Managing Financial Resources and Decision Making Report for Tesco

VerifiedAdded on 2020/01/28

|25

|5255

|266

Report

AI Summary

This report delves into the realm of financial resource management and decision-making, using Tesco as a case study. It explores various sources of finance, including equity, debt, retained earnings, and private equity, along with their respective implications and costs. The report emphasizes the importance of financial planning and analyzes the information needs of different decision-makers, such as managers, creditors, and the government. It includes the preparation of a cash budget and the application of project evaluation techniques like payback period, ARR, NPV, and IRR. Furthermore, the report provides an analysis of financial statements, including the income statement, balance sheet, and cash flow statement, along with ratio analysis to assess Tesco's financial position. The report offers a comprehensive overview of financial management principles and their practical application within a real-world business context.

MANAGING FINANCIAL

RESPOURCES AND DECISION

MAKING

RESPOURCES AND DECISION

MAKING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

1.1 Sources of finance available to business ..............................................................................3

1.2 Implications of different source of finance...........................................................................4

1.3 Appropriate source of finance...............................................................................................5

TASK 2............................................................................................................................................5

2.1 Cost of different sources of finance......................................................................................5

2.2 Importance of financial planning for Tesco..........................................................................6

2.3 Information needs of different decision makers....................................................................6

2.4 Impact of finance on the financial statements.......................................................................7

TASK 3............................................................................................................................................7

3.1 Analysis of budget and making appropriate decisions..........................................................7

3.2 Calculation of unit cost.........................................................................................................8

3.3 Project evaluation..................................................................................................................9

TASK 4..........................................................................................................................................11

4.1 Discussion on the main financial statements......................................................................11

4.2 Format of financial statements for different organizations.................................................12

...................................................................................................................................................13

...................................................................................................................................................14

4.3 Ratio analysis......................................................................................................................20

CONCLUSION..............................................................................................................................22

REFERENCES..............................................................................................................................23

INDEX OF TABLES

Table 1: Cash budget for Tesco.......................................................................................................8

Table 2: Calculation of unit cost......................................................................................................9

Table 3: Calculation of payback period method............................................................................10

Table 4: Calculation of ARR.........................................................................................................10

Table 5: Calculation of NPV..........................................................................................................11

Table 6: Calculation of IRR...........................................................................................................11

Table 7: Ratio analysis...................................................................................................................21

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

1.1 Sources of finance available to business ..............................................................................3

1.2 Implications of different source of finance...........................................................................4

1.3 Appropriate source of finance...............................................................................................5

TASK 2............................................................................................................................................5

2.1 Cost of different sources of finance......................................................................................5

2.2 Importance of financial planning for Tesco..........................................................................6

2.3 Information needs of different decision makers....................................................................6

2.4 Impact of finance on the financial statements.......................................................................7

TASK 3............................................................................................................................................7

3.1 Analysis of budget and making appropriate decisions..........................................................7

3.2 Calculation of unit cost.........................................................................................................8

3.3 Project evaluation..................................................................................................................9

TASK 4..........................................................................................................................................11

4.1 Discussion on the main financial statements......................................................................11

4.2 Format of financial statements for different organizations.................................................12

...................................................................................................................................................13

...................................................................................................................................................14

4.3 Ratio analysis......................................................................................................................20

CONCLUSION..............................................................................................................................22

REFERENCES..............................................................................................................................23

INDEX OF TABLES

Table 1: Cash budget for Tesco.......................................................................................................8

Table 2: Calculation of unit cost......................................................................................................9

Table 3: Calculation of payback period method............................................................................10

Table 4: Calculation of ARR.........................................................................................................10

Table 5: Calculation of NPV..........................................................................................................11

Table 6: Calculation of IRR...........................................................................................................11

Table 7: Ratio analysis...................................................................................................................21

ILLUSTRATION INDEX

Illustration 1: Income statement of the company...........................................................................13

Illustration 2: Balance sheet of the company.................................................................................14

Illustration 3: Cash flow statement of the company......................................................................15

Illustration 4: Income statement of sole trader..............................................................................16

Illustration 5: Balance sheet of sole trader.....................................................................................17

Illustration 6: Cash flow statement of sole trader..........................................................................18

Illustration 7: Income statement of partnership.............................................................................19

Illustration 8: Balance sheet of the partnership..............................................................................20

Illustration 9: Cash flow statement of partnership.........................................................................21

Illustration 1: Income statement of the company...........................................................................13

Illustration 2: Balance sheet of the company.................................................................................14

Illustration 3: Cash flow statement of the company......................................................................15

Illustration 4: Income statement of sole trader..............................................................................16

Illustration 5: Balance sheet of sole trader.....................................................................................17

Illustration 6: Cash flow statement of sole trader..........................................................................18

Illustration 7: Income statement of partnership.............................................................................19

Illustration 8: Balance sheet of the partnership..............................................................................20

Illustration 9: Cash flow statement of partnership.........................................................................21

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Finance is a life blood for any organization and no company can survive longer in the

absence of sufficient availability of finance. Tesco is one of the UK largest retail chain stores

that have a 29% market share in the entire industry. In the report Tesco is taken as a company in

order to understand various aspects of finance. In this report, sources of finance are made

available and discussed in detail. After that implication of each and every source of finance are

also described in the report. On the basis of implications appropriate source of finance is selected

for Tesco. Cost of source of finance also plays a key role in selection of source of finance.

Hence, in context to this, cost of each and every source of finance is discussed in the report. In

the middle part of the report cash budget is prepared and movements in the net balance are

described in detail. At the end of the report, project evaluation techniques are applied and ratio

analysis is done in order to evaluate Tesco from different sides.

TASK 1

1.1 Sources of finance available to business

There are many sources of finance that are available to business. Some of these sources

are as follows. Equity- It is a commonly used source of finance and under this, firm brings IPO or FPO

in the market. By bringing same, firm collects fund from the general public. In return,

people those makes investment in company get share in the profit earned by it. By using

this source, of finance cost of finance is controlled by the firms to large extent. Due to

this reason, equity is used by the firms to finance large sized projects. Debt- Tesco is widely used this source to fulfill its fund requirement and finance its

internal as well as external business operations. On the taken loan, firm needs to pay

interest which may be fixed or floating in nature (Davies and Crawford, 2011). If, rate of

interest is fixed then there will be no problem. But, if interest rate is floating in nature

then finance cost of the firm may increase. Hence, Sony Corporation must take loan by

using fixed interest rate. Retained earnings- It is a portion of revenue that remains after paying of all the

expenditures. This is an internal source of finance which does not have any cost of

Finance is a life blood for any organization and no company can survive longer in the

absence of sufficient availability of finance. Tesco is one of the UK largest retail chain stores

that have a 29% market share in the entire industry. In the report Tesco is taken as a company in

order to understand various aspects of finance. In this report, sources of finance are made

available and discussed in detail. After that implication of each and every source of finance are

also described in the report. On the basis of implications appropriate source of finance is selected

for Tesco. Cost of source of finance also plays a key role in selection of source of finance.

Hence, in context to this, cost of each and every source of finance is discussed in the report. In

the middle part of the report cash budget is prepared and movements in the net balance are

described in detail. At the end of the report, project evaluation techniques are applied and ratio

analysis is done in order to evaluate Tesco from different sides.

TASK 1

1.1 Sources of finance available to business

There are many sources of finance that are available to business. Some of these sources

are as follows. Equity- It is a commonly used source of finance and under this, firm brings IPO or FPO

in the market. By bringing same, firm collects fund from the general public. In return,

people those makes investment in company get share in the profit earned by it. By using

this source, of finance cost of finance is controlled by the firms to large extent. Due to

this reason, equity is used by the firms to finance large sized projects. Debt- Tesco is widely used this source to fulfill its fund requirement and finance its

internal as well as external business operations. On the taken loan, firm needs to pay

interest which may be fixed or floating in nature (Davies and Crawford, 2011). If, rate of

interest is fixed then there will be no problem. But, if interest rate is floating in nature

then finance cost of the firm may increase. Hence, Sony Corporation must take loan by

using fixed interest rate. Retained earnings- It is a portion of revenue that remains after paying of all the

expenditures. This is an internal source of finance which does not have any cost of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

capital. Due to this reason, this source is widely used by the firms in their business

practice.

Private equity- This source of finance is a variant of equity under which there is a private

equity firm which is owned a stake in the company and in return provides fund to the

firm (Elliott and Meyer, 2007). These companies purchase at least 60% stake in the

specific company in order to bring themselves in the position to influence company

decisions. This source of finance is used by the firms which are on growth stage and need

finance to accelerate growth rate.

1.2 Implications of different source of finance

Following are the implications of different source of finance. Equity- Like every source of finance, equity also has some merits and demerits. In case

of equity, firm has to pay dividend to the shareholders. However, it is not necessary to

pay dividend every year. However, the rate of dividend is always higher than interest

rate. This is the major demerit of this source of finance. On other hand, issue of shares

lead to the dilution of control in case of existing shareholders in the company (Hillier,

Grinblatt and Titman, 2011). Main advantage of equity is that finance cost is adjustable in

nature. So, it can be said that this source of finance has advantages and disadvantages and

companies by considering their internal factors must select an appropriate source of

finance. Debt- In case of debt, there is a fixed or floating finance cost but ownership of the firm

remains same in the single hand. In order to take loan, firm needs to fulfill some criteria

and require doing some paper formalities. Firms often take debt to finance their

operations instead of issuing shares. Retained earnings- There are no legal implications included in this source of finance.

Companies as per their requirements can use retained earnings. Apart from this, use of

retained earnings does not lead to dilution of control in the firm (Lin and Sun, 2006).

Hence, it can be said that this source of finance does not have any negative point.

Private equity – In order to use this source of finance, company needs to fulfill some

criteria and after that it can enter into agreement with the private equity firm. Under this

source of finance, control of the existing shareholders gets diluted that is the major

practice.

Private equity- This source of finance is a variant of equity under which there is a private

equity firm which is owned a stake in the company and in return provides fund to the

firm (Elliott and Meyer, 2007). These companies purchase at least 60% stake in the

specific company in order to bring themselves in the position to influence company

decisions. This source of finance is used by the firms which are on growth stage and need

finance to accelerate growth rate.

1.2 Implications of different source of finance

Following are the implications of different source of finance. Equity- Like every source of finance, equity also has some merits and demerits. In case

of equity, firm has to pay dividend to the shareholders. However, it is not necessary to

pay dividend every year. However, the rate of dividend is always higher than interest

rate. This is the major demerit of this source of finance. On other hand, issue of shares

lead to the dilution of control in case of existing shareholders in the company (Hillier,

Grinblatt and Titman, 2011). Main advantage of equity is that finance cost is adjustable in

nature. So, it can be said that this source of finance has advantages and disadvantages and

companies by considering their internal factors must select an appropriate source of

finance. Debt- In case of debt, there is a fixed or floating finance cost but ownership of the firm

remains same in the single hand. In order to take loan, firm needs to fulfill some criteria

and require doing some paper formalities. Firms often take debt to finance their

operations instead of issuing shares. Retained earnings- There are no legal implications included in this source of finance.

Companies as per their requirements can use retained earnings. Apart from this, use of

retained earnings does not lead to dilution of control in the firm (Lin and Sun, 2006).

Hence, it can be said that this source of finance does not have any negative point.

Private equity – In order to use this source of finance, company needs to fulfill some

criteria and after that it can enter into agreement with the private equity firm. Under this

source of finance, control of the existing shareholders gets diluted that is the major

implication of this source of finance. Private equity firm holds a majority of stake in the

company. However, companies must use carefully this source of finance.

1.3 Appropriate source of finance

In order to select an appropriate source of finance, it is necessary to understand the

company’s current position. Apart from this, managers also need to evaluate advantages and

disadvantages of each and every source of finance. Manager can select an appropriate source of

finance only when he analyzes company’s condition in a proper manner and identify positive and

negative points of all source of finance (Ge and McVay, 2005). On the basis of evaluating all the

sources of finance, equity and debt are selected for the firm. If, Tesco invests its entire project by

using single source of finance then it will have to face lot of problems. If, debt alone is take to

finance the project then there will be heavy finance cost which may elevate in case loan is taken

at the floating interest rate. On other hand, if shares are used to finance company’s operations

then control of the existing shareholders will get diluted. Hence, it will be better to use both the

sources of finance for financing project. Tesco cannot use private equity in order to finance its

project. This is because if, this will be done then private equity firm will purchase majority of

shares of the company and this in turn will affect day to day company’s operations (Cooper,

Seiford and Tone, 2007). Using only retained earnings is not sufficient to finance the firm’s

operations. It can be used to meet working capital needs of the company. Due to this reason, debt

and equity are considered as the appropriate sources of finance for the firm.

TASK 2

2.1 Cost of different sources of finance

Cost of different sources of finance is as follows. Equity- Dividend paid on issued shares and share issue expenses are the cost of the

equity as a source of finance. Determination of dividend rate depends on the top

management of company. Hence, it can be said that cost of this source of finance is

adjustable in nature. Debt- Interest paid on debt taken by firm is the cost of this source of finance. Interest is

charged at a certain percentage. This percentage may be fixed or floating in nature (Hill,

Leitch and Harrison, 2006). It depends on the firm that which option which it select while

taking a loan from the bank. Cost of this source of finance is adjustable in nature only in

company. However, companies must use carefully this source of finance.

1.3 Appropriate source of finance

In order to select an appropriate source of finance, it is necessary to understand the

company’s current position. Apart from this, managers also need to evaluate advantages and

disadvantages of each and every source of finance. Manager can select an appropriate source of

finance only when he analyzes company’s condition in a proper manner and identify positive and

negative points of all source of finance (Ge and McVay, 2005). On the basis of evaluating all the

sources of finance, equity and debt are selected for the firm. If, Tesco invests its entire project by

using single source of finance then it will have to face lot of problems. If, debt alone is take to

finance the project then there will be heavy finance cost which may elevate in case loan is taken

at the floating interest rate. On other hand, if shares are used to finance company’s operations

then control of the existing shareholders will get diluted. Hence, it will be better to use both the

sources of finance for financing project. Tesco cannot use private equity in order to finance its

project. This is because if, this will be done then private equity firm will purchase majority of

shares of the company and this in turn will affect day to day company’s operations (Cooper,

Seiford and Tone, 2007). Using only retained earnings is not sufficient to finance the firm’s

operations. It can be used to meet working capital needs of the company. Due to this reason, debt

and equity are considered as the appropriate sources of finance for the firm.

TASK 2

2.1 Cost of different sources of finance

Cost of different sources of finance is as follows. Equity- Dividend paid on issued shares and share issue expenses are the cost of the

equity as a source of finance. Determination of dividend rate depends on the top

management of company. Hence, it can be said that cost of this source of finance is

adjustable in nature. Debt- Interest paid on debt taken by firm is the cost of this source of finance. Interest is

charged at a certain percentage. This percentage may be fixed or floating in nature (Hill,

Leitch and Harrison, 2006). It depends on the firm that which option which it select while

taking a loan from the bank. Cost of this source of finance is adjustable in nature only in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

case of floating interest rate. But, sometimes in case of floating interest rate, finance cost

may also increase. Hence, Tesco managers must consider lot of factors while taking loan

at the specific interest rate.

Retained earnings- There is no cost of this source of finance because retained earnings is

a part of revenue that is earned by the firm (Love, Preve and Sarria-Allende, 2007).

Hence, Tesco must try to make possible use of retained earnings for the benefit of firm.

2.2 Importance of financial planning for Tesco

Money is a scarce resource and it is responsibility of the firm managers to make sure that

this resource is used in efficient and effective manner. In financial planning a plan is prepared

which will be followed in order to allocate entire available amount among several activities of

the firm. In order to prepare a good financial plan Tesco needs to identify the activities for which

it needs finance. These activities may be investment in derivatives, financing project and

company operations. Firm will look at the importance of these factors and accordingly will

allocate entire budget amount these activities. Under financial planning Tesco will also prepare a

plan about the way in which it will make an investment in the derivative instruments like

forward, future and options (Lewellen, 2004). This helps firm in making sure that allocated

amount will be invested wisely among all derivative contracts. Hence, it can be said that

financial planning play a very active role in making best use of funds and Tesco must do

financial planning in proper manner.

2.3 Information needs of different decision makers

Following are the different decision makers that needs company information. Managers- These are those who manage an organization by working at the top and

middle level of the management. These take day to day business decisions of the Tesco

and put efforts in order to enhance sale of the company product. Managers needs

company financial statements like income statement and balance sheet in order to identify

firm current business position (Nicholson and Aman, 2012). On the basis of analysis of

these statements managers identify a direction in which they need to work out. Thus, it

can be said that company financial statements are the major information need of the

managers. Creditors- These are those who lend money to the Tesco. They needs company financial

statements in order to identify company current financial position. By doing ratio analysis

may also increase. Hence, Tesco managers must consider lot of factors while taking loan

at the specific interest rate.

Retained earnings- There is no cost of this source of finance because retained earnings is

a part of revenue that is earned by the firm (Love, Preve and Sarria-Allende, 2007).

Hence, Tesco must try to make possible use of retained earnings for the benefit of firm.

2.2 Importance of financial planning for Tesco

Money is a scarce resource and it is responsibility of the firm managers to make sure that

this resource is used in efficient and effective manner. In financial planning a plan is prepared

which will be followed in order to allocate entire available amount among several activities of

the firm. In order to prepare a good financial plan Tesco needs to identify the activities for which

it needs finance. These activities may be investment in derivatives, financing project and

company operations. Firm will look at the importance of these factors and accordingly will

allocate entire budget amount these activities. Under financial planning Tesco will also prepare a

plan about the way in which it will make an investment in the derivative instruments like

forward, future and options (Lewellen, 2004). This helps firm in making sure that allocated

amount will be invested wisely among all derivative contracts. Hence, it can be said that

financial planning play a very active role in making best use of funds and Tesco must do

financial planning in proper manner.

2.3 Information needs of different decision makers

Following are the different decision makers that needs company information. Managers- These are those who manage an organization by working at the top and

middle level of the management. These take day to day business decisions of the Tesco

and put efforts in order to enhance sale of the company product. Managers needs

company financial statements like income statement and balance sheet in order to identify

firm current business position (Nicholson and Aman, 2012). On the basis of analysis of

these statements managers identify a direction in which they need to work out. Thus, it

can be said that company financial statements are the major information need of the

managers. Creditors- These are those who lend money to the Tesco. They needs company financial

statements in order to identify company current financial position. By doing ratio analysis

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

creditors identify the position where company currently stands (Ogayar and Vidal, 2009).

By using relevant ratios creditors identify the extent to which Tesco can pay its loan

amount on time.

Government- Tesco pay a tax to the government and latter entity is always interested in

the firm financial statements in order to make sure that it pay accurate amount of tax to

the itself. Hence, government as a stakeholder also needs company financial statements.

2.4 Impact of finance on the financial statements

Finance to large extent affects firm financial statements. Even company raise finance by

using debt or equity in both case changes will be observed in the financial statements of the firm.

If Tesco takes a debt of 50,000 then its long term liability will increase. This means that its

liability side will increase in the balance sheet. On taking a loan firm is getting cash and due to

this reason cash section in current assets of the asset side of the balance sheet will increase. It can

be said that if firm take a loan then both assets and liability side of the balance sheet will

increase. On other hand, suppose firm issue share of 1, 00,000 then shareholder equity in the

liability side of the balance sheet will increase (Obst, Graham and Christie, 2007). This amount

will be added in the called up capital part of the shareholder equity. On issue of shares firm is

receiving cash in large amount. Due to this reason, bank amount in the asset side of the balance

sheet will get increased. Hence, it can be said that finance affects financial statements of the

firm.

TASK 3

3.1 Analysis of budget and making appropriate decisions

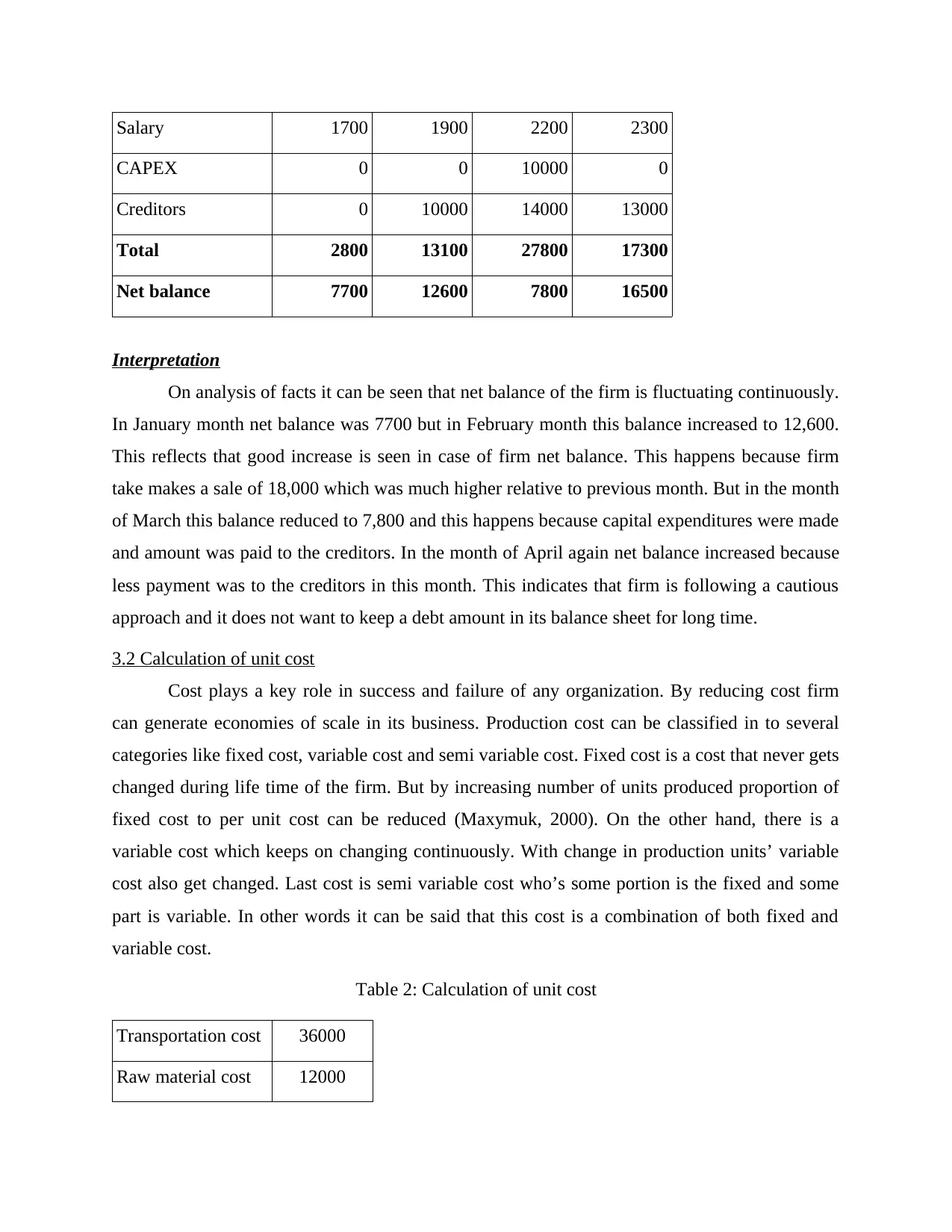

Table 1: Cash budget for Tesco

January February March April

Opening balance 7700 12600 7800

Sales 10500 18000 23000 26000

Total 10500 25700 35600 33800

Expense

Purchase 1100 1200 1600 2000

By using relevant ratios creditors identify the extent to which Tesco can pay its loan

amount on time.

Government- Tesco pay a tax to the government and latter entity is always interested in

the firm financial statements in order to make sure that it pay accurate amount of tax to

the itself. Hence, government as a stakeholder also needs company financial statements.

2.4 Impact of finance on the financial statements

Finance to large extent affects firm financial statements. Even company raise finance by

using debt or equity in both case changes will be observed in the financial statements of the firm.

If Tesco takes a debt of 50,000 then its long term liability will increase. This means that its

liability side will increase in the balance sheet. On taking a loan firm is getting cash and due to

this reason cash section in current assets of the asset side of the balance sheet will increase. It can

be said that if firm take a loan then both assets and liability side of the balance sheet will

increase. On other hand, suppose firm issue share of 1, 00,000 then shareholder equity in the

liability side of the balance sheet will increase (Obst, Graham and Christie, 2007). This amount

will be added in the called up capital part of the shareholder equity. On issue of shares firm is

receiving cash in large amount. Due to this reason, bank amount in the asset side of the balance

sheet will get increased. Hence, it can be said that finance affects financial statements of the

firm.

TASK 3

3.1 Analysis of budget and making appropriate decisions

Table 1: Cash budget for Tesco

January February March April

Opening balance 7700 12600 7800

Sales 10500 18000 23000 26000

Total 10500 25700 35600 33800

Expense

Purchase 1100 1200 1600 2000

Salary 1700 1900 2200 2300

CAPEX 0 0 10000 0

Creditors 0 10000 14000 13000

Total 2800 13100 27800 17300

Net balance 7700 12600 7800 16500

Interpretation

On analysis of facts it can be seen that net balance of the firm is fluctuating continuously.

In January month net balance was 7700 but in February month this balance increased to 12,600.

This reflects that good increase is seen in case of firm net balance. This happens because firm

take makes a sale of 18,000 which was much higher relative to previous month. But in the month

of March this balance reduced to 7,800 and this happens because capital expenditures were made

and amount was paid to the creditors. In the month of April again net balance increased because

less payment was to the creditors in this month. This indicates that firm is following a cautious

approach and it does not want to keep a debt amount in its balance sheet for long time.

3.2 Calculation of unit cost

Cost plays a key role in success and failure of any organization. By reducing cost firm

can generate economies of scale in its business. Production cost can be classified in to several

categories like fixed cost, variable cost and semi variable cost. Fixed cost is a cost that never gets

changed during life time of the firm. But by increasing number of units produced proportion of

fixed cost to per unit cost can be reduced (Maxymuk, 2000). On the other hand, there is a

variable cost which keeps on changing continuously. With change in production units’ variable

cost also get changed. Last cost is semi variable cost who’s some portion is the fixed and some

part is variable. In other words it can be said that this cost is a combination of both fixed and

variable cost.

Table 2: Calculation of unit cost

Transportation cost 36000

Raw material cost 12000

CAPEX 0 0 10000 0

Creditors 0 10000 14000 13000

Total 2800 13100 27800 17300

Net balance 7700 12600 7800 16500

Interpretation

On analysis of facts it can be seen that net balance of the firm is fluctuating continuously.

In January month net balance was 7700 but in February month this balance increased to 12,600.

This reflects that good increase is seen in case of firm net balance. This happens because firm

take makes a sale of 18,000 which was much higher relative to previous month. But in the month

of March this balance reduced to 7,800 and this happens because capital expenditures were made

and amount was paid to the creditors. In the month of April again net balance increased because

less payment was to the creditors in this month. This indicates that firm is following a cautious

approach and it does not want to keep a debt amount in its balance sheet for long time.

3.2 Calculation of unit cost

Cost plays a key role in success and failure of any organization. By reducing cost firm

can generate economies of scale in its business. Production cost can be classified in to several

categories like fixed cost, variable cost and semi variable cost. Fixed cost is a cost that never gets

changed during life time of the firm. But by increasing number of units produced proportion of

fixed cost to per unit cost can be reduced (Maxymuk, 2000). On the other hand, there is a

variable cost which keeps on changing continuously. With change in production units’ variable

cost also get changed. Last cost is semi variable cost who’s some portion is the fixed and some

part is variable. In other words it can be said that this cost is a combination of both fixed and

variable cost.

Table 2: Calculation of unit cost

Transportation cost 36000

Raw material cost 12000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

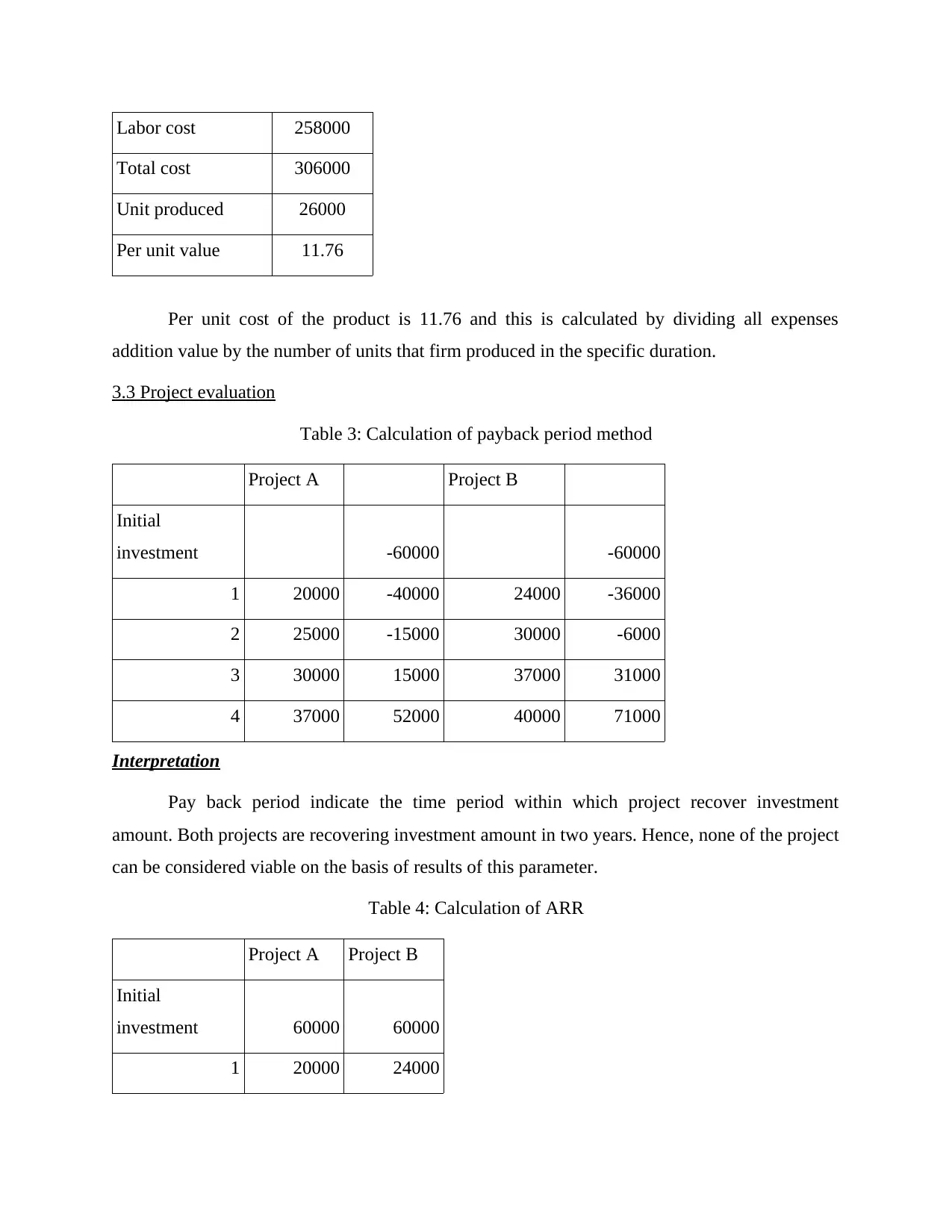

Labor cost 258000

Total cost 306000

Unit produced 26000

Per unit value 11.76

Per unit cost of the product is 11.76 and this is calculated by dividing all expenses

addition value by the number of units that firm produced in the specific duration.

3.3 Project evaluation

Table 3: Calculation of payback period method

Project A Project B

Initial

investment -60000 -60000

1 20000 -40000 24000 -36000

2 25000 -15000 30000 -6000

3 30000 15000 37000 31000

4 37000 52000 40000 71000

Interpretation

Pay back period indicate the time period within which project recover investment

amount. Both projects are recovering investment amount in two years. Hence, none of the project

can be considered viable on the basis of results of this parameter.

Table 4: Calculation of ARR

Project A Project B

Initial

investment 60000 60000

1 20000 24000

Total cost 306000

Unit produced 26000

Per unit value 11.76

Per unit cost of the product is 11.76 and this is calculated by dividing all expenses

addition value by the number of units that firm produced in the specific duration.

3.3 Project evaluation

Table 3: Calculation of payback period method

Project A Project B

Initial

investment -60000 -60000

1 20000 -40000 24000 -36000

2 25000 -15000 30000 -6000

3 30000 15000 37000 31000

4 37000 52000 40000 71000

Interpretation

Pay back period indicate the time period within which project recover investment

amount. Both projects are recovering investment amount in two years. Hence, none of the project

can be considered viable on the basis of results of this parameter.

Table 4: Calculation of ARR

Project A Project B

Initial

investment 60000 60000

1 20000 24000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

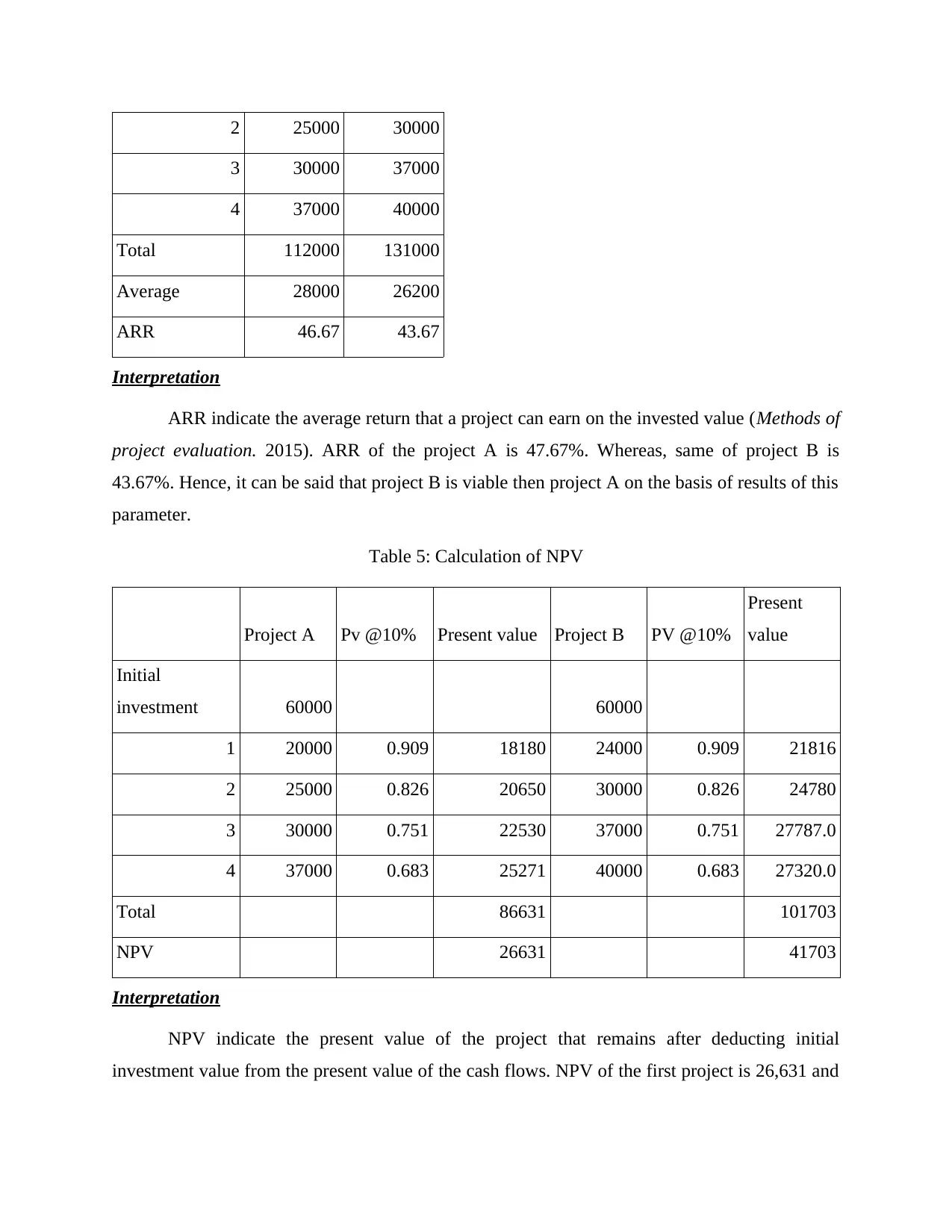

2 25000 30000

3 30000 37000

4 37000 40000

Total 112000 131000

Average 28000 26200

ARR 46.67 43.67

Interpretation

ARR indicate the average return that a project can earn on the invested value (Methods of

project evaluation. 2015). ARR of the project A is 47.67%. Whereas, same of project B is

43.67%. Hence, it can be said that project B is viable then project A on the basis of results of this

parameter.

Table 5: Calculation of NPV

Project A Pv @10% Present value Project B PV @10%

Present

value

Initial

investment 60000 60000

1 20000 0.909 18180 24000 0.909 21816

2 25000 0.826 20650 30000 0.826 24780

3 30000 0.751 22530 37000 0.751 27787.0

4 37000 0.683 25271 40000 0.683 27320.0

Total 86631 101703

NPV 26631 41703

Interpretation

NPV indicate the present value of the project that remains after deducting initial

investment value from the present value of the cash flows. NPV of the first project is 26,631 and

3 30000 37000

4 37000 40000

Total 112000 131000

Average 28000 26200

ARR 46.67 43.67

Interpretation

ARR indicate the average return that a project can earn on the invested value (Methods of

project evaluation. 2015). ARR of the project A is 47.67%. Whereas, same of project B is

43.67%. Hence, it can be said that project B is viable then project A on the basis of results of this

parameter.

Table 5: Calculation of NPV

Project A Pv @10% Present value Project B PV @10%

Present

value

Initial

investment 60000 60000

1 20000 0.909 18180 24000 0.909 21816

2 25000 0.826 20650 30000 0.826 24780

3 30000 0.751 22530 37000 0.751 27787.0

4 37000 0.683 25271 40000 0.683 27320.0

Total 86631 101703

NPV 26631 41703

Interpretation

NPV indicate the present value of the project that remains after deducting initial

investment value from the present value of the cash flows. NPV of the first project is 26,631 and

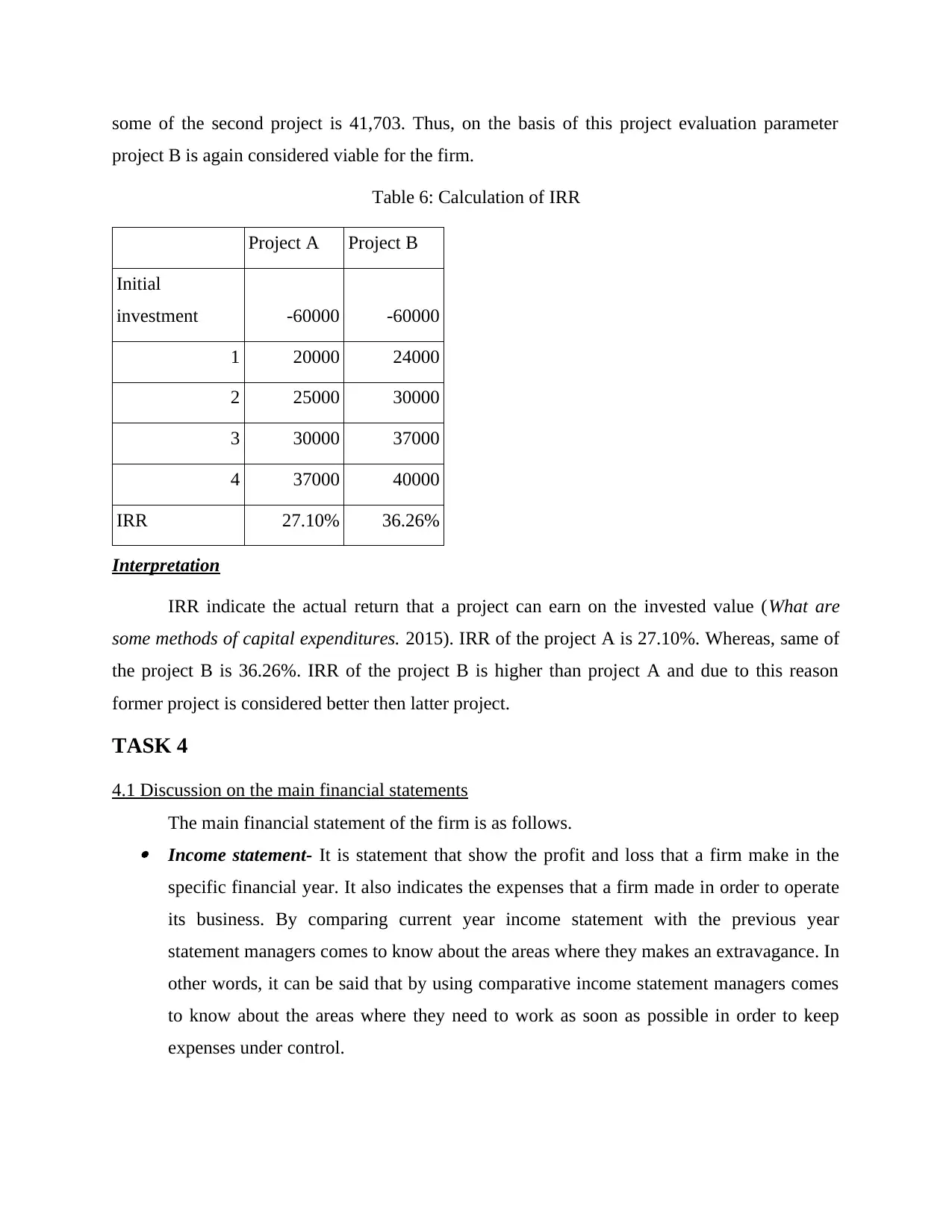

some of the second project is 41,703. Thus, on the basis of this project evaluation parameter

project B is again considered viable for the firm.

Table 6: Calculation of IRR

Project A Project B

Initial

investment -60000 -60000

1 20000 24000

2 25000 30000

3 30000 37000

4 37000 40000

IRR 27.10% 36.26%

Interpretation

IRR indicate the actual return that a project can earn on the invested value (What are

some methods of capital expenditures. 2015). IRR of the project A is 27.10%. Whereas, same of

the project B is 36.26%. IRR of the project B is higher than project A and due to this reason

former project is considered better then latter project.

TASK 4

4.1 Discussion on the main financial statements

The main financial statement of the firm is as follows. Income statement- It is statement that show the profit and loss that a firm make in the

specific financial year. It also indicates the expenses that a firm made in order to operate

its business. By comparing current year income statement with the previous year

statement managers comes to know about the areas where they makes an extravagance. In

other words, it can be said that by using comparative income statement managers comes

to know about the areas where they need to work as soon as possible in order to keep

expenses under control.

project B is again considered viable for the firm.

Table 6: Calculation of IRR

Project A Project B

Initial

investment -60000 -60000

1 20000 24000

2 25000 30000

3 30000 37000

4 37000 40000

IRR 27.10% 36.26%

Interpretation

IRR indicate the actual return that a project can earn on the invested value (What are

some methods of capital expenditures. 2015). IRR of the project A is 27.10%. Whereas, same of

the project B is 36.26%. IRR of the project B is higher than project A and due to this reason

former project is considered better then latter project.

TASK 4

4.1 Discussion on the main financial statements

The main financial statement of the firm is as follows. Income statement- It is statement that show the profit and loss that a firm make in the

specific financial year. It also indicates the expenses that a firm made in order to operate

its business. By comparing current year income statement with the previous year

statement managers comes to know about the areas where they makes an extravagance. In

other words, it can be said that by using comparative income statement managers comes

to know about the areas where they need to work as soon as possible in order to keep

expenses under control.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.