio is same across the years which reflects that same

level of control is maintained on direct expenses by the business firm. Further,

improvement in performance is required. Net profit ratio: Net profit ratio increased from 2% to 3% which is good but not

sufficient. It can be said that firm does not have control on its indirect expenses. Current ratio: This ratio is used to access firm liquidity position (Current ratio, 2016).

Ratio value improved from 0.22 to 0.31 which is below 1. This reflect that Clariton does

not have required value current assets to meet current liability.

Inventory turnover ratio: Inventory turnover ratio decline by negligible points. It can be

said that Clariton manage stability in its performance and it turned inventory in to sales

27 times in a year. It can be assumed good business performance.

12

Gross profit ratio 14% 14%

Net profit 33 23

Sales 1255 1220

Net profit ratio 3% 2%

2015 2014

Current ratio 101 71

Current liability 317 309

Current ratio 0.318612 0.229773

COGS 1077 1045

Inventory 47 46

Inventory turnover

ratio 22.91 22.72

Interpretation Gross profit ratio: Gross profit ratio is same across the years which reflects that same

level of control is maintained on direct expenses by the business firm. Further,

improvement in performance is required. Net profit ratio: Net profit ratio increased from 2% to 3% which is good but not

sufficient. It can be said that firm does not have control on its indirect expenses. Current ratio: This ratio is used to access firm liquidity position (Current ratio, 2016).

Ratio value improved from 0.22 to 0.31 which is below 1. This reflect that Clariton does

not have required value current assets to meet current liability.

Inventory turnover ratio: Inventory turnover ratio decline by negligible points. It can be

said that Clariton manage stability in its performance and it turned inventory in to sales

27 times in a year. It can be assumed good business performance.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.