ECON11026 Principles: Market Structures, Firm Behavior and Analysis

VerifiedAdded on 2023/04/22

|13

|1772

|373

Homework Assignment

AI Summary

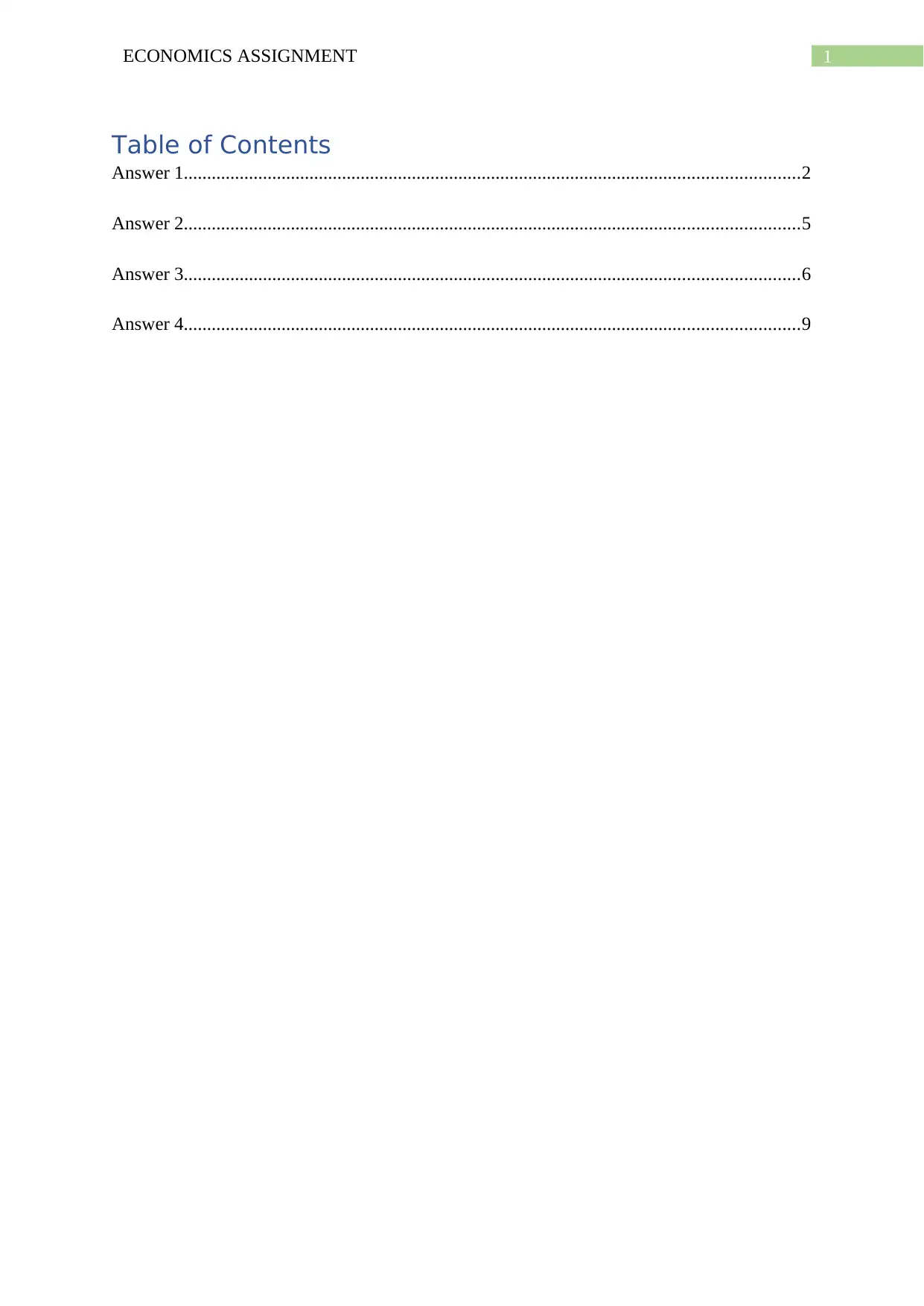

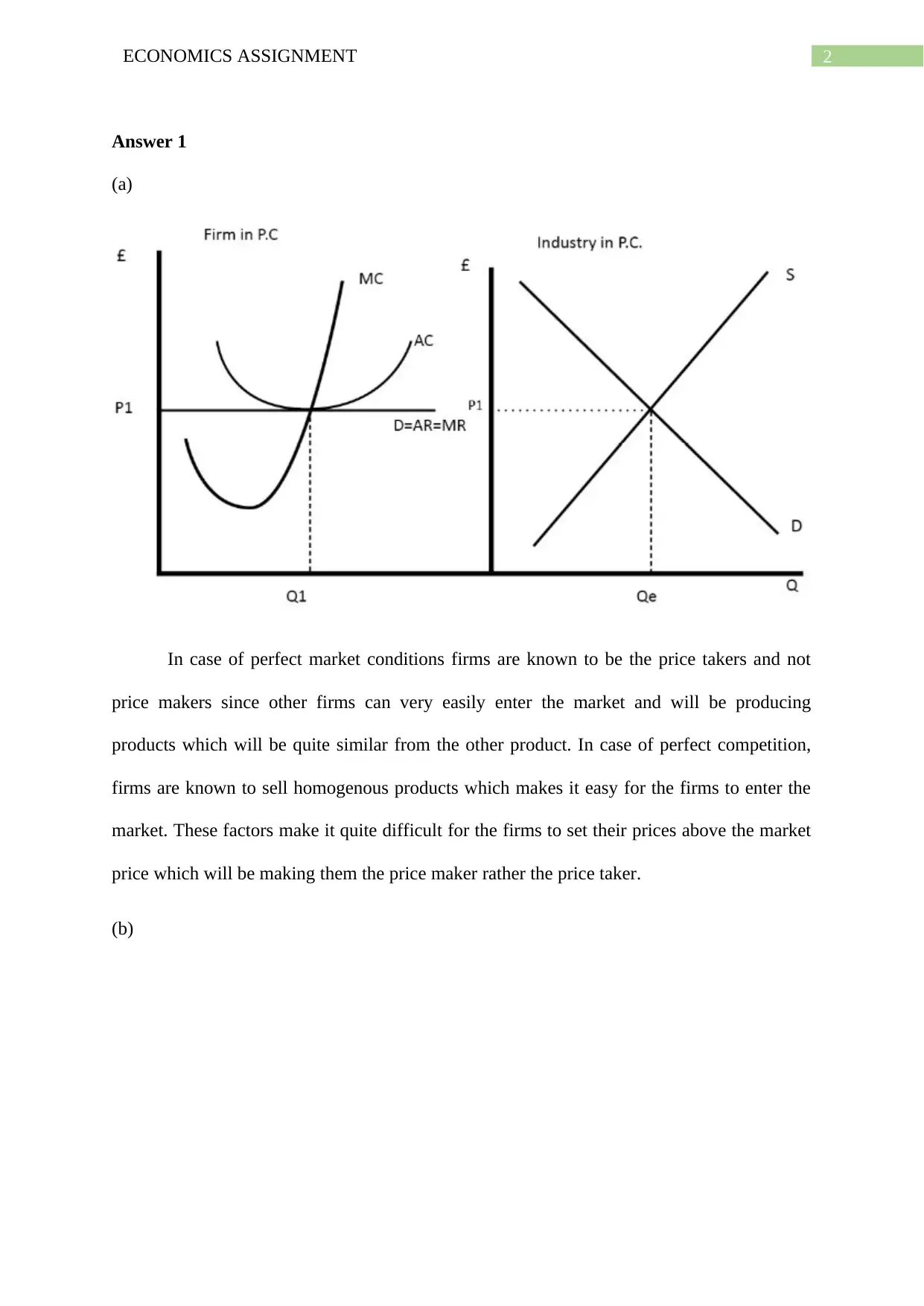

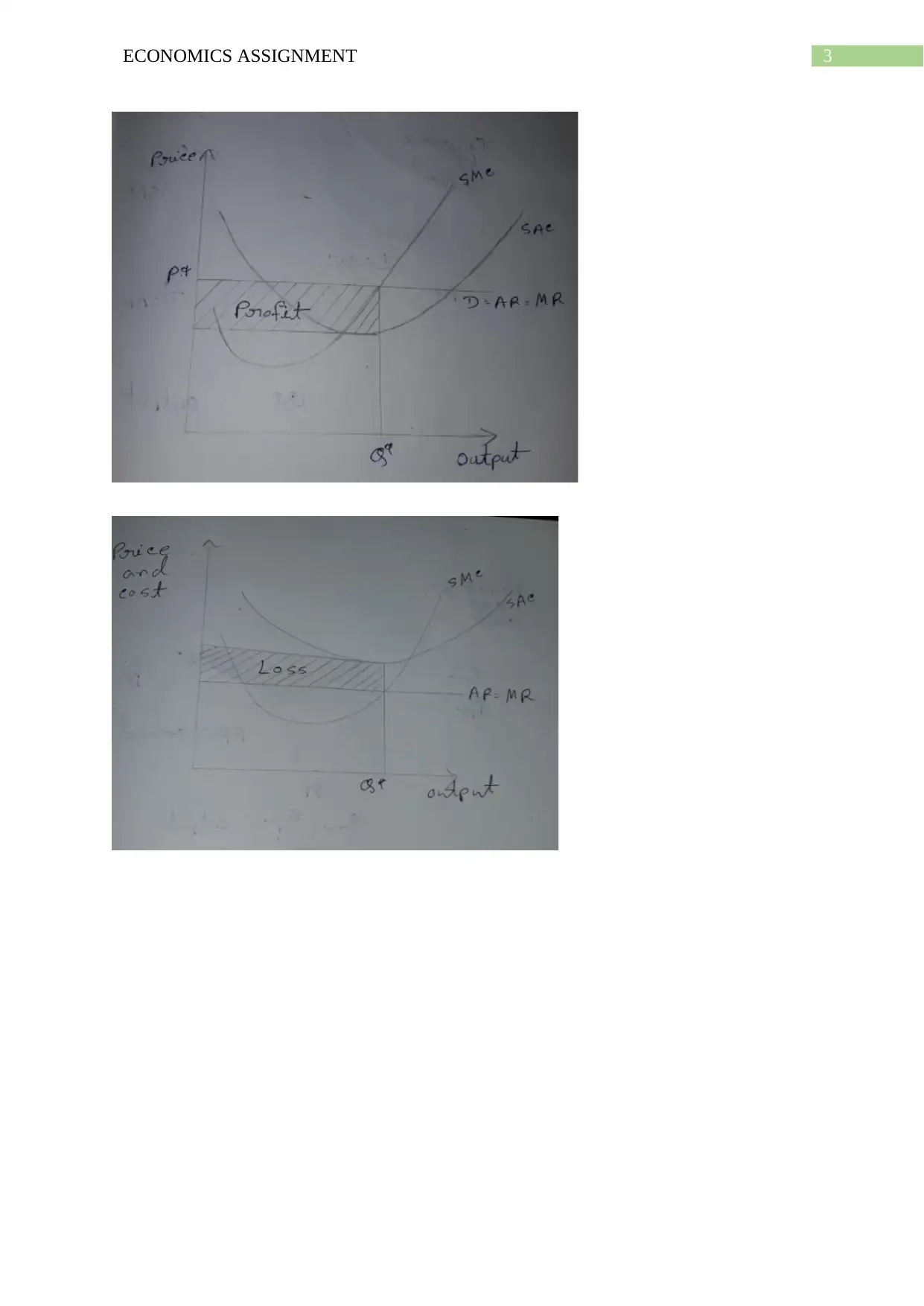

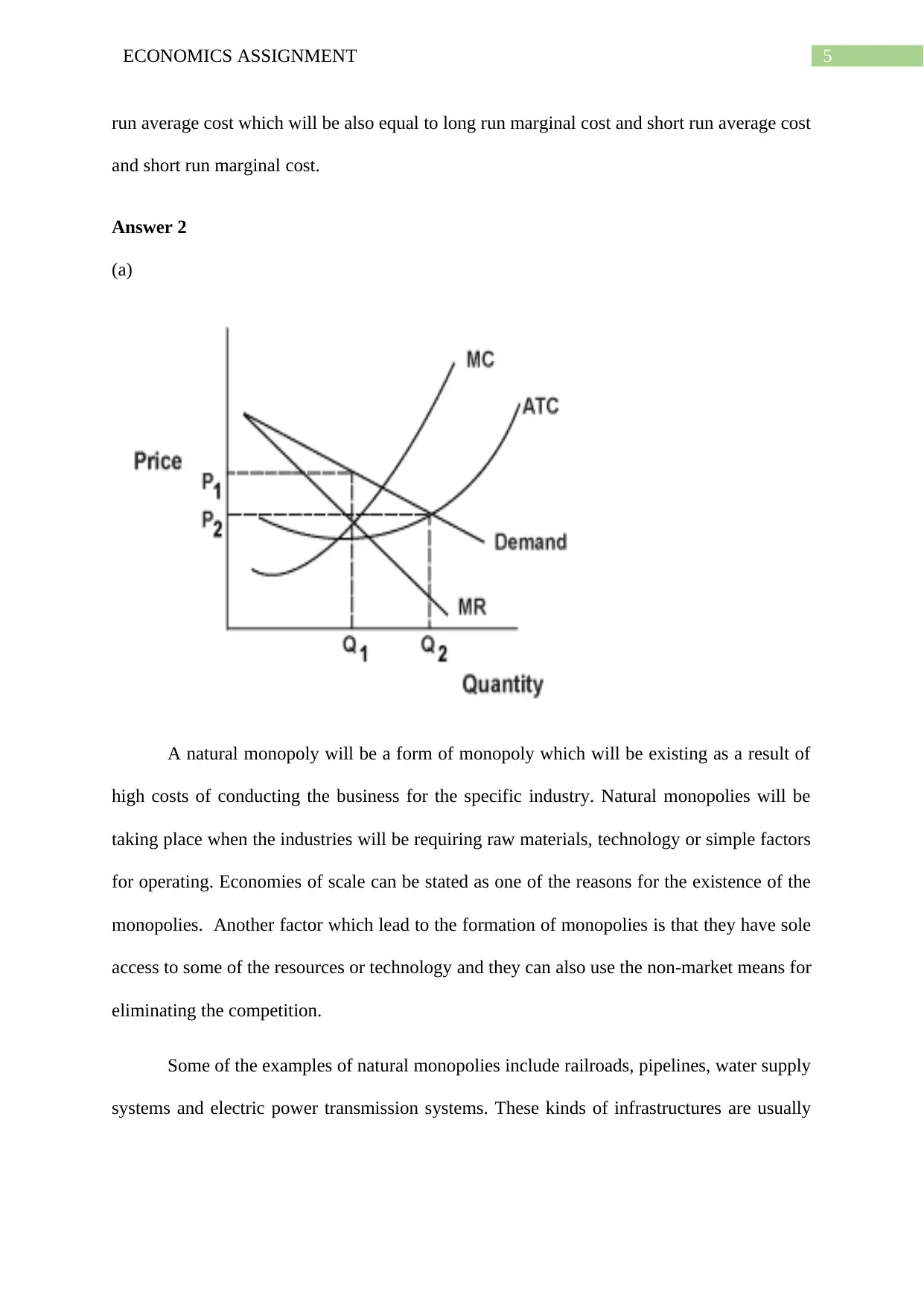

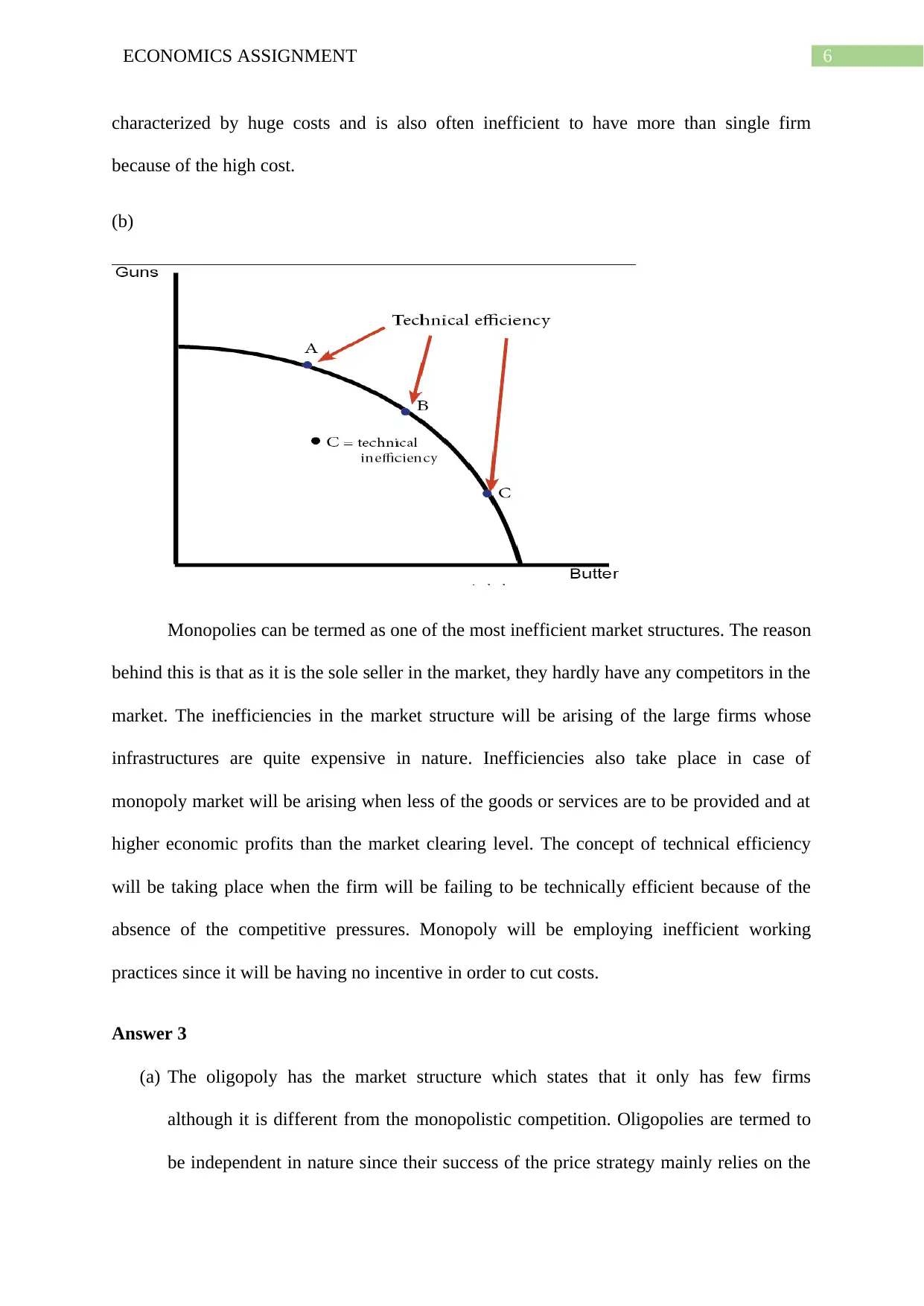

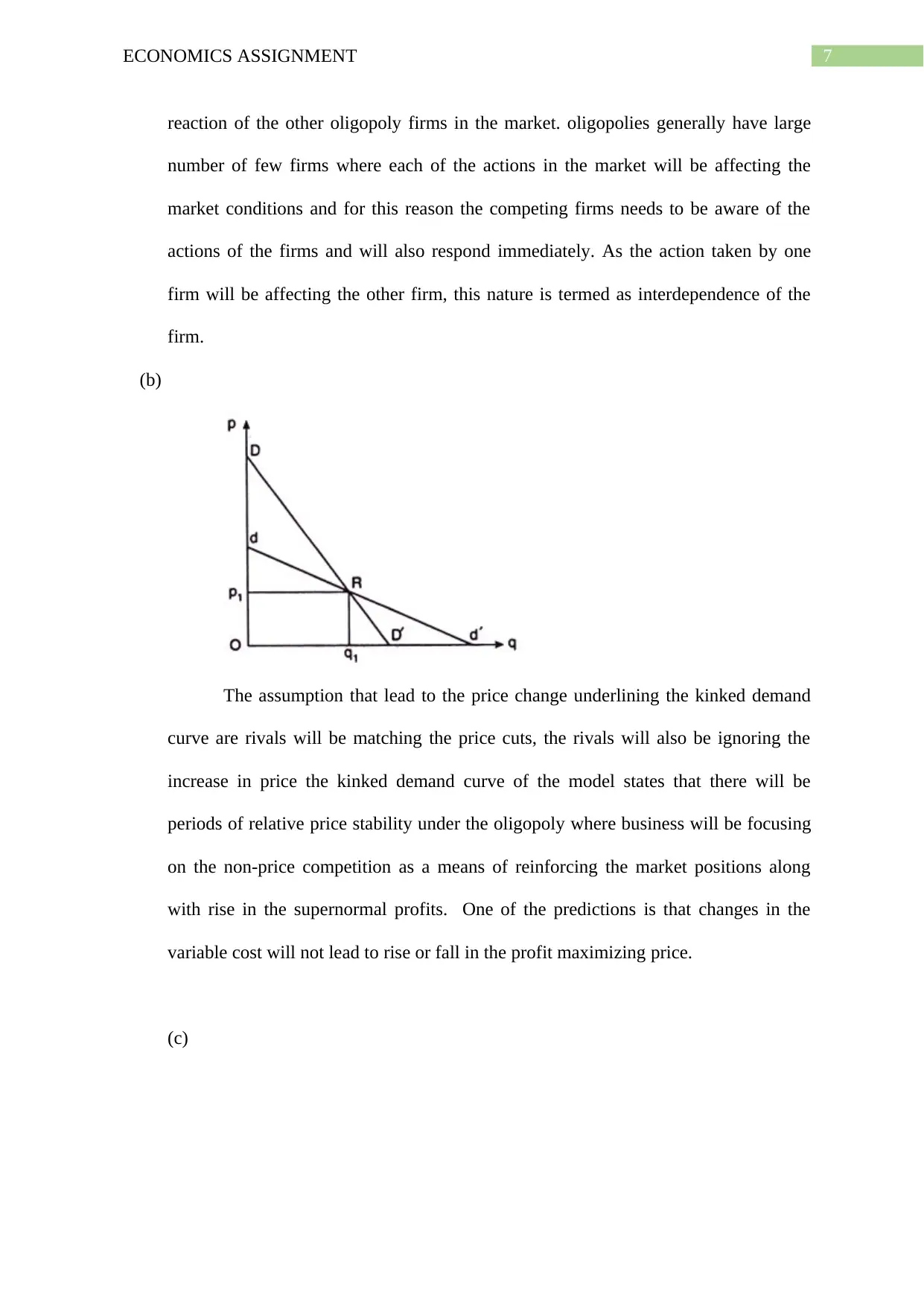

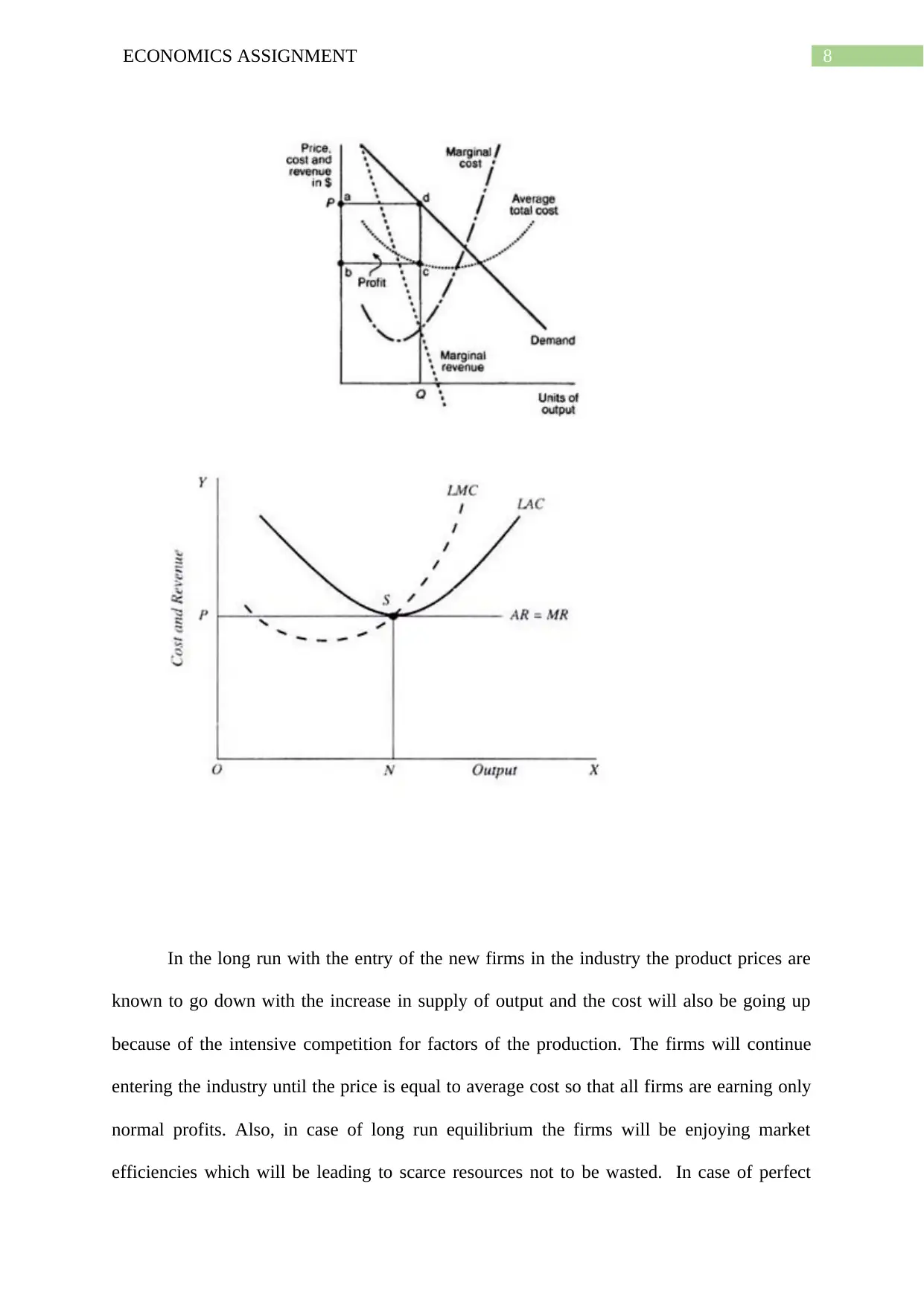

This economics assignment delves into various market structures, including perfect competition, natural monopolies, and oligopolies, analyzing firm behavior within each. It explains why perfectly competitive firms are price takers, illustrating short-run losses, short-run economic profits, and long-run normal profits with graphs. The document also discusses the inefficiencies associated with monopolies and the concept of interdependence in oligopolies. Furthermore, it contrasts monopolistic and perfectly competitive markets, highlighting differences in firm numbers, pricing strategies, and product homogeneity. Finally, the assignment classifies goods into private, public, common resources, and club goods, providing an analysis of marginal social benefit and cost in relation to environmental impact. This resource is available on Desklib, a platform offering a wide range of study tools and solved assignments for students.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.