University Finance Report: Managing Financial Resources and Decisions

VerifiedAdded on 2020/01/28

|23

|4822

|57

Report

AI Summary

This finance report comprehensively addresses financial resource management, encompassing various key aspects. It begins with the preparation and analysis of a cash budget, crucial for evaluating liquidity. The report then delves into calculating selling prices, profit margins, and the impact of markups on profitability. Investment decisions are analyzed using Net Present Value (NPV) and payback period calculations, offering insights into the viability of different investment options. The report also examines financial statements, including balance sheets and income statements, comparing their formats for different business organizations. Furthermore, it assesses the information needs of various financial statement users and interprets financial data using relevant ratios, such as profitability and gearing ratios. Finally, the report explores diverse sources of finance available to businesses, evaluating their implications and identifying the most appropriate funding options. It also discusses the cost of finance, its impact on financial statements, and the importance of financial planning.

Managing Financial

Resource and Decisions

Resource and Decisions

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Introduction......................................................................................................................................4

Task 1...............................................................................................................................................4

(a) Preparing the Cash Budget (3.1):...........................................................................................4

(b) Cash budget analysis (3.1):....................................................................................................5

Task 2 ..............................................................................................................................................5

(a) [I] Calculating selling price per unit (3.2)..............................................................................5

(a) [ii] Total profit on the sale of 300 units (3.2).........................................................................6

(b) [I] Calculating cost and selling price with a markup of 40% (3.2)........................................6

(b) [ii] total profit earned on selling of additional 100 units (3.2)...............................................6

Task 3...............................................................................................................................................7

(a). Analysis of budgets and making appropriate decision (3.3).................................................7

(b). Recommendation (3.3)..........................................................................................................9

Task 4...............................................................................................................................................9

(a). Main financial statements and Comparing the formats of financial statements for the

different types of business organization (4.1 and 4.2 )................................................................9

(b) Assessing the information needs of different users of financial

statements (2.3).........................................................................................................................15

(c). Interpretation of the financial statements using appropriate ratios & comparisons (4.3). . .15

Task 5.............................................................................................................................................17

5a [i] Different sources of finance available for business (1.1):................................................17

5a (ii) Assessment the implication of different sources of finance and most appropriate source

of finance for business (1.2 and 1.3)..........................................................................................18

5a (iii) Explanation the cost of sources of finance (2.1)............................................................19

5a (IV) Impact of sources of finance on financial statements of business (2.4)........................20

5a (v) the importance of financial planning (2.2)......................................................................21

Conclusion.....................................................................................................................................23

Reference.......................................................................................................................................24

Introduction......................................................................................................................................4

Task 1...............................................................................................................................................4

(a) Preparing the Cash Budget (3.1):...........................................................................................4

(b) Cash budget analysis (3.1):....................................................................................................5

Task 2 ..............................................................................................................................................5

(a) [I] Calculating selling price per unit (3.2)..............................................................................5

(a) [ii] Total profit on the sale of 300 units (3.2).........................................................................6

(b) [I] Calculating cost and selling price with a markup of 40% (3.2)........................................6

(b) [ii] total profit earned on selling of additional 100 units (3.2)...............................................6

Task 3...............................................................................................................................................7

(a). Analysis of budgets and making appropriate decision (3.3).................................................7

(b). Recommendation (3.3)..........................................................................................................9

Task 4...............................................................................................................................................9

(a). Main financial statements and Comparing the formats of financial statements for the

different types of business organization (4.1 and 4.2 )................................................................9

(b) Assessing the information needs of different users of financial

statements (2.3).........................................................................................................................15

(c). Interpretation of the financial statements using appropriate ratios & comparisons (4.3). . .15

Task 5.............................................................................................................................................17

5a [i] Different sources of finance available for business (1.1):................................................17

5a (ii) Assessment the implication of different sources of finance and most appropriate source

of finance for business (1.2 and 1.3)..........................................................................................18

5a (iii) Explanation the cost of sources of finance (2.1)............................................................19

5a (IV) Impact of sources of finance on financial statements of business (2.4)........................20

5a (v) the importance of financial planning (2.2)......................................................................21

Conclusion.....................................................................................................................................23

Reference.......................................................................................................................................24

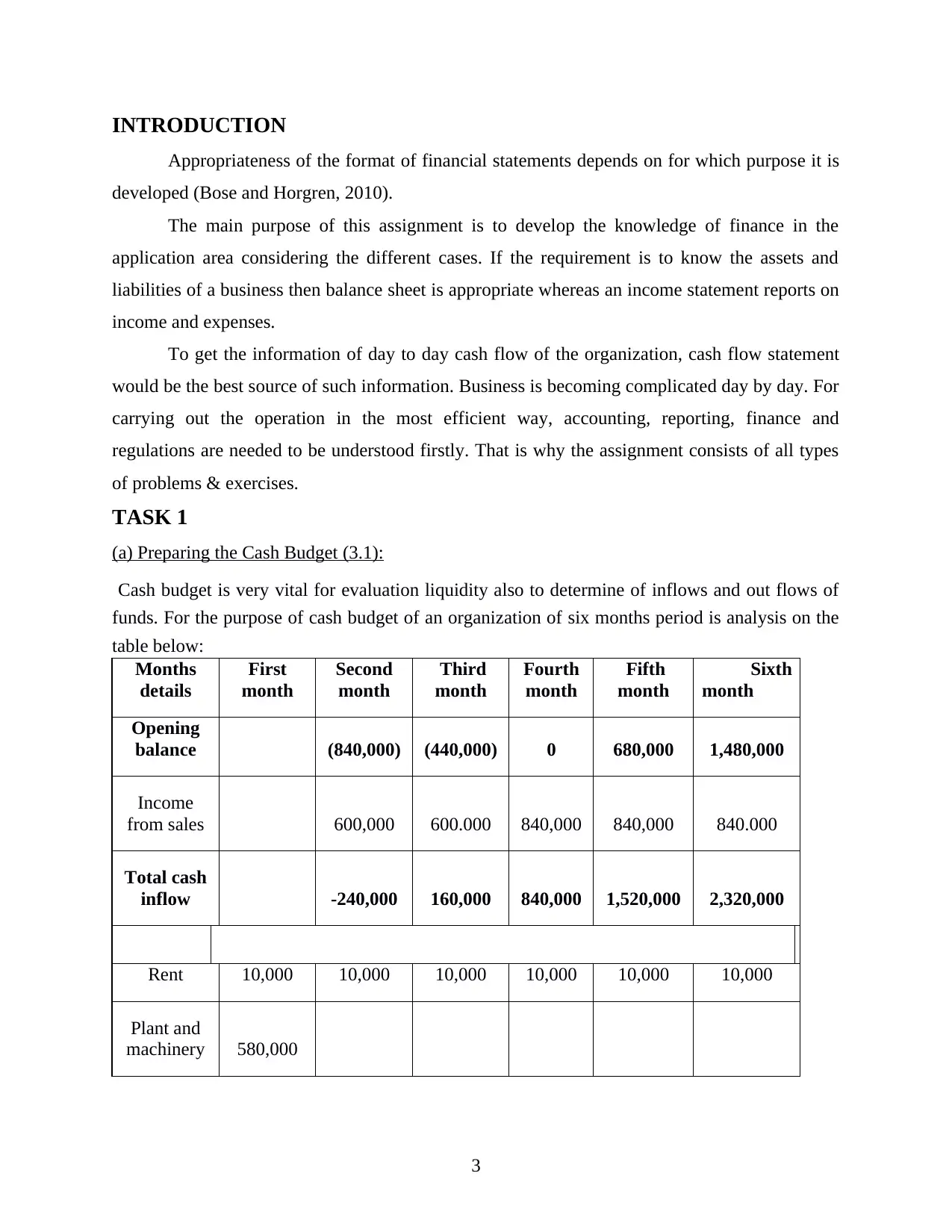

INTRODUCTION

Appropriateness of the format of financial statements depends on for which purpose it is

developed (Bose and Horgren, 2010).

The main purpose of this assignment is to develop the knowledge of finance in the

application area considering the different cases. If the requirement is to know the assets and

liabilities of a business then balance sheet is appropriate whereas an income statement reports on

income and expenses.

To get the information of day to day cash flow of the organization, cash flow statement

would be the best source of such information. Business is becoming complicated day by day. For

carrying out the operation in the most efficient way, accounting, reporting, finance and

regulations are needed to be understood firstly. That is why the assignment consists of all types

of problems & exercises.

TASK 1

(a) Preparing the Cash Budget (3.1):

Cash budget is very vital for evaluation liquidity also to determine of inflows and out flows of

funds. For the purpose of cash budget of an organization of six months period is analysis on the

table below:

Months

details

First

month

Second

month

Third

month

Fourth

month

Fifth

month

Sixth

month

Opening

balance (840,000) (440,000) 0 680,000 1,480,000

Income

from sales 600,000 600.000 840,000 840,000 840.000

Total cash

inflow -240,000 160,000 840,000 1,520,000 2,320,000

Rent 10,000 10,000 10,000 10,000 10,000 10,000

Plant and

machinery 580,000

3

Appropriateness of the format of financial statements depends on for which purpose it is

developed (Bose and Horgren, 2010).

The main purpose of this assignment is to develop the knowledge of finance in the

application area considering the different cases. If the requirement is to know the assets and

liabilities of a business then balance sheet is appropriate whereas an income statement reports on

income and expenses.

To get the information of day to day cash flow of the organization, cash flow statement

would be the best source of such information. Business is becoming complicated day by day. For

carrying out the operation in the most efficient way, accounting, reporting, finance and

regulations are needed to be understood firstly. That is why the assignment consists of all types

of problems & exercises.

TASK 1

(a) Preparing the Cash Budget (3.1):

Cash budget is very vital for evaluation liquidity also to determine of inflows and out flows of

funds. For the purpose of cash budget of an organization of six months period is analysis on the

table below:

Months

details

First

month

Second

month

Third

month

Fourth

month

Fifth

month

Sixth

month

Opening

balance (840,000) (440,000) 0 680,000 1,480,000

Income

from sales 600,000 600.000 840,000 840,000 840.000

Total cash

inflow -240,000 160,000 840,000 1,520,000 2,320,000

Rent 10,000 10,000 10,000 10,000 10,000 10,000

Plant and

machinery 580,000

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

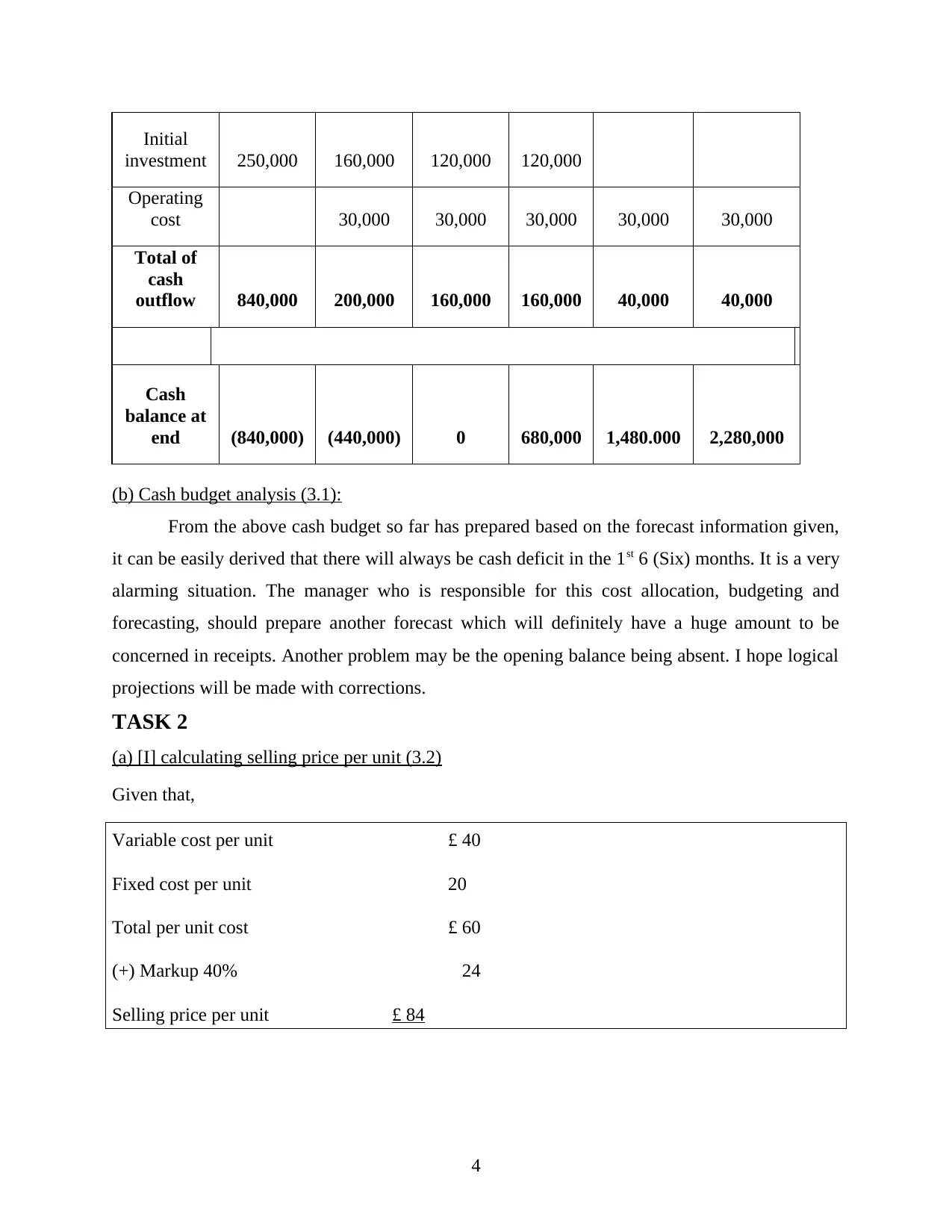

Initial

investment 250,000 160,000 120,000 120,000

Operating

cost 30,000 30,000 30,000 30,000 30,000

Total of

cash

outflow 840,000 200,000 160,000 160,000 40,000 40,000

Cash

balance at

end (840,000) (440,000) 0 680,000 1,480.000 2,280,000

(b) Cash budget analysis (3.1):

From the above cash budget so far has prepared based on the forecast information given,

it can be easily derived that there will always be cash deficit in the 1st 6 (Six) months. It is a very

alarming situation. The manager who is responsible for this cost allocation, budgeting and

forecasting, should prepare another forecast which will definitely have a huge amount to be

concerned in receipts. Another problem may be the opening balance being absent. I hope logical

projections will be made with corrections.

TASK 2

(a) [I] calculating selling price per unit (3.2)

Given that,

Variable cost per unit £ 40

Fixed cost per unit 20

Total per unit cost £ 60

(+) Markup 40% 24

Selling price per unit £ 84

4

investment 250,000 160,000 120,000 120,000

Operating

cost 30,000 30,000 30,000 30,000 30,000

Total of

cash

outflow 840,000 200,000 160,000 160,000 40,000 40,000

Cash

balance at

end (840,000) (440,000) 0 680,000 1,480.000 2,280,000

(b) Cash budget analysis (3.1):

From the above cash budget so far has prepared based on the forecast information given,

it can be easily derived that there will always be cash deficit in the 1st 6 (Six) months. It is a very

alarming situation. The manager who is responsible for this cost allocation, budgeting and

forecasting, should prepare another forecast which will definitely have a huge amount to be

concerned in receipts. Another problem may be the opening balance being absent. I hope logical

projections will be made with corrections.

TASK 2

(a) [I] calculating selling price per unit (3.2)

Given that,

Variable cost per unit £ 40

Fixed cost per unit 20

Total per unit cost £ 60

(+) Markup 40% 24

Selling price per unit £ 84

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

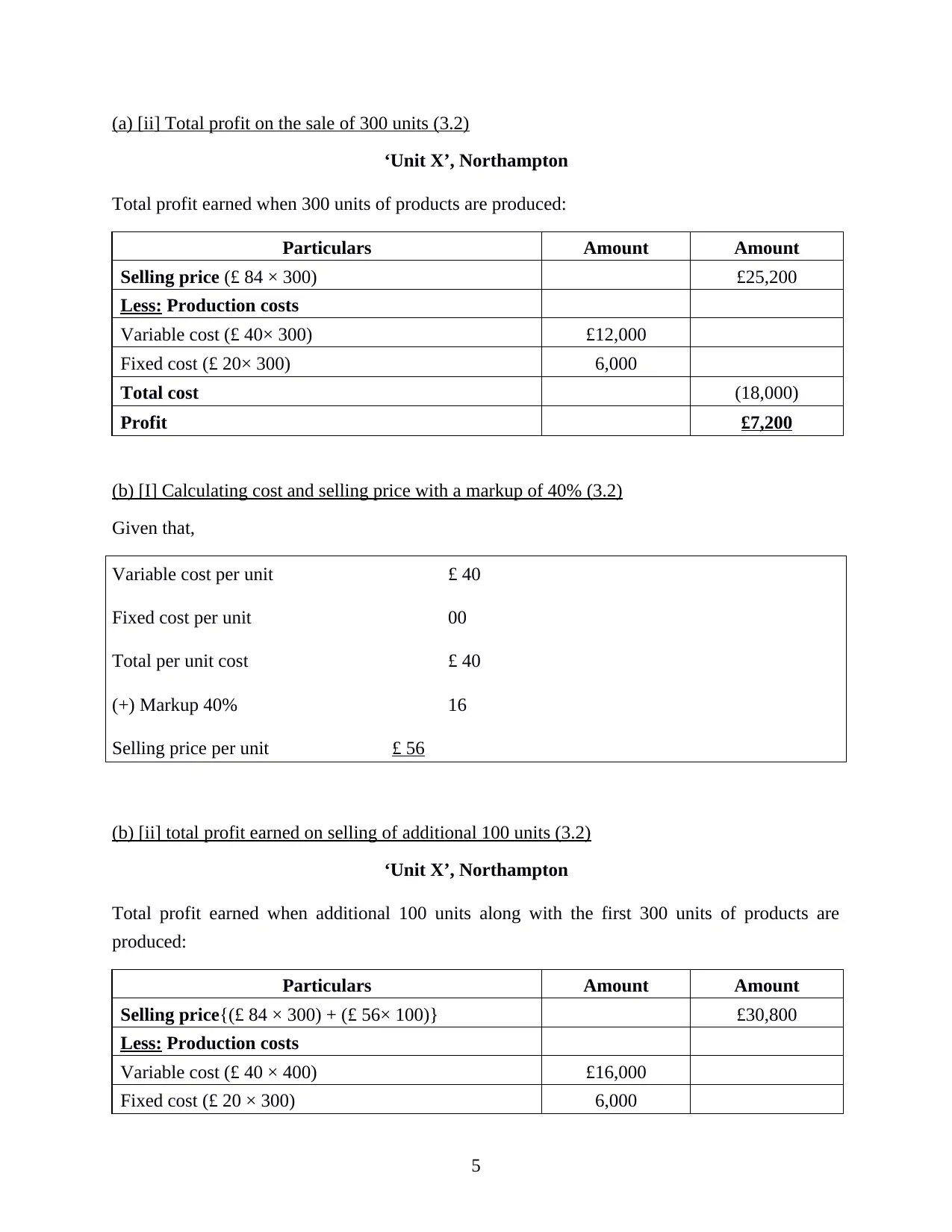

(a) [ii] Total profit on the sale of 300 units (3.2)

‘Unit X’, Northampton

Total profit earned when 300 units of products are produced:

Particulars Amount Amount

Selling price (£ 84 × 300) £25,200

Less: Production costs

Variable cost (£ 40× 300) £12,000

Fixed cost (£ 20× 300) 6,000

Total cost (18,000)

Profit £7,200

(b) [I] Calculating cost and selling price with a markup of 40% (3.2)

Given that,

Variable cost per unit £ 40

Fixed cost per unit 00

Total per unit cost £ 40

(+) Markup 40% 16

Selling price per unit £ 56

(b) [ii] total profit earned on selling of additional 100 units (3.2)

‘Unit X’, Northampton

Total profit earned when additional 100 units along with the first 300 units of products are

produced:

Particulars Amount Amount

Selling price{(£ 84 × 300) + (£ 56× 100)} £30,800

Less: Production costs

Variable cost (£ 40 × 400) £16,000

Fixed cost (£ 20 × 300) 6,000

5

‘Unit X’, Northampton

Total profit earned when 300 units of products are produced:

Particulars Amount Amount

Selling price (£ 84 × 300) £25,200

Less: Production costs

Variable cost (£ 40× 300) £12,000

Fixed cost (£ 20× 300) 6,000

Total cost (18,000)

Profit £7,200

(b) [I] Calculating cost and selling price with a markup of 40% (3.2)

Given that,

Variable cost per unit £ 40

Fixed cost per unit 00

Total per unit cost £ 40

(+) Markup 40% 16

Selling price per unit £ 56

(b) [ii] total profit earned on selling of additional 100 units (3.2)

‘Unit X’, Northampton

Total profit earned when additional 100 units along with the first 300 units of products are

produced:

Particulars Amount Amount

Selling price{(£ 84 × 300) + (£ 56× 100)} £30,800

Less: Production costs

Variable cost (£ 40 × 400) £16,000

Fixed cost (£ 20 × 300) 6,000

5

Total cost (22,000)

Profit £8,800

TASK 3

(a). Analysis of budgets and making appropriate decision (3.3)

Net present value calculations: Is effective way for processing investment assessment for

approximate of cash inflows and outflows at a reduced price as regard to inflation rate of the

economy so that money value technique can be measures in order to evaluate current value of

future cash flow (Drake and Fabozzi, 2012). .

Formula-

NPV = R ×, 1 − (1 + i)-n, − Initial Investment.

Table 2: NPV Investment for A

Yr Cash Inflow for

Option A (£) (R) D.F at 12%

(one) Present

Value(£)

1st yr 24,000 0.892 21,408

2rd yr 24,000 0.797 19,128

3rd yr 24,000 0.711 17,064

4th yr 24,000 0.6355 15,252

The Total of Present

Value 72,852

Less: Initial Investment 75,000

N/P/ Value -2,148

Table 3: NPV Investment for option B

Yr Cash Inflow for

Option B(£) D.F at 12% Present

Value(£)

1st yr 25,000 0.892 22,300

2nd yr 25,000 0.797 19,925

3rd yr 25,000 0.711 17,775

4th yr 25,000 0.6355 15,887.5

The total of Present Value 75,887.5

Less: Initial Investment 80,000

N/P/ Value -4,112.5

Table 4: NPV Investment for option C

Yr Cash Inflow for

Option C (£) D.F at 12% Present

Value(£)

1st Yr 36,000 0.892 32,112

6

Profit £8,800

TASK 3

(a). Analysis of budgets and making appropriate decision (3.3)

Net present value calculations: Is effective way for processing investment assessment for

approximate of cash inflows and outflows at a reduced price as regard to inflation rate of the

economy so that money value technique can be measures in order to evaluate current value of

future cash flow (Drake and Fabozzi, 2012). .

Formula-

NPV = R ×, 1 − (1 + i)-n, − Initial Investment.

Table 2: NPV Investment for A

Yr Cash Inflow for

Option A (£) (R) D.F at 12%

(one) Present

Value(£)

1st yr 24,000 0.892 21,408

2rd yr 24,000 0.797 19,128

3rd yr 24,000 0.711 17,064

4th yr 24,000 0.6355 15,252

The Total of Present

Value 72,852

Less: Initial Investment 75,000

N/P/ Value -2,148

Table 3: NPV Investment for option B

Yr Cash Inflow for

Option B(£) D.F at 12% Present

Value(£)

1st yr 25,000 0.892 22,300

2nd yr 25,000 0.797 19,925

3rd yr 25,000 0.711 17,775

4th yr 25,000 0.6355 15,887.5

The total of Present Value 75,887.5

Less: Initial Investment 80,000

N/P/ Value -4,112.5

Table 4: NPV Investment for option C

Yr Cash Inflow for

Option C (£) D.F at 12% Present

Value(£)

1st Yr 36,000 0.892 32,112

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

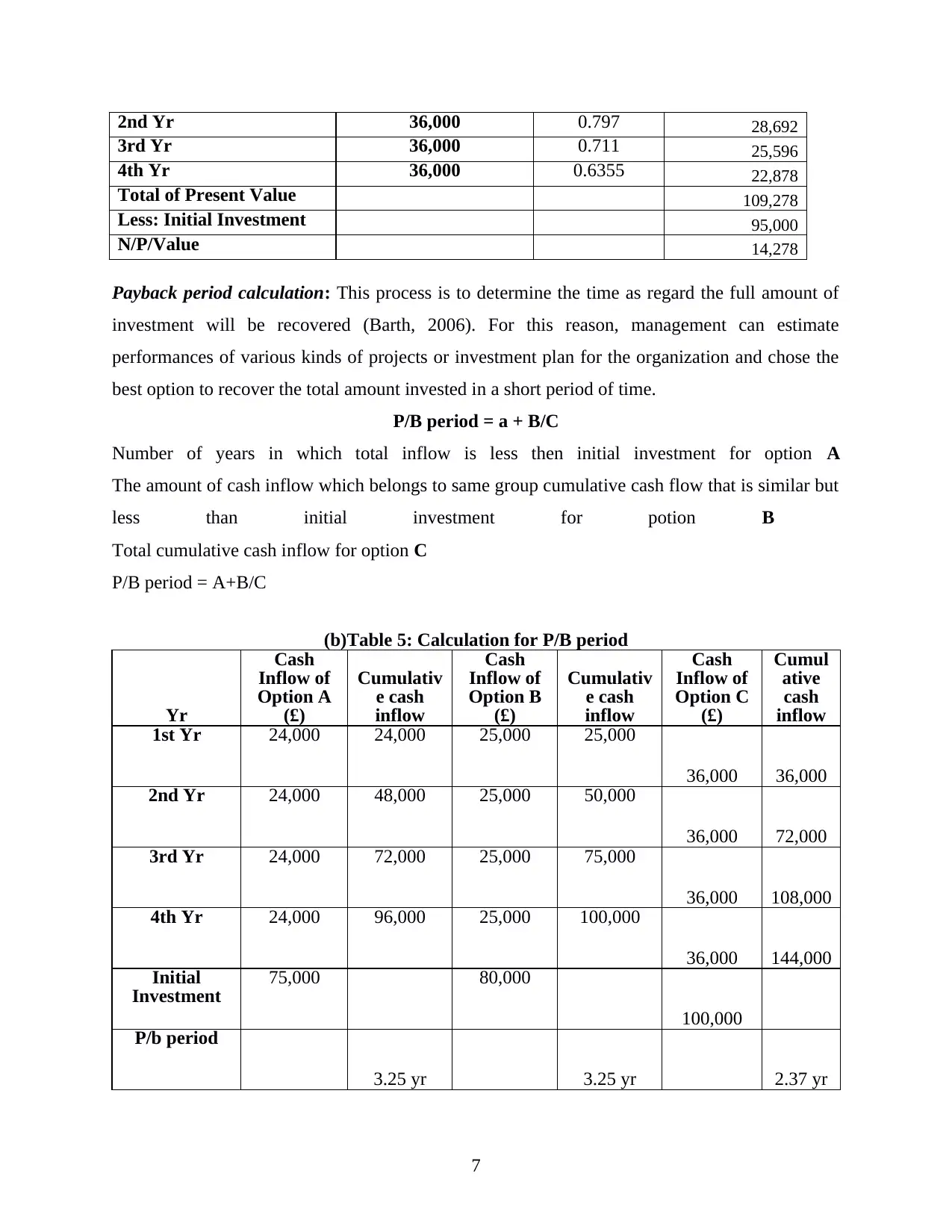

2nd Yr 36,000 0.797 28,692

3rd Yr 36,000 0.711 25,596

4th Yr 36,000 0.6355 22,878

Total of Present Value 109,278

Less: Initial Investment 95,000

N/P/Value 14,278

Payback period calculation: This process is to determine the time as regard the full amount of

investment will be recovered (Barth, 2006). For this reason, management can estimate

performances of various kinds of projects or investment plan for the organization and chose the

best option to recover the total amount invested in a short period of time.

P/B period = a + B/C

Number of years in which total inflow is less then initial investment for option A

The amount of cash inflow which belongs to same group cumulative cash flow that is similar but

less than initial investment for potion B

Total cumulative cash inflow for option C

P/B period = A+B/C

(b)Table 5: Calculation for P/B period

Yr

Cash

Inflow of

Option A

(£)

Cumulativ

e cash

inflow

Cash

Inflow of

Option B

(£)

Cumulativ

e cash

inflow

Cash

Inflow of

Option C

(£)

Cumul

ative

cash

inflow

1st Yr 24,000 24,000 25,000 25,000

36,000 36,000

2nd Yr 24,000 48,000 25,000 50,000

36,000 72,000

3rd Yr 24,000 72,000 25,000 75,000

36,000 108,000

4th Yr 24,000 96,000 25,000 100,000

36,000 144,000

Initial

Investment 75,000 80,000

100,000

P/b period

3.25 yr 3.25 yr 2.37 yr

7

3rd Yr 36,000 0.711 25,596

4th Yr 36,000 0.6355 22,878

Total of Present Value 109,278

Less: Initial Investment 95,000

N/P/Value 14,278

Payback period calculation: This process is to determine the time as regard the full amount of

investment will be recovered (Barth, 2006). For this reason, management can estimate

performances of various kinds of projects or investment plan for the organization and chose the

best option to recover the total amount invested in a short period of time.

P/B period = a + B/C

Number of years in which total inflow is less then initial investment for option A

The amount of cash inflow which belongs to same group cumulative cash flow that is similar but

less than initial investment for potion B

Total cumulative cash inflow for option C

P/B period = A+B/C

(b)Table 5: Calculation for P/B period

Yr

Cash

Inflow of

Option A

(£)

Cumulativ

e cash

inflow

Cash

Inflow of

Option B

(£)

Cumulativ

e cash

inflow

Cash

Inflow of

Option C

(£)

Cumul

ative

cash

inflow

1st Yr 24,000 24,000 25,000 25,000

36,000 36,000

2nd Yr 24,000 48,000 25,000 50,000

36,000 72,000

3rd Yr 24,000 72,000 25,000 75,000

36,000 108,000

4th Yr 24,000 96,000 25,000 100,000

36,000 144,000

Initial

Investment 75,000 80,000

100,000

P/b period

3.25 yr 3.25 yr 2.37 yr

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(b). Recommendation (3.3)

From above analysis management is require to accept C option for the assessment of net present

value of various plan which show that NPV of Project C is higher as contrast to other plan The

study of payback period decide that project will recover the total investment in less time as

contrast to other projects. So, data collected by both viewpoints obviously indicate that

management should accept Project C for growth (Ittelson, 2009).

TASK 4

(a). Main financial statements and Comparing the formats of financial statements for the

different types of business organization (4.1 and 4.2 )

There are various types of financial statements which are used to keep the records of financial

activities done by the business, which also helps managers and stakeholders to understand how

business is doing. The vital financial statement as follow: Balance sheet: Is the source that supplies vital information about all assets and liabilities

of the organization. Which study the current financial position of activities of the

business. Which is use by all firms’ big and small organization? Which reflect the vital

information requires such loan as well as share capital of the organization for a specific

period (Narayanan and Nanda, 2004). Income statement: Is a statement which is use by various kinds of organization. Which

assist the management understand position such as profit and the reduction of total

income from expense in an accounting period. Which is very effectual way to analyze

income and expense of the organization?

Cash flow statement: This is utilizing by big organization as it contains specific

information concerning every cash arrangement. This application explains the outflow

and inflow funds. This information assists in order to control liquidity position of the

organization. This explain position of cash transaction also income statement also shows

non cash application (Anthony, 2011).

Appropriateness of the format of financial statements depends on which purpose it is developed.

For example, if the requirement is to know the assets and liabilities of a business then balance

sheet is appropriate whereas an income statement reports on income and expenses.

To get the information of day to day cash flow of the organization, cash flow statement would be

the best source of such information (Smith & Brigham, 2007).

8

From above analysis management is require to accept C option for the assessment of net present

value of various plan which show that NPV of Project C is higher as contrast to other plan The

study of payback period decide that project will recover the total investment in less time as

contrast to other projects. So, data collected by both viewpoints obviously indicate that

management should accept Project C for growth (Ittelson, 2009).

TASK 4

(a). Main financial statements and Comparing the formats of financial statements for the

different types of business organization (4.1 and 4.2 )

There are various types of financial statements which are used to keep the records of financial

activities done by the business, which also helps managers and stakeholders to understand how

business is doing. The vital financial statement as follow: Balance sheet: Is the source that supplies vital information about all assets and liabilities

of the organization. Which study the current financial position of activities of the

business. Which is use by all firms’ big and small organization? Which reflect the vital

information requires such loan as well as share capital of the organization for a specific

period (Narayanan and Nanda, 2004). Income statement: Is a statement which is use by various kinds of organization. Which

assist the management understand position such as profit and the reduction of total

income from expense in an accounting period. Which is very effectual way to analyze

income and expense of the organization?

Cash flow statement: This is utilizing by big organization as it contains specific

information concerning every cash arrangement. This application explains the outflow

and inflow funds. This information assists in order to control liquidity position of the

organization. This explain position of cash transaction also income statement also shows

non cash application (Anthony, 2011).

Appropriateness of the format of financial statements depends on which purpose it is developed.

For example, if the requirement is to know the assets and liabilities of a business then balance

sheet is appropriate whereas an income statement reports on income and expenses.

To get the information of day to day cash flow of the organization, cash flow statement would be

the best source of such information (Smith & Brigham, 2007).

8

The main purpose of the financial statement is to represent financial information regarding

financial position, performance and changes in financial position of a business organization in

front of a wide range of users so that they can take the appropriate decision in future for the

betterment of that organization (Smith & Brigham, 2007). On the other hand, statement of retain

earnings helps to determine the equity issues more specifically.

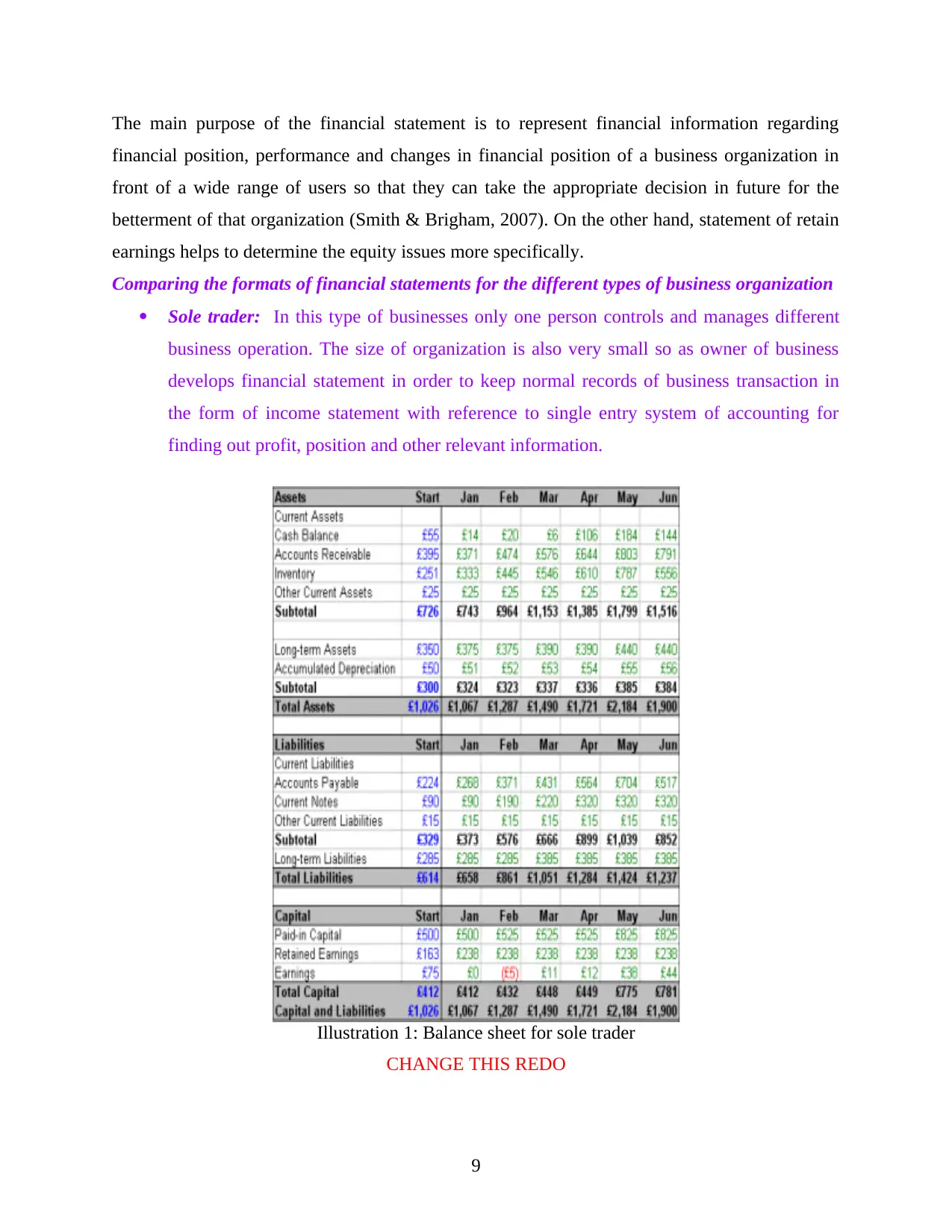

Comparing the formats of financial statements for the different types of business organization

Sole trader: In this type of businesses only one person controls and manages different

business operation. The size of organization is also very small so as owner of business

develops financial statement in order to keep normal records of business transaction in

the form of income statement with reference to single entry system of accounting for

finding out profit, position and other relevant information.

9

Illustration 1: Balance sheet for sole trader

CHANGE THIS REDO

financial position, performance and changes in financial position of a business organization in

front of a wide range of users so that they can take the appropriate decision in future for the

betterment of that organization (Smith & Brigham, 2007). On the other hand, statement of retain

earnings helps to determine the equity issues more specifically.

Comparing the formats of financial statements for the different types of business organization

Sole trader: In this type of businesses only one person controls and manages different

business operation. The size of organization is also very small so as owner of business

develops financial statement in order to keep normal records of business transaction in

the form of income statement with reference to single entry system of accounting for

finding out profit, position and other relevant information.

9

Illustration 1: Balance sheet for sole trader

CHANGE THIS REDO

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

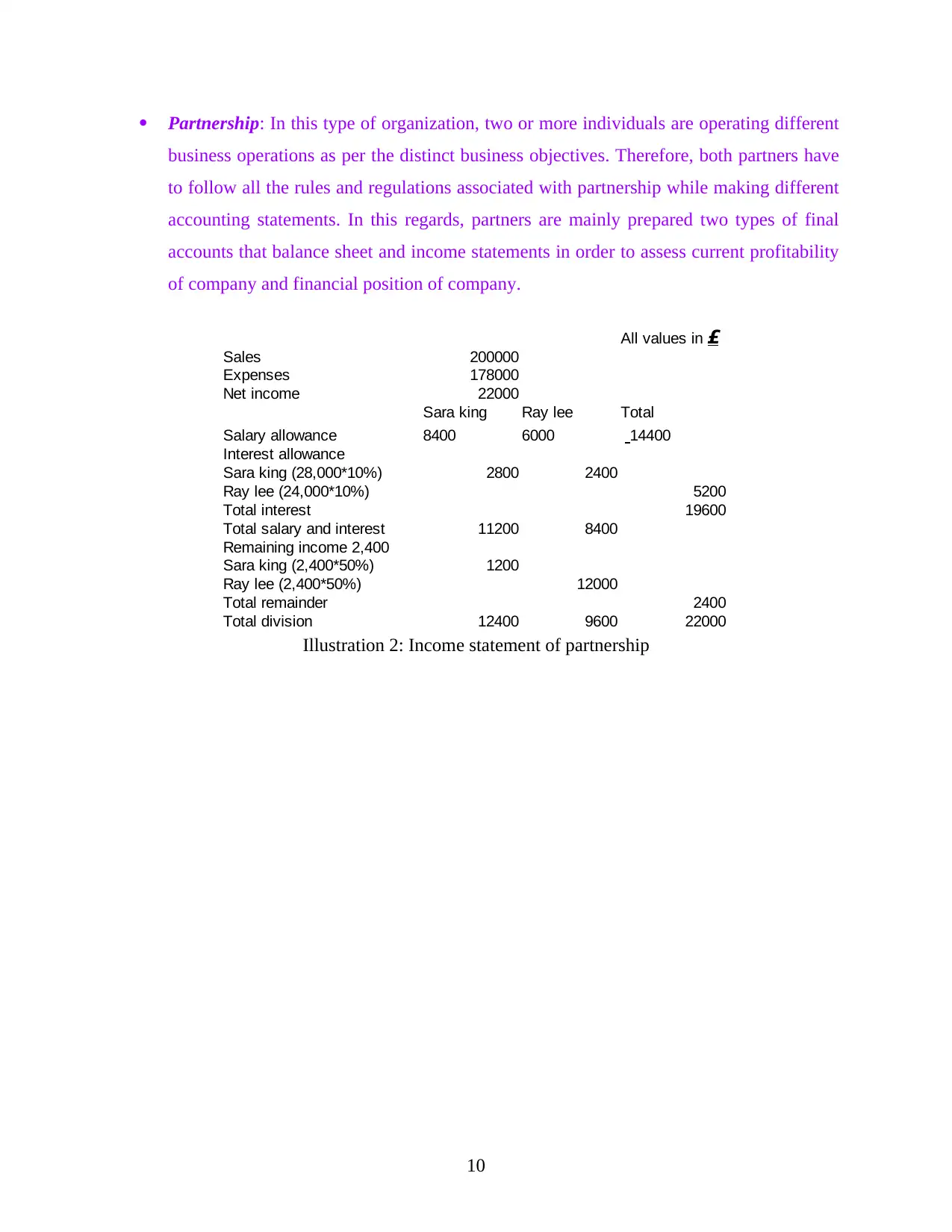

Partnership: In this type of organization, two or more individuals are operating different

business operations as per the distinct business objectives. Therefore, both partners have

to follow all the rules and regulations associated with partnership while making different

accounting statements. In this regards, partners are mainly prepared two types of final

accounts that balance sheet and income statements in order to assess current profitability

of company and financial position of company.

10

Sales 200000

Expenses 178000

Net income 22000

Sara king Ray lee Total

Salary allowance 8400 6000

Interest allowance

Sara king (28,000*10%) 2800 2400

Ray lee (24,000*10%) 5200

Total interest 19600

Total salary and interest 11200 8400

Remaining income 2,400

Sara king (2,400*50%) 1200

Ray lee (2,400*50%) 12000

Total remainder 2400

Total division 12400 9600 22000

All values in £

14400

Illustration 2: Income statement of partnership

business operations as per the distinct business objectives. Therefore, both partners have

to follow all the rules and regulations associated with partnership while making different

accounting statements. In this regards, partners are mainly prepared two types of final

accounts that balance sheet and income statements in order to assess current profitability

of company and financial position of company.

10

Sales 200000

Expenses 178000

Net income 22000

Sara king Ray lee Total

Salary allowance 8400 6000

Interest allowance

Sara king (28,000*10%) 2800 2400

Ray lee (24,000*10%) 5200

Total interest 19600

Total salary and interest 11200 8400

Remaining income 2,400

Sara king (2,400*50%) 1200

Ray lee (2,400*50%) 12000

Total remainder 2400

Total division 12400 9600 22000

All values in £

14400

Illustration 2: Income statement of partnership

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

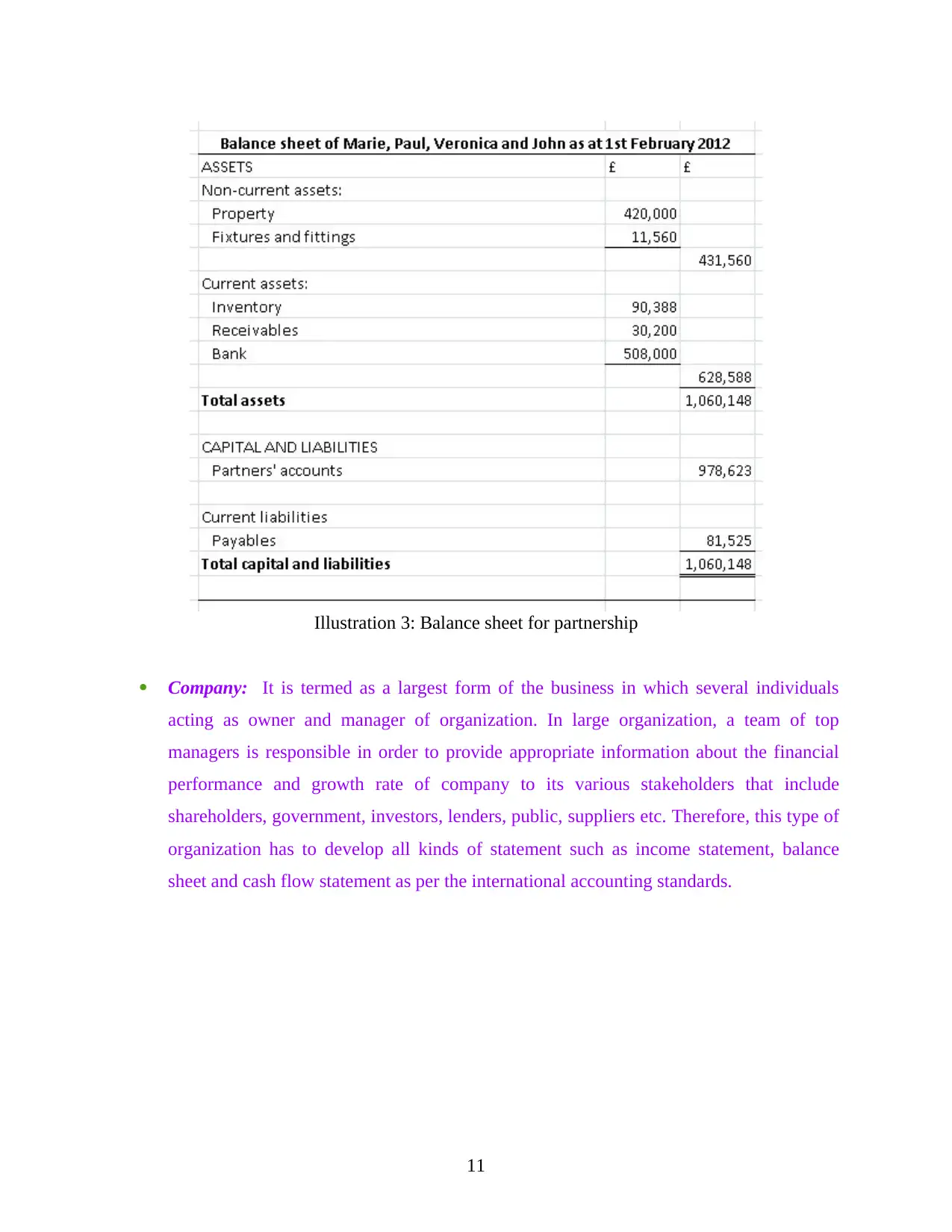

Company: It is termed as a largest form of the business in which several individuals

acting as owner and manager of organization. In large organization, a team of top

managers is responsible in order to provide appropriate information about the financial

performance and growth rate of company to its various stakeholders that include

shareholders, government, investors, lenders, public, suppliers etc. Therefore, this type of

organization has to develop all kinds of statement such as income statement, balance

sheet and cash flow statement as per the international accounting standards.

11

Illustration 3: Balance sheet for partnership

acting as owner and manager of organization. In large organization, a team of top

managers is responsible in order to provide appropriate information about the financial

performance and growth rate of company to its various stakeholders that include

shareholders, government, investors, lenders, public, suppliers etc. Therefore, this type of

organization has to develop all kinds of statement such as income statement, balance

sheet and cash flow statement as per the international accounting standards.

11

Illustration 3: Balance sheet for partnership

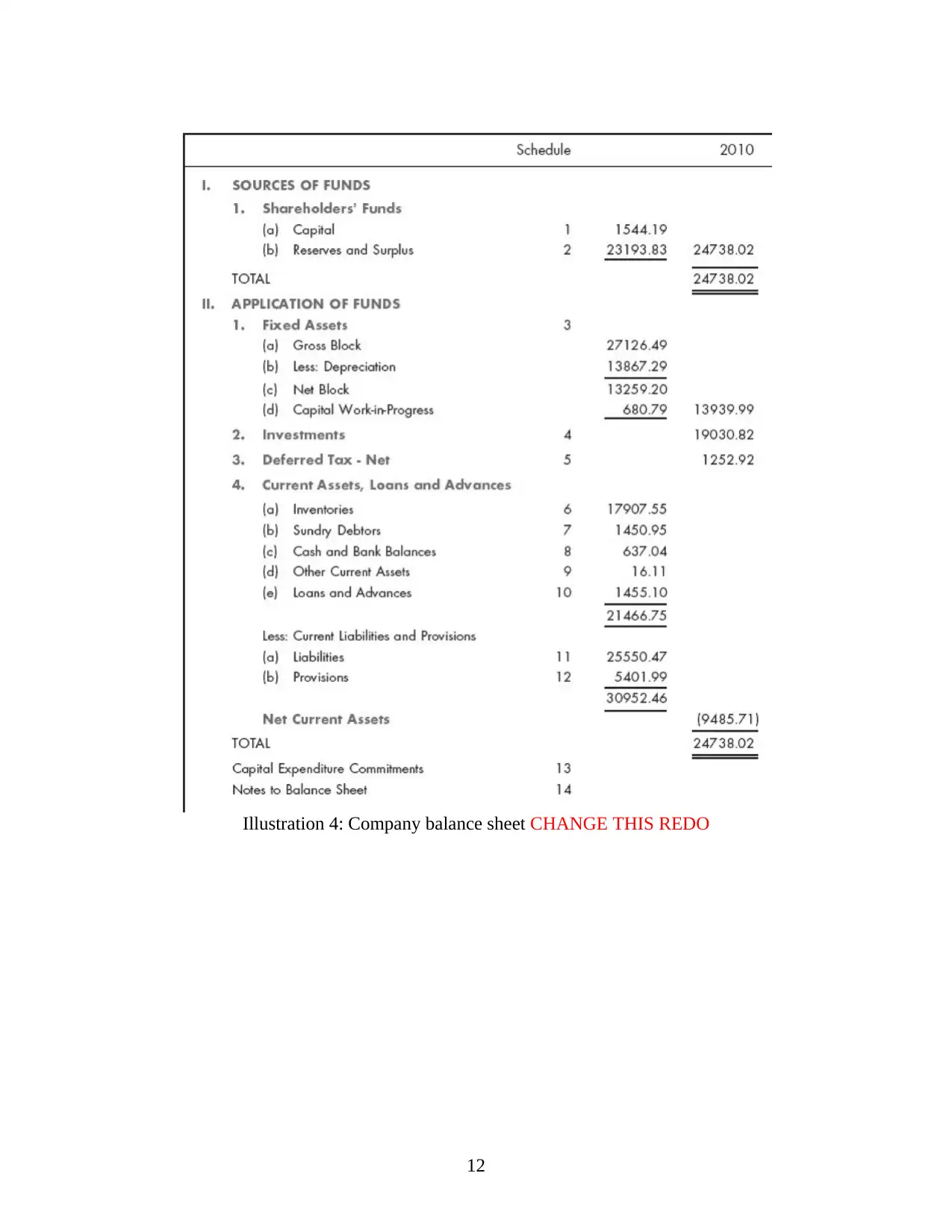

12

Illustration 4: Company balance sheet CHANGE THIS REDO

Illustration 4: Company balance sheet CHANGE THIS REDO

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.