Financial Resources and Decision Making: A Comprehensive Report

VerifiedAdded on 2020/01/15

|18

|5057

|232

Report

AI Summary

This report delves into the realm of financial resources and decision-making, exploring various aspects of finance within a business context. It begins by identifying diverse sources of finance available to different business units, such as large and small organizations and new startups, along with their implications and real-world case study examples. The report then examines the costs associated with different financing options, the key aspects of financial planning, and the crucial information required by decision-makers. It also analyzes the impact of finance on financial statements like the Trading and Profit & Loss account and the Balance Sheet. Furthermore, the report includes an analysis of sales and cash budgets, offering findings and recommendations for improvement. It also evaluates the viability of a project using investment appraisal techniques, calculates per-unit costs, and conducts ratio analysis to assess the financial position of a business. The report provides a comprehensive overview of financial management, from securing funds to evaluating project feasibility and assessing overall financial health.

MANAGING FINANCIAL

RESOURCES AND

DECISION MAKING

RESOURCES AND

DECISION MAKING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

MANAGING FINANCIAL RESOURCES AND DECISION MAKING......................................1

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Sources of finance available with different business units....................................................1

1.2 Implication of various sources of finance..............................................................................2

1.3 Case-study examples.............................................................................................................3

TASK 2............................................................................................................................................3

2.1 Cost of different sources of finance.......................................................................................3

2.2 Key aspects of financial planning..........................................................................................4

2.3 Information needed by decision maker..................................................................................4

2.4 Impact of finance on financial statements.............................................................................5

TASK 3............................................................................................................................................6

3.1 Findings and recommendation for the budget analyzed........................................................6

3.3 Viability of a project using the investment appraisal techniques..........................................6

3.2 Calculation of unit cost..........................................................................................................7

TASK 4............................................................................................................................................9

4.1 Main financial statements......................................................................................................9

4.2 Financial statements for different business type..................................................................10

4.3 Calculation of various ratio.................................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

APPENDIX....................................................................................................................................13

3.3 Calculation of payback period (In £).......................................................................................13

3.2 Calculation of unit cost............................................................................................................14

4.3 Ratio analysis of XYZ ltd. are as follows:...............................................................................17

MANAGING FINANCIAL RESOURCES AND DECISION MAKING......................................1

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Sources of finance available with different business units....................................................1

1.2 Implication of various sources of finance..............................................................................2

1.3 Case-study examples.............................................................................................................3

TASK 2............................................................................................................................................3

2.1 Cost of different sources of finance.......................................................................................3

2.2 Key aspects of financial planning..........................................................................................4

2.3 Information needed by decision maker..................................................................................4

2.4 Impact of finance on financial statements.............................................................................5

TASK 3............................................................................................................................................6

3.1 Findings and recommendation for the budget analyzed........................................................6

3.3 Viability of a project using the investment appraisal techniques..........................................6

3.2 Calculation of unit cost..........................................................................................................7

TASK 4............................................................................................................................................9

4.1 Main financial statements......................................................................................................9

4.2 Financial statements for different business type..................................................................10

4.3 Calculation of various ratio.................................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

APPENDIX....................................................................................................................................13

3.3 Calculation of payback period (In £).......................................................................................13

3.2 Calculation of unit cost............................................................................................................14

4.3 Ratio analysis of XYZ ltd. are as follows:...............................................................................17

INTRODUCTION

Finance is the science that describes the management of all activities related to banking,

investment, money and credit. It can also be said as the management of all the funds which flows

from inside and outside the organization. The following report interprets about various sources of

finance available to different business organization for the fulfillment of variety of needs. In this,

implication of finance as resources within a business is discussed. Further, cash and sales budget

are also analyzed in order to analyze cash flow forecast. By using various techniques an attempt

has been made to select best project out of the given project. In this, per unit cost of the company

is also calculated. At last, various ratios are calculated in order to find out the actual position of

the business.

TASK 1

1.1 Sources of finance available with different business units

There are various sources of finance available in world which aids various organizations

to meet requirement of funds. Some of the sources of finance for different organization are as

follows:

Large and small business organization: - Large business organization can raise their

finance by issuing equity shares to the general public. By using this method, company is able to

raise large amount of finance within a short period of time (Brigham and Daves, 2012).

Similarly, Small business organization can raise their funds by approaching various financial

institutions or by taking bank loan. This is one of the cost effective ways to aid various

organization in order to raise its funds.

Advantages

By issuing equity shares company can save its floating cost.

Company will be able to avail the tax deduction benefit if they raise their funds through

bank loan.

Disadvantages

Company is required to pay high rate of interest to the bank in order to raise finance

through loan which in turn increases the liability. Voting rights need to be given to the shareholders in various decision making process

which in turn can affect decision of the company (Brigham and Houston, 2011).

1

Finance is the science that describes the management of all activities related to banking,

investment, money and credit. It can also be said as the management of all the funds which flows

from inside and outside the organization. The following report interprets about various sources of

finance available to different business organization for the fulfillment of variety of needs. In this,

implication of finance as resources within a business is discussed. Further, cash and sales budget

are also analyzed in order to analyze cash flow forecast. By using various techniques an attempt

has been made to select best project out of the given project. In this, per unit cost of the company

is also calculated. At last, various ratios are calculated in order to find out the actual position of

the business.

TASK 1

1.1 Sources of finance available with different business units

There are various sources of finance available in world which aids various organizations

to meet requirement of funds. Some of the sources of finance for different organization are as

follows:

Large and small business organization: - Large business organization can raise their

finance by issuing equity shares to the general public. By using this method, company is able to

raise large amount of finance within a short period of time (Brigham and Daves, 2012).

Similarly, Small business organization can raise their funds by approaching various financial

institutions or by taking bank loan. This is one of the cost effective ways to aid various

organization in order to raise its funds.

Advantages

By issuing equity shares company can save its floating cost.

Company will be able to avail the tax deduction benefit if they raise their funds through

bank loan.

Disadvantages

Company is required to pay high rate of interest to the bank in order to raise finance

through loan which in turn increases the liability. Voting rights need to be given to the shareholders in various decision making process

which in turn can affect decision of the company (Brigham and Houston, 2011).

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

New business start up: - Personal saving of the individual can be used to start up a new

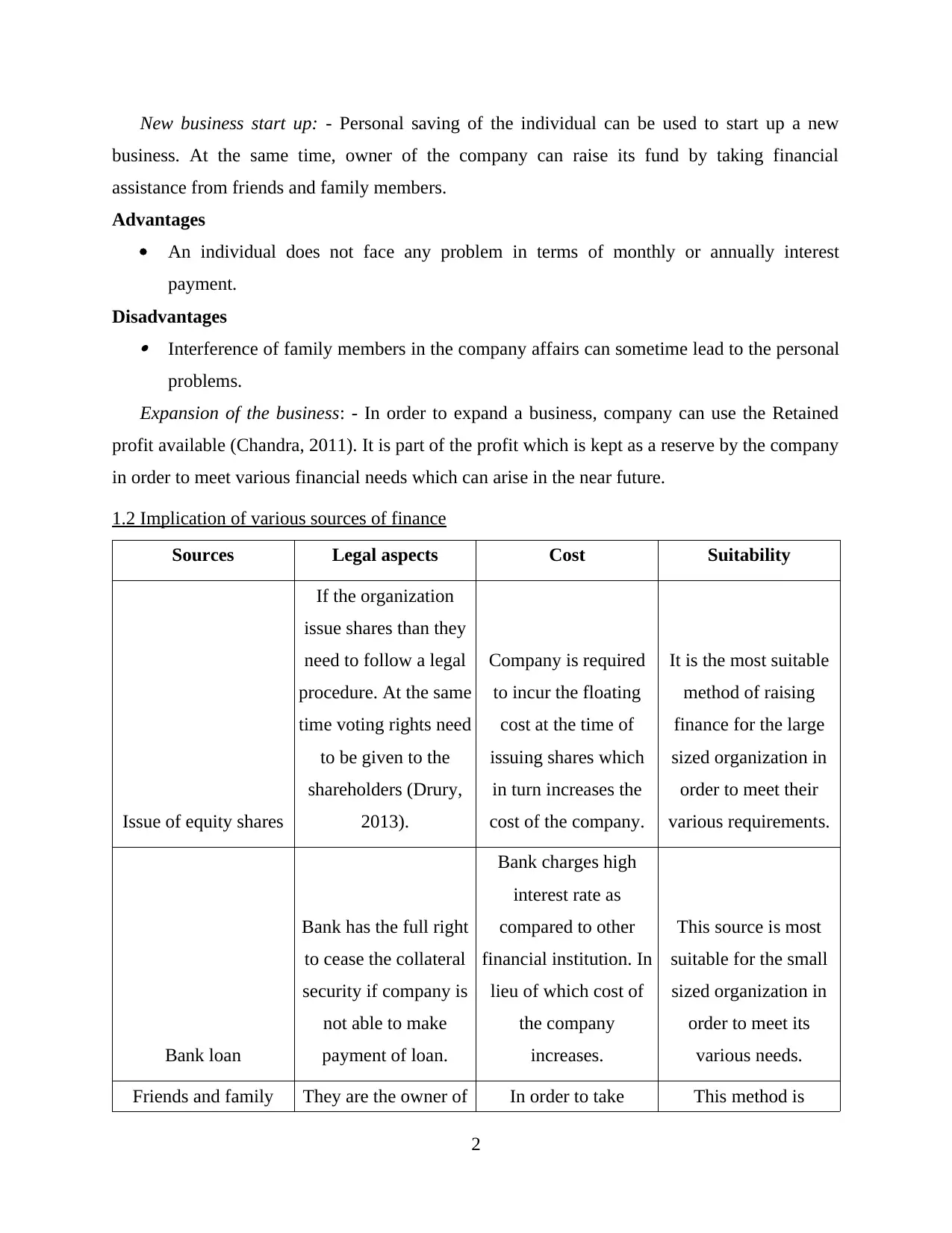

business. At the same time, owner of the company can raise its fund by taking financial

assistance from friends and family members.

Advantages

An individual does not face any problem in terms of monthly or annually interest

payment.

Disadvantages Interference of family members in the company affairs can sometime lead to the personal

problems.

Expansion of the business: - In order to expand a business, company can use the Retained

profit available (Chandra, 2011). It is part of the profit which is kept as a reserve by the company

in order to meet various financial needs which can arise in the near future.

1.2 Implication of various sources of finance

Sources Legal aspects Cost Suitability

Issue of equity shares

If the organization

issue shares than they

need to follow a legal

procedure. At the same

time voting rights need

to be given to the

shareholders (Drury,

2013).

Company is required

to incur the floating

cost at the time of

issuing shares which

in turn increases the

cost of the company.

It is the most suitable

method of raising

finance for the large

sized organization in

order to meet their

various requirements.

Bank loan

Bank has the full right

to cease the collateral

security if company is

not able to make

payment of loan.

Bank charges high

interest rate as

compared to other

financial institution. In

lieu of which cost of

the company

increases.

This source is most

suitable for the small

sized organization in

order to meet its

various needs.

Friends and family They are the owner of In order to take This method is

2

business. At the same time, owner of the company can raise its fund by taking financial

assistance from friends and family members.

Advantages

An individual does not face any problem in terms of monthly or annually interest

payment.

Disadvantages Interference of family members in the company affairs can sometime lead to the personal

problems.

Expansion of the business: - In order to expand a business, company can use the Retained

profit available (Chandra, 2011). It is part of the profit which is kept as a reserve by the company

in order to meet various financial needs which can arise in the near future.

1.2 Implication of various sources of finance

Sources Legal aspects Cost Suitability

Issue of equity shares

If the organization

issue shares than they

need to follow a legal

procedure. At the same

time voting rights need

to be given to the

shareholders (Drury,

2013).

Company is required

to incur the floating

cost at the time of

issuing shares which

in turn increases the

cost of the company.

It is the most suitable

method of raising

finance for the large

sized organization in

order to meet their

various requirements.

Bank loan

Bank has the full right

to cease the collateral

security if company is

not able to make

payment of loan.

Bank charges high

interest rate as

compared to other

financial institution. In

lieu of which cost of

the company

increases.

This source is most

suitable for the small

sized organization in

order to meet its

various needs.

Friends and family They are the owner of In order to take This method is

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

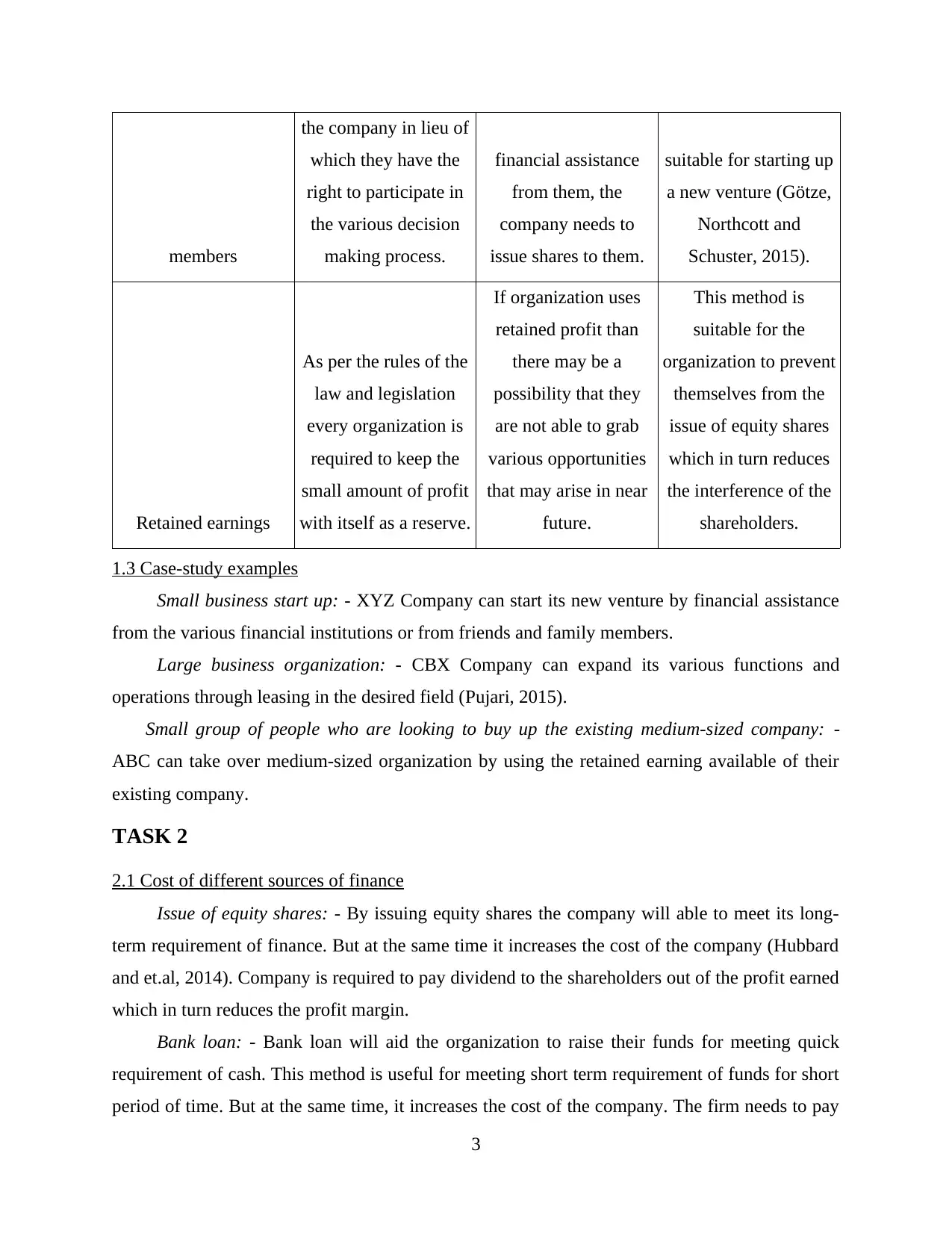

members

the company in lieu of

which they have the

right to participate in

the various decision

making process.

financial assistance

from them, the

company needs to

issue shares to them.

suitable for starting up

a new venture (Götze,

Northcott and

Schuster, 2015).

Retained earnings

As per the rules of the

law and legislation

every organization is

required to keep the

small amount of profit

with itself as a reserve.

If organization uses

retained profit than

there may be a

possibility that they

are not able to grab

various opportunities

that may arise in near

future.

This method is

suitable for the

organization to prevent

themselves from the

issue of equity shares

which in turn reduces

the interference of the

shareholders.

1.3 Case-study examples

Small business start up: - XYZ Company can start its new venture by financial assistance

from the various financial institutions or from friends and family members.

Large business organization: - CBX Company can expand its various functions and

operations through leasing in the desired field (Pujari, 2015).

Small group of people who are looking to buy up the existing medium-sized company: -

ABC can take over medium-sized organization by using the retained earning available of their

existing company.

TASK 2

2.1 Cost of different sources of finance

Issue of equity shares: - By issuing equity shares the company will able to meet its long-

term requirement of finance. But at the same time it increases the cost of the company (Hubbard

and et.al, 2014). Company is required to pay dividend to the shareholders out of the profit earned

which in turn reduces the profit margin.

Bank loan: - Bank loan will aid the organization to raise their funds for meeting quick

requirement of cash. This method is useful for meeting short term requirement of funds for short

period of time. But at the same time, it increases the cost of the company. The firm needs to pay

3

the company in lieu of

which they have the

right to participate in

the various decision

making process.

financial assistance

from them, the

company needs to

issue shares to them.

suitable for starting up

a new venture (Götze,

Northcott and

Schuster, 2015).

Retained earnings

As per the rules of the

law and legislation

every organization is

required to keep the

small amount of profit

with itself as a reserve.

If organization uses

retained profit than

there may be a

possibility that they

are not able to grab

various opportunities

that may arise in near

future.

This method is

suitable for the

organization to prevent

themselves from the

issue of equity shares

which in turn reduces

the interference of the

shareholders.

1.3 Case-study examples

Small business start up: - XYZ Company can start its new venture by financial assistance

from the various financial institutions or from friends and family members.

Large business organization: - CBX Company can expand its various functions and

operations through leasing in the desired field (Pujari, 2015).

Small group of people who are looking to buy up the existing medium-sized company: -

ABC can take over medium-sized organization by using the retained earning available of their

existing company.

TASK 2

2.1 Cost of different sources of finance

Issue of equity shares: - By issuing equity shares the company will able to meet its long-

term requirement of finance. But at the same time it increases the cost of the company (Hubbard

and et.al, 2014). Company is required to pay dividend to the shareholders out of the profit earned

which in turn reduces the profit margin.

Bank loan: - Bank loan will aid the organization to raise their funds for meeting quick

requirement of cash. This method is useful for meeting short term requirement of funds for short

period of time. But at the same time, it increases the cost of the company. The firm needs to pay

3

high rate of interest which in turn increases the expenses of the company. Increases expense

results in reduction of profitability of the company.

Retained profit: - Retained profit assists the company to meet its long term requirement of

the funds and at the same time it also aids the company to meet its quick or sudden requirement

of finance. Further, it also increases the cost of the company (Jackson, Schuler and Werner,

2011). It reduces the profit margin of the company which in turn can affect mind of the

shareholders in negative way.

2.2 Key aspects of financial planning

Creates a link between various present and future activities:- : - Planning all the financial

activities assists the company to create a proper link between present and future activities in

order to prepare various strategies and to achieve the desired objective.

Assist in allocating the right amount of finance in right department and projects:-

Financial planning aid the company to properly invest the fund in right activities and project in

order to avoid the condition of excess or lack of the funds in any project.

Helps in achieving the growth of the company: - Financial planning of all the activities

assists the company to easily achieve organization desired objectives (Kaplan and Atkinson,

2015). At the same time it also helps the firm to move towards achieving high growth rate.

Helps in maintaining the flow of cash: - Planning of all financial activities in advance aids

the company in maintaining balance between inflow and outflow of the funds within and outside

the organization.

2.3 Information needed by decision maker

There is varied range of information which is required by the decision maker to take

various decisions. They want to know the flow of funds, utilization of resources, profitability and

many more. Thus, in order to conclude all these information they require financial statements

and company’s audit report

Financial statements: - These are the statements which help the decision maker to know

the amount of profit earned by the company during a year, how much sales has been done by the

company, inflow and outflow of the fund from within and outside the organization (Loorbach,

and Rotmans, 2010). Therefore, this information is required by some decision maker to now the

financial position of the company and some are required to form various strategies.

4

results in reduction of profitability of the company.

Retained profit: - Retained profit assists the company to meet its long term requirement of

the funds and at the same time it also aids the company to meet its quick or sudden requirement

of finance. Further, it also increases the cost of the company (Jackson, Schuler and Werner,

2011). It reduces the profit margin of the company which in turn can affect mind of the

shareholders in negative way.

2.2 Key aspects of financial planning

Creates a link between various present and future activities:- : - Planning all the financial

activities assists the company to create a proper link between present and future activities in

order to prepare various strategies and to achieve the desired objective.

Assist in allocating the right amount of finance in right department and projects:-

Financial planning aid the company to properly invest the fund in right activities and project in

order to avoid the condition of excess or lack of the funds in any project.

Helps in achieving the growth of the company: - Financial planning of all the activities

assists the company to easily achieve organization desired objectives (Kaplan and Atkinson,

2015). At the same time it also helps the firm to move towards achieving high growth rate.

Helps in maintaining the flow of cash: - Planning of all financial activities in advance aids

the company in maintaining balance between inflow and outflow of the funds within and outside

the organization.

2.3 Information needed by decision maker

There is varied range of information which is required by the decision maker to take

various decisions. They want to know the flow of funds, utilization of resources, profitability and

many more. Thus, in order to conclude all these information they require financial statements

and company’s audit report

Financial statements: - These are the statements which help the decision maker to know

the amount of profit earned by the company during a year, how much sales has been done by the

company, inflow and outflow of the fund from within and outside the organization (Loorbach,

and Rotmans, 2010). Therefore, this information is required by some decision maker to now the

financial position of the company and some are required to form various strategies.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Company audit report:- This report is prepared by the company in order to find out

whether any fraud or illegal practice has been taking place in the organization or not. This report

is generally prepared by the auditor which is mostly appointed by the government. This report

aids the decision maker to know the financial position of the company and at the same time it

also helps the organization and government to calculate the amount of tax need to be paid.

2.4 Impact of finance on financial statements

Trading and Profit & loss account is prepared by the organization in order to find out the

income and expenditure made by the company during a financial year. This account also aids the

company to analyze the amount of net profit earned (Madura, 2012). Similarly, balance sheet is

prepared by the company in order to find out the financial obligations and assets & liabilities

incurred by the company in a year. Moreover, various transaction made by the company in a year

are recorded in various accounts such as profit & loss account and balance sheet.

For example- ABC company issue 10% preference shares of £300000 to the general public

in order to expand its business. Entry of this transaction will be made in following ways in profit

and loss account and balance sheet

Profit and loss account

Particulars Amount(£) Particular Amount(£)

To dividend 30000

Balance sheet

Liability Amount(£) Assets Amount(£)

Share capital:

Preference Shares 300000

TASK 3

3.1 Findings and recommendation for the budget analyzed

As a financial accountant of the company; after analyzing the sales budget it could be

analyzed that company's financial position is good. Every month, company's actual sales are

more than its budgeted sales. This in turn indicates that company's expenses are more as

compared to its income earned. Therefore, in order to overcome this problem the firm should

5

whether any fraud or illegal practice has been taking place in the organization or not. This report

is generally prepared by the auditor which is mostly appointed by the government. This report

aids the decision maker to know the financial position of the company and at the same time it

also helps the organization and government to calculate the amount of tax need to be paid.

2.4 Impact of finance on financial statements

Trading and Profit & loss account is prepared by the organization in order to find out the

income and expenditure made by the company during a financial year. This account also aids the

company to analyze the amount of net profit earned (Madura, 2012). Similarly, balance sheet is

prepared by the company in order to find out the financial obligations and assets & liabilities

incurred by the company in a year. Moreover, various transaction made by the company in a year

are recorded in various accounts such as profit & loss account and balance sheet.

For example- ABC company issue 10% preference shares of £300000 to the general public

in order to expand its business. Entry of this transaction will be made in following ways in profit

and loss account and balance sheet

Profit and loss account

Particulars Amount(£) Particular Amount(£)

To dividend 30000

Balance sheet

Liability Amount(£) Assets Amount(£)

Share capital:

Preference Shares 300000

TASK 3

3.1 Findings and recommendation for the budget analyzed

As a financial accountant of the company; after analyzing the sales budget it could be

analyzed that company's financial position is good. Every month, company's actual sales are

more than its budgeted sales. This in turn indicates that company's expenses are more as

compared to its income earned. Therefore, in order to overcome this problem the firm should

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

focus on preparing various strategies in order to reduce its expenses. Similarly, taking into

consideration the cash budget it is found out that the inflow and outflow of the funds is

constantly fluctuating. It is also found that in many months company’s expenditure is more as

compared to the income. Company's accumulative deficit is also increasing continuously. Thus,

in order to overcome this problem the firm should form various strategies and tries to plan all its

financial activities in advance which in turn aid the company to utilize available resources to the

full extent.

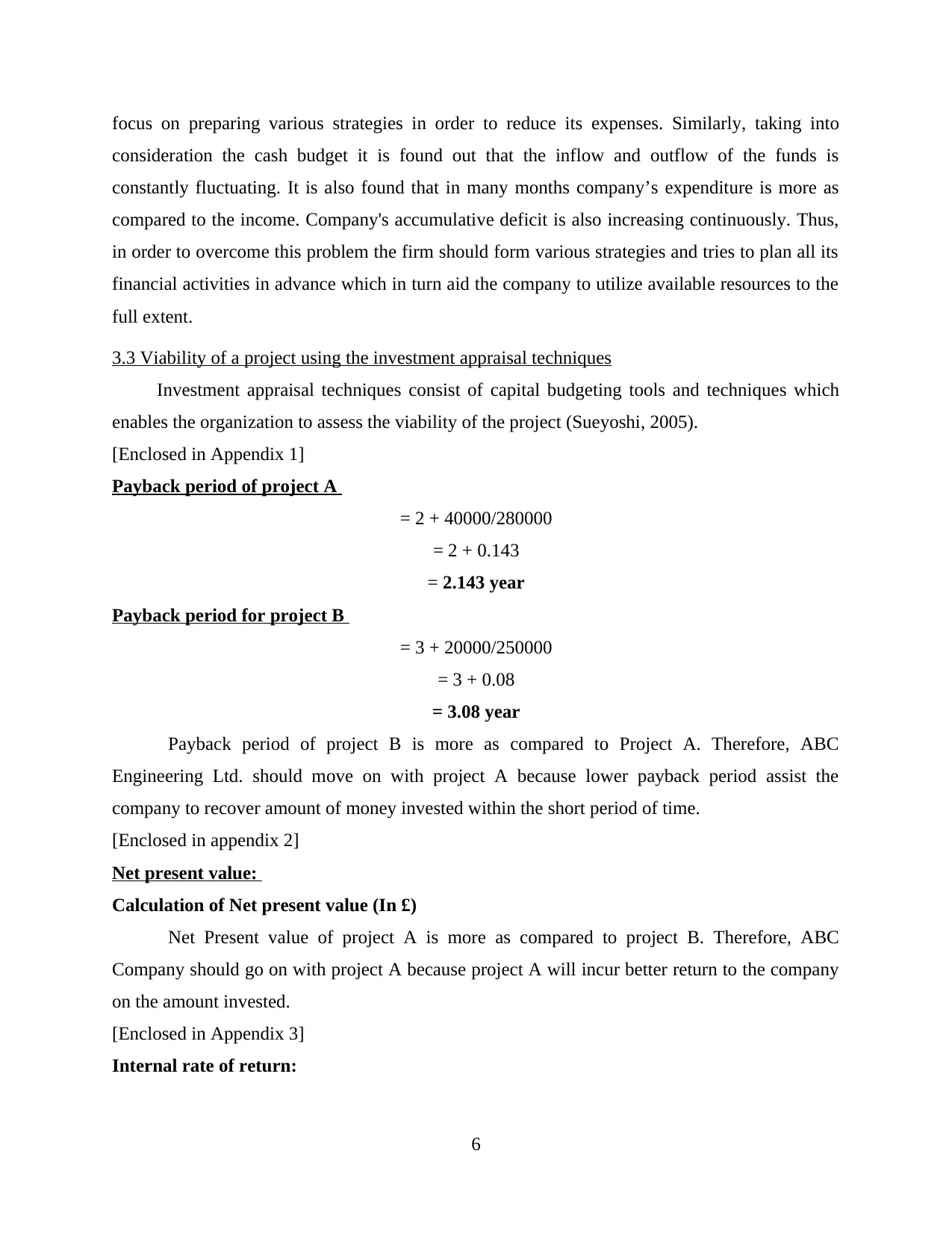

3.3 Viability of a project using the investment appraisal techniques

Investment appraisal techniques consist of capital budgeting tools and techniques which

enables the organization to assess the viability of the project (Sueyoshi, 2005).

[Enclosed in Appendix 1]

Payback period of project A

= 2 + 40000/280000

= 2 + 0.143

= 2.143 year

Payback period for project B

= 3 + 20000/250000

= 3 + 0.08

= 3.08 year

Payback period of project B is more as compared to Project A. Therefore, ABC

Engineering Ltd. should move on with project A because lower payback period assist the

company to recover amount of money invested within the short period of time.

[Enclosed in appendix 2]

Net present value:

Calculation of Net present value (In £)

Net Present value of project A is more as compared to project B. Therefore, ABC

Company should go on with project A because project A will incur better return to the company

on the amount invested.

[Enclosed in Appendix 3]

Internal rate of return:

6

consideration the cash budget it is found out that the inflow and outflow of the funds is

constantly fluctuating. It is also found that in many months company’s expenditure is more as

compared to the income. Company's accumulative deficit is also increasing continuously. Thus,

in order to overcome this problem the firm should form various strategies and tries to plan all its

financial activities in advance which in turn aid the company to utilize available resources to the

full extent.

3.3 Viability of a project using the investment appraisal techniques

Investment appraisal techniques consist of capital budgeting tools and techniques which

enables the organization to assess the viability of the project (Sueyoshi, 2005).

[Enclosed in Appendix 1]

Payback period of project A

= 2 + 40000/280000

= 2 + 0.143

= 2.143 year

Payback period for project B

= 3 + 20000/250000

= 3 + 0.08

= 3.08 year

Payback period of project B is more as compared to Project A. Therefore, ABC

Engineering Ltd. should move on with project A because lower payback period assist the

company to recover amount of money invested within the short period of time.

[Enclosed in appendix 2]

Net present value:

Calculation of Net present value (In £)

Net Present value of project A is more as compared to project B. Therefore, ABC

Company should go on with project A because project A will incur better return to the company

on the amount invested.

[Enclosed in Appendix 3]

Internal rate of return:

6

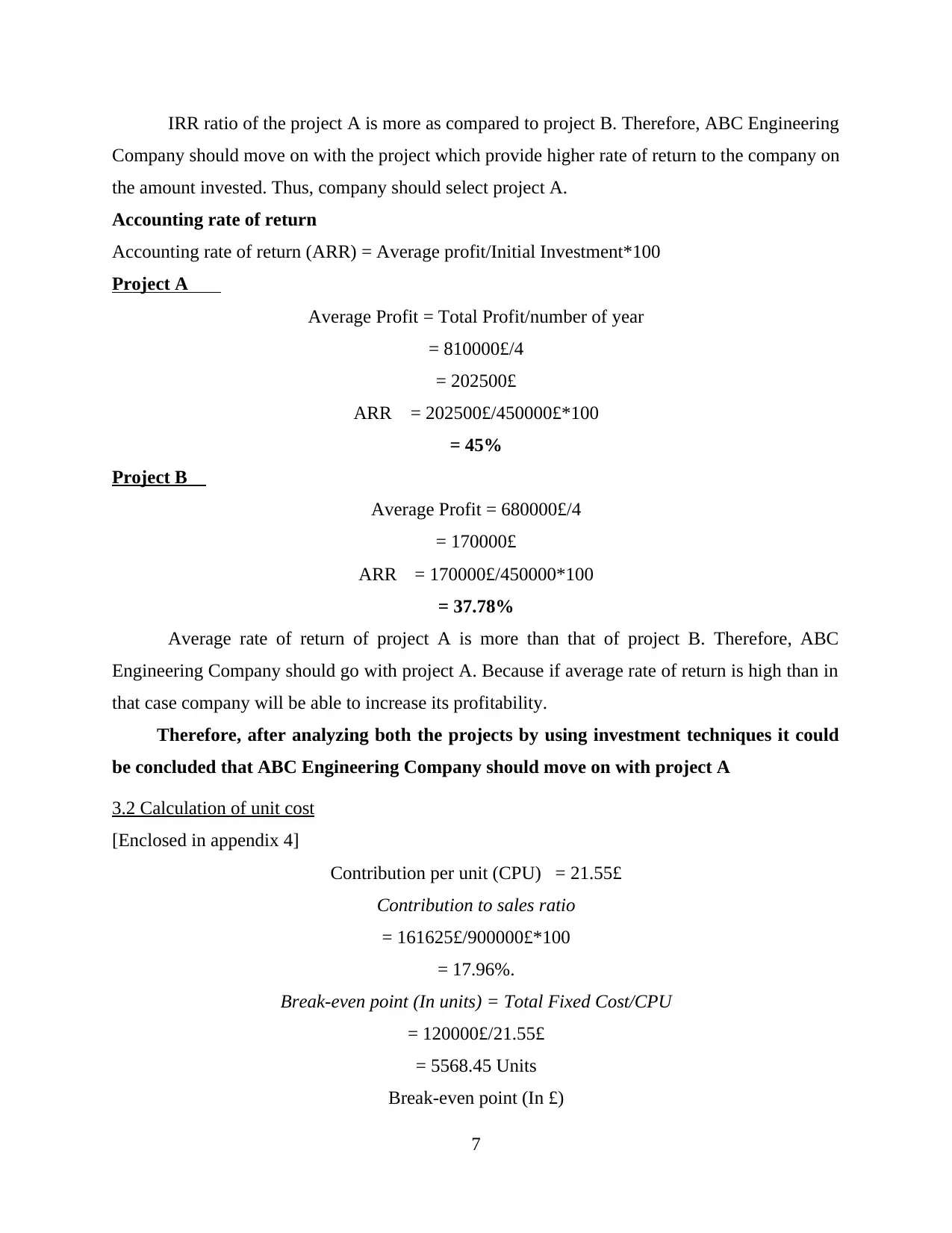

IRR ratio of the project A is more as compared to project B. Therefore, ABC Engineering

Company should move on with the project which provide higher rate of return to the company on

the amount invested. Thus, company should select project A.

Accounting rate of return

Accounting rate of return (ARR) = Average profit/Initial Investment*100

Project A

Average Profit = Total Profit/number of year

= 810000£/4

= 202500£

ARR = 202500£/450000£*100

= 45%

Project B

Average Profit = 680000£/4

= 170000£

ARR = 170000£/450000*100

= 37.78%

Average rate of return of project A is more than that of project B. Therefore, ABC

Engineering Company should go with project A. Because if average rate of return is high than in

that case company will be able to increase its profitability.

Therefore, after analyzing both the projects by using investment techniques it could

be concluded that ABC Engineering Company should move on with project A

3.2 Calculation of unit cost

[Enclosed in appendix 4]

Contribution per unit (CPU) = 21.55£

Contribution to sales ratio

= 161625£/900000£*100

= 17.96%.

Break-even point (In units) = Total Fixed Cost/CPU

= 120000£/21.55£

= 5568.45 Units

Break-even point (In £)

7

Company should move on with the project which provide higher rate of return to the company on

the amount invested. Thus, company should select project A.

Accounting rate of return

Accounting rate of return (ARR) = Average profit/Initial Investment*100

Project A

Average Profit = Total Profit/number of year

= 810000£/4

= 202500£

ARR = 202500£/450000£*100

= 45%

Project B

Average Profit = 680000£/4

= 170000£

ARR = 170000£/450000*100

= 37.78%

Average rate of return of project A is more than that of project B. Therefore, ABC

Engineering Company should go with project A. Because if average rate of return is high than in

that case company will be able to increase its profitability.

Therefore, after analyzing both the projects by using investment techniques it could

be concluded that ABC Engineering Company should move on with project A

3.2 Calculation of unit cost

[Enclosed in appendix 4]

Contribution per unit (CPU) = 21.55£

Contribution to sales ratio

= 161625£/900000£*100

= 17.96%.

Break-even point (In units) = Total Fixed Cost/CPU

= 120000£/21.55£

= 5568.45 Units

Break-even point (In £)

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

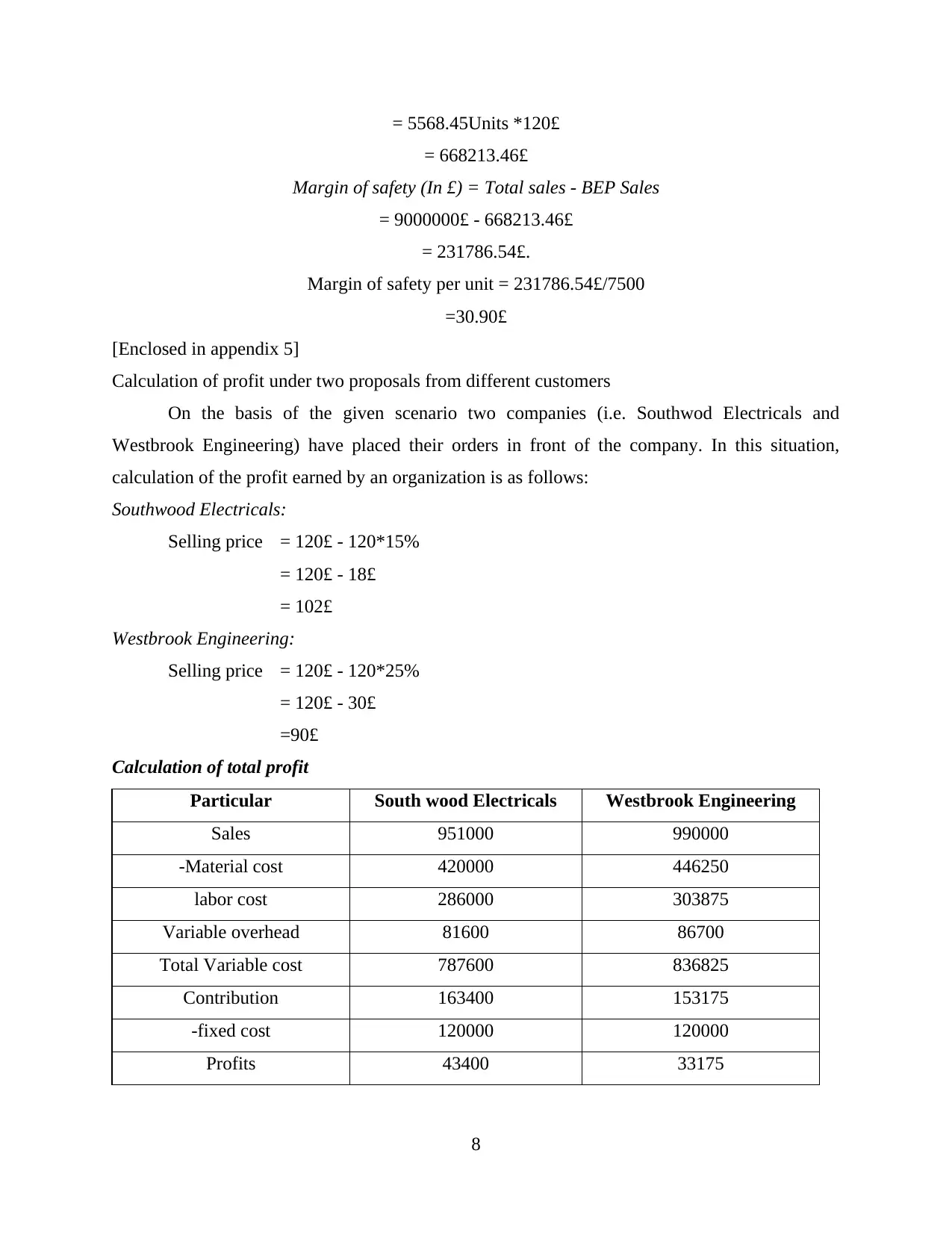

= 5568.45Units *120£

= 668213.46£

Margin of safety (In £) = Total sales - BEP Sales

= 9000000£ - 668213.46£

= 231786.54£.

Margin of safety per unit = 231786.54£/7500

=30.90£

[Enclosed in appendix 5]

Calculation of profit under two proposals from different customers

On the basis of the given scenario two companies (i.e. Southwod Electricals and

Westbrook Engineering) have placed their orders in front of the company. In this situation,

calculation of the profit earned by an organization is as follows:

Southwood Electricals:

Selling price = 120£ - 120*15%

= 120£ - 18£

= 102£

Westbrook Engineering:

Selling price = 120£ - 120*25%

= 120£ - 30£

=90£

Calculation of total profit

Particular South wood Electricals Westbrook Engineering

Sales 951000 990000

-Material cost 420000 446250

labor cost 286000 303875

Variable overhead 81600 86700

Total Variable cost 787600 836825

Contribution 163400 153175

-fixed cost 120000 120000

Profits 43400 33175

8

= 668213.46£

Margin of safety (In £) = Total sales - BEP Sales

= 9000000£ - 668213.46£

= 231786.54£.

Margin of safety per unit = 231786.54£/7500

=30.90£

[Enclosed in appendix 5]

Calculation of profit under two proposals from different customers

On the basis of the given scenario two companies (i.e. Southwod Electricals and

Westbrook Engineering) have placed their orders in front of the company. In this situation,

calculation of the profit earned by an organization is as follows:

Southwood Electricals:

Selling price = 120£ - 120*15%

= 120£ - 18£

= 102£

Westbrook Engineering:

Selling price = 120£ - 120*25%

= 120£ - 30£

=90£

Calculation of total profit

Particular South wood Electricals Westbrook Engineering

Sales 951000 990000

-Material cost 420000 446250

labor cost 286000 303875

Variable overhead 81600 86700

Total Variable cost 787600 836825

Contribution 163400 153175

-fixed cost 120000 120000

Profits 43400 33175

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

After analyzing the market condition of the both the companies, it can be concluded

that ABC Engineering company should expect the order of Southwood Electricals. Because the

profit margin of the Southwood Electricals is more as compared to that of Westbrook

Engineering.

Therefore, after analyzing the market condition of both the companies it could be concluded

that ABC Engineering Ltd. Company should expect the order of Southwood Electricals in lieu of

that of Westbrook Engineering. Because the profit margin Southwood Electricals is more.

TASK 4

4.1 Main financial statements

Prime entry: - All the daily transaction made by the company is recorded. Day book

includes sales book, purchase book, cash book and many more.

Debit & credit: - It consists of double entry book keeping system in which one account

balance is debited and another is credited with the same amount.

Trial balance: - It is a statement prepared by the company in which all the business

transaction made by the company in the financial year are summarized (McKinney, 2015). It

provides assistance to the company in preparing the financial statements of an organization.

Final accounts

Income statements: - Income statement assists the company to find out income

generated and expenses made by the company during a financial year. Preparation of this

statement aids the company to analyze the profit earned by them. Preparation of these

statements assists the company to identify the area on which company requires to exert

control.

Balance sheet: - This statement is normally prepared by each and every business

organization in order to conclude the financial health and its position. It provides

information to the company related to its assets, liabilities and financial obligations. This

statement also aids the organization to prepare various cost effective financial strategies

and policies which aid the company to achieve its desired objective.

Cash flow statements: - It assist the organization in identifying the inflow and outflow

of the funds from within and outside the organization (Moyer and et.al., 2011). It

9

that ABC Engineering company should expect the order of Southwood Electricals. Because the

profit margin of the Southwood Electricals is more as compared to that of Westbrook

Engineering.

Therefore, after analyzing the market condition of both the companies it could be concluded

that ABC Engineering Ltd. Company should expect the order of Southwood Electricals in lieu of

that of Westbrook Engineering. Because the profit margin Southwood Electricals is more.

TASK 4

4.1 Main financial statements

Prime entry: - All the daily transaction made by the company is recorded. Day book

includes sales book, purchase book, cash book and many more.

Debit & credit: - It consists of double entry book keeping system in which one account

balance is debited and another is credited with the same amount.

Trial balance: - It is a statement prepared by the company in which all the business

transaction made by the company in the financial year are summarized (McKinney, 2015). It

provides assistance to the company in preparing the financial statements of an organization.

Final accounts

Income statements: - Income statement assists the company to find out income

generated and expenses made by the company during a financial year. Preparation of this

statement aids the company to analyze the profit earned by them. Preparation of these

statements assists the company to identify the area on which company requires to exert

control.

Balance sheet: - This statement is normally prepared by each and every business

organization in order to conclude the financial health and its position. It provides

information to the company related to its assets, liabilities and financial obligations. This

statement also aids the organization to prepare various cost effective financial strategies

and policies which aid the company to achieve its desired objective.

Cash flow statements: - It assist the organization in identifying the inflow and outflow

of the funds from within and outside the organization (Moyer and et.al., 2011). It

9

provides assistance to the organization in making necessary decision in lieu of the

expansion of the business operation and functions.

4.2 Financial statements for different business type

Sole traders: - Sole traders are only concern about the profitability aspects of the company.

They prepare only income and expenditure account in order to find out the income generated and

expenses made by the company during the financial year.

Partnership firms: - These firms are required to prepare all the financial statements along

with the partners’ capital account. This account indicates the profit margin incurred by the every

partner. This account clearly states the business activities prepared by different partners.

Limited companies: - Public and Private limited companies are required to prepare all the

financial statements in order to assess the financial health and position of the business

organization (Zietlow, Hankin and Seidner, 2011). Along with this; these companies are also

required to issue these statements in order to gain the trust and faith of the various stakeholders

Non-profit making: - This is the organization who works for the betterment of the society.

Profit maximization is not their main aim. These organization are simply required to prepare

receipt and payment account.

4.3 Calculation of various ratio

[Enclosed in Appendix 6]

After analyzing the market situation of the company for two consecutive years, it could

be concluded that profitability ratio of the company has been declining from year 1995 to 1996.

This in turn indicates that financial position of the company is not good. The reason behind this

could be that companies’ expenses are increasing day by day as compared to its income

generated.

Similarly, Liquidity ratio of the company is also declining. This indicates that availability

of liquid cash with the company has been reduced. Therefore, in order to overcome this problem

company should form various strategies in order to avoid wastage of the resources.

Likewise on the other hand Solvency ratio of the company is declining which is also

declining. The reason behind this could be that company is left with much closing stock at the

end of the financial year.

10

expansion of the business operation and functions.

4.2 Financial statements for different business type

Sole traders: - Sole traders are only concern about the profitability aspects of the company.

They prepare only income and expenditure account in order to find out the income generated and

expenses made by the company during the financial year.

Partnership firms: - These firms are required to prepare all the financial statements along

with the partners’ capital account. This account indicates the profit margin incurred by the every

partner. This account clearly states the business activities prepared by different partners.

Limited companies: - Public and Private limited companies are required to prepare all the

financial statements in order to assess the financial health and position of the business

organization (Zietlow, Hankin and Seidner, 2011). Along with this; these companies are also

required to issue these statements in order to gain the trust and faith of the various stakeholders

Non-profit making: - This is the organization who works for the betterment of the society.

Profit maximization is not their main aim. These organization are simply required to prepare

receipt and payment account.

4.3 Calculation of various ratio

[Enclosed in Appendix 6]

After analyzing the market situation of the company for two consecutive years, it could

be concluded that profitability ratio of the company has been declining from year 1995 to 1996.

This in turn indicates that financial position of the company is not good. The reason behind this

could be that companies’ expenses are increasing day by day as compared to its income

generated.

Similarly, Liquidity ratio of the company is also declining. This indicates that availability

of liquid cash with the company has been reduced. Therefore, in order to overcome this problem

company should form various strategies in order to avoid wastage of the resources.

Likewise on the other hand Solvency ratio of the company is declining which is also

declining. The reason behind this could be that company is left with much closing stock at the

end of the financial year.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.