Financial Reporting: Analysis of Mark & Spencer (UK) for 2017 and 2018

VerifiedAdded on 2020/12/29

|13

|3702

|51

Report

AI Summary

This report provides a detailed analysis of financial reporting, focusing on the case of Mark & Spencer (M&S) located in the UK. It begins with an introduction to financial reporting, defining its purpose and importance in providing accurate financial information for decision-making. The main body of the report covers the purpose of financial accounting, the regulatory and conceptual frameworks, key principles, and the main stakeholders of an organization. It examines the value of financial reporting, presents the financial statements (profit and loss, and financial position), and discusses the use of financial statements. Furthermore, the report explores the differences between IAS and IFRS, evaluates the benefits of IFRS, and discusses the varying degrees of compliance. The report concludes by analyzing the financial performance of Mark & Spencer, highlighting the importance of financial reporting for internal management and external stakeholders. The financial statements and balance sheets provide a comprehensive overview of the company's financial health.

FINANCIAL REPORTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

1. Purpose of financial accounting...............................................................................................1

2. Requirement, purpose and key principles of regulatory and conceptual framework.............2

3. Main Stakeholders of an organisation and their benefits from financial information............3

4. Value of financial reporting ....................................................................................................4

5. Financial statements of the organisation.................................................................................5

A: Statement of profit and loss:...................................................................................................5

B: Statement of financial position:..............................................................................................5

6. Use of financial statements.....................................................................................................6

7. Difference between IAS and IFRS..........................................................................................7

8. Evaluation of benefits of IFRS...............................................................................................8

9. Ascertaining the varying degree of compliance......................................................................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

1. Purpose of financial accounting...............................................................................................1

2. Requirement, purpose and key principles of regulatory and conceptual framework.............2

3. Main Stakeholders of an organisation and their benefits from financial information............3

4. Value of financial reporting ....................................................................................................4

5. Financial statements of the organisation.................................................................................5

A: Statement of profit and loss:...................................................................................................5

B: Statement of financial position:..............................................................................................5

6. Use of financial statements.....................................................................................................6

7. Difference between IAS and IFRS..........................................................................................7

8. Evaluation of benefits of IFRS...............................................................................................8

9. Ascertaining the varying degree of compliance......................................................................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial reporting, is consider to be the process of analysing, collecting and posting

useful information in financial report that help internal management to make effective decisions.

This process help in formation or accurate and faithful cash flow statements, balance sheet and

income statements (Al-Matari, 2013). With the help of detail statements manager are able to

make decision and improve performance of company if required. For this report Mark and

Spenser is selected that is located in UK.

In this project report the purpose of financial reporting and its requirement is analysed.

The main stakeholder and the value of reporting for growth of company is shown and

formulation of financial statements and comparing of two years statements are covered under

this report. Report focuses on difference between IAS and IFRS and various benefit of IFRS.

MAIN BODY

1. Purpose of financial accounting.

The main purpose of financial reporting is to give exact detail about the performance of

company. It display the financial position and changes in the market position of company.

According to IASB the activity of maintaining financial records about a company is known

financial reporting. It is very important for company to record and display their financial status to

external shareholder do that they are able to make investment decision (Chae, and Oh, 2016).

Report must be liable, faithful and transparent enough that shows the current status about an

organisation. There are various objective of financial reporting for M&S that are discussed

below:

It provide suitable information to external shareholder and other investor to make

effective investment decision.

This report help auditors to conduct proper audit to ascertain the financial position of

company.

With the help of appropriate report manager are able to analyse and measure performance

of operation and employees of company.

Financial report gives information to stakeholder about the performance management of

Mark & Spencer, that how ethically they are executing job work.

1

Financial reporting, is consider to be the process of analysing, collecting and posting

useful information in financial report that help internal management to make effective decisions.

This process help in formation or accurate and faithful cash flow statements, balance sheet and

income statements (Al-Matari, 2013). With the help of detail statements manager are able to

make decision and improve performance of company if required. For this report Mark and

Spenser is selected that is located in UK.

In this project report the purpose of financial reporting and its requirement is analysed.

The main stakeholder and the value of reporting for growth of company is shown and

formulation of financial statements and comparing of two years statements are covered under

this report. Report focuses on difference between IAS and IFRS and various benefit of IFRS.

MAIN BODY

1. Purpose of financial accounting.

The main purpose of financial reporting is to give exact detail about the performance of

company. It display the financial position and changes in the market position of company.

According to IASB the activity of maintaining financial records about a company is known

financial reporting. It is very important for company to record and display their financial status to

external shareholder do that they are able to make investment decision (Chae, and Oh, 2016).

Report must be liable, faithful and transparent enough that shows the current status about an

organisation. There are various objective of financial reporting for M&S that are discussed

below:

It provide suitable information to external shareholder and other investor to make

effective investment decision.

This report help auditors to conduct proper audit to ascertain the financial position of

company.

With the help of appropriate report manager are able to analyse and measure performance

of operation and employees of company.

Financial report gives information to stakeholder about the performance management of

Mark & Spencer, that how ethically they are executing job work.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It help in providing the detail information about the utilization of various resources in

different activity.

External stakeholder are able to analyse or examine that weather their money is

effectively used or not (Duncan, 2014).

Decently managed financial reports are crucial for invitation, labour contracts and

government supplying, as it give summary of the enterprises to outside parties.

Generic aim of financial reporting is to examine the result of those activity that have been

performed by company during a particular period.

2. Requirement, purpose and key principles of regulatory and conceptual framework

In accounting, it is very important for an organisation to follow the quantitative and

qualitative framework in order to prepare their annual statements. So the regulatory frameworks

involves set of legal guidelines and regulation that are formed by UK legal authorities. So

companies are bounded to follow these rule as it help in ascertaining actual position at a

particular time. On the other side conceptual frameworks is defined as a analytical tool that is

implemented by an organisation in order to determine the entire information about performance

during an accounting year. In Mark & Spencer the regulation formed by IASB are followed

because, it support stakeholder to examine and measure the overall performance. The basic need

and purpose of framework are described below:

It help companies to prepare annual financial statements with the application of IFRS.

These framework are useful in development of Future IFRS and set rule for existing one.

This help manager to make a specific accounting treatment and avoid other alternative for

recording various transaction that happened in company (Eker and Aytaç, 2016).

The conceptual and regulatory frameworks have some advantages for companies that are

discussed below.

Qualitative features of financial information: The main features of financial

information that helps to make the content more reliable. It can be understood with the help of

following points:

Relevance: It is very crucial for the institution to post applicable data in the financial

report so that it may assist to examine actual execution and financial position.

2

different activity.

External stakeholder are able to analyse or examine that weather their money is

effectively used or not (Duncan, 2014).

Decently managed financial reports are crucial for invitation, labour contracts and

government supplying, as it give summary of the enterprises to outside parties.

Generic aim of financial reporting is to examine the result of those activity that have been

performed by company during a particular period.

2. Requirement, purpose and key principles of regulatory and conceptual framework

In accounting, it is very important for an organisation to follow the quantitative and

qualitative framework in order to prepare their annual statements. So the regulatory frameworks

involves set of legal guidelines and regulation that are formed by UK legal authorities. So

companies are bounded to follow these rule as it help in ascertaining actual position at a

particular time. On the other side conceptual frameworks is defined as a analytical tool that is

implemented by an organisation in order to determine the entire information about performance

during an accounting year. In Mark & Spencer the regulation formed by IASB are followed

because, it support stakeholder to examine and measure the overall performance. The basic need

and purpose of framework are described below:

It help companies to prepare annual financial statements with the application of IFRS.

These framework are useful in development of Future IFRS and set rule for existing one.

This help manager to make a specific accounting treatment and avoid other alternative for

recording various transaction that happened in company (Eker and Aytaç, 2016).

The conceptual and regulatory frameworks have some advantages for companies that are

discussed below.

Qualitative features of financial information: The main features of financial

information that helps to make the content more reliable. It can be understood with the help of

following points:

Relevance: It is very crucial for the institution to post applicable data in the financial

report so that it may assist to examine actual execution and financial position.

2

Faithful representation: This attribute help to advantage trust of shareholder like

capitalist and stockholder as it assist them to ensure that structure is in good status and

they may get long term welfare like investments.

So M&S follows these standard that assist company to operate their business at global

level. This will also support company to increased investment and expand market share.

3. Main Stakeholders of an organisation and their benefits from financial information.

Stakeholder

The internal and external parties of an enterprises that have the power to receive and

examine the current and accurate financial statements of an accounting year are known as

stakeholder. They are categorise in various types such as creditor, employees, supplier,

government bodies and other investor from where company utilize its resources. Whenever

company perform an action, set policies and objective stakeholder might get affected. All

corporate stakeholder requires statements that help them to analyse equity investment which

support to take informed decision. Basically there are two types of stakeholder for company that

are described below:

Internal stakeholder:

Those individual or group that have direct relation with company are internal stakeholder

(Elbayoumi and Awadallah, 2017). They are basically employees, board of director etc. which

formulate effective plans, produce good and manage project and operation. Some are discussed

underneath:

Board of director:

They have the power to control and investigate the internal management of company.

They gather information for different sources within organisation to analyse the performance of

employee and make plans for improvement. Board of director of M&S requires financial

information and statements to make effective decision.

Auditor

An auditor examine the financial statements of an enterprises that help them to ascertain

the difference in statement and make modification to resolve these differences.

External stakeholders

3

capitalist and stockholder as it assist them to ensure that structure is in good status and

they may get long term welfare like investments.

So M&S follows these standard that assist company to operate their business at global

level. This will also support company to increased investment and expand market share.

3. Main Stakeholders of an organisation and their benefits from financial information.

Stakeholder

The internal and external parties of an enterprises that have the power to receive and

examine the current and accurate financial statements of an accounting year are known as

stakeholder. They are categorise in various types such as creditor, employees, supplier,

government bodies and other investor from where company utilize its resources. Whenever

company perform an action, set policies and objective stakeholder might get affected. All

corporate stakeholder requires statements that help them to analyse equity investment which

support to take informed decision. Basically there are two types of stakeholder for company that

are described below:

Internal stakeholder:

Those individual or group that have direct relation with company are internal stakeholder

(Elbayoumi and Awadallah, 2017). They are basically employees, board of director etc. which

formulate effective plans, produce good and manage project and operation. Some are discussed

underneath:

Board of director:

They have the power to control and investigate the internal management of company.

They gather information for different sources within organisation to analyse the performance of

employee and make plans for improvement. Board of director of M&S requires financial

information and statements to make effective decision.

Auditor

An auditor examine the financial statements of an enterprises that help them to ascertain

the difference in statement and make modification to resolve these differences.

External stakeholders

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Those stakeholder those are not effected by the business directly. External stakeholder

make a large impact on the decision making process of company. Some of these are described

below:

Customer

Customer are consider to be the backbone of company and their decision have a direct

impact on the business of company. These external stakeholder prefer to make investment or buy

product for companies that have good financial position and produces goods that satisfy them

most (Formisano, Fedele and Calabrese, 2018).

Shareholder

Shareholder or owner are the one who buy company share and make direct impact on the

company. Therefore it is very crucial for company to provide accurate financial statements that

make shareholder aware about the financial status and market position of company.

4. Value of financial reporting

In present era, it is very crucial for company to prepare a detail, accurate, faithful

financial statements that help in attainment of annual goals and determine opportunities for

growth and development. These statement must be prepared by applying General accepted

accounting standard so that business can be performed at global level. In M&S internal manager

formulate financial statements for external stakeholder so that they show more interest in

company and make investment decision. It is very common that a company that display more

accurate financial report and statements and performing well in market have possibility to have

large number of investor.

As Mark & Spencer prepare and keep appropriate record of their overall dealing, this aid

stakeholder to examine their performance and make investment within company. It is possible

that if customer are more satisfied with the company product then market share will be going to

expand for M&S. With the help of accurate and transparent financial statement manager able to

measured competitive advantages in market. One more advantage of financial statements for

M&S that it help in maximising profit by performing good in market and producing those

product that are mostly demanded by customer (Guo, 2018). Manager of company are able to

ascertain the development possibility and grab them in order to make effective plan to achieve

these possibility.

4

make a large impact on the decision making process of company. Some of these are described

below:

Customer

Customer are consider to be the backbone of company and their decision have a direct

impact on the business of company. These external stakeholder prefer to make investment or buy

product for companies that have good financial position and produces goods that satisfy them

most (Formisano, Fedele and Calabrese, 2018).

Shareholder

Shareholder or owner are the one who buy company share and make direct impact on the

company. Therefore it is very crucial for company to provide accurate financial statements that

make shareholder aware about the financial status and market position of company.

4. Value of financial reporting

In present era, it is very crucial for company to prepare a detail, accurate, faithful

financial statements that help in attainment of annual goals and determine opportunities for

growth and development. These statement must be prepared by applying General accepted

accounting standard so that business can be performed at global level. In M&S internal manager

formulate financial statements for external stakeholder so that they show more interest in

company and make investment decision. It is very common that a company that display more

accurate financial report and statements and performing well in market have possibility to have

large number of investor.

As Mark & Spencer prepare and keep appropriate record of their overall dealing, this aid

stakeholder to examine their performance and make investment within company. It is possible

that if customer are more satisfied with the company product then market share will be going to

expand for M&S. With the help of accurate and transparent financial statement manager able to

measured competitive advantages in market. One more advantage of financial statements for

M&S that it help in maximising profit by performing good in market and producing those

product that are mostly demanded by customer (Guo, 2018). Manager of company are able to

ascertain the development possibility and grab them in order to make effective plan to achieve

these possibility.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5. Financial statements of the organisation

A: Statement of profit and loss:

Consolidated statement of profit or loss

Continuing operations

Revenue 385100.00

Cost of sales of goods 291700.00

Gross Profit 93400.00

Operating Expenses 78500.00

Operating Profits 14900.00

Finance Income 5600.00

Finance Cost 830.00

Profit before income tax 19670.00

Income tax expenses 15000.00

Profit after tax 4670.00

Dividend

Equity 830.00

Preference 2330.00

Retained Earning 1510.00

P&L account are prepared by the companies in an accounting year in order to determine

the actual profit. The profit is ascertain by making all relevant adjustment like, tax and other

expenses. From the above mention Profit and loss account the gross profit for company is 93400

and operating profit is 14900. The profit of company before deducting income tax is 19670 and

the actual profit of company after deducting taxes is 4670. The P&L statements shows retained

earning of amount 1510 (Haneef and Smolo, 2014).

B: Statement of financial position:

Financial Statement

5

A: Statement of profit and loss:

Consolidated statement of profit or loss

Continuing operations

Revenue 385100.00

Cost of sales of goods 291700.00

Gross Profit 93400.00

Operating Expenses 78500.00

Operating Profits 14900.00

Finance Income 5600.00

Finance Cost 830.00

Profit before income tax 19670.00

Income tax expenses 15000.00

Profit after tax 4670.00

Dividend

Equity 830.00

Preference 2330.00

Retained Earning 1510.00

P&L account are prepared by the companies in an accounting year in order to determine

the actual profit. The profit is ascertain by making all relevant adjustment like, tax and other

expenses. From the above mention Profit and loss account the gross profit for company is 93400

and operating profit is 14900. The profit of company before deducting income tax is 19670 and

the actual profit of company after deducting taxes is 4670. The P&L statements shows retained

earning of amount 1510 (Haneef and Smolo, 2014).

B: Statement of financial position:

Financial Statement

5

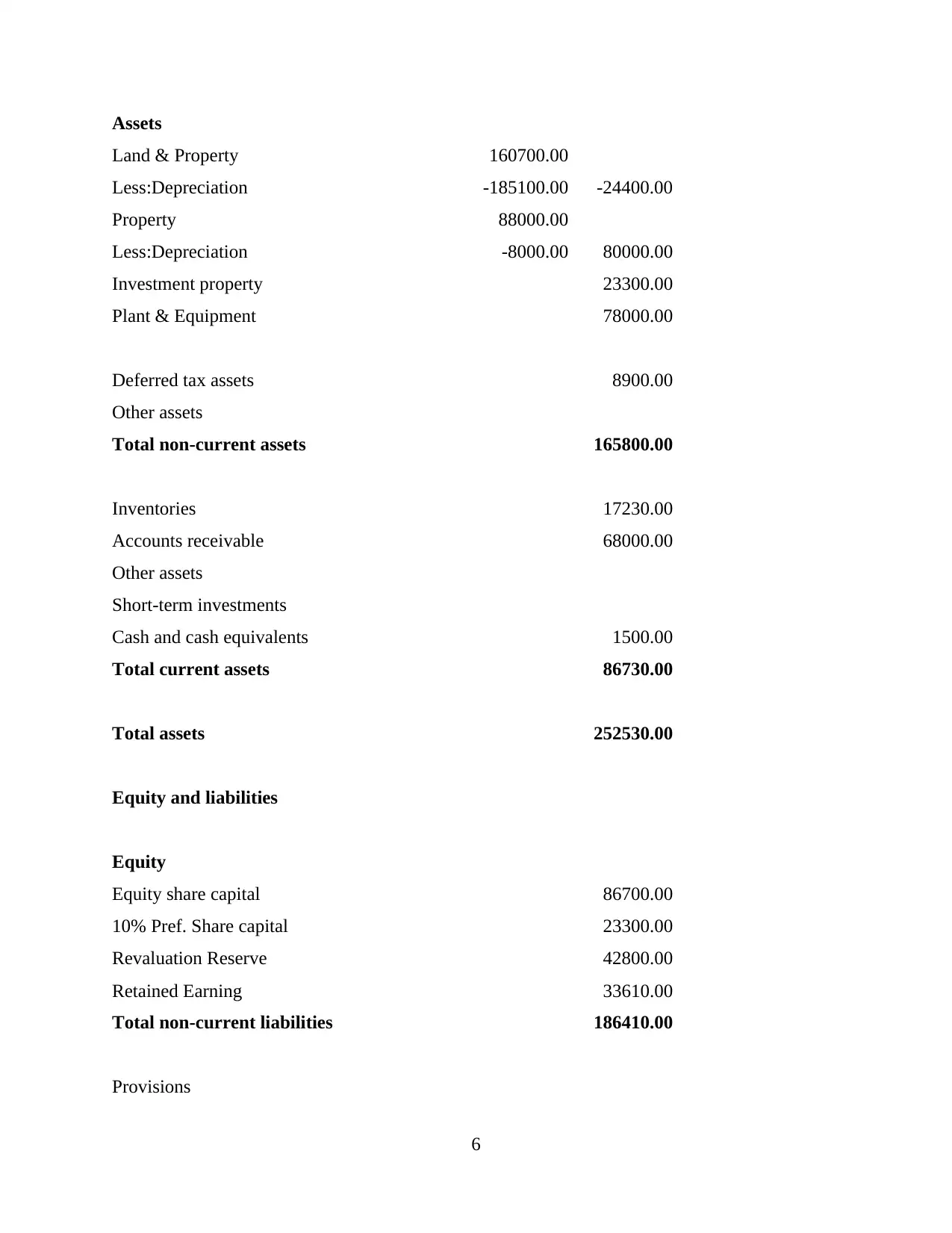

Assets

Land & Property 160700.00

Less:Depreciation -185100.00 -24400.00

Property 88000.00

Less:Depreciation -8000.00 80000.00

Investment property 23300.00

Plant & Equipment 78000.00

Deferred tax assets 8900.00

Other assets

Total non-current assets 165800.00

Inventories 17230.00

Accounts receivable 68000.00

Other assets

Short-term investments

Cash and cash equivalents 1500.00

Total current assets 86730.00

Total assets 252530.00

Equity and liabilities

Equity

Equity share capital 86700.00

10% Pref. Share capital 23300.00

Revaluation Reserve 42800.00

Retained Earning 33610.00

Total non-current liabilities 186410.00

Provisions

6

Land & Property 160700.00

Less:Depreciation -185100.00 -24400.00

Property 88000.00

Less:Depreciation -8000.00 80000.00

Investment property 23300.00

Plant & Equipment 78000.00

Deferred tax assets 8900.00

Other assets

Total non-current assets 165800.00

Inventories 17230.00

Accounts receivable 68000.00

Other assets

Short-term investments

Cash and cash equivalents 1500.00

Total current assets 86730.00

Total assets 252530.00

Equity and liabilities

Equity

Equity share capital 86700.00

10% Pref. Share capital 23300.00

Revaluation Reserve 42800.00

Retained Earning 33610.00

Total non-current liabilities 186410.00

Provisions

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounts payable 66120.00

Total current liabilities 66120.00

Total equity and liabilities 252530.00

The above mention balance sheet describe the actual cash position of company during an

accounting year. The balance sheet shows the total assets and liabilities held within company at a

particular time. Total current assets of company shows the balance of 86730 and non current

assets are equal to 165800 during a year. And the balance of total assets are 252530. The total

balance of non current liabilities are 186410 and current assets is 66120. And the total equity and

liabilities for an accounting year are 252530.

6. Use of financial statements.

From the appendix, it has been analysed that Mark & Spencer were 10622000 during

2017 and increase to 10698200 at the end of year 2018. It has been observed that profit for year

2017 is 3992700 and increased up to 3952600 in year 2018. The balance of total operating

expenses were 10020800 in 2018 and income from operation has diminished to 6677400 in

2018. Net profit has been decreased from 2017 which was 117100 to 25700 in year 2018. cash of

company has been also decreased up to 207700 (Li and Yang, 2015). The balance of total current

assets of company has been decreased as current assets were 1723300 in year 2017 that reduces

to 1323300 and total assets shows the balance of 7550200 in year 2018. It has been observed that

capital surplus for both year were same and the shareholder equity have been decreased up to

2956700 in year 2018. There are many other related information gather from financial statements

that shows that financial year 2018 is not good for company. Manager need to formulae effective

polices to overcome losses.

Financial ratios of Marks and Spencer

Particular ratios Formula 2017 2018

Liquidity ratio’s:

Current ratio: Current asset/ current liabilities

0.7217415

115

0.7277449

324

Liquid ratio: Current asset- inventory+ prepaid 0.2940306 0.4073057

7

Total current liabilities 66120.00

Total equity and liabilities 252530.00

The above mention balance sheet describe the actual cash position of company during an

accounting year. The balance sheet shows the total assets and liabilities held within company at a

particular time. Total current assets of company shows the balance of 86730 and non current

assets are equal to 165800 during a year. And the balance of total assets are 252530. The total

balance of non current liabilities are 186410 and current assets is 66120. And the total equity and

liabilities for an accounting year are 252530.

6. Use of financial statements.

From the appendix, it has been analysed that Mark & Spencer were 10622000 during

2017 and increase to 10698200 at the end of year 2018. It has been observed that profit for year

2017 is 3992700 and increased up to 3952600 in year 2018. The balance of total operating

expenses were 10020800 in 2018 and income from operation has diminished to 6677400 in

2018. Net profit has been decreased from 2017 which was 117100 to 25700 in year 2018. cash of

company has been also decreased up to 207700 (Li and Yang, 2015). The balance of total current

assets of company has been decreased as current assets were 1723300 in year 2017 that reduces

to 1323300 and total assets shows the balance of 7550200 in year 2018. It has been observed that

capital surplus for both year were same and the shareholder equity have been decreased up to

2956700 in year 2018. There are many other related information gather from financial statements

that shows that financial year 2018 is not good for company. Manager need to formulae effective

polices to overcome losses.

Financial ratios of Marks and Spencer

Particular ratios Formula 2017 2018

Liquidity ratio’s:

Current ratio: Current asset/ current liabilities

0.7217415

115

0.7277449

324

Liquid ratio: Current asset- inventory+ prepaid 0.2940306 0.4073057

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

expenses/ Current liabilities 681 432

Profitability ratio

Net profit ratio: Net profit / Sales *100

1.0892487

291 0.272008

Gross profit ratios Gross profit/ Sales *100

2.3837318

772

1.4628629

115

ROE Total income/ shareholder equity

0.0224313

278

0.0310481

28

Efficiency ratio's

Total assets turnover

ratios Net sales/ average total assets

1.0983443

709

1.4169161

082

Fixed assets turnover Net sales/ Averages total fixed assets

1.6169396

578

1.7165412

448

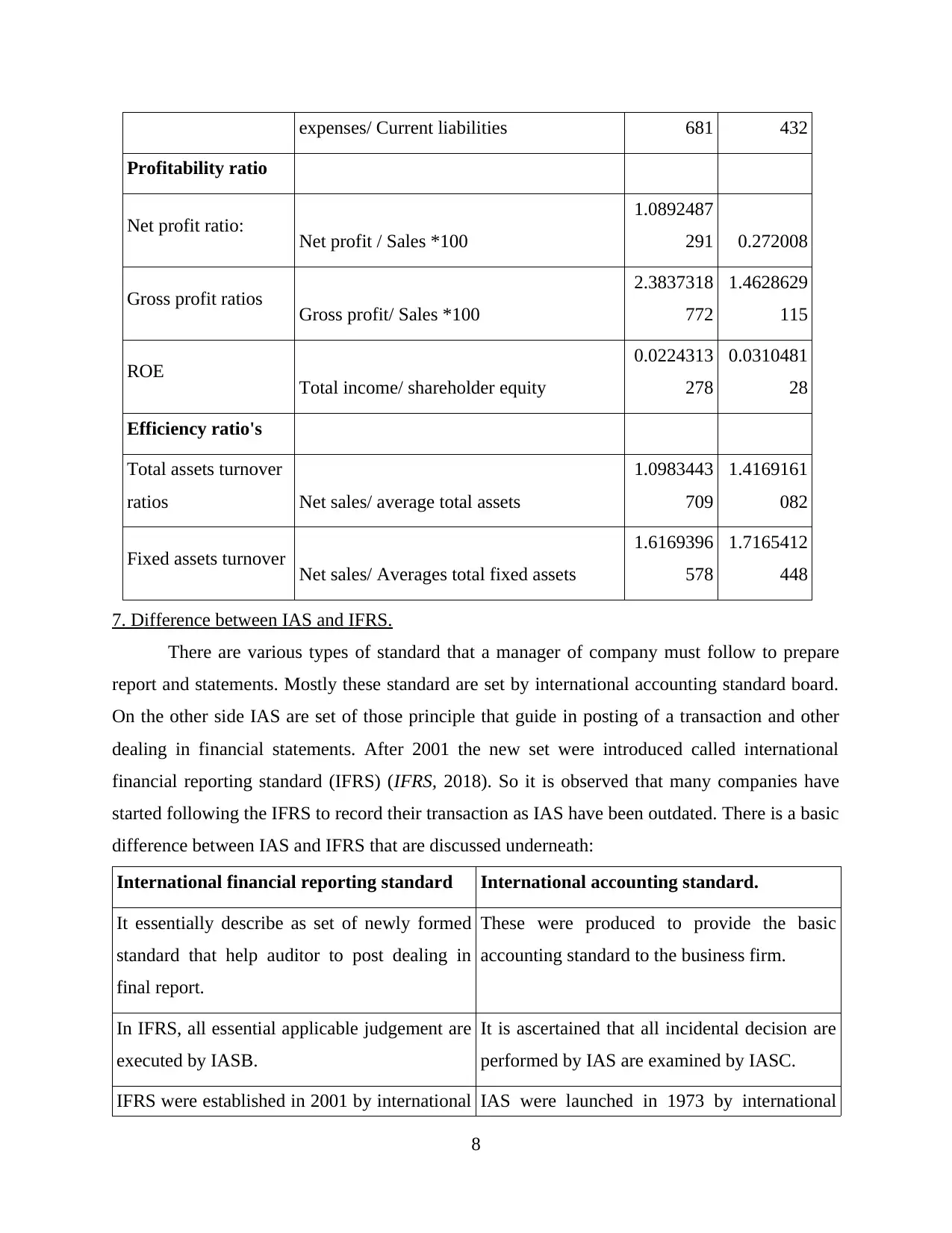

7. Difference between IAS and IFRS.

There are various types of standard that a manager of company must follow to prepare

report and statements. Mostly these standard are set by international accounting standard board.

On the other side IAS are set of those principle that guide in posting of a transaction and other

dealing in financial statements. After 2001 the new set were introduced called international

financial reporting standard (IFRS) (IFRS, 2018). So it is observed that many companies have

started following the IFRS to record their transaction as IAS have been outdated. There is a basic

difference between IAS and IFRS that are discussed underneath:

International financial reporting standard International accounting standard.

It essentially describe as set of newly formed

standard that help auditor to post dealing in

final report.

These were produced to provide the basic

accounting standard to the business firm.

In IFRS, all essential applicable judgement are

executed by IASB.

It is ascertained that all incidental decision are

performed by IAS are examined by IASC.

IFRS were established in 2001 by international IAS were launched in 1973 by international

8

Profitability ratio

Net profit ratio: Net profit / Sales *100

1.0892487

291 0.272008

Gross profit ratios Gross profit/ Sales *100

2.3837318

772

1.4628629

115

ROE Total income/ shareholder equity

0.0224313

278

0.0310481

28

Efficiency ratio's

Total assets turnover

ratios Net sales/ average total assets

1.0983443

709

1.4169161

082

Fixed assets turnover Net sales/ Averages total fixed assets

1.6169396

578

1.7165412

448

7. Difference between IAS and IFRS.

There are various types of standard that a manager of company must follow to prepare

report and statements. Mostly these standard are set by international accounting standard board.

On the other side IAS are set of those principle that guide in posting of a transaction and other

dealing in financial statements. After 2001 the new set were introduced called international

financial reporting standard (IFRS) (IFRS, 2018). So it is observed that many companies have

started following the IFRS to record their transaction as IAS have been outdated. There is a basic

difference between IAS and IFRS that are discussed underneath:

International financial reporting standard International accounting standard.

It essentially describe as set of newly formed

standard that help auditor to post dealing in

final report.

These were produced to provide the basic

accounting standard to the business firm.

In IFRS, all essential applicable judgement are

executed by IASB.

It is ascertained that all incidental decision are

performed by IAS are examined by IASC.

IFRS were established in 2001 by international IAS were launched in 1973 by international

8

accounting standard board. accounting standard committee.

There is same main significance valuable noting, is that any rule inside IFRS found to be

conflicting, that will be definitely regenerate those of the IAS. Basically, when opposed

standards are published, older ones are normally regard.

8. Evaluation of benefits of IFRS

In present era, business world is becoming focused in respect to apply different rules and

regulation in order to record and maintain financial statements. The manager of company

consider all the related guidelines and rules to perform various business activities. Recently

almost every companies apply generally accepted accounting standard principle towards

international financial reporting standard (IFRS). These IFRS state that every business happing

within an organisation is going to be posted in financial statements. It also explain in detail the

method related to posting of a transaction in annual statements and report. Thus, with the support

of these IFRS organisation are ease to resolve the accounting issue, detect error, within the

statements that might be a reason for diminishing profitability of company. IFRS help manager

of company to make effective plans and strategies that aid in maintaining long term, financial

sustainability. The execution of IFRS sort establishment businesses statements clear and

appropriate that benefits stockholder and capitalist to recognise more of company financial place

in current market. There are various advantages of IFRS that are described below:

Organisation implementing IFRS gives better display of their financial status to

shareholder. This support in making right investment decision (Mohd Nasir and et.al.,

2012).

The main advantage of IFRS is to create a language that is accepted at global level. This

will benefit investor to look at company financial potion at make decision from any part

of world.

The chief importance of using IFRS is that it assist in accelerator the money from the

abroad market at very cheap rate.

9. Ascertaining the varying degree of compliance

Nowadays it has been observed that IFRS are considering at the global level. These are

accepted by almost each nation that help various business enterprises manager to form and

represent financial statements. In recent time, there are 13 international financial accounting

9

There is same main significance valuable noting, is that any rule inside IFRS found to be

conflicting, that will be definitely regenerate those of the IAS. Basically, when opposed

standards are published, older ones are normally regard.

8. Evaluation of benefits of IFRS

In present era, business world is becoming focused in respect to apply different rules and

regulation in order to record and maintain financial statements. The manager of company

consider all the related guidelines and rules to perform various business activities. Recently

almost every companies apply generally accepted accounting standard principle towards

international financial reporting standard (IFRS). These IFRS state that every business happing

within an organisation is going to be posted in financial statements. It also explain in detail the

method related to posting of a transaction in annual statements and report. Thus, with the support

of these IFRS organisation are ease to resolve the accounting issue, detect error, within the

statements that might be a reason for diminishing profitability of company. IFRS help manager

of company to make effective plans and strategies that aid in maintaining long term, financial

sustainability. The execution of IFRS sort establishment businesses statements clear and

appropriate that benefits stockholder and capitalist to recognise more of company financial place

in current market. There are various advantages of IFRS that are described below:

Organisation implementing IFRS gives better display of their financial status to

shareholder. This support in making right investment decision (Mohd Nasir and et.al.,

2012).

The main advantage of IFRS is to create a language that is accepted at global level. This

will benefit investor to look at company financial potion at make decision from any part

of world.

The chief importance of using IFRS is that it assist in accelerator the money from the

abroad market at very cheap rate.

9. Ascertaining the varying degree of compliance

Nowadays it has been observed that IFRS are considering at the global level. These are

accepted by almost each nation that help various business enterprises manager to form and

represent financial statements. In recent time, there are 13 international financial accounting

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.