Financial Performance Analysis: Contribution and Investment Decisions

VerifiedAdded on 2022/09/07

|9

|1717

|21

Report

AI Summary

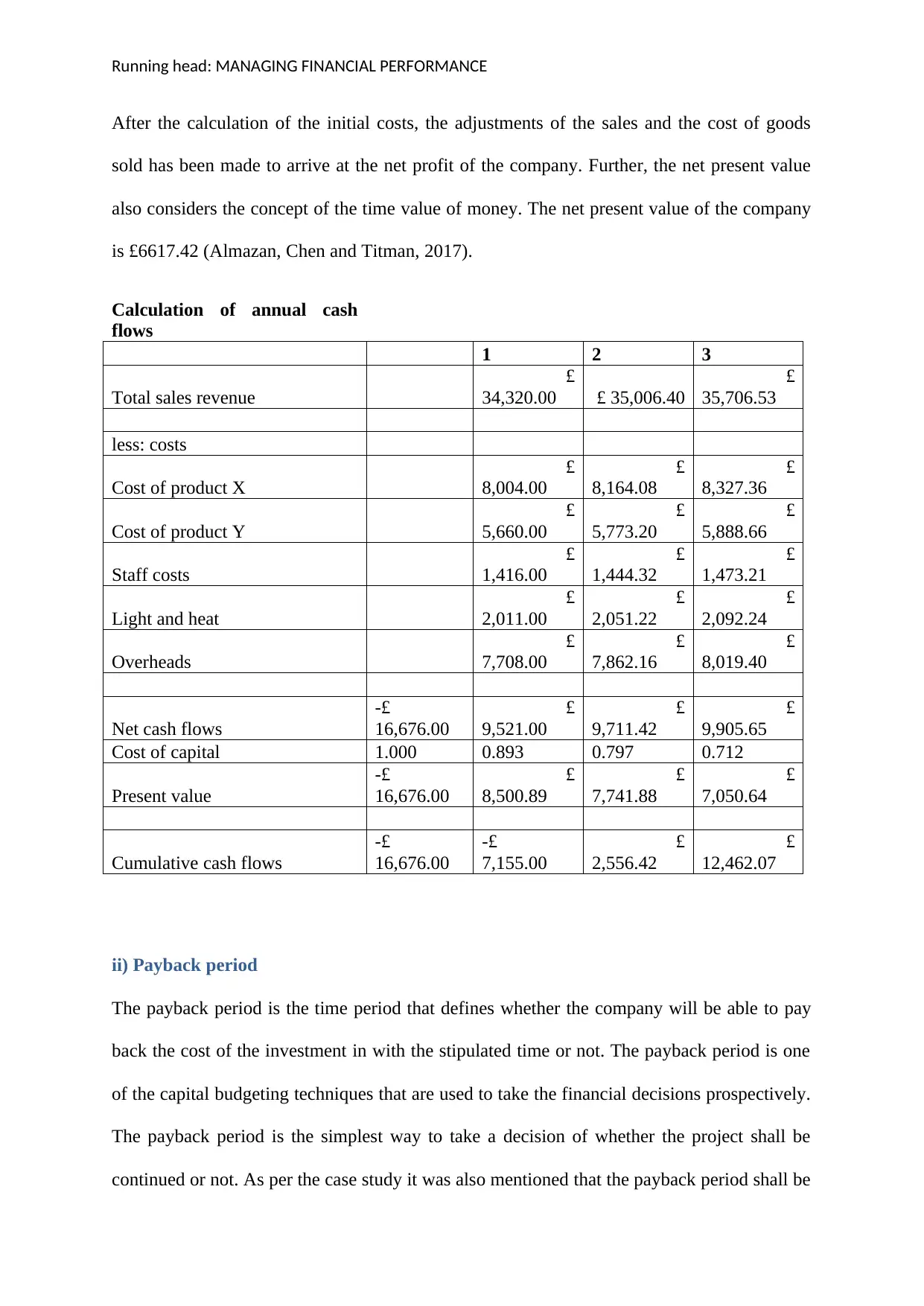

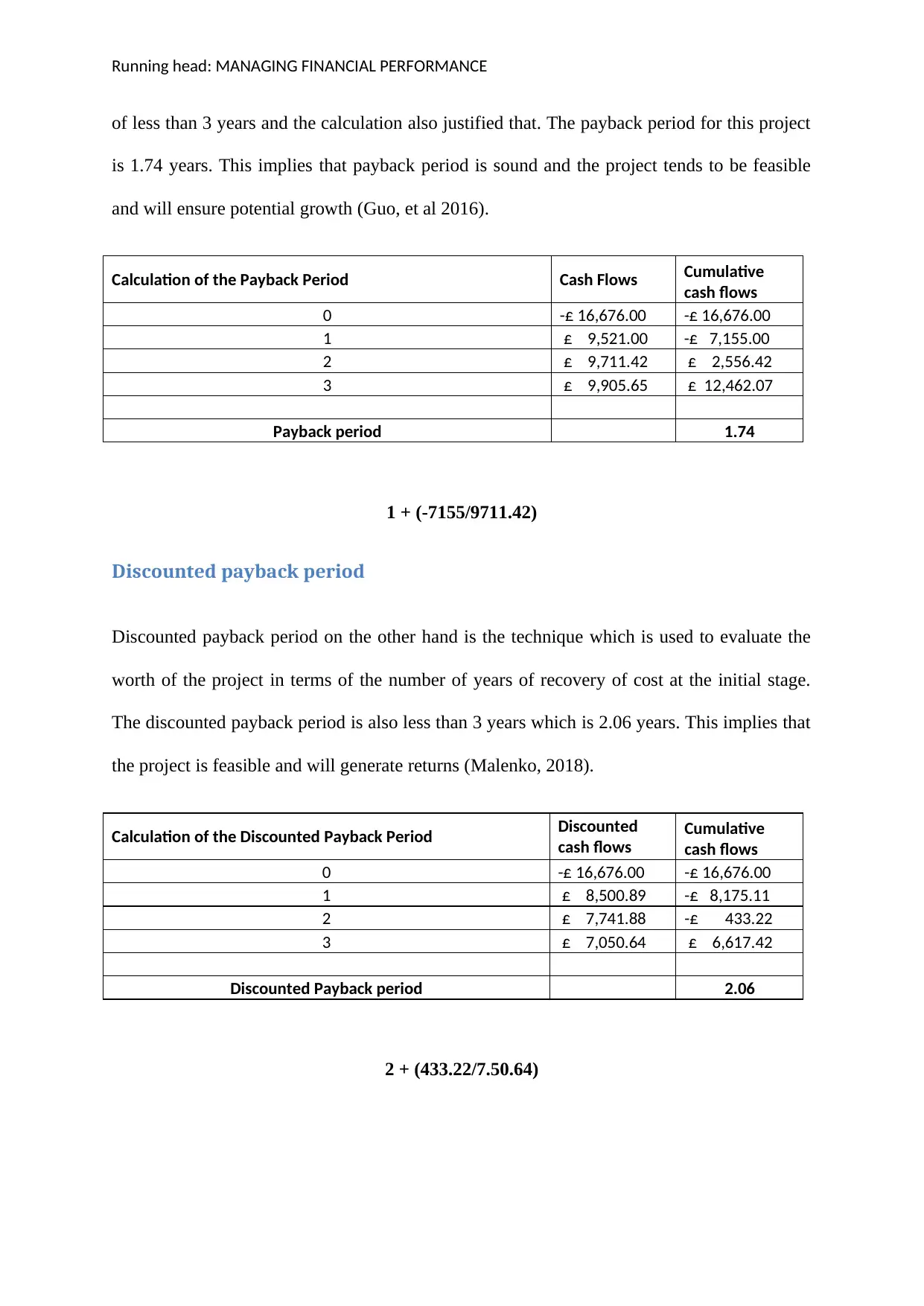

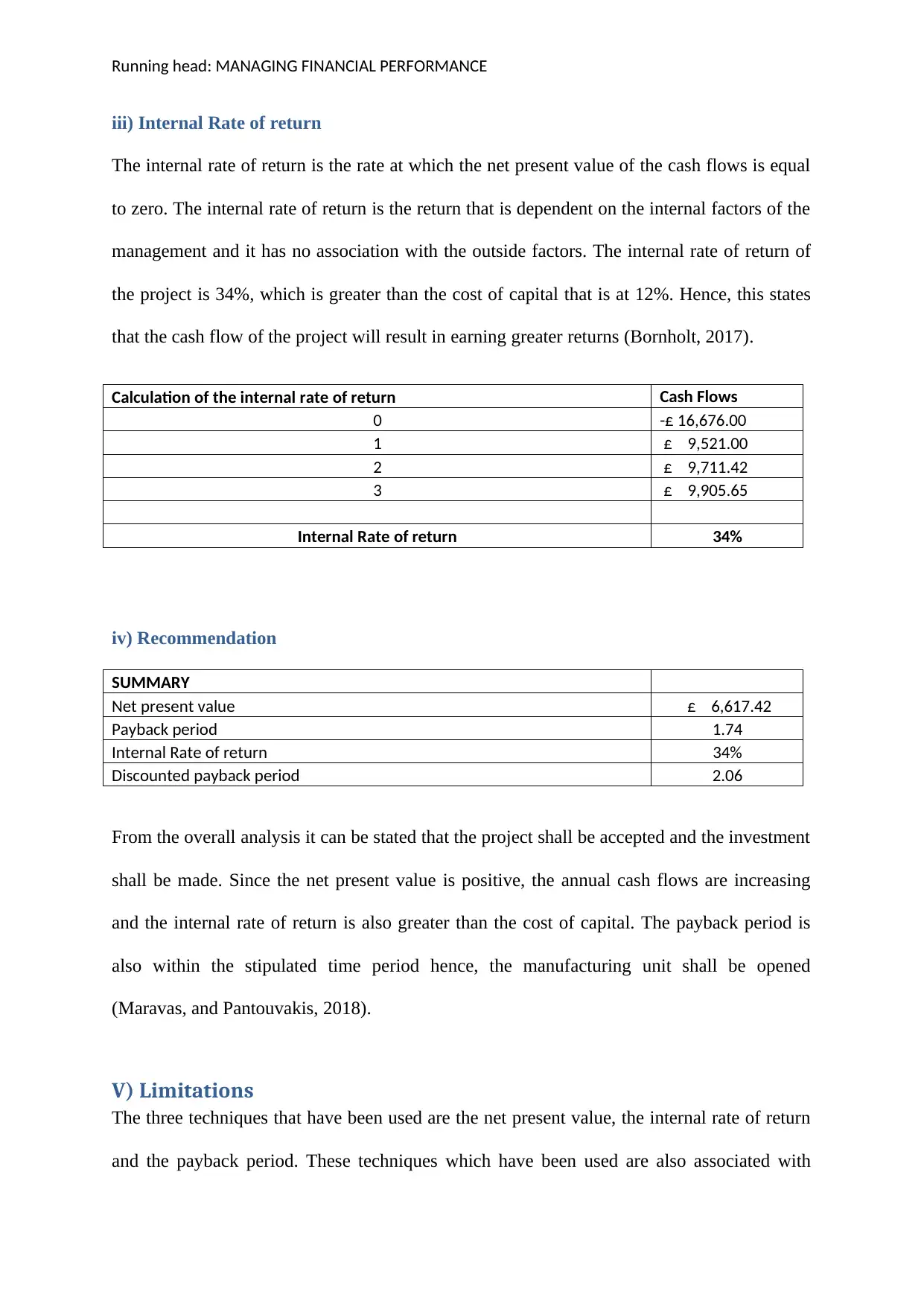

This report presents a comprehensive financial analysis of a company's performance, focusing on product profitability and investment appraisal. The analysis begins with calculating the contribution of each product (X, Y, and Z), considering sales and variable costs, and evaluating whether the company should cease production of certain products based on their contribution margins and impact on overall profitability. The report then delves into capital budgeting techniques, including the calculation of net present value (NPV), payback period, discounted payback period, and internal rate of return (IRR) for a potential investment. The analysis evaluates the feasibility of the investment by comparing these metrics against the cost of capital and other benchmarks. The report concludes with recommendations regarding the investment decision and acknowledges the limitations of the methods employed, providing a well-rounded perspective on financial decision-making.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.