University Finance Report: Financial Resource Management and Decisions

VerifiedAdded on 2019/12/03

|23

|6157

|373

Report

AI Summary

This report comprehensively addresses financial resource management and decision-making within an organization. It begins by outlining the types of finance sources available, differentiating between internal and external options, and assessing the implications of each source, supported by case study examples. The report then delves into the costs associated with raising funds and emphasizes the importance of financial planning, including the types of financial information necessary for informed decision-making. It also includes an analysis of financial statements. The report further explores investment appraisal techniques such as payback period, accounting rate of return, net present value (NPV), and internal rate of return (IRR), while also examining contribution, profit, breakeven point, and margin of safety. Additionally, the report highlights the purpose and use of various financial statements, comparing statements across different organization types and concluding with an analysis of financial statements and their implications. The report uses tables to illustrate calculations and analysis.

MANAGING FINANCIAL

RESOURCES AND

DECISIONS

1 | P a g e

RESOURCES AND

DECISIONS

1 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION......................................................................................................................1

TASK 1......................................................................................................................................1

AC 1.1 Types of finance sources...........................................................................................1

AC 1.2 Implication of each finance sources..........................................................................1

AC 1.3 Case study examples.................................................................................................2

TASK 2......................................................................................................................................2

AC 2.1 cost of finance sources to raise the funds..................................................................2

AC 2.2 Importance of financial planning..............................................................................3

AC 2.3 Types of financial information required for decision making purpose.....................4

AC 2.4 Financial statements of the organizations.................................................................4

TASK 3......................................................................................................................................5

AC 3.1 Analysis of sales budget and cash budget ................................................................5

AC 3.3 Investment appraisal techniques...............................................................................5

AC 3.2 Contribution, profit, breakeven point and margin of safety......................................6

TASK 4....................................................................................................................................11

AC 4.1 Purpose and use of different statements of the organization..................................11

AC 4.2 Financial statements of different types of organization..........................................12

AC 4.3 Analysis of financial statements.............................................................................13

CONCLUSION........................................................................................................................14

REFERENCES.........................................................................................................................14

2 | P a g e

INTRODUCTION......................................................................................................................1

TASK 1......................................................................................................................................1

AC 1.1 Types of finance sources...........................................................................................1

AC 1.2 Implication of each finance sources..........................................................................1

AC 1.3 Case study examples.................................................................................................2

TASK 2......................................................................................................................................2

AC 2.1 cost of finance sources to raise the funds..................................................................2

AC 2.2 Importance of financial planning..............................................................................3

AC 2.3 Types of financial information required for decision making purpose.....................4

AC 2.4 Financial statements of the organizations.................................................................4

TASK 3......................................................................................................................................5

AC 3.1 Analysis of sales budget and cash budget ................................................................5

AC 3.3 Investment appraisal techniques...............................................................................5

AC 3.2 Contribution, profit, breakeven point and margin of safety......................................6

TASK 4....................................................................................................................................11

AC 4.1 Purpose and use of different statements of the organization..................................11

AC 4.2 Financial statements of different types of organization..........................................12

AC 4.3 Analysis of financial statements.............................................................................13

CONCLUSION........................................................................................................................14

REFERENCES.........................................................................................................................14

2 | P a g e

INDEX OF TABLES

Table 1: Calculation of payback period and accounting rate of return (In £)............................6

Table 2: Calculation of NPV and IRR (In £)..............................................................................6

Table 3: Calculation of BEP, Profits and contribution (In £).....................................................7

Table 4: Calculation of profit and Break Even point (In £)......................................................7

Table 5: Calculation of profit and Break Even point (In £).......................................................8

Table 6: Calculation of profit and Break Even point (In £).......................................................8

Table 7: Calculation of profit and Break Even point (In £).......................................................9

Table 8: Analysis of respective changes on BEP and profits (In £)...........................................9

Table 9: Calculation of selling prices for different order (In £)...............................................10

Table 10: Calculation of total profits (In £).............................................................................10

Table 11: Financial statement analysis by ratio analysis method............................................13

3 | P a g e

Table 1: Calculation of payback period and accounting rate of return (In £)............................6

Table 2: Calculation of NPV and IRR (In £)..............................................................................6

Table 3: Calculation of BEP, Profits and contribution (In £).....................................................7

Table 4: Calculation of profit and Break Even point (In £)......................................................7

Table 5: Calculation of profit and Break Even point (In £).......................................................8

Table 6: Calculation of profit and Break Even point (In £).......................................................8

Table 7: Calculation of profit and Break Even point (In £).......................................................9

Table 8: Analysis of respective changes on BEP and profits (In £)...........................................9

Table 9: Calculation of selling prices for different order (In £)...............................................10

Table 10: Calculation of total profits (In £).............................................................................10

Table 11: Financial statement analysis by ratio analysis method............................................13

3 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Finance plays a vital role for all the organization whether it is new business or already

existed and large or small sized business. New business organization require finance sources

to establish in the market while existed business organization require finance for different

purposes such as to make payments for both revenue and capital expenditures. They also

need finance to expand their operations to occupy a large market share with the objective of

increasing the business growth. This report determine that how different organizations can

fulfil its capital requirement by using both internal and external finance sources.

TASK 1

AC 1.1 Types of finance sources

There are two types of finance sources available to the organization internal and

external. By using both the sources organizations can fulfil its short term, medium term and

long term financial needs.

New business organizations: The need of finance arises for establishment purpose.

Personal savings can be used for such purpose. Business owner can invest his funds and

mitigate their finance requirement. In addition, loans from relatives can also be taken

(Brigham and Ehrhardt, 2013). Bank loans are also available to fulfil its short term and

medium term requirement up to a limited extent on the basis of owner’s ability to pay it on

right time.

Old organizations: it requires operational finance to manage the business operations.

For that purpose, organization can issue shares, overdraft facility, lease financing and take

bank loans. Both the ordinary and preference shares can be issued by organizations. Further,

retained earnings are also available to fulfil their financial needs.

Large organization: The organizations that have a good market share and provide

services to a larger scale can gather funds from different sources. It includes debentures, bank

loans, share capital, overdraft and use of retained earnings (Altman and Hotchkiss, 2010).

Moreover, venture capital and other business profits are also available to such organizations.

Small organizations: Bank loans, share capital, retained earnings and return from

investment in other organizations can be used by these organizations. Moreover, funds can

be generated from overdraft and cash squeezing operations.

4 | P a g e

Finance plays a vital role for all the organization whether it is new business or already

existed and large or small sized business. New business organization require finance sources

to establish in the market while existed business organization require finance for different

purposes such as to make payments for both revenue and capital expenditures. They also

need finance to expand their operations to occupy a large market share with the objective of

increasing the business growth. This report determine that how different organizations can

fulfil its capital requirement by using both internal and external finance sources.

TASK 1

AC 1.1 Types of finance sources

There are two types of finance sources available to the organization internal and

external. By using both the sources organizations can fulfil its short term, medium term and

long term financial needs.

New business organizations: The need of finance arises for establishment purpose.

Personal savings can be used for such purpose. Business owner can invest his funds and

mitigate their finance requirement. In addition, loans from relatives can also be taken

(Brigham and Ehrhardt, 2013). Bank loans are also available to fulfil its short term and

medium term requirement up to a limited extent on the basis of owner’s ability to pay it on

right time.

Old organizations: it requires operational finance to manage the business operations.

For that purpose, organization can issue shares, overdraft facility, lease financing and take

bank loans. Both the ordinary and preference shares can be issued by organizations. Further,

retained earnings are also available to fulfil their financial needs.

Large organization: The organizations that have a good market share and provide

services to a larger scale can gather funds from different sources. It includes debentures, bank

loans, share capital, overdraft and use of retained earnings (Altman and Hotchkiss, 2010).

Moreover, venture capital and other business profits are also available to such organizations.

Small organizations: Bank loans, share capital, retained earnings and return from

investment in other organizations can be used by these organizations. Moreover, funds can

be generated from overdraft and cash squeezing operations.

4 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AC 1.2 Implication of each finance sources

Finance source Advantage Disadvantage

Share capital Large funds requirements can

be fulfil by issuing share

capital and the company is

not liable to pay regularly

dividend to the shareholders.

Shareholders have voting

rights and they play a major

role in business decisions.

Debt capital Short term and long term

both finance requirement can

be fulfil by using debt capital.

The company is obliged to

pay timely the interest and

instalment.

Overdraft Urgent or immediate funds

requirement can be generated

by bank overdraft.

Business has to pay a high

interest amount on these

facilities.

Cost and Legal Aspect:

Sources Cost Legal aspects

Bank Loans Charged interest rate by the

banks.

The business has to keep any

assets for securing the loan.

Share capital Shareholders return The business has to follow

respective corporate law for

issuing share capital.

Retained earnings No cost No legal formalities only a

resolution to be passed in

annual general meeting.

M2

This task has been covered in AC 1.3

AC 1.3 Case study examples

Case Finance source Appropriate source

XYZ Ltd. wants

to start up a Personal savings, loan from

Personal savings will be considered

as the most appropriate finance

5 | P a g e

Finance source Advantage Disadvantage

Share capital Large funds requirements can

be fulfil by issuing share

capital and the company is

not liable to pay regularly

dividend to the shareholders.

Shareholders have voting

rights and they play a major

role in business decisions.

Debt capital Short term and long term

both finance requirement can

be fulfil by using debt capital.

The company is obliged to

pay timely the interest and

instalment.

Overdraft Urgent or immediate funds

requirement can be generated

by bank overdraft.

Business has to pay a high

interest amount on these

facilities.

Cost and Legal Aspect:

Sources Cost Legal aspects

Bank Loans Charged interest rate by the

banks.

The business has to keep any

assets for securing the loan.

Share capital Shareholders return The business has to follow

respective corporate law for

issuing share capital.

Retained earnings No cost No legal formalities only a

resolution to be passed in

annual general meeting.

M2

This task has been covered in AC 1.3

AC 1.3 Case study examples

Case Finance source Appropriate source

XYZ Ltd. wants

to start up a Personal savings, loan from

Personal savings will be considered

as the most appropriate finance

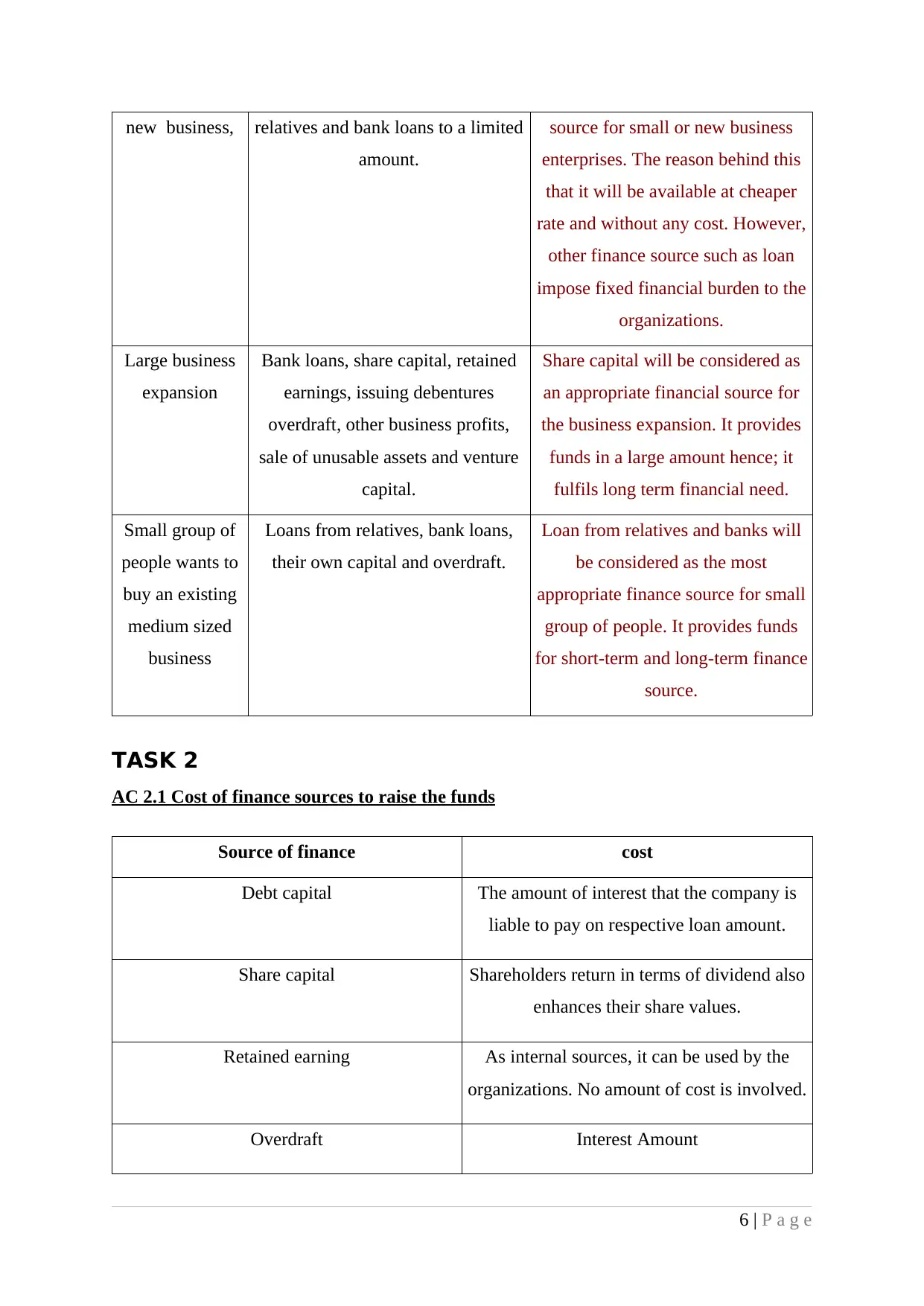

5 | P a g e

new business, relatives and bank loans to a limited

amount.

source for small or new business

enterprises. The reason behind this

that it will be available at cheaper

rate and without any cost. However,

other finance source such as loan

impose fixed financial burden to the

organizations.

Large business

expansion

Bank loans, share capital, retained

earnings, issuing debentures

overdraft, other business profits,

sale of unusable assets and venture

capital.

Share capital will be considered as

an appropriate financial source for

the business expansion. It provides

funds in a large amount hence; it

fulfils long term financial need.

Small group of

people wants to

buy an existing

medium sized

business

Loans from relatives, bank loans,

their own capital and overdraft.

Loan from relatives and banks will

be considered as the most

appropriate finance source for small

group of people. It provides funds

for short-term and long-term finance

source.

TASK 2

AC 2.1 Cost of finance sources to raise the funds

Source of finance cost

Debt capital The amount of interest that the company is

liable to pay on respective loan amount.

Share capital Shareholders return in terms of dividend also

enhances their share values.

Retained earning As internal sources, it can be used by the

organizations. No amount of cost is involved.

Overdraft Interest Amount

6 | P a g e

amount.

source for small or new business

enterprises. The reason behind this

that it will be available at cheaper

rate and without any cost. However,

other finance source such as loan

impose fixed financial burden to the

organizations.

Large business

expansion

Bank loans, share capital, retained

earnings, issuing debentures

overdraft, other business profits,

sale of unusable assets and venture

capital.

Share capital will be considered as

an appropriate financial source for

the business expansion. It provides

funds in a large amount hence; it

fulfils long term financial need.

Small group of

people wants to

buy an existing

medium sized

business

Loans from relatives, bank loans,

their own capital and overdraft.

Loan from relatives and banks will

be considered as the most

appropriate finance source for small

group of people. It provides funds

for short-term and long-term finance

source.

TASK 2

AC 2.1 Cost of finance sources to raise the funds

Source of finance cost

Debt capital The amount of interest that the company is

liable to pay on respective loan amount.

Share capital Shareholders return in terms of dividend also

enhances their share values.

Retained earning As internal sources, it can be used by the

organizations. No amount of cost is involved.

Overdraft Interest Amount

6 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Dispose of the assets The efforts that the organization has to make

for sale the assets in the market.

AC 2.2 Importance of financial planning

Financial planning is considered as a special financial instrument that helps in making

effective business decisions for different purposes (Hayre, 2013).

S. No. Importance Description

1 Capital requirement Initially, financial planning considers the amount of

total funds requirement to start and run the business.

2 Debt and capital

composition

It decides the debt equity ratio so as to collect the funds

at minimum the cost that helps in getting larger the

return.

3 Business growth and

success

Financial planning has the objective of maximizing the

profit, wealth and dividend. This in turn, resulted in

achieving the business growth and success.

4 Maximum utilization of

resources

It frames policies in order to ensure optimum

utilization of used finance sources.

5 Cash flow management It evaluates the cash inflows and outflows on a regular

basis that helps in having proper availability of

working capital.

AC 2.3 Types of financial information required for decision making purpose

Every organization need to evaluate and examining its financial information for

decision making purpose. Collecting, processing and analysing the financial data help the

organization in taking strategic decisions. Financial information can be acquired by the

business financial statements. Trading and profit and loss account provide details regarding

business sales, purchase and direct as well as indirect incomes and expenses (Chandra, 2011).

The management can take decisions for reducing the cost and increase the sales by analyse

such statements. This in turn, resulted in increasing the business operational performance.

7 | P a g e

for sale the assets in the market.

AC 2.2 Importance of financial planning

Financial planning is considered as a special financial instrument that helps in making

effective business decisions for different purposes (Hayre, 2013).

S. No. Importance Description

1 Capital requirement Initially, financial planning considers the amount of

total funds requirement to start and run the business.

2 Debt and capital

composition

It decides the debt equity ratio so as to collect the funds

at minimum the cost that helps in getting larger the

return.

3 Business growth and

success

Financial planning has the objective of maximizing the

profit, wealth and dividend. This in turn, resulted in

achieving the business growth and success.

4 Maximum utilization of

resources

It frames policies in order to ensure optimum

utilization of used finance sources.

5 Cash flow management It evaluates the cash inflows and outflows on a regular

basis that helps in having proper availability of

working capital.

AC 2.3 Types of financial information required for decision making purpose

Every organization need to evaluate and examining its financial information for

decision making purpose. Collecting, processing and analysing the financial data help the

organization in taking strategic decisions. Financial information can be acquired by the

business financial statements. Trading and profit and loss account provide details regarding

business sales, purchase and direct as well as indirect incomes and expenses (Chandra, 2011).

The management can take decisions for reducing the cost and increase the sales by analyse

such statements. This in turn, resulted in increasing the business operational performance.

7 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Moreover, the financial performance can be analyse by the balance sheet so it helps to take

decisions for identifying the funds requirements and identify the best sources for it. Further, it

ensures proper utilization of available funds (Zager and Zager, 2006). In addition, budgets

also provide important information’s regarding business sales, purchase and cash flows. By

proper analysis of it the business will be able to have significant balance among cash flows

and increase the business performance for the future period. Different decisions makers and

their information need are described as under:

Managers: They manage the overall business operations and enhance profitability and

financial status. Thus, they need information about company's profit through profit and loss

statement and want to know the financial position through using balance sheet. Proper

analysis of revenues and expenses make managers able to take appropriate decisions for

improving incomes. Moreover, through regular monitoring and controlling operating

functions, managers can reduce the business cost. Thus, in turn, profitability can be

improved. Further, balance sheet provides information about business liquidity, efficiency

and solvency to discharge their liabilities. It assists the managers in taking effective

decisions, in making competitive policies and in strengthening the financial position.

Investors: They invest funds for getting maximum return on their own funds. They

need information about solvency position and profit margin to ensure their return and funds

security. By high profit earnings and good solvency position, firms are able to attract large

number of investors and can fulfil their financial requirement.

Lenders: They provide funds at an interest rate hence, need information about profits,

solvency, interest bearing capacity and cash generating ability. Analysis of profits, earnings,

interest bearing ability and cash generating capacity provide assistance to lender for taking

effective lending decisions. They ensure that company can bear fixed burden and pay interest

timely. Further, they demand collateral security and analyse business solvency to secure their

funds.

Creditors: They supply material on credit henceforth; they need information about

profits and liquidity. Good creditworthiness firms are able to attract creditors and extend their

credit period.

AC 2.4 Financial statements of the organizations

Financial statements are prepared to determine the past business operational and

financial performance.

particular Amount particular Amount

8 | P a g e

decisions for identifying the funds requirements and identify the best sources for it. Further, it

ensures proper utilization of available funds (Zager and Zager, 2006). In addition, budgets

also provide important information’s regarding business sales, purchase and cash flows. By

proper analysis of it the business will be able to have significant balance among cash flows

and increase the business performance for the future period. Different decisions makers and

their information need are described as under:

Managers: They manage the overall business operations and enhance profitability and

financial status. Thus, they need information about company's profit through profit and loss

statement and want to know the financial position through using balance sheet. Proper

analysis of revenues and expenses make managers able to take appropriate decisions for

improving incomes. Moreover, through regular monitoring and controlling operating

functions, managers can reduce the business cost. Thus, in turn, profitability can be

improved. Further, balance sheet provides information about business liquidity, efficiency

and solvency to discharge their liabilities. It assists the managers in taking effective

decisions, in making competitive policies and in strengthening the financial position.

Investors: They invest funds for getting maximum return on their own funds. They

need information about solvency position and profit margin to ensure their return and funds

security. By high profit earnings and good solvency position, firms are able to attract large

number of investors and can fulfil their financial requirement.

Lenders: They provide funds at an interest rate hence, need information about profits,

solvency, interest bearing capacity and cash generating ability. Analysis of profits, earnings,

interest bearing ability and cash generating capacity provide assistance to lender for taking

effective lending decisions. They ensure that company can bear fixed burden and pay interest

timely. Further, they demand collateral security and analyse business solvency to secure their

funds.

Creditors: They supply material on credit henceforth; they need information about

profits and liquidity. Good creditworthiness firms are able to attract creditors and extend their

credit period.

AC 2.4 Financial statements of the organizations

Financial statements are prepared to determine the past business operational and

financial performance.

particular Amount particular Amount

8 | P a g e

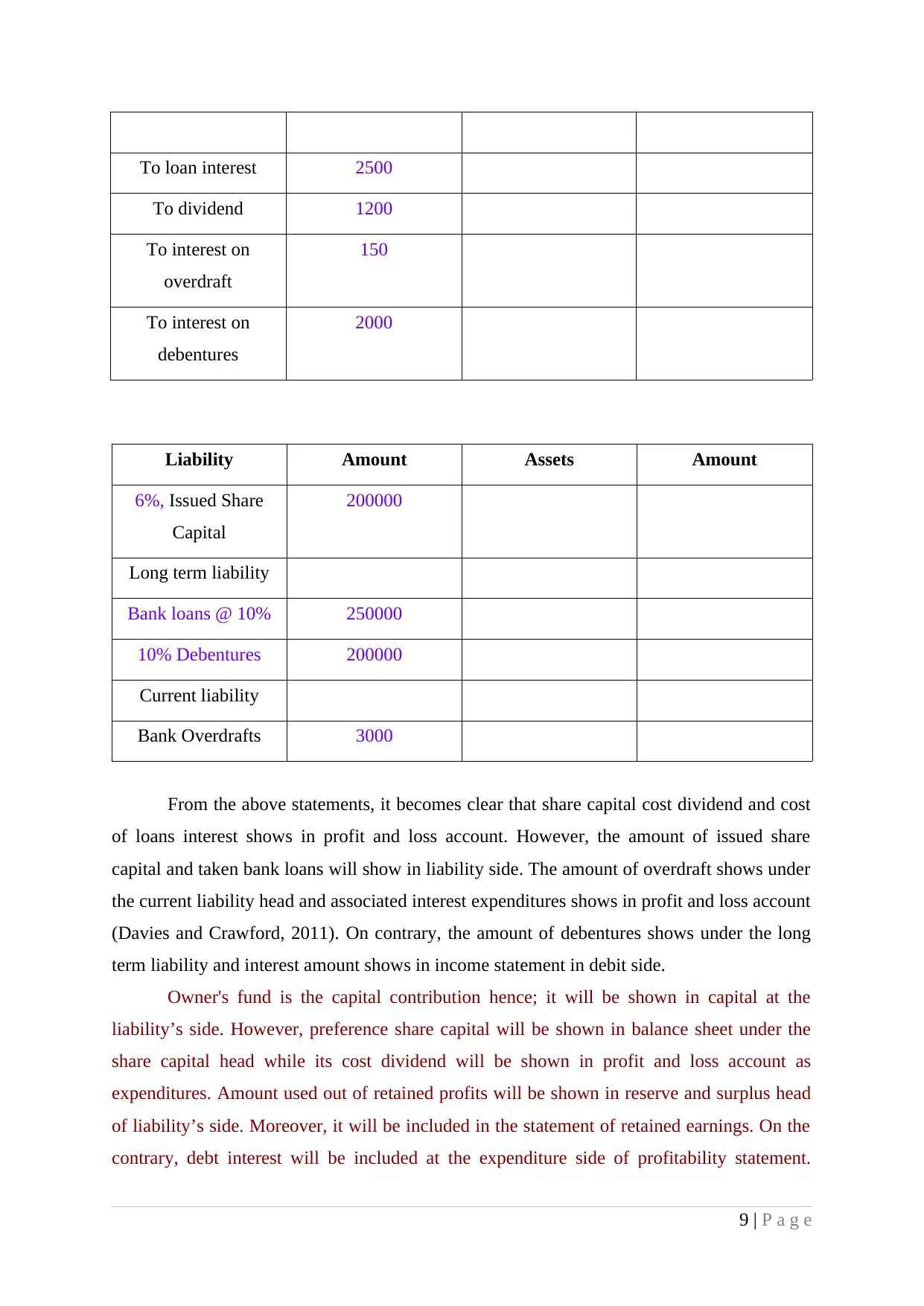

To loan interest 2500

To dividend 1200

To interest on

overdraft

150

To interest on

debentures

2000

Liability Amount Assets Amount

6%, Issued Share

Capital

200000

Long term liability

Bank loans @ 10% 250000

10% Debentures 200000

Current liability

Bank Overdrafts 3000

From the above statements, it becomes clear that share capital cost dividend and cost

of loans interest shows in profit and loss account. However, the amount of issued share

capital and taken bank loans will show in liability side. The amount of overdraft shows under

the current liability head and associated interest expenditures shows in profit and loss account

(Davies and Crawford, 2011). On contrary, the amount of debentures shows under the long

term liability and interest amount shows in income statement in debit side.

Owner's fund is the capital contribution hence; it will be shown in capital at the

liability’s side. However, preference share capital will be shown in balance sheet under the

share capital head while its cost dividend will be shown in profit and loss account as

expenditures. Amount used out of retained profits will be shown in reserve and surplus head

of liability’s side. Moreover, it will be included in the statement of retained earnings. On the

contrary, debt interest will be included at the expenditure side of profitability statement.

9 | P a g e

To dividend 1200

To interest on

overdraft

150

To interest on

debentures

2000

Liability Amount Assets Amount

6%, Issued Share

Capital

200000

Long term liability

Bank loans @ 10% 250000

10% Debentures 200000

Current liability

Bank Overdrafts 3000

From the above statements, it becomes clear that share capital cost dividend and cost

of loans interest shows in profit and loss account. However, the amount of issued share

capital and taken bank loans will show in liability side. The amount of overdraft shows under

the current liability head and associated interest expenditures shows in profit and loss account

(Davies and Crawford, 2011). On contrary, the amount of debentures shows under the long

term liability and interest amount shows in income statement in debit side.

Owner's fund is the capital contribution hence; it will be shown in capital at the

liability’s side. However, preference share capital will be shown in balance sheet under the

share capital head while its cost dividend will be shown in profit and loss account as

expenditures. Amount used out of retained profits will be shown in reserve and surplus head

of liability’s side. Moreover, it will be included in the statement of retained earnings. On the

contrary, debt interest will be included at the expenditure side of profitability statement.

9 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

However, in balance sheet, the amount of borrowed funds will be shown at the liability’s

side. Moreover, it will improve the cash balance in asset’s side.

TASK 3

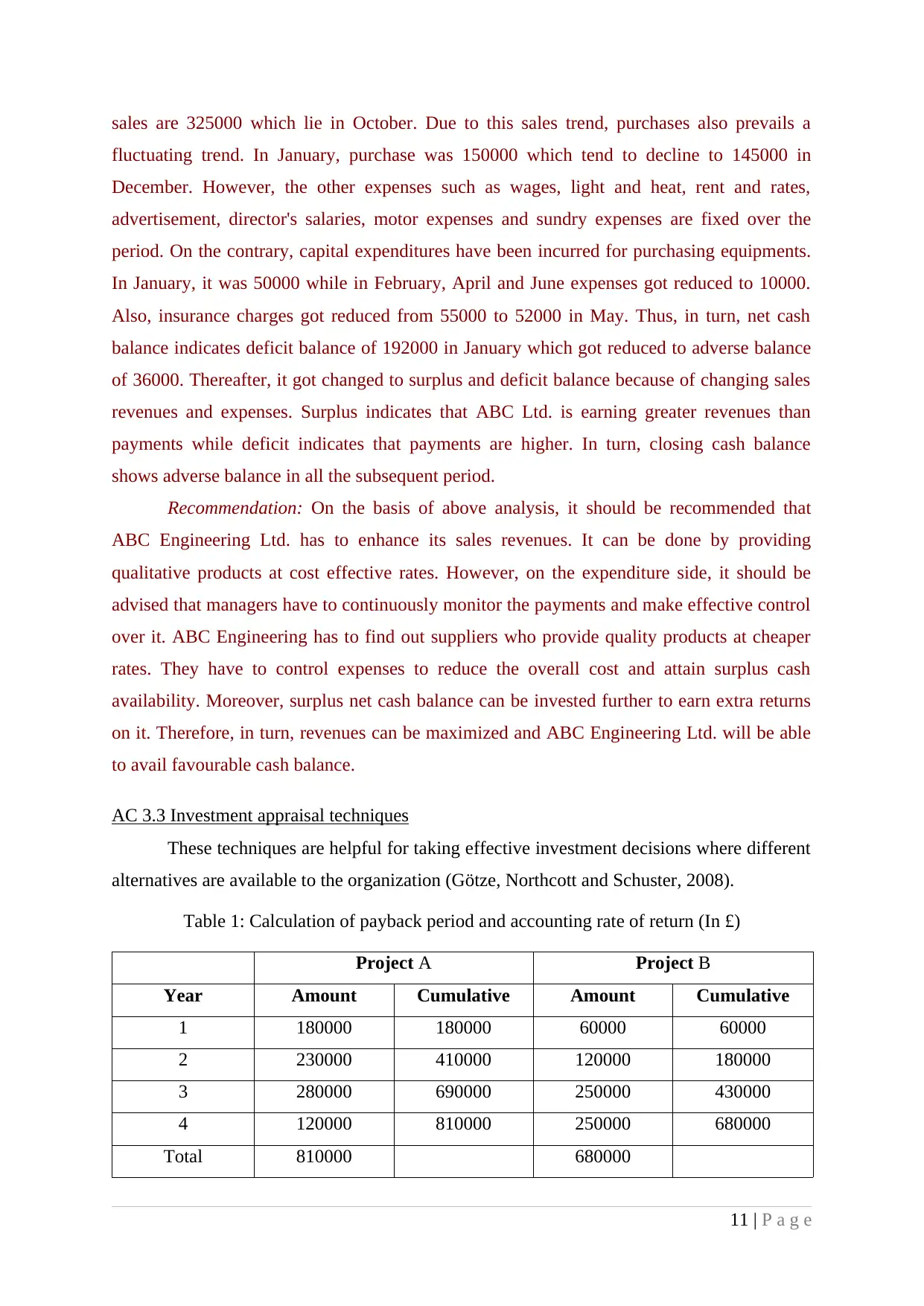

AC 3.1 Analysis of sales budget and cash budget

Sales budget: Prepared sales budget indicate that the actual sales are increasing from

215000£ to 270000£. However, budgeted sales are higher than actual sales to 230000£ and

300000£ respectively. Therefore, variances are increases from 15000£ to 138000£. The

reason behind such variances may be decline the demand, worst quality, increase the product

cost results in increase the prices. Moreover, other factors such as competition, substitute

product and marketing also impact the sales volume (Manyard, 2013). To increase the

business sales the organization should improve its quality and discounting the rates by

curtailment of unnecessary costs. Moreover, effective advertising methods can be employed

for such purpose.

To

The ABC Engineering Ltd. Director

Date – 5th December, 2015

On the basis of above identification it becomes necessary to be reported that ABC

Manufacturing Ltd. sales are declining continuously. Various reasons such as product

quality, consumer dissatisfactions, competitor’s product, their pricing policies and the

production techniques influenced the sales. Therefore, it is advisable that ABC

manufacturing Ltd. has to improve the quality by using new and innovative technology.

Further, to eliminate the competitors impact the company has to decide the product prices

considering the competitors policies. This in turn, the business will be able to increase the

product sales and the cash surplus. One more way to increase the cash and eliminate the

deficit balance is to replough its PY cash balances.

D2

Analysis of cash budget for ABC Manufacturing Ltd.

As per the scenario, cash budget indicated that ABC Manufacturing Ltd. is generating

revenues through sales. Business sales revenues show a fluctuating trend as it got increased

or decreased over the period. In January, sales were 200000 which got increased to 265000 in

December. However, in most of the months, sales were around 300000 while the maximum

10 | P a g e

side. Moreover, it will improve the cash balance in asset’s side.

TASK 3

AC 3.1 Analysis of sales budget and cash budget

Sales budget: Prepared sales budget indicate that the actual sales are increasing from

215000£ to 270000£. However, budgeted sales are higher than actual sales to 230000£ and

300000£ respectively. Therefore, variances are increases from 15000£ to 138000£. The

reason behind such variances may be decline the demand, worst quality, increase the product

cost results in increase the prices. Moreover, other factors such as competition, substitute

product and marketing also impact the sales volume (Manyard, 2013). To increase the

business sales the organization should improve its quality and discounting the rates by

curtailment of unnecessary costs. Moreover, effective advertising methods can be employed

for such purpose.

To

The ABC Engineering Ltd. Director

Date – 5th December, 2015

On the basis of above identification it becomes necessary to be reported that ABC

Manufacturing Ltd. sales are declining continuously. Various reasons such as product

quality, consumer dissatisfactions, competitor’s product, their pricing policies and the

production techniques influenced the sales. Therefore, it is advisable that ABC

manufacturing Ltd. has to improve the quality by using new and innovative technology.

Further, to eliminate the competitors impact the company has to decide the product prices

considering the competitors policies. This in turn, the business will be able to increase the

product sales and the cash surplus. One more way to increase the cash and eliminate the

deficit balance is to replough its PY cash balances.

D2

Analysis of cash budget for ABC Manufacturing Ltd.

As per the scenario, cash budget indicated that ABC Manufacturing Ltd. is generating

revenues through sales. Business sales revenues show a fluctuating trend as it got increased

or decreased over the period. In January, sales were 200000 which got increased to 265000 in

December. However, in most of the months, sales were around 300000 while the maximum

10 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

sales are 325000 which lie in October. Due to this sales trend, purchases also prevails a

fluctuating trend. In January, purchase was 150000 which tend to decline to 145000 in

December. However, the other expenses such as wages, light and heat, rent and rates,

advertisement, director's salaries, motor expenses and sundry expenses are fixed over the

period. On the contrary, capital expenditures have been incurred for purchasing equipments.

In January, it was 50000 while in February, April and June expenses got reduced to 10000.

Also, insurance charges got reduced from 55000 to 52000 in May. Thus, in turn, net cash

balance indicates deficit balance of 192000 in January which got reduced to adverse balance

of 36000. Thereafter, it got changed to surplus and deficit balance because of changing sales

revenues and expenses. Surplus indicates that ABC Ltd. is earning greater revenues than

payments while deficit indicates that payments are higher. In turn, closing cash balance

shows adverse balance in all the subsequent period.

Recommendation: On the basis of above analysis, it should be recommended that

ABC Engineering Ltd. has to enhance its sales revenues. It can be done by providing

qualitative products at cost effective rates. However, on the expenditure side, it should be

advised that managers have to continuously monitor the payments and make effective control

over it. ABC Engineering has to find out suppliers who provide quality products at cheaper

rates. They have to control expenses to reduce the overall cost and attain surplus cash

availability. Moreover, surplus net cash balance can be invested further to earn extra returns

on it. Therefore, in turn, revenues can be maximized and ABC Engineering Ltd. will be able

to avail favourable cash balance.

AC 3.3 Investment appraisal techniques

These techniques are helpful for taking effective investment decisions where different

alternatives are available to the organization (Götze, Northcott and Schuster, 2008).

Table 1: Calculation of payback period and accounting rate of return (In £)

Project A Project B

Year Amount Cumulative Amount Cumulative

1 180000 180000 60000 60000

2 230000 410000 120000 180000

3 280000 690000 250000 430000

4 120000 810000 250000 680000

Total 810000 680000

11 | P a g e

fluctuating trend. In January, purchase was 150000 which tend to decline to 145000 in

December. However, the other expenses such as wages, light and heat, rent and rates,

advertisement, director's salaries, motor expenses and sundry expenses are fixed over the

period. On the contrary, capital expenditures have been incurred for purchasing equipments.

In January, it was 50000 while in February, April and June expenses got reduced to 10000.

Also, insurance charges got reduced from 55000 to 52000 in May. Thus, in turn, net cash

balance indicates deficit balance of 192000 in January which got reduced to adverse balance

of 36000. Thereafter, it got changed to surplus and deficit balance because of changing sales

revenues and expenses. Surplus indicates that ABC Ltd. is earning greater revenues than

payments while deficit indicates that payments are higher. In turn, closing cash balance

shows adverse balance in all the subsequent period.

Recommendation: On the basis of above analysis, it should be recommended that

ABC Engineering Ltd. has to enhance its sales revenues. It can be done by providing

qualitative products at cost effective rates. However, on the expenditure side, it should be

advised that managers have to continuously monitor the payments and make effective control

over it. ABC Engineering has to find out suppliers who provide quality products at cheaper

rates. They have to control expenses to reduce the overall cost and attain surplus cash

availability. Moreover, surplus net cash balance can be invested further to earn extra returns

on it. Therefore, in turn, revenues can be maximized and ABC Engineering Ltd. will be able

to avail favourable cash balance.

AC 3.3 Investment appraisal techniques

These techniques are helpful for taking effective investment decisions where different

alternatives are available to the organization (Götze, Northcott and Schuster, 2008).

Table 1: Calculation of payback period and accounting rate of return (In £)

Project A Project B

Year Amount Cumulative Amount Cumulative

1 180000 180000 60000 60000

2 230000 410000 120000 180000

3 280000 690000 250000 430000

4 120000 810000 250000 680000

Total 810000 680000

11 | P a g e

Average profit 202500 170000

Payback period (proposal A) = 2year + 40000£/280000£ = 2.143 year

Payback period (proposal B) = 3year + 20000£/250000£ = 3.08 year

ARR = Average profit/Total investment *100

(Proposal A) = 202500£/450000£*100 = 45%

(Proposal B) = 170000£/450000£*100 = 37.78%

Table 2: Calculation of NPV and IRR (In £)

Project A Project B

Year Amount

Discounted

value@6%

Discounted

cash inflow Amount

Discounted

value

@6%

Discounted

cash inflow

0 -450000 1 -450000 -450000 1 -450000

1 180000 0.943 169740 60000 0.943 56580

2 230000 0.89 204700 120000 0.89 106800

3 280000 0.84 235200 250000 0.84 210000

4 120000 0.763 91560 250000 0.763 190750

Total 29.20% 251200 15.02% 114130

NPV (Proposal A) = 251200£

NPV (Proposal B) = 114130£

IRR (Proposal A) = 29.20%

IRR (Proposal B) = 15.02%

Conclusion: on the basis of above calculation, it can be concluded that ABC Engineering

Ltd. has to invest their funds in project A because of lower the payback period and higher

return.

D1

Investment appraisal techniques for ABC Engineering Ltd.

These techniques provide assistance to test the project viability for ABC Engineering

Ltd. and make company able to determine the most viable project. Payback period (PP)

method assists ABC Ltd. to determine the recovery period of available investment proposal.

12 | P a g e

Payback period (proposal A) = 2year + 40000£/280000£ = 2.143 year

Payback period (proposal B) = 3year + 20000£/250000£ = 3.08 year

ARR = Average profit/Total investment *100

(Proposal A) = 202500£/450000£*100 = 45%

(Proposal B) = 170000£/450000£*100 = 37.78%

Table 2: Calculation of NPV and IRR (In £)

Project A Project B

Year Amount

Discounted

value@6%

Discounted

cash inflow Amount

Discounted

value

@6%

Discounted

cash inflow

0 -450000 1 -450000 -450000 1 -450000

1 180000 0.943 169740 60000 0.943 56580

2 230000 0.89 204700 120000 0.89 106800

3 280000 0.84 235200 250000 0.84 210000

4 120000 0.763 91560 250000 0.763 190750

Total 29.20% 251200 15.02% 114130

NPV (Proposal A) = 251200£

NPV (Proposal B) = 114130£

IRR (Proposal A) = 29.20%

IRR (Proposal B) = 15.02%

Conclusion: on the basis of above calculation, it can be concluded that ABC Engineering

Ltd. has to invest their funds in project A because of lower the payback period and higher

return.

D1

Investment appraisal techniques for ABC Engineering Ltd.

These techniques provide assistance to test the project viability for ABC Engineering

Ltd. and make company able to determine the most viable project. Payback period (PP)

method assists ABC Ltd. to determine the recovery period of available investment proposal.

12 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.