Case Study Analysis: Managing Operations and Finance - ACC4029 Module

VerifiedAdded on 2023/01/19

|15

|3519

|75

Case Study

AI Summary

This case study analyzes Cucumber Ltd, a smartphone company, examining the role of management accounting, investment appraisal, business planning, and budgetary control. The assignment addresses the differences between management and financial accounting, explores various costing models like ABC costing and breakeven analysis, and applies capital investment appraisal techniques such as NPV, IRR, and payback period to evaluate potential projects. It also evaluates the importance of business plans and budgets in achieving the company's financial targets, including a target profit of £5m and an 18% return on capital employed. The analysis includes recommendations for improvement and the development of a budgetary control report, considering factors like sales price, variable costs, and fixed costs to determine the required sales volume to meet the profit goals. The study also discusses the balanced scorecard approach for performance measurement, providing a holistic view of the company's performance beyond financial metrics.

MANAGING OPERATIONS AND FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Solution 1: Role of management accounting...................................................................................3

Solution 2: Investment Appraisal....................................................................................................5

Solution 3- Business Plan and budgetary control............................................................................8

Solution 4 – Balanced scorecard approach....................................................................................12

References:....................................................................................................................................14

Solution 1: Role of management accounting...................................................................................3

Solution 2: Investment Appraisal....................................................................................................5

Solution 3- Business Plan and budgetary control............................................................................8

Solution 4 – Balanced scorecard approach....................................................................................12

References:....................................................................................................................................14

Solution 1: Role of management accounting

Management accounting is a process of finance that involves preparation of certain accounts and

reports, and also provides financial and statistical information which helps to take short term

decisions of the company appropriately. The reports that are prepared by the management of the

company usually includes information relating to sales, creditors/ debtors, abnormal losses or

gains, advances receives, outstanding liabilities, cash in hand etc. This information are useful in

the process of decision making. It is important to take the decisions of the company on a

reasonable basis so that the company does not have to suffer in the long run. The following

points explain the role of management accounting in the organization (Peterson & Fabozzi,

2012).

Preparation or reports: The management accountant of the company has the duty to

prepare accounts as well as reports that would help the company to take short term

financial decisions intellectually.

Forecasting future impacts: The managers of the company forecast the impact of the

present actions and act accordingly. This also includes formulating strategies and

corporate planning.

Monitoring the capital structure: It is very important for the manager of the company to

monitor the capital structure and maintain a favorable proportion of debt and equity. A

favorable capital structure is one which has optimal weighted average cost of capital.

There are certain theories that have to be kept in mind while monitoring the capital

structure such as leverage and trading on equity.

Control: It is important for the company to reduce costs in order to generate higher

revenues. In order to reduce costs the management has to prepare budgets, standard

costs, variances, cash flow and fund flow statement and analyze the same before making

any kind of expenditure (Adelaja, 2015).

Decision making – The position of management accountant is better than that of

employees and other accountants. He provides instruction to the other executives of the

company relating to cost control and the various methods that could be adopted to do so.

Management accounting is a process of finance that involves preparation of certain accounts and

reports, and also provides financial and statistical information which helps to take short term

decisions of the company appropriately. The reports that are prepared by the management of the

company usually includes information relating to sales, creditors/ debtors, abnormal losses or

gains, advances receives, outstanding liabilities, cash in hand etc. This information are useful in

the process of decision making. It is important to take the decisions of the company on a

reasonable basis so that the company does not have to suffer in the long run. The following

points explain the role of management accounting in the organization (Peterson & Fabozzi,

2012).

Preparation or reports: The management accountant of the company has the duty to

prepare accounts as well as reports that would help the company to take short term

financial decisions intellectually.

Forecasting future impacts: The managers of the company forecast the impact of the

present actions and act accordingly. This also includes formulating strategies and

corporate planning.

Monitoring the capital structure: It is very important for the manager of the company to

monitor the capital structure and maintain a favorable proportion of debt and equity. A

favorable capital structure is one which has optimal weighted average cost of capital.

There are certain theories that have to be kept in mind while monitoring the capital

structure such as leverage and trading on equity.

Control: It is important for the company to reduce costs in order to generate higher

revenues. In order to reduce costs the management has to prepare budgets, standard

costs, variances, cash flow and fund flow statement and analyze the same before making

any kind of expenditure (Adelaja, 2015).

Decision making – The position of management accountant is better than that of

employees and other accountants. He provides instruction to the other executives of the

company relating to cost control and the various methods that could be adopted to do so.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management accounting and financial accounting are two different branch of finance. The

difference between the two is discussed below:

The business results are presented in the financial reports of the company whereas the

management report tells about the efficiency of the management of the company; it is

more detailed in nature as compared to financial reports (Rivenbark, Vogt, & Marlowe,

2009).

Financial reports give information about the profitability of the company whereas the

management reports defines the problems that are arising in the organization and its

proposed solutions (Bierman & Smidt, 2010).

The financial reports of the company contain facts and any mistake in it would invite

legal and ethical troubles for the company. But the management report contains various

kind of information which may be correct or incorrect as it is prepared on a judgmental

basis. Any incorrect information that is contained in the management reports does not

cause any problems (Menifield, 2014).

Financial reports are prepared to provide information about the company to both internal

as well as external stakeholders whereas management reports are prepared only for the

internal stakeholders.

There is certain accounting as well as auditing standards that has to be complied with for

the preparation of financial reports. However, the preparation of management reports

does not require compliance with any such standards (Dayananda, Irons, Harrison,

Herbohn, & Rowland, 2008).

There are different cost models that are used within an organization. The most common cost

models that are used by the operational managers are explained below:

ABC costing: In this costing method, all the activities performed by the company are

identified and then costs are allocated to different products and services on the basis of

consumption made by them (Seitz & Ellison, 2009).

Cost Breakeven analysis: A breakeven point can be defined as the level at which the

company will have no profits or gains. It helps the company to know the level after which

the company will start making profits because initially the company is busy at recovering

the fixed costs and variable costs incurred (Peterson & Fabozzi, 2012).

difference between the two is discussed below:

The business results are presented in the financial reports of the company whereas the

management report tells about the efficiency of the management of the company; it is

more detailed in nature as compared to financial reports (Rivenbark, Vogt, & Marlowe,

2009).

Financial reports give information about the profitability of the company whereas the

management reports defines the problems that are arising in the organization and its

proposed solutions (Bierman & Smidt, 2010).

The financial reports of the company contain facts and any mistake in it would invite

legal and ethical troubles for the company. But the management report contains various

kind of information which may be correct or incorrect as it is prepared on a judgmental

basis. Any incorrect information that is contained in the management reports does not

cause any problems (Menifield, 2014).

Financial reports are prepared to provide information about the company to both internal

as well as external stakeholders whereas management reports are prepared only for the

internal stakeholders.

There is certain accounting as well as auditing standards that has to be complied with for

the preparation of financial reports. However, the preparation of management reports

does not require compliance with any such standards (Dayananda, Irons, Harrison,

Herbohn, & Rowland, 2008).

There are different cost models that are used within an organization. The most common cost

models that are used by the operational managers are explained below:

ABC costing: In this costing method, all the activities performed by the company are

identified and then costs are allocated to different products and services on the basis of

consumption made by them (Seitz & Ellison, 2009).

Cost Breakeven analysis: A breakeven point can be defined as the level at which the

company will have no profits or gains. It helps the company to know the level after which

the company will start making profits because initially the company is busy at recovering

the fixed costs and variable costs incurred (Peterson & Fabozzi, 2012).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Solution 2: Investment Appraisal

Capital budgeting is a process carried out for investment appraisal. Investment appraisal is done

to determine whether the fixed capital investments done by the firm is worth it or not. The main

objective of carrying out investment appraisal practice is to maximize the wealth of shareholders

and earn huge profits in the long run.

There are different kinds of investment appraisal techniques available on the basis of investor

and stakeholder’s expectation. The investment appraisal techniques are explained below:

Net present value (NPV) – This technique is used to calculate the net cash flow after the

payment of all committed costs. A company accepts a project only if the forecasted net

present value is positive. The calculation of net present value is done by discounting the

cash flows and at a particular point of time (Schroeder, 2014).

Accounting rate of return – The accounting rate of return is calculated by dividing the

profit earned by the total investment made for a particular project. The projects whose

accounting rate of return is higher are considered to be more favorable than those having

low required rate of return. However, this technique is not very preferable as it ignores

the concept of time value of money (Fridson & Alvarez, 2012).

Internal rate of return – The discounting rate which equates the amount of cash outflow to

the cash inflow at a particular date is known as internal rate of return. This technique is

very frequently used by the management of the company as it helps to determine the

efficiency of the investment that has been made. If the cost of capital is higher than IRR

then the project might be rejected, and if the IRR exceeds the cost of capital then the

project will be accepted. Time value of money is taken into consideration while

calculating IRR.

Modified rate of return – There is a drawback in the IRR technique that it does not

consider the reinvestment of cash flows. The modified rate of return technique overcomes

this drawback by investing the cash flows at the rate of cost of capital (Rosenfield, 2009).

Profitability Index- The value per unit of investment is calculated with the help of

profitability index.

Capital budgeting is a process carried out for investment appraisal. Investment appraisal is done

to determine whether the fixed capital investments done by the firm is worth it or not. The main

objective of carrying out investment appraisal practice is to maximize the wealth of shareholders

and earn huge profits in the long run.

There are different kinds of investment appraisal techniques available on the basis of investor

and stakeholder’s expectation. The investment appraisal techniques are explained below:

Net present value (NPV) – This technique is used to calculate the net cash flow after the

payment of all committed costs. A company accepts a project only if the forecasted net

present value is positive. The calculation of net present value is done by discounting the

cash flows and at a particular point of time (Schroeder, 2014).

Accounting rate of return – The accounting rate of return is calculated by dividing the

profit earned by the total investment made for a particular project. The projects whose

accounting rate of return is higher are considered to be more favorable than those having

low required rate of return. However, this technique is not very preferable as it ignores

the concept of time value of money (Fridson & Alvarez, 2012).

Internal rate of return – The discounting rate which equates the amount of cash outflow to

the cash inflow at a particular date is known as internal rate of return. This technique is

very frequently used by the management of the company as it helps to determine the

efficiency of the investment that has been made. If the cost of capital is higher than IRR

then the project might be rejected, and if the IRR exceeds the cost of capital then the

project will be accepted. Time value of money is taken into consideration while

calculating IRR.

Modified rate of return – There is a drawback in the IRR technique that it does not

consider the reinvestment of cash flows. The modified rate of return technique overcomes

this drawback by investing the cash flows at the rate of cost of capital (Rosenfield, 2009).

Profitability Index- The value per unit of investment is calculated with the help of

profitability index.

Payback period - The time period in which the company will be able to recover the cost

that it has incurred for a particular project is known as the payback period. This technique

is considered to be the most easy and also shot term projects are considered to be more

preferable than long term projects as per this technique (McLaney & Adril, 2016).

Discounted payback period- This technique is very similar to payback period. The

difference between these two technique is that payback period does not considers time

value of money whereas discounted payback period takes time value of money into

consideration (Girard, 2014).

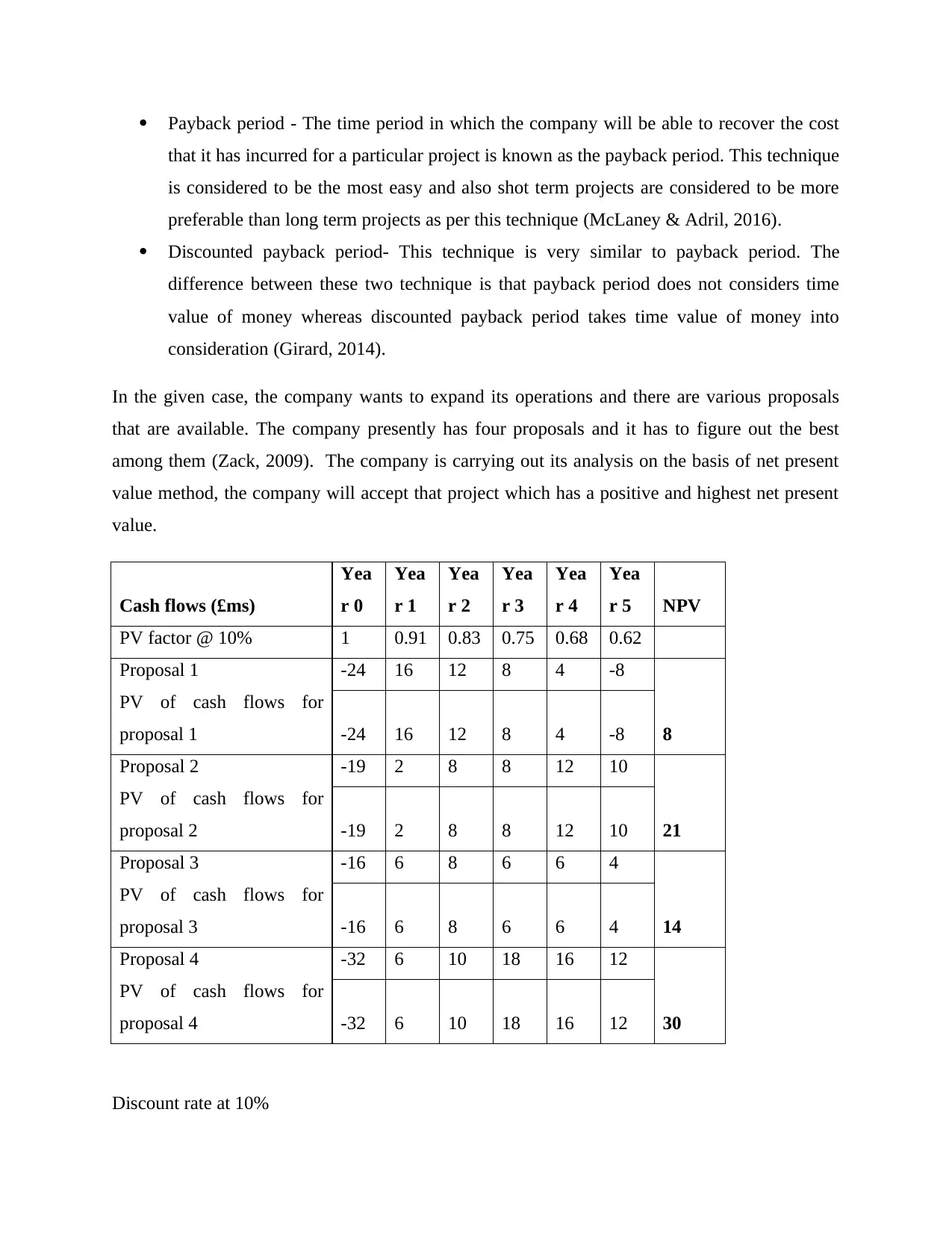

In the given case, the company wants to expand its operations and there are various proposals

that are available. The company presently has four proposals and it has to figure out the best

among them (Zack, 2009). The company is carrying out its analysis on the basis of net present

value method, the company will accept that project which has a positive and highest net present

value.

Cash flows (£ms)

Yea

r 0

Yea

r 1

Yea

r 2

Yea

r 3

Yea

r 4

Yea

r 5 NPV

PV factor @ 10% 1 0.91 0.83 0.75 0.68 0.62

Proposal 1 -24 16 12 8 4 -8

PV of cash flows for

proposal 1 -24 16 12 8 4 -8 8

Proposal 2 -19 2 8 8 12 10

PV of cash flows for

proposal 2 -19 2 8 8 12 10 21

Proposal 3 -16 6 8 6 6 4

PV of cash flows for

proposal 3 -16 6 8 6 6 4 14

Proposal 4 -32 6 10 18 16 12

PV of cash flows for

proposal 4 -32 6 10 18 16 12 30

Discount rate at 10%

that it has incurred for a particular project is known as the payback period. This technique

is considered to be the most easy and also shot term projects are considered to be more

preferable than long term projects as per this technique (McLaney & Adril, 2016).

Discounted payback period- This technique is very similar to payback period. The

difference between these two technique is that payback period does not considers time

value of money whereas discounted payback period takes time value of money into

consideration (Girard, 2014).

In the given case, the company wants to expand its operations and there are various proposals

that are available. The company presently has four proposals and it has to figure out the best

among them (Zack, 2009). The company is carrying out its analysis on the basis of net present

value method, the company will accept that project which has a positive and highest net present

value.

Cash flows (£ms)

Yea

r 0

Yea

r 1

Yea

r 2

Yea

r 3

Yea

r 4

Yea

r 5 NPV

PV factor @ 10% 1 0.91 0.83 0.75 0.68 0.62

Proposal 1 -24 16 12 8 4 -8

PV of cash flows for

proposal 1 -24 16 12 8 4 -8 8

Proposal 2 -19 2 8 8 12 10

PV of cash flows for

proposal 2 -19 2 8 8 12 10 21

Proposal 3 -16 6 8 6 6 4

PV of cash flows for

proposal 3 -16 6 8 6 6 4 14

Proposal 4 -32 6 10 18 16 12

PV of cash flows for

proposal 4 -32 6 10 18 16 12 30

Discount rate at 10%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

0 1.00

1 0.91

2 0.83

3 0.75

4 0.68

5 0.62

The company should accept proposal 4 as it has highest net present value.

1 0.91

2 0.83

3 0.75

4 0.68

5 0.62

The company should accept proposal 4 as it has highest net present value.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Solution 3- Business Plan and budgetary control

The procedures that have to be followed to carry out the business operations are stated in the

business plan developed the operational management of the company. The factors that are to be

considered while setting up a business plan are time duration taken, equipment usage, labor

inefficiencies and the objective of the company (Rayman, 2009). A business plan differentiates

the role that each department has to play individually in order to achieve the objective that has

been set by the company. In the case provided to us, Cucumber ltd has six departments in its

company which have different targets and these targets have to be achieved for fulfilling the

mission of the company (Piper, 2015). The functions business plan for the given case is as

follows:

A business plan acts as a guide in achieving the targets that is planned by the organization

and so it binds the management of the company together to work towards a common

goal.

If the business plan developed by the company is strong then the investors might get

attracted and start investing funds into it (Paul, 2014).

The different business activity along with different levels of managers of employees is

explained in the business plan.

One of the most important components of the management accounting process is the preparation

of budgets. The budget includes estimation of revenues and cost that will be incurred in the

future period. A budget is prepared by the company to control cost and set standards regarding

the revenues of the company. The role of budget is as follows (Pratt, 2009).:

It states the financial as well as operational objective of the business.

It manages the amount of cash that is held along with cash that would be allocated for

carrying out different activities.

The budget helps to set standards in order to compare the actual profits that is generated

by the company.

It also helps in carrying out variance analysis i.e it helps to determine the difference

between the actual cost and estimated cost.

The procedures that have to be followed to carry out the business operations are stated in the

business plan developed the operational management of the company. The factors that are to be

considered while setting up a business plan are time duration taken, equipment usage, labor

inefficiencies and the objective of the company (Rayman, 2009). A business plan differentiates

the role that each department has to play individually in order to achieve the objective that has

been set by the company. In the case provided to us, Cucumber ltd has six departments in its

company which have different targets and these targets have to be achieved for fulfilling the

mission of the company (Piper, 2015). The functions business plan for the given case is as

follows:

A business plan acts as a guide in achieving the targets that is planned by the organization

and so it binds the management of the company together to work towards a common

goal.

If the business plan developed by the company is strong then the investors might get

attracted and start investing funds into it (Paul, 2014).

The different business activity along with different levels of managers of employees is

explained in the business plan.

One of the most important components of the management accounting process is the preparation

of budgets. The budget includes estimation of revenues and cost that will be incurred in the

future period. A budget is prepared by the company to control cost and set standards regarding

the revenues of the company. The role of budget is as follows (Pratt, 2009).:

It states the financial as well as operational objective of the business.

It manages the amount of cash that is held along with cash that would be allocated for

carrying out different activities.

The budget helps to set standards in order to compare the actual profits that is generated

by the company.

It also helps in carrying out variance analysis i.e it helps to determine the difference

between the actual cost and estimated cost.

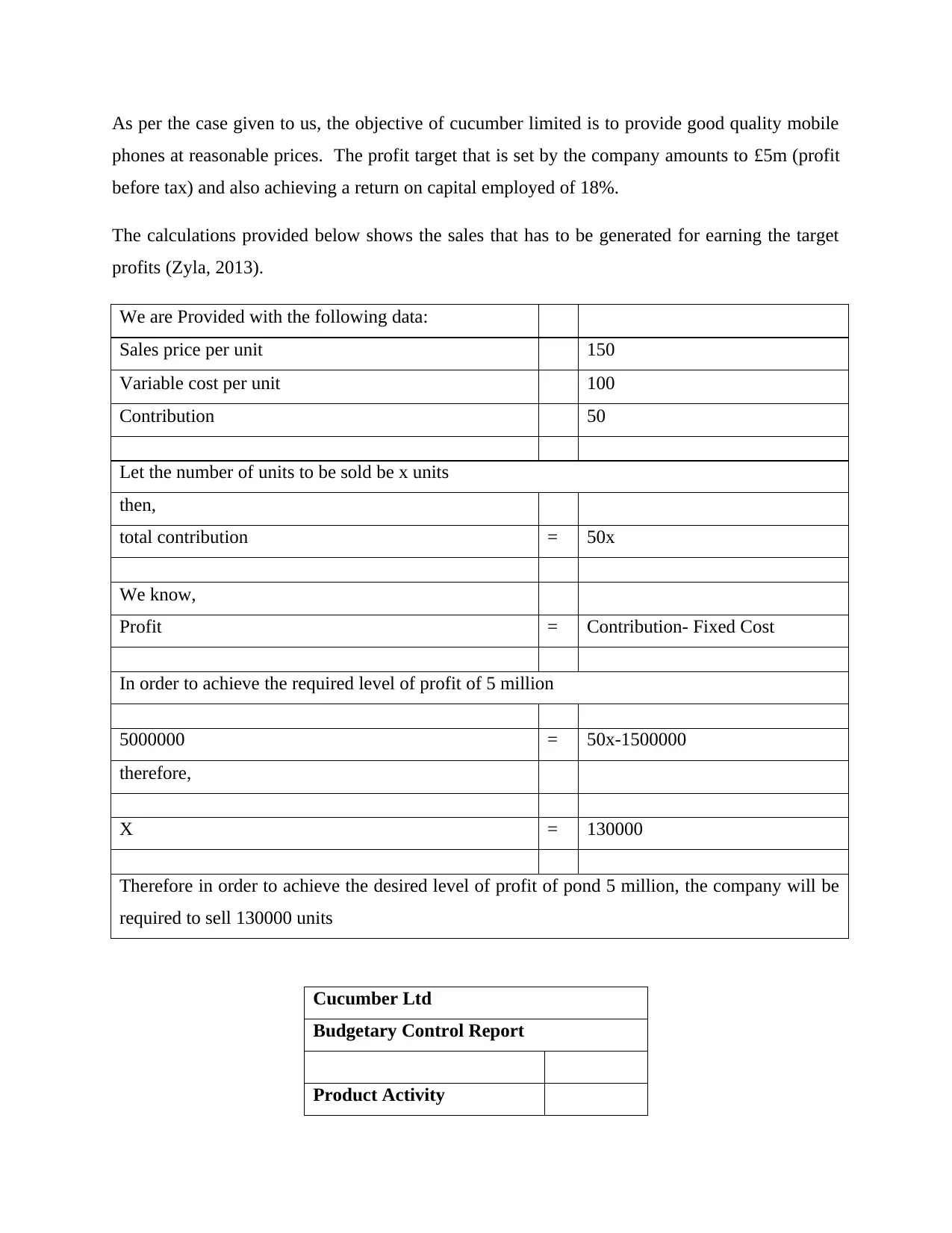

As per the case given to us, the objective of cucumber limited is to provide good quality mobile

phones at reasonable prices. The profit target that is set by the company amounts to £5m (profit

before tax) and also achieving a return on capital employed of 18%.

The calculations provided below shows the sales that has to be generated for earning the target

profits (Zyla, 2013).

We are Provided with the following data:

Sales price per unit 150

Variable cost per unit 100

Contribution 50

Let the number of units to be sold be x units

then,

total contribution = 50x

We know,

Profit = Contribution- Fixed Cost

In order to achieve the required level of profit of 5 million

5000000 = 50x-1500000

therefore,

X = 130000

Therefore in order to achieve the desired level of profit of pond 5 million, the company will be

required to sell 130000 units

Cucumber Ltd

Budgetary Control Report

Product Activity

phones at reasonable prices. The profit target that is set by the company amounts to £5m (profit

before tax) and also achieving a return on capital employed of 18%.

The calculations provided below shows the sales that has to be generated for earning the target

profits (Zyla, 2013).

We are Provided with the following data:

Sales price per unit 150

Variable cost per unit 100

Contribution 50

Let the number of units to be sold be x units

then,

total contribution = 50x

We know,

Profit = Contribution- Fixed Cost

In order to achieve the required level of profit of 5 million

5000000 = 50x-1500000

therefore,

X = 130000

Therefore in order to achieve the desired level of profit of pond 5 million, the company will be

required to sell 130000 units

Cucumber Ltd

Budgetary Control Report

Product Activity

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

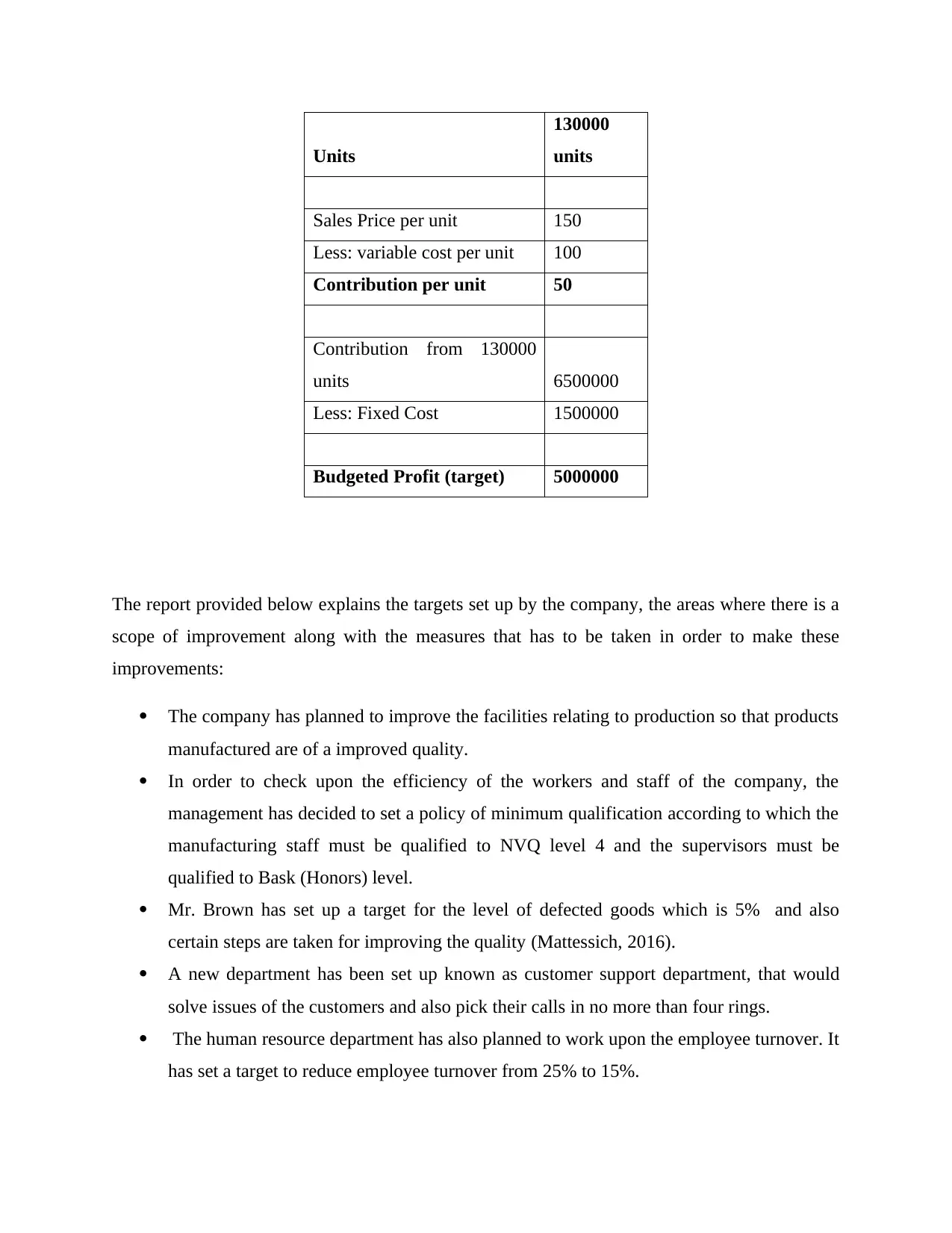

Units

130000

units

Sales Price per unit 150

Less: variable cost per unit 100

Contribution per unit 50

Contribution from 130000

units 6500000

Less: Fixed Cost 1500000

Budgeted Profit (target) 5000000

The report provided below explains the targets set up by the company, the areas where there is a

scope of improvement along with the measures that has to be taken in order to make these

improvements:

The company has planned to improve the facilities relating to production so that products

manufactured are of a improved quality.

In order to check upon the efficiency of the workers and staff of the company, the

management has decided to set a policy of minimum qualification according to which the

manufacturing staff must be qualified to NVQ level 4 and the supervisors must be

qualified to Bask (Honors) level.

Mr. Brown has set up a target for the level of defected goods which is 5% and also

certain steps are taken for improving the quality (Mattessich, 2016).

A new department has been set up known as customer support department, that would

solve issues of the customers and also pick their calls in no more than four rings.

The human resource department has also planned to work upon the employee turnover. It

has set a target to reduce employee turnover from 25% to 15%.

130000

units

Sales Price per unit 150

Less: variable cost per unit 100

Contribution per unit 50

Contribution from 130000

units 6500000

Less: Fixed Cost 1500000

Budgeted Profit (target) 5000000

The report provided below explains the targets set up by the company, the areas where there is a

scope of improvement along with the measures that has to be taken in order to make these

improvements:

The company has planned to improve the facilities relating to production so that products

manufactured are of a improved quality.

In order to check upon the efficiency of the workers and staff of the company, the

management has decided to set a policy of minimum qualification according to which the

manufacturing staff must be qualified to NVQ level 4 and the supervisors must be

qualified to Bask (Honors) level.

Mr. Brown has set up a target for the level of defected goods which is 5% and also

certain steps are taken for improving the quality (Mattessich, 2016).

A new department has been set up known as customer support department, that would

solve issues of the customers and also pick their calls in no more than four rings.

The human resource department has also planned to work upon the employee turnover. It

has set a target to reduce employee turnover from 25% to 15%.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

A survey would be done after 4 weeks the sales has been made as it would help them to

the level of satisfaction it is providing to the customers. However, the company plans to

achieve excellent rating from 80% of the customers to which he has sold the products.

There is no well explained budgetary plan set by the company because of which the sales

target cannot be set. The company has chosen to use breakeven cost analysis as its cost

model in order to determine the breakeven sales. The sales target that has been set by the

company is earnings before tax $5m.

The cost centre shows that there is a negative variance of screen product which has a

higher degree of concern and which has a scope of improvement. It shows that the actual

production (4000 units) exceed the forecasted units of production which is 3000 units.

This increased production increases the cost of production thereby increasing the cost per

unit. We all know that an extra production made by the company leads to suffer negative

variances. For example, the material cost per unit as per the budget was 9.75 whereas it

has increased to 10.33 due to extra production.

the level of satisfaction it is providing to the customers. However, the company plans to

achieve excellent rating from 80% of the customers to which he has sold the products.

There is no well explained budgetary plan set by the company because of which the sales

target cannot be set. The company has chosen to use breakeven cost analysis as its cost

model in order to determine the breakeven sales. The sales target that has been set by the

company is earnings before tax $5m.

The cost centre shows that there is a negative variance of screen product which has a

higher degree of concern and which has a scope of improvement. It shows that the actual

production (4000 units) exceed the forecasted units of production which is 3000 units.

This increased production increases the cost of production thereby increasing the cost per

unit. We all know that an extra production made by the company leads to suffer negative

variances. For example, the material cost per unit as per the budget was 9.75 whereas it

has increased to 10.33 due to extra production.

Solution 4 – Balanced scorecard approach

Balanced Scorecard is an approach used in the strategic management to evaluate the performance

of various activities and functions of the entity and proposing the improvements and analyzing

the outcomes (Paul, 2014). It is a measure to provide the information to the business enterprises

regarding both qualitative and quantitative information which are used by the top level

management of the enterprise to make decisions in a better way for the entity (Piper, 2015). The

balanced scorecard focuses on the four areas which can be summarized as below:

This approach is used as a part of strategic management; it is used for the evaluation of

performance. This approach provides qualitative as well as quantitative information to the

management of the company which uses such information for the process of decision making.

There are four areas that are mainly focused in balanced scorecard approach which are explained

below:

1. Profitability from financial perspective- This perspective tells us the process if

implementing and executing such strategies and how this strategy helps in improving the

workings of the company.

2. Customer satisfaction from customer prospective- This strategy deals with providing best

facilities and products to the customers and maximizing their wealth to the extent

possible. It helps the business to survive in the long run.

3. Internal business perspective – The policy and procedures and their stability is considered

in this perspective. This approach helps to narrow the gap between customer and

financial perspective.

4. Learning as well as growth perspective – The training as well as improvement of

efficiency of labor is considered in this strategy. It assumes that the labor is skilled and

knowledgeable enough to meet the targets of the company.

Balanced Scorecard is an approach used in the strategic management to evaluate the performance

of various activities and functions of the entity and proposing the improvements and analyzing

the outcomes (Paul, 2014). It is a measure to provide the information to the business enterprises

regarding both qualitative and quantitative information which are used by the top level

management of the enterprise to make decisions in a better way for the entity (Piper, 2015). The

balanced scorecard focuses on the four areas which can be summarized as below:

This approach is used as a part of strategic management; it is used for the evaluation of

performance. This approach provides qualitative as well as quantitative information to the

management of the company which uses such information for the process of decision making.

There are four areas that are mainly focused in balanced scorecard approach which are explained

below:

1. Profitability from financial perspective- This perspective tells us the process if

implementing and executing such strategies and how this strategy helps in improving the

workings of the company.

2. Customer satisfaction from customer prospective- This strategy deals with providing best

facilities and products to the customers and maximizing their wealth to the extent

possible. It helps the business to survive in the long run.

3. Internal business perspective – The policy and procedures and their stability is considered

in this perspective. This approach helps to narrow the gap between customer and

financial perspective.

4. Learning as well as growth perspective – The training as well as improvement of

efficiency of labor is considered in this strategy. It assumes that the labor is skilled and

knowledgeable enough to meet the targets of the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.