Financial Management Report: Samsung Electronics Co Ltd

VerifiedAdded on 2019/12/03

|19

|4967

|2518

Report

AI Summary

This report provides a comprehensive analysis of financial resource management and decision-making, focusing on Samsung Electronics Co Ltd. It begins by evaluating various sources of finance, including issuing shares, bank borrowings, and retained earnings, along with their implications and associated costs. The report emphasizes the significance of financial planning, detailing the information required by different stakeholders such as management, creditors, government, and employees. It further examines the impact of finance on financial statements like the income statement, cash flow statement, and balance sheet. The report then delves into budgeting, including cash, sales, and production budgets, and assesses the viability of investment projects using techniques like Net Present Value (NPV), Payback Period, Average Rate of Return (ARR), and Internal Rate of Return (IRR). Finally, it concludes with a discussion on the purpose and formats of financial statements, along with a detailed ratio analysis of Samsung Electronics Co Ltd, offering insights into its financial position and performance.

MANAGING FINANCIAL RESOURCES

AND DECISIONS

1

AND DECISIONS

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction................................................................................................................................................3

Managing Finance Part 1...........................................................................................................................3

1.1 Evaluate different sources of finance.........................................................................................3

1.2 Implications of identified sources...............................................................................................4

1.3 Appropriate source of finance.....................................................................................................6

2.1 Assess the costs associated with different sources of finance....................................................6

2.2 Significance of financial planning..............................................................................................6

2.3 Information required by different users......................................................................................7

2.4 Impact of finance on financial statements..................................................................................8

MANAGING FINANCE TASK 2.............................................................................................................9

3.1 Cash, Sales and Production budgets...........................................................................................9

3.2 Calculation of Unit Costing......................................................................................................10

3.3 Assessing the viability of investment project...........................................................................11

4.1 Purpose of financial statements................................................................................................16

4.2 Formats of different business entities.......................................................................................17

4.3 Ratio Analysis...........................................................................................................................17

CONCLUSION........................................................................................................................................18

REFERENCES.........................................................................................................................................19

2

Introduction................................................................................................................................................3

Managing Finance Part 1...........................................................................................................................3

1.1 Evaluate different sources of finance.........................................................................................3

1.2 Implications of identified sources...............................................................................................4

1.3 Appropriate source of finance.....................................................................................................6

2.1 Assess the costs associated with different sources of finance....................................................6

2.2 Significance of financial planning..............................................................................................6

2.3 Information required by different users......................................................................................7

2.4 Impact of finance on financial statements..................................................................................8

MANAGING FINANCE TASK 2.............................................................................................................9

3.1 Cash, Sales and Production budgets...........................................................................................9

3.2 Calculation of Unit Costing......................................................................................................10

3.3 Assessing the viability of investment project...........................................................................11

4.1 Purpose of financial statements................................................................................................16

4.2 Formats of different business entities.......................................................................................17

4.3 Ratio Analysis...........................................................................................................................17

CONCLUSION........................................................................................................................................18

REFERENCES.........................................................................................................................................19

2

Index of Tables

Table 1: Implications of Sources................................................................................................................6

Table 2: Cash Budget...............................................................................................................................10

Table 3: Production Budget......................................................................................................................10

Table 4: Sales Budget...............................................................................................................................11

Table 5: Calculation of unit price.............................................................................................................11

Table 6: NPV of Project A........................................................................................................................12

Table 7: NPV of Project B........................................................................................................................13

Table 8: NPV of Project C........................................................................................................................13

Table 9: Payback period of Project A.......................................................................................................14

Table 10: Payback period of Project B.....................................................................................................14

Table 11: Payback period of Project C.....................................................................................................14

Table 12: ARR of Project A.....................................................................................................................15

Table 13: ARR of Project B.....................................................................................................................15

Table 14: ARR of Project C.....................................................................................................................16

Table 15: IRR of Project A.......................................................................................................................16

Table 16: IRR of Project B ......................................................................................................................16

Table 17: IRR of Project C.......................................................................................................................17

Table 18: Ratio Analysis of Samsung Electronics Co Ltd.......................................................................18

3

Table 1: Implications of Sources................................................................................................................6

Table 2: Cash Budget...............................................................................................................................10

Table 3: Production Budget......................................................................................................................10

Table 4: Sales Budget...............................................................................................................................11

Table 5: Calculation of unit price.............................................................................................................11

Table 6: NPV of Project A........................................................................................................................12

Table 7: NPV of Project B........................................................................................................................13

Table 8: NPV of Project C........................................................................................................................13

Table 9: Payback period of Project A.......................................................................................................14

Table 10: Payback period of Project B.....................................................................................................14

Table 11: Payback period of Project C.....................................................................................................14

Table 12: ARR of Project A.....................................................................................................................15

Table 13: ARR of Project B.....................................................................................................................15

Table 14: ARR of Project C.....................................................................................................................16

Table 15: IRR of Project A.......................................................................................................................16

Table 16: IRR of Project B ......................................................................................................................16

Table 17: IRR of Project C.......................................................................................................................17

Table 18: Ratio Analysis of Samsung Electronics Co Ltd.......................................................................18

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Looking at the present competitiveness of corporate world it has been identified that, managing

available resources in an appropriate manner to generate desired results and outcomes. In particular,

financial resources play vital role in executing business activities irrespective to the sector. However,

these days industry experts rate the success of enterprise on the basis of utilization of financial

resources (Burns, Hopper and Yazdifar, 2004). There are several aspects which management has to

consider in the process financial planning such as requirement of funds, economic position, and

appropriateness of available resources of funds. In the present report, financial management of

Samsung Electronics Co Ltd has been focused upon and the source required by the company to expand

its business for the future contingency. Thereafter, researcher illustrates the major financial statements

and its users for making decisions. Through the help of different appraisal techniques, feasibility of

future investment has been evaluated. Lastly, ratio analysis helps in highlighting the actual economic

position of Samsung Electronics Co Ltd in comparison to past performances and industry standards.

MANAGING FINANCE PART 1

1.1 Evaluate different sources of finance

There are different sources of funds available to the management of Samsung Electronics Co

Ltd through the help of which they can raise funds for the expansion of business activities are as

follows: Issue of shares: Listed on Korea exchange (KRX) and London stock exchange (LSE), Samsung

Electronics Co Ltd can issue shares and raise adequate amount of funds from the market (Sutter,

2006). The main purpose of issuing shares is that, company can involve several investors and

through these huge funds can be raised and in the form of return, management only has to pay

dividends whenever firm generates profits. Bank Borrowings: It is also considered as the most common source of fund through the means

of which Samsung Electronics Co Ltd can raise funds. However, it is defined as the debt

financing in which liability of firm increases. Firm carrying higher reputation in the market

avail wide range of financial institution from which funds can be generated at affordable

interest rates. The main advantage of this source is that, with the brand name of Samsung

Electronics Co Ltd and few legal formalities large amount can be raised quickly.

Retained earnings: Operating at such a large level it is important for Samsung Electronics Co

Ltd to maintain the level of retained earnings so that, management can use at the time of future

4

Looking at the present competitiveness of corporate world it has been identified that, managing

available resources in an appropriate manner to generate desired results and outcomes. In particular,

financial resources play vital role in executing business activities irrespective to the sector. However,

these days industry experts rate the success of enterprise on the basis of utilization of financial

resources (Burns, Hopper and Yazdifar, 2004). There are several aspects which management has to

consider in the process financial planning such as requirement of funds, economic position, and

appropriateness of available resources of funds. In the present report, financial management of

Samsung Electronics Co Ltd has been focused upon and the source required by the company to expand

its business for the future contingency. Thereafter, researcher illustrates the major financial statements

and its users for making decisions. Through the help of different appraisal techniques, feasibility of

future investment has been evaluated. Lastly, ratio analysis helps in highlighting the actual economic

position of Samsung Electronics Co Ltd in comparison to past performances and industry standards.

MANAGING FINANCE PART 1

1.1 Evaluate different sources of finance

There are different sources of funds available to the management of Samsung Electronics Co

Ltd through the help of which they can raise funds for the expansion of business activities are as

follows: Issue of shares: Listed on Korea exchange (KRX) and London stock exchange (LSE), Samsung

Electronics Co Ltd can issue shares and raise adequate amount of funds from the market (Sutter,

2006). The main purpose of issuing shares is that, company can involve several investors and

through these huge funds can be raised and in the form of return, management only has to pay

dividends whenever firm generates profits. Bank Borrowings: It is also considered as the most common source of fund through the means

of which Samsung Electronics Co Ltd can raise funds. However, it is defined as the debt

financing in which liability of firm increases. Firm carrying higher reputation in the market

avail wide range of financial institution from which funds can be generated at affordable

interest rates. The main advantage of this source is that, with the brand name of Samsung

Electronics Co Ltd and few legal formalities large amount can be raised quickly.

Retained earnings: Operating at such a large level it is important for Samsung Electronics Co

Ltd to maintain the level of retained earnings so that, management can use at the time of future

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

expansion and growth (Armitage, Marschke and Plummer, 2008). It is suitable source in the

context to the cited company as it will not raise the liability for the firm.

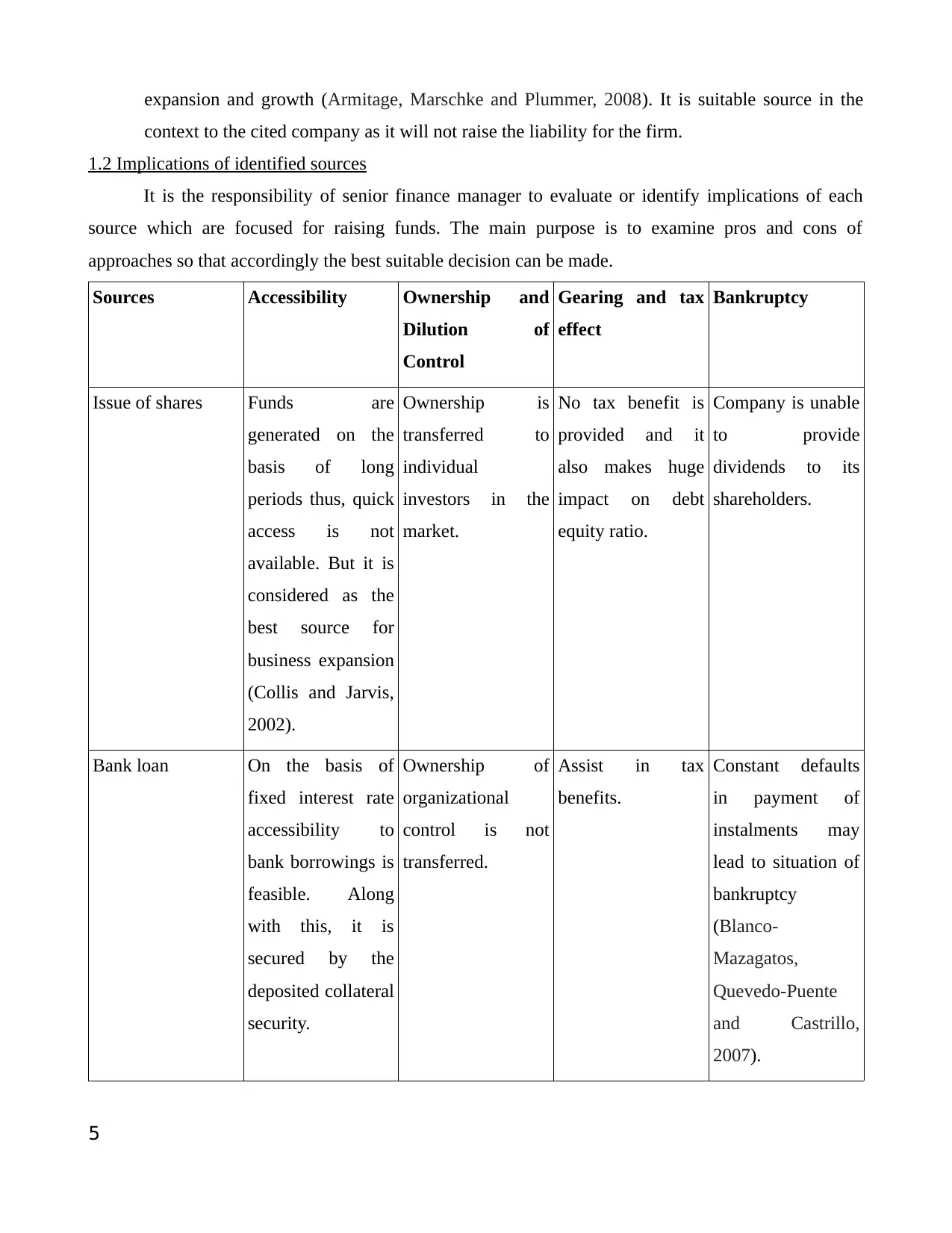

1.2 Implications of identified sources

It is the responsibility of senior finance manager to evaluate or identify implications of each

source which are focused for raising funds. The main purpose is to examine pros and cons of

approaches so that accordingly the best suitable decision can be made.

Sources Accessibility Ownership and

Dilution of

Control

Gearing and tax

effect

Bankruptcy

Issue of shares Funds are

generated on the

basis of long

periods thus, quick

access is not

available. But it is

considered as the

best source for

business expansion

(Collis and Jarvis,

2002).

Ownership is

transferred to

individual

investors in the

market.

No tax benefit is

provided and it

also makes huge

impact on debt

equity ratio.

Company is unable

to provide

dividends to its

shareholders.

Bank loan On the basis of

fixed interest rate

accessibility to

bank borrowings is

feasible. Along

with this, it is

secured by the

deposited collateral

security.

Ownership of

organizational

control is not

transferred.

Assist in tax

benefits.

Constant defaults

in payment of

instalments may

lead to situation of

bankruptcy

(Blanco‐

Mazagatos,

Quevedo‐Puente

and Castrillo,

2007).

5

context to the cited company as it will not raise the liability for the firm.

1.2 Implications of identified sources

It is the responsibility of senior finance manager to evaluate or identify implications of each

source which are focused for raising funds. The main purpose is to examine pros and cons of

approaches so that accordingly the best suitable decision can be made.

Sources Accessibility Ownership and

Dilution of

Control

Gearing and tax

effect

Bankruptcy

Issue of shares Funds are

generated on the

basis of long

periods thus, quick

access is not

available. But it is

considered as the

best source for

business expansion

(Collis and Jarvis,

2002).

Ownership is

transferred to

individual

investors in the

market.

No tax benefit is

provided and it

also makes huge

impact on debt

equity ratio.

Company is unable

to provide

dividends to its

shareholders.

Bank loan On the basis of

fixed interest rate

accessibility to

bank borrowings is

feasible. Along

with this, it is

secured by the

deposited collateral

security.

Ownership of

organizational

control is not

transferred.

Assist in tax

benefits.

Constant defaults

in payment of

instalments may

lead to situation of

bankruptcy

(Blanco‐

Mazagatos,

Quevedo‐Puente

and Castrillo,

2007).

5

Retained earnings It is easy to access

as funds are

already kept

reserved for the

future contingency

(EUGENE, 2014).

No ownership is

transferred.

No tax effect on

this source.

Will be considered

as the loss for the

firm.

Table 1: Implications of Sources

1.3 Appropriate source of finance

On the basis of above study on different sources of funds and their implications for Samsung

Electronics Co Ltd it can be recommended to the management that they should go for issuing shares as

well as bank loan for raising large amount and executing the activities of the company. It is already

established in several markets of the world so it will not be difficult for the Samsung Electronics Co

Ltd to expand its business and offer wide range of quality of electronic products to its target audience.

However, issue of share and bank borrowings will assist in maintaining the balance of debt/equity ratio

for the firm which is significant aspect in such competitive environment.

2.1 Assess the costs associated with different sources of finance

In general, with each above stated sources of funds different costs are associated. However, it is

the duty of finance managers to examine costs keeping in mind short and long term financial needs.

Following are the costs of different sources: Issue of shares: There are several costs associated with this source that can have major impact

on the overall functioning of business such as: payment of dividend to shareholders, stock

market charges, underwriter's commission and other legal registration charges (James, Leavel

and Mainam, 2002). These are the costs that Samsung Electronics Co Ltd has to incur while

issuing shares. Bank loan: This source of fund increases liability of business in the form of paying fixed

interest payment on monthly basis, documentation charges, legal charges and annual payment

of principle amount.

Retained earnings: This main cost associated with this source decreases overall financial

capability of business. Further it is the part of profit thus, net profit ratio of Samsung

6

as funds are

already kept

reserved for the

future contingency

(EUGENE, 2014).

No ownership is

transferred.

No tax effect on

this source.

Will be considered

as the loss for the

firm.

Table 1: Implications of Sources

1.3 Appropriate source of finance

On the basis of above study on different sources of funds and their implications for Samsung

Electronics Co Ltd it can be recommended to the management that they should go for issuing shares as

well as bank loan for raising large amount and executing the activities of the company. It is already

established in several markets of the world so it will not be difficult for the Samsung Electronics Co

Ltd to expand its business and offer wide range of quality of electronic products to its target audience.

However, issue of share and bank borrowings will assist in maintaining the balance of debt/equity ratio

for the firm which is significant aspect in such competitive environment.

2.1 Assess the costs associated with different sources of finance

In general, with each above stated sources of funds different costs are associated. However, it is

the duty of finance managers to examine costs keeping in mind short and long term financial needs.

Following are the costs of different sources: Issue of shares: There are several costs associated with this source that can have major impact

on the overall functioning of business such as: payment of dividend to shareholders, stock

market charges, underwriter's commission and other legal registration charges (James, Leavel

and Mainam, 2002). These are the costs that Samsung Electronics Co Ltd has to incur while

issuing shares. Bank loan: This source of fund increases liability of business in the form of paying fixed

interest payment on monthly basis, documentation charges, legal charges and annual payment

of principle amount.

Retained earnings: This main cost associated with this source decreases overall financial

capability of business. Further it is the part of profit thus, net profit ratio of Samsung

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Electronics Co Ltd declines to great margin.

2.2 Significance of financial planning

To,

The Managing Director of Samsung Electronics Co Ltd

Subject: Importance of Financial Planning

Introduction:

Operating in such a competitive market it is essential for the management of Samsung

Electronics Co Ltd to make appropriate planning regarding use of available funds.

Significance:

The main purpose behind having appropriate and feasible financial forecasting is that, it assists

in managing inflow and outflow of cash for maintaining overall liquidity position.

However, it promotes in optimum utilization of available funds or money in order to maximize

profitability of the business.

Furthermore, the main benefit of having proper financial planning is that it considers both

short and long term goals which help managerial level people in achieving desired aim and

objectives of Samsung Electronics Co Ltd in suitable way (Drake and Fabozzi, 2012). In addition to it, through the means of effective planning, top level management of cited

company can easily reduce the cost by eliminating non-beneficial expenditure. Lastly, it guides

to make feasible and reliable investment decisions (Fung, 2012).

Conclusion:

Thus, it can be stated that management of Samsung Electronics Co Ltd should promote

financial planning as it will help in managing its funds or money in an appropriate manner and assist

in attaining sustainable position in near future.

Signature:

Financial Director

Date: 7th October 2015

2.3 Information required by different users

To,

The Managing Director of Samsung Electronics Co Ltd

7

2.2 Significance of financial planning

To,

The Managing Director of Samsung Electronics Co Ltd

Subject: Importance of Financial Planning

Introduction:

Operating in such a competitive market it is essential for the management of Samsung

Electronics Co Ltd to make appropriate planning regarding use of available funds.

Significance:

The main purpose behind having appropriate and feasible financial forecasting is that, it assists

in managing inflow and outflow of cash for maintaining overall liquidity position.

However, it promotes in optimum utilization of available funds or money in order to maximize

profitability of the business.

Furthermore, the main benefit of having proper financial planning is that it considers both

short and long term goals which help managerial level people in achieving desired aim and

objectives of Samsung Electronics Co Ltd in suitable way (Drake and Fabozzi, 2012). In addition to it, through the means of effective planning, top level management of cited

company can easily reduce the cost by eliminating non-beneficial expenditure. Lastly, it guides

to make feasible and reliable investment decisions (Fung, 2012).

Conclusion:

Thus, it can be stated that management of Samsung Electronics Co Ltd should promote

financial planning as it will help in managing its funds or money in an appropriate manner and assist

in attaining sustainable position in near future.

Signature:

Financial Director

Date: 7th October 2015

2.3 Information required by different users

To,

The Managing Director of Samsung Electronics Co Ltd

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Subject: Importance of Financial Planning

There are several stakeholders associated with a business enterprise and requires range of

information as per their interest for making viable decisions. Management: Senior authority requires wide range of information for making decision

regarding policies and procedures to manage all the commercial activities of Samsung

Electronics Co Ltd. For this purpose, management mainly assess the profitability and

efficiency areas of the business. Creditors: These stakeholders evaluate the information regarding liquidity position of the

company so that, they can easily make decision on credit policy (Sonnenberg, 2008). However,

for this, trade payable consider currents assets in order to meet the short term financial

obligations. Government: Government in context to Samsung Electronics Co Ltd is one of the major

stakeholders as firm operates in different parts of world. However, legal authority requires

information related to tax obligations, that company has abided it properly or not. Employees: Workforce is the integral part of an organisation. However, in case of Samsung

Electronics Co Ltd in which employees play the most significant role in carrying out the

activities of business in the best possible manner (Ryan, 2009). Employees evaluate financial

statements to generate the information regarding future growth opportunities, salary, wages,

bonuses etc.

Signature:

Financial Director

Date: 7th October 2015

2.4 Impact of finance on financial statements

Operating at such a large level, management of Samsung Electronics Co Ltd has to prepare all

the major financial statements so that, different users can acquire information of their need or interest.

Following are the financial statements of Samsung Electronics Co Ltd: Income statement: The costs of issuing shares and charges on legal documentation of bank loan

will be recorded in the expenditure side of income statement which directly decreases the net

profit of the Samsung Electronics Co Ltd (Nicholson and Aman, 2012). Cash flow statement: Amount taken by bank loan and issues of shares will be recorded in

8

There are several stakeholders associated with a business enterprise and requires range of

information as per their interest for making viable decisions. Management: Senior authority requires wide range of information for making decision

regarding policies and procedures to manage all the commercial activities of Samsung

Electronics Co Ltd. For this purpose, management mainly assess the profitability and

efficiency areas of the business. Creditors: These stakeholders evaluate the information regarding liquidity position of the

company so that, they can easily make decision on credit policy (Sonnenberg, 2008). However,

for this, trade payable consider currents assets in order to meet the short term financial

obligations. Government: Government in context to Samsung Electronics Co Ltd is one of the major

stakeholders as firm operates in different parts of world. However, legal authority requires

information related to tax obligations, that company has abided it properly or not. Employees: Workforce is the integral part of an organisation. However, in case of Samsung

Electronics Co Ltd in which employees play the most significant role in carrying out the

activities of business in the best possible manner (Ryan, 2009). Employees evaluate financial

statements to generate the information regarding future growth opportunities, salary, wages,

bonuses etc.

Signature:

Financial Director

Date: 7th October 2015

2.4 Impact of finance on financial statements

Operating at such a large level, management of Samsung Electronics Co Ltd has to prepare all

the major financial statements so that, different users can acquire information of their need or interest.

Following are the financial statements of Samsung Electronics Co Ltd: Income statement: The costs of issuing shares and charges on legal documentation of bank loan

will be recorded in the expenditure side of income statement which directly decreases the net

profit of the Samsung Electronics Co Ltd (Nicholson and Aman, 2012). Cash flow statement: Amount taken by bank loan and issues of shares will be recorded in

8

financing activities of cash flow statement. Moreover, the interest paid and costs of issuing

shares will be headed to the cash outflow of the statement.

Balance sheet: Both the sources of finance will affect assets and liabilities side of the balance

sheet. It is because, liability increases with amount of bank borrowings and with the same

amount cash at bank will be increased in the asset side (Toten, 2006). Other than this, money

generated to equity shares will be recorded in the liability side under the heading of share

capital.

MANAGING FINANCE TASK 2

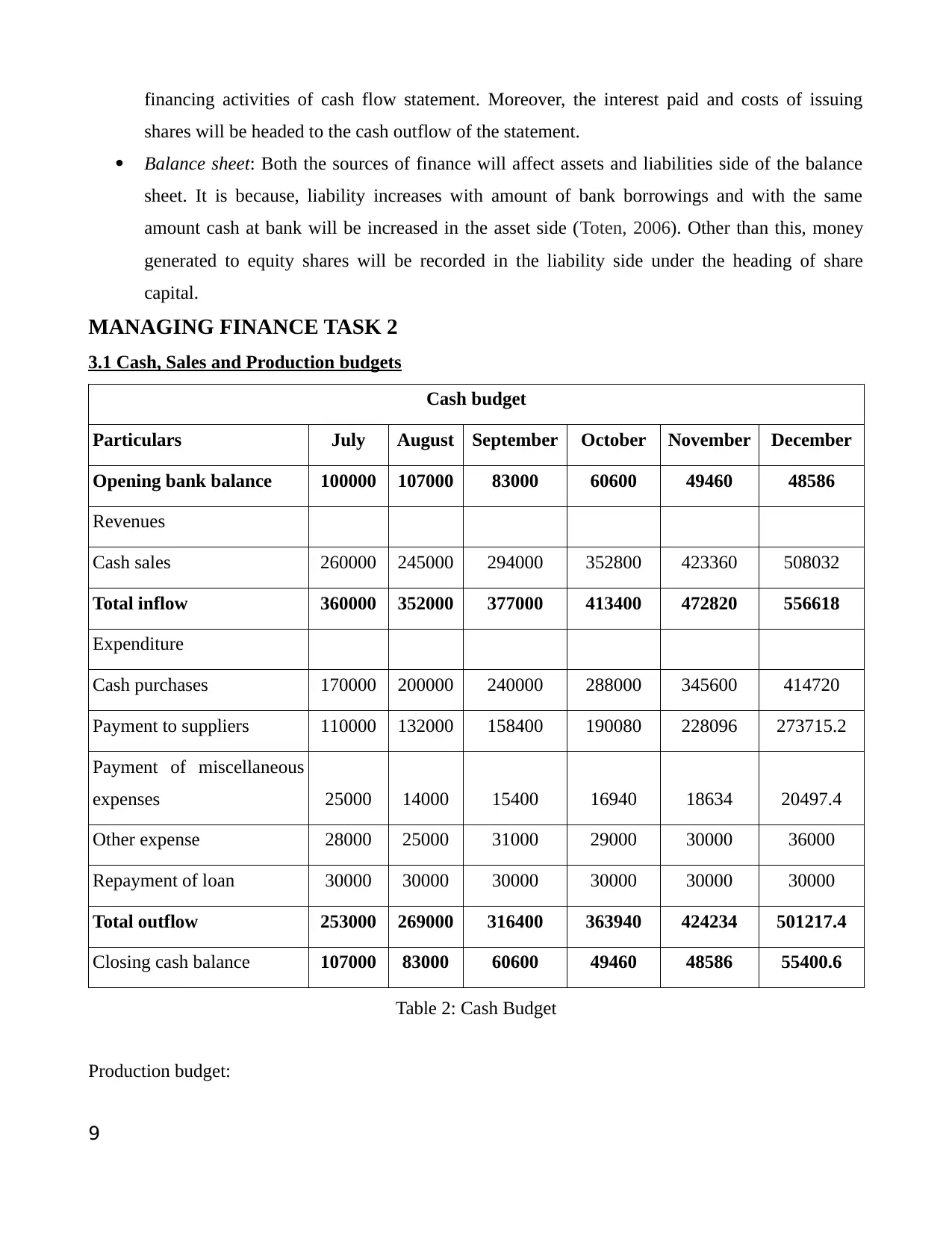

3.1 Cash, Sales and Production budgets

Cash budget

Particulars July August September October November December

Opening bank balance 100000 107000 83000 60600 49460 48586

Revenues

Cash sales 260000 245000 294000 352800 423360 508032

Total inflow 360000 352000 377000 413400 472820 556618

Expenditure

Cash purchases 170000 200000 240000 288000 345600 414720

Payment to suppliers 110000 132000 158400 190080 228096 273715.2

Payment of miscellaneous

expenses 25000 14000 15400 16940 18634 20497.4

Other expense 28000 25000 31000 29000 30000 36000

Repayment of loan 30000 30000 30000 30000 30000 30000

Total outflow 253000 269000 316400 363940 424234 501217.4

Closing cash balance 107000 83000 60600 49460 48586 55400.6

Table 2: Cash Budget

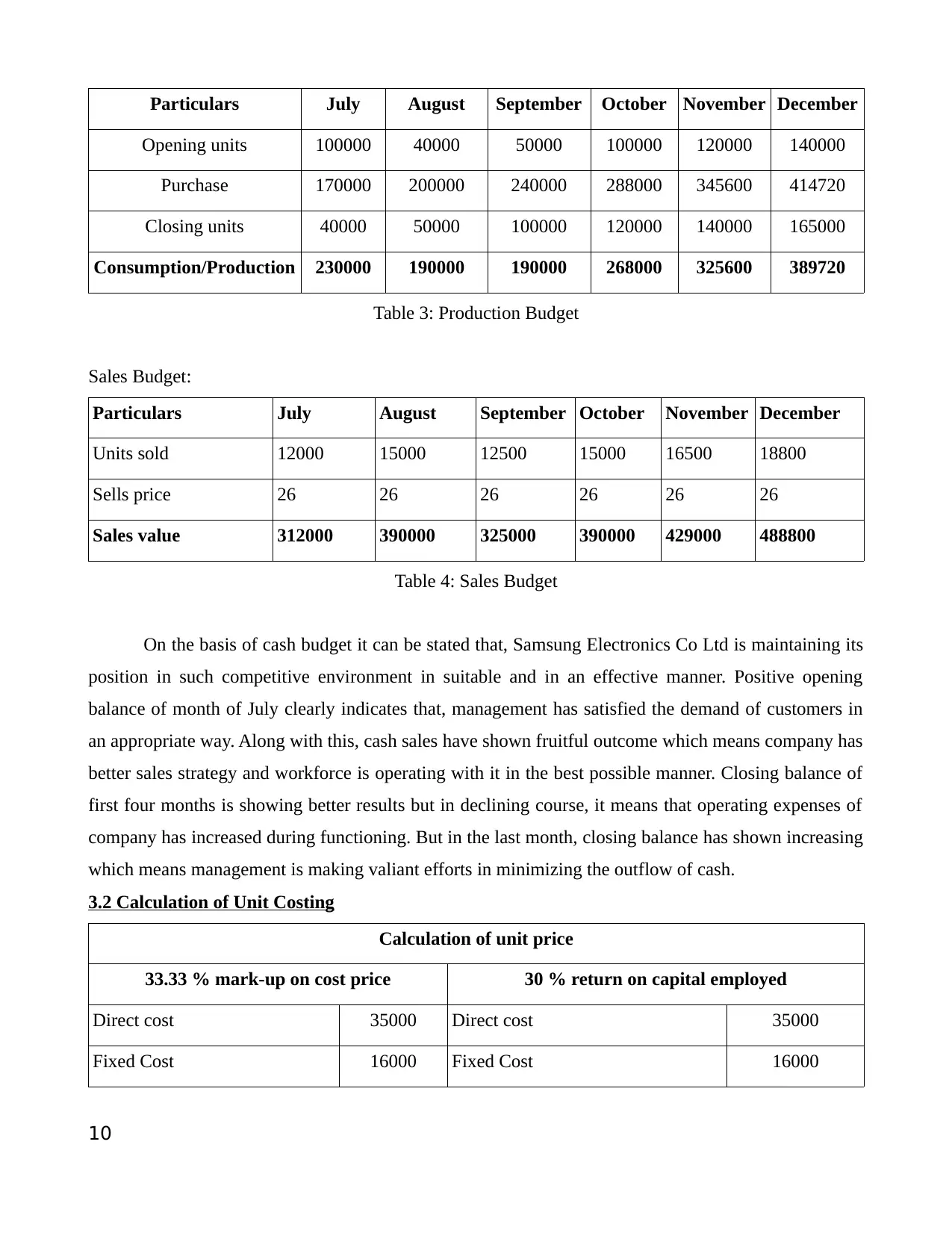

Production budget:

9

shares will be headed to the cash outflow of the statement.

Balance sheet: Both the sources of finance will affect assets and liabilities side of the balance

sheet. It is because, liability increases with amount of bank borrowings and with the same

amount cash at bank will be increased in the asset side (Toten, 2006). Other than this, money

generated to equity shares will be recorded in the liability side under the heading of share

capital.

MANAGING FINANCE TASK 2

3.1 Cash, Sales and Production budgets

Cash budget

Particulars July August September October November December

Opening bank balance 100000 107000 83000 60600 49460 48586

Revenues

Cash sales 260000 245000 294000 352800 423360 508032

Total inflow 360000 352000 377000 413400 472820 556618

Expenditure

Cash purchases 170000 200000 240000 288000 345600 414720

Payment to suppliers 110000 132000 158400 190080 228096 273715.2

Payment of miscellaneous

expenses 25000 14000 15400 16940 18634 20497.4

Other expense 28000 25000 31000 29000 30000 36000

Repayment of loan 30000 30000 30000 30000 30000 30000

Total outflow 253000 269000 316400 363940 424234 501217.4

Closing cash balance 107000 83000 60600 49460 48586 55400.6

Table 2: Cash Budget

Production budget:

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Particulars July August September October November December

Opening units 100000 40000 50000 100000 120000 140000

Purchase 170000 200000 240000 288000 345600 414720

Closing units 40000 50000 100000 120000 140000 165000

Consumption/Production 230000 190000 190000 268000 325600 389720

Table 3: Production Budget

Sales Budget:

Particulars July August September October November December

Units sold 12000 15000 12500 15000 16500 18800

Sells price 26 26 26 26 26 26

Sales value 312000 390000 325000 390000 429000 488800

Table 4: Sales Budget

On the basis of cash budget it can be stated that, Samsung Electronics Co Ltd is maintaining its

position in such competitive environment in suitable and in an effective manner. Positive opening

balance of month of July clearly indicates that, management has satisfied the demand of customers in

an appropriate way. Along with this, cash sales have shown fruitful outcome which means company has

better sales strategy and workforce is operating with it in the best possible manner. Closing balance of

first four months is showing better results but in declining course, it means that operating expenses of

company has increased during functioning. But in the last month, closing balance has shown increasing

which means management is making valiant efforts in minimizing the outflow of cash.

3.2 Calculation of Unit Costing

Calculation of unit price

33.33 % mark-up on cost price 30 % return on capital employed

Direct cost 35000 Direct cost 35000

Fixed Cost 16000 Fixed Cost 16000

10

Opening units 100000 40000 50000 100000 120000 140000

Purchase 170000 200000 240000 288000 345600 414720

Closing units 40000 50000 100000 120000 140000 165000

Consumption/Production 230000 190000 190000 268000 325600 389720

Table 3: Production Budget

Sales Budget:

Particulars July August September October November December

Units sold 12000 15000 12500 15000 16500 18800

Sells price 26 26 26 26 26 26

Sales value 312000 390000 325000 390000 429000 488800

Table 4: Sales Budget

On the basis of cash budget it can be stated that, Samsung Electronics Co Ltd is maintaining its

position in such competitive environment in suitable and in an effective manner. Positive opening

balance of month of July clearly indicates that, management has satisfied the demand of customers in

an appropriate way. Along with this, cash sales have shown fruitful outcome which means company has

better sales strategy and workforce is operating with it in the best possible manner. Closing balance of

first four months is showing better results but in declining course, it means that operating expenses of

company has increased during functioning. But in the last month, closing balance has shown increasing

which means management is making valiant efforts in minimizing the outflow of cash.

3.2 Calculation of Unit Costing

Calculation of unit price

33.33 % mark-up on cost price 30 % return on capital employed

Direct cost 35000 Direct cost 35000

Fixed Cost 16000 Fixed Cost 16000

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Total Cost 51000 Total Cost 51000

Units 500 units 500 units

Cost per unit 102 102

33.33 % mark-up on cost price 33.9966 30 % return on capital employed 10000

Per unit return 20

Selling price 135.99 Selling price 122

Table 5: Calculation of unit price

On the basis of above unit price calculation, top level management of Samsung Electronics Co

Ltd can make feasible and reliable judgement on selling price of their new products and services. From

the above computation it can be recommended to the firm that, it should use mark-up pricing strategy

to price its products and services. Rationale behind this is that, it is helping them to set affordable

prices of products as well as increasing the profit margin on the single commodity.

3.3 Assessing the viability of investment project

Investment appraisal techniques play crucial role for managers in making smart decision

regarding investment decisions (Greasley, 2001). However, these techniques assist in evaluating

reliability and viability of proposed projects so that, company can undertake best suitable option for

further investments and generate higher return. Following are the various investment appraisal

techniques:

Cash flows:

Year Project A Project B Option 2

0 Investment 60,000 Investment 60,000 Investment 60,000

1 £22,000 £21,500 £26,500

2 £26,500 £32,000 £35,000

3 £33,000 £29,800 £29,500

4 £42,000 £33,000 £30,500

11

Units 500 units 500 units

Cost per unit 102 102

33.33 % mark-up on cost price 33.9966 30 % return on capital employed 10000

Per unit return 20

Selling price 135.99 Selling price 122

Table 5: Calculation of unit price

On the basis of above unit price calculation, top level management of Samsung Electronics Co

Ltd can make feasible and reliable judgement on selling price of their new products and services. From

the above computation it can be recommended to the firm that, it should use mark-up pricing strategy

to price its products and services. Rationale behind this is that, it is helping them to set affordable

prices of products as well as increasing the profit margin on the single commodity.

3.3 Assessing the viability of investment project

Investment appraisal techniques play crucial role for managers in making smart decision

regarding investment decisions (Greasley, 2001). However, these techniques assist in evaluating

reliability and viability of proposed projects so that, company can undertake best suitable option for

further investments and generate higher return. Following are the various investment appraisal

techniques:

Cash flows:

Year Project A Project B Option 2

0 Investment 60,000 Investment 60,000 Investment 60,000

1 £22,000 £21,500 £26,500

2 £26,500 £32,000 £35,000

3 £33,000 £29,800 £29,500

4 £42,000 £33,000 £30,500

11

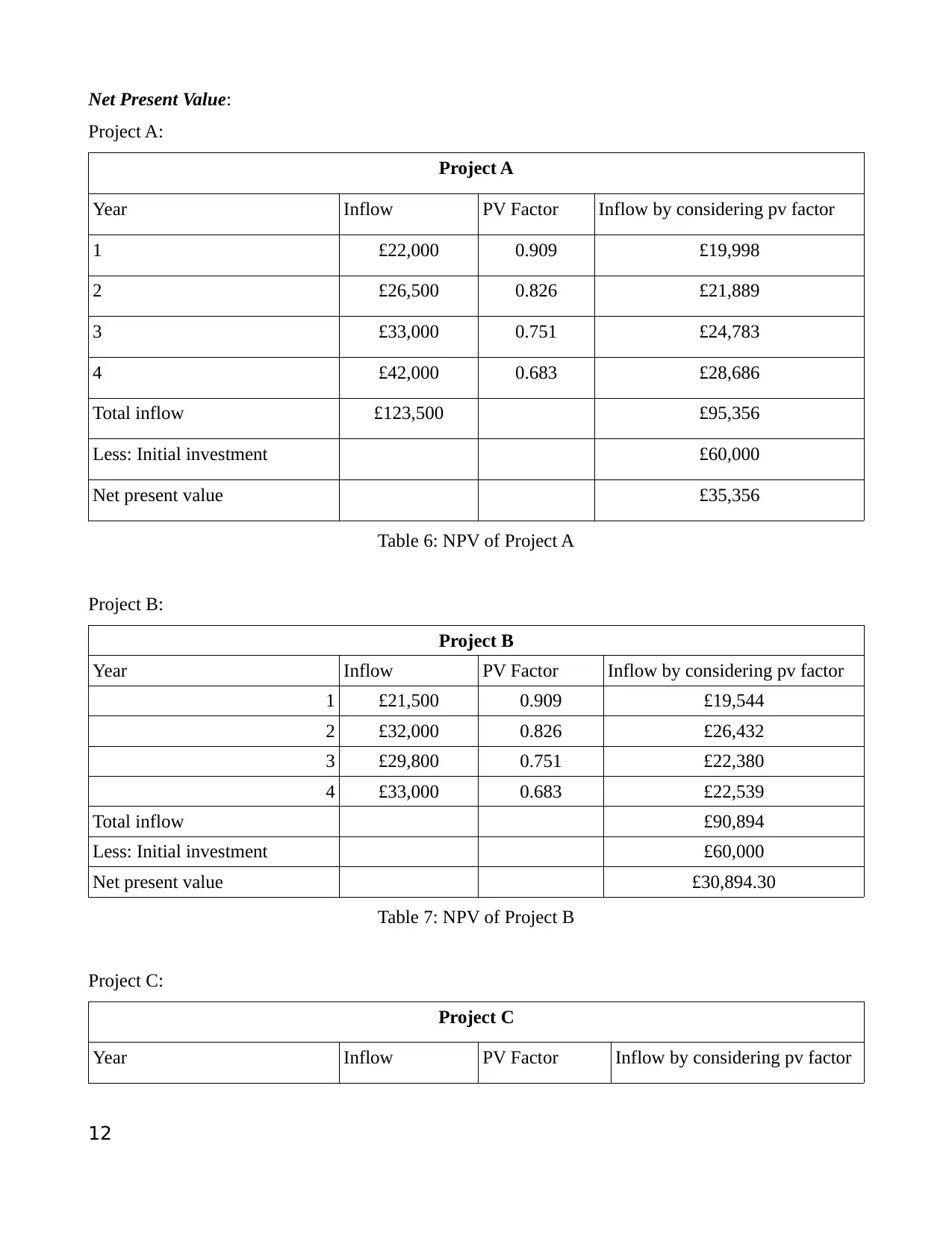

Net Present Value:

Project A:

Project A

Year Inflow PV Factor Inflow by considering pv factor

1 £22,000 0.909 £19,998

2 £26,500 0.826 £21,889

3 £33,000 0.751 £24,783

4 £42,000 0.683 £28,686

Total inflow £123,500 £95,356

Less: Initial investment £60,000

Net present value £35,356

Table 6: NPV of Project A

Project B:

Project B

Year Inflow PV Factor Inflow by considering pv factor

1 £21,500 0.909 £19,544

2 £32,000 0.826 £26,432

3 £29,800 0.751 £22,380

4 £33,000 0.683 £22,539

Total inflow £90,894

Less: Initial investment £60,000

Net present value £30,894.30

Table 7: NPV of Project B

Project C:

Project C

Year Inflow PV Factor Inflow by considering pv factor

12

Project A:

Project A

Year Inflow PV Factor Inflow by considering pv factor

1 £22,000 0.909 £19,998

2 £26,500 0.826 £21,889

3 £33,000 0.751 £24,783

4 £42,000 0.683 £28,686

Total inflow £123,500 £95,356

Less: Initial investment £60,000

Net present value £35,356

Table 6: NPV of Project A

Project B:

Project B

Year Inflow PV Factor Inflow by considering pv factor

1 £21,500 0.909 £19,544

2 £32,000 0.826 £26,432

3 £29,800 0.751 £22,380

4 £33,000 0.683 £22,539

Total inflow £90,894

Less: Initial investment £60,000

Net present value £30,894.30

Table 7: NPV of Project B

Project C:

Project C

Year Inflow PV Factor Inflow by considering pv factor

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.