Managing Financial Resources for J Sainsbury PLC: A Detailed Report

VerifiedAdded on 2020/02/03

|13

|4253

|49

Report

AI Summary

This report provides a comprehensive analysis of financial resource management, specifically focusing on J Sainsbury PLC. It begins with an introduction to financial management and its importance, followed by an examination of various sources of finance, both internal and external, along with their implications. The report then delves into the factors influencing the selection of appropriate financing sources, the associated costs, and the significance of financial planning. It further explores the information needs of different decision-makers within the company and the impact of financial activities on financial statements. A detailed cash budget for J Sainsbury PLC is presented, along with calculations of unit costs. The report also discusses the viability of a project using investment appraisal techniques. Finally, it covers the different types of financial statements, their application in various business contexts, and the interpretation of these statements using relevant financial ratios. The report concludes with a summary of the key findings and insights.

Managing Financial

Resources

Resources

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................4

1.1 Sources of finance.................................................................................................................4

1.2 Implications of the different sources.....................................................................................4

1.3 Appropriate sources of finance.............................................................................................5

2.1 Cost of different sources.......................................................................................................5

2.2 Importance of financial planning..........................................................................................5

2.3 Information needs of different decision makers....................................................................6

2.4 Impact of finance on financial statements.............................................................................6

3.1 Cash budget for the business entity.......................................................................................6

3.2 Calculation of Unit Cost........................................................................................................7

3.3 Viability of a project by using the investment appraisal technique......................................8

TASK 2..........................................................................................................................................11

4.1 Different financial statements.............................................................................................11

4.2 In the different type of business have to use different financial statements.......................11

4.3 Interpretation of financial statements using appropriate ratios by using internal and

external ratios............................................................................................................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................4

1.1 Sources of finance.................................................................................................................4

1.2 Implications of the different sources.....................................................................................4

1.3 Appropriate sources of finance.............................................................................................5

2.1 Cost of different sources.......................................................................................................5

2.2 Importance of financial planning..........................................................................................5

2.3 Information needs of different decision makers....................................................................6

2.4 Impact of finance on financial statements.............................................................................6

3.1 Cash budget for the business entity.......................................................................................6

3.2 Calculation of Unit Cost........................................................................................................7

3.3 Viability of a project by using the investment appraisal technique......................................8

TASK 2..........................................................................................................................................11

4.1 Different financial statements.............................................................................................11

4.2 In the different type of business have to use different financial statements.......................11

4.3 Interpretation of financial statements using appropriate ratios by using internal and

external ratios............................................................................................................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

Management of finance is necessary in each and every company as it helps in attaining

the goals and objectives. Financial management includes the different functions that is planning,

organising, controlling along with the monitoring of the financial resources so that they can

achieve the organisational objectives (Arthur, Cheng and Czernkowski, 2010). For managing the

different financial resources they have to make proper and appropriate plans which succour in

managing the standard of the business entity in the different market. They have to utilise

appropriate resources in managing all the operational activities so that they can attain the targets

as well as success in the market place at the time of high competition (Financial Resource

Management, 2016). The present report is focused on J Sainsbury PLC which is a largest

supermarket in UK. In the below mentioned report, discussion based on the different sources of

finance. Along with the calculation of cost so that product should be sell efficiently.

TASK 1

1.1 Sources of finance

In any business finance is very important thing and there are various ways through which

it can be collected and those are known as sources of finance. Finance can be obtained for short

term or long term as per the requirement (Bennouna, Meredith and Marchant, 2010). There are

basically two main sources of finance available on the basis of source of generation which are

internal sources which are found inside the business and second one is external sources of

finance which are found outside the J Sainsbury PLC.

Internal sources of finance:- These are those sources which are obtained from insides of

business. Some of the internal sources are retained earnings, controlling or reduction of working

capital, and sale of assets etc.. owned capital and internal sources have same characteristic. The

main advantage of these sources are that for them dependence on outside party is not required

(Bodie, 2013).

External sources of finance:- the sources which are to be obtained from outside. Some of them

are loans, debentures, hire purchase grants etc.

1.2 Implications of the different sources

There are various sources of finance and they have different implications of them.

Implication may be positive or negative. In case of loans it is that the amount to be repaid at

Management of finance is necessary in each and every company as it helps in attaining

the goals and objectives. Financial management includes the different functions that is planning,

organising, controlling along with the monitoring of the financial resources so that they can

achieve the organisational objectives (Arthur, Cheng and Czernkowski, 2010). For managing the

different financial resources they have to make proper and appropriate plans which succour in

managing the standard of the business entity in the different market. They have to utilise

appropriate resources in managing all the operational activities so that they can attain the targets

as well as success in the market place at the time of high competition (Financial Resource

Management, 2016). The present report is focused on J Sainsbury PLC which is a largest

supermarket in UK. In the below mentioned report, discussion based on the different sources of

finance. Along with the calculation of cost so that product should be sell efficiently.

TASK 1

1.1 Sources of finance

In any business finance is very important thing and there are various ways through which

it can be collected and those are known as sources of finance. Finance can be obtained for short

term or long term as per the requirement (Bennouna, Meredith and Marchant, 2010). There are

basically two main sources of finance available on the basis of source of generation which are

internal sources which are found inside the business and second one is external sources of

finance which are found outside the J Sainsbury PLC.

Internal sources of finance:- These are those sources which are obtained from insides of

business. Some of the internal sources are retained earnings, controlling or reduction of working

capital, and sale of assets etc.. owned capital and internal sources have same characteristic. The

main advantage of these sources are that for them dependence on outside party is not required

(Bodie, 2013).

External sources of finance:- the sources which are to be obtained from outside. Some of them

are loans, debentures, hire purchase grants etc.

1.2 Implications of the different sources

There are various sources of finance and they have different implications of them.

Implication may be positive or negative. In case of loans it is that the amount to be repaid at

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

intervals is fixed and the bank cannot demand it anytime. But it also has a disadvantage that it

carries a interest rate and also some special fees is added in case any covenant is broken and

some legal cost are to be incurred (Bradbury, 2011). Than comes the securities which is a

financial instrument issued by the J Sainsbury PLC and can be traded. It includes loan stocks,

debentures, etc. and they have a fixed rate of interest and they can be converted into ordinary

shares. Then comes the Equities which is known as the finance with least risk. In this investors

will earn more return if they take more risk that is higher the risk higher will be the return

(Financial Resources Management (FiRM), 2017).

1.3 Appropriate sources of finance

For choosing the source of finance it should be considered that we choose the most

appropriate source for which there are various factors which are to be considered. Some of the

factors are cost in which two things will have to be considered that is the cost incurred for the

procurement of the funds and also the cost which will be required for its utilisation. Then the

purpose and the time period for which it is to be acquired should be considered (Carballo-Penela

and Doménech, 2010). Finance required for a short period of time can be borrowed through trade

credit on which rate of interest is low and the funds which are required for long term shares or

debentures can b considered as they will be more appropriate for it. Next is the form of the

organisation and its legal status as in case of J Sainsbury PLC it can rais funds with the help of

issuing shares.

2.1 Cost of different sources

in order to avail different different sources of finance there is a need to incur various cost

in order to get them. As in case of a loan that is taken from any bank J Sainsbury PLC will have

to pay interest at the rate specified in the agreement and also if any default is made in the

procedure then additional charges will also be required to be paid. Then next in case of equity

that is share issued by J Sainsbury PLC it will required to pay the dividend to the shareholders at

a specified rate from its earnings and there should be no default made in context of it (Collier,

and et. al., 2010). In case of debentures also J Sainsbury PLC will have to pay certain interest at

the pre defined rate. Due to all this internal sources are considered somewhere better as in case of

that such as retained earnings there will be no extra cost that will be required to be incurred.

carries a interest rate and also some special fees is added in case any covenant is broken and

some legal cost are to be incurred (Bradbury, 2011). Than comes the securities which is a

financial instrument issued by the J Sainsbury PLC and can be traded. It includes loan stocks,

debentures, etc. and they have a fixed rate of interest and they can be converted into ordinary

shares. Then comes the Equities which is known as the finance with least risk. In this investors

will earn more return if they take more risk that is higher the risk higher will be the return

(Financial Resources Management (FiRM), 2017).

1.3 Appropriate sources of finance

For choosing the source of finance it should be considered that we choose the most

appropriate source for which there are various factors which are to be considered. Some of the

factors are cost in which two things will have to be considered that is the cost incurred for the

procurement of the funds and also the cost which will be required for its utilisation. Then the

purpose and the time period for which it is to be acquired should be considered (Carballo-Penela

and Doménech, 2010). Finance required for a short period of time can be borrowed through trade

credit on which rate of interest is low and the funds which are required for long term shares or

debentures can b considered as they will be more appropriate for it. Next is the form of the

organisation and its legal status as in case of J Sainsbury PLC it can rais funds with the help of

issuing shares.

2.1 Cost of different sources

in order to avail different different sources of finance there is a need to incur various cost

in order to get them. As in case of a loan that is taken from any bank J Sainsbury PLC will have

to pay interest at the rate specified in the agreement and also if any default is made in the

procedure then additional charges will also be required to be paid. Then next in case of equity

that is share issued by J Sainsbury PLC it will required to pay the dividend to the shareholders at

a specified rate from its earnings and there should be no default made in context of it (Collier,

and et. al., 2010). In case of debentures also J Sainsbury PLC will have to pay certain interest at

the pre defined rate. Due to all this internal sources are considered somewhere better as in case of

that such as retained earnings there will be no extra cost that will be required to be incurred.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2.2 Importance of financial planning

determining the amount of finance required and how it will be utilised is known as

financial planning. It is very important for J Sainsbury PLC to carry on the business effectively

and efficiently. With the help of financial planning collection of optimum funds can be

facilitated as it will avoid wastage (Collins, Hribar and Tian, 2014). By this an appropriate

capital structure could be fixed which means funds can be collected from the most appropriate

sources at most appropriate time. By proper planning funds can be utilised in a proper way and

can also be invested in most profitable options. It will establish a control over the finance as due

to planning financial activities could be checked with the help of comparing estimated and the

actual figures. As the funds will be available at right time any hindrance will not have to be faced

while conducting any operational work.

2.3 Information needs of different decision makers

The different decision makers will require different types of information in order to take

the most appropriate decisions. The finance department will require information in relation to

finance for taking financial decisions which they can obtain from the financial statements of J

Sainsbury PLC. This will include the profit and loss account which will be proving information

regarding efficient utilisation of funds, the balance sheet will provide the department with the

information regarding the assets and the liabilities of the business and also about its liquidity

(Cui and Ryan, 2011). Information regarding purchase and sales and other expenses can also be

obtained and on the basis of all this information decisions will be made on how the cost can be

reduced, sales can be increased and if any new asset is required to be purchased. By all these

decisions in all the profitability of J Sainsbury PLC can be increased.

2.4 Impact of finance on financial statements

financial statements include balance sheet, profit and loss account, and cash flow

statements. There are various aspects of finance such as sales, purchase, expenses, payment of

dividend,etc. Which will have impact on the financial statements. As in case of sales it will lead

to increase in revenue and the cost of goods sold associated with it and thereby having an effect

on the net profit. It will also have impact on balance sheet as sales will also lead to change in the

cash available with the company (Drivelos and Georgiou, 2012). Then comes the amount of

money collected from the debtors it will decrease the amount of receivables but on the other

determining the amount of finance required and how it will be utilised is known as

financial planning. It is very important for J Sainsbury PLC to carry on the business effectively

and efficiently. With the help of financial planning collection of optimum funds can be

facilitated as it will avoid wastage (Collins, Hribar and Tian, 2014). By this an appropriate

capital structure could be fixed which means funds can be collected from the most appropriate

sources at most appropriate time. By proper planning funds can be utilised in a proper way and

can also be invested in most profitable options. It will establish a control over the finance as due

to planning financial activities could be checked with the help of comparing estimated and the

actual figures. As the funds will be available at right time any hindrance will not have to be faced

while conducting any operational work.

2.3 Information needs of different decision makers

The different decision makers will require different types of information in order to take

the most appropriate decisions. The finance department will require information in relation to

finance for taking financial decisions which they can obtain from the financial statements of J

Sainsbury PLC. This will include the profit and loss account which will be proving information

regarding efficient utilisation of funds, the balance sheet will provide the department with the

information regarding the assets and the liabilities of the business and also about its liquidity

(Cui and Ryan, 2011). Information regarding purchase and sales and other expenses can also be

obtained and on the basis of all this information decisions will be made on how the cost can be

reduced, sales can be increased and if any new asset is required to be purchased. By all these

decisions in all the profitability of J Sainsbury PLC can be increased.

2.4 Impact of finance on financial statements

financial statements include balance sheet, profit and loss account, and cash flow

statements. There are various aspects of finance such as sales, purchase, expenses, payment of

dividend,etc. Which will have impact on the financial statements. As in case of sales it will lead

to increase in revenue and the cost of goods sold associated with it and thereby having an effect

on the net profit. It will also have impact on balance sheet as sales will also lead to change in the

cash available with the company (Drivelos and Georgiou, 2012). Then comes the amount of

money collected from the debtors it will decrease the amount of receivables but on the other

hand will increase the cash level. Next comes the issue of shares it will increase the interest cost

and also company will be required to pay the dividend thereby affecting profit and loss account.

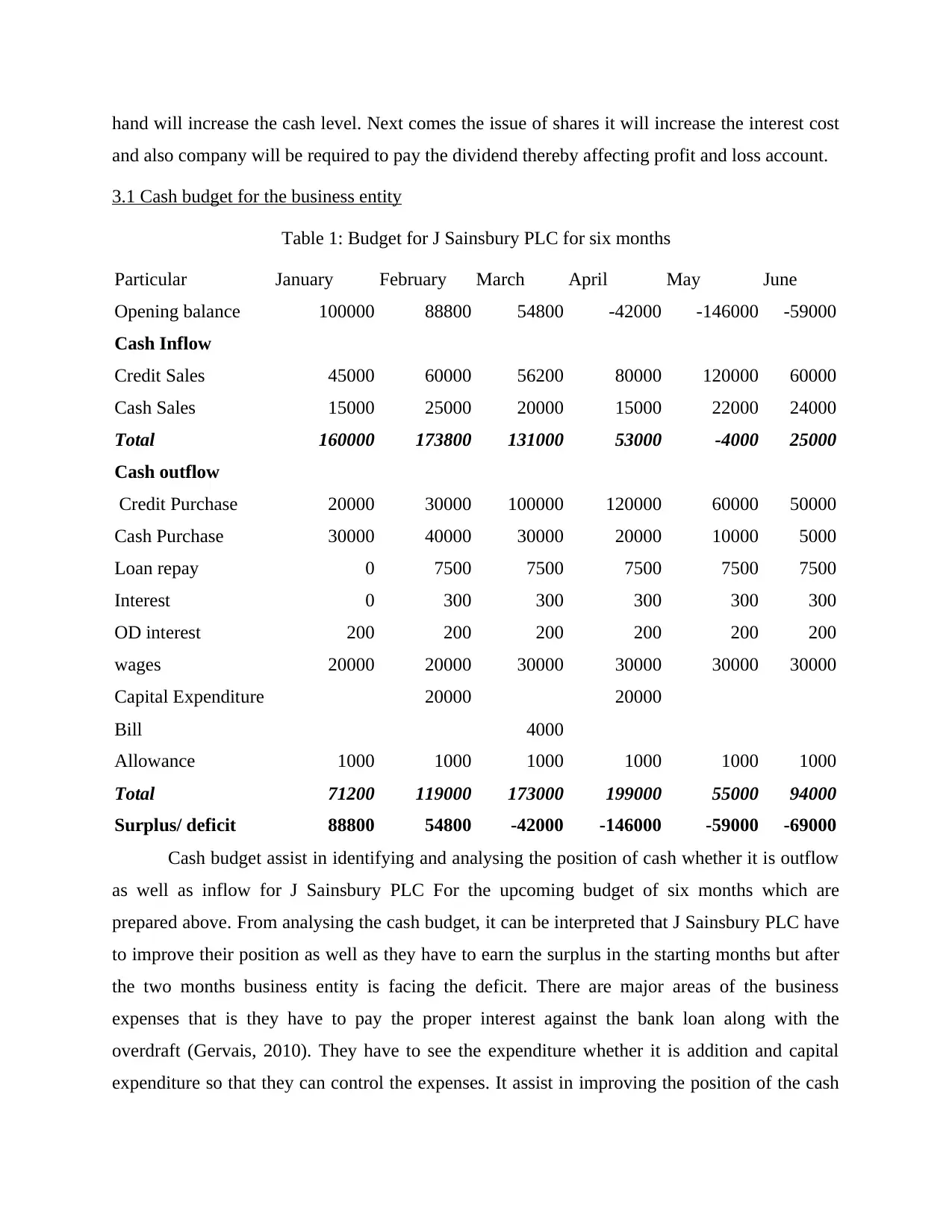

3.1 Cash budget for the business entity

Table 1: Budget for J Sainsbury PLC for six months

Particular January February March April May June

Opening balance 100000 88800 54800 -42000 -146000 -59000

Cash Inflow

Credit Sales 45000 60000 56200 80000 120000 60000

Cash Sales 15000 25000 20000 15000 22000 24000

Total 160000 173800 131000 53000 -4000 25000

Cash outflow

Credit Purchase 20000 30000 100000 120000 60000 50000

Cash Purchase 30000 40000 30000 20000 10000 5000

Loan repay 0 7500 7500 7500 7500 7500

Interest 0 300 300 300 300 300

OD interest 200 200 200 200 200 200

wages 20000 20000 30000 30000 30000 30000

Capital Expenditure 20000 20000

Bill 4000

Allowance 1000 1000 1000 1000 1000 1000

Total 71200 119000 173000 199000 55000 94000

Surplus/ deficit 88800 54800 -42000 -146000 -59000 -69000

Cash budget assist in identifying and analysing the position of cash whether it is outflow

as well as inflow for J Sainsbury PLC For the upcoming budget of six months which are

prepared above. From analysing the cash budget, it can be interpreted that J Sainsbury PLC have

to improve their position as well as they have to earn the surplus in the starting months but after

the two months business entity is facing the deficit. There are major areas of the business

expenses that is they have to pay the proper interest against the bank loan along with the

overdraft (Gervais, 2010). They have to see the expenditure whether it is addition and capital

expenditure so that they can control the expenses. It assist in improving the position of the cash

and also company will be required to pay the dividend thereby affecting profit and loss account.

3.1 Cash budget for the business entity

Table 1: Budget for J Sainsbury PLC for six months

Particular January February March April May June

Opening balance 100000 88800 54800 -42000 -146000 -59000

Cash Inflow

Credit Sales 45000 60000 56200 80000 120000 60000

Cash Sales 15000 25000 20000 15000 22000 24000

Total 160000 173800 131000 53000 -4000 25000

Cash outflow

Credit Purchase 20000 30000 100000 120000 60000 50000

Cash Purchase 30000 40000 30000 20000 10000 5000

Loan repay 0 7500 7500 7500 7500 7500

Interest 0 300 300 300 300 300

OD interest 200 200 200 200 200 200

wages 20000 20000 30000 30000 30000 30000

Capital Expenditure 20000 20000

Bill 4000

Allowance 1000 1000 1000 1000 1000 1000

Total 71200 119000 173000 199000 55000 94000

Surplus/ deficit 88800 54800 -42000 -146000 -59000 -69000

Cash budget assist in identifying and analysing the position of cash whether it is outflow

as well as inflow for J Sainsbury PLC For the upcoming budget of six months which are

prepared above. From analysing the cash budget, it can be interpreted that J Sainsbury PLC have

to improve their position as well as they have to earn the surplus in the starting months but after

the two months business entity is facing the deficit. There are major areas of the business

expenses that is they have to pay the proper interest against the bank loan along with the

overdraft (Gervais, 2010). They have to see the expenditure whether it is addition and capital

expenditure so that they can control the expenses. It assist in improving the position of the cash

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and this can be only be done by using the appropriate management techniques so that they can

attain the success.

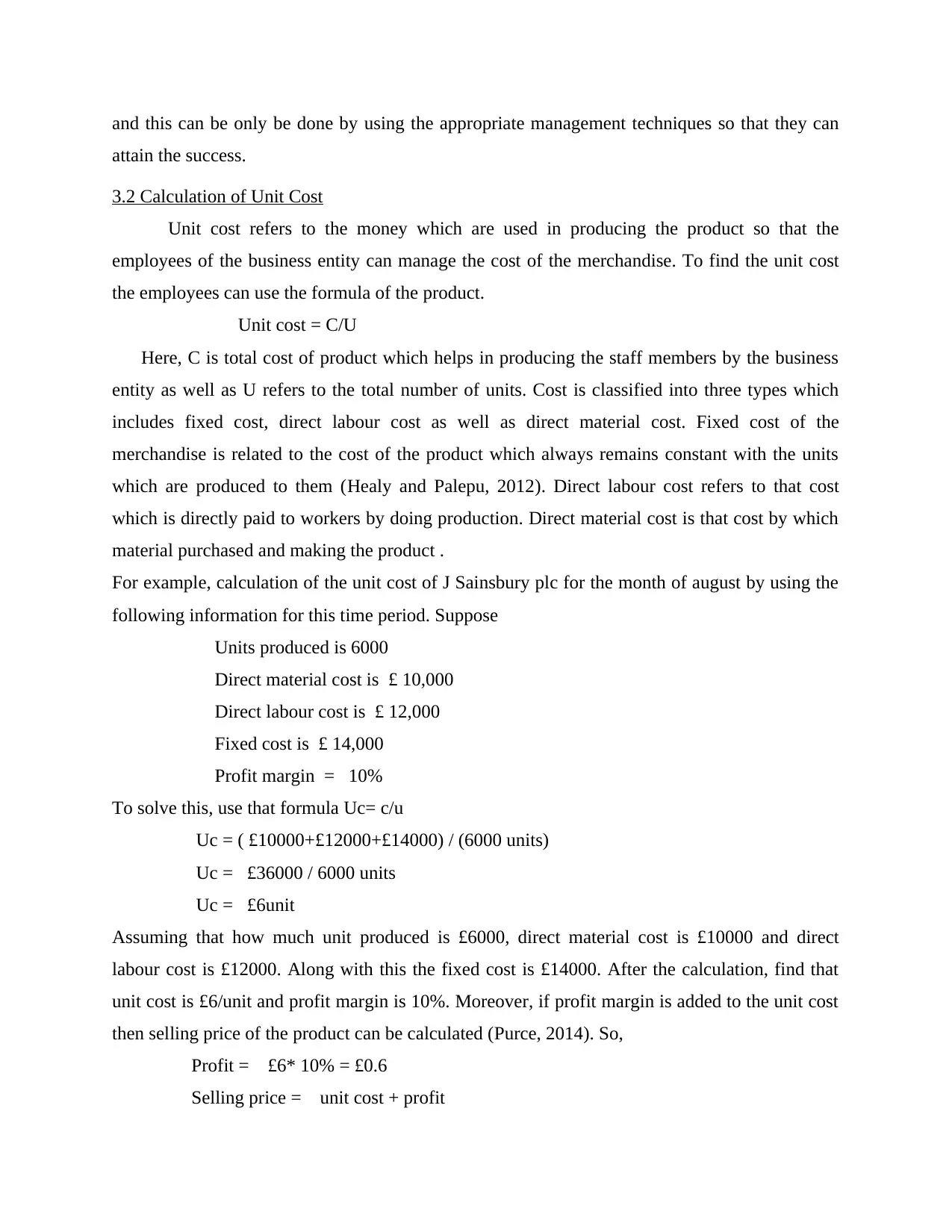

3.2 Calculation of Unit Cost

Unit cost refers to the money which are used in producing the product so that the

employees of the business entity can manage the cost of the merchandise. To find the unit cost

the employees can use the formula of the product.

Unit cost = C/U

Here, C is total cost of product which helps in producing the staff members by the business

entity as well as U refers to the total number of units. Cost is classified into three types which

includes fixed cost, direct labour cost as well as direct material cost. Fixed cost of the

merchandise is related to the cost of the product which always remains constant with the units

which are produced to them (Healy and Palepu, 2012). Direct labour cost refers to that cost

which is directly paid to workers by doing production. Direct material cost is that cost by which

material purchased and making the product .

For example, calculation of the unit cost of J Sainsbury plc for the month of august by using the

following information for this time period. Suppose

Units produced is 6000

Direct material cost is £ 10,000

Direct labour cost is £ 12,000

Fixed cost is £ 14,000

Profit margin = 10%

To solve this, use that formula Uc= c/u

Uc = ( £10000+£12000+£14000) / (6000 units)

Uc = £36000 / 6000 units

Uc = £6unit

Assuming that how much unit produced is £6000, direct material cost is £10000 and direct

labour cost is £12000. Along with this the fixed cost is £14000. After the calculation, find that

unit cost is £6/unit and profit margin is 10%. Moreover, if profit margin is added to the unit cost

then selling price of the product can be calculated (Purce, 2014). So,

Profit = £6* 10% = £0.6

Selling price = unit cost + profit

attain the success.

3.2 Calculation of Unit Cost

Unit cost refers to the money which are used in producing the product so that the

employees of the business entity can manage the cost of the merchandise. To find the unit cost

the employees can use the formula of the product.

Unit cost = C/U

Here, C is total cost of product which helps in producing the staff members by the business

entity as well as U refers to the total number of units. Cost is classified into three types which

includes fixed cost, direct labour cost as well as direct material cost. Fixed cost of the

merchandise is related to the cost of the product which always remains constant with the units

which are produced to them (Healy and Palepu, 2012). Direct labour cost refers to that cost

which is directly paid to workers by doing production. Direct material cost is that cost by which

material purchased and making the product .

For example, calculation of the unit cost of J Sainsbury plc for the month of august by using the

following information for this time period. Suppose

Units produced is 6000

Direct material cost is £ 10,000

Direct labour cost is £ 12,000

Fixed cost is £ 14,000

Profit margin = 10%

To solve this, use that formula Uc= c/u

Uc = ( £10000+£12000+£14000) / (6000 units)

Uc = £36000 / 6000 units

Uc = £6unit

Assuming that how much unit produced is £6000, direct material cost is £10000 and direct

labour cost is £12000. Along with this the fixed cost is £14000. After the calculation, find that

unit cost is £6/unit and profit margin is 10%. Moreover, if profit margin is added to the unit cost

then selling price of the product can be calculated (Purce, 2014). So,

Profit = £6* 10% = £0.6

Selling price = unit cost + profit

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

SP = £6+ £0.6

SP = £6.06

So, selling price of the product is £6.06 and on the basis of that J Sainsbury PLC earn £0.6 profit.

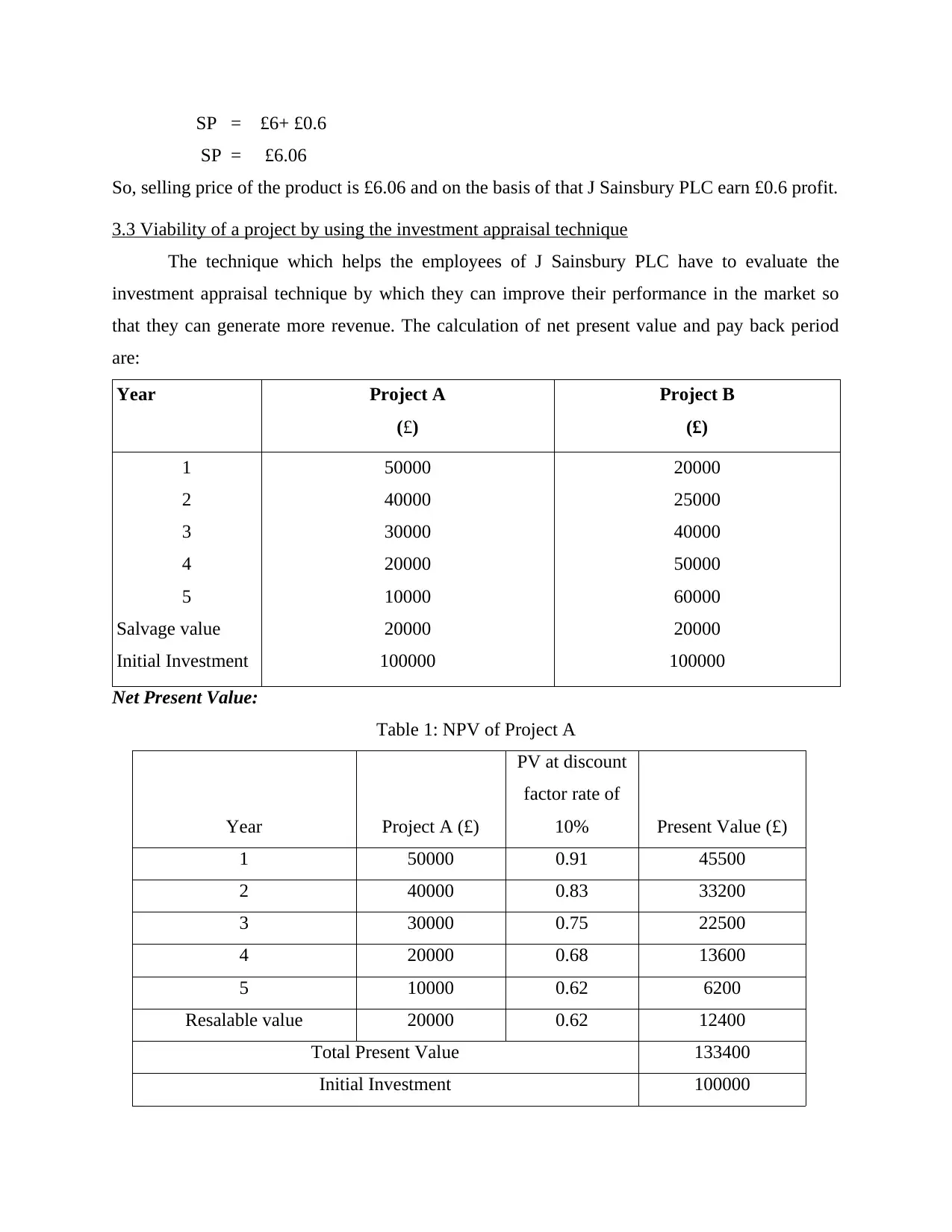

3.3 Viability of a project by using the investment appraisal technique

The technique which helps the employees of J Sainsbury PLC have to evaluate the

investment appraisal technique by which they can improve their performance in the market so

that they can generate more revenue. The calculation of net present value and pay back period

are:

Year Project A

(£)

Project B

(£)

1

2

3

4

5

Salvage value

Initial Investment

50000

40000

30000

20000

10000

20000

100000

20000

25000

40000

50000

60000

20000

100000

Net Present Value:

Table 1: NPV of Project A

Year Project A (£)

PV at discount

factor rate of

10% Present Value (£)

1 50000 0.91 45500

2 40000 0.83 33200

3 30000 0.75 22500

4 20000 0.68 13600

5 10000 0.62 6200

Resalable value 20000 0.62 12400

Total Present Value 133400

Initial Investment 100000

SP = £6.06

So, selling price of the product is £6.06 and on the basis of that J Sainsbury PLC earn £0.6 profit.

3.3 Viability of a project by using the investment appraisal technique

The technique which helps the employees of J Sainsbury PLC have to evaluate the

investment appraisal technique by which they can improve their performance in the market so

that they can generate more revenue. The calculation of net present value and pay back period

are:

Year Project A

(£)

Project B

(£)

1

2

3

4

5

Salvage value

Initial Investment

50000

40000

30000

20000

10000

20000

100000

20000

25000

40000

50000

60000

20000

100000

Net Present Value:

Table 1: NPV of Project A

Year Project A (£)

PV at discount

factor rate of

10% Present Value (£)

1 50000 0.91 45500

2 40000 0.83 33200

3 30000 0.75 22500

4 20000 0.68 13600

5 10000 0.62 6200

Resalable value 20000 0.62 12400

Total Present Value 133400

Initial Investment 100000

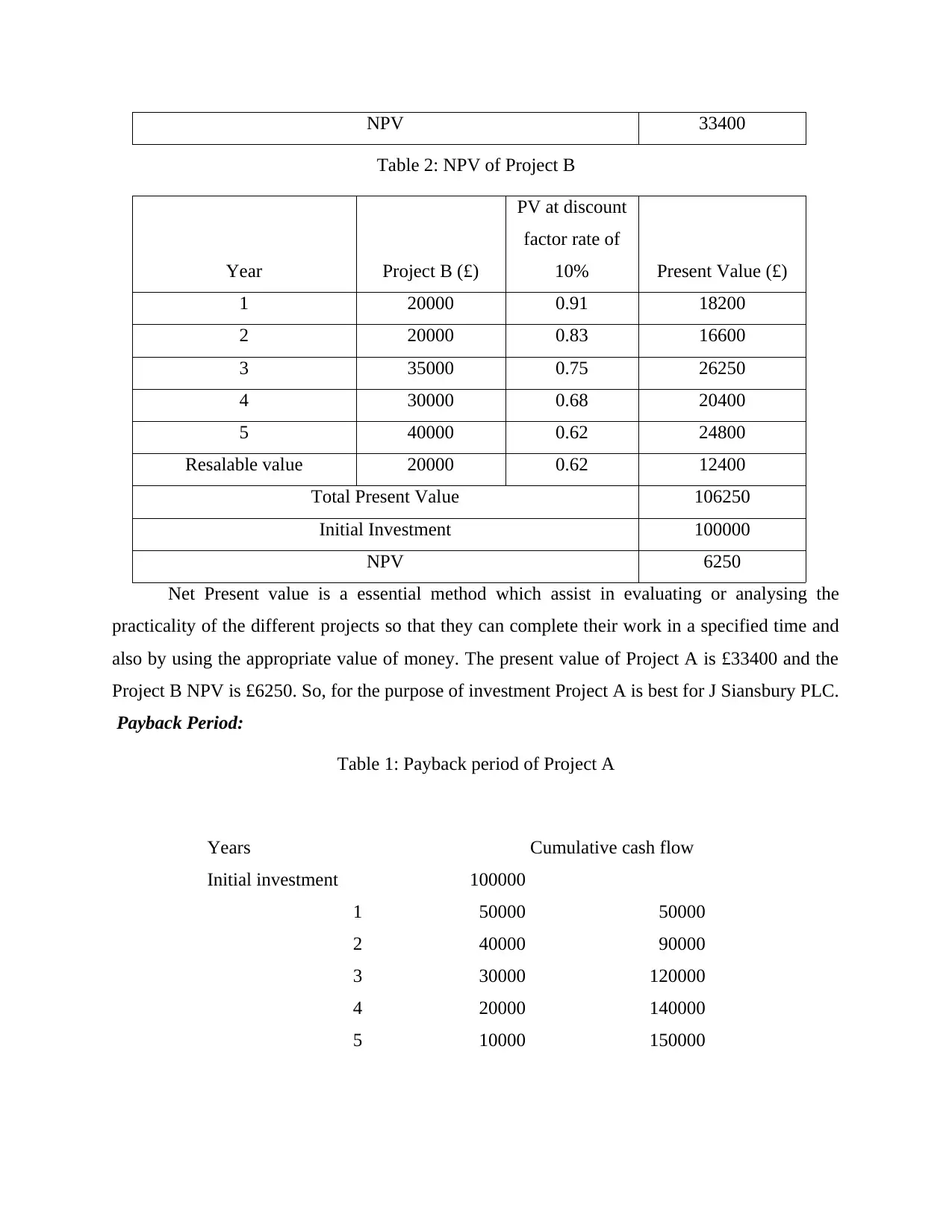

NPV 33400

Table 2: NPV of Project B

Year Project B (£)

PV at discount

factor rate of

10% Present Value (£)

1 20000 0.91 18200

2 20000 0.83 16600

3 35000 0.75 26250

4 30000 0.68 20400

5 40000 0.62 24800

Resalable value 20000 0.62 12400

Total Present Value 106250

Initial Investment 100000

NPV 6250

Net Present value is a essential method which assist in evaluating or analysing the

practicality of the different projects so that they can complete their work in a specified time and

also by using the appropriate value of money. The present value of Project A is £33400 and the

Project B NPV is £6250. So, for the purpose of investment Project A is best for J Siansbury PLC.

Payback Period:

Table 1: Payback period of Project A

Years Cumulative cash flow

Initial investment 100000

1 50000 50000

2 40000 90000

3 30000 120000

4 20000 140000

5 10000 150000

Table 2: NPV of Project B

Year Project B (£)

PV at discount

factor rate of

10% Present Value (£)

1 20000 0.91 18200

2 20000 0.83 16600

3 35000 0.75 26250

4 30000 0.68 20400

5 40000 0.62 24800

Resalable value 20000 0.62 12400

Total Present Value 106250

Initial Investment 100000

NPV 6250

Net Present value is a essential method which assist in evaluating or analysing the

practicality of the different projects so that they can complete their work in a specified time and

also by using the appropriate value of money. The present value of Project A is £33400 and the

Project B NPV is £6250. So, for the purpose of investment Project A is best for J Siansbury PLC.

Payback Period:

Table 1: Payback period of Project A

Years Cumulative cash flow

Initial investment 100000

1 50000 50000

2 40000 90000

3 30000 120000

4 20000 140000

5 10000 150000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

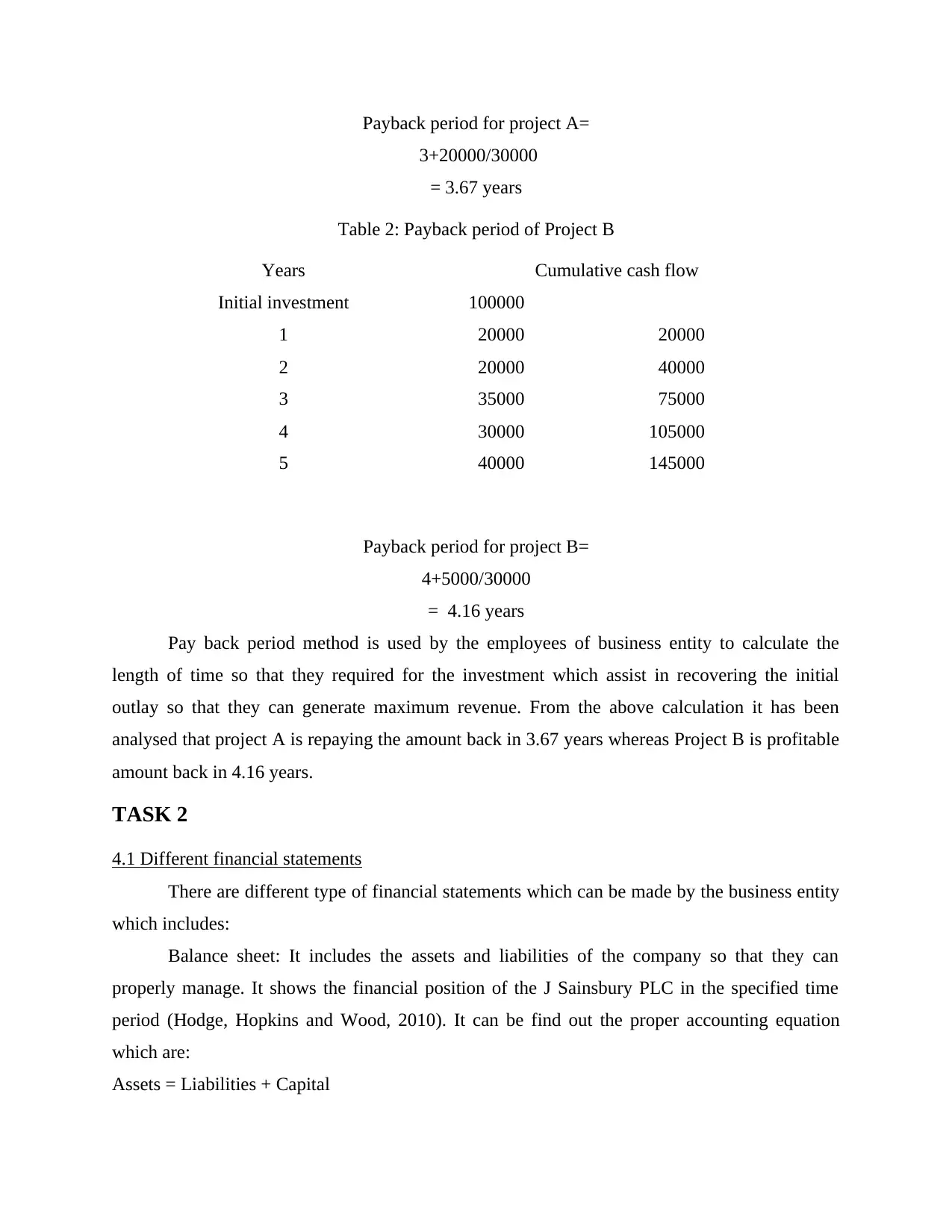

Payback period for project A=

3+20000/30000

= 3.67 years

Table 2: Payback period of Project B

Years Cumulative cash flow

Initial investment 100000

1 20000 20000

2 20000 40000

3 35000 75000

4 30000 105000

5 40000 145000

Payback period for project B=

4+5000/30000

= 4.16 years

Pay back period method is used by the employees of business entity to calculate the

length of time so that they required for the investment which assist in recovering the initial

outlay so that they can generate maximum revenue. From the above calculation it has been

analysed that project A is repaying the amount back in 3.67 years whereas Project B is profitable

amount back in 4.16 years.

TASK 2

4.1 Different financial statements

There are different type of financial statements which can be made by the business entity

which includes:

Balance sheet: It includes the assets and liabilities of the company so that they can

properly manage. It shows the financial position of the J Sainsbury PLC in the specified time

period (Hodge, Hopkins and Wood, 2010). It can be find out the proper accounting equation

which are:

Assets = Liabilities + Capital

3+20000/30000

= 3.67 years

Table 2: Payback period of Project B

Years Cumulative cash flow

Initial investment 100000

1 20000 20000

2 20000 40000

3 35000 75000

4 30000 105000

5 40000 145000

Payback period for project B=

4+5000/30000

= 4.16 years

Pay back period method is used by the employees of business entity to calculate the

length of time so that they required for the investment which assist in recovering the initial

outlay so that they can generate maximum revenue. From the above calculation it has been

analysed that project A is repaying the amount back in 3.67 years whereas Project B is profitable

amount back in 4.16 years.

TASK 2

4.1 Different financial statements

There are different type of financial statements which can be made by the business entity

which includes:

Balance sheet: It includes the assets and liabilities of the company so that they can

properly manage. It shows the financial position of the J Sainsbury PLC in the specified time

period (Hodge, Hopkins and Wood, 2010). It can be find out the proper accounting equation

which are:

Assets = Liabilities + Capital

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Income statement: It is also a type of financial statement which can be used by J

Sainsbury PLC and it includes all the income and expenditure of the company and by which they

can identify the financial position of the business in the given accounting period. Along with this

it assist in identifying the profit and loss.

Cash flow statement: It is also included in the financial statement and it helps in

managing the cash as well as liquidity of the J Sainsbury PLC. Along with this it helps in

identifying the cash inflow and outflow of the business entity and by that they can attain the

success in the market (Kirkham, 2012).

4.2 In the different type of business have to use different financial statements

There are different type of business entities which are using the different financial

statements that is:

Sole proprietorship: It is a type of business entity which is run by a single person and in

this the owner of the company having all rights. In this business owners can use the financial

statements to manage the income and expenditure and this includes the income statement and

balance sheet so that they can manage their cash in the marketplace.

Partnership: It is a type of business which is run by the two or more persons and they

enter in the partnership by taking the some amount of capital. The financial statements which

they can make that are income statement, balance sheet and the statement of partner's account

(Kumbirai and Webb, 2010).

Corporations: It is also a part of the different type of business entities and it is owned and

run by the legal person by using the appropriate laws as well as rules and regulations. They can

make the different financial statements and they are P&L account, income statement, cash flow

statement and balance sheet.

4.3 Interpretation of financial statements using appropriate ratios by using internal and external

ratios

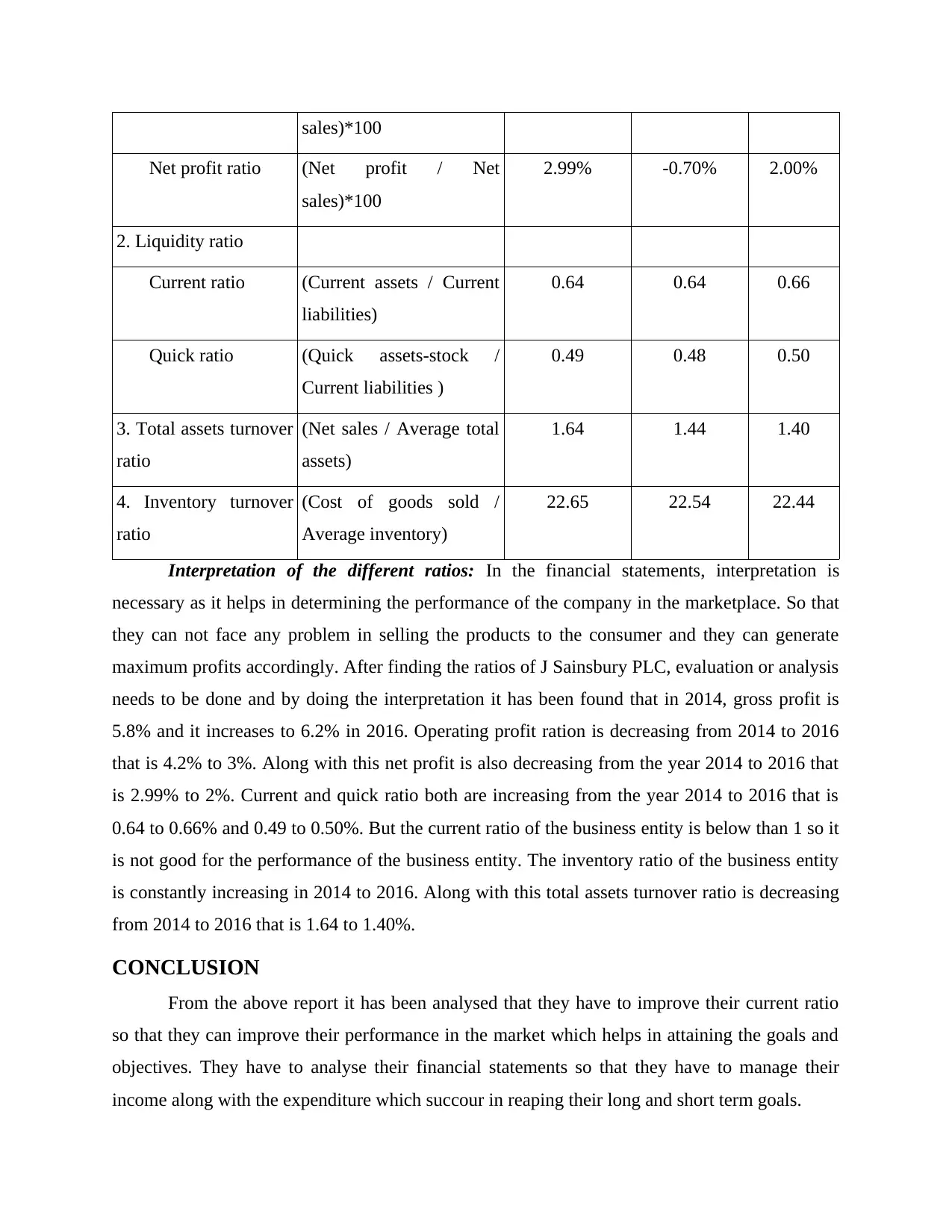

Ratios Formula 2014 2015 2016

1.Profitability ratio

Gross profit ratio (Gross profit / Net

sales)*100

5.8% 5.1% 6.2%

Operating profit ratio (Operating profit / Net 4.2% 0.3% 3.0%

Sainsbury PLC and it includes all the income and expenditure of the company and by which they

can identify the financial position of the business in the given accounting period. Along with this

it assist in identifying the profit and loss.

Cash flow statement: It is also included in the financial statement and it helps in

managing the cash as well as liquidity of the J Sainsbury PLC. Along with this it helps in

identifying the cash inflow and outflow of the business entity and by that they can attain the

success in the market (Kirkham, 2012).

4.2 In the different type of business have to use different financial statements

There are different type of business entities which are using the different financial

statements that is:

Sole proprietorship: It is a type of business entity which is run by a single person and in

this the owner of the company having all rights. In this business owners can use the financial

statements to manage the income and expenditure and this includes the income statement and

balance sheet so that they can manage their cash in the marketplace.

Partnership: It is a type of business which is run by the two or more persons and they

enter in the partnership by taking the some amount of capital. The financial statements which

they can make that are income statement, balance sheet and the statement of partner's account

(Kumbirai and Webb, 2010).

Corporations: It is also a part of the different type of business entities and it is owned and

run by the legal person by using the appropriate laws as well as rules and regulations. They can

make the different financial statements and they are P&L account, income statement, cash flow

statement and balance sheet.

4.3 Interpretation of financial statements using appropriate ratios by using internal and external

ratios

Ratios Formula 2014 2015 2016

1.Profitability ratio

Gross profit ratio (Gross profit / Net

sales)*100

5.8% 5.1% 6.2%

Operating profit ratio (Operating profit / Net 4.2% 0.3% 3.0%

sales)*100

Net profit ratio (Net profit / Net

sales)*100

2.99% -0.70% 2.00%

2. Liquidity ratio

Current ratio (Current assets / Current

liabilities)

0.64 0.64 0.66

Quick ratio (Quick assets-stock /

Current liabilities )

0.49 0.48 0.50

3. Total assets turnover

ratio

(Net sales / Average total

assets)

1.64 1.44 1.40

4. Inventory turnover

ratio

(Cost of goods sold /

Average inventory)

22.65 22.54 22.44

Interpretation of the different ratios: In the financial statements, interpretation is

necessary as it helps in determining the performance of the company in the marketplace. So that

they can not face any problem in selling the products to the consumer and they can generate

maximum profits accordingly. After finding the ratios of J Sainsbury PLC, evaluation or analysis

needs to be done and by doing the interpretation it has been found that in 2014, gross profit is

5.8% and it increases to 6.2% in 2016. Operating profit ration is decreasing from 2014 to 2016

that is 4.2% to 3%. Along with this net profit is also decreasing from the year 2014 to 2016 that

is 2.99% to 2%. Current and quick ratio both are increasing from the year 2014 to 2016 that is

0.64 to 0.66% and 0.49 to 0.50%. But the current ratio of the business entity is below than 1 so it

is not good for the performance of the business entity. The inventory ratio of the business entity

is constantly increasing in 2014 to 2016. Along with this total assets turnover ratio is decreasing

from 2014 to 2016 that is 1.64 to 1.40%.

CONCLUSION

From the above report it has been analysed that they have to improve their current ratio

so that they can improve their performance in the market which helps in attaining the goals and

objectives. They have to analyse their financial statements so that they have to manage their

income along with the expenditure which succour in reaping their long and short term goals.

Net profit ratio (Net profit / Net

sales)*100

2.99% -0.70% 2.00%

2. Liquidity ratio

Current ratio (Current assets / Current

liabilities)

0.64 0.64 0.66

Quick ratio (Quick assets-stock /

Current liabilities )

0.49 0.48 0.50

3. Total assets turnover

ratio

(Net sales / Average total

assets)

1.64 1.44 1.40

4. Inventory turnover

ratio

(Cost of goods sold /

Average inventory)

22.65 22.54 22.44

Interpretation of the different ratios: In the financial statements, interpretation is

necessary as it helps in determining the performance of the company in the marketplace. So that

they can not face any problem in selling the products to the consumer and they can generate

maximum profits accordingly. After finding the ratios of J Sainsbury PLC, evaluation or analysis

needs to be done and by doing the interpretation it has been found that in 2014, gross profit is

5.8% and it increases to 6.2% in 2016. Operating profit ration is decreasing from 2014 to 2016

that is 4.2% to 3%. Along with this net profit is also decreasing from the year 2014 to 2016 that

is 2.99% to 2%. Current and quick ratio both are increasing from the year 2014 to 2016 that is

0.64 to 0.66% and 0.49 to 0.50%. But the current ratio of the business entity is below than 1 so it

is not good for the performance of the business entity. The inventory ratio of the business entity

is constantly increasing in 2014 to 2016. Along with this total assets turnover ratio is decreasing

from 2014 to 2016 that is 1.64 to 1.40%.

CONCLUSION

From the above report it has been analysed that they have to improve their current ratio

so that they can improve their performance in the market which helps in attaining the goals and

objectives. They have to analyse their financial statements so that they have to manage their

income along with the expenditure which succour in reaping their long and short term goals.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.