Audit Report: Analyzing Market Risk and Return for Cochlear and CSL

VerifiedAdded on 2020/07/23

|13

|2475

|59

Report

AI Summary

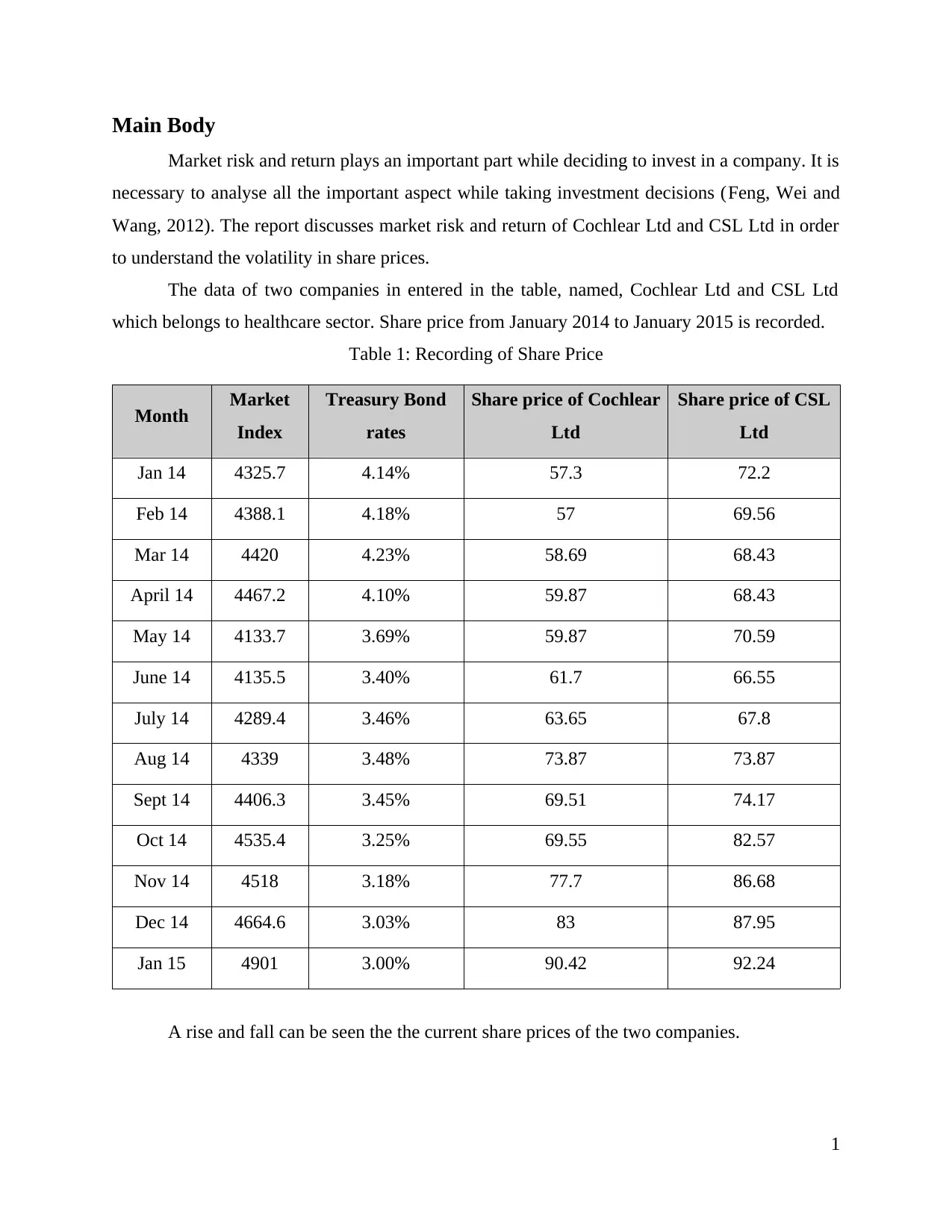

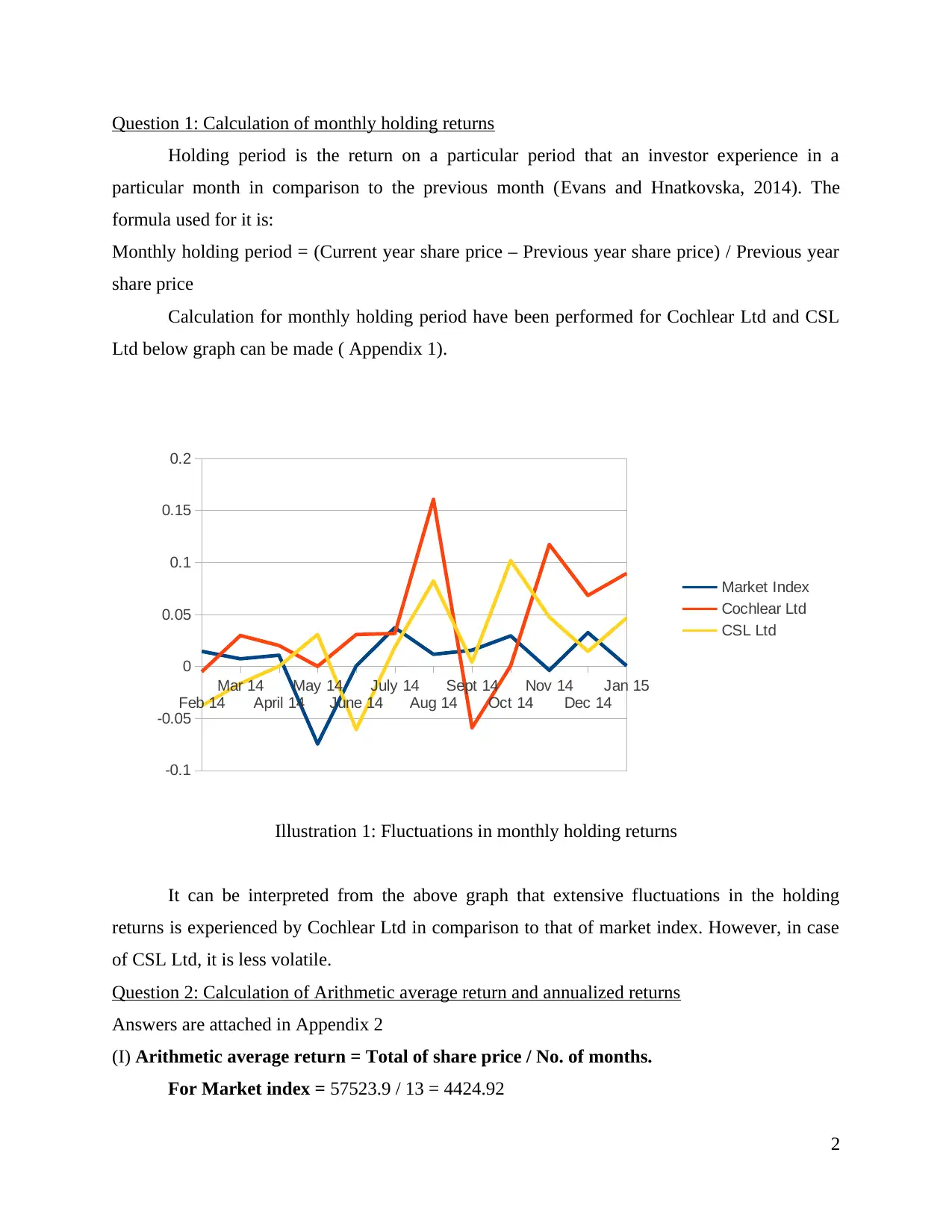

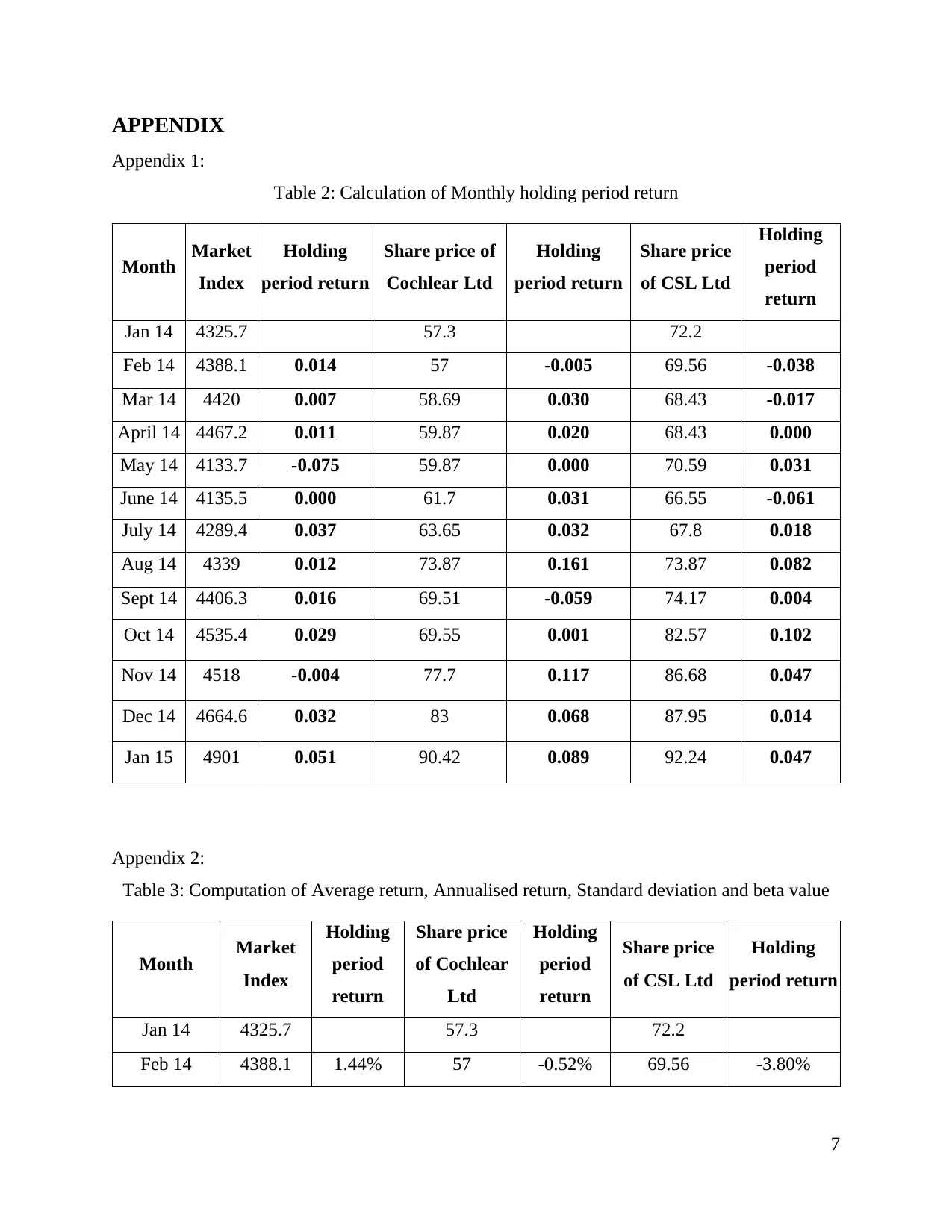

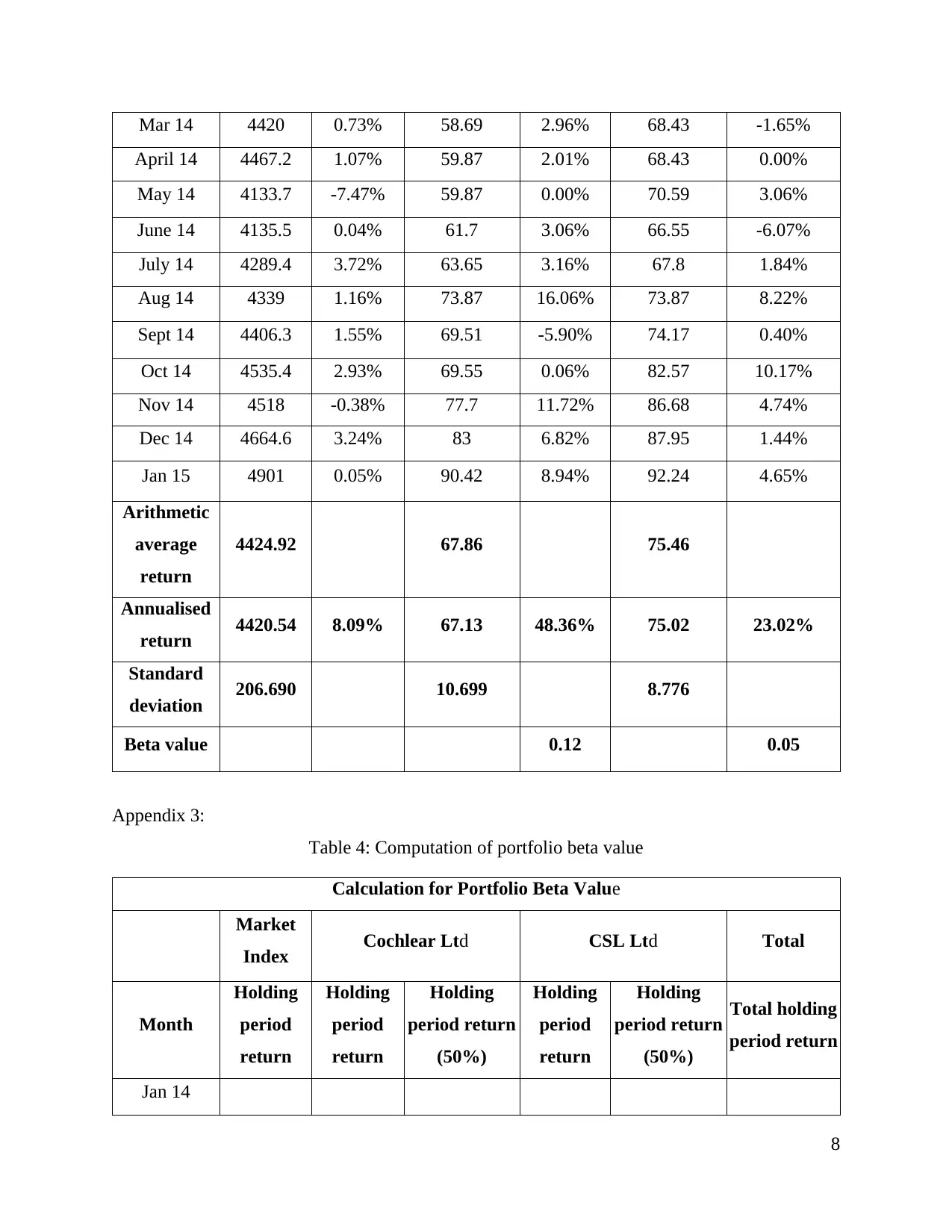

This audit report provides a detailed analysis of market risk and return for Cochlear Ltd and CSL Ltd, two companies in the healthcare sector. The report examines share price fluctuations from January 2014 to January 2015, calculating monthly holding returns, arithmetic average return, annualized returns, standard deviation, and beta values for both companies. It further assesses portfolio beta risk and the required rate of return using the CAPM model. The report concludes with a calculation of the Weighted Average Cost of Capital (WACC) for each company, providing a comprehensive financial evaluation for investment decision-making. The report includes tables and appendices with supporting data and calculations, offering a thorough examination of the companies' financial performance and risk profiles.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.