Financial Resources and Decisions: Report and Analysis of Finance

VerifiedAdded on 2020/02/14

|17

|4697

|133

Report

AI Summary

This report delves into the critical aspects of managing financial resources and making informed financial decisions. It begins by exploring various sources of finance, including long-term options like share capital and retained earnings, as well as short to medium-term options such as hire purchase and bank loans. The report analyzes the legal, financial, and bankruptcy implications of each source, comparing their advantages and disadvantages to determine the most suitable options for a business enterprise. Furthermore, it examines the costs associated with different financing methods, like interest, dividends, and opportunity costs, and emphasizes the importance of financial planning, including cash budgeting and capital management. The report also identifies the key users of financial information, such as workers, customers, suppliers, shareholders, and regulatory authorities, and highlights how they utilize financial statements for decision-making. Finally, the report provides a comprehensive analysis of the financial ratios of Tesco Limited and their impact on decision making.

Managing Financial

Resources and Decisions

Resources and Decisions

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1...........................................................................................................................................1

1.2...........................................................................................................................................2

1.3...........................................................................................................................................3

TASK 2............................................................................................................................................4

2.1...........................................................................................................................................4

2.2...........................................................................................................................................4

2.3...........................................................................................................................................5

2.4...........................................................................................................................................6

TASK 3............................................................................................................................................6

3.1...........................................................................................................................................6

3.2...........................................................................................................................................8

3.3...........................................................................................................................................9

TASK 4..........................................................................................................................................11

4.1.........................................................................................................................................11

4.2.........................................................................................................................................12

4.3.........................................................................................................................................13

CONCLUSION .............................................................................................................................14

Index of Tables

Table 1: Operating budget...............................................................................................................7

Table 2: Calculation of unit cost.....................................................................................................8

Table 3: Calculation of NPV..........................................................................................................10

Table 4: Calculation of NPV..........................................................................................................10

Table 5: Calculation of IRR...........................................................................................................11

Table 6: Calculation of ratios of TESCO.......................................................................................13

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1...........................................................................................................................................1

1.2...........................................................................................................................................2

1.3...........................................................................................................................................3

TASK 2............................................................................................................................................4

2.1...........................................................................................................................................4

2.2...........................................................................................................................................4

2.3...........................................................................................................................................5

2.4...........................................................................................................................................6

TASK 3............................................................................................................................................6

3.1...........................................................................................................................................6

3.2...........................................................................................................................................8

3.3...........................................................................................................................................9

TASK 4..........................................................................................................................................11

4.1.........................................................................................................................................11

4.2.........................................................................................................................................12

4.3.........................................................................................................................................13

CONCLUSION .............................................................................................................................14

Index of Tables

Table 1: Operating budget...............................................................................................................7

Table 2: Calculation of unit cost.....................................................................................................8

Table 3: Calculation of NPV..........................................................................................................10

Table 4: Calculation of NPV..........................................................................................................10

Table 5: Calculation of IRR...........................................................................................................11

Table 6: Calculation of ratios of TESCO.......................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Finance is the major source or elements of an organization that aids in carrying out various

activities of a business organization. It is the backbone of every enterprise on which the business

function effectively. The present research report is designed to provide readers with a deep

understanding of varied sources of finance and their availability for the business. The aim of this

study is to create an insight on how and where to access distinct sources of finance and the

ability to utilize financial information for decision making. Furthermore, the report presents

advantages and disadvantages of various sources such as retained earnings, share capital, bank

loan and hire purchase and their suitability as well (Ojha, Gianiodis and Manuj, 2013). Likewise,

various ratios of Tesco limited has also been highlighted in this report that becomes the basis for

making various decisions by several users of it. Moreover, a budget has also been prepared and

the calculation of unit cost to provide readers and insight on the usefulness of it and how

decisions are taken based these data's.

TASK 1

1.1

Funds are required for various purposes and an entrepreneur needs funds to start-up a

new venture and carry on the operations of the same. In order to purchase various equipments,

leasing land, buying stocks, an owner opts for several sources of finance through which it can

avail money. In the present research report, the best sources of funds for the entrepreneur have

been highlighted below:

Long term sources: An entrepreneur may require high amount of funds to invest in

purchasing equipments, land and machinery. They can refund the amount of money in the either

5, 10, 20 or more years according to the terms and conditions of the respective source. Some of

them have been enlisted below: Share Capital: This is a method used to raise funds by selling the companies share to the

external members. The shareholders invest their money the respective company and for

this purpose they receive dividends at the end of the financial period (Nga and Yield,

2013). Retained earnings: This is the amount of funds that is earned by an organization in the

previous financial year. For instance, the entrepreneur has invested £100000 in purchase

1

Finance is the major source or elements of an organization that aids in carrying out various

activities of a business organization. It is the backbone of every enterprise on which the business

function effectively. The present research report is designed to provide readers with a deep

understanding of varied sources of finance and their availability for the business. The aim of this

study is to create an insight on how and where to access distinct sources of finance and the

ability to utilize financial information for decision making. Furthermore, the report presents

advantages and disadvantages of various sources such as retained earnings, share capital, bank

loan and hire purchase and their suitability as well (Ojha, Gianiodis and Manuj, 2013). Likewise,

various ratios of Tesco limited has also been highlighted in this report that becomes the basis for

making various decisions by several users of it. Moreover, a budget has also been prepared and

the calculation of unit cost to provide readers and insight on the usefulness of it and how

decisions are taken based these data's.

TASK 1

1.1

Funds are required for various purposes and an entrepreneur needs funds to start-up a

new venture and carry on the operations of the same. In order to purchase various equipments,

leasing land, buying stocks, an owner opts for several sources of finance through which it can

avail money. In the present research report, the best sources of funds for the entrepreneur have

been highlighted below:

Long term sources: An entrepreneur may require high amount of funds to invest in

purchasing equipments, land and machinery. They can refund the amount of money in the either

5, 10, 20 or more years according to the terms and conditions of the respective source. Some of

them have been enlisted below: Share Capital: This is a method used to raise funds by selling the companies share to the

external members. The shareholders invest their money the respective company and for

this purpose they receive dividends at the end of the financial period (Nga and Yield,

2013). Retained earnings: This is the amount of funds that is earned by an organization in the

previous financial year. For instance, the entrepreneur has invested £100000 in purchase

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

of inventory and the amount availed by him at the end of the period by sale of respective

goods can be invested again the business (Magni, 2010).

Short/ medium term sources: These are small amount of money required by an business

enterprise to meet its routine of daily expenses. Moreover, these can be used to purchase small

equipments of the organization. Furthermore, these are generally refundable in the period of 3 to

1 years. Hire purchase: The sad entrepreneur can purchase various assets for its company on the

basis of hire purchase. Herein, the owner gets possession of the goods or assets as soon as

he repays its last instalments (Kaplan and Atkinson, 2015).

Bank Loan: There are several banks in UK that provide loans to the entrepreneur and

pursue them to start up new businesses in regard with taking some documents as security.

The owner can refund the amount of money taken as loan along with the interest in the

prescribed time limit stated by the bank.

1.2

The above suggested different sources of finance have diverse effects on the functioning

of concerned business enterprise. There are several stages of a business entity and at that time

each source of finance has distinct implication and the same has been illustrated in this section:

Legal Implications:

In case of raising share capital, the owner needs to share its various rights with it various

shareholders. They has the power to make decisions in regard to the concerned company.

Moreover, a company cannot raise shares through public offering till it turns into a public

limited corporation (Jenkins, 2002).

The ownership of goods of assets does not transfer to the hire purchaser until and unless

all the instalments is paid to owner. Though he can use the machine in the prescribed

period. As discussed above a bank provides loan on the basis of certain documents or asset kept

as security. These can be seize anytime by the bank if the owner fails to pay respective

instalments.

Financial Implications:

2

goods can be invested again the business (Magni, 2010).

Short/ medium term sources: These are small amount of money required by an business

enterprise to meet its routine of daily expenses. Moreover, these can be used to purchase small

equipments of the organization. Furthermore, these are generally refundable in the period of 3 to

1 years. Hire purchase: The sad entrepreneur can purchase various assets for its company on the

basis of hire purchase. Herein, the owner gets possession of the goods or assets as soon as

he repays its last instalments (Kaplan and Atkinson, 2015).

Bank Loan: There are several banks in UK that provide loans to the entrepreneur and

pursue them to start up new businesses in regard with taking some documents as security.

The owner can refund the amount of money taken as loan along with the interest in the

prescribed time limit stated by the bank.

1.2

The above suggested different sources of finance have diverse effects on the functioning

of concerned business enterprise. There are several stages of a business entity and at that time

each source of finance has distinct implication and the same has been illustrated in this section:

Legal Implications:

In case of raising share capital, the owner needs to share its various rights with it various

shareholders. They has the power to make decisions in regard to the concerned company.

Moreover, a company cannot raise shares through public offering till it turns into a public

limited corporation (Jenkins, 2002).

The ownership of goods of assets does not transfer to the hire purchaser until and unless

all the instalments is paid to owner. Though he can use the machine in the prescribed

period. As discussed above a bank provides loan on the basis of certain documents or asset kept

as security. These can be seize anytime by the bank if the owner fails to pay respective

instalments.

Financial Implications:

2

Shareholders are part owners of a company and they have the right to share profits of the

company. Apart from it, the owner is not entitled to repay the amount of investment, they

only need to give dividends from the amount of profit made in the current period.

Regarding the hire purchase the owner needs to pay periodic instalments to the owner in

order to avail the full possession of the assets (Hildreth, 2004). The financial implication that governs bank loan is that the amount of amortization or

interest shall be paid timely by the owner.

Implication at times of dilution:

At the time of closure of said enterprise, the control that shareholders possesses in the

company gets diluted at the time of dilution.

If the owner repays all the instalments to the hirer then the possession of good remains

with is and vice versa if the full amount is not repaid (Helfert, 2004). In case of bank loan there is not any dilution of control.

Implication at Bankruptcy:

At times when the company is disclosed bankrupt, the shareholders are the least to avail

the amount of profit or remaining assets of the company.

At times of bankruptcy of owner, the possession of respective asset transfers to the initial

owner.

In case if the borrower is declared bankrupt, it must use its assets to repay the loan first

and thereafter it can address and refund various shareholders, creditors, etc.

There is as such no implications with regard to using retained earnings. It is owners property and

he can make the use of it as and when he wants.

1.3

For the current business enterprise, the above enlisted sources of finance are best for the

entrepreneur. But it is essential to evaluate and analyse one best source that can be adapted by

the owner. For this purpose, it is essential to assess various pros and cons of the same. In order to

avail long term finance, share capital is the best source of finance. It will enable the owner to

make investments by purchasing assets (Grieve, 2013). It is beneficial because the return on

investment in particular source is much higher than the other sources. Moreover, the cost of

implementation is quite low. Whereas, it is not intellectual to use all the retained earnings in the

business because it causes serious cash flow troubles thereby affecting the financial statements.

3

company. Apart from it, the owner is not entitled to repay the amount of investment, they

only need to give dividends from the amount of profit made in the current period.

Regarding the hire purchase the owner needs to pay periodic instalments to the owner in

order to avail the full possession of the assets (Hildreth, 2004). The financial implication that governs bank loan is that the amount of amortization or

interest shall be paid timely by the owner.

Implication at times of dilution:

At the time of closure of said enterprise, the control that shareholders possesses in the

company gets diluted at the time of dilution.

If the owner repays all the instalments to the hirer then the possession of good remains

with is and vice versa if the full amount is not repaid (Helfert, 2004). In case of bank loan there is not any dilution of control.

Implication at Bankruptcy:

At times when the company is disclosed bankrupt, the shareholders are the least to avail

the amount of profit or remaining assets of the company.

At times of bankruptcy of owner, the possession of respective asset transfers to the initial

owner.

In case if the borrower is declared bankrupt, it must use its assets to repay the loan first

and thereafter it can address and refund various shareholders, creditors, etc.

There is as such no implications with regard to using retained earnings. It is owners property and

he can make the use of it as and when he wants.

1.3

For the current business enterprise, the above enlisted sources of finance are best for the

entrepreneur. But it is essential to evaluate and analyse one best source that can be adapted by

the owner. For this purpose, it is essential to assess various pros and cons of the same. In order to

avail long term finance, share capital is the best source of finance. It will enable the owner to

make investments by purchasing assets (Grieve, 2013). It is beneficial because the return on

investment in particular source is much higher than the other sources. Moreover, the cost of

implementation is quite low. Whereas, it is not intellectual to use all the retained earnings in the

business because it causes serious cash flow troubles thereby affecting the financial statements.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Likewise, in regards with the short or medium term financing, the best out of two is hire

purchase if the owner needs to buy goods or assets urgently. It is easy to repay the amount of

money in instalments without any interest as in the case of Bank loan. Moreover, there is a high

amount of risk involved in taking loan and along with that at times there are high penalty fees

and number of limitations relating to it (Elearn, 2013). Additionally, too much of loan

undertaken to purchase assets affects the cash flow statement and repayment of borrowings can

even result in overtaking incomes. Thus the best sources of finance for said enterprise is share

capital and hire purchase.

TASK 2

2.1

In order to implement any of the above source of finance in the said business

organization, it is essential to analyse and evaluate the cost of it. There are several lenders who

provide a firm with the prescribed money and they charge interest for the same. This is the basic

element of cost that is charged in each of the source (Dayananda, 2002). The various prices that

comes along with the enlisted sources of finance are interest, dividends, opportunity cost.

When the owner of the said organization opts for raising funds from share capital, then it

has to surrender some amount of its profit to the shareholders in for of dividends. Moreover,

undertaking the following source requires money to register in the share market and promote its

company's share. Contrary if the owner prefers to reinvest its profit in the company, then it has to

lose alternative projects that can provide much more benefit than the retained earnings. This can

also be termed as opportunity cost.

Likewise, choosing to raise funds from bank loan, the entrepreneur needs to incur several

cost along with repaying interest and these are penalty fees, various taxes and large amount of

risk in keeping assets as security (Davis and McKevitt, 2013). Contrastingly, there is no physical

cost involved in purchasing equipments on hire purchase basis.

2.2

Financial plan of company is an outline of various activities that will enable the

entrepreneur to manage its funds effectively. It involves setting up of budgets, policies,

objectives to monitor its financial resources and manage them in the most efficient manner that

renders huge profits to the organization. Relevance of financial planning in context with the

current organization is enlisted below:

4

purchase if the owner needs to buy goods or assets urgently. It is easy to repay the amount of

money in instalments without any interest as in the case of Bank loan. Moreover, there is a high

amount of risk involved in taking loan and along with that at times there are high penalty fees

and number of limitations relating to it (Elearn, 2013). Additionally, too much of loan

undertaken to purchase assets affects the cash flow statement and repayment of borrowings can

even result in overtaking incomes. Thus the best sources of finance for said enterprise is share

capital and hire purchase.

TASK 2

2.1

In order to implement any of the above source of finance in the said business

organization, it is essential to analyse and evaluate the cost of it. There are several lenders who

provide a firm with the prescribed money and they charge interest for the same. This is the basic

element of cost that is charged in each of the source (Dayananda, 2002). The various prices that

comes along with the enlisted sources of finance are interest, dividends, opportunity cost.

When the owner of the said organization opts for raising funds from share capital, then it

has to surrender some amount of its profit to the shareholders in for of dividends. Moreover,

undertaking the following source requires money to register in the share market and promote its

company's share. Contrary if the owner prefers to reinvest its profit in the company, then it has to

lose alternative projects that can provide much more benefit than the retained earnings. This can

also be termed as opportunity cost.

Likewise, choosing to raise funds from bank loan, the entrepreneur needs to incur several

cost along with repaying interest and these are penalty fees, various taxes and large amount of

risk in keeping assets as security (Davis and McKevitt, 2013). Contrastingly, there is no physical

cost involved in purchasing equipments on hire purchase basis.

2.2

Financial plan of company is an outline of various activities that will enable the

entrepreneur to manage its funds effectively. It involves setting up of budgets, policies,

objectives to monitor its financial resources and manage them in the most efficient manner that

renders huge profits to the organization. Relevance of financial planning in context with the

current organization is enlisted below:

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cash Budgeting: It aids in managing the outflow of cash by undertaking several

measures such as tax planning, judicial spending thereby increasing the cash flow of the

company. Income: Planning assist in increasing the income of said concern by duly reducing the

amount in tax payments, ensuring optimum supply and demand of money. It also enables

the firm to increase its savings thereby leading to rise in profits (Cox and Fardon, 2005).

Capital: It also aids in building a strong capital base of the company that will enable the

entrepreneur to carry out investment decisions most efficiently.

Apart from the above enlisted points, there are several other uses of financial plan and its

imperativeness in the present organization. It also helps in evaluating the potential

opportunities and threats of the future and plan actions accordingly.

2.3

There are mainly three types of decisions that are required to be made by each and every

business enterprise. These constitutes of strategic, operational and managerial decisions. For this

purpose varied informations are needed in form of financial statement of the company, audit

report, etc. The various users of these information have been listed below: Workers: They require various information of the company in order to ascertain relative

changes in the price and compensation trends of the company (Brigham and Ehrhardt,

2013). Their salary and bonus depends upon the profit made by the said organisation on

the respective period. Customers and Suppliers: They are the external users of the information and review the

financial position of the said organization in order to make various decisions regarding

providing credit and purchasing products and services of the firm. Shareholders: These are the internal users of information and review these statements to

ascertain the amounts of dividend that can be availed by them. Moreover, their

investment decisions are based on these data's and further judgements to make alteration

in the current policies and procedures are made by them (Brigham 2001).

Regulatory authorities: These includes governments, tax consultants, auditors, etc. They

require various information of the company to ascertain the financial position of the

company and acknowledge that the current enterprise is capable of paying the amount or

not.

5

measures such as tax planning, judicial spending thereby increasing the cash flow of the

company. Income: Planning assist in increasing the income of said concern by duly reducing the

amount in tax payments, ensuring optimum supply and demand of money. It also enables

the firm to increase its savings thereby leading to rise in profits (Cox and Fardon, 2005).

Capital: It also aids in building a strong capital base of the company that will enable the

entrepreneur to carry out investment decisions most efficiently.

Apart from the above enlisted points, there are several other uses of financial plan and its

imperativeness in the present organization. It also helps in evaluating the potential

opportunities and threats of the future and plan actions accordingly.

2.3

There are mainly three types of decisions that are required to be made by each and every

business enterprise. These constitutes of strategic, operational and managerial decisions. For this

purpose varied informations are needed in form of financial statement of the company, audit

report, etc. The various users of these information have been listed below: Workers: They require various information of the company in order to ascertain relative

changes in the price and compensation trends of the company (Brigham and Ehrhardt,

2013). Their salary and bonus depends upon the profit made by the said organisation on

the respective period. Customers and Suppliers: They are the external users of the information and review the

financial position of the said organization in order to make various decisions regarding

providing credit and purchasing products and services of the firm. Shareholders: These are the internal users of information and review these statements to

ascertain the amounts of dividend that can be availed by them. Moreover, their

investment decisions are based on these data's and further judgements to make alteration

in the current policies and procedures are made by them (Brigham 2001).

Regulatory authorities: These includes governments, tax consultants, auditors, etc. They

require various information of the company to ascertain the financial position of the

company and acknowledge that the current enterprise is capable of paying the amount or

not.

5

2.4

Each companies carries out several transactions in a day and the same has consequent

impact on the financial statements of the firm. Further, it becomes the basis of decision making

of firm and its investors (Bose, 2006). The ways in which finance affects the financial statements

of the concerned business enterprise have been enlisted below:

From the above enlisted sources of finance, share capital affects the balance sheet as it is

shown in the liability side which demonstrates that the same amount is to be repaid back to the

shareholders in terms of dividends. Likewise, it has a consequent impact in the profit and loss

account as the dividend paid to the shareholders is shown in the indirect expenses of the firm.

Similarly, is the entrepreneur uses its existing profits in the company the capital of the firm will

increase thereby affecting the balance sheet and the cash statesmen will show a negative balance

as the profit is being used again. Moreover, the cash will also increase (Bennouna, Meredith and

Marchant, 2010).

Contrary in the case of Bank loan, the amount of loan shall be highlighted in the balance

sheet on the liability side and the amount of interest and various expenses availed in taking it

shall be shown in the profit and loss account in the head indirect expenditure. The cash flow also

has a consequent impact as the loan taken brings in the amount of money in the company.

Whereas in the case of hire purchase, the assets of the firm will increase thereby duly reducing

the amount of cash that has been incurred in repaying the instalment money (Baker and Powell,

2009).

TASK 3

3.1

Budget is that quantitative statement which prepares in present in order to forecast its

future as it is uncertain which can only predict (Bose, 2006). It is quantitative expression of a

programme which is designed by the owner for a specific period. It is also regarded as “first aid”

box for an organisation in accidental business situations. It will carry all the tools such as

planning of sales and revenue, monitoring of costs and expenses, increasing assets and

decreasing its liabilities by enhancing the cash flows in an enterprise.

The basic aim behind preparation of this kind of budget is to alert the business owner to

deal with the upcoming difficulties by strengthening its existing financial capabilities (Brigham

6

Each companies carries out several transactions in a day and the same has consequent

impact on the financial statements of the firm. Further, it becomes the basis of decision making

of firm and its investors (Bose, 2006). The ways in which finance affects the financial statements

of the concerned business enterprise have been enlisted below:

From the above enlisted sources of finance, share capital affects the balance sheet as it is

shown in the liability side which demonstrates that the same amount is to be repaid back to the

shareholders in terms of dividends. Likewise, it has a consequent impact in the profit and loss

account as the dividend paid to the shareholders is shown in the indirect expenses of the firm.

Similarly, is the entrepreneur uses its existing profits in the company the capital of the firm will

increase thereby affecting the balance sheet and the cash statesmen will show a negative balance

as the profit is being used again. Moreover, the cash will also increase (Bennouna, Meredith and

Marchant, 2010).

Contrary in the case of Bank loan, the amount of loan shall be highlighted in the balance

sheet on the liability side and the amount of interest and various expenses availed in taking it

shall be shown in the profit and loss account in the head indirect expenditure. The cash flow also

has a consequent impact as the loan taken brings in the amount of money in the company.

Whereas in the case of hire purchase, the assets of the firm will increase thereby duly reducing

the amount of cash that has been incurred in repaying the instalment money (Baker and Powell,

2009).

TASK 3

3.1

Budget is that quantitative statement which prepares in present in order to forecast its

future as it is uncertain which can only predict (Bose, 2006). It is quantitative expression of a

programme which is designed by the owner for a specific period. It is also regarded as “first aid”

box for an organisation in accidental business situations. It will carry all the tools such as

planning of sales and revenue, monitoring of costs and expenses, increasing assets and

decreasing its liabilities by enhancing the cash flows in an enterprise.

The basic aim behind preparation of this kind of budget is to alert the business owner to

deal with the upcoming difficulties by strengthening its existing financial capabilities (Brigham

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

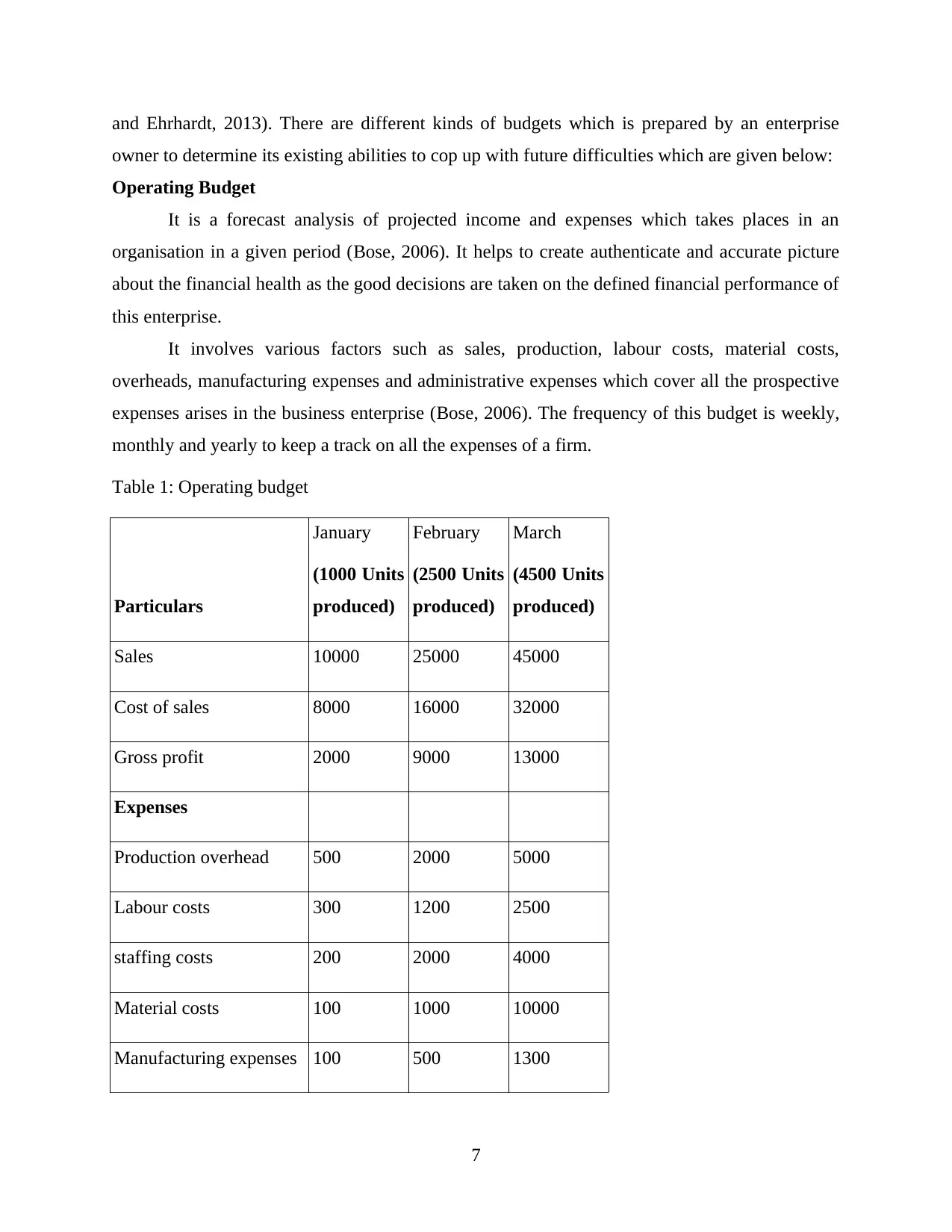

and Ehrhardt, 2013). There are different kinds of budgets which is prepared by an enterprise

owner to determine its existing abilities to cop up with future difficulties which are given below:

Operating Budget

It is a forecast analysis of projected income and expenses which takes places in an

organisation in a given period (Bose, 2006). It helps to create authenticate and accurate picture

about the financial health as the good decisions are taken on the defined financial performance of

this enterprise.

It involves various factors such as sales, production, labour costs, material costs,

overheads, manufacturing expenses and administrative expenses which cover all the prospective

expenses arises in the business enterprise (Bose, 2006). The frequency of this budget is weekly,

monthly and yearly to keep a track on all the expenses of a firm.

Table 1: Operating budget

Particulars

January

(1000 Units

produced)

February

(2500 Units

produced)

March

(4500 Units

produced)

Sales 10000 25000 45000

Cost of sales 8000 16000 32000

Gross profit 2000 9000 13000

Expenses

Production overhead 500 2000 5000

Labour costs 300 1200 2500

staffing costs 200 2000 4000

Material costs 100 1000 10000

Manufacturing expenses 100 500 1300

7

owner to determine its existing abilities to cop up with future difficulties which are given below:

Operating Budget

It is a forecast analysis of projected income and expenses which takes places in an

organisation in a given period (Bose, 2006). It helps to create authenticate and accurate picture

about the financial health as the good decisions are taken on the defined financial performance of

this enterprise.

It involves various factors such as sales, production, labour costs, material costs,

overheads, manufacturing expenses and administrative expenses which cover all the prospective

expenses arises in the business enterprise (Bose, 2006). The frequency of this budget is weekly,

monthly and yearly to keep a track on all the expenses of a firm.

Table 1: Operating budget

Particulars

January

(1000 Units

produced)

February

(2500 Units

produced)

March

(4500 Units

produced)

Sales 10000 25000 45000

Cost of sales 8000 16000 32000

Gross profit 2000 9000 13000

Expenses

Production overhead 500 2000 5000

Labour costs 300 1200 2500

staffing costs 200 2000 4000

Material costs 100 1000 10000

Manufacturing expenses 100 500 1300

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Administrative expenses 1000 1000 1000

Total 2200 7700 23800

Variance -200 1300 -10800

Interpretations

The above operating budget of an enterprise is prepared for three months which covers all

the expenses and sales generated by the organisations.

Sales generated in January is 10000 which is increases in February is 25000 and later on

45000 as the production unit is showing increasing trend from 1000 units then 1500 units

and lastly at 2000 units in March.

Expenses are also increasing from one period to another in proportion to the sales

generated by an enterprise in a given month.

It has observed from this budget that only in February month this enterprise generated

positive results otherwise in starting month and last month there are negative results.

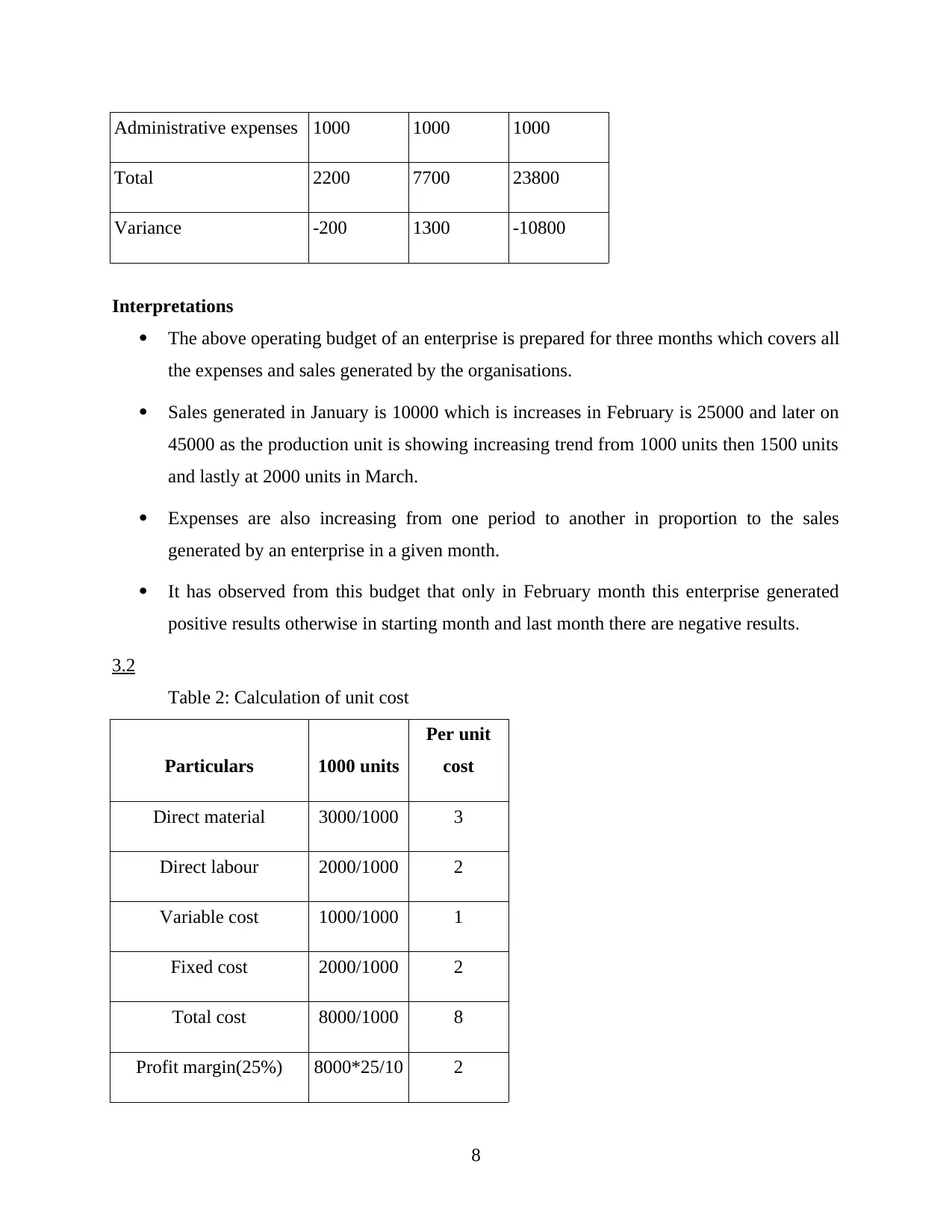

3.2

Table 2: Calculation of unit cost

Particulars 1000 units

Per unit

cost

Direct material 3000/1000 3

Direct labour 2000/1000 2

Variable cost 1000/1000 1

Fixed cost 2000/1000 2

Total cost 8000/1000 8

Profit margin(25%) 8000*25/10 2

8

Total 2200 7700 23800

Variance -200 1300 -10800

Interpretations

The above operating budget of an enterprise is prepared for three months which covers all

the expenses and sales generated by the organisations.

Sales generated in January is 10000 which is increases in February is 25000 and later on

45000 as the production unit is showing increasing trend from 1000 units then 1500 units

and lastly at 2000 units in March.

Expenses are also increasing from one period to another in proportion to the sales

generated by an enterprise in a given month.

It has observed from this budget that only in February month this enterprise generated

positive results otherwise in starting month and last month there are negative results.

3.2

Table 2: Calculation of unit cost

Particulars 1000 units

Per unit

cost

Direct material 3000/1000 3

Direct labour 2000/1000 2

Variable cost 1000/1000 1

Fixed cost 2000/1000 2

Total cost 8000/1000 8

Profit margin(25%) 8000*25/10 2

8

0

Selling price 10

Pricing techniques

It has been observed that in the above cost plus pricing technique has been utilised in

order to determine the selling price of an enterprise.

Cost plus pricing technique is that technique which is useful for an enterprise as it will cover all

the costs involved in the business should be taken into considerations (Brigham, 2001). It can be

seen from the above mentioned calculation in which the owner has determined the specific

amount of profit percentage in the price of the products to compensate the costs incurred in its

business with the higher generation of the sales and the revenue.

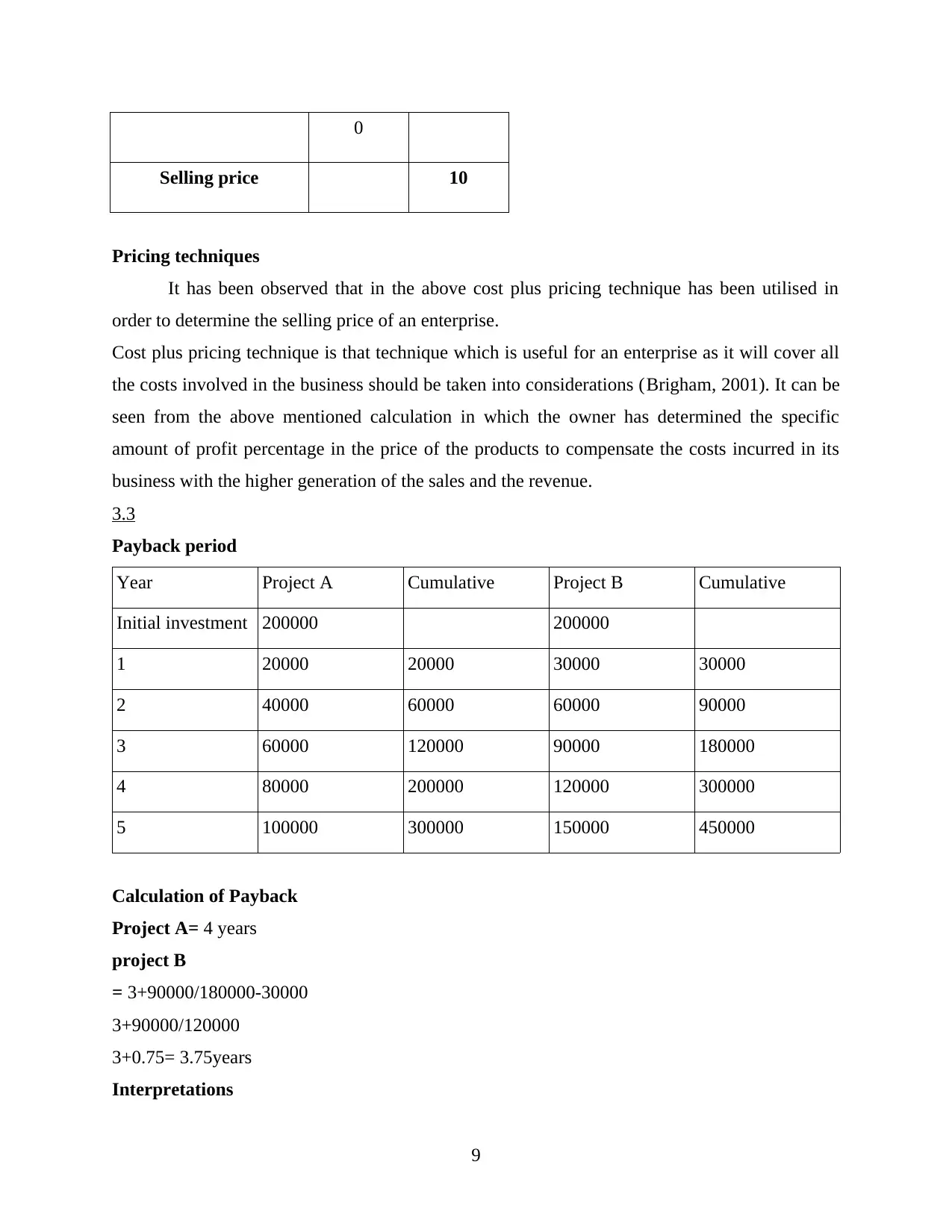

3.3

Payback period

Year Project A Cumulative Project B Cumulative

Initial investment 200000 200000

1 20000 20000 30000 30000

2 40000 60000 60000 90000

3 60000 120000 90000 180000

4 80000 200000 120000 300000

5 100000 300000 150000 450000

Calculation of Payback

Project A= 4 years

project B

= 3+90000/180000-30000

3+90000/120000

3+0.75= 3.75years

Interpretations

9

Selling price 10

Pricing techniques

It has been observed that in the above cost plus pricing technique has been utilised in

order to determine the selling price of an enterprise.

Cost plus pricing technique is that technique which is useful for an enterprise as it will cover all

the costs involved in the business should be taken into considerations (Brigham, 2001). It can be

seen from the above mentioned calculation in which the owner has determined the specific

amount of profit percentage in the price of the products to compensate the costs incurred in its

business with the higher generation of the sales and the revenue.

3.3

Payback period

Year Project A Cumulative Project B Cumulative

Initial investment 200000 200000

1 20000 20000 30000 30000

2 40000 60000 60000 90000

3 60000 120000 90000 180000

4 80000 200000 120000 300000

5 100000 300000 150000 450000

Calculation of Payback

Project A= 4 years

project B

= 3+90000/180000-30000

3+90000/120000

3+0.75= 3.75years

Interpretations

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.