Financial Resource Management: Analysis, Planning, and Decision Making

VerifiedAdded on 2020/06/05

|13

|2964

|49

Report

AI Summary

This report comprehensively examines financial resource management within a business context, focusing on a case study involving a restaurant chain's expansion. The report begins by identifying various sources of finance, including internal and external options like personal savings, government grants, bank loans, and leasing, along with their respective implications. It then delves into the importance of financial planning, budgeting, and investment appraisal tools, such as payback period and NPV, for making informed decisions. The analysis extends to cost analysis, including financial and opportunity costs. Furthermore, the report explores the information needs of different stakeholders and the impact of financial sources on financial statements. The second task involves analyzing Sainsbury's financial statements, including the income statement, balance sheet, and cash flow statement, and interpreting them through ratio analysis to assess the company's financial health. The report concludes with recommendations for effective financial resource management and decision-making.

Managing Financial Resources

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION......................................................................................................................1

TASK 1......................................................................................................................................1

1.1 Identifying sources of finance available to business........................................................1

1.2 Presenting the implication of financial sources identified...............................................2

1.3 Evaluating appropriate sources of finance that is suitable for business project...............3

2.1 Analyzing cost of different financial sources...................................................................3

2.2 Explaining the importance of financial planning.............................................................4

2.3 Assessing the information need of different decision makers.........................................4

2.4 Impact of sources on financial statement of the firm.......................................................4

3.1 Analyzing budgets for making appropriate decisions......................................................5

3.2 Calculation of unit cost for making pricing decisions.....................................................6

3.3 Evaluating the viability of projects using investment appraisal tools..............................6

TASK 2......................................................................................................................................8

4.1 Discussing the main financial statements that are prepared by Sainsbury.......................8

4.2 Comparing the financial statement formats of different business units...........................8

4.3 Interpreting financial statements of Sainsbury through ratio analysis.............................9

CONCUSION..........................................................................................................................10

REFERENCES.........................................................................................................................11

INTRODUCTION......................................................................................................................1

TASK 1......................................................................................................................................1

1.1 Identifying sources of finance available to business........................................................1

1.2 Presenting the implication of financial sources identified...............................................2

1.3 Evaluating appropriate sources of finance that is suitable for business project...............3

2.1 Analyzing cost of different financial sources...................................................................3

2.2 Explaining the importance of financial planning.............................................................4

2.3 Assessing the information need of different decision makers.........................................4

2.4 Impact of sources on financial statement of the firm.......................................................4

3.1 Analyzing budgets for making appropriate decisions......................................................5

3.2 Calculation of unit cost for making pricing decisions.....................................................6

3.3 Evaluating the viability of projects using investment appraisal tools..............................6

TASK 2......................................................................................................................................8

4.1 Discussing the main financial statements that are prepared by Sainsbury.......................8

4.2 Comparing the financial statement formats of different business units...........................8

4.3 Interpreting financial statements of Sainsbury through ratio analysis.............................9

CONCUSION..........................................................................................................................10

REFERENCES.........................................................................................................................11

INTRODUCTION

In the business unit, effective allocation, management and utilization of financial

resources are highly required to meet the organizational goals or objectives. In this,

considering the supported which is provided by the government authority business of Food

for Friends is planning to open another restaurant in London for the purpose of expansion. In

this, report will entail the sources that can be considered by business entity for fulfilling

monetary requirements. Along with this, it will provide deeper insight about the manner in

which concepts such as financial planning, budgeting, investment and ratio analysis aid in

effective decision making.

TASK 1

1.1 Identifying sources of finance available to business

For opening another restaurant in London business entity requires £160000, whereas

now entrepreneur has only £20000 for the purpose of investment. In this regard, by using the

following sources entrepreneur can meet financial needs such as:

Internal sources

Personal savings In the recent times, with the motive to fulfil future need and meeting

contingent situation business entity lays emphasis on saving money.

Thus, by using personal savings business entity can generate fund for

implementing business plan.

Sale of unused

assets

Company can also meet financial needs by selling fixed assets that are

not used recently in productive activities.

External sources

Government grant Now, government is offering financial assistance to the firms at

concessional rates. Hence, by presenting lucrative business plan to

government authority entrepreneur of F&F can raise funds.

Bank loan Business entity can meet monetary requirements by applying to the

banking institution for loan. Moreover, banks are usually ready to give

loan to the company on the basis of collateral security (Peirson and

et.al., 2014).

Leasing For making investment in fixed assets such as land & building, plant

In the business unit, effective allocation, management and utilization of financial

resources are highly required to meet the organizational goals or objectives. In this,

considering the supported which is provided by the government authority business of Food

for Friends is planning to open another restaurant in London for the purpose of expansion. In

this, report will entail the sources that can be considered by business entity for fulfilling

monetary requirements. Along with this, it will provide deeper insight about the manner in

which concepts such as financial planning, budgeting, investment and ratio analysis aid in

effective decision making.

TASK 1

1.1 Identifying sources of finance available to business

For opening another restaurant in London business entity requires £160000, whereas

now entrepreneur has only £20000 for the purpose of investment. In this regard, by using the

following sources entrepreneur can meet financial needs such as:

Internal sources

Personal savings In the recent times, with the motive to fulfil future need and meeting

contingent situation business entity lays emphasis on saving money.

Thus, by using personal savings business entity can generate fund for

implementing business plan.

Sale of unused

assets

Company can also meet financial needs by selling fixed assets that are

not used recently in productive activities.

External sources

Government grant Now, government is offering financial assistance to the firms at

concessional rates. Hence, by presenting lucrative business plan to

government authority entrepreneur of F&F can raise funds.

Bank loan Business entity can meet monetary requirements by applying to the

banking institution for loan. Moreover, banks are usually ready to give

loan to the company on the basis of collateral security (Peirson and

et.al., 2014).

Leasing For making investment in fixed assets such as land & building, plant

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and machinery etc business entity requires high funds. In this regard,

by taking assets on lease restaurant owner can meet monetary needs.

1.2 Presenting the implication of financial sources identified

At the time of taking decision or making section of sources, owner of F&F should

keep in mind following implications:

Sources of

finance

Legal

implications

Financial Dilution of

control

Bankruptcy

Personal savings No Opportunity cost

in terms of loss of

interest on capital

No Least priority

Sales of assets On the basis of

legal aspect, in

this, ownership

rights are shifted

to others.

Charges of

advertisement and

other

documentary

aspects

No -

Government grant Need or obliged

to use money in

the activities for

which it is

granted.

Interest on loan Limited At the time of

bankruptcy,

concerned

authority enjoys

priority in getting

back amount

Leasing In leasing,

business entity is

obliged to return

back asset after

the specific time

frame (Kemp and

et.al., 2015).

Periodical rent

pertaining to the

asset taken on

lease

Limited to the

assets provided

Same as above

Bank loan In the case of

default, banking

unit has legal

right to take

action in against

Interest charges Limited to the

financial

assistance offered

Likewise in

government grant

and leasing

by taking assets on lease restaurant owner can meet monetary needs.

1.2 Presenting the implication of financial sources identified

At the time of taking decision or making section of sources, owner of F&F should

keep in mind following implications:

Sources of

finance

Legal

implications

Financial Dilution of

control

Bankruptcy

Personal savings No Opportunity cost

in terms of loss of

interest on capital

No Least priority

Sales of assets On the basis of

legal aspect, in

this, ownership

rights are shifted

to others.

Charges of

advertisement and

other

documentary

aspects

No -

Government grant Need or obliged

to use money in

the activities for

which it is

granted.

Interest on loan Limited At the time of

bankruptcy,

concerned

authority enjoys

priority in getting

back amount

Leasing In leasing,

business entity is

obliged to return

back asset after

the specific time

frame (Kemp and

et.al., 2015).

Periodical rent

pertaining to the

asset taken on

lease

Limited to the

assets provided

Same as above

Bank loan In the case of

default, banking

unit has legal

right to take

action in against

Interest charges Limited to the

financial

assistance offered

Likewise in

government grant

and leasing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

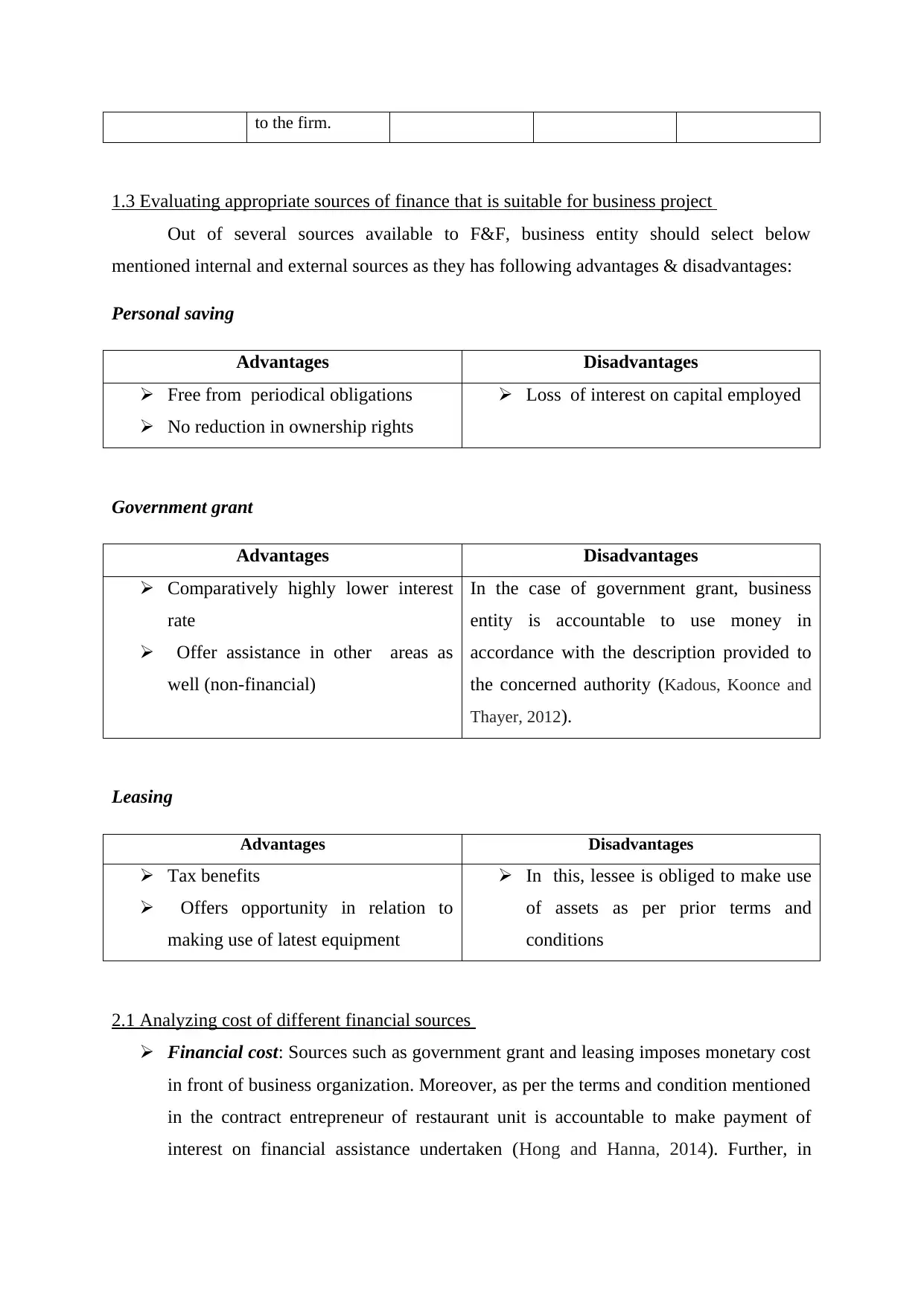

to the firm.

1.3 Evaluating appropriate sources of finance that is suitable for business project

Out of several sources available to F&F, business entity should select below

mentioned internal and external sources as they has following advantages & disadvantages:

Personal saving

Advantages Disadvantages

Free from periodical obligations

No reduction in ownership rights

Loss of interest on capital employed

Government grant

Advantages Disadvantages

Comparatively highly lower interest

rate

Offer assistance in other areas as

well (non-financial)

In the case of government grant, business

entity is accountable to use money in

accordance with the description provided to

the concerned authority (Kadous, Koonce and

Thayer, 2012).

Leasing

Advantages Disadvantages

Tax benefits

Offers opportunity in relation to

making use of latest equipment

In this, lessee is obliged to make use

of assets as per prior terms and

conditions

2.1 Analyzing cost of different financial sources

Financial cost: Sources such as government grant and leasing imposes monetary cost

in front of business organization. Moreover, as per the terms and condition mentioned

in the contract entrepreneur of restaurant unit is accountable to make payment of

interest on financial assistance undertaken (Hong and Hanna, 2014). Further, in

1.3 Evaluating appropriate sources of finance that is suitable for business project

Out of several sources available to F&F, business entity should select below

mentioned internal and external sources as they has following advantages & disadvantages:

Personal saving

Advantages Disadvantages

Free from periodical obligations

No reduction in ownership rights

Loss of interest on capital employed

Government grant

Advantages Disadvantages

Comparatively highly lower interest

rate

Offer assistance in other areas as

well (non-financial)

In the case of government grant, business

entity is accountable to use money in

accordance with the description provided to

the concerned authority (Kadous, Koonce and

Thayer, 2012).

Leasing

Advantages Disadvantages

Tax benefits

Offers opportunity in relation to

making use of latest equipment

In this, lessee is obliged to make use

of assets as per prior terms and

conditions

2.1 Analyzing cost of different financial sources

Financial cost: Sources such as government grant and leasing imposes monetary cost

in front of business organization. Moreover, as per the terms and condition mentioned

in the contract entrepreneur of restaurant unit is accountable to make payment of

interest on financial assistance undertaken (Hong and Hanna, 2014). Further, in

leasing, in return of making use of assets sole trader obliged to pay rent. Hence, both

interest and rent are considered as financial cost for F&F.

Opportunity cost: Personal saving source of finance has opportunity cost to the firm.

Moreover, if business unit uses personal savings then it is not in position to capitalize

future opportunities or contingent situations. In this way, such internal source of

finance imposes opportunity cost in front of the firm.

2.2 Explaining the importance of financial planning

Financial planning is the process that is associated with the procurement, investment

and administration of funds. In the context of F&F, financial planning is highly significant

which in turn helps in ensuing stability by making proper balance in inflows and outflows.

Besides this, competent financial plan assists in reducing uncertainties pertaining to current

trends (Hong and Hanna, 2014). Moreover, it enables business entity to keep some fund for

the contingent situation and thereby ensure smooth functioning of operations.

2.3 Assessing the information need of different decision makers

Information need of all the internal and external stakeholders vary to the significant

level in the following way:

Internal stakeholders

Management: In the context of F&F, manager undertakes all the financial statements

with the motive to assess monetary position and performance. Monetary information

assists manager in developing strategic framework for the upcoming time period

(Rehan and et.al., 2015).

Personnel or employees: They make assessment of profitability statements with the

objective to evaluate their growth in monetary terms such as bonus, incentives etc.

External stakeholders

Investors: For making estimation about return in the form of dividend investors or

shareholders make evaluation of profitability statement.

Financial institution: To assess the capability of firm in relation to meeting monetary

obligations financial institution does evaluation of balance sheet (Users of financial

statements, 2016).

interest and rent are considered as financial cost for F&F.

Opportunity cost: Personal saving source of finance has opportunity cost to the firm.

Moreover, if business unit uses personal savings then it is not in position to capitalize

future opportunities or contingent situations. In this way, such internal source of

finance imposes opportunity cost in front of the firm.

2.2 Explaining the importance of financial planning

Financial planning is the process that is associated with the procurement, investment

and administration of funds. In the context of F&F, financial planning is highly significant

which in turn helps in ensuing stability by making proper balance in inflows and outflows.

Besides this, competent financial plan assists in reducing uncertainties pertaining to current

trends (Hong and Hanna, 2014). Moreover, it enables business entity to keep some fund for

the contingent situation and thereby ensure smooth functioning of operations.

2.3 Assessing the information need of different decision makers

Information need of all the internal and external stakeholders vary to the significant

level in the following way:

Internal stakeholders

Management: In the context of F&F, manager undertakes all the financial statements

with the motive to assess monetary position and performance. Monetary information

assists manager in developing strategic framework for the upcoming time period

(Rehan and et.al., 2015).

Personnel or employees: They make assessment of profitability statements with the

objective to evaluate their growth in monetary terms such as bonus, incentives etc.

External stakeholders

Investors: For making estimation about return in the form of dividend investors or

shareholders make evaluation of profitability statement.

Financial institution: To assess the capability of firm in relation to meeting monetary

obligations financial institution does evaluation of balance sheet (Users of financial

statements, 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

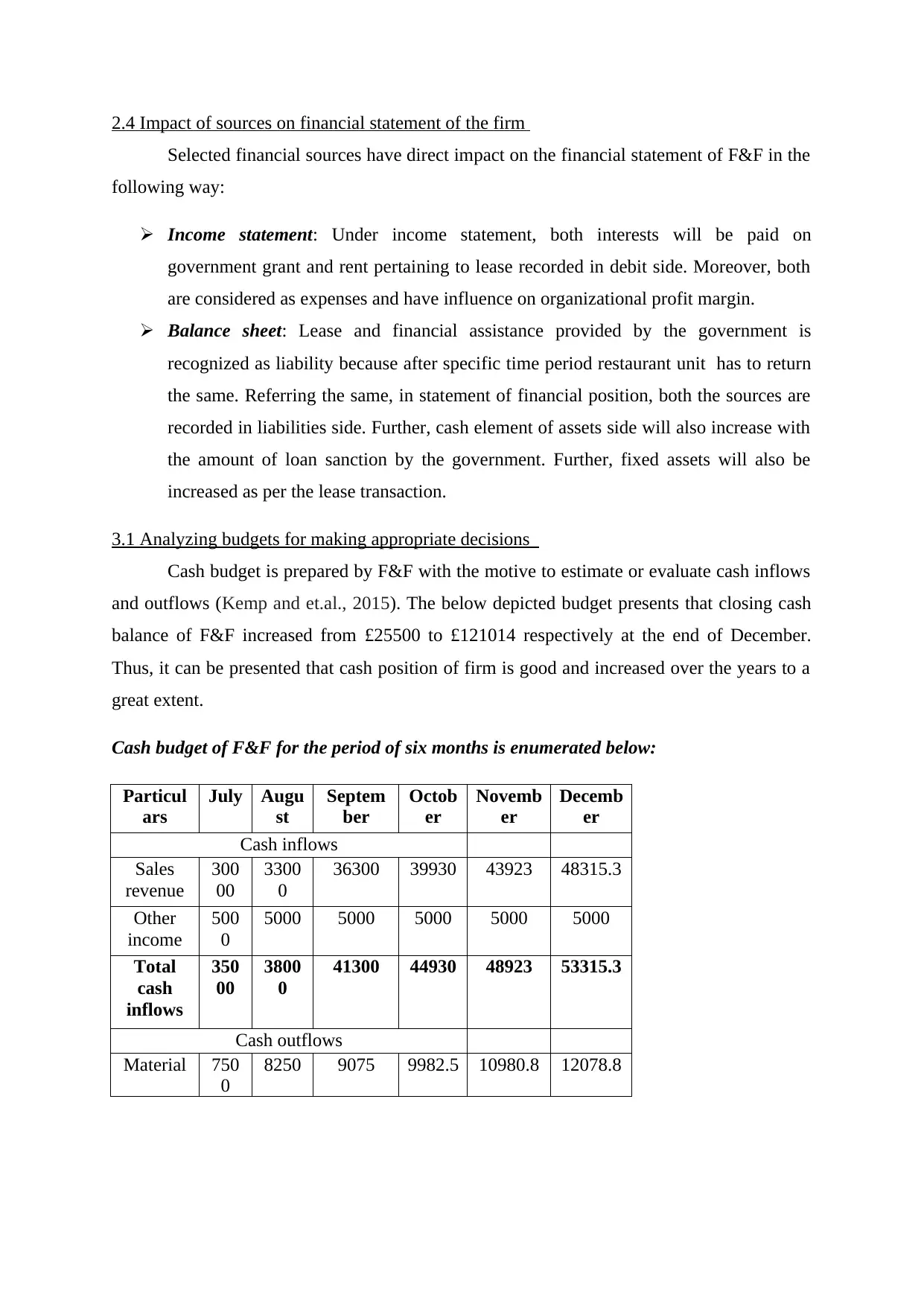

2.4 Impact of sources on financial statement of the firm

Selected financial sources have direct impact on the financial statement of F&F in the

following way:

Income statement: Under income statement, both interests will be paid on

government grant and rent pertaining to lease recorded in debit side. Moreover, both

are considered as expenses and have influence on organizational profit margin.

Balance sheet: Lease and financial assistance provided by the government is

recognized as liability because after specific time period restaurant unit has to return

the same. Referring the same, in statement of financial position, both the sources are

recorded in liabilities side. Further, cash element of assets side will also increase with

the amount of loan sanction by the government. Further, fixed assets will also be

increased as per the lease transaction.

3.1 Analyzing budgets for making appropriate decisions

Cash budget is prepared by F&F with the motive to estimate or evaluate cash inflows

and outflows (Kemp and et.al., 2015). The below depicted budget presents that closing cash

balance of F&F increased from £25500 to £121014 respectively at the end of December.

Thus, it can be presented that cash position of firm is good and increased over the years to a

great extent.

Cash budget of F&F for the period of six months is enumerated below:

Particul

ars

July Augu

st

Septem

ber

Octob

er

Novemb

er

Decemb

er

Cash inflows

Sales

revenue

300

00

3300

0

36300 39930 43923 48315.3

Other

income

500

0

5000 5000 5000 5000 5000

Total

cash

inflows

350

00

3800

0

41300 44930 48923 53315.3

Cash outflows

Material 750

0

8250 9075 9982.5 10980.8 12078.8

Selected financial sources have direct impact on the financial statement of F&F in the

following way:

Income statement: Under income statement, both interests will be paid on

government grant and rent pertaining to lease recorded in debit side. Moreover, both

are considered as expenses and have influence on organizational profit margin.

Balance sheet: Lease and financial assistance provided by the government is

recognized as liability because after specific time period restaurant unit has to return

the same. Referring the same, in statement of financial position, both the sources are

recorded in liabilities side. Further, cash element of assets side will also increase with

the amount of loan sanction by the government. Further, fixed assets will also be

increased as per the lease transaction.

3.1 Analyzing budgets for making appropriate decisions

Cash budget is prepared by F&F with the motive to estimate or evaluate cash inflows

and outflows (Kemp and et.al., 2015). The below depicted budget presents that closing cash

balance of F&F increased from £25500 to £121014 respectively at the end of December.

Thus, it can be presented that cash position of firm is good and increased over the years to a

great extent.

Cash budget of F&F for the period of six months is enumerated below:

Particul

ars

July Augu

st

Septem

ber

Octob

er

Novemb

er

Decemb

er

Cash inflows

Sales

revenue

300

00

3300

0

36300 39930 43923 48315.3

Other

income

500

0

5000 5000 5000 5000 5000

Total

cash

inflows

350

00

3800

0

41300 44930 48923 53315.3

Cash outflows

Material 750

0

8250 9075 9982.5 10980.8 12078.8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Labor

and

salaries

of

personne

l

450

0

4950 5445 5989.5 6588.45 7247.3

overhead

s

360

0

3960 4356 4791.6 5270.76 5797.84

Other

expenses

390

0

4290 4719 5190.9 5709.99 6280.99

Total

cash

outflows

195

00

2145

0

23595 25954.

5

28550 31404.9

Net cash

flow/

deficit/

surplus

155

00

1655

0

17705 18975.

5

20373.1 21910.4

Opening

balance

100

00

2550

0

42050 59755 78730.5 99103.6

Closing

cash

balance

255

00

4205

0

59755 78730.

5

99103.6 121014

3.2 Calculation of unit cost for making pricing decisions

Unit cost implies for the expenses incurred by the firm for offering services to each

customer. In this, by adding profit % in the unit cost owner of F&F can determine suitable

price and would become able to get desired margin (Peirson and et.al., 2014).

For example:

Particulars Formula

Figure

s

Fixed cost £5000

Variable expenses £10000

Total cost (TC)

TC: Fixed + variable

cost £15000

Number of people

served £300

Unit cost TC / Number of people £50

Mark-up 20%

Profit per unit (Unit cost * mark up ) £10

Price per unit TC + profit per unit £60

and

salaries

of

personne

l

450

0

4950 5445 5989.5 6588.45 7247.3

overhead

s

360

0

3960 4356 4791.6 5270.76 5797.84

Other

expenses

390

0

4290 4719 5190.9 5709.99 6280.99

Total

cash

outflows

195

00

2145

0

23595 25954.

5

28550 31404.9

Net cash

flow/

deficit/

surplus

155

00

1655

0

17705 18975.

5

20373.1 21910.4

Opening

balance

100

00

2550

0

42050 59755 78730.5 99103.6

Closing

cash

balance

255

00

4205

0

59755 78730.

5

99103.6 121014

3.2 Calculation of unit cost for making pricing decisions

Unit cost implies for the expenses incurred by the firm for offering services to each

customer. In this, by adding profit % in the unit cost owner of F&F can determine suitable

price and would become able to get desired margin (Peirson and et.al., 2014).

For example:

Particulars Formula

Figure

s

Fixed cost £5000

Variable expenses £10000

Total cost (TC)

TC: Fixed + variable

cost £15000

Number of people

served £300

Unit cost TC / Number of people £50

Mark-up 20%

Profit per unit (Unit cost * mark up ) £10

Price per unit TC + profit per unit £60

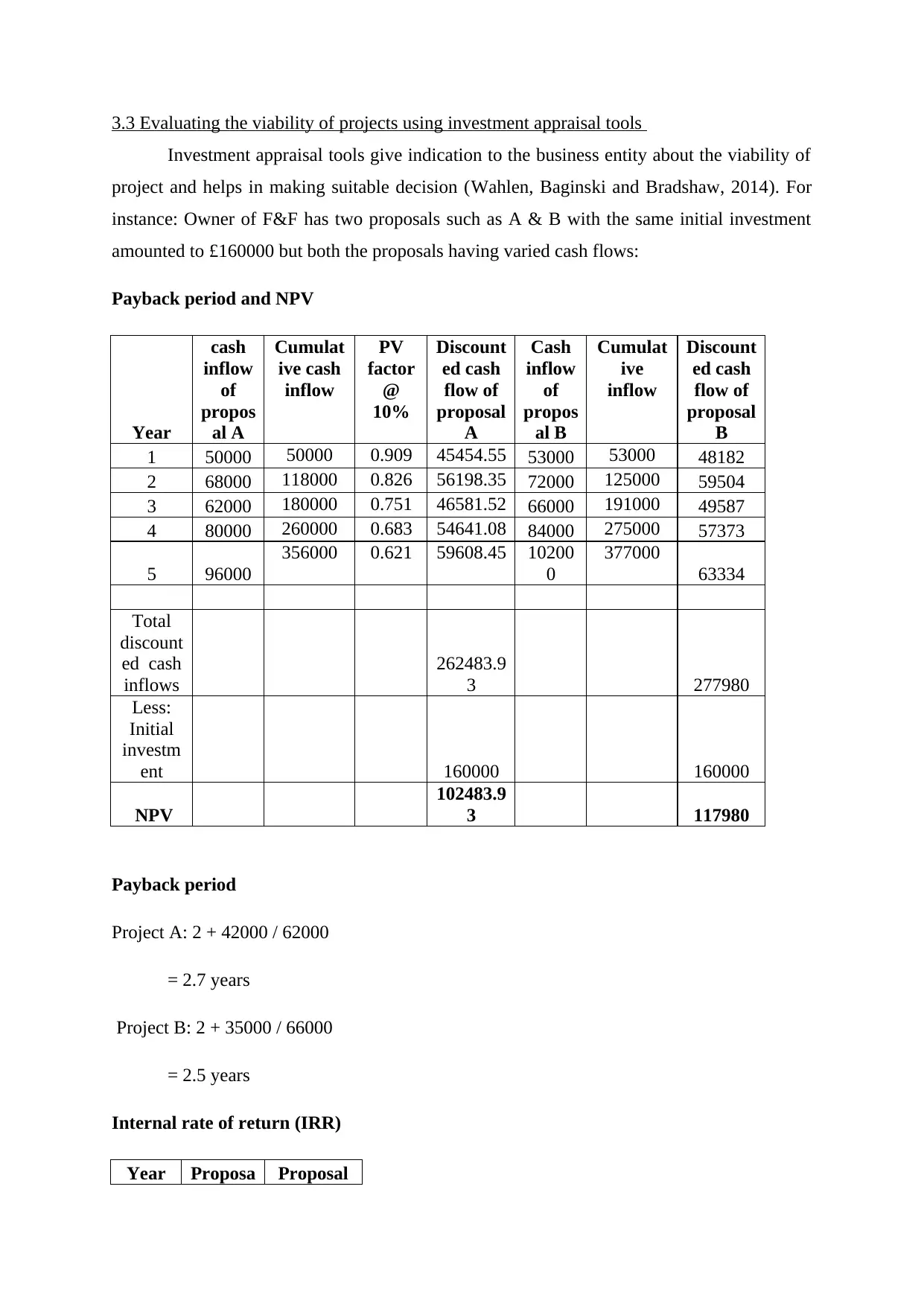

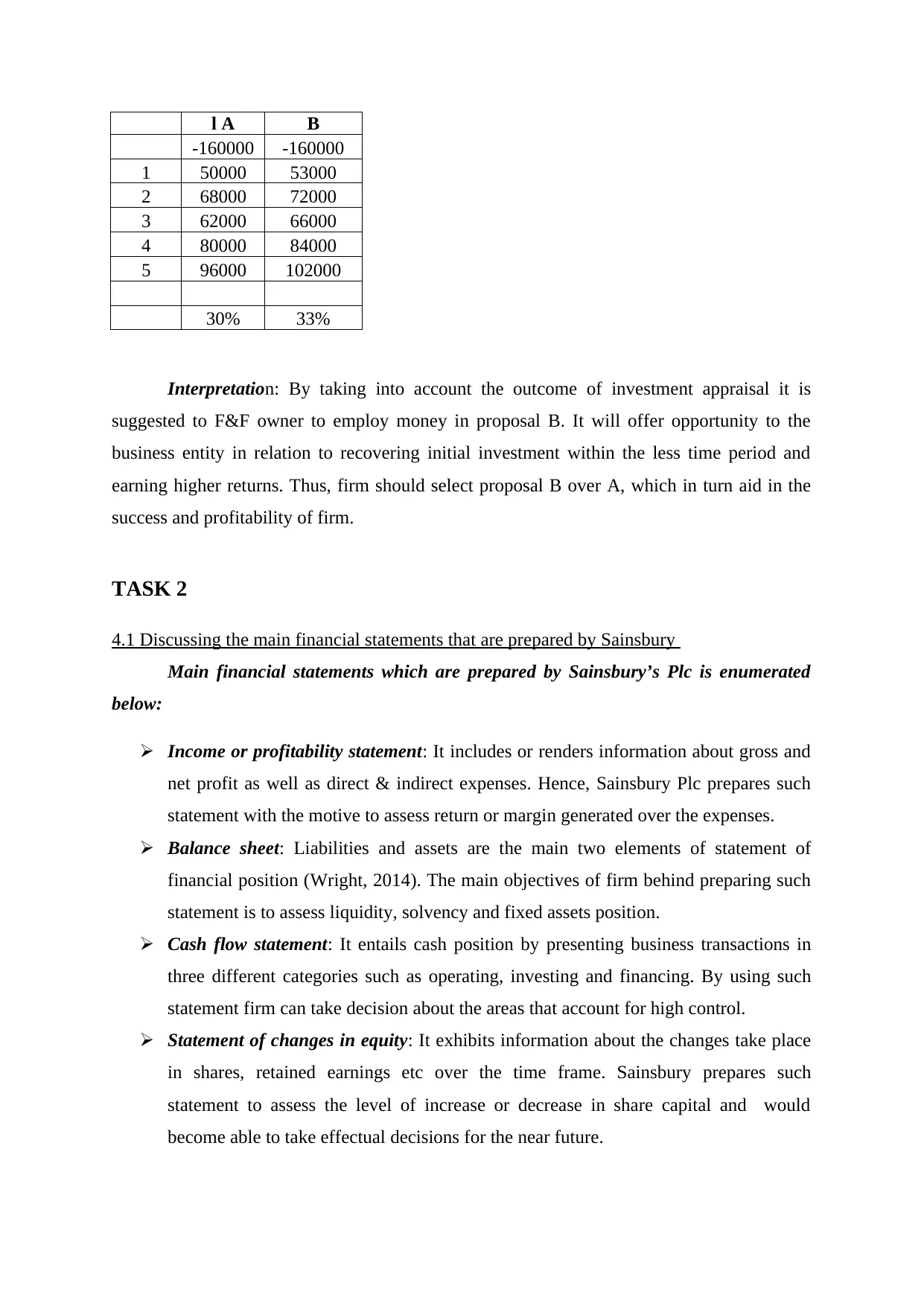

3.3 Evaluating the viability of projects using investment appraisal tools

Investment appraisal tools give indication to the business entity about the viability of

project and helps in making suitable decision (Wahlen, Baginski and Bradshaw, 2014). For

instance: Owner of F&F has two proposals such as A & B with the same initial investment

amounted to £160000 but both the proposals having varied cash flows:

Payback period and NPV

Year

cash

inflow

of

propos

al A

Cumulat

ive cash

inflow

PV

factor

@

10%

Discount

ed cash

flow of

proposal

A

Cash

inflow

of

propos

al B

Cumulat

ive

inflow

Discount

ed cash

flow of

proposal

B

1 50000 50000 0.909 45454.55 53000 53000 48182

2 68000 118000 0.826 56198.35 72000 125000 59504

3 62000 180000 0.751 46581.52 66000 191000 49587

4 80000 260000 0.683 54641.08 84000 275000 57373

5 96000

356000 0.621 59608.45 10200

0

377000

63334

Total

discount

ed cash

inflows

262483.9

3 277980

Less:

Initial

investm

ent 160000 160000

NPV

102483.9

3 117980

Payback period

Project A: 2 + 42000 / 62000

= 2.7 years

Project B: 2 + 35000 / 66000

= 2.5 years

Internal rate of return (IRR)

Year Proposa Proposal

Investment appraisal tools give indication to the business entity about the viability of

project and helps in making suitable decision (Wahlen, Baginski and Bradshaw, 2014). For

instance: Owner of F&F has two proposals such as A & B with the same initial investment

amounted to £160000 but both the proposals having varied cash flows:

Payback period and NPV

Year

cash

inflow

of

propos

al A

Cumulat

ive cash

inflow

PV

factor

@

10%

Discount

ed cash

flow of

proposal

A

Cash

inflow

of

propos

al B

Cumulat

ive

inflow

Discount

ed cash

flow of

proposal

B

1 50000 50000 0.909 45454.55 53000 53000 48182

2 68000 118000 0.826 56198.35 72000 125000 59504

3 62000 180000 0.751 46581.52 66000 191000 49587

4 80000 260000 0.683 54641.08 84000 275000 57373

5 96000

356000 0.621 59608.45 10200

0

377000

63334

Total

discount

ed cash

inflows

262483.9

3 277980

Less:

Initial

investm

ent 160000 160000

NPV

102483.9

3 117980

Payback period

Project A: 2 + 42000 / 62000

= 2.7 years

Project B: 2 + 35000 / 66000

= 2.5 years

Internal rate of return (IRR)

Year Proposa Proposal

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

l A B

-160000 -160000

1 50000 53000

2 68000 72000

3 62000 66000

4 80000 84000

5 96000 102000

30% 33%

Interpretation: By taking into account the outcome of investment appraisal it is

suggested to F&F owner to employ money in proposal B. It will offer opportunity to the

business entity in relation to recovering initial investment within the less time period and

earning higher returns. Thus, firm should select proposal B over A, which in turn aid in the

success and profitability of firm.

TASK 2

4.1 Discussing the main financial statements that are prepared by Sainsbury

Main financial statements which are prepared by Sainsbury’s Plc is enumerated

below:

Income or profitability statement: It includes or renders information about gross and

net profit as well as direct & indirect expenses. Hence, Sainsbury Plc prepares such

statement with the motive to assess return or margin generated over the expenses.

Balance sheet: Liabilities and assets are the main two elements of statement of

financial position (Wright, 2014). The main objectives of firm behind preparing such

statement is to assess liquidity, solvency and fixed assets position.

Cash flow statement: It entails cash position by presenting business transactions in

three different categories such as operating, investing and financing. By using such

statement firm can take decision about the areas that account for high control.

Statement of changes in equity: It exhibits information about the changes take place

in shares, retained earnings etc over the time frame. Sainsbury prepares such

statement to assess the level of increase or decrease in share capital and would

become able to take effectual decisions for the near future.

-160000 -160000

1 50000 53000

2 68000 72000

3 62000 66000

4 80000 84000

5 96000 102000

30% 33%

Interpretation: By taking into account the outcome of investment appraisal it is

suggested to F&F owner to employ money in proposal B. It will offer opportunity to the

business entity in relation to recovering initial investment within the less time period and

earning higher returns. Thus, firm should select proposal B over A, which in turn aid in the

success and profitability of firm.

TASK 2

4.1 Discussing the main financial statements that are prepared by Sainsbury

Main financial statements which are prepared by Sainsbury’s Plc is enumerated

below:

Income or profitability statement: It includes or renders information about gross and

net profit as well as direct & indirect expenses. Hence, Sainsbury Plc prepares such

statement with the motive to assess return or margin generated over the expenses.

Balance sheet: Liabilities and assets are the main two elements of statement of

financial position (Wright, 2014). The main objectives of firm behind preparing such

statement is to assess liquidity, solvency and fixed assets position.

Cash flow statement: It entails cash position by presenting business transactions in

three different categories such as operating, investing and financing. By using such

statement firm can take decision about the areas that account for high control.

Statement of changes in equity: It exhibits information about the changes take place

in shares, retained earnings etc over the time frame. Sainsbury prepares such

statement to assess the level of increase or decrease in share capital and would

become able to take effectual decisions for the near future.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

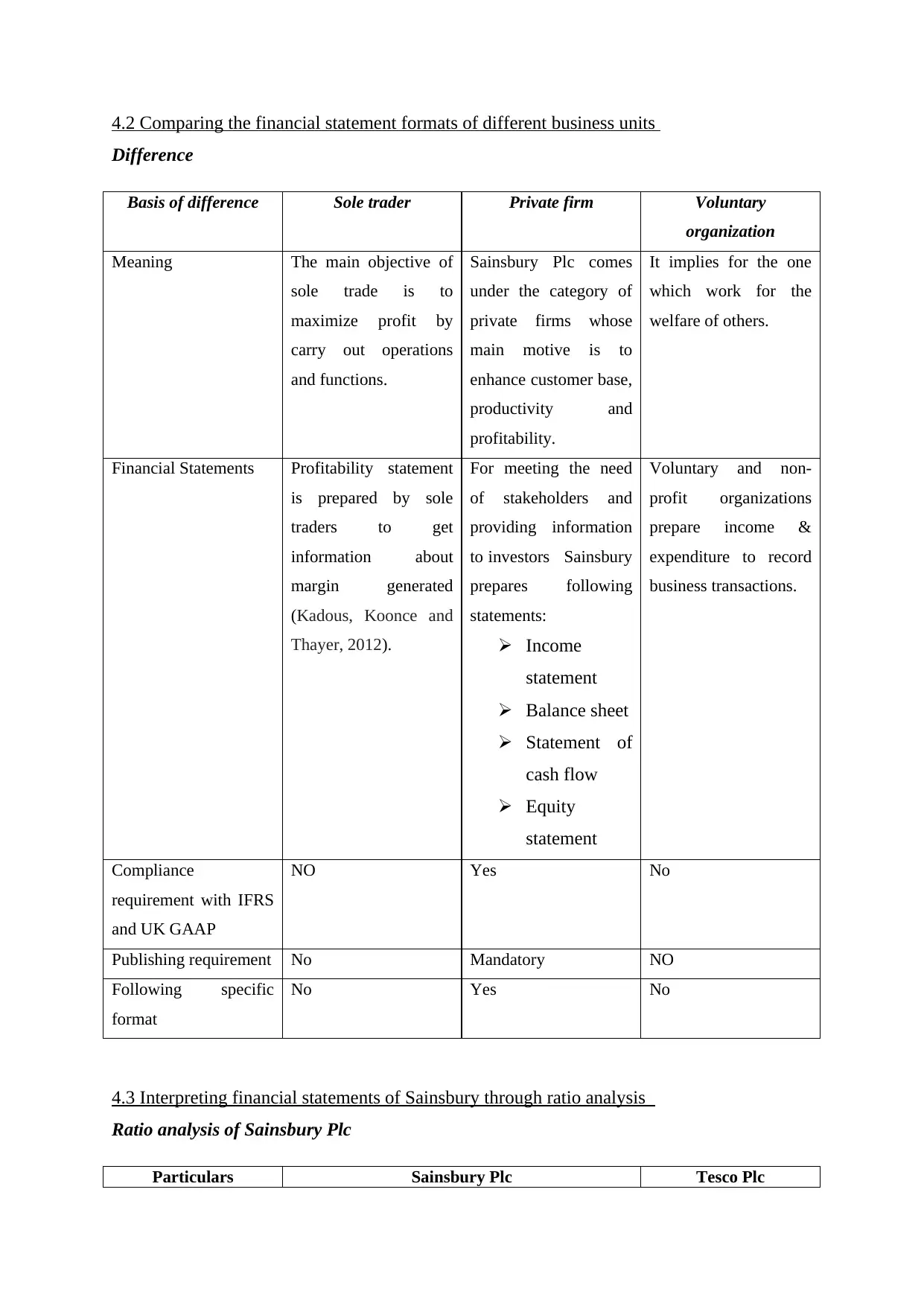

4.2 Comparing the financial statement formats of different business units

Difference

Basis of difference Sole trader Private firm Voluntary

organization

Meaning The main objective of

sole trade is to

maximize profit by

carry out operations

and functions.

Sainsbury Plc comes

under the category of

private firms whose

main motive is to

enhance customer base,

productivity and

profitability.

It implies for the one

which work for the

welfare of others.

Financial Statements Profitability statement

is prepared by sole

traders to get

information about

margin generated

(Kadous, Koonce and

Thayer, 2012).

For meeting the need

of stakeholders and

providing information

to investors Sainsbury

prepares following

statements:

Income

statement

Balance sheet

Statement of

cash flow

Equity

statement

Voluntary and non-

profit organizations

prepare income &

expenditure to record

business transactions.

Compliance

requirement with IFRS

and UK GAAP

NO Yes No

Publishing requirement No Mandatory NO

Following specific

format

No Yes No

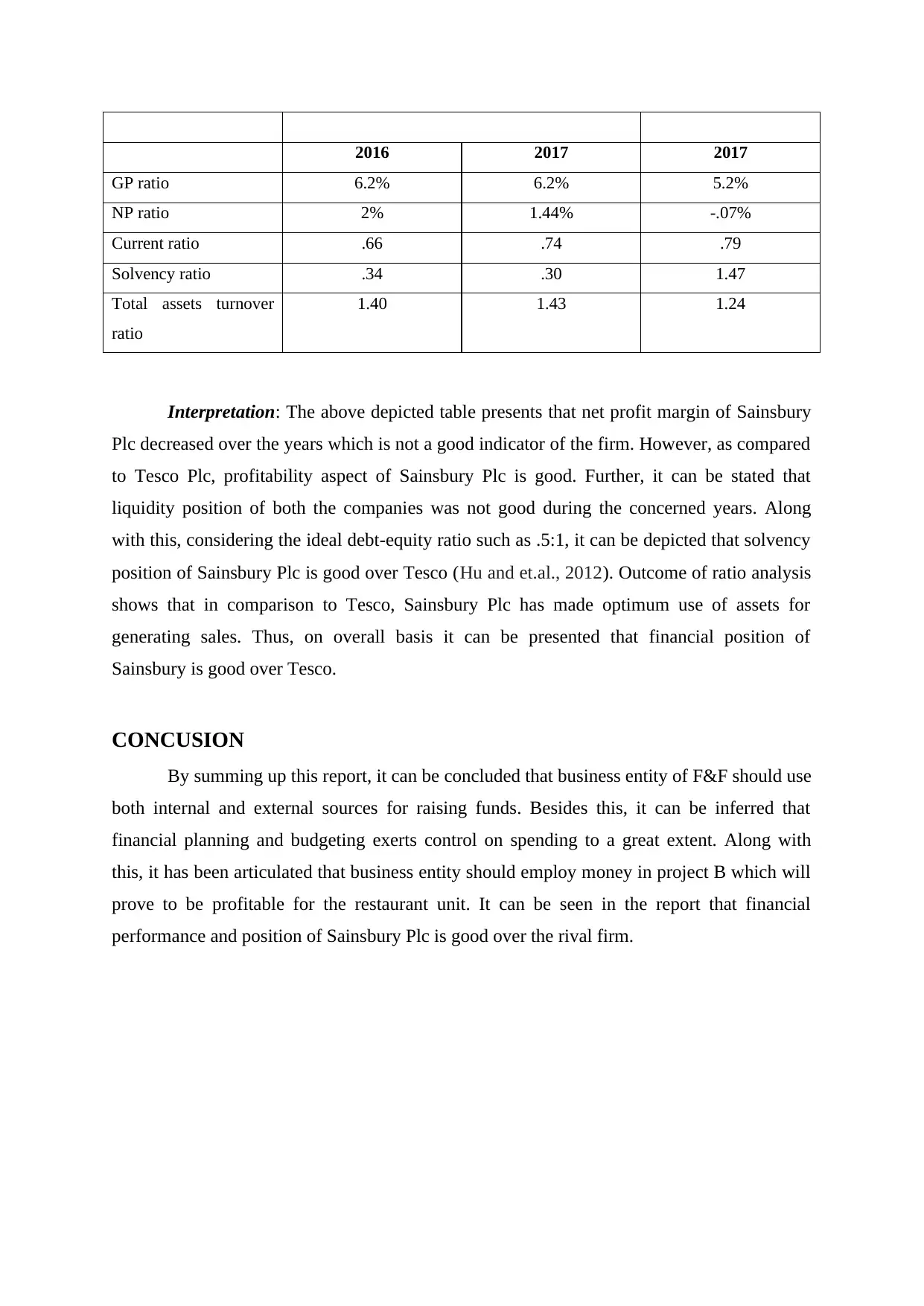

4.3 Interpreting financial statements of Sainsbury through ratio analysis

Ratio analysis of Sainsbury Plc

Particulars Sainsbury Plc Tesco Plc

Difference

Basis of difference Sole trader Private firm Voluntary

organization

Meaning The main objective of

sole trade is to

maximize profit by

carry out operations

and functions.

Sainsbury Plc comes

under the category of

private firms whose

main motive is to

enhance customer base,

productivity and

profitability.

It implies for the one

which work for the

welfare of others.

Financial Statements Profitability statement

is prepared by sole

traders to get

information about

margin generated

(Kadous, Koonce and

Thayer, 2012).

For meeting the need

of stakeholders and

providing information

to investors Sainsbury

prepares following

statements:

Income

statement

Balance sheet

Statement of

cash flow

Equity

statement

Voluntary and non-

profit organizations

prepare income &

expenditure to record

business transactions.

Compliance

requirement with IFRS

and UK GAAP

NO Yes No

Publishing requirement No Mandatory NO

Following specific

format

No Yes No

4.3 Interpreting financial statements of Sainsbury through ratio analysis

Ratio analysis of Sainsbury Plc

Particulars Sainsbury Plc Tesco Plc

2016 2017 2017

GP ratio 6.2% 6.2% 5.2%

NP ratio 2% 1.44% -.07%

Current ratio .66 .74 .79

Solvency ratio .34 .30 1.47

Total assets turnover

ratio

1.40 1.43 1.24

Interpretation: The above depicted table presents that net profit margin of Sainsbury

Plc decreased over the years which is not a good indicator of the firm. However, as compared

to Tesco Plc, profitability aspect of Sainsbury Plc is good. Further, it can be stated that

liquidity position of both the companies was not good during the concerned years. Along

with this, considering the ideal debt-equity ratio such as .5:1, it can be depicted that solvency

position of Sainsbury Plc is good over Tesco (Hu and et.al., 2012). Outcome of ratio analysis

shows that in comparison to Tesco, Sainsbury Plc has made optimum use of assets for

generating sales. Thus, on overall basis it can be presented that financial position of

Sainsbury is good over Tesco.

CONCUSION

By summing up this report, it can be concluded that business entity of F&F should use

both internal and external sources for raising funds. Besides this, it can be inferred that

financial planning and budgeting exerts control on spending to a great extent. Along with

this, it has been articulated that business entity should employ money in project B which will

prove to be profitable for the restaurant unit. It can be seen in the report that financial

performance and position of Sainsbury Plc is good over the rival firm.

GP ratio 6.2% 6.2% 5.2%

NP ratio 2% 1.44% -.07%

Current ratio .66 .74 .79

Solvency ratio .34 .30 1.47

Total assets turnover

ratio

1.40 1.43 1.24

Interpretation: The above depicted table presents that net profit margin of Sainsbury

Plc decreased over the years which is not a good indicator of the firm. However, as compared

to Tesco Plc, profitability aspect of Sainsbury Plc is good. Further, it can be stated that

liquidity position of both the companies was not good during the concerned years. Along

with this, considering the ideal debt-equity ratio such as .5:1, it can be depicted that solvency

position of Sainsbury Plc is good over Tesco (Hu and et.al., 2012). Outcome of ratio analysis

shows that in comparison to Tesco, Sainsbury Plc has made optimum use of assets for

generating sales. Thus, on overall basis it can be presented that financial position of

Sainsbury is good over Tesco.

CONCUSION

By summing up this report, it can be concluded that business entity of F&F should use

both internal and external sources for raising funds. Besides this, it can be inferred that

financial planning and budgeting exerts control on spending to a great extent. Along with

this, it has been articulated that business entity should employ money in project B which will

prove to be profitable for the restaurant unit. It can be seen in the report that financial

performance and position of Sainsbury Plc is good over the rival firm.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.