Mario's Pizza Business Report

VerifiedAdded on 2020/02/05

|14

|1891

|519

Report

AI Summary

This report provides a comprehensive financial analysis of Mario's Pizza. It includes a detailed income statement and balance sheet, followed by a thorough ratio analysis evaluating profitability, liquidity, and solvency. The analysis uses various financial ratios such as gross profit ratio, net profit ratio, current ratio, quick ratio, debt-to-equity ratio, total assets turnover ratio, and inventory turnover ratio to assess the business's performance. Limitations of ratio analysis are also discussed. Finally, the report concludes with recommendations for Mario, suggesting the purchase of a new vehicle and emphasizing the need for better control over indirect expenses to improve profitability. The report highlights the importance of accounting records for effective business management and decision-making.

MARIO PIZZA

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Income statement of Mario's Pizza.....................................................................................................................................................3

Balance sheet of Mario's Pizza...........................................................................................................................................................8

Evaluation of business performance through ratio analysis.............................................................................................................11

Limitations of ratio analysis.............................................................................................................................................................11

Recommend to Mario.......................................................................................................................................................................12

REFERENCES..........................................................................................................................................................................................13

Income statement of Mario's Pizza.....................................................................................................................................................3

Balance sheet of Mario's Pizza...........................................................................................................................................................8

Evaluation of business performance through ratio analysis.............................................................................................................11

Limitations of ratio analysis.............................................................................................................................................................11

Recommend to Mario.......................................................................................................................................................................12

REFERENCES..........................................................................................................................................................................................13

INTRODUCTION

Accounting is the one of the field to which due importance is given in the current time period by the business firms. This is

because in same accounts are prepared which revealed different business transactions and performance of the business firm. In the

current report, income statement and balance sheet is prepared by following specific approach. Ratio analysis tools are used to analyze

the data and making interpretation in respect to the business firm. In depth analysis is done in the report and conclusion is formed on

that basis. Moreover, recommendation is made at end of the report. In this way, entire research work is carried out in the present study.

Analysis

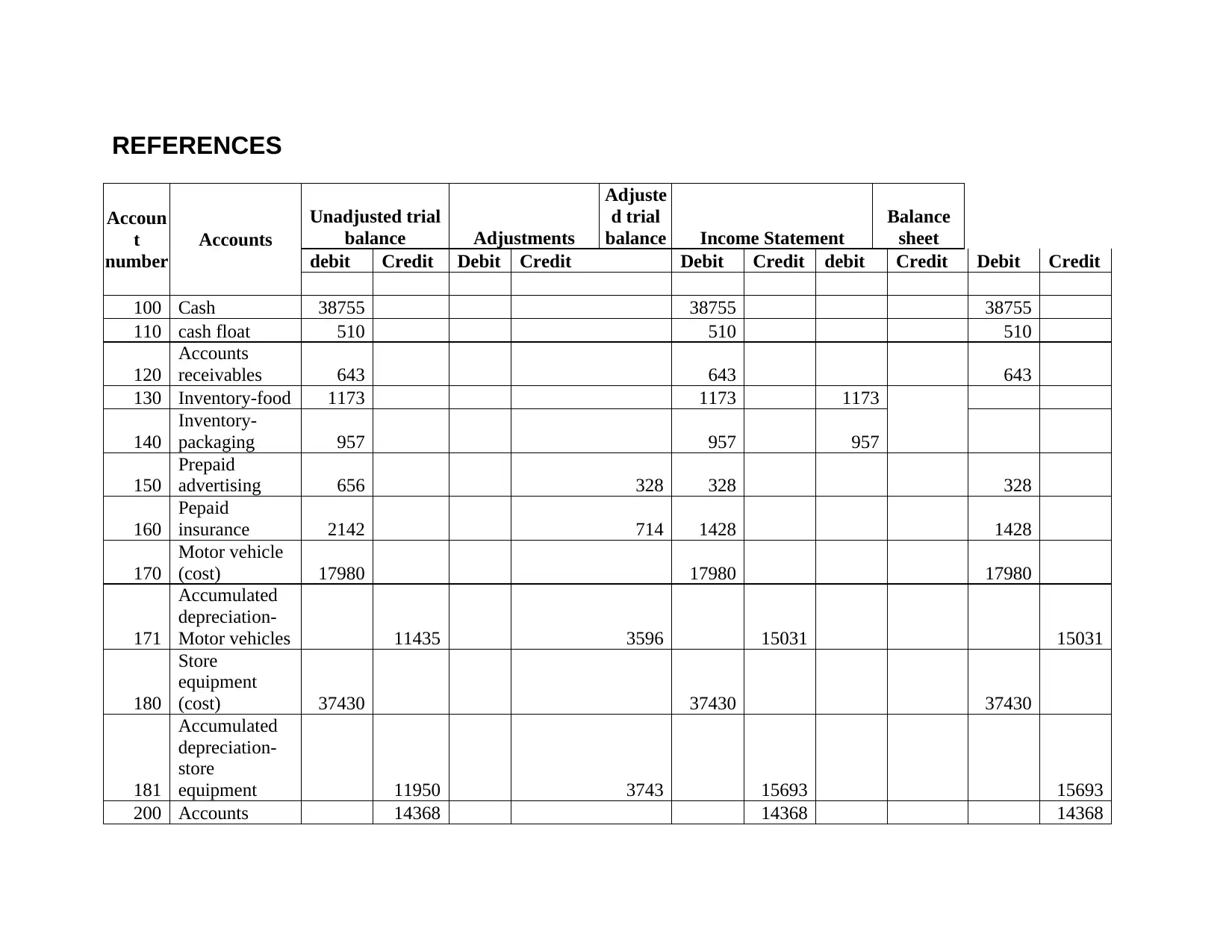

In the current report on analysis of balance sheet that is given in appendix it can be observed that current assets valued at 47995 and

current liability valued at 17219. On the basis of difference it can be observed that current assets proportion is much higher than

current liability. This happened because firm management is excellent and it is managing its current assets in systematic way. Current

assets are larger multiple times then current liability. It can be said that there is huge amount of liquidity in the firm business.

Fundamentals of the firm on this front are very strong and it is able to pay its current liabilities multiple times in its business. It is the

proper cash management through which firm successfully recover debt from the debtors and make effective use of cash in the

business. All these things lead to generation of sufficient amount of money in the business. It can be said that firm is making effective

use of cash in its business and due to fast receipt of cash from the debtors accumulate sufficient amount of current assets in its

business. Thus, its short term financial position is excellent. Total sales of 183737 is made in the business followed by gross profit

value 116852. Net profit of the firm is 16463 and it can be said that low amount of profit is earned by the firm in the business. It can

be said that expenses in the business are very high. Facts are clearly reflecting that burden of indirect expenses is very high on the

business then direct expenses.

As per the findings of profitability ratio, it can be seen that Mario Pizza palace’s GP and NP ratios are computed to 63.70%

and 8.98% respectively. According to the industrial benchmark for the current year 2014-15, company incur a cost of sales under the

Accounting is the one of the field to which due importance is given in the current time period by the business firms. This is

because in same accounts are prepared which revealed different business transactions and performance of the business firm. In the

current report, income statement and balance sheet is prepared by following specific approach. Ratio analysis tools are used to analyze

the data and making interpretation in respect to the business firm. In depth analysis is done in the report and conclusion is formed on

that basis. Moreover, recommendation is made at end of the report. In this way, entire research work is carried out in the present study.

Analysis

In the current report on analysis of balance sheet that is given in appendix it can be observed that current assets valued at 47995 and

current liability valued at 17219. On the basis of difference it can be observed that current assets proportion is much higher than

current liability. This happened because firm management is excellent and it is managing its current assets in systematic way. Current

assets are larger multiple times then current liability. It can be said that there is huge amount of liquidity in the firm business.

Fundamentals of the firm on this front are very strong and it is able to pay its current liabilities multiple times in its business. It is the

proper cash management through which firm successfully recover debt from the debtors and make effective use of cash in the

business. All these things lead to generation of sufficient amount of money in the business. It can be said that firm is making effective

use of cash in its business and due to fast receipt of cash from the debtors accumulate sufficient amount of current assets in its

business. Thus, its short term financial position is excellent. Total sales of 183737 is made in the business followed by gross profit

value 116852. Net profit of the firm is 16463 and it can be said that low amount of profit is earned by the firm in the business. It can

be said that expenses in the business are very high. Facts are clearly reflecting that burden of indirect expenses is very high on the

business then direct expenses.

As per the findings of profitability ratio, it can be seen that Mario Pizza palace’s GP and NP ratios are computed to 63.70%

and 8.98% respectively. According to the industrial benchmark for the current year 2014-15, company incur a cost of sales under the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

range of 36% to 41% and Mario Pizza’s cost of sales is 36.30% which is under the benchmark and indicates that it is performing well

and have effective control over costs.

On the other side, under the liquidity performance, current ratio and quick ratio are computed to 2.79:1 and 2.42:1 respectively,

both the ratios are above the industrial benchmark of 2:1 and 1:1. Although it is a good indication of sound liquidity position as

company has enough resources available to pay their suppliers, still, productive use of the resources is necessary. Firm is making best

use of assets in its business as it is reflected by higher value of the ratio which is 39.63 times. On other hand, inventory turnover ratio

value is 3.45 times which is very low and on this basis it can be said that firm failed to make best use of inventory in its business. It

can be said that firm need to make inventory best use in its business.

Besides this, Debt to equity ratio is derived to 0.50 which is perfect because target or idle ratio indicates that Mario Pizza must

utilize half proportion of their total capital in the business so as to manage long-term financial risks and solvency position to repay

their long-term liabilities on time.

Limitations of ratio analysis

The analysis does not help to analyse qualitative performance as it only gives quantitative results and also cannot be used for

the forecasting purpose because historical performance can be evaluated from this method. Further, change in accounting policies,

rules and reporting also does not reflect by the annual reports may mislead the decisions (Demerits Of Ratio Analysis, 2010.). Apart

from this, there is no idle ratio available for every ratio, in such case, it becomes too difficult for Mario Pizza to interpret a single ratio

CONCLUSION

On the basis of report it is concluded that there is huge importance of the accounting records for the managers because by

using they access firm performance. There are varied elements of the income statement and balance sheet and by using same

performance of the firm is accessed by the managers. By using ratio analysis method performance of the firm is measured and

and have effective control over costs.

On the other side, under the liquidity performance, current ratio and quick ratio are computed to 2.79:1 and 2.42:1 respectively,

both the ratios are above the industrial benchmark of 2:1 and 1:1. Although it is a good indication of sound liquidity position as

company has enough resources available to pay their suppliers, still, productive use of the resources is necessary. Firm is making best

use of assets in its business as it is reflected by higher value of the ratio which is 39.63 times. On other hand, inventory turnover ratio

value is 3.45 times which is very low and on this basis it can be said that firm failed to make best use of inventory in its business. It

can be said that firm need to make inventory best use in its business.

Besides this, Debt to equity ratio is derived to 0.50 which is perfect because target or idle ratio indicates that Mario Pizza must

utilize half proportion of their total capital in the business so as to manage long-term financial risks and solvency position to repay

their long-term liabilities on time.

Limitations of ratio analysis

The analysis does not help to analyse qualitative performance as it only gives quantitative results and also cannot be used for

the forecasting purpose because historical performance can be evaluated from this method. Further, change in accounting policies,

rules and reporting also does not reflect by the annual reports may mislead the decisions (Demerits Of Ratio Analysis, 2010.). Apart

from this, there is no idle ratio available for every ratio, in such case, it becomes too difficult for Mario Pizza to interpret a single ratio

CONCLUSION

On the basis of report it is concluded that there is huge importance of the accounting records for the managers because by

using they access firm performance. There are varied elements of the income statement and balance sheet and by using same

performance of the firm is accessed by the managers. By using ratio analysis method performance of the firm is measured and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

managers identify areas where they need to do lots of work in order to improve performance. It can be said that there is huge

importance of ratio analysis method for the managers of the business by using same performance is accessed in systematic way.

Recommend to Mario

It can be recommended to the Mario that in needs to adopt option number three which is purchase of the new vehicle. If he will

purchase and buy the new vehicle then can use new features as well as it will have long life and beneficial for it. Apart from this, in

case if it buys second hand vehicle then there is no surety that vehicle will be better and along with this at here also cost needs to pay.

It is recommended that firm must not further issue equity in the upcoming time period because already there is high amount of equity

in the firm business. If firm will further issue fresh equity then in that case burden of cost of capital will increased on the firm. It is

also recommended that firm must maintain deep control on its indirect expense. This is because by doing profitability can be increased

in the business. In this regard cost control methods like process reengineering can be used by the business firm at the workplace. By

using method EOQ appropriate quantity can be purchased and storage cost can be reduced in the business.

importance of ratio analysis method for the managers of the business by using same performance is accessed in systematic way.

Recommend to Mario

It can be recommended to the Mario that in needs to adopt option number three which is purchase of the new vehicle. If he will

purchase and buy the new vehicle then can use new features as well as it will have long life and beneficial for it. Apart from this, in

case if it buys second hand vehicle then there is no surety that vehicle will be better and along with this at here also cost needs to pay.

It is recommended that firm must not further issue equity in the upcoming time period because already there is high amount of equity

in the firm business. If firm will further issue fresh equity then in that case burden of cost of capital will increased on the firm. It is

also recommended that firm must maintain deep control on its indirect expense. This is because by doing profitability can be increased

in the business. In this regard cost control methods like process reengineering can be used by the business firm at the workplace. By

using method EOQ appropriate quantity can be purchased and storage cost can be reduced in the business.

REFERENCES

Agha, H., 2014. Impact of working capital management on profitability. European Scientific Journal, ESJ. 10(1).

Demerits Of Ratio Analysis, 2010. [Online]. Available through: <http://www.managementparadise.com/forums/financial-

management-fm/202052-demerits-ratio-analysis.html> [Accessed on 6th March 2017].

Lin, L. H. and et.al., 2014. The analysis of company liquidity a using cash conversion cycle application: evidence from Taiwan.

Global Journal of Business Research. 8(5). pp. 97.

Agha, H., 2014. Impact of working capital management on profitability. European Scientific Journal, ESJ. 10(1).

Demerits Of Ratio Analysis, 2010. [Online]. Available through: <http://www.managementparadise.com/forums/financial-

management-fm/202052-demerits-ratio-analysis.html> [Accessed on 6th March 2017].

Lin, L. H. and et.al., 2014. The analysis of company liquidity a using cash conversion cycle application: evidence from Taiwan.

Global Journal of Business Research. 8(5). pp. 97.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

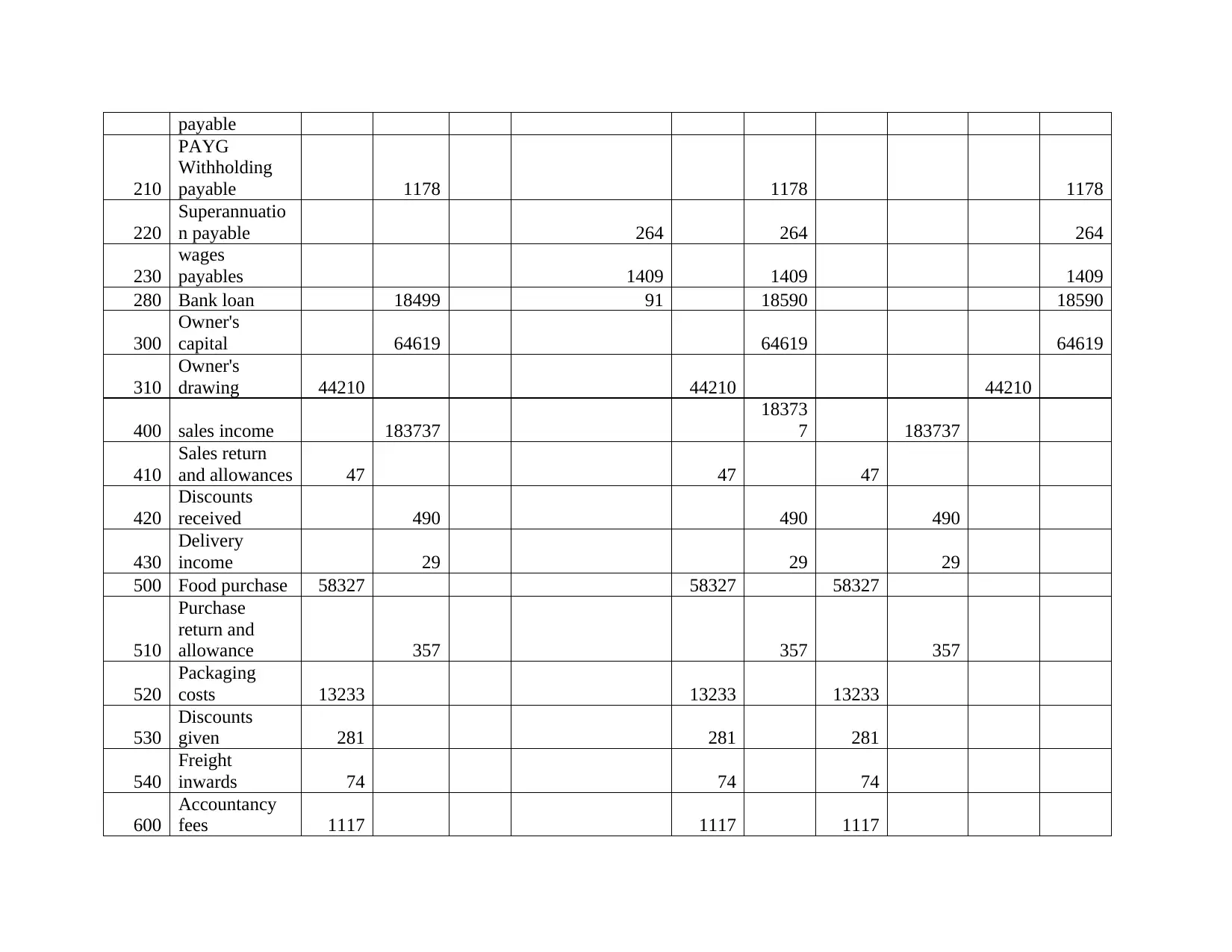

Accoun

t

number

Accounts

Unadjusted trial

balance Adjustments

Adjuste

d trial

balance Income Statement

Balance

sheet

debit Credit Debit Credit Debit Credit debit Credit Debit Credit

100 Cash 38755 38755 38755

110 cash float 510 510 510

120

Accounts

receivables 643 643 643

130 Inventory-food 1173 1173 1173

140

Inventory-

packaging 957 957 957

150

Prepaid

advertising 656 328 328 328

160

Pepaid

insurance 2142 714 1428 1428

170

Motor vehicle

(cost) 17980 17980 17980

171

Accumulated

depreciation-

Motor vehicles 11435 3596 15031 15031

180

Store

equipment

(cost) 37430 37430 37430

181

Accumulated

depreciation-

store

equipment 11950 3743 15693 15693

200 Accounts 14368 14368 14368

Accoun

t

number

Accounts

Unadjusted trial

balance Adjustments

Adjuste

d trial

balance Income Statement

Balance

sheet

debit Credit Debit Credit Debit Credit debit Credit Debit Credit

100 Cash 38755 38755 38755

110 cash float 510 510 510

120

Accounts

receivables 643 643 643

130 Inventory-food 1173 1173 1173

140

Inventory-

packaging 957 957 957

150

Prepaid

advertising 656 328 328 328

160

Pepaid

insurance 2142 714 1428 1428

170

Motor vehicle

(cost) 17980 17980 17980

171

Accumulated

depreciation-

Motor vehicles 11435 3596 15031 15031

180

Store

equipment

(cost) 37430 37430 37430

181

Accumulated

depreciation-

store

equipment 11950 3743 15693 15693

200 Accounts 14368 14368 14368

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

payable

210

PAYG

Withholding

payable 1178 1178 1178

220

Superannuatio

n payable 264 264 264

230

wages

payables 1409 1409 1409

280 Bank loan 18499 91 18590 18590

300

Owner's

capital 64619 64619 64619

310

Owner's

drawing 44210 44210 44210

400 sales income 183737

18373

7 183737

410

Sales return

and allowances 47 47 47

420

Discounts

received 490 490 490

430

Delivery

income 29 29 29

500 Food purchase 58327 58327 58327

510

Purchase

return and

allowance 357 357 357

520

Packaging

costs 13233 13233 13233

530

Discounts

given 281 281 281

540

Freight

inwards 74 74 74

600

Accountancy

fees 1117 1117 1117

210

PAYG

Withholding

payable 1178 1178 1178

220

Superannuatio

n payable 264 264 264

230

wages

payables 1409 1409 1409

280 Bank loan 18499 91 18590 18590

300

Owner's

capital 64619 64619 64619

310

Owner's

drawing 44210 44210 44210

400 sales income 183737

18373

7 183737

410

Sales return

and allowances 47 47 47

420

Discounts

received 490 490 490

430

Delivery

income 29 29 29

500 Food purchase 58327 58327 58327

510

Purchase

return and

allowance 357 357 357

520

Packaging

costs 13233 13233 13233

530

Discounts

given 281 281 281

540

Freight

inwards 74 74 74

600

Accountancy

fees 1117 1117 1117

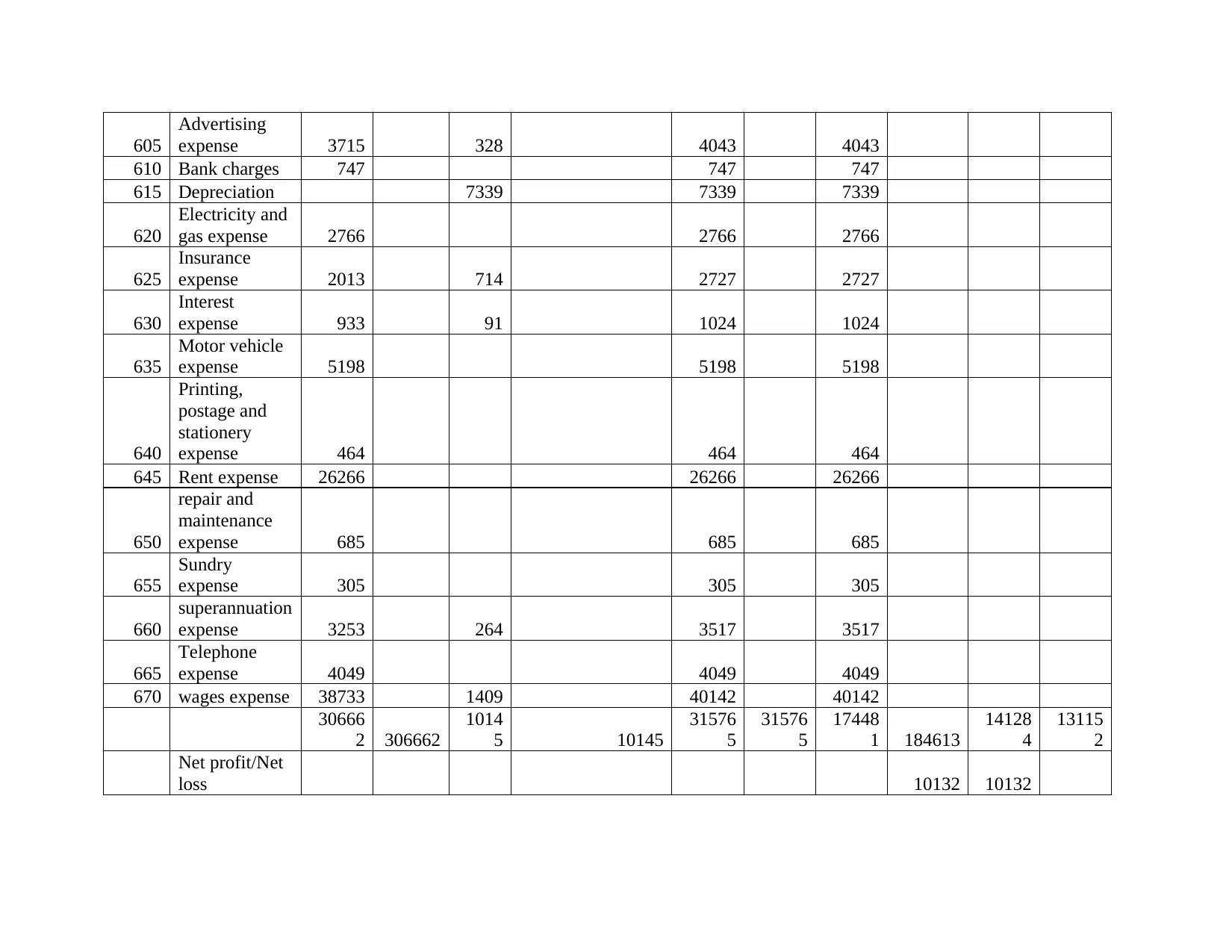

605

Advertising

expense 3715 328 4043 4043

610 Bank charges 747 747 747

615 Depreciation 7339 7339 7339

620

Electricity and

gas expense 2766 2766 2766

625

Insurance

expense 2013 714 2727 2727

630

Interest

expense 933 91 1024 1024

635

Motor vehicle

expense 5198 5198 5198

640

Printing,

postage and

stationery

expense 464 464 464

645 Rent expense 26266 26266 26266

650

repair and

maintenance

expense 685 685 685

655

Sundry

expense 305 305 305

660

superannuation

expense 3253 264 3517 3517

665

Telephone

expense 4049 4049 4049

670 wages expense 38733 1409 40142 40142

30666

2 306662

1014

5 10145

31576

5

31576

5

17448

1 184613

14128

4

13115

2

Net profit/Net

loss 10132 10132

Advertising

expense 3715 328 4043 4043

610 Bank charges 747 747 747

615 Depreciation 7339 7339 7339

620

Electricity and

gas expense 2766 2766 2766

625

Insurance

expense 2013 714 2727 2727

630

Interest

expense 933 91 1024 1024

635

Motor vehicle

expense 5198 5198 5198

640

Printing,

postage and

stationery

expense 464 464 464

645 Rent expense 26266 26266 26266

650

repair and

maintenance

expense 685 685 685

655

Sundry

expense 305 305 305

660

superannuation

expense 3253 264 3517 3517

665

Telephone

expense 4049 4049 4049

670 wages expense 38733 1409 40142 40142

30666

2 306662

1014

5 10145

31576

5

31576

5

17448

1 184613

14128

4

13115

2

Net profit/Net

loss 10132 10132

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

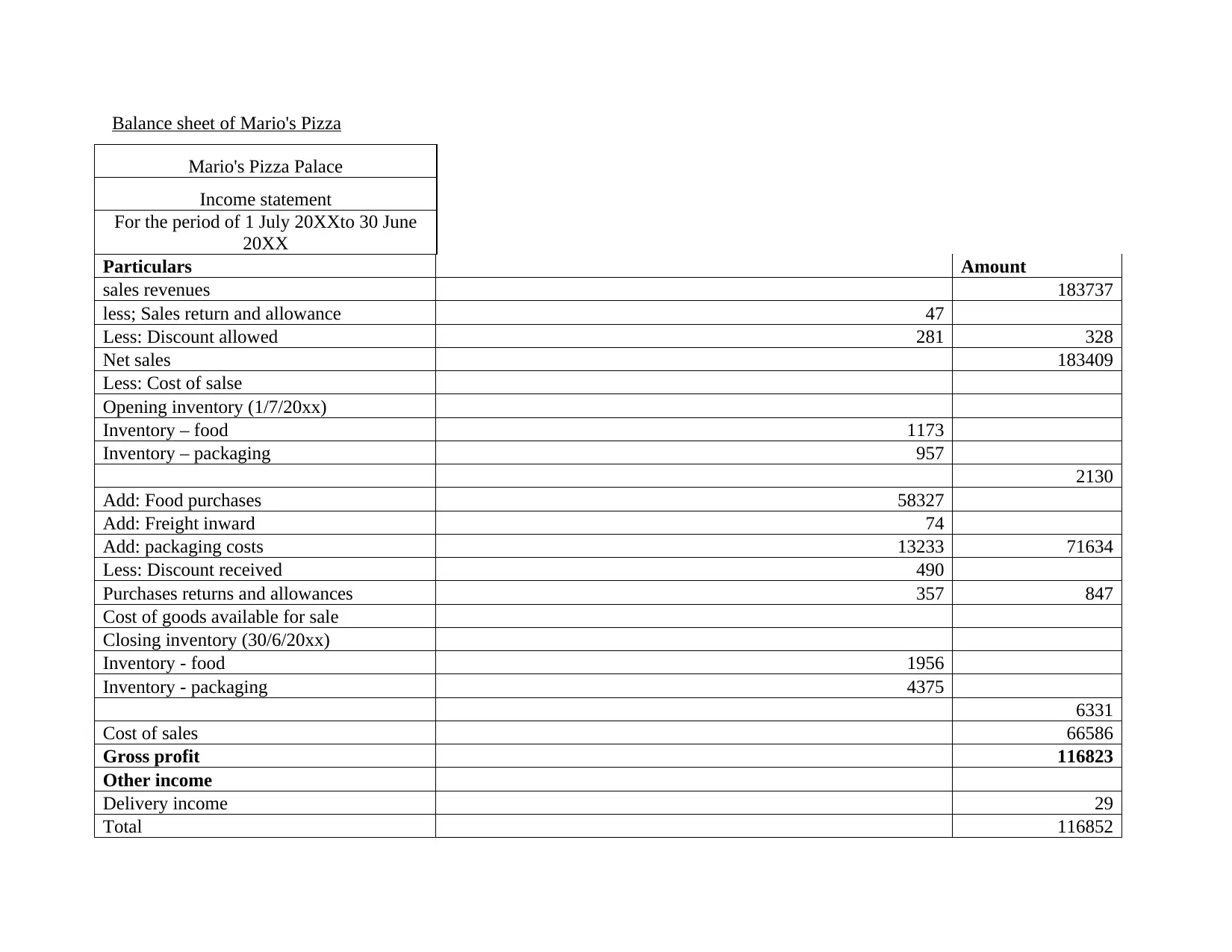

Balance sheet of Mario's Pizza

Mario's Pizza Palace

Income statement

For the period of 1 July 20XXto 30 June

20XX

Particulars Amount

sales revenues 183737

less; Sales return and allowance 47

Less: Discount allowed 281 328

Net sales 183409

Less: Cost of salse

Opening inventory (1/7/20xx)

Inventory – food 1173

Inventory – packaging 957

2130

Add: Food purchases 58327

Add: Freight inward 74

Add: packaging costs 13233 71634

Less: Discount received 490

Purchases returns and allowances 357 847

Cost of goods available for sale

Closing inventory (30/6/20xx)

Inventory - food 1956

Inventory - packaging 4375

6331

Cost of sales 66586

Gross profit 116823

Other income

Delivery income 29

Total 116852

Mario's Pizza Palace

Income statement

For the period of 1 July 20XXto 30 June

20XX

Particulars Amount

sales revenues 183737

less; Sales return and allowance 47

Less: Discount allowed 281 328

Net sales 183409

Less: Cost of salse

Opening inventory (1/7/20xx)

Inventory – food 1173

Inventory – packaging 957

2130

Add: Food purchases 58327

Add: Freight inward 74

Add: packaging costs 13233 71634

Less: Discount received 490

Purchases returns and allowances 357 847

Cost of goods available for sale

Closing inventory (30/6/20xx)

Inventory - food 1956

Inventory - packaging 4375

6331

Cost of sales 66586

Gross profit 116823

Other income

Delivery income 29

Total 116852

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

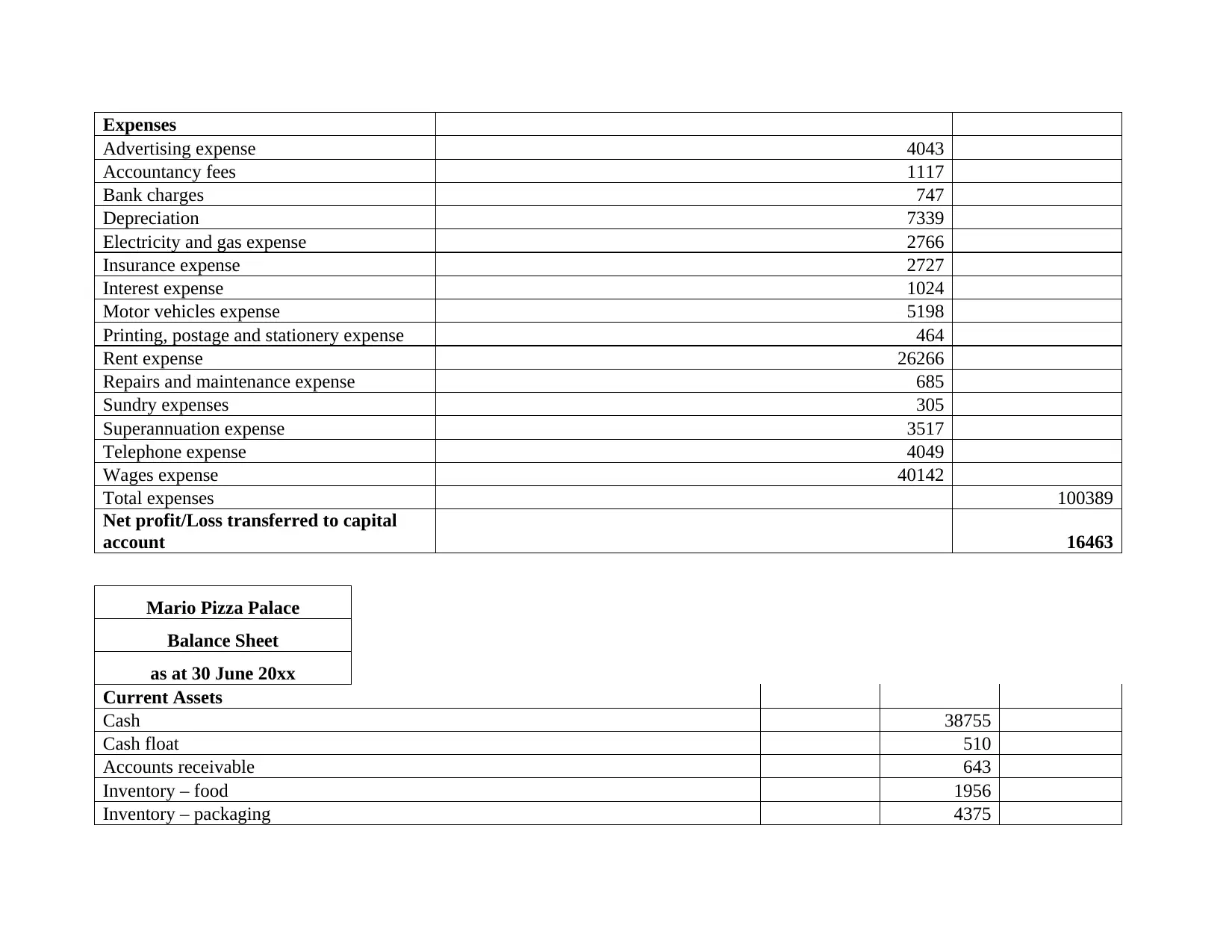

Expenses

Advertising expense 4043

Accountancy fees 1117

Bank charges 747

Depreciation 7339

Electricity and gas expense 2766

Insurance expense 2727

Interest expense 1024

Motor vehicles expense 5198

Printing, postage and stationery expense 464

Rent expense 26266

Repairs and maintenance expense 685

Sundry expenses 305

Superannuation expense 3517

Telephone expense 4049

Wages expense 40142

Total expenses 100389

Net profit/Loss transferred to capital

account 16463

Mario Pizza Palace

Balance Sheet

as at 30 June 20xx

Current Assets

Cash 38755

Cash float 510

Accounts receivable 643

Inventory – food 1956

Inventory – packaging 4375

Advertising expense 4043

Accountancy fees 1117

Bank charges 747

Depreciation 7339

Electricity and gas expense 2766

Insurance expense 2727

Interest expense 1024

Motor vehicles expense 5198

Printing, postage and stationery expense 464

Rent expense 26266

Repairs and maintenance expense 685

Sundry expenses 305

Superannuation expense 3517

Telephone expense 4049

Wages expense 40142

Total expenses 100389

Net profit/Loss transferred to capital

account 16463

Mario Pizza Palace

Balance Sheet

as at 30 June 20xx

Current Assets

Cash 38755

Cash float 510

Accounts receivable 643

Inventory – food 1956

Inventory – packaging 4375

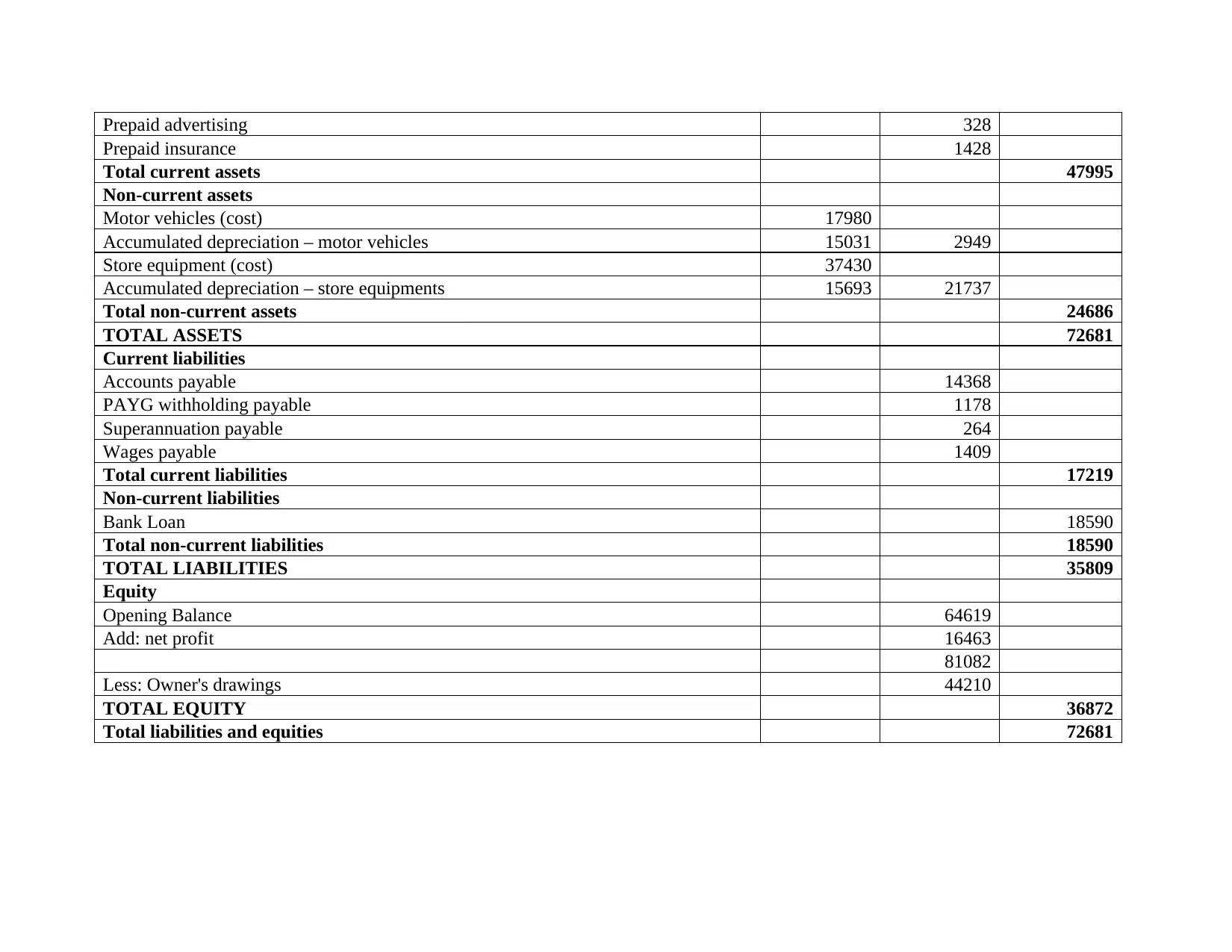

Prepaid advertising 328

Prepaid insurance 1428

Total current assets 47995

Non-current assets

Motor vehicles (cost) 17980

Accumulated depreciation – motor vehicles 15031 2949

Store equipment (cost) 37430

Accumulated depreciation – store equipments 15693 21737

Total non-current assets 24686

TOTAL ASSETS 72681

Current liabilities

Accounts payable 14368

PAYG withholding payable 1178

Superannuation payable 264

Wages payable 1409

Total current liabilities 17219

Non-current liabilities

Bank Loan 18590

Total non-current liabilities 18590

TOTAL LIABILITIES 35809

Equity

Opening Balance 64619

Add: net profit 16463

81082

Less: Owner's drawings 44210

TOTAL EQUITY 36872

Total liabilities and equities 72681

Prepaid insurance 1428

Total current assets 47995

Non-current assets

Motor vehicles (cost) 17980

Accumulated depreciation – motor vehicles 15031 2949

Store equipment (cost) 37430

Accumulated depreciation – store equipments 15693 21737

Total non-current assets 24686

TOTAL ASSETS 72681

Current liabilities

Accounts payable 14368

PAYG withholding payable 1178

Superannuation payable 264

Wages payable 1409

Total current liabilities 17219

Non-current liabilities

Bank Loan 18590

Total non-current liabilities 18590

TOTAL LIABILITIES 35809

Equity

Opening Balance 64619

Add: net profit 16463

81082

Less: Owner's drawings 44210

TOTAL EQUITY 36872

Total liabilities and equities 72681

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.