Analysis of Financial Principles and Techniques for Business Growth

VerifiedAdded on 2020/07/22

|28

|9716

|47

Report

AI Summary

This report delves into the application of financial principles and techniques to enhance organizational performance. It begins by examining various costing and pricing strategies, including profit drivers, value-based pricing, and competitive analysis, using a hotel revenue example to illustrate their impact. The report then explores the design of costing systems, emphasizing direct cost methods and their role in financial health. Forecasting techniques are discussed in relation to revenue and cost decisions, alongside an analysis of fund availability. Budgetary control, including variance analysis and monitoring processes, is presented. Furthermore, the report covers cost management processes, including activity-based costing, and financial appraisal techniques for strategic investment decisions, with a focus on post-audit appraisals. Finally, the report concludes with an analysis of financial ratios and recommendations for strategic portfolio management to ensure the firm's financial viability and growth.

Managing Financial

Principles and Techniques

Principles and Techniques

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Determining the costs in the pricing strategy of a company............................................1

1.2 Designing a costing system for a firm..............................................................................5

1.3 Evaluating the costing and pricing techniques for business.............................................7

TASK 2............................................................................................................................................7

2.1 Application of forecasting techniques to enhance the costs and revenue decisions for firms

................................................................................................................................................7

2.2 Analysing the availability of funds for the business operations.......................................9

TASK 3..........................................................................................................................................10

3.1.........................................................................................................................................10

3.2.........................................................................................................................................10

3.3 Comparison of actual expenditures with the master budget...........................................11

3.4 Determining the budgetary monitoring process in an entity..........................................12

TASK 4..........................................................................................................................................13

4.1 Presenting the process for cost management in entity....................................................13

4.2 Determining the use of activity based costing method...................................................15

TASK 5..........................................................................................................................................17

5.1 Application of the financial appraisal techniques..........................................................17

5.2 Justifying the strategic investment decisions for organisation.......................................19

5.3 Reporting the appropriateness of strategic investment decision by implicating the post

audit appraisal.......................................................................................................................20

TASK 6..........................................................................................................................................20

6.1 Analysing the data set to determine the financing viability of firm...............................20

2. Computation of financial ratios........................................................................................21

6.3 Recommending the strategic portfolio of the organisation............................................22

CONCLUSION..............................................................................................................................23

REFERENCES..............................................................................................................................24

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Determining the costs in the pricing strategy of a company............................................1

1.2 Designing a costing system for a firm..............................................................................5

1.3 Evaluating the costing and pricing techniques for business.............................................7

TASK 2............................................................................................................................................7

2.1 Application of forecasting techniques to enhance the costs and revenue decisions for firms

................................................................................................................................................7

2.2 Analysing the availability of funds for the business operations.......................................9

TASK 3..........................................................................................................................................10

3.1.........................................................................................................................................10

3.2.........................................................................................................................................10

3.3 Comparison of actual expenditures with the master budget...........................................11

3.4 Determining the budgetary monitoring process in an entity..........................................12

TASK 4..........................................................................................................................................13

4.1 Presenting the process for cost management in entity....................................................13

4.2 Determining the use of activity based costing method...................................................15

TASK 5..........................................................................................................................................17

5.1 Application of the financial appraisal techniques..........................................................17

5.2 Justifying the strategic investment decisions for organisation.......................................19

5.3 Reporting the appropriateness of strategic investment decision by implicating the post

audit appraisal.......................................................................................................................20

TASK 6..........................................................................................................................................20

6.1 Analysing the data set to determine the financing viability of firm...............................20

2. Computation of financial ratios........................................................................................21

6.3 Recommending the strategic portfolio of the organisation............................................22

CONCLUSION..............................................................................................................................23

REFERENCES..............................................................................................................................24

INTRODUCTION

The motive behind presenting principles and techniques that will be fruitful for enhancing

the performance of organisation. In there present report there will be determination and analysis

of various costing principles and techniques which are need to be implement by a firm.

Therefore, such techniques will be helpful in terms of enhancing the performance, efficiency as

well as revenue gathering of the entities. Allocating the costs to any task and operations will help

firm in estimating the required level of funds for the business operations. Therefore, on the other

side it can be said that with the help of such analysis the business will have adequate amount of

revenue generation and tat will be helpful for further industrial activities. The report also

contains various forecasting techniques which will help the managerial professionals in any

organisation in terms of revenue decisions as well as determine the availability of the funds for

the further organisational activities.

There will be presentation of appropriate budgetary targets and the preparation of master

budgets that will be helpful for the growth of entity as well as fund generation of the business.

Therefore, these methods will be helpful for the venture in context with investment decisions and

profitability of the projects. Analysing and interpreting the reports will be fruitful as to enhance

the operations of the firm. To analyse the costs it will be beneficial for the firm in terms of

pricing decision, setting the organisational objectives and analysing the profitability from such

tasks. It will also help the business in proper management, adequate utilisation of the resources

such as men, material, machineries and funds.

TASK 1

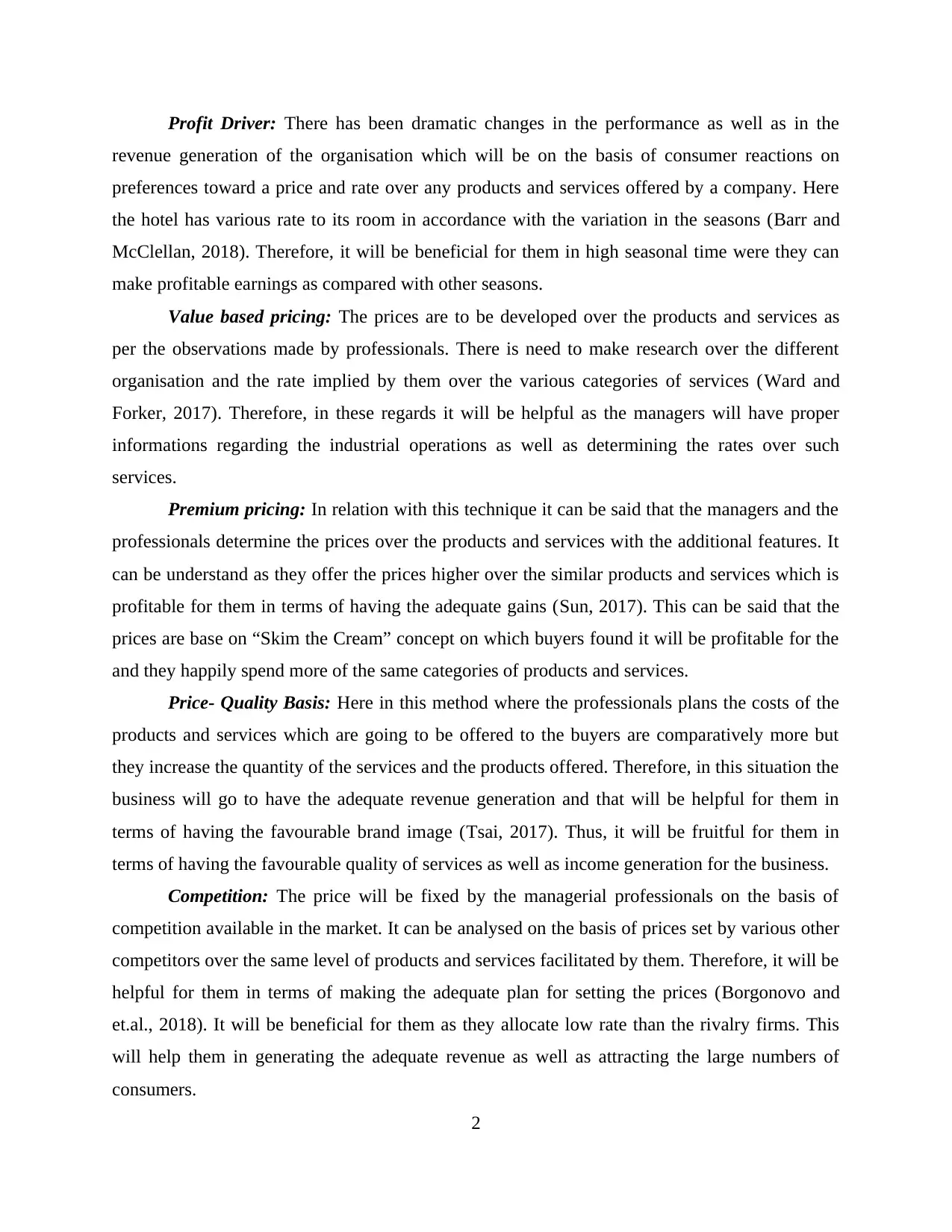

1.1 Determining the costs in the pricing strategy of a company

In accordance with allocating the costs to the business activities which will be beneficial

in terms of analysing the profits from such operations as well as the ability of firm in terms of

meeting such expenditures. Therefore, in these regards the firm need to make effective pricing

decision which will be appropriate to meet the demands of firm as well as helpful in revenue

generation. The rates over products and services must be affordable by the consumers as well as

it will be profitable for the entity in terms of attaining the proper revenue on the long term basis.

However, there has been various techniques and methods that will help them in allocating the

prices to the products and services such as:

1

The motive behind presenting principles and techniques that will be fruitful for enhancing

the performance of organisation. In there present report there will be determination and analysis

of various costing principles and techniques which are need to be implement by a firm.

Therefore, such techniques will be helpful in terms of enhancing the performance, efficiency as

well as revenue gathering of the entities. Allocating the costs to any task and operations will help

firm in estimating the required level of funds for the business operations. Therefore, on the other

side it can be said that with the help of such analysis the business will have adequate amount of

revenue generation and tat will be helpful for further industrial activities. The report also

contains various forecasting techniques which will help the managerial professionals in any

organisation in terms of revenue decisions as well as determine the availability of the funds for

the further organisational activities.

There will be presentation of appropriate budgetary targets and the preparation of master

budgets that will be helpful for the growth of entity as well as fund generation of the business.

Therefore, these methods will be helpful for the venture in context with investment decisions and

profitability of the projects. Analysing and interpreting the reports will be fruitful as to enhance

the operations of the firm. To analyse the costs it will be beneficial for the firm in terms of

pricing decision, setting the organisational objectives and analysing the profitability from such

tasks. It will also help the business in proper management, adequate utilisation of the resources

such as men, material, machineries and funds.

TASK 1

1.1 Determining the costs in the pricing strategy of a company

In accordance with allocating the costs to the business activities which will be beneficial

in terms of analysing the profits from such operations as well as the ability of firm in terms of

meeting such expenditures. Therefore, in these regards the firm need to make effective pricing

decision which will be appropriate to meet the demands of firm as well as helpful in revenue

generation. The rates over products and services must be affordable by the consumers as well as

it will be profitable for the entity in terms of attaining the proper revenue on the long term basis.

However, there has been various techniques and methods that will help them in allocating the

prices to the products and services such as:

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Profit Driver: There has been dramatic changes in the performance as well as in the

revenue generation of the organisation which will be on the basis of consumer reactions on

preferences toward a price and rate over any products and services offered by a company. Here

the hotel has various rate to its room in accordance with the variation in the seasons (Barr and

McClellan, 2018). Therefore, it will be beneficial for them in high seasonal time were they can

make profitable earnings as compared with other seasons.

Value based pricing: The prices are to be developed over the products and services as

per the observations made by professionals. There is need to make research over the different

organisation and the rate implied by them over the various categories of services (Ward and

Forker, 2017). Therefore, in these regards it will be helpful as the managers will have proper

informations regarding the industrial operations as well as determining the rates over such

services.

Premium pricing: In relation with this technique it can be said that the managers and the

professionals determine the prices over the products and services with the additional features. It

can be understand as they offer the prices higher over the similar products and services which is

profitable for them in terms of having the adequate gains (Sun, 2017). This can be said that the

prices are base on “Skim the Cream” concept on which buyers found it will be profitable for the

and they happily spend more of the same categories of products and services.

Price- Quality Basis: Here in this method where the professionals plans the costs of the

products and services which are going to be offered to the buyers are comparatively more but

they increase the quantity of the services and the products offered. Therefore, in this situation the

business will go to have the adequate revenue generation and that will be helpful for them in

terms of having the favourable brand image (Tsai, 2017). Thus, it will be fruitful for them in

terms of having the favourable quality of services as well as income generation for the business.

Competition: The price will be fixed by the managerial professionals on the basis of

competition available in the market. It can be analysed on the basis of prices set by various other

competitors over the same level of products and services facilitated by them. Therefore, it will be

helpful for them in terms of making the adequate plan for setting the prices (Borgonovo and

et.al., 2018). It will be beneficial for them as they allocate low rate than the rivalry firms. This

will help them in generating the adequate revenue as well as attracting the large numbers of

consumers.

2

revenue generation of the organisation which will be on the basis of consumer reactions on

preferences toward a price and rate over any products and services offered by a company. Here

the hotel has various rate to its room in accordance with the variation in the seasons (Barr and

McClellan, 2018). Therefore, it will be beneficial for them in high seasonal time were they can

make profitable earnings as compared with other seasons.

Value based pricing: The prices are to be developed over the products and services as

per the observations made by professionals. There is need to make research over the different

organisation and the rate implied by them over the various categories of services (Ward and

Forker, 2017). Therefore, in these regards it will be helpful as the managers will have proper

informations regarding the industrial operations as well as determining the rates over such

services.

Premium pricing: In relation with this technique it can be said that the managers and the

professionals determine the prices over the products and services with the additional features. It

can be understand as they offer the prices higher over the similar products and services which is

profitable for them in terms of having the adequate gains (Sun, 2017). This can be said that the

prices are base on “Skim the Cream” concept on which buyers found it will be profitable for the

and they happily spend more of the same categories of products and services.

Price- Quality Basis: Here in this method where the professionals plans the costs of the

products and services which are going to be offered to the buyers are comparatively more but

they increase the quantity of the services and the products offered. Therefore, in this situation the

business will go to have the adequate revenue generation and that will be helpful for them in

terms of having the favourable brand image (Tsai, 2017). Thus, it will be fruitful for them in

terms of having the favourable quality of services as well as income generation for the business.

Competition: The price will be fixed by the managerial professionals on the basis of

competition available in the market. It can be analysed on the basis of prices set by various other

competitors over the same level of products and services facilitated by them. Therefore, it will be

helpful for them in terms of making the adequate plan for setting the prices (Borgonovo and

et.al., 2018). It will be beneficial for them as they allocate low rate than the rivalry firms. This

will help them in generating the adequate revenue as well as attracting the large numbers of

consumers.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

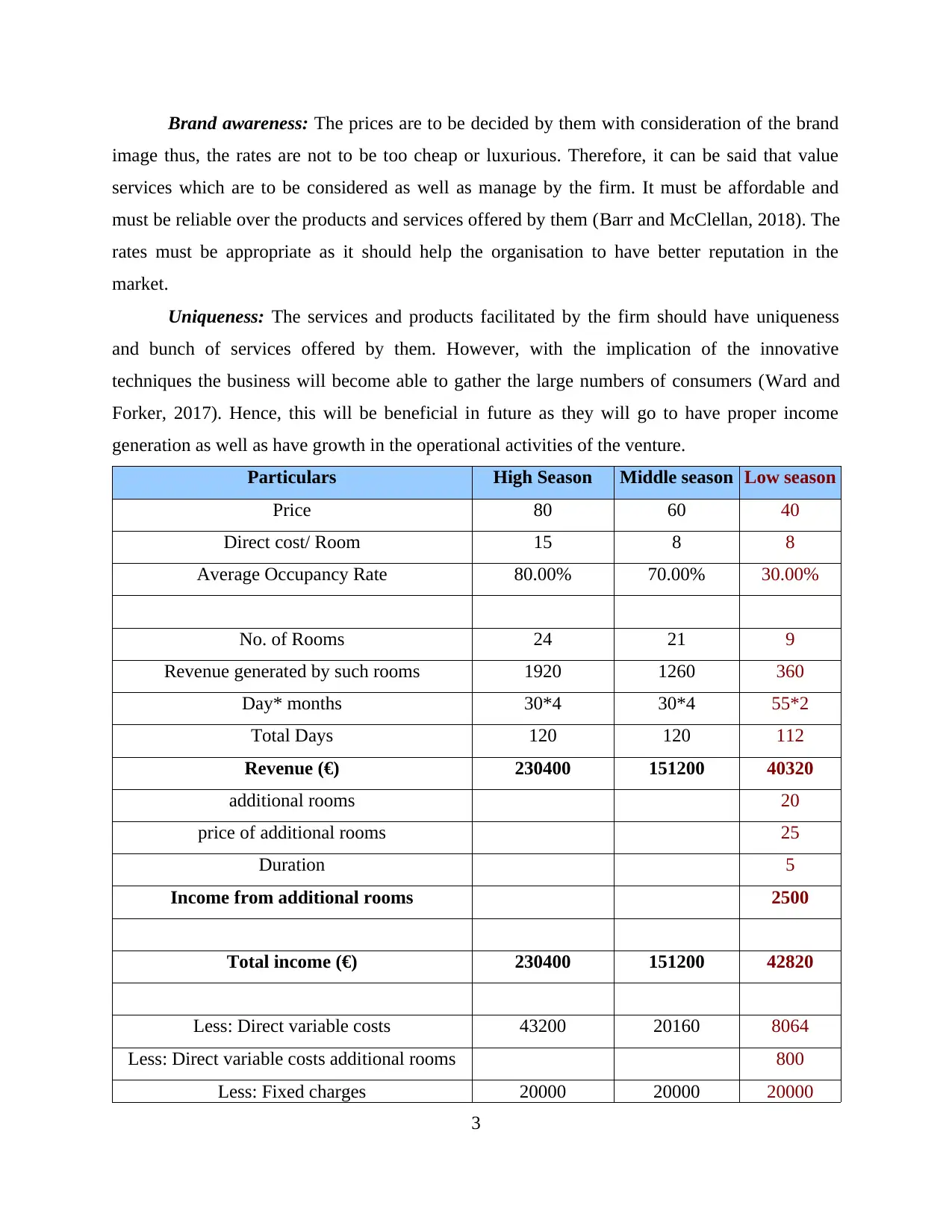

Brand awareness: The prices are to be decided by them with consideration of the brand

image thus, the rates are not to be too cheap or luxurious. Therefore, it can be said that value

services which are to be considered as well as manage by the firm. It must be affordable and

must be reliable over the products and services offered by them (Barr and McClellan, 2018). The

rates must be appropriate as it should help the organisation to have better reputation in the

market.

Uniqueness: The services and products facilitated by the firm should have uniqueness

and bunch of services offered by them. However, with the implication of the innovative

techniques the business will become able to gather the large numbers of consumers (Ward and

Forker, 2017). Hence, this will be beneficial in future as they will go to have proper income

generation as well as have growth in the operational activities of the venture.

Particulars High Season Middle season Low season

Price 80 60 40

Direct cost/ Room 15 8 8

Average Occupancy Rate 80.00% 70.00% 30.00%

No. of Rooms 24 21 9

Revenue generated by such rooms 1920 1260 360

Day* months 30*4 30*4 55*2

Total Days 120 120 112

Revenue (€) 230400 151200 40320

additional rooms 20

price of additional rooms 25

Duration 5

Income from additional rooms 2500

Total income (€) 230400 151200 42820

Less: Direct variable costs 43200 20160 8064

Less: Direct variable costs additional rooms 800

Less: Fixed charges 20000 20000 20000

3

image thus, the rates are not to be too cheap or luxurious. Therefore, it can be said that value

services which are to be considered as well as manage by the firm. It must be affordable and

must be reliable over the products and services offered by them (Barr and McClellan, 2018). The

rates must be appropriate as it should help the organisation to have better reputation in the

market.

Uniqueness: The services and products facilitated by the firm should have uniqueness

and bunch of services offered by them. However, with the implication of the innovative

techniques the business will become able to gather the large numbers of consumers (Ward and

Forker, 2017). Hence, this will be beneficial in future as they will go to have proper income

generation as well as have growth in the operational activities of the venture.

Particulars High Season Middle season Low season

Price 80 60 40

Direct cost/ Room 15 8 8

Average Occupancy Rate 80.00% 70.00% 30.00%

No. of Rooms 24 21 9

Revenue generated by such rooms 1920 1260 360

Day* months 30*4 30*4 55*2

Total Days 120 120 112

Revenue (€) 230400 151200 40320

additional rooms 20

price of additional rooms 25

Duration 5

Income from additional rooms 2500

Total income (€) 230400 151200 42820

Less: Direct variable costs 43200 20160 8064

Less: Direct variable costs additional rooms 800

Less: Fixed charges 20000 20000 20000

3

Profit (€) 167200 111040 13956

Interpretation: In accordance with the above mentioned table it can be said that the

managers has planned to allocate prices over the numbers of rooms on the basis of different

seasons. However, it will be fruitful for them in terms of attaining the adequate amount of

revenue as well as gaining the fruitful gains. As per the profits generated in the high season

which is competitively higher than the other seasons. Here the professionals has fixed the costs

over services such as 80 per rooms on the with 80% of occupancy that means 24 rooms are being

reserved out of 30. There will be direct variance costs of 15 per room and the revenue will be

determine on the basis of days. This was fixed by them as per month they will estimate the costs

over the rooms on the basis of 30 days. Therefore, in the high season the period was of 4 months

and during that period the income was being gathered by them for 230400. The variable cost of

43200 and the fixed cost of 20000 will be reduced and the net profit has been generated by them

as 167200.

On the other side, The middle season also has the period for 4 months and at the rate of

60 per room. There has been occupancy of 21 rooms during that season which has facilitated the

revenue of 151200. The direct variance cost of 20160 as 8 per room has been deducted from the

revenue with fixed charges of 200000. Therefore, the total profit earned by the firm is amounted

to 111040. The profit gathered during this period is comparatively lower than higher season.

However, In accordance with the low season the prices are too cheap as compared with

the other seasons such as 40 and with the same direct cost as in middle season for 8 per room.

There is 30% of occupancy which means 9 rooms were booked during this season. As per the

additional information there has requirements of 20 rooms for 5 days. Therefore, the 9 rooms has

been occupied for the period of 55 days at the rate of 40 per room as well as the direct variance

costs for 8 per room on the same period. In the 5 days of November the 20 rooms were booked

on comparatively low rate such as 25 per room and which amounted to 2500. However, after

analysing all the direct variances and fixed charges over it the net profit will be analysed as

13956 for the low season.

4

Interpretation: In accordance with the above mentioned table it can be said that the

managers has planned to allocate prices over the numbers of rooms on the basis of different

seasons. However, it will be fruitful for them in terms of attaining the adequate amount of

revenue as well as gaining the fruitful gains. As per the profits generated in the high season

which is competitively higher than the other seasons. Here the professionals has fixed the costs

over services such as 80 per rooms on the with 80% of occupancy that means 24 rooms are being

reserved out of 30. There will be direct variance costs of 15 per room and the revenue will be

determine on the basis of days. This was fixed by them as per month they will estimate the costs

over the rooms on the basis of 30 days. Therefore, in the high season the period was of 4 months

and during that period the income was being gathered by them for 230400. The variable cost of

43200 and the fixed cost of 20000 will be reduced and the net profit has been generated by them

as 167200.

On the other side, The middle season also has the period for 4 months and at the rate of

60 per room. There has been occupancy of 21 rooms during that season which has facilitated the

revenue of 151200. The direct variance cost of 20160 as 8 per room has been deducted from the

revenue with fixed charges of 200000. Therefore, the total profit earned by the firm is amounted

to 111040. The profit gathered during this period is comparatively lower than higher season.

However, In accordance with the low season the prices are too cheap as compared with

the other seasons such as 40 and with the same direct cost as in middle season for 8 per room.

There is 30% of occupancy which means 9 rooms were booked during this season. As per the

additional information there has requirements of 20 rooms for 5 days. Therefore, the 9 rooms has

been occupied for the period of 55 days at the rate of 40 per room as well as the direct variance

costs for 8 per room on the same period. In the 5 days of November the 20 rooms were booked

on comparatively low rate such as 25 per room and which amounted to 2500. However, after

analysing all the direct variances and fixed charges over it the net profit will be analysed as

13956 for the low season.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Therefore, after analysing the profits earned by hotel in all the period which is helpful for

them in terms of earning the adequate revenue and having the fruitful operations. In

consideration with the low season transactions it can be said that firm is earning adequately in

the high season while in the low season the revenue generation is comparatively below the

expectation. However, it can be said that there is need to have proper pricing techniques which

will help the hotel in terms of retain the favourable gains. In context with facilitating the 20

rooms as 25 of the price for 5 days which is the cheapest rate but in accordance with earning in

the low season it has brought the profits to the firm.

1.2 Designing a costing system for a firm

To improve the financial health of the organisation as well as make the adequate changes

in the operations of the business there will be need of developing a costing system. Therefore,

such techniques will help the organisation in having the proper funds for the business operations

with appropriate utilisation. However, there has been various methods which will be helpful for

the entity to have better growth and performance:

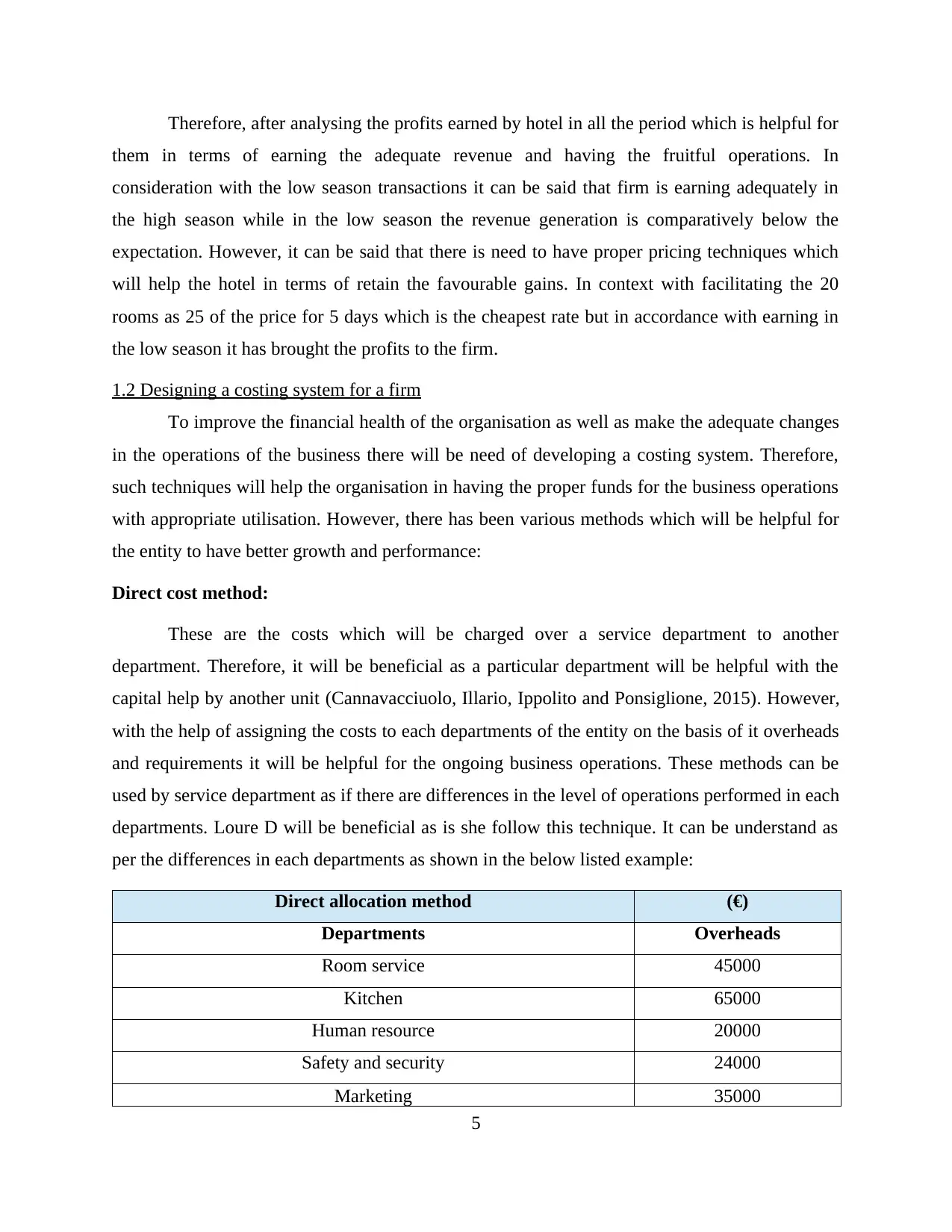

Direct cost method:

These are the costs which will be charged over a service department to another

department. Therefore, it will be beneficial as a particular department will be helpful with the

capital help by another unit (Cannavacciuolo, Illario, Ippolito and Ponsiglione, 2015). However,

with the help of assigning the costs to each departments of the entity on the basis of it overheads

and requirements it will be helpful for the ongoing business operations. These methods can be

used by service department as if there are differences in the level of operations performed in each

departments. Loure D will be beneficial as is she follow this technique. It can be understand as

per the differences in each departments as shown in the below listed example:

Direct allocation method (€)

Departments Overheads

Room service 45000

Kitchen 65000

Human resource 20000

Safety and security 24000

Marketing 35000

5

them in terms of earning the adequate revenue and having the fruitful operations. In

consideration with the low season transactions it can be said that firm is earning adequately in

the high season while in the low season the revenue generation is comparatively below the

expectation. However, it can be said that there is need to have proper pricing techniques which

will help the hotel in terms of retain the favourable gains. In context with facilitating the 20

rooms as 25 of the price for 5 days which is the cheapest rate but in accordance with earning in

the low season it has brought the profits to the firm.

1.2 Designing a costing system for a firm

To improve the financial health of the organisation as well as make the adequate changes

in the operations of the business there will be need of developing a costing system. Therefore,

such techniques will help the organisation in having the proper funds for the business operations

with appropriate utilisation. However, there has been various methods which will be helpful for

the entity to have better growth and performance:

Direct cost method:

These are the costs which will be charged over a service department to another

department. Therefore, it will be beneficial as a particular department will be helpful with the

capital help by another unit (Cannavacciuolo, Illario, Ippolito and Ponsiglione, 2015). However,

with the help of assigning the costs to each departments of the entity on the basis of it overheads

and requirements it will be helpful for the ongoing business operations. These methods can be

used by service department as if there are differences in the level of operations performed in each

departments. Loure D will be beneficial as is she follow this technique. It can be understand as

per the differences in each departments as shown in the below listed example:

Direct allocation method (€)

Departments Overheads

Room service 45000

Kitchen 65000

Human resource 20000

Safety and security 24000

Marketing 35000

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

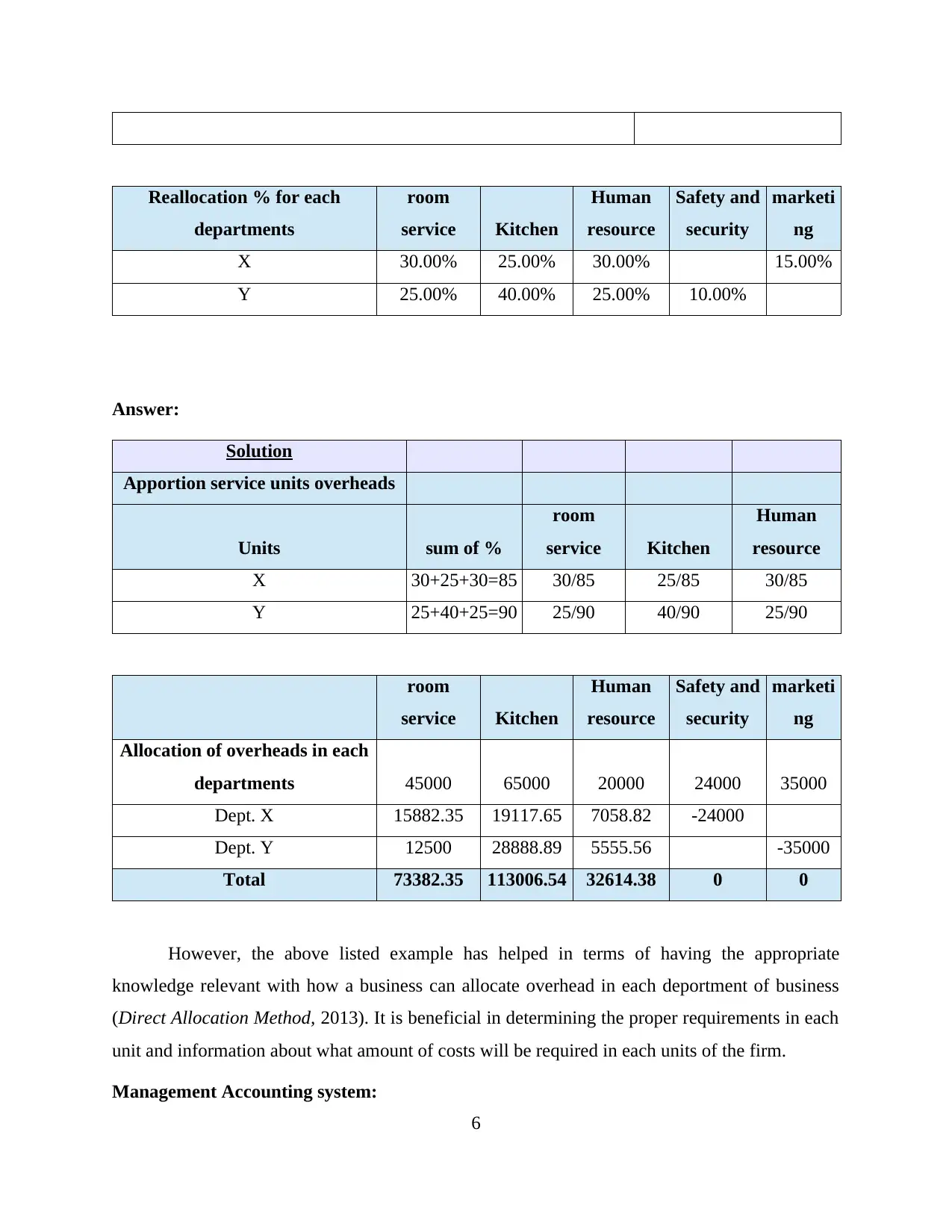

Reallocation % for each

departments

room

service Kitchen

Human

resource

Safety and

security

marketi

ng

X 30.00% 25.00% 30.00% 15.00%

Y 25.00% 40.00% 25.00% 10.00%

Answer:

Solution

Apportion service units overheads

Units sum of %

room

service Kitchen

Human

resource

X 30+25+30=85 30/85 25/85 30/85

Y 25+40+25=90 25/90 40/90 25/90

room

service Kitchen

Human

resource

Safety and

security

marketi

ng

Allocation of overheads in each

departments 45000 65000 20000 24000 35000

Dept. X 15882.35 19117.65 7058.82 -24000

Dept. Y 12500 28888.89 5555.56 -35000

Total 73382.35 113006.54 32614.38 0 0

However, the above listed example has helped in terms of having the appropriate

knowledge relevant with how a business can allocate overhead in each deportment of business

(Direct Allocation Method, 2013). It is beneficial in determining the proper requirements in each

unit and information about what amount of costs will be required in each units of the firm.

Management Accounting system:

6

departments

room

service Kitchen

Human

resource

Safety and

security

marketi

ng

X 30.00% 25.00% 30.00% 15.00%

Y 25.00% 40.00% 25.00% 10.00%

Answer:

Solution

Apportion service units overheads

Units sum of %

room

service Kitchen

Human

resource

X 30+25+30=85 30/85 25/85 30/85

Y 25+40+25=90 25/90 40/90 25/90

room

service Kitchen

Human

resource

Safety and

security

marketi

ng

Allocation of overheads in each

departments 45000 65000 20000 24000 35000

Dept. X 15882.35 19117.65 7058.82 -24000

Dept. Y 12500 28888.89 5555.56 -35000

Total 73382.35 113006.54 32614.38 0 0

However, the above listed example has helped in terms of having the appropriate

knowledge relevant with how a business can allocate overhead in each deportment of business

(Direct Allocation Method, 2013). It is beneficial in determining the proper requirements in each

unit and information about what amount of costs will be required in each units of the firm.

Management Accounting system:

6

This technique will be helpful for the firm in terms of decision making, cost controlling

as well as investments planning., however, the management accounting is used for the internal

auditing of the organisation (Waters, 2015). Here, the managerial and accounting professionals

analyse the costs implicated in each departments and piece of operations and then analyse the

actual requirement as well as revenue gathered by such units. This will be beneficial as these

professional make efficient decision to lower down the costs r to increase the funds for such

operational units. It includes various reporting and presentation of accounts as well as

preparation of budgets as to enhance thee efficiency of entity.

Responsible person for reporting:

There has been various departments in the organisation and each unit must have adequate

record of each business transactions which are need to be recorded by the professionals.

However, the disclosure of the financial health of an organisation is the prime responsibilities of

the board members, chairperson, executive directors, audit committee, accountants as well as

mangers various department (Christ, and Burritt, 2015). Therefore, in consideration with the

internal environment of the organisation thee are different units and departments and each of the

units has their own managers, head, leader and supervisor who executes the work and manager

the workforce to make efforts. Thus, it can be said that with the help of such analysis the

business will have better performance and profitability.

1.3 Evaluating the costing and pricing techniques for business

In accordance with the scenario of the business operation it can be said that there is need

to have adequate improvements in the operational activities of the Hotel as to have better cost

control. Here, uncle of Laure D. has proposed to have the reduction on such rooms which not

booked at that time and were vacant throughout the season (Subramaniam and Watson, 2016).

However, it will be helpful for them in terms of not paying of rent and electricity or various non-

operating costs on them. Thus, it will not enough as to improve the profitability of the firm

during the Low season. Hence, it will be recommended to such stakeholders that they must make

appropriate improvements in the operations of the business as well as generate the profitable

gains that will be beneficial to have proper improvements.

7

as well as investments planning., however, the management accounting is used for the internal

auditing of the organisation (Waters, 2015). Here, the managerial and accounting professionals

analyse the costs implicated in each departments and piece of operations and then analyse the

actual requirement as well as revenue gathered by such units. This will be beneficial as these

professional make efficient decision to lower down the costs r to increase the funds for such

operational units. It includes various reporting and presentation of accounts as well as

preparation of budgets as to enhance thee efficiency of entity.

Responsible person for reporting:

There has been various departments in the organisation and each unit must have adequate

record of each business transactions which are need to be recorded by the professionals.

However, the disclosure of the financial health of an organisation is the prime responsibilities of

the board members, chairperson, executive directors, audit committee, accountants as well as

mangers various department (Christ, and Burritt, 2015). Therefore, in consideration with the

internal environment of the organisation thee are different units and departments and each of the

units has their own managers, head, leader and supervisor who executes the work and manager

the workforce to make efforts. Thus, it can be said that with the help of such analysis the

business will have better performance and profitability.

1.3 Evaluating the costing and pricing techniques for business

In accordance with the scenario of the business operation it can be said that there is need

to have adequate improvements in the operational activities of the Hotel as to have better cost

control. Here, uncle of Laure D. has proposed to have the reduction on such rooms which not

booked at that time and were vacant throughout the season (Subramaniam and Watson, 2016).

However, it will be helpful for them in terms of not paying of rent and electricity or various non-

operating costs on them. Thus, it will not enough as to improve the profitability of the firm

during the Low season. Hence, it will be recommended to such stakeholders that they must make

appropriate improvements in the operations of the business as well as generate the profitable

gains that will be beneficial to have proper improvements.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 2

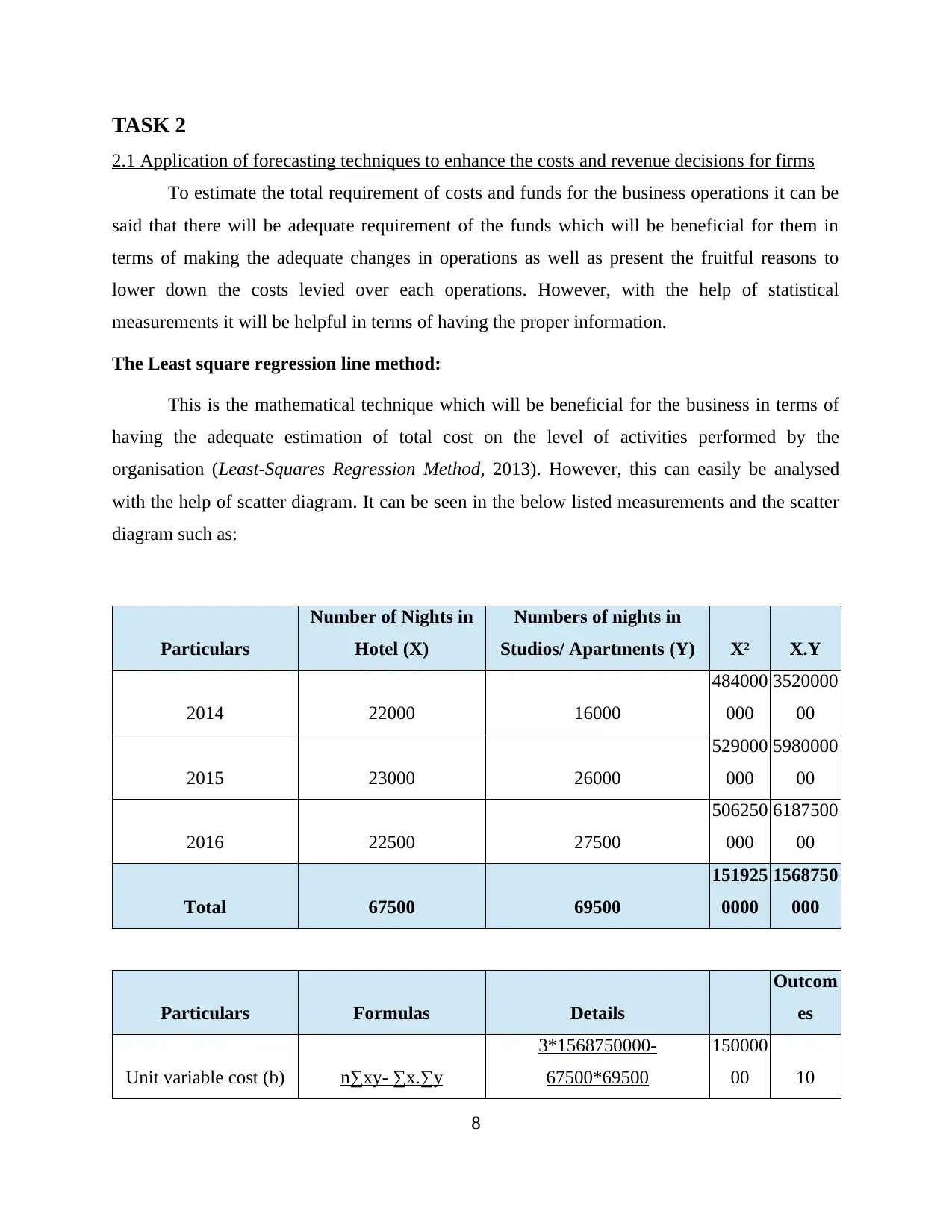

2.1 Application of forecasting techniques to enhance the costs and revenue decisions for firms

To estimate the total requirement of costs and funds for the business operations it can be

said that there will be adequate requirement of the funds which will be beneficial for them in

terms of making the adequate changes in operations as well as present the fruitful reasons to

lower down the costs levied over each operations. However, with the help of statistical

measurements it will be helpful in terms of having the proper information.

The Least square regression line method:

This is the mathematical technique which will be beneficial for the business in terms of

having the adequate estimation of total cost on the level of activities performed by the

organisation (Least-Squares Regression Method, 2013). However, this can easily be analysed

with the help of scatter diagram. It can be seen in the below listed measurements and the scatter

diagram such as:

Particulars

Number of Nights in

Hotel (X)

Numbers of nights in

Studios/ Apartments (Y) X² X.Y

2014 22000 16000

484000

000

3520000

00

2015 23000 26000

529000

000

5980000

00

2016 22500 27500

506250

000

6187500

00

Total 67500 69500

151925

0000

1568750

000

Particulars Formulas Details

Outcom

es

Unit variable cost (b) n∑xy- ∑x.∑y

3*1568750000-

67500*69500

150000

00 10

8

2.1 Application of forecasting techniques to enhance the costs and revenue decisions for firms

To estimate the total requirement of costs and funds for the business operations it can be

said that there will be adequate requirement of the funds which will be beneficial for them in

terms of making the adequate changes in operations as well as present the fruitful reasons to

lower down the costs levied over each operations. However, with the help of statistical

measurements it will be helpful in terms of having the proper information.

The Least square regression line method:

This is the mathematical technique which will be beneficial for the business in terms of

having the adequate estimation of total cost on the level of activities performed by the

organisation (Least-Squares Regression Method, 2013). However, this can easily be analysed

with the help of scatter diagram. It can be seen in the below listed measurements and the scatter

diagram such as:

Particulars

Number of Nights in

Hotel (X)

Numbers of nights in

Studios/ Apartments (Y) X² X.Y

2014 22000 16000

484000

000

3520000

00

2015 23000 26000

529000

000

5980000

00

2016 22500 27500

506250

000

6187500

00

Total 67500 69500

151925

0000

1568750

000

Particulars Formulas Details

Outcom

es

Unit variable cost (b) n∑xy- ∑x.∑y

3*1568750000-

67500*69500

150000

00 10

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

n∑x²- (∑x)² 3*1519250000- (67500)²

150000

0

Fixed cost (a) ∑y- b∑x 69500- 10*67500

-

605500

-

201833.

33

n 3 3

Cost volume formula Y= -201833.33 + 10

2013 2014 2015 2016 2017

0

100000000

200000000

300000000

400000000

500000000

600000000

700000000 f(x) = 133375000x - 268227708333.333

R² = 0.807960839

f(x) = 11125000x - 21910458333.3333

R² = 0.2444652483

Number of Nights in Hotel (X)

Numbers of nights in Studios/

Apartments (Y)

X²

Linear (X²)

X.Y

Linear (X.Y)

9

150000

0

Fixed cost (a) ∑y- b∑x 69500- 10*67500

-

605500

-

201833.

33

n 3 3

Cost volume formula Y= -201833.33 + 10

2013 2014 2015 2016 2017

0

100000000

200000000

300000000

400000000

500000000

600000000

700000000 f(x) = 133375000x - 268227708333.333

R² = 0.807960839

f(x) = 11125000x - 21910458333.3333

R² = 0.2444652483

Number of Nights in Hotel (X)

Numbers of nights in Studios/

Apartments (Y)

X²

Linear (X²)

X.Y

Linear (X.Y)

9

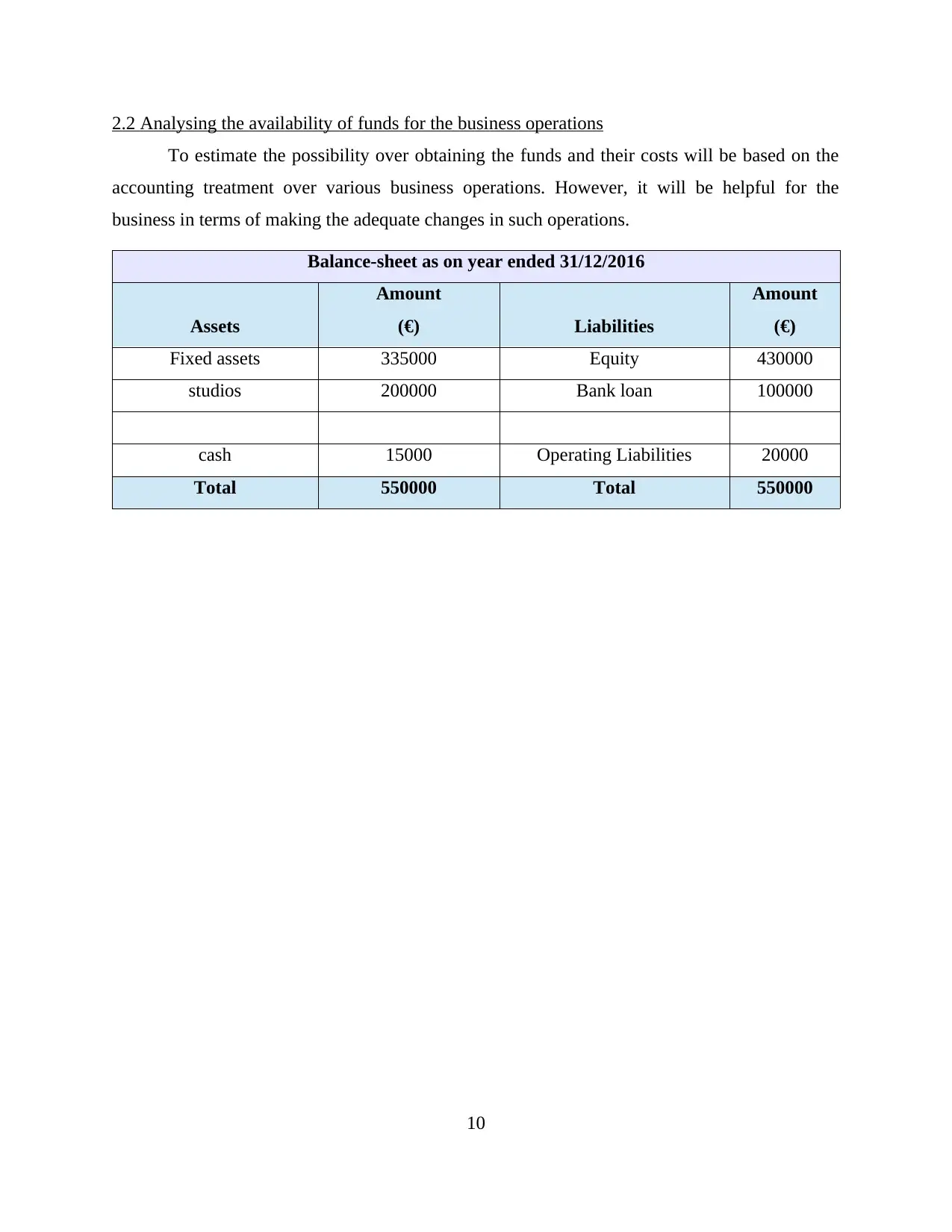

2.2 Analysing the availability of funds for the business operations

To estimate the possibility over obtaining the funds and their costs will be based on the

accounting treatment over various business operations. However, it will be helpful for the

business in terms of making the adequate changes in such operations.

Balance-sheet as on year ended 31/12/2016

Assets

Amount

(€) Liabilities

Amount

(€)

Fixed assets 335000 Equity 430000

studios 200000 Bank loan 100000

cash 15000 Operating Liabilities 20000

Total 550000 Total 550000

10

To estimate the possibility over obtaining the funds and their costs will be based on the

accounting treatment over various business operations. However, it will be helpful for the

business in terms of making the adequate changes in such operations.

Balance-sheet as on year ended 31/12/2016

Assets

Amount

(€) Liabilities

Amount

(€)

Fixed assets 335000 Equity 430000

studios 200000 Bank loan 100000

cash 15000 Operating Liabilities 20000

Total 550000 Total 550000

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 28

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.