Analysis of Financial Resources and Decisions: Clariton Antiques Ltd

VerifiedAdded on 2020/02/03

|21

|7363

|28

Report

AI Summary

This report provides a comprehensive analysis of financial resources and decisions for Clariton Antiques Ltd, a partnership business seeking expansion. It explores various sources of finance available to both unincorporated and incorporated businesses, including their implications. The report delves into the cost of finance, focusing on bank loans and venture capital, and emphasizes the importance of financial planning. It outlines the information needed for effective financial decision-making and examines the impact of different financing sources on Clariton's financial statements. Furthermore, the report explains budgeting, cost and pricing decisions, and project feasibility analysis through capital budgeting. It also covers important financial statements, comparing the final accounts of a partnership with Clariton Antiques Ltd and analyzing the company's financial performance over two years using financial ratios. The report aims to provide insights into managing financial resources effectively and making informed financial decisions for business growth.

MANAGING FINANCIAL

RESOURCES AND

DECISIONS

RESOURCES AND

DECISIONS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION......................................................................................................................3

TASK 1......................................................................................................................................3

1.1 Sources of finance available for unincorporated and incorporated businesses................3

1.2 Implications of sources of finance on the firm.................................................................4

1.3 Appropriate sources of finance for firm such as Clariton Antiques Ltd..........................5

TASK 2......................................................................................................................................6

2.1 Cost of sources of finance such as bank loan and venture capital...................................6

2.2 Importance of financial planning on the Clariton company.............................................6

2.3 Information’s needed for the firm in order to take financial decisions............................7

2.4 Impact of various sources of finance on financial statement of Clariton Antiques Ltd...7

TASK 3......................................................................................................................................8

3.1 Explaining budget along with its significance for the Clariton Antiques Ltd..................8

3.2 Computation of cost and pricing decisions....................................................................10

3.3 Analysis of project feasibility through capital budgeting..............................................11

TASK 4....................................................................................................................................13

4.1 Explaining important financial statements.....................................................................13

4.2 Comparison of final accounts of partnership & Clariton Antiques Ltd.........................14

4.3 Comparing Clariton’s business performance for two financial years............................16

CONCLUSION........................................................................................................................17

REFERENCES.........................................................................................................................18

INTRODUCTION......................................................................................................................3

TASK 1......................................................................................................................................3

1.1 Sources of finance available for unincorporated and incorporated businesses................3

1.2 Implications of sources of finance on the firm.................................................................4

1.3 Appropriate sources of finance for firm such as Clariton Antiques Ltd..........................5

TASK 2......................................................................................................................................6

2.1 Cost of sources of finance such as bank loan and venture capital...................................6

2.2 Importance of financial planning on the Clariton company.............................................6

2.3 Information’s needed for the firm in order to take financial decisions............................7

2.4 Impact of various sources of finance on financial statement of Clariton Antiques Ltd...7

TASK 3......................................................................................................................................8

3.1 Explaining budget along with its significance for the Clariton Antiques Ltd..................8

3.2 Computation of cost and pricing decisions....................................................................10

3.3 Analysis of project feasibility through capital budgeting..............................................11

TASK 4....................................................................................................................................13

4.1 Explaining important financial statements.....................................................................13

4.2 Comparison of final accounts of partnership & Clariton Antiques Ltd.........................14

4.3 Comparing Clariton’s business performance for two financial years............................16

CONCLUSION........................................................................................................................17

REFERENCES.........................................................................................................................18

INTRODUCTION

Finance is an important element of the firm which is base of each business in order to

come into consideration. Without the financial resources an organisation cannot exist in the

industry where it operates. Further, it is necessary to manage and effectively utilize financial

resources in the business entity. The present case is based on Clariton Antiques Limited firm

which is a partnership business and going to expand business in country Birmingham. In

order to raise fund it uses bank loan as well as venture capital. The report throws light on

different sources of finance and their implications on the company. Further, it describes about

cost of finance and its impact on various financial statements of the Clarion organisation.

Apart from this it focuses on cash budget as well as financial tools used in order to take

investment decisions. At the last it emphasis on financial performance of the Clariton with

help of numerous financial rations.

TASK 1

1.1 Sources of finance available for unincorporated and incorporated businesses

Unincorporated Businesses: Company which not operating in the industry using

legal rules and regulations as well as have not legal identity, known as unincorporated firms.

When this type of entities wants to expand their business then they have different sources of

finance which provide fund (Kumar and Rao, 2016). The sources are such as follows:

Sale of assets: As per the sources the company sale its assets which are unproductive

as well as unused in the firm. Further, those assets which are not comes into

consideration for generating sales are sold out and amount is to be used in firm for

business expansion. When the company raise fund using the respective financing

source then it helps to reduce level of dent in the financial statements of such firms.

Apart from this it will lead to increase profitability of the company by which financial

performance will improve in the industry. However, it leads to decrease total assets of

the firm as well as valuation of the business entity in the overall industry. Further,

ability to meet with short term obligations reduce ultimately which is loss for the

organisation.

Personal savings: Every businessman whether he has small or big firm, saving some

amount from his earnings. The saved amount is used in the company which helps to

enhance level of firm and expand as well. It is the sources in which the business not

need to take external help as well as there is not any type financing costs are imposes

Finance is an important element of the firm which is base of each business in order to

come into consideration. Without the financial resources an organisation cannot exist in the

industry where it operates. Further, it is necessary to manage and effectively utilize financial

resources in the business entity. The present case is based on Clariton Antiques Limited firm

which is a partnership business and going to expand business in country Birmingham. In

order to raise fund it uses bank loan as well as venture capital. The report throws light on

different sources of finance and their implications on the company. Further, it describes about

cost of finance and its impact on various financial statements of the Clarion organisation.

Apart from this it focuses on cash budget as well as financial tools used in order to take

investment decisions. At the last it emphasis on financial performance of the Clariton with

help of numerous financial rations.

TASK 1

1.1 Sources of finance available for unincorporated and incorporated businesses

Unincorporated Businesses: Company which not operating in the industry using

legal rules and regulations as well as have not legal identity, known as unincorporated firms.

When this type of entities wants to expand their business then they have different sources of

finance which provide fund (Kumar and Rao, 2016). The sources are such as follows:

Sale of assets: As per the sources the company sale its assets which are unproductive

as well as unused in the firm. Further, those assets which are not comes into

consideration for generating sales are sold out and amount is to be used in firm for

business expansion. When the company raise fund using the respective financing

source then it helps to reduce level of dent in the financial statements of such firms.

Apart from this it will lead to increase profitability of the company by which financial

performance will improve in the industry. However, it leads to decrease total assets of

the firm as well as valuation of the business entity in the overall industry. Further,

ability to meet with short term obligations reduce ultimately which is loss for the

organisation.

Personal savings: Every businessman whether he has small or big firm, saving some

amount from his earnings. The saved amount is used in the company which helps to

enhance level of firm and expand as well. It is the sources in which the business not

need to take external help as well as there is not any type financing costs are imposes

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

on the business. It helps to the owner when emergencies occurs in the company as

well as very typical situations arises. Further, it helps to avoid different types of

indirect expenses such as interest, dividend etc. which lead to make beneficial. Apart

from this it leads to reduce net worth of finance of the owner in his personal life.

Retained earnings: Profit which remains from net profit after give dividend to

shareholders is known as retained earnings (Malik, Field and Gorwood, 2016). The

amount is used in order to expanding the firm which is widely using source of finance

by most of the firms. It helps to the company in order to make new projects as well as

expand the business in another market. Further, these types of sources are readily

available in the firm as well as it helps to decrease cots of issue shares in the market.

However, when company use such type of source then it leads to increase opportunity

cost by which level of profit get decrease. So, it is adverse as well as disadvantage for

the company.

Incorporated Businesses: The firm which operates using all the rules, laws and

legislations of regulatory body and has legal identity, known as an incorporated company. In

order to raise finance for business expansion of these forms of organizations, there are

sources of finance available which are enumerated below:

Equity financing: Most of the companies are using such source of finance in order to

raise firm from the market. According to the source organisation issues shares through

IPO and FPO process (Ranjan, 2016). The shares are purchased by investors known

as shareholders and the amount is using for expanding company. It is widely used

source in order to raise fund through external markets. It is beneficial for the company

because it helps to increase stockholders as well as investment in the company. On the

other side if firm issues preference shares then it must give dividend to shareholders

in every financial year. Further, it has to complete all the legal formalities as well as

listing in the stock market as well.

Bank loan: Another source of finance for incorporated companies is bank loan in

which the firm takes debt amount from commercial banks. It is widely used external

source of finance in order to raise fund in the organisation. As per the source the

company is most beneficial in terms of raising finance because it helps to analyses

valuation of the company in the market. On the other side it provides financial

services to the organisation when it has sufficient ability to pay debt. In case company

is not able to pay all the debts then bank has right to wind up overall firm.

well as very typical situations arises. Further, it helps to avoid different types of

indirect expenses such as interest, dividend etc. which lead to make beneficial. Apart

from this it leads to reduce net worth of finance of the owner in his personal life.

Retained earnings: Profit which remains from net profit after give dividend to

shareholders is known as retained earnings (Malik, Field and Gorwood, 2016). The

amount is used in order to expanding the firm which is widely using source of finance

by most of the firms. It helps to the company in order to make new projects as well as

expand the business in another market. Further, these types of sources are readily

available in the firm as well as it helps to decrease cots of issue shares in the market.

However, when company use such type of source then it leads to increase opportunity

cost by which level of profit get decrease. So, it is adverse as well as disadvantage for

the company.

Incorporated Businesses: The firm which operates using all the rules, laws and

legislations of regulatory body and has legal identity, known as an incorporated company. In

order to raise finance for business expansion of these forms of organizations, there are

sources of finance available which are enumerated below:

Equity financing: Most of the companies are using such source of finance in order to

raise firm from the market. According to the source organisation issues shares through

IPO and FPO process (Ranjan, 2016). The shares are purchased by investors known

as shareholders and the amount is using for expanding company. It is widely used

source in order to raise fund through external markets. It is beneficial for the company

because it helps to increase stockholders as well as investment in the company. On the

other side if firm issues preference shares then it must give dividend to shareholders

in every financial year. Further, it has to complete all the legal formalities as well as

listing in the stock market as well.

Bank loan: Another source of finance for incorporated companies is bank loan in

which the firm takes debt amount from commercial banks. It is widely used external

source of finance in order to raise fund in the organisation. As per the source the

company is most beneficial in terms of raising finance because it helps to analyses

valuation of the company in the market. On the other side it provides financial

services to the organisation when it has sufficient ability to pay debt. In case company

is not able to pay all the debts then bank has right to wind up overall firm.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Venture capital: As per the sources the business takes fund from venture capital

companies. There are many number of venture capital companies which are provide

facilities of finance to the incorporated businesses (Richards, 2015). It provides

amount of fund for expanding business when the company have sufficient return on

investment ratio. If it has not effective return then venture capitalist will not give such

facilities to the company. Apart from this it influences cash flow of the enterprise at

the end of an accounting period.

1.2 Implications of sources of finance on the firm

Internal sources of finance:

Name of source Financial

Implications

Legal Implications Dilution of control

Sales of assets In order to raise fund

through selling

unused assets, it

impacts on balance

of the firm where

assets are decreases.

There are not any

legal implications of

respective sources.

-

Personal savings Due to using

personal fund it not

affects on the

company (Salisbury,

2014).

Not any types of

legal implications are

there.

-

Retained earnings Here company is

reinvest the profit so

it leads to increase

sales in the firm.

Not any legal

formalities or

documentation

process is here.

No dilution of

control.

External sources of finance:

Name of source Financial

Implications

Legal Implications Dilution of control

Equity financing The business has to

give dividend from

profit of the firm to

the shareholders. So,

using the source

profitability is

decreases.

In case of raise fund

through equity, the

company has to

listing in the stock

market and then can

issues shares in the

market (Crosby and

Henneberry, 2016).

Control is with

shareholders because

the firm has to

involve shareholders

and they interfere in

order to take

decisions.

Bank loan The businessman has

to pay interest

amount as a cost of

finance to the bank.

Hence, it affects to

net profit in negative

Here organisation has

to complete

documentation

process, further bank

allows for loan.

Dilution of control is

not in the bank loan.

companies. There are many number of venture capital companies which are provide

facilities of finance to the incorporated businesses (Richards, 2015). It provides

amount of fund for expanding business when the company have sufficient return on

investment ratio. If it has not effective return then venture capitalist will not give such

facilities to the company. Apart from this it influences cash flow of the enterprise at

the end of an accounting period.

1.2 Implications of sources of finance on the firm

Internal sources of finance:

Name of source Financial

Implications

Legal Implications Dilution of control

Sales of assets In order to raise fund

through selling

unused assets, it

impacts on balance

of the firm where

assets are decreases.

There are not any

legal implications of

respective sources.

-

Personal savings Due to using

personal fund it not

affects on the

company (Salisbury,

2014).

Not any types of

legal implications are

there.

-

Retained earnings Here company is

reinvest the profit so

it leads to increase

sales in the firm.

Not any legal

formalities or

documentation

process is here.

No dilution of

control.

External sources of finance:

Name of source Financial

Implications

Legal Implications Dilution of control

Equity financing The business has to

give dividend from

profit of the firm to

the shareholders. So,

using the source

profitability is

decreases.

In case of raise fund

through equity, the

company has to

listing in the stock

market and then can

issues shares in the

market (Crosby and

Henneberry, 2016).

Control is with

shareholders because

the firm has to

involve shareholders

and they interfere in

order to take

decisions.

Bank loan The businessman has

to pay interest

amount as a cost of

finance to the bank.

Hence, it affects to

net profit in negative

Here organisation has

to complete

documentation

process, further bank

allows for loan.

Dilution of control is

not in the bank loan.

manner.

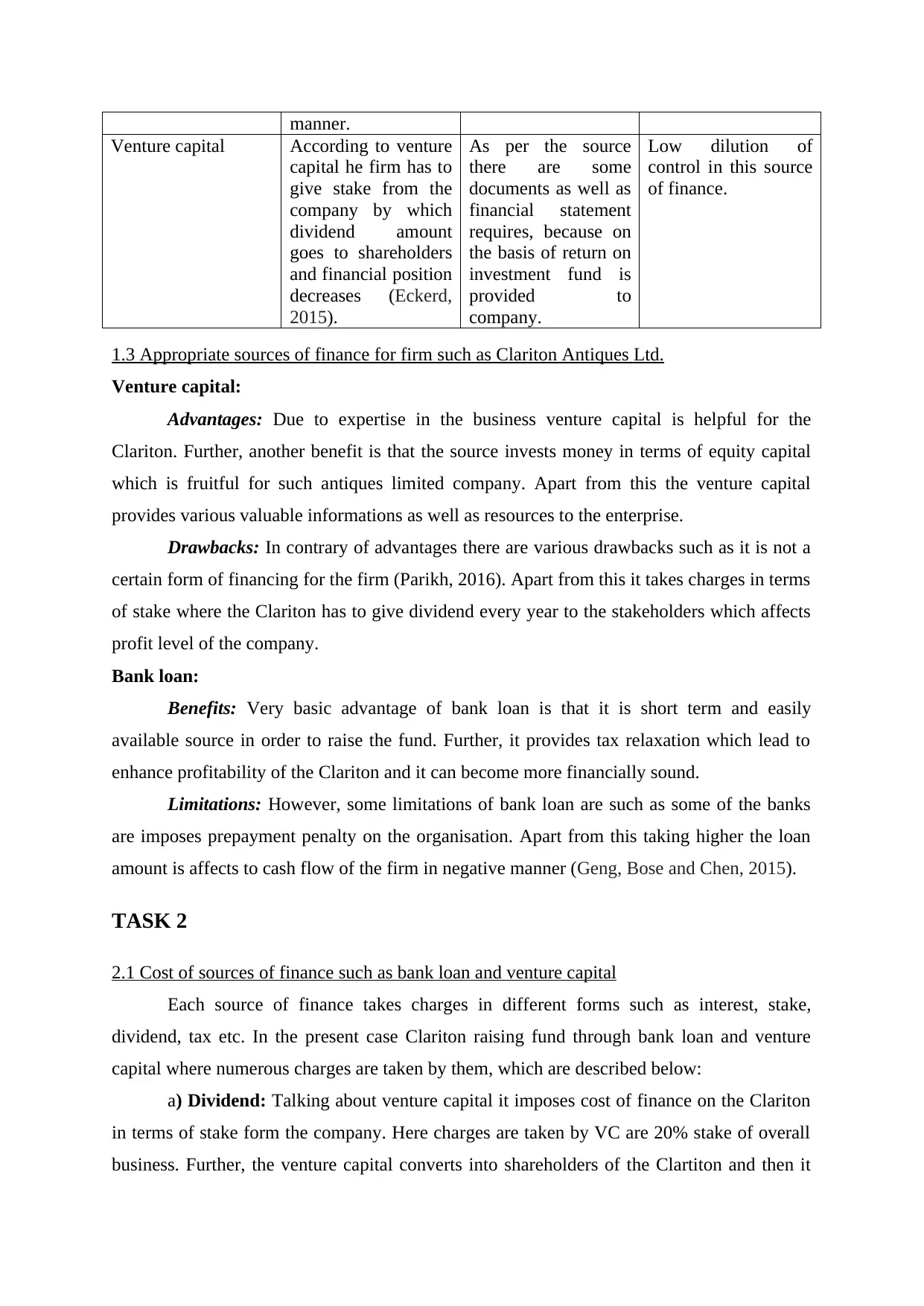

Venture capital According to venture

capital he firm has to

give stake from the

company by which

dividend amount

goes to shareholders

and financial position

decreases (Eckerd,

2015).

As per the source

there are some

documents as well as

financial statement

requires, because on

the basis of return on

investment fund is

provided to

company.

Low dilution of

control in this source

of finance.

1.3 Appropriate sources of finance for firm such as Clariton Antiques Ltd.

Venture capital:

Advantages: Due to expertise in the business venture capital is helpful for the

Clariton. Further, another benefit is that the source invests money in terms of equity capital

which is fruitful for such antiques limited company. Apart from this the venture capital

provides various valuable informations as well as resources to the enterprise.

Drawbacks: In contrary of advantages there are various drawbacks such as it is not a

certain form of financing for the firm (Parikh, 2016). Apart from this it takes charges in terms

of stake where the Clariton has to give dividend every year to the stakeholders which affects

profit level of the company.

Bank loan:

Benefits: Very basic advantage of bank loan is that it is short term and easily

available source in order to raise the fund. Further, it provides tax relaxation which lead to

enhance profitability of the Clariton and it can become more financially sound.

Limitations: However, some limitations of bank loan are such as some of the banks

are imposes prepayment penalty on the organisation. Apart from this taking higher the loan

amount is affects to cash flow of the firm in negative manner (Geng, Bose and Chen, 2015).

TASK 2

2.1 Cost of sources of finance such as bank loan and venture capital

Each source of finance takes charges in different forms such as interest, stake,

dividend, tax etc. In the present case Clariton raising fund through bank loan and venture

capital where numerous charges are taken by them, which are described below:

a) Dividend: Talking about venture capital it imposes cost of finance on the Clariton

in terms of stake form the company. Here charges are taken by VC are 20% stake of overall

business. Further, the venture capital converts into shareholders of the Clartiton and then it

Venture capital According to venture

capital he firm has to

give stake from the

company by which

dividend amount

goes to shareholders

and financial position

decreases (Eckerd,

2015).

As per the source

there are some

documents as well as

financial statement

requires, because on

the basis of return on

investment fund is

provided to

company.

Low dilution of

control in this source

of finance.

1.3 Appropriate sources of finance for firm such as Clariton Antiques Ltd.

Venture capital:

Advantages: Due to expertise in the business venture capital is helpful for the

Clariton. Further, another benefit is that the source invests money in terms of equity capital

which is fruitful for such antiques limited company. Apart from this the venture capital

provides various valuable informations as well as resources to the enterprise.

Drawbacks: In contrary of advantages there are various drawbacks such as it is not a

certain form of financing for the firm (Parikh, 2016). Apart from this it takes charges in terms

of stake where the Clariton has to give dividend every year to the stakeholders which affects

profit level of the company.

Bank loan:

Benefits: Very basic advantage of bank loan is that it is short term and easily

available source in order to raise the fund. Further, it provides tax relaxation which lead to

enhance profitability of the Clariton and it can become more financially sound.

Limitations: However, some limitations of bank loan are such as some of the banks

are imposes prepayment penalty on the organisation. Apart from this taking higher the loan

amount is affects to cash flow of the firm in negative manner (Geng, Bose and Chen, 2015).

TASK 2

2.1 Cost of sources of finance such as bank loan and venture capital

Each source of finance takes charges in different forms such as interest, stake,

dividend, tax etc. In the present case Clariton raising fund through bank loan and venture

capital where numerous charges are taken by them, which are described below:

a) Dividend: Talking about venture capital it imposes cost of finance on the Clariton

in terms of stake form the company. Here charges are taken by VC are 20% stake of overall

business. Further, the venture capital converts into shareholders of the Clartiton and then it

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

has to provide dividend amount to potential shareholders which lead to decrease profit of the

company (Greenbaum, Thakor and Boot, 2015).

b) & c) Interest and tax: Apart from the dividend, another source used by the

Clariton is bank loan where cost of finance is different from dividend. In terms of the bank

loan cost imposes on firm are in form of interest amount which is set out in the economy of

country. Higher the amount of loan is lead to charge higher interest amount. Moreover, there

is a broker who plays role of intermediary between Clariton and bank, known as finance

broker. It also takes charges in terms of percentage of overall loan amount. In the present case

bank imposes 2% interest amount or annual rate over the 10 financial years. On the other side

finance broker imposes cost of service is 1% brokerage amount of 0.5million GBP on the

Clariton.

Moreover, the company is beneficial in terms of tax amount due to provide taxation

allowances. As per the rules and regulations firm which raise fund from bank loan, it has not

require to pay tax amount which lead to enhance profitability of the business such as Clariton

(Matheson and et.al., 2016).

2.2 Importance of financial planning on the Clariton company

Financial plan is most important for the company for smooth functioning of the firm

in market. Significance of the plan for Clariton Antiques limited is enumerated below:

a) Budgeting: Budget is a process in order to forecast financial data for the future

accounting period on the basis of past financial position of the company. Hence, for estimate

future financial performance as well as formulate effective business strategies the financial

plan plays an integral role. If the company not use respective planning process then it is

unable to know future data. Finance organisation that have successfully revamped their

planning processes can today complete a forecast in two days or less and develop an annual

budget in less than three months. These organisations have reduced the time spent on lower

value planning activities and benefited from having prospective information and plan

available earlier in cycle to impact business performance.

b) Implications of failure to finance adequately: Further, adequate financial

resources are help to the business in order to run the company in a smooth way. Due to lack

of financial availability the entity is not able to produce better products and services as well

as run the organisation in proper manner. The management is able to manage and allocate

adequate finance with help of financial plan, so it is very significant (Fallon, 2014). In case of

failure of adequate finance it affects smooth functioning of the Clariton company adversely.

company (Greenbaum, Thakor and Boot, 2015).

b) & c) Interest and tax: Apart from the dividend, another source used by the

Clariton is bank loan where cost of finance is different from dividend. In terms of the bank

loan cost imposes on firm are in form of interest amount which is set out in the economy of

country. Higher the amount of loan is lead to charge higher interest amount. Moreover, there

is a broker who plays role of intermediary between Clariton and bank, known as finance

broker. It also takes charges in terms of percentage of overall loan amount. In the present case

bank imposes 2% interest amount or annual rate over the 10 financial years. On the other side

finance broker imposes cost of service is 1% brokerage amount of 0.5million GBP on the

Clariton.

Moreover, the company is beneficial in terms of tax amount due to provide taxation

allowances. As per the rules and regulations firm which raise fund from bank loan, it has not

require to pay tax amount which lead to enhance profitability of the business such as Clariton

(Matheson and et.al., 2016).

2.2 Importance of financial planning on the Clariton company

Financial plan is most important for the company for smooth functioning of the firm

in market. Significance of the plan for Clariton Antiques limited is enumerated below:

a) Budgeting: Budget is a process in order to forecast financial data for the future

accounting period on the basis of past financial position of the company. Hence, for estimate

future financial performance as well as formulate effective business strategies the financial

plan plays an integral role. If the company not use respective planning process then it is

unable to know future data. Finance organisation that have successfully revamped their

planning processes can today complete a forecast in two days or less and develop an annual

budget in less than three months. These organisations have reduced the time spent on lower

value planning activities and benefited from having prospective information and plan

available earlier in cycle to impact business performance.

b) Implications of failure to finance adequately: Further, adequate financial

resources are help to the business in order to run the company in a smooth way. Due to lack

of financial availability the entity is not able to produce better products and services as well

as run the organisation in proper manner. The management is able to manage and allocate

adequate finance with help of financial plan, so it is very significant (Fallon, 2014). In case of

failure of adequate finance it affects smooth functioning of the Clariton company adversely.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

If the company is not able to allocate adequate financial resources to the different

organisational functions then it leads to hamper smooth functioning of the overall Clariton

firm in an adverse manner. If company use this planning in its daily routine surely it can save

money and incurred where it is necessary to be used. This process helps entity to see its short-

term goals which company plan for a better future management.

c) Over trading: It is a situation where the firm enhance its products and services in

comparison to availability of resources and raw material. Overtrading is reduces profit of the

company as well as financial performance in the industry. The management can overcome

such situation using effective and appropriate financial plan where it able to control over the

extra cost and expenses as well as extra production level. It is necessary for the management

to reduce and overcome situation of over trading in the company. The Clariton requires to

control over the cost, needs to increase cash balance, increase account receivables etc. which

helps to overcome such situations. This process includes a large number of planning,

strategies, and policies which us in the future. Financial planning includes tax, education,

estate, investment, saving, risk, and cash-flow planning.

2.3 Information’s needed for the firm in order to take financial decisions

When an organisation is going to take business decisions in terms of finance then

collect or gather appropriate informations. Here the Clariton taking finance from venture

capital and bank loan where it requires necessary informations, which are shown below:

a) Partners: In order to take financial decisions with help of partners of business the

company needs informations such as proportion of the capital amount as well as profit will be

divided according to which one criteria. Further, it needs to take information related to

different rules and regulations impose by regulatory body on partnership business (Kumar

and Rao, 2016).

b) Venture capitalist (We Finance Limited): For raising finance from venture

capital firm such as We Finance Limited the Clariton need information related to various

documentation processes. Further the business needs to collect information for paying the

amount and cost of provided finance to the Clarriton. It is too much necessary to know

information related to cost or charges of the finance provided by the We Finance limited fir

of venture capital.

c) Finance Broker: Further, the business takes finance or fund from bank loan where

a person is hired by the firm who plays role as an intermediary among the bank as well as

organisational functions then it leads to hamper smooth functioning of the overall Clariton

firm in an adverse manner. If company use this planning in its daily routine surely it can save

money and incurred where it is necessary to be used. This process helps entity to see its short-

term goals which company plan for a better future management.

c) Over trading: It is a situation where the firm enhance its products and services in

comparison to availability of resources and raw material. Overtrading is reduces profit of the

company as well as financial performance in the industry. The management can overcome

such situation using effective and appropriate financial plan where it able to control over the

extra cost and expenses as well as extra production level. It is necessary for the management

to reduce and overcome situation of over trading in the company. The Clariton requires to

control over the cost, needs to increase cash balance, increase account receivables etc. which

helps to overcome such situations. This process includes a large number of planning,

strategies, and policies which us in the future. Financial planning includes tax, education,

estate, investment, saving, risk, and cash-flow planning.

2.3 Information’s needed for the firm in order to take financial decisions

When an organisation is going to take business decisions in terms of finance then

collect or gather appropriate informations. Here the Clariton taking finance from venture

capital and bank loan where it requires necessary informations, which are shown below:

a) Partners: In order to take financial decisions with help of partners of business the

company needs informations such as proportion of the capital amount as well as profit will be

divided according to which one criteria. Further, it needs to take information related to

different rules and regulations impose by regulatory body on partnership business (Kumar

and Rao, 2016).

b) Venture capitalist (We Finance Limited): For raising finance from venture

capital firm such as We Finance Limited the Clariton need information related to various

documentation processes. Further the business needs to collect information for paying the

amount and cost of provided finance to the Clarriton. It is too much necessary to know

information related to cost or charges of the finance provided by the We Finance limited fir

of venture capital.

c) Finance Broker: Further, the business takes finance or fund from bank loan where

a person is hired by the firm who plays role as an intermediary among the bank as well as

organisation. In such case the management requires to take information related to brokerage

charges which are taken by finance broker from the business entity.

2.4 Impact of various sources of finance on financial statement of Clariton Antiques Ltd.

When the company going to raise fund from various sources then it has to pay cost of

finance which lead to affect financial statement of Clariton in following way:

a) Venture capitalist (We Finance Limited): The We Finance Limited charges stake

of the firm and management has to pay dividend amount to its investors or shareholders. This

affects to the income statement in order to reduce total net profit as well as enhance level of

total expenditures in the financial year. On the other hand in the balance sheet assets will be

increase and total liabilities as well because venture capital treated in both side (Ranjan,

2016). Hence, expenses side increases in the profit and loss account as well as total liabilities

and assets of the Clariton will increase in the statement of financial position.

b) Finance broker: Another source is bank loan where it has to give interest from the

operating profit of Clariton. In this the amount of interest is an expense which goes to the

expense side of profit and loss statement by which it affects in negative manner. Apart from

this loan which is taken by the bank is transacted in the liabilities side as a bank loan which

shown in below mentioned balance sheet. Apart from this due to increasing capital assets also

enhances in the balance sheet.

Influences of both the financing sources used by the Clariton on its financial

statements are shown below:

Income Statement

Expenditures side Amount (in GBP) Profits side Amount (in GBP)

To Dividend on

shareholders a/c

xxx

To Interest on bank

loan a/c

xxx

To brokerage on

finance broker a/c

xxx

Balance sheet

Liabilities side Amount (in GBP) Assets side Amount (in GBP)

charges which are taken by finance broker from the business entity.

2.4 Impact of various sources of finance on financial statement of Clariton Antiques Ltd.

When the company going to raise fund from various sources then it has to pay cost of

finance which lead to affect financial statement of Clariton in following way:

a) Venture capitalist (We Finance Limited): The We Finance Limited charges stake

of the firm and management has to pay dividend amount to its investors or shareholders. This

affects to the income statement in order to reduce total net profit as well as enhance level of

total expenditures in the financial year. On the other hand in the balance sheet assets will be

increase and total liabilities as well because venture capital treated in both side (Ranjan,

2016). Hence, expenses side increases in the profit and loss account as well as total liabilities

and assets of the Clariton will increase in the statement of financial position.

b) Finance broker: Another source is bank loan where it has to give interest from the

operating profit of Clariton. In this the amount of interest is an expense which goes to the

expense side of profit and loss statement by which it affects in negative manner. Apart from

this loan which is taken by the bank is transacted in the liabilities side as a bank loan which

shown in below mentioned balance sheet. Apart from this due to increasing capital assets also

enhances in the balance sheet.

Influences of both the financing sources used by the Clariton on its financial

statements are shown below:

Income Statement

Expenditures side Amount (in GBP) Profits side Amount (in GBP)

To Dividend on

shareholders a/c

xxx

To Interest on bank

loan a/c

xxx

To brokerage on

finance broker a/c

xxx

Balance sheet

Liabilities side Amount (in GBP) Assets side Amount (in GBP)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

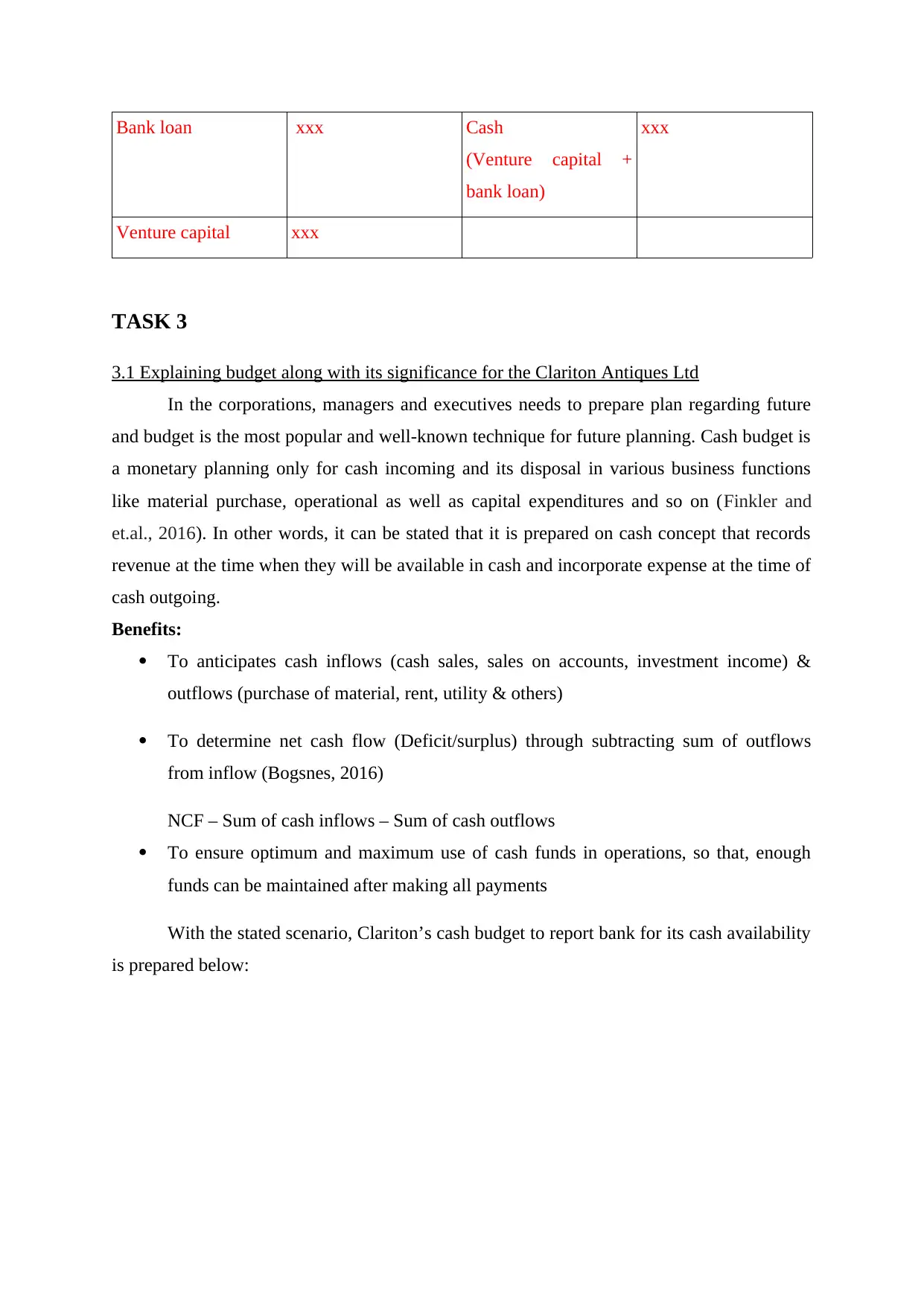

Bank loan xxx Cash

(Venture capital +

bank loan)

xxx

Venture capital xxx

TASK 3

3.1 Explaining budget along with its significance for the Clariton Antiques Ltd

In the corporations, managers and executives needs to prepare plan regarding future

and budget is the most popular and well-known technique for future planning. Cash budget is

a monetary planning only for cash incoming and its disposal in various business functions

like material purchase, operational as well as capital expenditures and so on (Finkler and

et.al., 2016). In other words, it can be stated that it is prepared on cash concept that records

revenue at the time when they will be available in cash and incorporate expense at the time of

cash outgoing.

Benefits:

To anticipates cash inflows (cash sales, sales on accounts, investment income) &

outflows (purchase of material, rent, utility & others)

To determine net cash flow (Deficit/surplus) through subtracting sum of outflows

from inflow (Bogsnes, 2016)

NCF – Sum of cash inflows – Sum of cash outflows

To ensure optimum and maximum use of cash funds in operations, so that, enough

funds can be maintained after making all payments

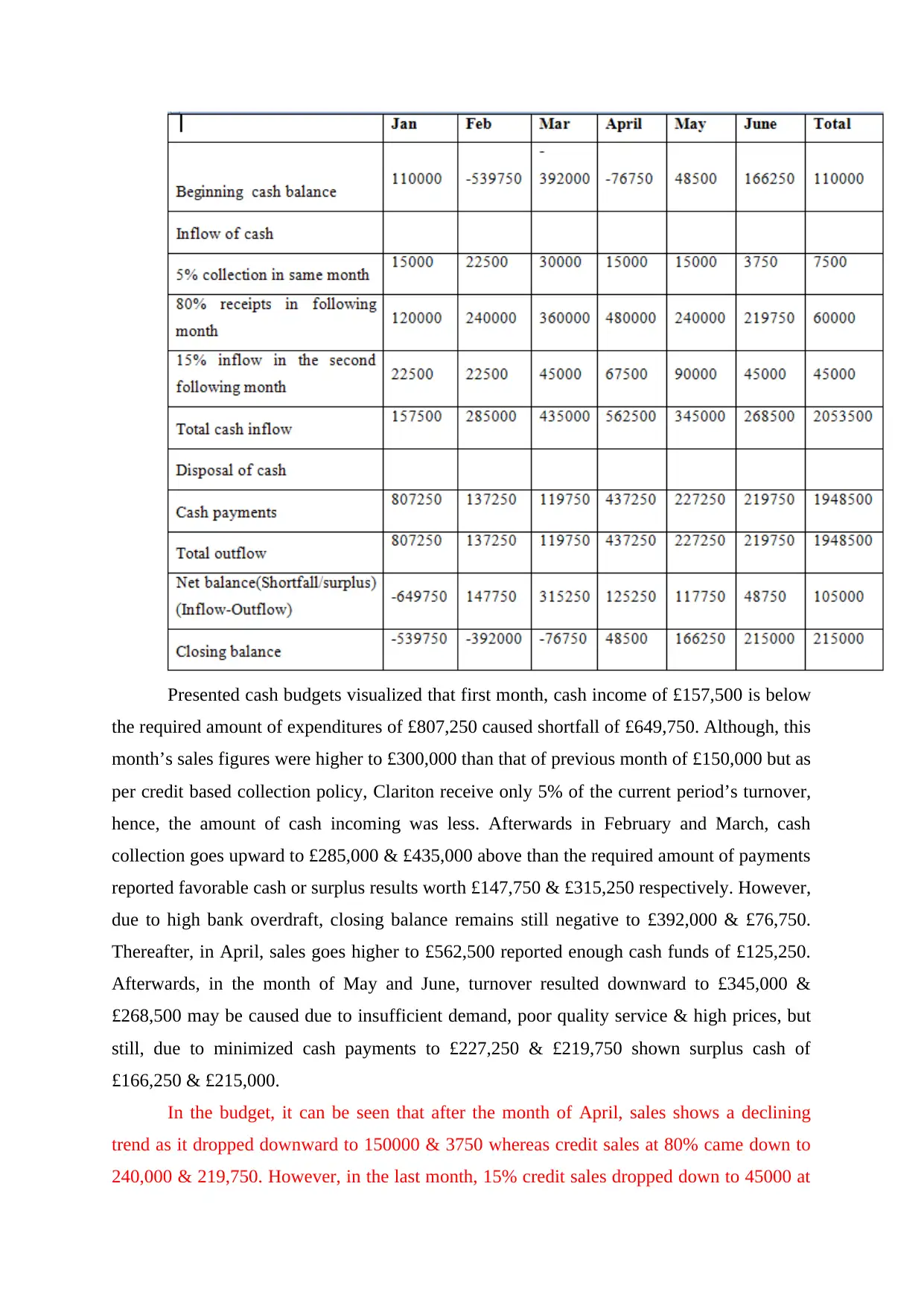

With the stated scenario, Clariton’s cash budget to report bank for its cash availability

is prepared below:

(Venture capital +

bank loan)

xxx

Venture capital xxx

TASK 3

3.1 Explaining budget along with its significance for the Clariton Antiques Ltd

In the corporations, managers and executives needs to prepare plan regarding future

and budget is the most popular and well-known technique for future planning. Cash budget is

a monetary planning only for cash incoming and its disposal in various business functions

like material purchase, operational as well as capital expenditures and so on (Finkler and

et.al., 2016). In other words, it can be stated that it is prepared on cash concept that records

revenue at the time when they will be available in cash and incorporate expense at the time of

cash outgoing.

Benefits:

To anticipates cash inflows (cash sales, sales on accounts, investment income) &

outflows (purchase of material, rent, utility & others)

To determine net cash flow (Deficit/surplus) through subtracting sum of outflows

from inflow (Bogsnes, 2016)

NCF – Sum of cash inflows – Sum of cash outflows

To ensure optimum and maximum use of cash funds in operations, so that, enough

funds can be maintained after making all payments

With the stated scenario, Clariton’s cash budget to report bank for its cash availability

is prepared below:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Presented cash budgets visualized that first month, cash income of £157,500 is below

the required amount of expenditures of £807,250 caused shortfall of £649,750. Although, this

month’s sales figures were higher to £300,000 than that of previous month of £150,000 but as

per credit based collection policy, Clariton receive only 5% of the current period’s turnover,

hence, the amount of cash incoming was less. Afterwards in February and March, cash

collection goes upward to £285,000 & £435,000 above than the required amount of payments

reported favorable cash or surplus results worth £147,750 & £315,250 respectively. However,

due to high bank overdraft, closing balance remains still negative to £392,000 & £76,750.

Thereafter, in April, sales goes higher to £562,500 reported enough cash funds of £125,250.

Afterwards, in the month of May and June, turnover resulted downward to £345,000 &

£268,500 may be caused due to insufficient demand, poor quality service & high prices, but

still, due to minimized cash payments to £227,250 & £219,750 shown surplus cash of

£166,250 & £215,000.

In the budget, it can be seen that after the month of April, sales shows a declining

trend as it dropped downward to 150000 & 3750 whereas credit sales at 80% came down to

240,000 & 219,750. However, in the last month, 15% credit sales dropped down to 45000 at

the required amount of expenditures of £807,250 caused shortfall of £649,750. Although, this

month’s sales figures were higher to £300,000 than that of previous month of £150,000 but as

per credit based collection policy, Clariton receive only 5% of the current period’s turnover,

hence, the amount of cash incoming was less. Afterwards in February and March, cash

collection goes upward to £285,000 & £435,000 above than the required amount of payments

reported favorable cash or surplus results worth £147,750 & £315,250 respectively. However,

due to high bank overdraft, closing balance remains still negative to £392,000 & £76,750.

Thereafter, in April, sales goes higher to £562,500 reported enough cash funds of £125,250.

Afterwards, in the month of May and June, turnover resulted downward to £345,000 &

£268,500 may be caused due to insufficient demand, poor quality service & high prices, but

still, due to minimized cash payments to £227,250 & £219,750 shown surplus cash of

£166,250 & £215,000.

In the budget, it can be seen that after the month of April, sales shows a declining

trend as it dropped downward to 150000 & 3750 whereas credit sales at 80% came down to

240,000 & 219,750. However, in the last month, 15% credit sales dropped down to 45000 at

a lower cash revenue worth 268500. On the contrary, to this, sudden and rapid increase in the

month of April to 437250 is a sign of heavy cash payments. It may be due to higher supplier

charges, poor controlling over the operations and so on resulted less net balance worth

125250. Moreover, after the period, it shows a declining trend to 117750 & 48750, although,

cash payments came down still less revenue is the reason behind insufficient cash. It indicates

that in future, Clariton may face problems due to cash shortage to carry out regular

operations.

Recommendations to combat shortfall:

Policymaker needs to alter its credit collection procedures to promote and boost cash

sales and minimize the percentage of sales on account (George, Irwin and Reuvid,

2016). Here, it must be noted that total turnover should not be reduced otherwise;

profitability of the firm will come down. Clariton’s credit policy should be changed to

reduce extensive credit to the receivables & encourage sales on immediate cash

receipts to improve cash incoming.

Advertisement, cash discounting offers, promotional policy needs to be focused to

attract high-yielding consumers and maximize net profitability. It is because, in order

to get discounts, end-users will be ready or willing to purchase goods on cash basis so

that payments can be reduced.

Expenditures should be controlled through proper utilization and minimizing wastage.

In such respect, managers must consistently look to the regular business functions

carrying out by their subordinates and make appropriate plans to allign all the regular

functioning with the set targets so that goals can be attained.

3.2 Computation of cost and pricing decisions

Fixed cost refers to the expenditures that remains constant over and have no relations

with the goods produced and service delivered. However, in contrast to this, variable

expenditures are regarded as payments that are directly related to the productions and

services delivery system (Rehan and et.al., 2016). With reference to chosen scenario, it

specializes in antiques delivery, henceforth; it can compute cost as follows:

Designing: £20000

Labor cost: £8000

Marketing: £5000

Electricity: £2000

month of April to 437250 is a sign of heavy cash payments. It may be due to higher supplier

charges, poor controlling over the operations and so on resulted less net balance worth

125250. Moreover, after the period, it shows a declining trend to 117750 & 48750, although,

cash payments came down still less revenue is the reason behind insufficient cash. It indicates

that in future, Clariton may face problems due to cash shortage to carry out regular

operations.

Recommendations to combat shortfall:

Policymaker needs to alter its credit collection procedures to promote and boost cash

sales and minimize the percentage of sales on account (George, Irwin and Reuvid,

2016). Here, it must be noted that total turnover should not be reduced otherwise;

profitability of the firm will come down. Clariton’s credit policy should be changed to

reduce extensive credit to the receivables & encourage sales on immediate cash

receipts to improve cash incoming.

Advertisement, cash discounting offers, promotional policy needs to be focused to

attract high-yielding consumers and maximize net profitability. It is because, in order

to get discounts, end-users will be ready or willing to purchase goods on cash basis so

that payments can be reduced.

Expenditures should be controlled through proper utilization and minimizing wastage.

In such respect, managers must consistently look to the regular business functions

carrying out by their subordinates and make appropriate plans to allign all the regular

functioning with the set targets so that goals can be attained.

3.2 Computation of cost and pricing decisions

Fixed cost refers to the expenditures that remains constant over and have no relations

with the goods produced and service delivered. However, in contrast to this, variable

expenditures are regarded as payments that are directly related to the productions and

services delivery system (Rehan and et.al., 2016). With reference to chosen scenario, it

specializes in antiques delivery, henceforth; it can compute cost as follows:

Designing: £20000

Labor cost: £8000

Marketing: £5000

Electricity: £2000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.