Managing Financial Resources: Budgeting and Performance

VerifiedAdded on 2023/06/15

|10

|2633

|367

Report

AI Summary

This report provides a comprehensive overview of managing financial resources, covering key aspects such as fixed and variable cost computation, money raising calculations, variance analysis (including adverse and favorable variances), flexible and static budgets, and performance metrics. It explains concepts like Average Daily Rate (ADR), Revenue per Available Room (RevPAR), Average Length of Stay, Market Penetration Index, and Customer Satisfaction, illustrating their importance in evaluating business performance. The report uses examples to clarify theoretical concepts, demonstrating how these tools and metrics are applied in real-world scenarios to assess profitability, efficiency, and market penetration. Desklib offers a platform to explore similar solved assignments and study resources for students.

MANAGING FINANCIAL

RESOURCES

RESOURCES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

SECTION-A....................................................................................................................................3

Question 2....................................................................................................................................3

SECTION-B....................................................................................................................................4

Question 4....................................................................................................................................4

Question 5....................................................................................................................................6

REFERENCES................................................................................................................................1

SECTION-A....................................................................................................................................3

Question 2....................................................................................................................................3

SECTION-B....................................................................................................................................4

Question 4....................................................................................................................................4

Question 5....................................................................................................................................6

REFERENCES................................................................................................................................1

SECTION-A

Question 2

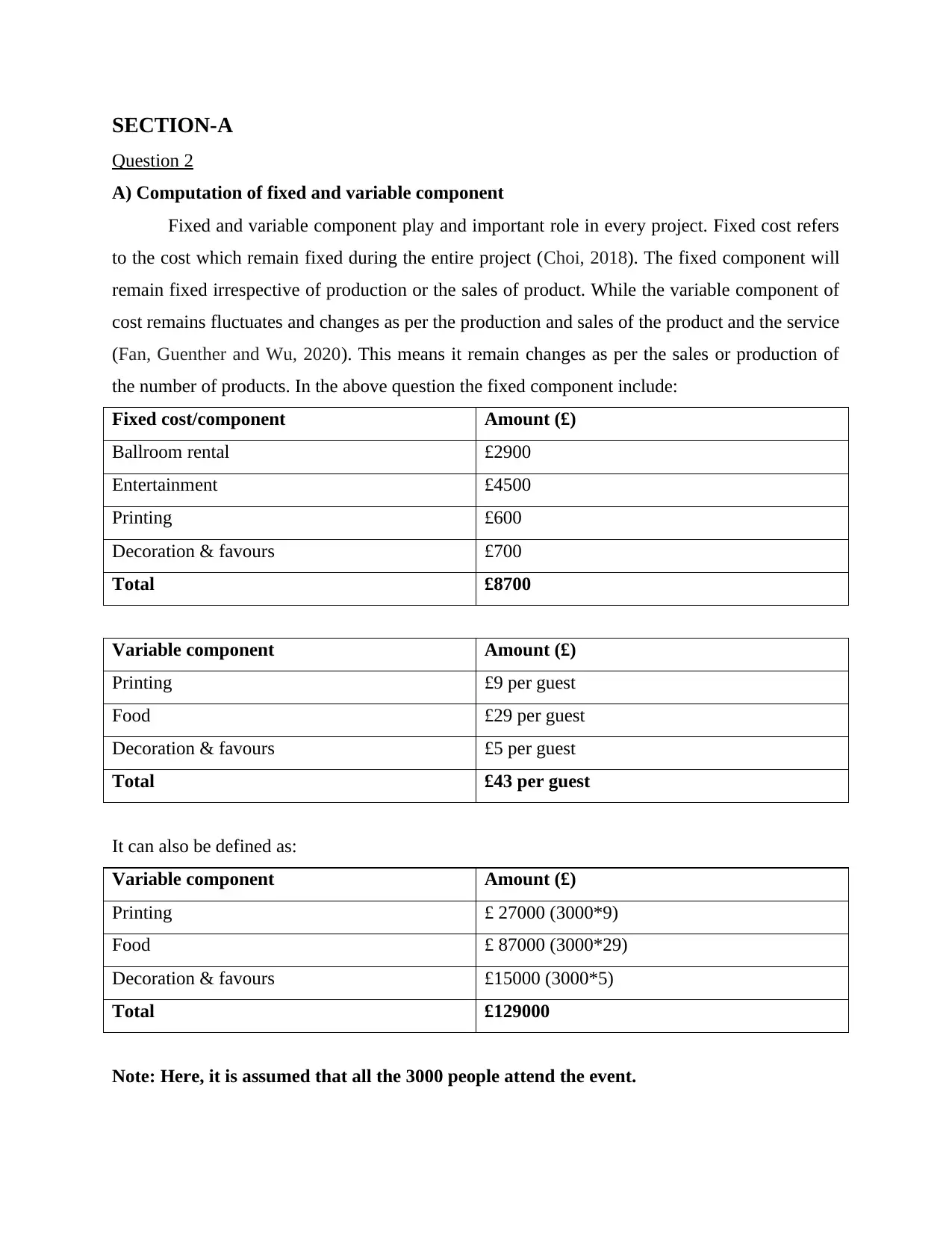

A) Computation of fixed and variable component

Fixed and variable component play and important role in every project. Fixed cost refers

to the cost which remain fixed during the entire project (Choi, 2018). The fixed component will

remain fixed irrespective of production or the sales of product. While the variable component of

cost remains fluctuates and changes as per the production and sales of the product and the service

(Fan, Guenther and Wu, 2020). This means it remain changes as per the sales or production of

the number of products. In the above question the fixed component include:

Fixed cost/component Amount (£)

Ballroom rental £2900

Entertainment £4500

Printing £600

Decoration & favours £700

Total £8700

Variable component Amount (£)

Printing £9 per guest

Food £29 per guest

Decoration & favours £5 per guest

Total £43 per guest

It can also be defined as:

Variable component Amount (£)

Printing £ 27000 (3000*9)

Food £ 87000 (3000*29)

Decoration & favours £15000 (3000*5)

Total £129000

Note: Here, it is assumed that all the 3000 people attend the event.

Question 2

A) Computation of fixed and variable component

Fixed and variable component play and important role in every project. Fixed cost refers

to the cost which remain fixed during the entire project (Choi, 2018). The fixed component will

remain fixed irrespective of production or the sales of product. While the variable component of

cost remains fluctuates and changes as per the production and sales of the product and the service

(Fan, Guenther and Wu, 2020). This means it remain changes as per the sales or production of

the number of products. In the above question the fixed component include:

Fixed cost/component Amount (£)

Ballroom rental £2900

Entertainment £4500

Printing £600

Decoration & favours £700

Total £8700

Variable component Amount (£)

Printing £9 per guest

Food £29 per guest

Decoration & favours £5 per guest

Total £43 per guest

It can also be defined as:

Variable component Amount (£)

Printing £ 27000 (3000*9)

Food £ 87000 (3000*29)

Decoration & favours £15000 (3000*5)

Total £129000

Note: Here, it is assumed that all the 3000 people attend the event.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

b) Calculation of money raised

The money which can be raised from the event would be calculated as:

Sales £300000 (3000*100)

Less:

Fixed cost £8700

Variable cost £129000

Profit £162300

In order to identify the calculation of money that would be raised from the event, the sales

which would be made from the event would be counted as overall revenue from which both the

fixed and variable cost will be deducted. This will give the profit or the exact amount of money

that will be raised from the event.

As per the above calculation it would be right to said that the conduction of the event would

raise the money in because while making a deduction of all the fixed and variable component of

cost the event still earn money i.e. £162300 which shows the success of the event along with its

profitability. As under the given case it was assumed that the all the expected 3000 people would

make a participation in the event which make the variable cost to be £129000 and as fixed cost

i.e. £8700 will remain fixed instead of the fact that how many number of people would attend the

event. And as the charge per person is £100 which is multiplied by number of participants that

gives £300000 amount of revenue. Lastly, after making a deduction of all the cost the net amount

that would be raised from the event would be identified i.e. £162300.

SECTION-B

Question 4

2. Variance analysis

It refers to the analysis under which variances can be identified i.e. with the help of

variance analysis the deviation between the actual performance and the planned and forecasted

performance can be identified and analysed (Batur, Wang and Choobineh, 2018). This will assist

in raising the efficiency of production in terms of taking of corrective actions as per the

deviation. This can be understood with an example that: suppose a company ABC makes sales

The money which can be raised from the event would be calculated as:

Sales £300000 (3000*100)

Less:

Fixed cost £8700

Variable cost £129000

Profit £162300

In order to identify the calculation of money that would be raised from the event, the sales

which would be made from the event would be counted as overall revenue from which both the

fixed and variable cost will be deducted. This will give the profit or the exact amount of money

that will be raised from the event.

As per the above calculation it would be right to said that the conduction of the event would

raise the money in because while making a deduction of all the fixed and variable component of

cost the event still earn money i.e. £162300 which shows the success of the event along with its

profitability. As under the given case it was assumed that the all the expected 3000 people would

make a participation in the event which make the variable cost to be £129000 and as fixed cost

i.e. £8700 will remain fixed instead of the fact that how many number of people would attend the

event. And as the charge per person is £100 which is multiplied by number of participants that

gives £300000 amount of revenue. Lastly, after making a deduction of all the cost the net amount

that would be raised from the event would be identified i.e. £162300.

SECTION-B

Question 4

2. Variance analysis

It refers to the analysis under which variances can be identified i.e. with the help of

variance analysis the deviation between the actual performance and the planned and forecasted

performance can be identified and analysed (Batur, Wang and Choobineh, 2018). This will assist

in raising the efficiency of production in terms of taking of corrective actions as per the

deviation. This can be understood with an example that: suppose a company ABC makes sales

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

forecasting of £2000 at the yearend 2021. Later when it will be compared with the actual sales of

the company and found that the actual sales were £1800. This shows the variance analysis under

which a variation of £200 was found. This will assist the company in terms of raising the

efficiency in terms of raising efforts and cover deviation.

3. Adverse variance

It is a type of variance which occur and noticed when the actual sales are less than

budgeted sales or the actual expenses is more than budgeted expenses. This means when the

actual outcome is less than the projected and forecasted outcome then it will be termed as

adverse variance. This is bad for the organization because with the occurrence of adverse

variances the company would be affected negatively in terms of its decline in sales and raising of

expenses. This can also be understood with an example that suppose the company ABC make an

estimation of expenses of £1500 till the end of year 2021. And when it was compared with the

actual expenses it was found that the expenses were £2000. This shows that the adverse expenses

under which the actual expenses were more than estimated.

4. Favourable variance

It is just opposite of adverse variance in which the actual expenses were usually lower

than forecasted expenses and the actual income would be higher than the forecasted income

(Odu, 2019). This is considered as good for the business because with the grabbing of favourable

variances the organization can achieve success or it would be right to said that it reflect the

success of the business. This can be explained with an example i.e. suppose a company ABC

projected the income of £2000 and expenses as £1500 for the year end 2021. When it compared

with the actual income it was found that the actual income earned was £2500 and actual expenses

was £1200. This is termed as favourable variance because here the actual income is higher than

the estimated and actual expenses were less than estimated expenses.

5. Flexible budget

It refers to the budget under which the cost associated with the budget get fluctuate and

changes as per the change occurred in the cost. This budget adjusts the activity or volume level

of the company. It reflects accurate state of finance (Mouter, 2021). As per the occurrence of

the company and found that the actual sales were £1800. This shows the variance analysis under

which a variation of £200 was found. This will assist the company in terms of raising the

efficiency in terms of raising efforts and cover deviation.

3. Adverse variance

It is a type of variance which occur and noticed when the actual sales are less than

budgeted sales or the actual expenses is more than budgeted expenses. This means when the

actual outcome is less than the projected and forecasted outcome then it will be termed as

adverse variance. This is bad for the organization because with the occurrence of adverse

variances the company would be affected negatively in terms of its decline in sales and raising of

expenses. This can also be understood with an example that suppose the company ABC make an

estimation of expenses of £1500 till the end of year 2021. And when it was compared with the

actual expenses it was found that the expenses were £2000. This shows that the adverse expenses

under which the actual expenses were more than estimated.

4. Favourable variance

It is just opposite of adverse variance in which the actual expenses were usually lower

than forecasted expenses and the actual income would be higher than the forecasted income

(Odu, 2019). This is considered as good for the business because with the grabbing of favourable

variances the organization can achieve success or it would be right to said that it reflect the

success of the business. This can be explained with an example i.e. suppose a company ABC

projected the income of £2000 and expenses as £1500 for the year end 2021. When it compared

with the actual income it was found that the actual income earned was £2500 and actual expenses

was £1200. This is termed as favourable variance because here the actual income is higher than

the estimated and actual expenses were less than estimated expenses.

5. Flexible budget

It refers to the budget under which the cost associated with the budget get fluctuate and

changes as per the change occurred in the cost. This budget adjusts the activity or volume level

of the company. It reflects accurate state of finance (Mouter, 2021). As per the occurrence of

variation in the production and sales the flexible budget also varies. With the use of this budget

better opportunities can be grabbed by the business. In the same way it reflects more accuracy in

terms of finance. On the other hand, it is time consuming and more attention and maintenance.

For example: Suppose the company XYZ has a budget of £10 million of revenue and the cost of

goods sold was £4 million. Under £4 million of COGS £1 million is fixed while the remaining £3

million is flexible. This shows that the variable portion of COGS is 305 of revenue. When the

budgeted period is completed it was found that the actual sales were £9 million. Here as per

flexible budget, the £1 million will remain fixed while the variable cost would become £2.7

million. This shows that the resulted COGS would be £3.7 million with respect to the sales of £9

million of sales.

6. Static budget

It is a type of budget under which anticipated value related with input and output would be

conceived before the period begin. The results of static budget are usually different from the

actual figures. Under this budget the fixed amount related with sales, revenue and expenses

would be identified (Azizi, Kveton and Ghavamzadeh, 2021). As per the stated budget the

company make distribution and imply its resources. The use of this budget is easy and it does not

require any kind of modification as per the changing situation and occurrence of fluctuations.

However, it lack the aspect of flexibility which affect the efficiency of the budget. This can be

understood with an example that if the company ABC make an estimation of marketing

campaign as £15000 for the year 2021. Now it is depended up to the managers that how they

make compliance with the budgeted expenses and make the performance of their operation.

Question 5

1. Average daily Rate (ADR)

The average daily rate measures the average rental revenue that can be earned with

respect to occupying of room per day. With the use of ADR the operating performance in respect

to hotel can be identified and determined. The rising ADR reflect the positive performance of the

hotel. This means if the ADR of the hotel raise then it shows that the revenue and performance of

the hotel also enhance.

better opportunities can be grabbed by the business. In the same way it reflects more accuracy in

terms of finance. On the other hand, it is time consuming and more attention and maintenance.

For example: Suppose the company XYZ has a budget of £10 million of revenue and the cost of

goods sold was £4 million. Under £4 million of COGS £1 million is fixed while the remaining £3

million is flexible. This shows that the variable portion of COGS is 305 of revenue. When the

budgeted period is completed it was found that the actual sales were £9 million. Here as per

flexible budget, the £1 million will remain fixed while the variable cost would become £2.7

million. This shows that the resulted COGS would be £3.7 million with respect to the sales of £9

million of sales.

6. Static budget

It is a type of budget under which anticipated value related with input and output would be

conceived before the period begin. The results of static budget are usually different from the

actual figures. Under this budget the fixed amount related with sales, revenue and expenses

would be identified (Azizi, Kveton and Ghavamzadeh, 2021). As per the stated budget the

company make distribution and imply its resources. The use of this budget is easy and it does not

require any kind of modification as per the changing situation and occurrence of fluctuations.

However, it lack the aspect of flexibility which affect the efficiency of the budget. This can be

understood with an example that if the company ABC make an estimation of marketing

campaign as £15000 for the year 2021. Now it is depended up to the managers that how they

make compliance with the budgeted expenses and make the performance of their operation.

Question 5

1. Average daily Rate (ADR)

The average daily rate measures the average rental revenue that can be earned with

respect to occupying of room per day. With the use of ADR the operating performance in respect

to hotel can be identified and determined. The rising ADR reflect the positive performance of the

hotel. This means if the ADR of the hotel raise then it shows that the revenue and performance of

the hotel also enhance.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It can be calculated from formula i.e. average revenue earned from rooms that will be

divided by number of room sold. Under this the complementary rooms allotted to hotel staff

would be excluded.

For example, the suppose the hotel has a total of £100000 revenue and the number of rooms

is 500. Then ADR would be equal to £200 per room.

2. Revenue per available room

It is one of the important performance measure that is used in hospitality industry. it can be

calculated by multiplying the hotel average daily room rate with the occupancy rate

(Chattopadhyay and Mitra, 2019). With the use of RevPAR, the hotels can make measurement of

overall success of their hotel. As there will be of no use to run the business until the adequate

revenue would not be earned. Thus, with the use of RevPAR the success of the business would

be analysed in terms of generation of revenue by the business.

Its formula is room revenue divided with room available.

It can be explained with an example i.e. if the ADR of the hotel is £100 per room and the

occupancy rate is 80% then the RevPAR would be £80.

3. Average length of stay

It is usually used in hospital under other related industry. It can be defined as the average

number of days the patient diagnosed with the same disease and falling under the same category

lies in the hospital bed. It is an indicator through which the efficiency would be measured i.e.

with an assumption that all other things would be constant, shorter the stay will reduce the cost

of discharge of patient along with shift care. In short, it measures the number of days the patient

stays in the hospital.

It can be calculated with a formula i.e. dividing the sum of inpatient days with the

number of patient admitted with the same diagnosis.

For example: there are four patient named as John, Maria, Joseph and David admitted in

hospital. John was admitted on 01/01/2022 and discharged on 05/01/2022. Maria was admitted

on 04/01/2022 and discharged on 07/01/2022. Joseph was admitted on 10/01/2022 and

discharged on 13/01/2022 and David was admitted on 02/01/2022 and discharged on 06/01/2022.

With this information the average length of stay would be calculated as:

divided by number of room sold. Under this the complementary rooms allotted to hotel staff

would be excluded.

For example, the suppose the hotel has a total of £100000 revenue and the number of rooms

is 500. Then ADR would be equal to £200 per room.

2. Revenue per available room

It is one of the important performance measure that is used in hospitality industry. it can be

calculated by multiplying the hotel average daily room rate with the occupancy rate

(Chattopadhyay and Mitra, 2019). With the use of RevPAR, the hotels can make measurement of

overall success of their hotel. As there will be of no use to run the business until the adequate

revenue would not be earned. Thus, with the use of RevPAR the success of the business would

be analysed in terms of generation of revenue by the business.

Its formula is room revenue divided with room available.

It can be explained with an example i.e. if the ADR of the hotel is £100 per room and the

occupancy rate is 80% then the RevPAR would be £80.

3. Average length of stay

It is usually used in hospital under other related industry. It can be defined as the average

number of days the patient diagnosed with the same disease and falling under the same category

lies in the hospital bed. It is an indicator through which the efficiency would be measured i.e.

with an assumption that all other things would be constant, shorter the stay will reduce the cost

of discharge of patient along with shift care. In short, it measures the number of days the patient

stays in the hospital.

It can be calculated with a formula i.e. dividing the sum of inpatient days with the

number of patient admitted with the same diagnosis.

For example: there are four patient named as John, Maria, Joseph and David admitted in

hospital. John was admitted on 01/01/2022 and discharged on 05/01/2022. Maria was admitted

on 04/01/2022 and discharged on 07/01/2022. Joseph was admitted on 10/01/2022 and

discharged on 13/01/2022 and David was admitted on 02/01/2022 and discharged on 06/01/2022.

With this information the average length of stay would be calculated as:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Number of patient: 4

Number of days John admitted: 5 days

Maria admitted: 4 days

Joseph admitted: 4 days

David admitted: 5 days

Thus, average length of stay would be: 5+4+4+5/4

= 4.5 days.

6. Market penetration index

It refers to an index which measures the penetration of hotel in the market. with the use of

Market penetration index the occupancy of the hotel in the market in comparison of the

competitors would be measured (Viktorov, 2020). It shows the performance of the hotel in the

market with the comparison of the competitors. This is an important factor for every business

because if the organization with the use of its products and services is not able to capture the

market share or penetrate in the market then it will not be able to sustain in the market and the

competition of the market. Thus making an analysis of market penetration by the business is

highly important.

It can be calculated as current sales volume of the product or service that will be divided

by the total sales volume of similar products, including those which are sold by the competitors.

And if the result is multiplied by 100 then the percentage will be grabbed.

This can be explained with an example i.e. if there are 200 million of household present

in the market and out of them 10 million is of home automation device then the market

penetration would be equal to 5%.

7. Customer satisfaction

It can be defined as the measurement which shows that how happy the customers are with

respect to the use of company’s product and services and capabilities. With the use of this

measure the company can make improvement in the existing product and services so that the

customer satisfaction would be raised and enhanced (Budur and Poturak, 2021). It has a major

role in the company’s sales and revenue generation. This is an important component in respect to

every business because if the customers of any business are not satisfied with the products and

Number of days John admitted: 5 days

Maria admitted: 4 days

Joseph admitted: 4 days

David admitted: 5 days

Thus, average length of stay would be: 5+4+4+5/4

= 4.5 days.

6. Market penetration index

It refers to an index which measures the penetration of hotel in the market. with the use of

Market penetration index the occupancy of the hotel in the market in comparison of the

competitors would be measured (Viktorov, 2020). It shows the performance of the hotel in the

market with the comparison of the competitors. This is an important factor for every business

because if the organization with the use of its products and services is not able to capture the

market share or penetrate in the market then it will not be able to sustain in the market and the

competition of the market. Thus making an analysis of market penetration by the business is

highly important.

It can be calculated as current sales volume of the product or service that will be divided

by the total sales volume of similar products, including those which are sold by the competitors.

And if the result is multiplied by 100 then the percentage will be grabbed.

This can be explained with an example i.e. if there are 200 million of household present

in the market and out of them 10 million is of home automation device then the market

penetration would be equal to 5%.

7. Customer satisfaction

It can be defined as the measurement which shows that how happy the customers are with

respect to the use of company’s product and services and capabilities. With the use of this

measure the company can make improvement in the existing product and services so that the

customer satisfaction would be raised and enhanced (Budur and Poturak, 2021). It has a major

role in the company’s sales and revenue generation. This is an important component in respect to

every business because if the customers of any business are not satisfied with the products and

services of the business then it will lead to have a direct and negative impact towards the

business.

This can be determined as total number of 4 and 5 responses divided with number of total

responses*100. With the use of this method the customer satisfaction can be measured.

The best evidence and example with regard to the measurement of customer satisfaction

is related with the reviews and feedback received from customer in respect to the company’s

product. in the same way the satisfaction can be measured with the comparison of actual sales

with the past sales data of the company that truly reflect the customer satisfaction i.e. inclining

sales trend of the business.

business.

This can be determined as total number of 4 and 5 responses divided with number of total

responses*100. With the use of this method the customer satisfaction can be measured.

The best evidence and example with regard to the measurement of customer satisfaction

is related with the reviews and feedback received from customer in respect to the company’s

product. in the same way the satisfaction can be measured with the comparison of actual sales

with the past sales data of the company that truly reflect the customer satisfaction i.e. inclining

sales trend of the business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and journals

Azizi, M., Kveton, B. and Ghavamzadeh, M., 2021. Fixed-Budget Best-Arm Identification in

Contextual Bandits: A Static-Adaptive Algorithm. arXiv preprint arXiv:2106.04763.

Batur, D., Wang, L. and Choobineh, F.F., 2018. Methods for system selection based on

sequential mean–variance analysis. INFORMS Journal on Computing. 30(4). pp.724-738.

Budur, T. and Poturak, M., 2021. Employee performance and customer loyalty: Mediation effect

of customer satisfaction. Middle East Journal of Management. 8(5). pp.453-474.

Chattopadhyay, M. and Mitra, S.K., 2019. Determinants of revenue per available room:

Influential roles of average daily rate, demand, seasonality and yearly trend. International

Journal of Hospitality Management. 77. pp.573-582.

Choi, H., 2018. How to Handle Fixed Cost in Business Accounting. Available at SSRN 3179288.

Fan, Q., Guenther, D.A. and Wu, K., 2020. Fixed and Variable Tax Expense and the Cost of

Equity Capital. Available at SSRN 3575256.

Mouter, N., 2021. Willingness to allocate public budget and Participatory Value Evaluation.

In Advances in Transport Policy and Planning (Vol. 7, pp. 83-102). Academic Press.

Odu, G.O., 2019. Weighting methods for multi-criteria decision making technique. Journal of

Applied Sciences and Environmental Management. 23(8). pp.1449-1457.

Viktorov, D., 2020. Market penetration of a Finnish start-up operating as an online marketplace

for freelancers.

1

Books and journals

Azizi, M., Kveton, B. and Ghavamzadeh, M., 2021. Fixed-Budget Best-Arm Identification in

Contextual Bandits: A Static-Adaptive Algorithm. arXiv preprint arXiv:2106.04763.

Batur, D., Wang, L. and Choobineh, F.F., 2018. Methods for system selection based on

sequential mean–variance analysis. INFORMS Journal on Computing. 30(4). pp.724-738.

Budur, T. and Poturak, M., 2021. Employee performance and customer loyalty: Mediation effect

of customer satisfaction. Middle East Journal of Management. 8(5). pp.453-474.

Chattopadhyay, M. and Mitra, S.K., 2019. Determinants of revenue per available room:

Influential roles of average daily rate, demand, seasonality and yearly trend. International

Journal of Hospitality Management. 77. pp.573-582.

Choi, H., 2018. How to Handle Fixed Cost in Business Accounting. Available at SSRN 3179288.

Fan, Q., Guenther, D.A. and Wu, K., 2020. Fixed and Variable Tax Expense and the Cost of

Equity Capital. Available at SSRN 3575256.

Mouter, N., 2021. Willingness to allocate public budget and Participatory Value Evaluation.

In Advances in Transport Policy and Planning (Vol. 7, pp. 83-102). Academic Press.

Odu, G.O., 2019. Weighting methods for multi-criteria decision making technique. Journal of

Applied Sciences and Environmental Management. 23(8). pp.1449-1457.

Viktorov, D., 2020. Market penetration of a Finnish start-up operating as an online marketplace

for freelancers.

1

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.