MAPM5029 Management Accounting and Performance: Cost & Budget Report

VerifiedAdded on 2023/04/17

|11

|2922

|239

Report

AI Summary

This management accounting report analyzes the cost and revenue structure of a cookie manufacturing business, Kkrunchies Cookies, including a break-even analysis. It details the introduction of the business, market analysis, target market size, and penetration strategies. The report discusses various funding strategies such as debts, asset financing, equity, and mortgage. It computes the break-even point by evaluating fixed and variable costs, presenting a cost structure that includes branding, staffing, fixed input costs, and variable input costs. The analysis includes considerations for attracting and retaining customers, focusing on tourists, children, local residents, and working professionals. The report uses assumptions regarding cost structure, revenue, demand, and supply to provide a comprehensive financial overview.

UNIVERSITY NAME Australia

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

SECTION A...................................................................................................................................................2

(A) INTRODUCTION.................................................................................................................................2

(B) STRUCTURE OF COST AND REVENUE.................................................................................................3

(C ) BREAK EVEN ANALYSIS.....................................................................................................................5

(D) CONCLUSION.....................................................................................................................................7

SECTION B....................................................................................................................................................8

(A) COST STATEMENT..............................................................................................................................8

(B) OPERATING BUDGET.........................................................................................................................8

(C) CASH FLOW BUDGET..........................................................................................................................9

References.................................................................................................................................................10

SECTION A...................................................................................................................................................2

(A) INTRODUCTION.................................................................................................................................2

(B) STRUCTURE OF COST AND REVENUE.................................................................................................3

(C ) BREAK EVEN ANALYSIS.....................................................................................................................5

(D) CONCLUSION.....................................................................................................................................7

SECTION B....................................................................................................................................................8

(A) COST STATEMENT..............................................................................................................................8

(B) OPERATING BUDGET.........................................................................................................................8

(C) CASH FLOW BUDGET..........................................................................................................................9

References.................................................................................................................................................10

SECTION A

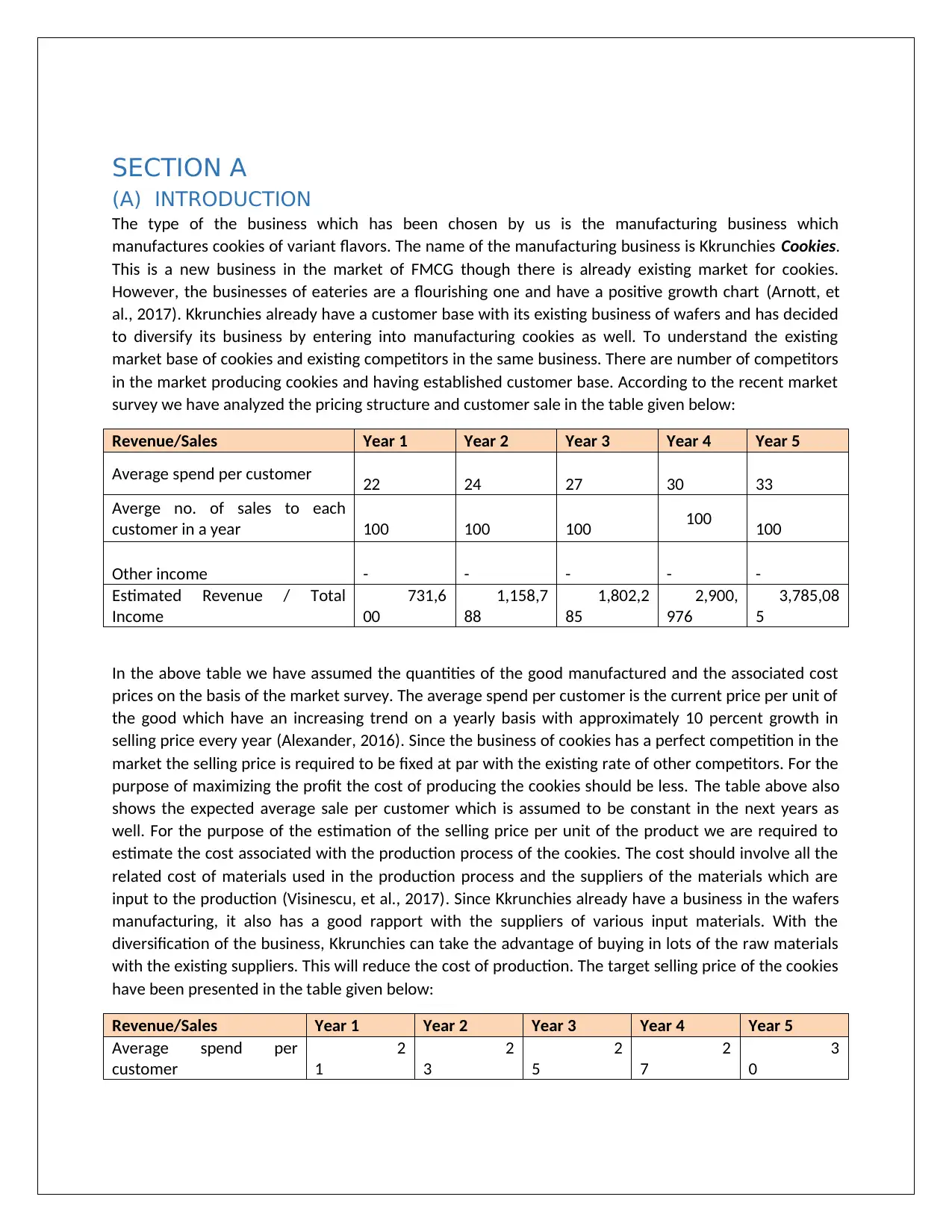

(A) INTRODUCTION

The type of the business which has been chosen by us is the manufacturing business which

manufactures cookies of variant flavors. The name of the manufacturing business is Kkrunchies Cookies.

This is a new business in the market of FMCG though there is already existing market for cookies.

However, the businesses of eateries are a flourishing one and have a positive growth chart (Arnott, et

al., 2017). Kkrunchies already have a customer base with its existing business of wafers and has decided

to diversify its business by entering into manufacturing cookies as well. To understand the existing

market base of cookies and existing competitors in the same business. There are number of competitors

in the market producing cookies and having established customer base. According to the recent market

survey we have analyzed the pricing structure and customer sale in the table given below:

Revenue/Sales Year 1 Year 2 Year 3 Year 4 Year 5

Average spend per customer 22 24 27 30 33

Averge no. of sales to each

customer in a year 100 100 100 100 100

Other income - - - - -

Estimated Revenue / Total

Income

731,6

00

1,158,7

88

1,802,2

85

2,900,

976

3,785,08

5

In the above table we have assumed the quantities of the good manufactured and the associated cost

prices on the basis of the market survey. The average spend per customer is the current price per unit of

the good which have an increasing trend on a yearly basis with approximately 10 percent growth in

selling price every year (Alexander, 2016). Since the business of cookies has a perfect competition in the

market the selling price is required to be fixed at par with the existing rate of other competitors. For the

purpose of maximizing the profit the cost of producing the cookies should be less. The table above also

shows the expected average sale per customer which is assumed to be constant in the next years as

well. For the purpose of the estimation of the selling price per unit of the product we are required to

estimate the cost associated with the production process of the cookies. The cost should involve all the

related cost of materials used in the production process and the suppliers of the materials which are

input to the production (Visinescu, et al., 2017). Since Kkrunchies already have a business in the wafers

manufacturing, it also has a good rapport with the suppliers of various input materials. With the

diversification of the business, Kkrunchies can take the advantage of buying in lots of the raw materials

with the existing suppliers. This will reduce the cost of production. The target selling price of the cookies

have been presented in the table given below:

Revenue/Sales Year 1 Year 2 Year 3 Year 4 Year 5

Average spend per

customer

2

1

2

3

2

5

2

7

3

0

(A) INTRODUCTION

The type of the business which has been chosen by us is the manufacturing business which

manufactures cookies of variant flavors. The name of the manufacturing business is Kkrunchies Cookies.

This is a new business in the market of FMCG though there is already existing market for cookies.

However, the businesses of eateries are a flourishing one and have a positive growth chart (Arnott, et

al., 2017). Kkrunchies already have a customer base with its existing business of wafers and has decided

to diversify its business by entering into manufacturing cookies as well. To understand the existing

market base of cookies and existing competitors in the same business. There are number of competitors

in the market producing cookies and having established customer base. According to the recent market

survey we have analyzed the pricing structure and customer sale in the table given below:

Revenue/Sales Year 1 Year 2 Year 3 Year 4 Year 5

Average spend per customer 22 24 27 30 33

Averge no. of sales to each

customer in a year 100 100 100 100 100

Other income - - - - -

Estimated Revenue / Total

Income

731,6

00

1,158,7

88

1,802,2

85

2,900,

976

3,785,08

5

In the above table we have assumed the quantities of the good manufactured and the associated cost

prices on the basis of the market survey. The average spend per customer is the current price per unit of

the good which have an increasing trend on a yearly basis with approximately 10 percent growth in

selling price every year (Alexander, 2016). Since the business of cookies has a perfect competition in the

market the selling price is required to be fixed at par with the existing rate of other competitors. For the

purpose of maximizing the profit the cost of producing the cookies should be less. The table above also

shows the expected average sale per customer which is assumed to be constant in the next years as

well. For the purpose of the estimation of the selling price per unit of the product we are required to

estimate the cost associated with the production process of the cookies. The cost should involve all the

related cost of materials used in the production process and the suppliers of the materials which are

input to the production (Visinescu, et al., 2017). Since Kkrunchies already have a business in the wafers

manufacturing, it also has a good rapport with the suppliers of various input materials. With the

diversification of the business, Kkrunchies can take the advantage of buying in lots of the raw materials

with the existing suppliers. This will reduce the cost of production. The target selling price of the cookies

have been presented in the table given below:

Revenue/Sales Year 1 Year 2 Year 3 Year 4 Year 5

Average spend per

customer

2

1

2

3

2

5

2

7

3

0

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

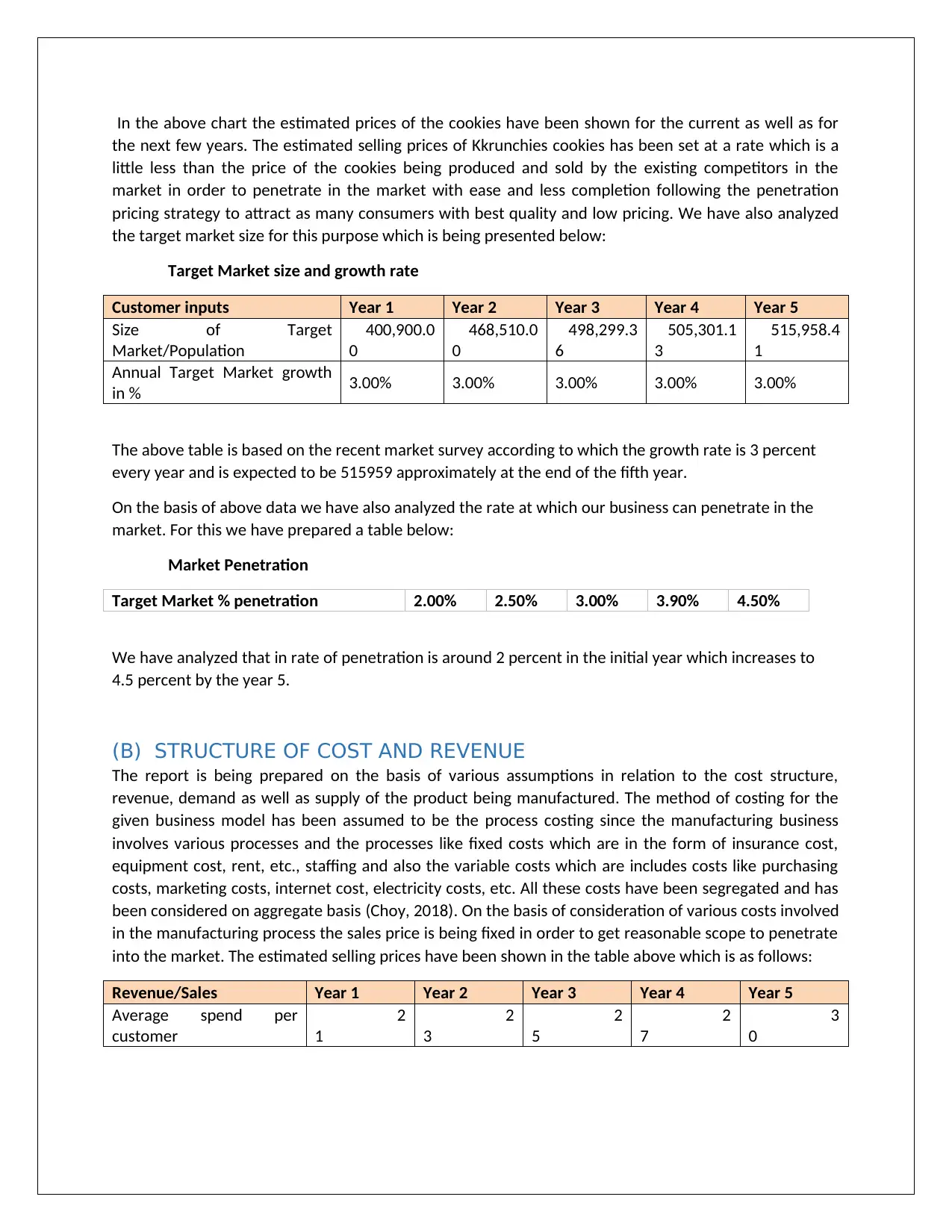

In the above chart the estimated prices of the cookies have been shown for the current as well as for

the next few years. The estimated selling prices of Kkrunchies cookies has been set at a rate which is a

little less than the price of the cookies being produced and sold by the existing competitors in the

market in order to penetrate in the market with ease and less completion following the penetration

pricing strategy to attract as many consumers with best quality and low pricing. We have also analyzed

the target market size for this purpose which is being presented below:

Target Market size and growth rate

Customer inputs Year 1 Year 2 Year 3 Year 4 Year 5

Size of Target

Market/Population

400,900.0

0

468,510.0

0

498,299.3

6

505,301.1

3

515,958.4

1

Annual Target Market growth

in % 3.00% 3.00% 3.00% 3.00% 3.00%

The above table is based on the recent market survey according to which the growth rate is 3 percent

every year and is expected to be 515959 approximately at the end of the fifth year.

On the basis of above data we have also analyzed the rate at which our business can penetrate in the

market. For this we have prepared a table below:

Market Penetration

Target Market % penetration 2.00% 2.50% 3.00% 3.90% 4.50%

We have analyzed that in rate of penetration is around 2 percent in the initial year which increases to

4.5 percent by the year 5.

(B) STRUCTURE OF COST AND REVENUE

The report is being prepared on the basis of various assumptions in relation to the cost structure,

revenue, demand as well as supply of the product being manufactured. The method of costing for the

given business model has been assumed to be the process costing since the manufacturing business

involves various processes and the processes like fixed costs which are in the form of insurance cost,

equipment cost, rent, etc., staffing and also the variable costs which are includes costs like purchasing

costs, marketing costs, internet cost, electricity costs, etc. All these costs have been segregated and has

been considered on aggregate basis (Choy, 2018). On the basis of consideration of various costs involved

in the manufacturing process the sales price is being fixed in order to get reasonable scope to penetrate

into the market. The estimated selling prices have been shown in the table above which is as follows:

Revenue/Sales Year 1 Year 2 Year 3 Year 4 Year 5

Average spend per

customer

2

1

2

3

2

5

2

7

3

0

the next few years. The estimated selling prices of Kkrunchies cookies has been set at a rate which is a

little less than the price of the cookies being produced and sold by the existing competitors in the

market in order to penetrate in the market with ease and less completion following the penetration

pricing strategy to attract as many consumers with best quality and low pricing. We have also analyzed

the target market size for this purpose which is being presented below:

Target Market size and growth rate

Customer inputs Year 1 Year 2 Year 3 Year 4 Year 5

Size of Target

Market/Population

400,900.0

0

468,510.0

0

498,299.3

6

505,301.1

3

515,958.4

1

Annual Target Market growth

in % 3.00% 3.00% 3.00% 3.00% 3.00%

The above table is based on the recent market survey according to which the growth rate is 3 percent

every year and is expected to be 515959 approximately at the end of the fifth year.

On the basis of above data we have also analyzed the rate at which our business can penetrate in the

market. For this we have prepared a table below:

Market Penetration

Target Market % penetration 2.00% 2.50% 3.00% 3.90% 4.50%

We have analyzed that in rate of penetration is around 2 percent in the initial year which increases to

4.5 percent by the year 5.

(B) STRUCTURE OF COST AND REVENUE

The report is being prepared on the basis of various assumptions in relation to the cost structure,

revenue, demand as well as supply of the product being manufactured. The method of costing for the

given business model has been assumed to be the process costing since the manufacturing business

involves various processes and the processes like fixed costs which are in the form of insurance cost,

equipment cost, rent, etc., staffing and also the variable costs which are includes costs like purchasing

costs, marketing costs, internet cost, electricity costs, etc. All these costs have been segregated and has

been considered on aggregate basis (Choy, 2018). On the basis of consideration of various costs involved

in the manufacturing process the sales price is being fixed in order to get reasonable scope to penetrate

into the market. The estimated selling prices have been shown in the table above which is as follows:

Revenue/Sales Year 1 Year 2 Year 3 Year 4 Year 5

Average spend per

customer

2

1

2

3

2

5

2

7

3

0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

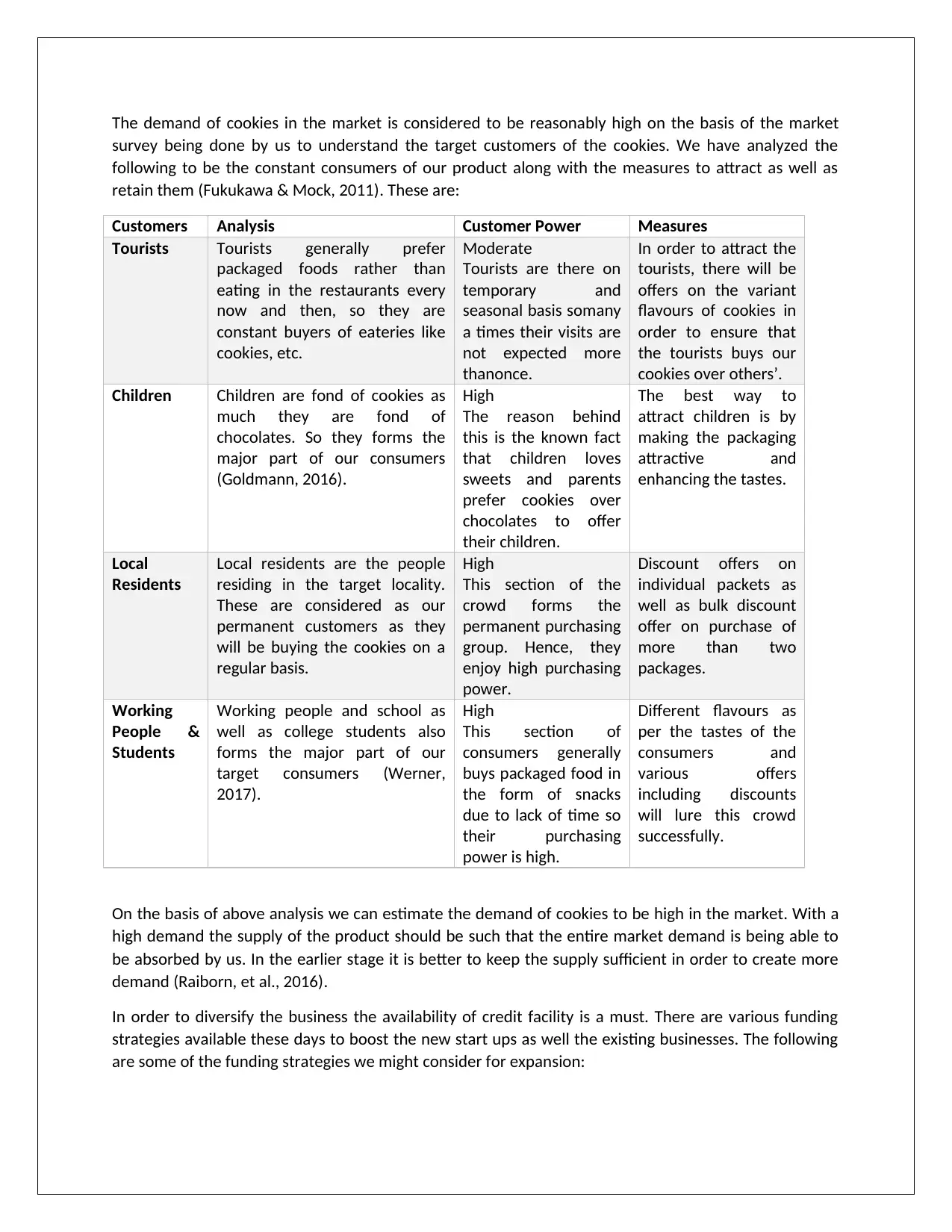

The demand of cookies in the market is considered to be reasonably high on the basis of the market

survey being done by us to understand the target customers of the cookies. We have analyzed the

following to be the constant consumers of our product along with the measures to attract as well as

retain them (Fukukawa & Mock, 2011). These are:

Customers Analysis Customer Power Measures

Tourists Tourists generally prefer

packaged foods rather than

eating in the restaurants every

now and then, so they are

constant buyers of eateries like

cookies, etc.

Moderate

Tourists are there on

temporary and

seasonal basis somany

a times their visits are

not expected more

thanonce.

In order to attract the

tourists, there will be

offers on the variant

flavours of cookies in

order to ensure that

the tourists buys our

cookies over others’.

Children Children are fond of cookies as

much they are fond of

chocolates. So they forms the

major part of our consumers

(Goldmann, 2016).

High

The reason behind

this is the known fact

that children loves

sweets and parents

prefer cookies over

chocolates to offer

their children.

The best way to

attract children is by

making the packaging

attractive and

enhancing the tastes.

Local

Residents

Local residents are the people

residing in the target locality.

These are considered as our

permanent customers as they

will be buying the cookies on a

regular basis.

High

This section of the

crowd forms the

permanent purchasing

group. Hence, they

enjoy high purchasing

power.

Discount offers on

individual packets as

well as bulk discount

offer on purchase of

more than two

packages.

Working

People &

Students

Working people and school as

well as college students also

forms the major part of our

target consumers (Werner,

2017).

High

This section of

consumers generally

buys packaged food in

the form of snacks

due to lack of time so

their purchasing

power is high.

Different flavours as

per the tastes of the

consumers and

various offers

including discounts

will lure this crowd

successfully.

On the basis of above analysis we can estimate the demand of cookies to be high in the market. With a

high demand the supply of the product should be such that the entire market demand is being able to

be absorbed by us. In the earlier stage it is better to keep the supply sufficient in order to create more

demand (Raiborn, et al., 2016).

In order to diversify the business the availability of credit facility is a must. There are various funding

strategies available these days to boost the new start ups as well the existing businesses. The following

are some of the funding strategies we might consider for expansion:

survey being done by us to understand the target customers of the cookies. We have analyzed the

following to be the constant consumers of our product along with the measures to attract as well as

retain them (Fukukawa & Mock, 2011). These are:

Customers Analysis Customer Power Measures

Tourists Tourists generally prefer

packaged foods rather than

eating in the restaurants every

now and then, so they are

constant buyers of eateries like

cookies, etc.

Moderate

Tourists are there on

temporary and

seasonal basis somany

a times their visits are

not expected more

thanonce.

In order to attract the

tourists, there will be

offers on the variant

flavours of cookies in

order to ensure that

the tourists buys our

cookies over others’.

Children Children are fond of cookies as

much they are fond of

chocolates. So they forms the

major part of our consumers

(Goldmann, 2016).

High

The reason behind

this is the known fact

that children loves

sweets and parents

prefer cookies over

chocolates to offer

their children.

The best way to

attract children is by

making the packaging

attractive and

enhancing the tastes.

Local

Residents

Local residents are the people

residing in the target locality.

These are considered as our

permanent customers as they

will be buying the cookies on a

regular basis.

High

This section of the

crowd forms the

permanent purchasing

group. Hence, they

enjoy high purchasing

power.

Discount offers on

individual packets as

well as bulk discount

offer on purchase of

more than two

packages.

Working

People &

Students

Working people and school as

well as college students also

forms the major part of our

target consumers (Werner,

2017).

High

This section of

consumers generally

buys packaged food in

the form of snacks

due to lack of time so

their purchasing

power is high.

Different flavours as

per the tastes of the

consumers and

various offers

including discounts

will lure this crowd

successfully.

On the basis of above analysis we can estimate the demand of cookies to be high in the market. With a

high demand the supply of the product should be such that the entire market demand is being able to

be absorbed by us. In the earlier stage it is better to keep the supply sufficient in order to create more

demand (Raiborn, et al., 2016).

In order to diversify the business the availability of credit facility is a must. There are various funding

strategies available these days to boost the new start ups as well the existing businesses. The following

are some of the funding strategies we might consider for expansion:

Debts

Debt is the type of capital which is very commonly known as the loan capital. There are various

types of debts in the market. The most common modes are loans from various financial

institutions like banking as well as non banking institutions, issue of bonds and debentures, etc.

In case of debt financing the credit facility is being given at a fixed rate of interest (Heminway,

2017). As the name suggests it is fixed in nature irrespective of the amount of profit being

earned, which is considered to be biggest disadvantage in this kind of funding.

Financing through Assets

This type of credit facility is most commonly known as Asset Financing. Under this method of

financing the assets of the company are being used to raise working capital loans as well as

short term loans. This kind of credit facility is being provided by various kinds of financing and

asset restructuring companies which may provide the credit facility using assets like fixed assets,

receivables, etc. Though this kind of credit facility is currently not being considered by us for the

cookies business (Jefferson, 2017).

Equity

Equity is the most cost effective mode of funding as it involves lower cash outflow. This refers to

the owners’ fund. In the business of producing cookies this is the best mode of funding since the

controlling power will vest in the hands of owners only and profit will also be shared among the

owners (Kew & Stredwick, 2017).

Mortgage

Under the mortgage method of funding the company enters into an agreement with the

financial institution providing the credit facility to the company whereby the ownership of the

building is transferred in lieu of the loan to the financial institution providing the credit facility.

This mode of credit facility is not being considered in the business of cookies.

(C ) BREAK EVEN ANALYSIS

Break even point is the point at which the total revenue equals the total cost. The break even point can

be determined by evaluating the total costs and total revenue. For the computation of total costs we

have assumed the occurrence of all the relevant fixed as well as variable expenditures. On the basis of

this data we have arrived at the total cost which is being presented in the chart below along with the

total estimated revenue of the cookies business (Linden & Freeman, 2017).

The cost structure of the cookies business is given in the below table:

Branding & Advertisement Year 1 Year 2 Year 3 Year 4 Year 5

Brochures 3,00

0

3,00

0

3,00

0

3,00

0

3,00

0

Advertising and marketing 10,4

07

12,68

2

18,53

0

22,01

3

28,97

6

Total 13,4

07

15,68

2

21,53

0

25,01

3

31,97

6

Debt is the type of capital which is very commonly known as the loan capital. There are various

types of debts in the market. The most common modes are loans from various financial

institutions like banking as well as non banking institutions, issue of bonds and debentures, etc.

In case of debt financing the credit facility is being given at a fixed rate of interest (Heminway,

2017). As the name suggests it is fixed in nature irrespective of the amount of profit being

earned, which is considered to be biggest disadvantage in this kind of funding.

Financing through Assets

This type of credit facility is most commonly known as Asset Financing. Under this method of

financing the assets of the company are being used to raise working capital loans as well as

short term loans. This kind of credit facility is being provided by various kinds of financing and

asset restructuring companies which may provide the credit facility using assets like fixed assets,

receivables, etc. Though this kind of credit facility is currently not being considered by us for the

cookies business (Jefferson, 2017).

Equity

Equity is the most cost effective mode of funding as it involves lower cash outflow. This refers to

the owners’ fund. In the business of producing cookies this is the best mode of funding since the

controlling power will vest in the hands of owners only and profit will also be shared among the

owners (Kew & Stredwick, 2017).

Mortgage

Under the mortgage method of funding the company enters into an agreement with the

financial institution providing the credit facility to the company whereby the ownership of the

building is transferred in lieu of the loan to the financial institution providing the credit facility.

This mode of credit facility is not being considered in the business of cookies.

(C ) BREAK EVEN ANALYSIS

Break even point is the point at which the total revenue equals the total cost. The break even point can

be determined by evaluating the total costs and total revenue. For the computation of total costs we

have assumed the occurrence of all the relevant fixed as well as variable expenditures. On the basis of

this data we have arrived at the total cost which is being presented in the chart below along with the

total estimated revenue of the cookies business (Linden & Freeman, 2017).

The cost structure of the cookies business is given in the below table:

Branding & Advertisement Year 1 Year 2 Year 3 Year 4 Year 5

Brochures 3,00

0

3,00

0

3,00

0

3,00

0

3,00

0

Advertising and marketing 10,4

07

12,68

2

18,53

0

22,01

3

28,97

6

Total 13,4

07

15,68

2

21,53

0

25,01

3

31,97

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

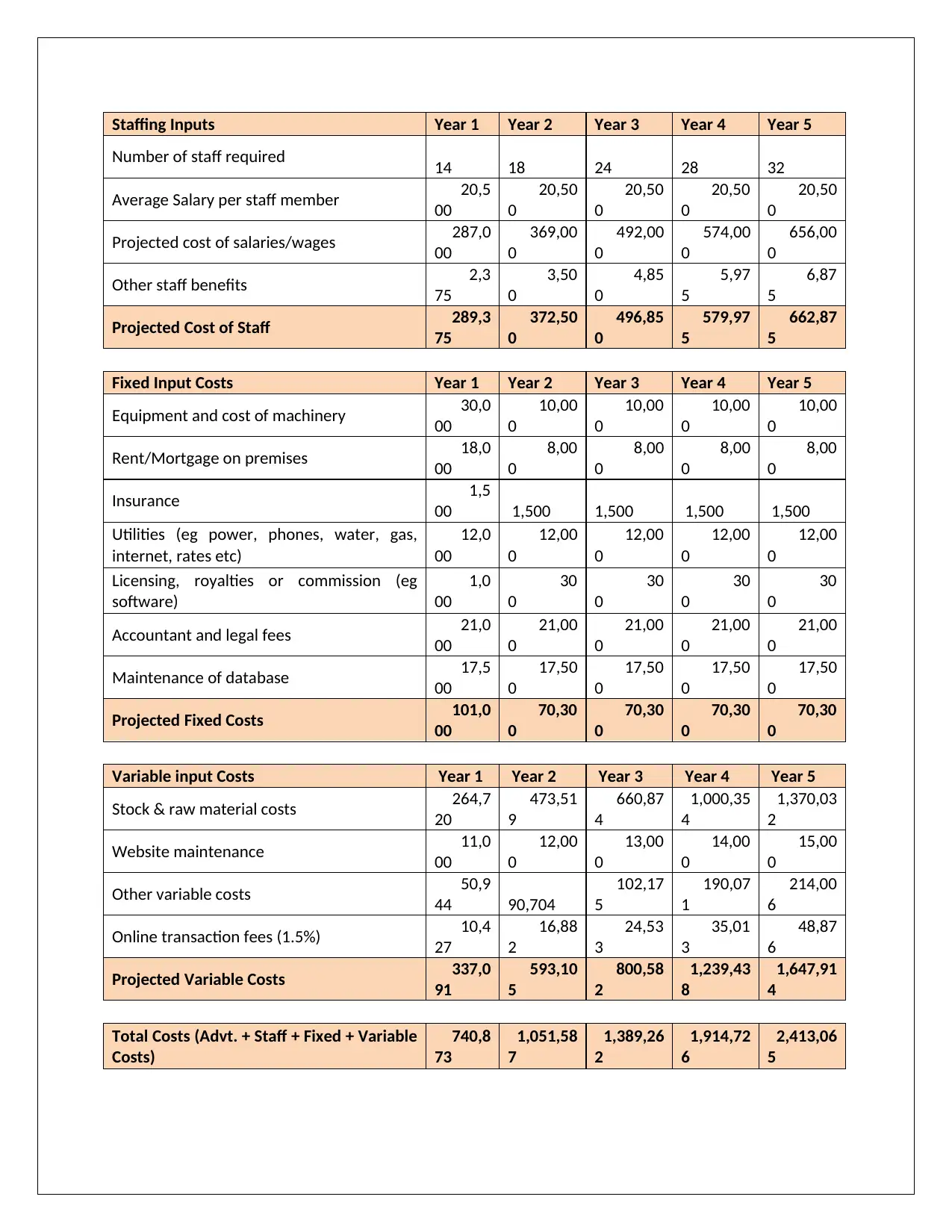

Staffing Inputs Year 1 Year 2 Year 3 Year 4 Year 5

Number of staff required 14 18 24 28 32

Average Salary per staff member 20,5

00

20,50

0

20,50

0

20,50

0

20,50

0

Projected cost of salaries/wages 287,0

00

369,00

0

492,00

0

574,00

0

656,00

0

Other staff benefits 2,3

75

3,50

0

4,85

0

5,97

5

6,87

5

Projected Cost of Staff 289,3

75

372,50

0

496,85

0

579,97

5

662,87

5

Fixed Input Costs Year 1 Year 2 Year 3 Year 4 Year 5

Equipment and cost of machinery 30,0

00

10,00

0

10,00

0

10,00

0

10,00

0

Rent/Mortgage on premises 18,0

00

8,00

0

8,00

0

8,00

0

8,00

0

Insurance 1,5

00 1,500 1,500 1,500 1,500

Utilities (eg power, phones, water, gas,

internet, rates etc)

12,0

00

12,00

0

12,00

0

12,00

0

12,00

0

Licensing, royalties or commission (eg

software)

1,0

00

30

0

30

0

30

0

30

0

Accountant and legal fees 21,0

00

21,00

0

21,00

0

21,00

0

21,00

0

Maintenance of database 17,5

00

17,50

0

17,50

0

17,50

0

17,50

0

Projected Fixed Costs 101,0

00

70,30

0

70,30

0

70,30

0

70,30

0

Variable input Costs Year 1 Year 2 Year 3 Year 4 Year 5

Stock & raw material costs 264,7

20

473,51

9

660,87

4

1,000,35

4

1,370,03

2

Website maintenance 11,0

00

12,00

0

13,00

0

14,00

0

15,00

0

Other variable costs 50,9

44 90,704

102,17

5

190,07

1

214,00

6

Online transaction fees (1.5%) 10,4

27

16,88

2

24,53

3

35,01

3

48,87

6

Projected Variable Costs 337,0

91

593,10

5

800,58

2

1,239,43

8

1,647,91

4

Total Costs (Advt. + Staff + Fixed + Variable

Costs)

740,8

73

1,051,58

7

1,389,26

2

1,914,72

6

2,413,06

5

Number of staff required 14 18 24 28 32

Average Salary per staff member 20,5

00

20,50

0

20,50

0

20,50

0

20,50

0

Projected cost of salaries/wages 287,0

00

369,00

0

492,00

0

574,00

0

656,00

0

Other staff benefits 2,3

75

3,50

0

4,85

0

5,97

5

6,87

5

Projected Cost of Staff 289,3

75

372,50

0

496,85

0

579,97

5

662,87

5

Fixed Input Costs Year 1 Year 2 Year 3 Year 4 Year 5

Equipment and cost of machinery 30,0

00

10,00

0

10,00

0

10,00

0

10,00

0

Rent/Mortgage on premises 18,0

00

8,00

0

8,00

0

8,00

0

8,00

0

Insurance 1,5

00 1,500 1,500 1,500 1,500

Utilities (eg power, phones, water, gas,

internet, rates etc)

12,0

00

12,00

0

12,00

0

12,00

0

12,00

0

Licensing, royalties or commission (eg

software)

1,0

00

30

0

30

0

30

0

30

0

Accountant and legal fees 21,0

00

21,00

0

21,00

0

21,00

0

21,00

0

Maintenance of database 17,5

00

17,50

0

17,50

0

17,50

0

17,50

0

Projected Fixed Costs 101,0

00

70,30

0

70,30

0

70,30

0

70,30

0

Variable input Costs Year 1 Year 2 Year 3 Year 4 Year 5

Stock & raw material costs 264,7

20

473,51

9

660,87

4

1,000,35

4

1,370,03

2

Website maintenance 11,0

00

12,00

0

13,00

0

14,00

0

15,00

0

Other variable costs 50,9

44 90,704

102,17

5

190,07

1

214,00

6

Online transaction fees (1.5%) 10,4

27

16,88

2

24,53

3

35,01

3

48,87

6

Projected Variable Costs 337,0

91

593,10

5

800,58

2

1,239,43

8

1,647,91

4

Total Costs (Advt. + Staff + Fixed + Variable

Costs)

740,8

73

1,051,58

7

1,389,26

2

1,914,72

6

2,413,06

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

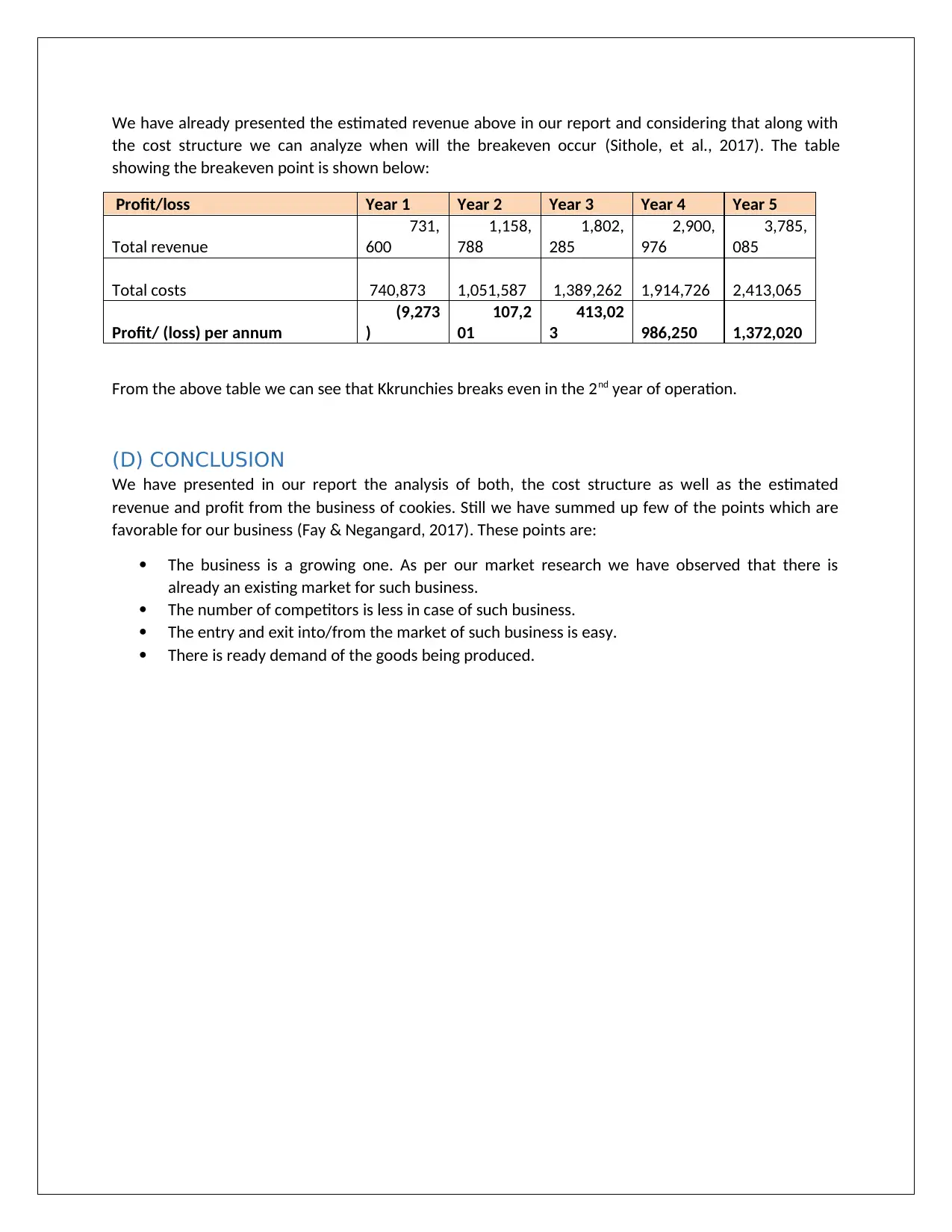

We have already presented the estimated revenue above in our report and considering that along with

the cost structure we can analyze when will the breakeven occur (Sithole, et al., 2017). The table

showing the breakeven point is shown below:

Profit/loss Year 1 Year 2 Year 3 Year 4 Year 5

Total revenue

731,

600

1,158,

788

1,802,

285

2,900,

976

3,785,

085

Total costs 740,873 1,051,587 1,389,262 1,914,726 2,413,065

Profit/ (loss) per annum

(9,273

)

107,2

01

413,02

3 986,250 1,372,020

From the above table we can see that Kkrunchies breaks even in the 2nd year of operation.

(D) CONCLUSION

We have presented in our report the analysis of both, the cost structure as well as the estimated

revenue and profit from the business of cookies. Still we have summed up few of the points which are

favorable for our business (Fay & Negangard, 2017). These points are:

The business is a growing one. As per our market research we have observed that there is

already an existing market for such business.

The number of competitors is less in case of such business.

The entry and exit into/from the market of such business is easy.

There is ready demand of the goods being produced.

the cost structure we can analyze when will the breakeven occur (Sithole, et al., 2017). The table

showing the breakeven point is shown below:

Profit/loss Year 1 Year 2 Year 3 Year 4 Year 5

Total revenue

731,

600

1,158,

788

1,802,

285

2,900,

976

3,785,

085

Total costs 740,873 1,051,587 1,389,262 1,914,726 2,413,065

Profit/ (loss) per annum

(9,273

)

107,2

01

413,02

3 986,250 1,372,020

From the above table we can see that Kkrunchies breaks even in the 2nd year of operation.

(D) CONCLUSION

We have presented in our report the analysis of both, the cost structure as well as the estimated

revenue and profit from the business of cookies. Still we have summed up few of the points which are

favorable for our business (Fay & Negangard, 2017). These points are:

The business is a growing one. As per our market research we have observed that there is

already an existing market for such business.

The number of competitors is less in case of such business.

The entry and exit into/from the market of such business is easy.

There is ready demand of the goods being produced.

SECTION B

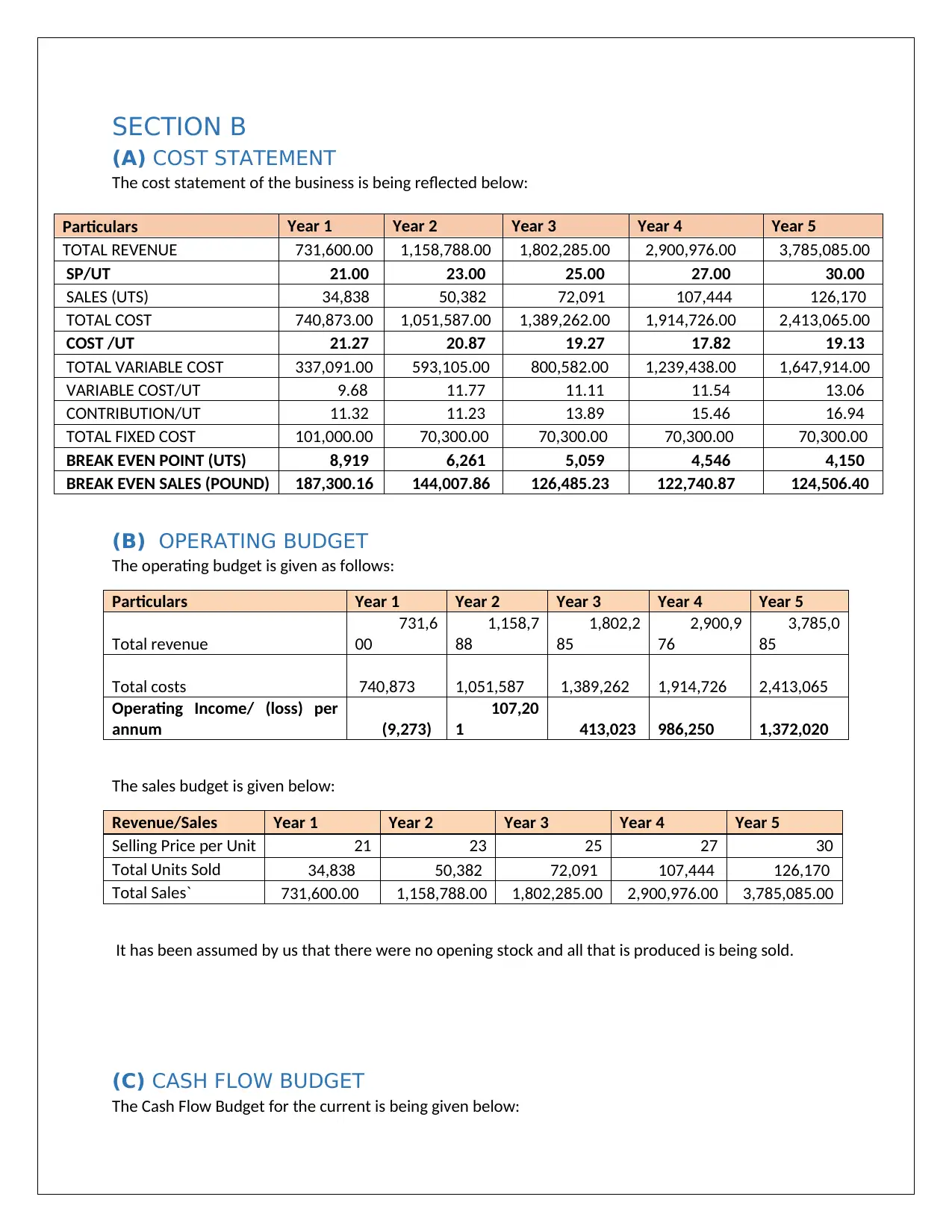

(A) COST STATEMENT

The cost statement of the business is being reflected below:

Particulars Year 1 Year 2 Year 3 Year 4 Year 5

TOTAL REVENUE 731,600.00 1,158,788.00 1,802,285.00 2,900,976.00 3,785,085.00

SP/UT 21.00 23.00 25.00 27.00 30.00

SALES (UTS) 34,838 50,382 72,091 107,444 126,170

TOTAL COST 740,873.00 1,051,587.00 1,389,262.00 1,914,726.00 2,413,065.00

COST /UT 21.27 20.87 19.27 17.82 19.13

TOTAL VARIABLE COST 337,091.00 593,105.00 800,582.00 1,239,438.00 1,647,914.00

VARIABLE COST/UT 9.68 11.77 11.11 11.54 13.06

CONTRIBUTION/UT 11.32 11.23 13.89 15.46 16.94

TOTAL FIXED COST 101,000.00 70,300.00 70,300.00 70,300.00 70,300.00

BREAK EVEN POINT (UTS) 8,919 6,261 5,059 4,546 4,150

BREAK EVEN SALES (POUND) 187,300.16 144,007.86 126,485.23 122,740.87 124,506.40

(B) OPERATING BUDGET

The operating budget is given as follows:

Particulars Year 1 Year 2 Year 3 Year 4 Year 5

Total revenue

731,6

00

1,158,7

88

1,802,2

85

2,900,9

76

3,785,0

85

Total costs 740,873 1,051,587 1,389,262 1,914,726 2,413,065

Operating Income/ (loss) per

annum (9,273)

107,20

1 413,023 986,250 1,372,020

The sales budget is given below:

Revenue/Sales Year 1 Year 2 Year 3 Year 4 Year 5

Selling Price per Unit 21 23 25 27 30

Total Units Sold 34,838 50,382 72,091 107,444 126,170

Total Sales` 731,600.00 1,158,788.00 1,802,285.00 2,900,976.00 3,785,085.00

It has been assumed by us that there were no opening stock and all that is produced is being sold.

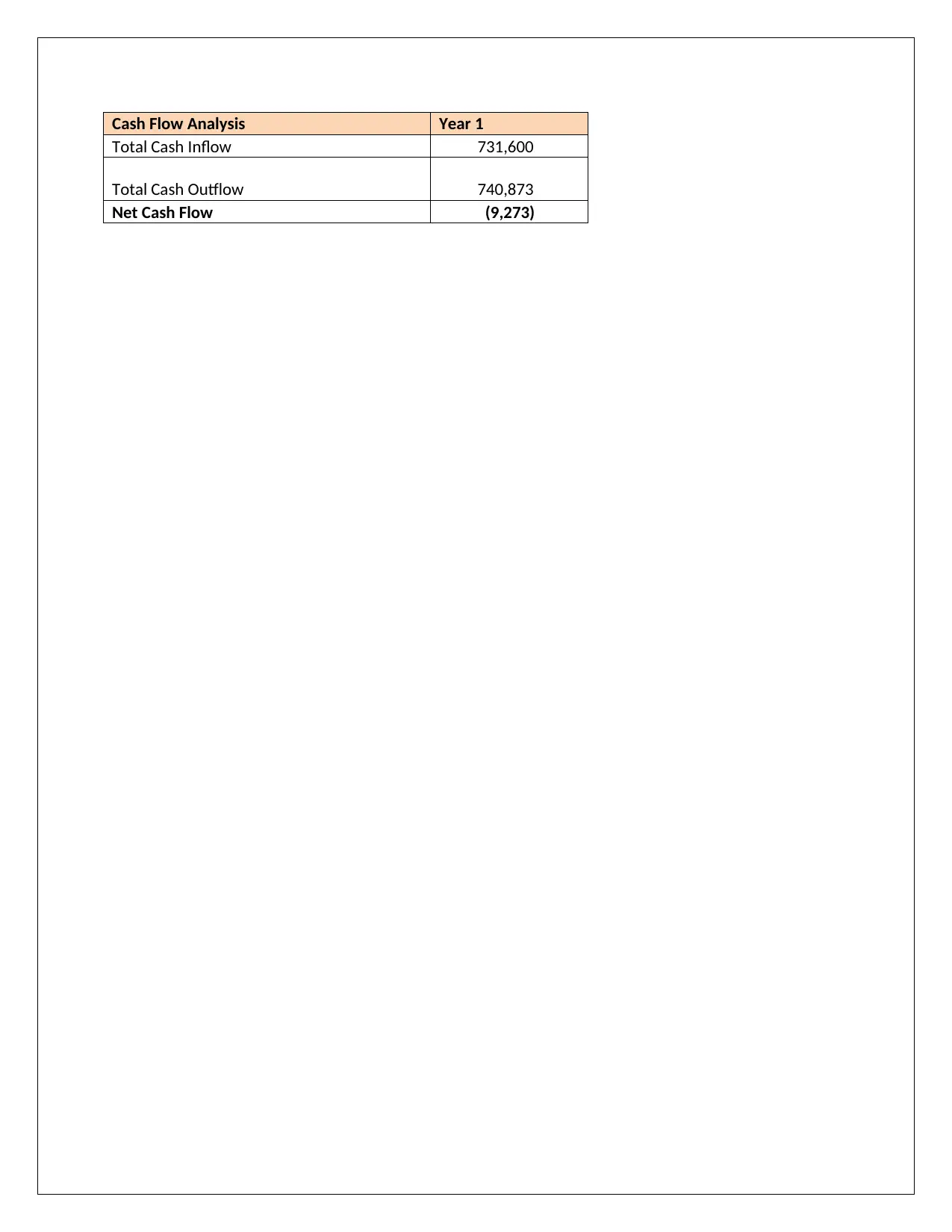

(C) CASH FLOW BUDGET

The Cash Flow Budget for the current is being given below:

(A) COST STATEMENT

The cost statement of the business is being reflected below:

Particulars Year 1 Year 2 Year 3 Year 4 Year 5

TOTAL REVENUE 731,600.00 1,158,788.00 1,802,285.00 2,900,976.00 3,785,085.00

SP/UT 21.00 23.00 25.00 27.00 30.00

SALES (UTS) 34,838 50,382 72,091 107,444 126,170

TOTAL COST 740,873.00 1,051,587.00 1,389,262.00 1,914,726.00 2,413,065.00

COST /UT 21.27 20.87 19.27 17.82 19.13

TOTAL VARIABLE COST 337,091.00 593,105.00 800,582.00 1,239,438.00 1,647,914.00

VARIABLE COST/UT 9.68 11.77 11.11 11.54 13.06

CONTRIBUTION/UT 11.32 11.23 13.89 15.46 16.94

TOTAL FIXED COST 101,000.00 70,300.00 70,300.00 70,300.00 70,300.00

BREAK EVEN POINT (UTS) 8,919 6,261 5,059 4,546 4,150

BREAK EVEN SALES (POUND) 187,300.16 144,007.86 126,485.23 122,740.87 124,506.40

(B) OPERATING BUDGET

The operating budget is given as follows:

Particulars Year 1 Year 2 Year 3 Year 4 Year 5

Total revenue

731,6

00

1,158,7

88

1,802,2

85

2,900,9

76

3,785,0

85

Total costs 740,873 1,051,587 1,389,262 1,914,726 2,413,065

Operating Income/ (loss) per

annum (9,273)

107,20

1 413,023 986,250 1,372,020

The sales budget is given below:

Revenue/Sales Year 1 Year 2 Year 3 Year 4 Year 5

Selling Price per Unit 21 23 25 27 30

Total Units Sold 34,838 50,382 72,091 107,444 126,170

Total Sales` 731,600.00 1,158,788.00 1,802,285.00 2,900,976.00 3,785,085.00

It has been assumed by us that there were no opening stock and all that is produced is being sold.

(C) CASH FLOW BUDGET

The Cash Flow Budget for the current is being given below:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cash Flow Analysis Year 1

Total Cash Inflow 731,600

Total Cash Outflow 740,873

Net Cash Flow (9,273)

Total Cash Inflow 731,600

Total Cash Outflow 740,873

Net Cash Flow (9,273)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Alexander, F., 2016. The Changing Face of Accountability. The Journal of Higher Education, 71(4), pp.

411-431.

Arnott, D., Lizama, F. & Song, Y., 2017. Patterns of business intelligence systems use in organizations.

Decision Support Systems, Volume 97, pp. 58-68.

Choy, Y. K., 2018. Cost-benefit Analysis, Values, Wellbeing and Ethics: An Indigenous Worldview Analysis.

Ecological Economics, 3(1), p. 145.

Fay, R. & Negangard, E., 2017. Manual journal entry testing : Data analytics and the risk of fraud. Journal

of Accounting Education, Volume 38, pp. 37-49.

Fukukawa, H. & Mock, T., 2011. Audit risk assessments using belief versus probability. Auditing: A

Journal of Practice & Theory, 30(1), pp. 75-99.

Goldmann, K., 2016. Financial Liquidity and Profitability Management in Practice of Polish Business.

Financial Environment and Business Development, 4(3), pp. 103-112.

Heminway, J., 2017. Shareholder Wealth Maximization as a Function of Statutes, Decisional Law, and

Organic Documents. SSRN, pp. 1-35.

Jefferson, M., 2017. Energy, Complexity and Wealth Maximization, R. Ayres. Springer, Switzerland.

Technological Forecasting and Social Change, pp. 353-354.

Kew, J. & Stredwick, J., 2017. Business Environment: Managing in a Strategic Context. second ed.

London: Chartered Institute of Personnel and Development.

Linden, B. & Freeman, R., 2017. Profit and Other Values: Thick Evaluation in Decision Making. Business

Ethics Quarterly, 27(3), pp. 353-379.

Raiborn, C., Butler, J. & Martin, K., 2016. The internal audit function: A prerequisite for Good

Governance. Journal of Corporate Accounting and Finance, 28(2), pp. 10-21.

Sithole, S., Chandler, P., Abeysekera, I. & Paas, F., 2017. Benefits of guided self-management of attention

on learning accounting. Journal of Educational Psychology, 109(2), p. 220.

Visinescu, L., Jones, M. & Sidorova, A., 2017. Improving Decision Quality: The Role of Business

Intelligence. Journal of Computer Information Systems, 57(1), pp. 58-66.

Werner, M., 2017. Financial process mining - Accounting data structure dependent control flow

inference. International Journal of Accounting Information Systems, 25(1), pp. 57-80.

Alexander, F., 2016. The Changing Face of Accountability. The Journal of Higher Education, 71(4), pp.

411-431.

Arnott, D., Lizama, F. & Song, Y., 2017. Patterns of business intelligence systems use in organizations.

Decision Support Systems, Volume 97, pp. 58-68.

Choy, Y. K., 2018. Cost-benefit Analysis, Values, Wellbeing and Ethics: An Indigenous Worldview Analysis.

Ecological Economics, 3(1), p. 145.

Fay, R. & Negangard, E., 2017. Manual journal entry testing : Data analytics and the risk of fraud. Journal

of Accounting Education, Volume 38, pp. 37-49.

Fukukawa, H. & Mock, T., 2011. Audit risk assessments using belief versus probability. Auditing: A

Journal of Practice & Theory, 30(1), pp. 75-99.

Goldmann, K., 2016. Financial Liquidity and Profitability Management in Practice of Polish Business.

Financial Environment and Business Development, 4(3), pp. 103-112.

Heminway, J., 2017. Shareholder Wealth Maximization as a Function of Statutes, Decisional Law, and

Organic Documents. SSRN, pp. 1-35.

Jefferson, M., 2017. Energy, Complexity and Wealth Maximization, R. Ayres. Springer, Switzerland.

Technological Forecasting and Social Change, pp. 353-354.

Kew, J. & Stredwick, J., 2017. Business Environment: Managing in a Strategic Context. second ed.

London: Chartered Institute of Personnel and Development.

Linden, B. & Freeman, R., 2017. Profit and Other Values: Thick Evaluation in Decision Making. Business

Ethics Quarterly, 27(3), pp. 353-379.

Raiborn, C., Butler, J. & Martin, K., 2016. The internal audit function: A prerequisite for Good

Governance. Journal of Corporate Accounting and Finance, 28(2), pp. 10-21.

Sithole, S., Chandler, P., Abeysekera, I. & Paas, F., 2017. Benefits of guided self-management of attention

on learning accounting. Journal of Educational Psychology, 109(2), p. 220.

Visinescu, L., Jones, M. & Sidorova, A., 2017. Improving Decision Quality: The Role of Business

Intelligence. Journal of Computer Information Systems, 57(1), pp. 58-66.

Werner, M., 2017. Financial process mining - Accounting data structure dependent control flow

inference. International Journal of Accounting Information Systems, 25(1), pp. 57-80.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.