Comprehensive Report on Managing Financial Resources Effectively

VerifiedAdded on 2023/06/15

|12

|2647

|373

Report

AI Summary

This report provides a detailed analysis of managing financial resources, covering budgeting, forecasting, and various financial metrics. Section A focuses on fixed and variable components in event planning, calculating profit with varying guest numbers. Section B discusses budgeting and forecasting techniques, including variance analysis, flexible budgets, static budgets, and direct labor variances. It further explains key performance indicators such as Average Daily Rate (ADR), Revenue per Available Room (RevPAR), Average Rate Index, and Market Penetration Index, illustrating their calculation and importance in the hospitality industry. The report offers practical examples and formulas for effective financial management and performance measurement.

Managing Financial

Resources

Resources

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

MAIN BODY...................................................................................................................................3

SECTION A.....................................................................................................................................3

Question 2....................................................................................................................................3

SECTION B.....................................................................................................................................5

Question 4....................................................................................................................................5

Question 5....................................................................................................................................8

REFERENCES..............................................................................................................................11

MAIN BODY...................................................................................................................................3

SECTION A.....................................................................................................................................3

Question 2....................................................................................................................................3

SECTION B.....................................................................................................................................5

Question 4....................................................................................................................................5

Question 5....................................................................................................................................8

REFERENCES..............................................................................................................................11

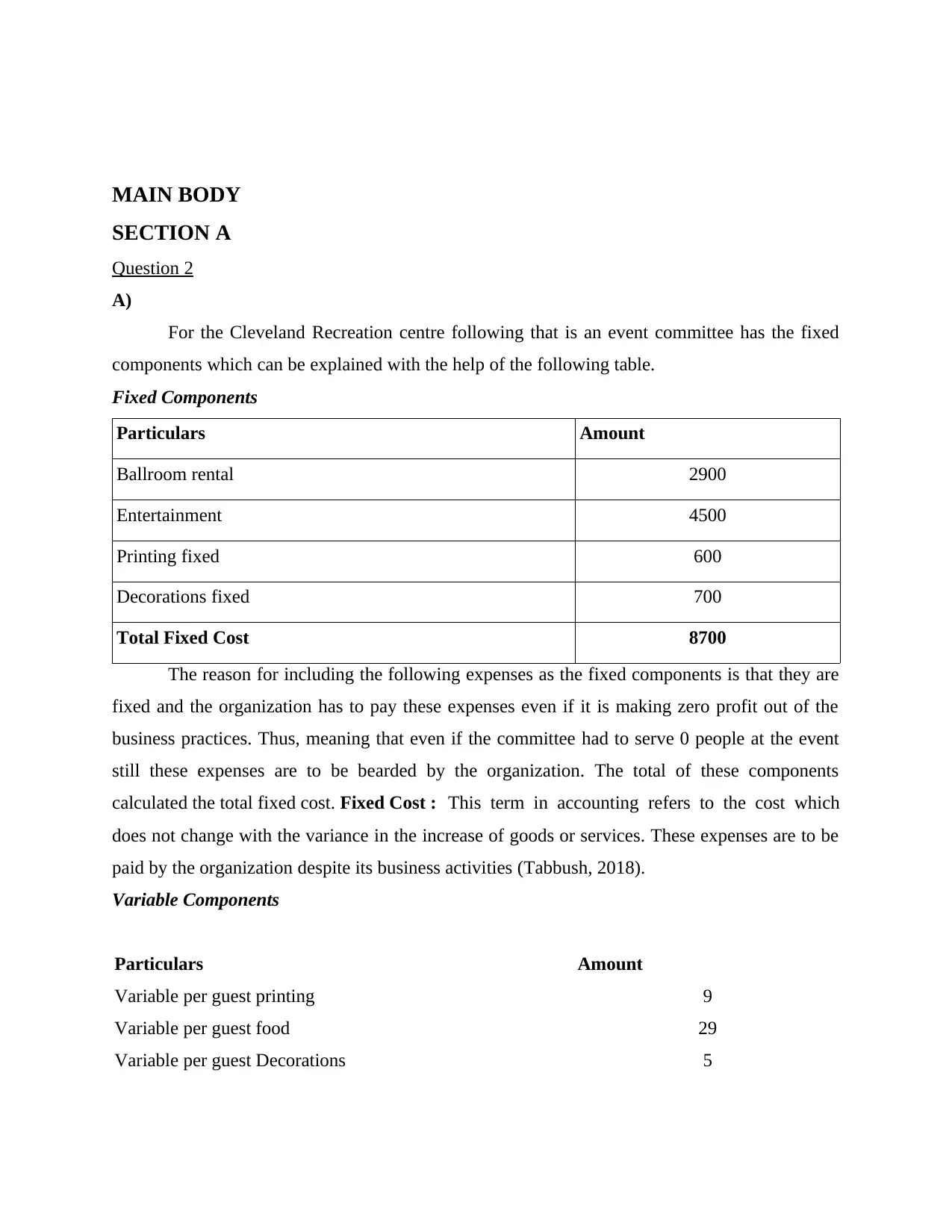

MAIN BODY

SECTION A

Question 2

A)

For the Cleveland Recreation centre following that is an event committee has the fixed

components which can be explained with the help of the following table.

Fixed Components

Particulars Amount

Ballroom rental 2900

Entertainment 4500

Printing fixed 600

Decorations fixed 700

Total Fixed Cost 8700

The reason for including the following expenses as the fixed components is that they are

fixed and the organization has to pay these expenses even if it is making zero profit out of the

business practices. Thus, meaning that even if the committee had to serve 0 people at the event

still these expenses are to be bearded by the organization. The total of these components

calculated the total fixed cost. Fixed Cost : This term in accounting refers to the cost which

does not change with the variance in the increase of goods or services. These expenses are to be

paid by the organization despite its business activities (Tabbush, 2018).

Variable Components

Particulars Amount

Variable per guest printing 9

Variable per guest food 29

Variable per guest Decorations 5

SECTION A

Question 2

A)

For the Cleveland Recreation centre following that is an event committee has the fixed

components which can be explained with the help of the following table.

Fixed Components

Particulars Amount

Ballroom rental 2900

Entertainment 4500

Printing fixed 600

Decorations fixed 700

Total Fixed Cost 8700

The reason for including the following expenses as the fixed components is that they are

fixed and the organization has to pay these expenses even if it is making zero profit out of the

business practices. Thus, meaning that even if the committee had to serve 0 people at the event

still these expenses are to be bearded by the organization. The total of these components

calculated the total fixed cost. Fixed Cost : This term in accounting refers to the cost which

does not change with the variance in the increase of goods or services. These expenses are to be

paid by the organization despite its business activities (Tabbush, 2018).

Variable Components

Particulars Amount

Variable per guest printing 9

Variable per guest food 29

Variable per guest Decorations 5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

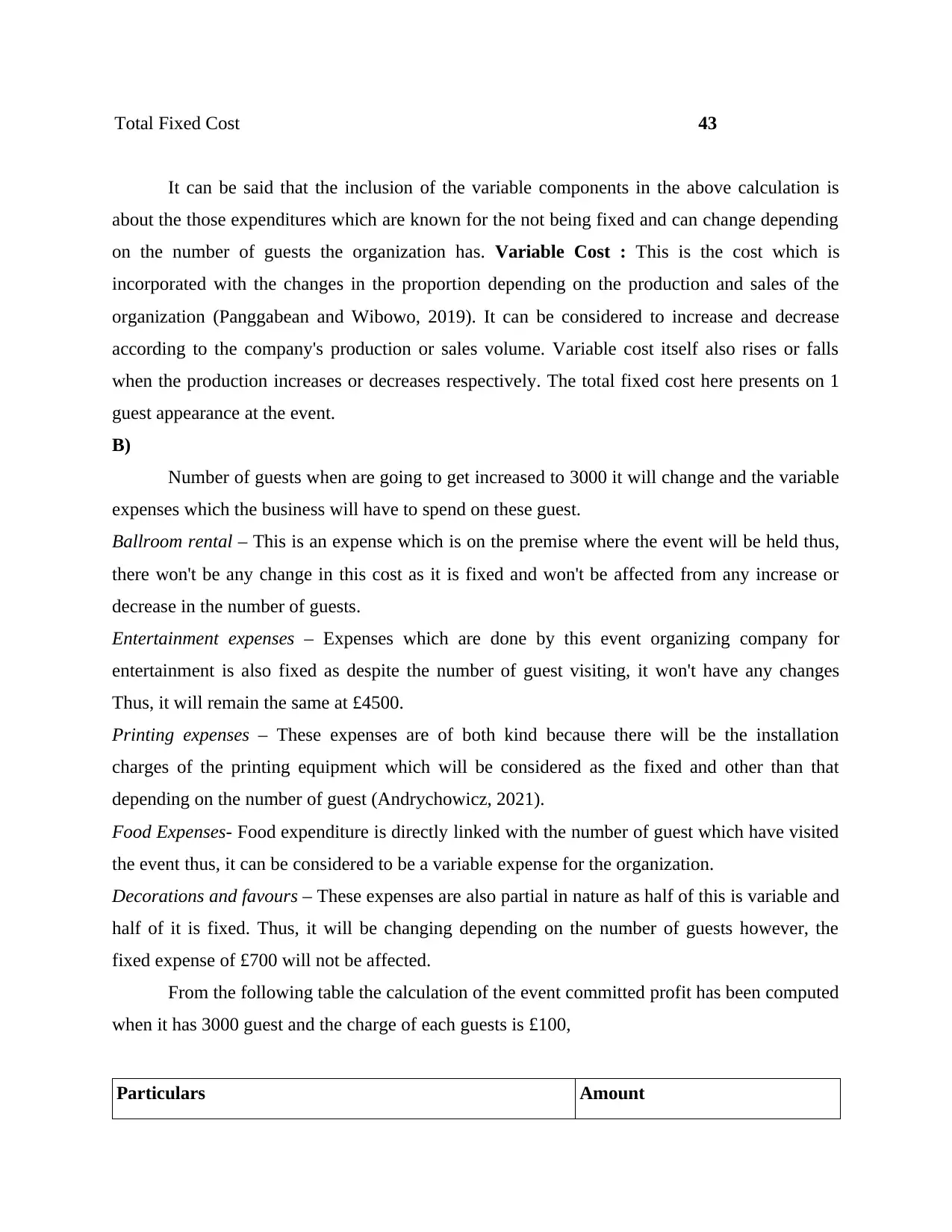

Total Fixed Cost 43

It can be said that the inclusion of the variable components in the above calculation is

about the those expenditures which are known for the not being fixed and can change depending

on the number of guests the organization has. Variable Cost : This is the cost which is

incorporated with the changes in the proportion depending on the production and sales of the

organization (Panggabean and Wibowo, 2019). It can be considered to increase and decrease

according to the company's production or sales volume. Variable cost itself also rises or falls

when the production increases or decreases respectively. The total fixed cost here presents on 1

guest appearance at the event.

B)

Number of guests when are going to get increased to 3000 it will change and the variable

expenses which the business will have to spend on these guest.

Ballroom rental – This is an expense which is on the premise where the event will be held thus,

there won't be any change in this cost as it is fixed and won't be affected from any increase or

decrease in the number of guests.

Entertainment expenses – Expenses which are done by this event organizing company for

entertainment is also fixed as despite the number of guest visiting, it won't have any changes

Thus, it will remain the same at £4500.

Printing expenses – These expenses are of both kind because there will be the installation

charges of the printing equipment which will be considered as the fixed and other than that

depending on the number of guest (Andrychowicz, 2021).

Food Expenses- Food expenditure is directly linked with the number of guest which have visited

the event thus, it can be considered to be a variable expense for the organization.

Decorations and favours – These expenses are also partial in nature as half of this is variable and

half of it is fixed. Thus, it will be changing depending on the number of guests however, the

fixed expense of £700 will not be affected.

From the following table the calculation of the event committed profit has been computed

when it has 3000 guest and the charge of each guests is £100,

Particulars Amount

It can be said that the inclusion of the variable components in the above calculation is

about the those expenditures which are known for the not being fixed and can change depending

on the number of guests the organization has. Variable Cost : This is the cost which is

incorporated with the changes in the proportion depending on the production and sales of the

organization (Panggabean and Wibowo, 2019). It can be considered to increase and decrease

according to the company's production or sales volume. Variable cost itself also rises or falls

when the production increases or decreases respectively. The total fixed cost here presents on 1

guest appearance at the event.

B)

Number of guests when are going to get increased to 3000 it will change and the variable

expenses which the business will have to spend on these guest.

Ballroom rental – This is an expense which is on the premise where the event will be held thus,

there won't be any change in this cost as it is fixed and won't be affected from any increase or

decrease in the number of guests.

Entertainment expenses – Expenses which are done by this event organizing company for

entertainment is also fixed as despite the number of guest visiting, it won't have any changes

Thus, it will remain the same at £4500.

Printing expenses – These expenses are of both kind because there will be the installation

charges of the printing equipment which will be considered as the fixed and other than that

depending on the number of guest (Andrychowicz, 2021).

Food Expenses- Food expenditure is directly linked with the number of guest which have visited

the event thus, it can be considered to be a variable expense for the organization.

Decorations and favours – These expenses are also partial in nature as half of this is variable and

half of it is fixed. Thus, it will be changing depending on the number of guests however, the

fixed expense of £700 will not be affected.

From the following table the calculation of the event committed profit has been computed

when it has 3000 guest and the charge of each guests is £100,

Particulars Amount

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

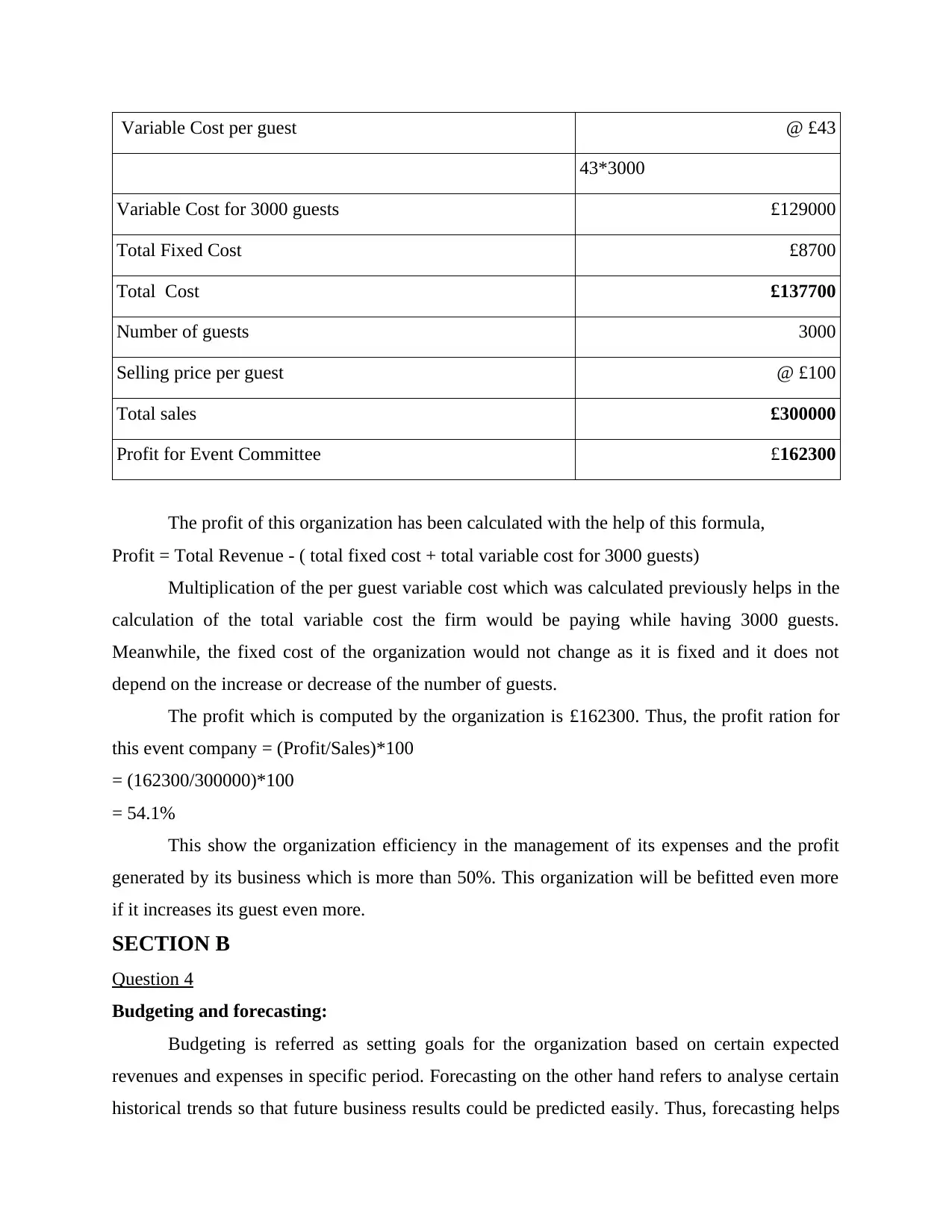

Variable Cost per guest @ £43

43*3000

Variable Cost for 3000 guests £129000

Total Fixed Cost £8700

Total Cost £137700

Number of guests 3000

Selling price per guest @ £100

Total sales £300000

Profit for Event Committee £162300

The profit of this organization has been calculated with the help of this formula,

Profit = Total Revenue - ( total fixed cost + total variable cost for 3000 guests)

Multiplication of the per guest variable cost which was calculated previously helps in the

calculation of the total variable cost the firm would be paying while having 3000 guests.

Meanwhile, the fixed cost of the organization would not change as it is fixed and it does not

depend on the increase or decrease of the number of guests.

The profit which is computed by the organization is £162300. Thus, the profit ration for

this event company = (Profit/Sales)*100

= (162300/300000)*100

= 54.1%

This show the organization efficiency in the management of its expenses and the profit

generated by its business which is more than 50%. This organization will be befitted even more

if it increases its guest even more.

SECTION B

Question 4

Budgeting and forecasting:

Budgeting is referred as setting goals for the organization based on certain expected

revenues and expenses in specific period. Forecasting on the other hand refers to analyse certain

historical trends so that future business results could be predicted easily. Thus, forecasting helps

43*3000

Variable Cost for 3000 guests £129000

Total Fixed Cost £8700

Total Cost £137700

Number of guests 3000

Selling price per guest @ £100

Total sales £300000

Profit for Event Committee £162300

The profit of this organization has been calculated with the help of this formula,

Profit = Total Revenue - ( total fixed cost + total variable cost for 3000 guests)

Multiplication of the per guest variable cost which was calculated previously helps in the

calculation of the total variable cost the firm would be paying while having 3000 guests.

Meanwhile, the fixed cost of the organization would not change as it is fixed and it does not

depend on the increase or decrease of the number of guests.

The profit which is computed by the organization is £162300. Thus, the profit ration for

this event company = (Profit/Sales)*100

= (162300/300000)*100

= 54.1%

This show the organization efficiency in the management of its expenses and the profit

generated by its business which is more than 50%. This organization will be befitted even more

if it increases its guest even more.

SECTION B

Question 4

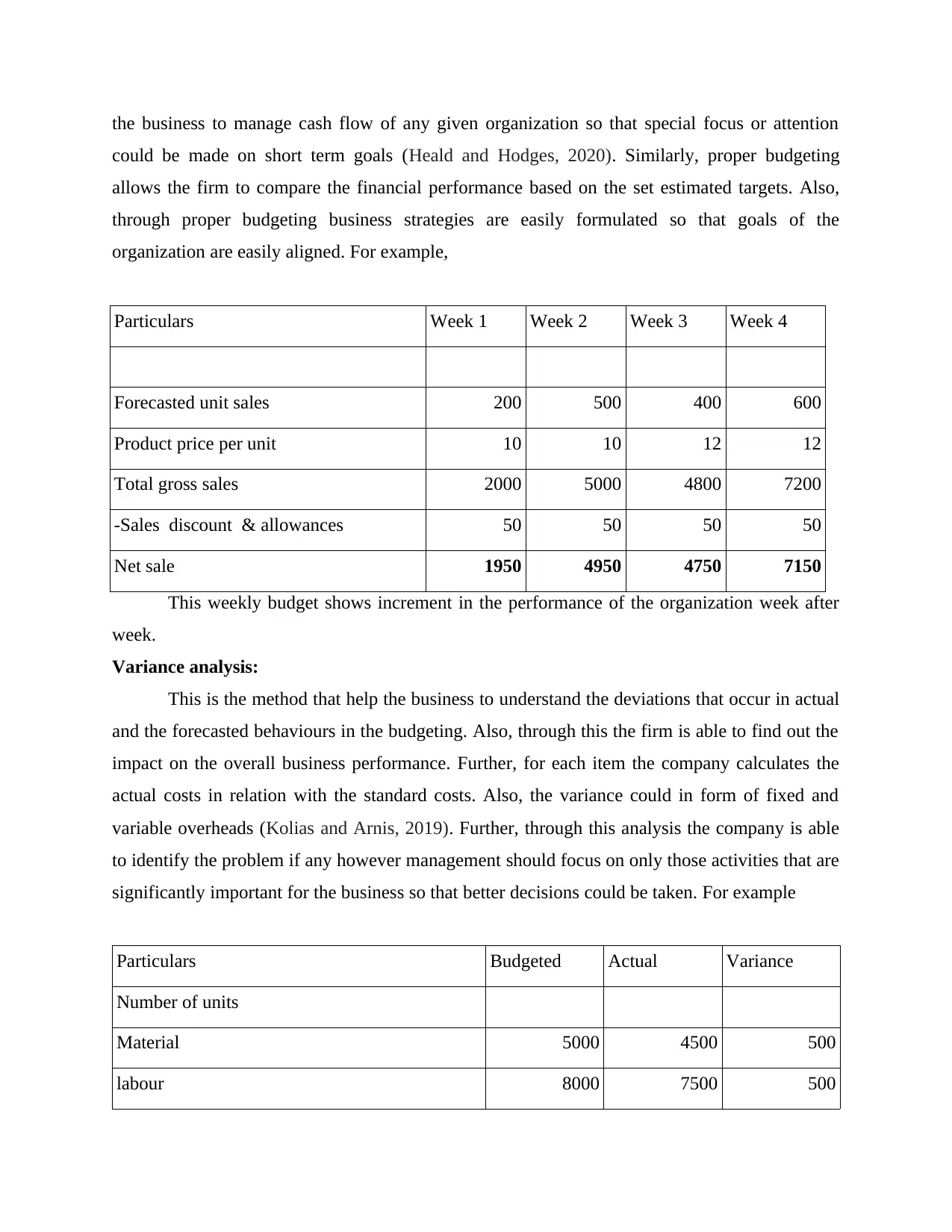

Budgeting and forecasting:

Budgeting is referred as setting goals for the organization based on certain expected

revenues and expenses in specific period. Forecasting on the other hand refers to analyse certain

historical trends so that future business results could be predicted easily. Thus, forecasting helps

the business to manage cash flow of any given organization so that special focus or attention

could be made on short term goals (Heald and Hodges, 2020). Similarly, proper budgeting

allows the firm to compare the financial performance based on the set estimated targets. Also,

through proper budgeting business strategies are easily formulated so that goals of the

organization are easily aligned. For example,

Particulars Week 1 Week 2 Week 3 Week 4

Forecasted unit sales 200 500 400 600

Product price per unit 10 10 12 12

Total gross sales 2000 5000 4800 7200

-Sales discount & allowances 50 50 50 50

Net sale 1950 4950 4750 7150

This weekly budget shows increment in the performance of the organization week after

week.

Variance analysis:

This is the method that help the business to understand the deviations that occur in actual

and the forecasted behaviours in the budgeting. Also, through this the firm is able to find out the

impact on the overall business performance. Further, for each item the company calculates the

actual costs in relation with the standard costs. Also, the variance could in form of fixed and

variable overheads (Kolias and Arnis, 2019). Further, through this analysis the company is able

to identify the problem if any however management should focus on only those activities that are

significantly important for the business so that better decisions could be taken. For example

Particulars Budgeted Actual Variance

Number of units

Material 5000 4500 500

labour 8000 7500 500

could be made on short term goals (Heald and Hodges, 2020). Similarly, proper budgeting

allows the firm to compare the financial performance based on the set estimated targets. Also,

through proper budgeting business strategies are easily formulated so that goals of the

organization are easily aligned. For example,

Particulars Week 1 Week 2 Week 3 Week 4

Forecasted unit sales 200 500 400 600

Product price per unit 10 10 12 12

Total gross sales 2000 5000 4800 7200

-Sales discount & allowances 50 50 50 50

Net sale 1950 4950 4750 7150

This weekly budget shows increment in the performance of the organization week after

week.

Variance analysis:

This is the method that help the business to understand the deviations that occur in actual

and the forecasted behaviours in the budgeting. Also, through this the firm is able to find out the

impact on the overall business performance. Further, for each item the company calculates the

actual costs in relation with the standard costs. Also, the variance could in form of fixed and

variable overheads (Kolias and Arnis, 2019). Further, through this analysis the company is able

to identify the problem if any however management should focus on only those activities that are

significantly important for the business so that better decisions could be taken. For example

Particulars Budgeted Actual Variance

Number of units

Material 5000 4500 500

labour 8000 7500 500

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

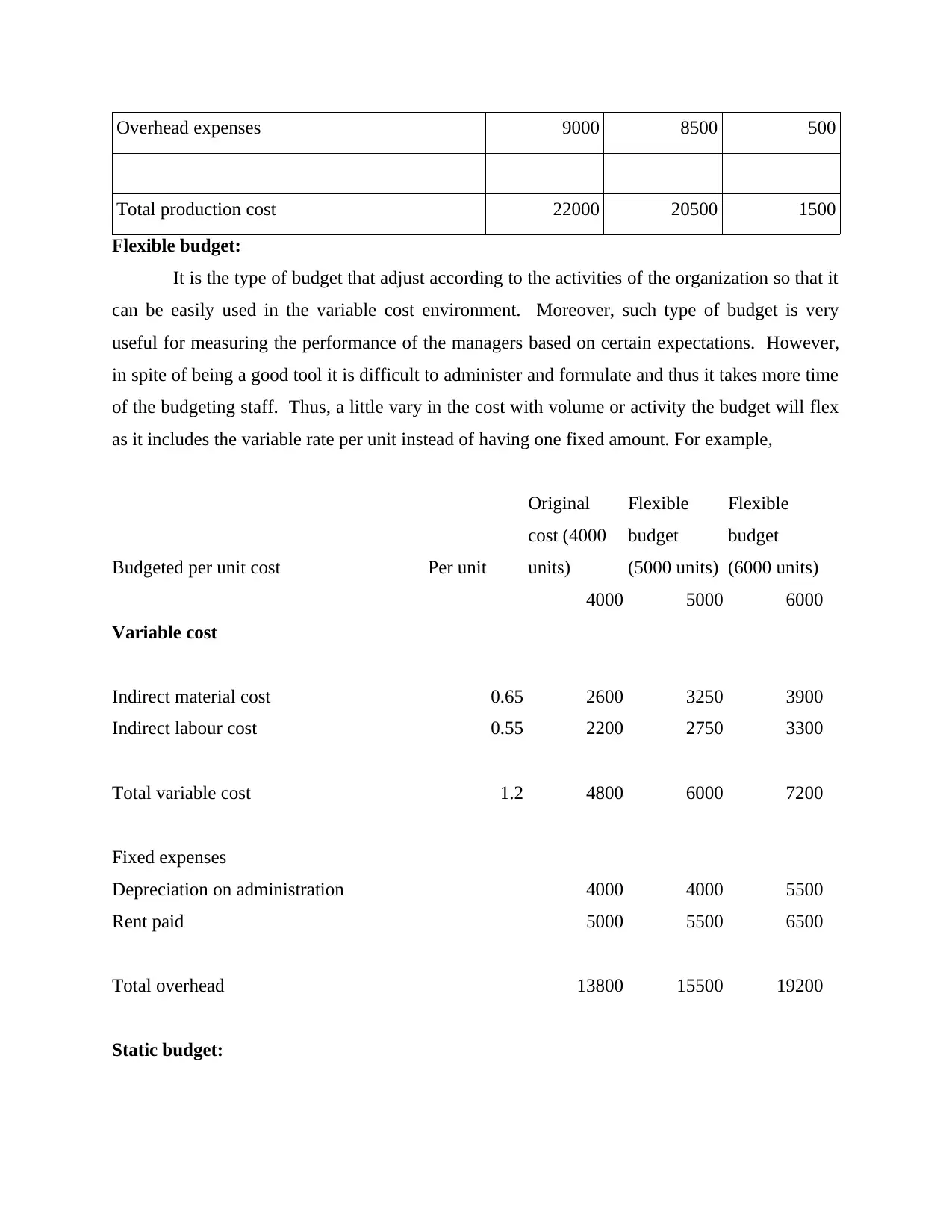

Overhead expenses 9000 8500 500

Total production cost 22000 20500 1500

Flexible budget:

It is the type of budget that adjust according to the activities of the organization so that it

can be easily used in the variable cost environment. Moreover, such type of budget is very

useful for measuring the performance of the managers based on certain expectations. However,

in spite of being a good tool it is difficult to administer and formulate and thus it takes more time

of the budgeting staff. Thus, a little vary in the cost with volume or activity the budget will flex

as it includes the variable rate per unit instead of having one fixed amount. For example,

Budgeted per unit cost Per unit

Original

cost (4000

units)

Flexible

budget

(5000 units)

Flexible

budget

(6000 units)

4000 5000 6000

Variable cost

Indirect material cost 0.65 2600 3250 3900

Indirect labour cost 0.55 2200 2750 3300

Total variable cost 1.2 4800 6000 7200

Fixed expenses

Depreciation on administration 4000 4000 5500

Rent paid 5000 5500 6500

Total overhead 13800 15500 19200

Static budget:

Total production cost 22000 20500 1500

Flexible budget:

It is the type of budget that adjust according to the activities of the organization so that it

can be easily used in the variable cost environment. Moreover, such type of budget is very

useful for measuring the performance of the managers based on certain expectations. However,

in spite of being a good tool it is difficult to administer and formulate and thus it takes more time

of the budgeting staff. Thus, a little vary in the cost with volume or activity the budget will flex

as it includes the variable rate per unit instead of having one fixed amount. For example,

Budgeted per unit cost Per unit

Original

cost (4000

units)

Flexible

budget

(5000 units)

Flexible

budget

(6000 units)

4000 5000 6000

Variable cost

Indirect material cost 0.65 2600 3250 3900

Indirect labour cost 0.55 2200 2750 3300

Total variable cost 1.2 4800 6000 7200

Fixed expenses

Depreciation on administration 4000 4000 5500

Rent paid 5000 5500 6500

Total overhead 13800 15500 19200

Static budget:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

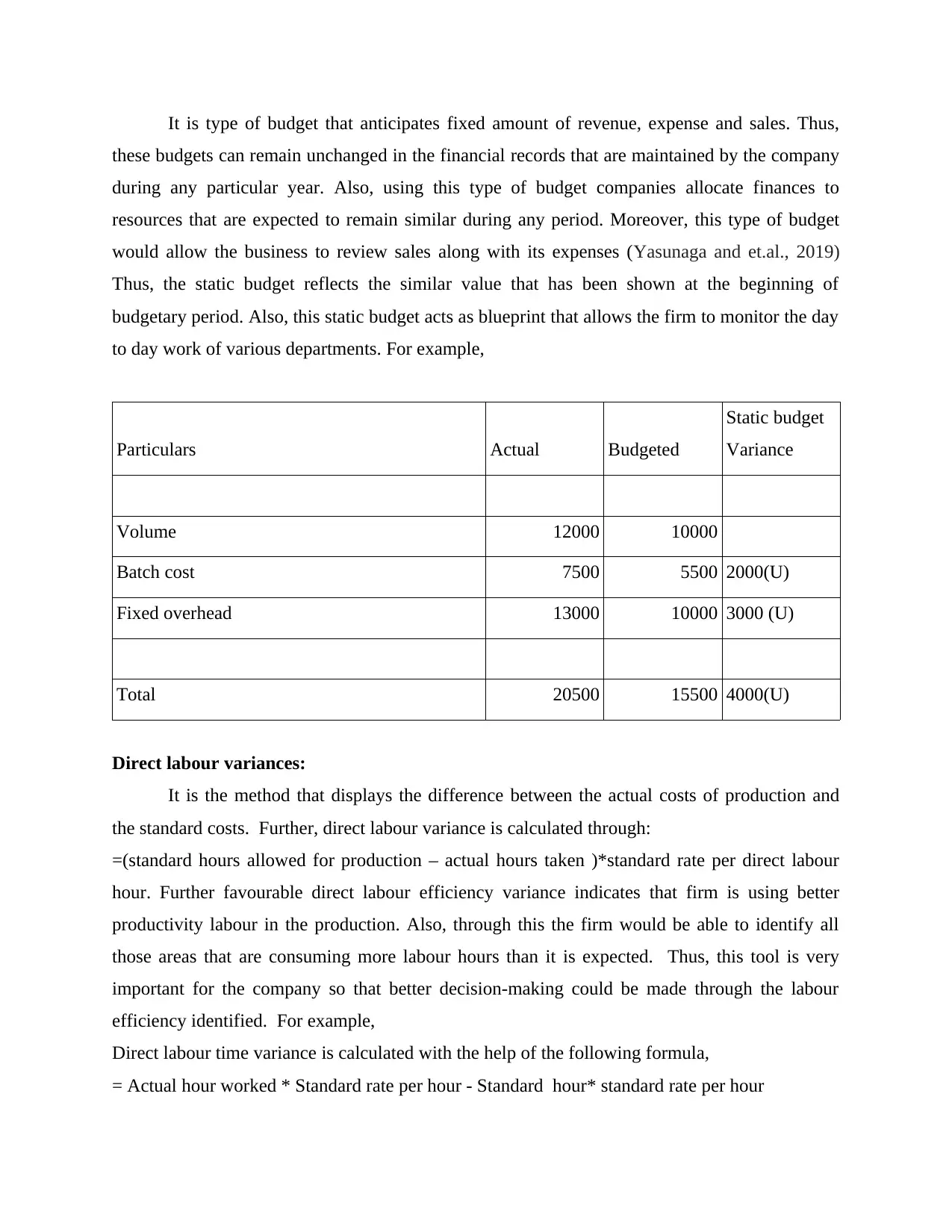

It is type of budget that anticipates fixed amount of revenue, expense and sales. Thus,

these budgets can remain unchanged in the financial records that are maintained by the company

during any particular year. Also, using this type of budget companies allocate finances to

resources that are expected to remain similar during any period. Moreover, this type of budget

would allow the business to review sales along with its expenses (Yasunaga and et.al., 2019)

Thus, the static budget reflects the similar value that has been shown at the beginning of

budgetary period. Also, this static budget acts as blueprint that allows the firm to monitor the day

to day work of various departments. For example,

Particulars Actual Budgeted

Static budget

Variance

Volume 12000 10000

Batch cost 7500 5500 2000(U)

Fixed overhead 13000 10000 3000 (U)

Total 20500 15500 4000(U)

Direct labour variances:

It is the method that displays the difference between the actual costs of production and

the standard costs. Further, direct labour variance is calculated through:

=(standard hours allowed for production – actual hours taken )*standard rate per direct labour

hour. Further favourable direct labour efficiency variance indicates that firm is using better

productivity labour in the production. Also, through this the firm would be able to identify all

those areas that are consuming more labour hours than it is expected. Thus, this tool is very

important for the company so that better decision-making could be made through the labour

efficiency identified. For example,

Direct labour time variance is calculated with the help of the following formula,

= Actual hour worked * Standard rate per hour - Standard hour* standard rate per hour

these budgets can remain unchanged in the financial records that are maintained by the company

during any particular year. Also, using this type of budget companies allocate finances to

resources that are expected to remain similar during any period. Moreover, this type of budget

would allow the business to review sales along with its expenses (Yasunaga and et.al., 2019)

Thus, the static budget reflects the similar value that has been shown at the beginning of

budgetary period. Also, this static budget acts as blueprint that allows the firm to monitor the day

to day work of various departments. For example,

Particulars Actual Budgeted

Static budget

Variance

Volume 12000 10000

Batch cost 7500 5500 2000(U)

Fixed overhead 13000 10000 3000 (U)

Total 20500 15500 4000(U)

Direct labour variances:

It is the method that displays the difference between the actual costs of production and

the standard costs. Further, direct labour variance is calculated through:

=(standard hours allowed for production – actual hours taken )*standard rate per direct labour

hour. Further favourable direct labour efficiency variance indicates that firm is using better

productivity labour in the production. Also, through this the firm would be able to identify all

those areas that are consuming more labour hours than it is expected. Thus, this tool is very

important for the company so that better decision-making could be made through the labour

efficiency identified. For example,

Direct labour time variance is calculated with the help of the following formula,

= Actual hour worked * Standard rate per hour - Standard hour* standard rate per hour

= 5*11 – 4*9

=55-36

= 19

Question 5

Average Daily Rate :

Also known as the ADR, average daily rate is the rental revenue earned in average for the

occupation of the room per day. It can be said that the operations of the hotel is measured with

the help of this rate. In the lodging business the use of ADR is considered to be very helpful as it

the multiplication of the ADR with the occupancy rate helps in the calculation of the per room

revenue of the firm. The formula for ADR calculation is,

ADR= Total revenue from rooms/Total number of sold rooms.

For example in a hotel which has a room revenue of £100000 and has a total of 750

rooms sold therefore the total ADR for this hotel would be,

=100000/750

=133.33

Revenue per available room (RevPAR) :

The revenue per available room is also abbreviated as the RevPAR and is one of the most

used tool in the hospitality industry. It helps with the calculation of the performance

measurement in the hospitality industry (Santana and Castro, 2019). It calculates the hotel's

average which is also known as the occupancy rate of the organization. With the help of this

occupancy rate the division of the total room revenue is also known understood as the number of

rooms for a given time period (Accounting CPE Courses & Books, 2021). Example of RevPAR

the given number of total rooms are 250, the occupancy rate is give at 85%. Average cost that is

incurred by hotel for single room is £1000 therefore this helps in the calculation of RevPAR =

per night cost multiplied by occupancy rate.

= (1000*85%)

= £850.00

Average Rate Index :

it is the index which show the actual comparison of the hotel with its competitors and is

known for the determination of the hotels. This shows that the organization is considered to hold

a lower rate of room which helps in the showing a greater average price which helps the business

=55-36

= 19

Question 5

Average Daily Rate :

Also known as the ADR, average daily rate is the rental revenue earned in average for the

occupation of the room per day. It can be said that the operations of the hotel is measured with

the help of this rate. In the lodging business the use of ADR is considered to be very helpful as it

the multiplication of the ADR with the occupancy rate helps in the calculation of the per room

revenue of the firm. The formula for ADR calculation is,

ADR= Total revenue from rooms/Total number of sold rooms.

For example in a hotel which has a room revenue of £100000 and has a total of 750

rooms sold therefore the total ADR for this hotel would be,

=100000/750

=133.33

Revenue per available room (RevPAR) :

The revenue per available room is also abbreviated as the RevPAR and is one of the most

used tool in the hospitality industry. It helps with the calculation of the performance

measurement in the hospitality industry (Santana and Castro, 2019). It calculates the hotel's

average which is also known as the occupancy rate of the organization. With the help of this

occupancy rate the division of the total room revenue is also known understood as the number of

rooms for a given time period (Accounting CPE Courses & Books, 2021). Example of RevPAR

the given number of total rooms are 250, the occupancy rate is give at 85%. Average cost that is

incurred by hotel for single room is £1000 therefore this helps in the calculation of RevPAR =

per night cost multiplied by occupancy rate.

= (1000*85%)

= £850.00

Average Rate Index :

it is the index which show the actual comparison of the hotel with its competitors and is

known for the determination of the hotels. This shows that the organization is considered to hold

a lower rate of room which helps in the showing a greater average price which helps the business

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

of the hotel to be higher than that of the competitors. The calculation of this index is done with

the help of the formula which is, Organization ADR/ Competitors Average ADR

For example,

Given

Competitors ADR = 1000

Room Revenue =£105000

Total Number of Rooms = 500

Organizations ADR = (105000/125)

=840

Therefore,

ARI = 840/1000

=0.84

Market Penetration Index :

This is that index which is mostly utilized in the hospitality industry for the measurement

of its position in comparison to the set of competitors which is considered to be very helpful for

the preselection of the set of competitors. It can also be considered to be the showing the

business and its relative about the relations which impacts the competitors of the market. The

formula for its calculation is, Occupancy Rate/ Competitors set of occupancy rate,

For example, If the given occupancy rate is 85% and the set of competitors have the occupancy

rate of 95% then,

MPI= 85%/95%

= 0.894

This shows that the organization has cheaper rooms available in comparison to its competition.

Customer Satisfaction :

Customer satisfaction is the known as the measurement of the key determinants of the

level of happiness which the company's products, services and capabilities have. It can be known

as the key determinant to the information that includes the surveys and ratings that can help the

company in determining the ways in which the hotel and improve the room services which are

provided by it. For example

Formula of Cs= (The total number of 12 of 15) / total respondents *100%

the help of the formula which is, Organization ADR/ Competitors Average ADR

For example,

Given

Competitors ADR = 1000

Room Revenue =£105000

Total Number of Rooms = 500

Organizations ADR = (105000/125)

=840

Therefore,

ARI = 840/1000

=0.84

Market Penetration Index :

This is that index which is mostly utilized in the hospitality industry for the measurement

of its position in comparison to the set of competitors which is considered to be very helpful for

the preselection of the set of competitors. It can also be considered to be the showing the

business and its relative about the relations which impacts the competitors of the market. The

formula for its calculation is, Occupancy Rate/ Competitors set of occupancy rate,

For example, If the given occupancy rate is 85% and the set of competitors have the occupancy

rate of 95% then,

MPI= 85%/95%

= 0.894

This shows that the organization has cheaper rooms available in comparison to its competition.

Customer Satisfaction :

Customer satisfaction is the known as the measurement of the key determinants of the

level of happiness which the company's products, services and capabilities have. It can be known

as the key determinant to the information that includes the surveys and ratings that can help the

company in determining the ways in which the hotel and improve the room services which are

provided by it. For example

Formula of Cs= (The total number of 12 of 15) / total respondents *100%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

If the result of survey is 82 out of 100 responses given, if the average response from the

customers rating is of 12 of 15 then it is at 80%, thus, it can be said that the majority of the

customers are satisfied.

customers rating is of 12 of 15 then it is at 80%, thus, it can be said that the majority of the

customers are satisfied.

REFERENCES

Books and Journals

Andrychowicz, M., 2021. The impact of energy storage along with the allocation of RES on the

reduction of energy costs using MILP. Energies. 14(13). p.3783.

Heald, D. and Hodges, R., 2020. The accounting, budgeting and fiscal impact of COVID-19 on

the United Kingdom. Journal of Public Budgeting, Accounting & Financial

Management.

Kolias, G. and Arnis, N., 2019. The optimal allocation of current assets using mean-variance

analysis. Accounting and Management Information Systems. 18(1). pp.50-72.

Panggabean, G.M. and Wibowo, D., 2019, March. Cost Structure Evaluation of Variable Costs

and Business Forecast in Spooring Services at SME Trijaya Ban 83. In 12th

International Conference on Business and Management Research (ICBMR 2018) (pp.

264-268). Atlantis Press.

Santana, J. and Castro, R., 2019. Electricity markets in Europe: How to recover the production

costs?. International Transactions on Electrical Energy Systems. 29(10). p.e12068.

Tabbush, V., 2018. Understanding costs: How cbos can build business acumen for future

partnerships. Generations. 42(1). pp.61-64.

Yasunaga, K. and et.al., 2019. Space–time spectral analysis of the moist static energy budget

equation. Journal of Climate. 32(2). pp.501-529.

Online

Accounting CPE Courses & Books, 2021[Online]. Available through:

<https://www.accountingtools.com/articles/what-are-examples-of-fixed-costs.html>

Books and Journals

Andrychowicz, M., 2021. The impact of energy storage along with the allocation of RES on the

reduction of energy costs using MILP. Energies. 14(13). p.3783.

Heald, D. and Hodges, R., 2020. The accounting, budgeting and fiscal impact of COVID-19 on

the United Kingdom. Journal of Public Budgeting, Accounting & Financial

Management.

Kolias, G. and Arnis, N., 2019. The optimal allocation of current assets using mean-variance

analysis. Accounting and Management Information Systems. 18(1). pp.50-72.

Panggabean, G.M. and Wibowo, D., 2019, March. Cost Structure Evaluation of Variable Costs

and Business Forecast in Spooring Services at SME Trijaya Ban 83. In 12th

International Conference on Business and Management Research (ICBMR 2018) (pp.

264-268). Atlantis Press.

Santana, J. and Castro, R., 2019. Electricity markets in Europe: How to recover the production

costs?. International Transactions on Electrical Energy Systems. 29(10). p.e12068.

Tabbush, V., 2018. Understanding costs: How cbos can build business acumen for future

partnerships. Generations. 42(1). pp.61-64.

Yasunaga, K. and et.al., 2019. Space–time spectral analysis of the moist static energy budget

equation. Journal of Climate. 32(2). pp.501-529.

Online

Accounting CPE Courses & Books, 2021[Online]. Available through:

<https://www.accountingtools.com/articles/what-are-examples-of-fixed-costs.html>

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.