Marketing and Management Assignment: Cost, Volume, Profit Analysis

VerifiedAdded on 2023/01/19

|14

|2069

|94

Homework Assignment

AI Summary

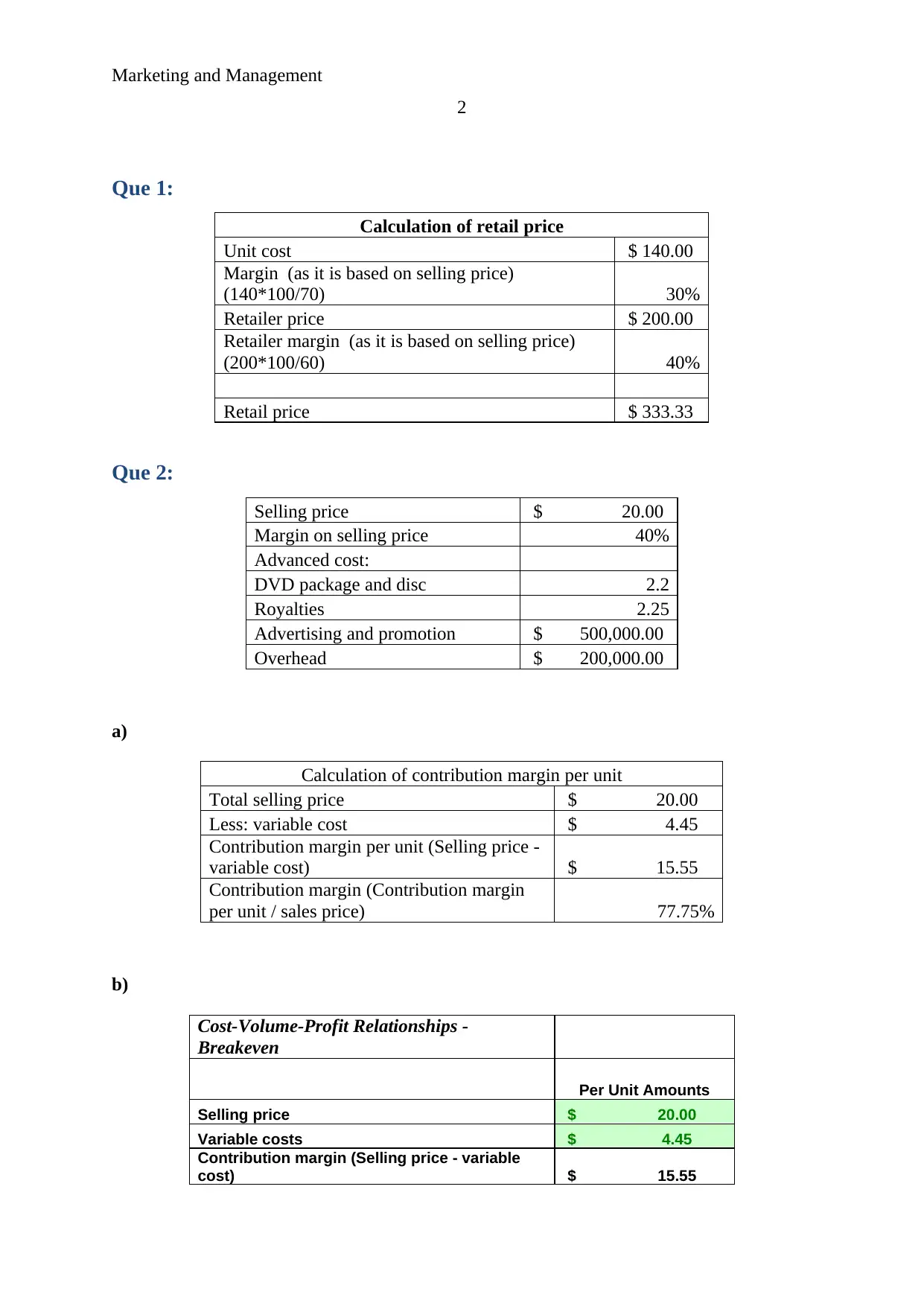

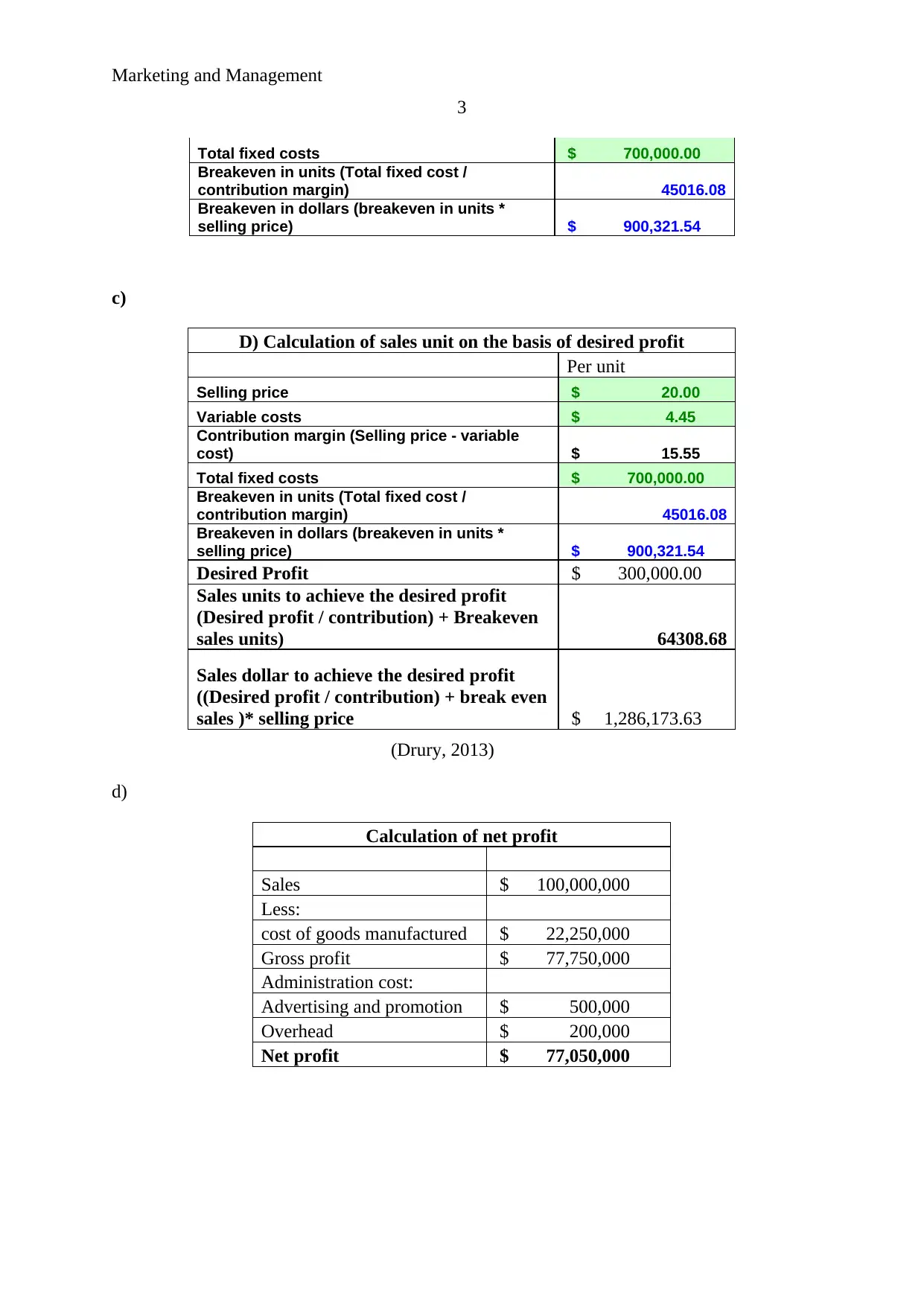

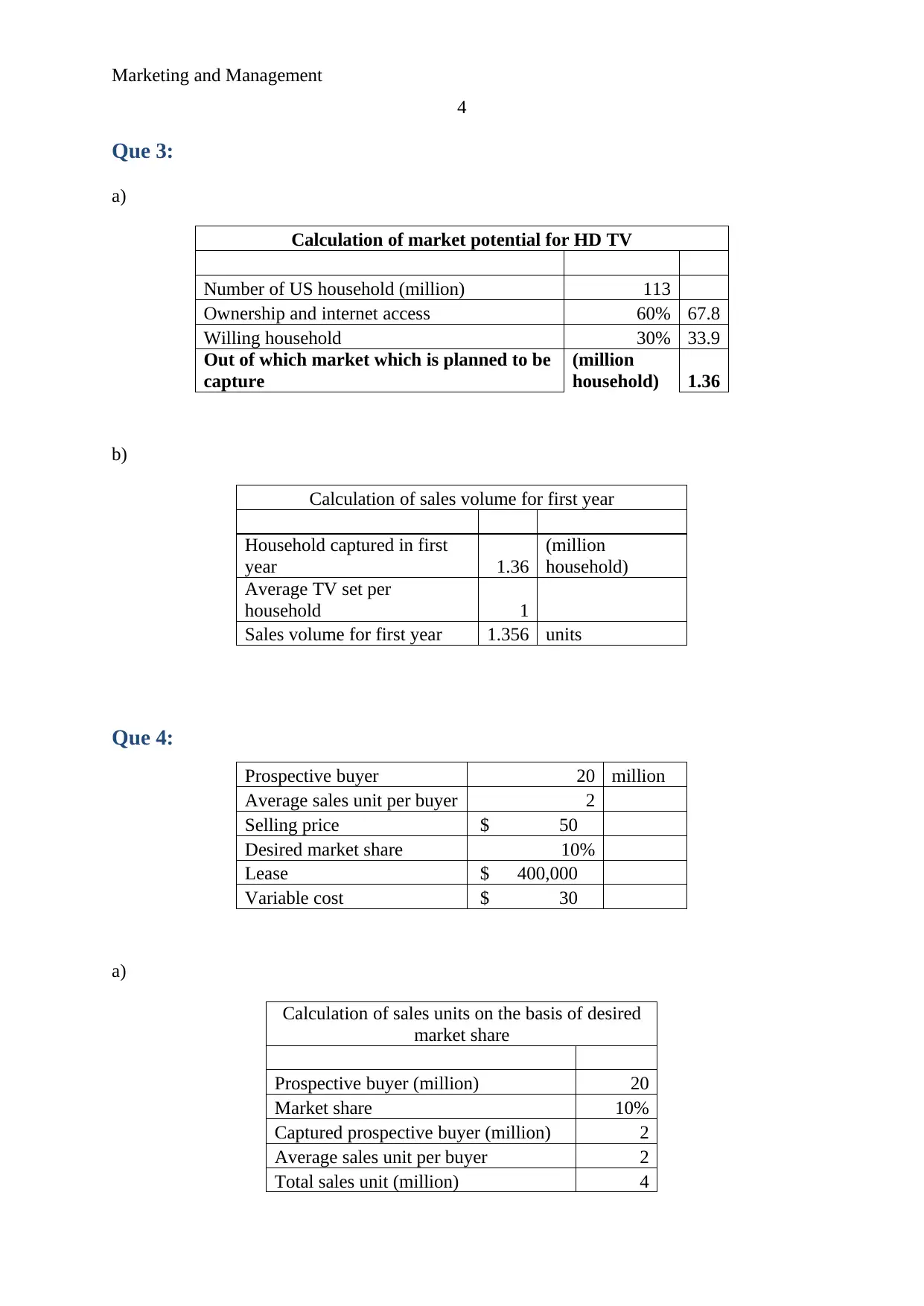

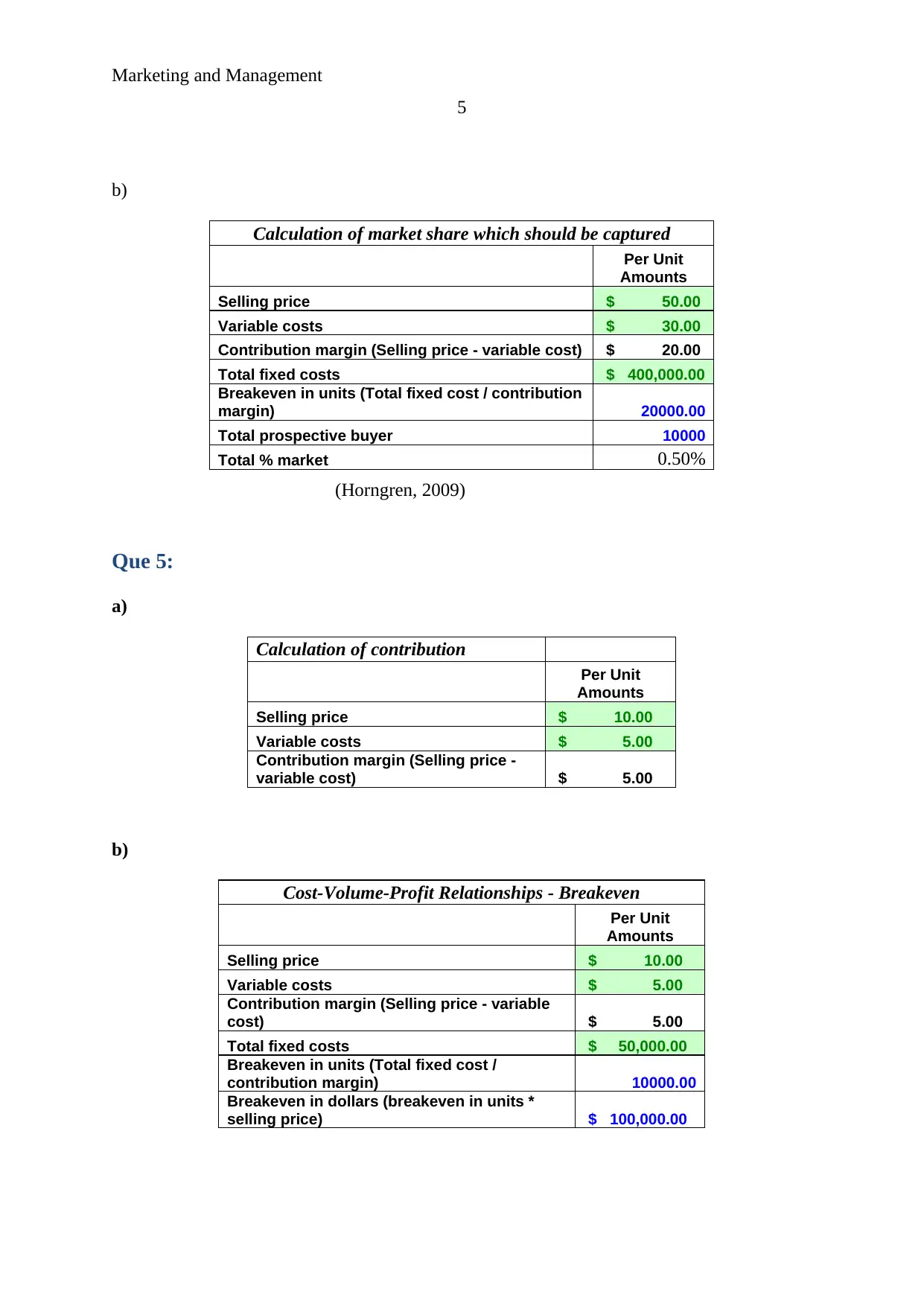

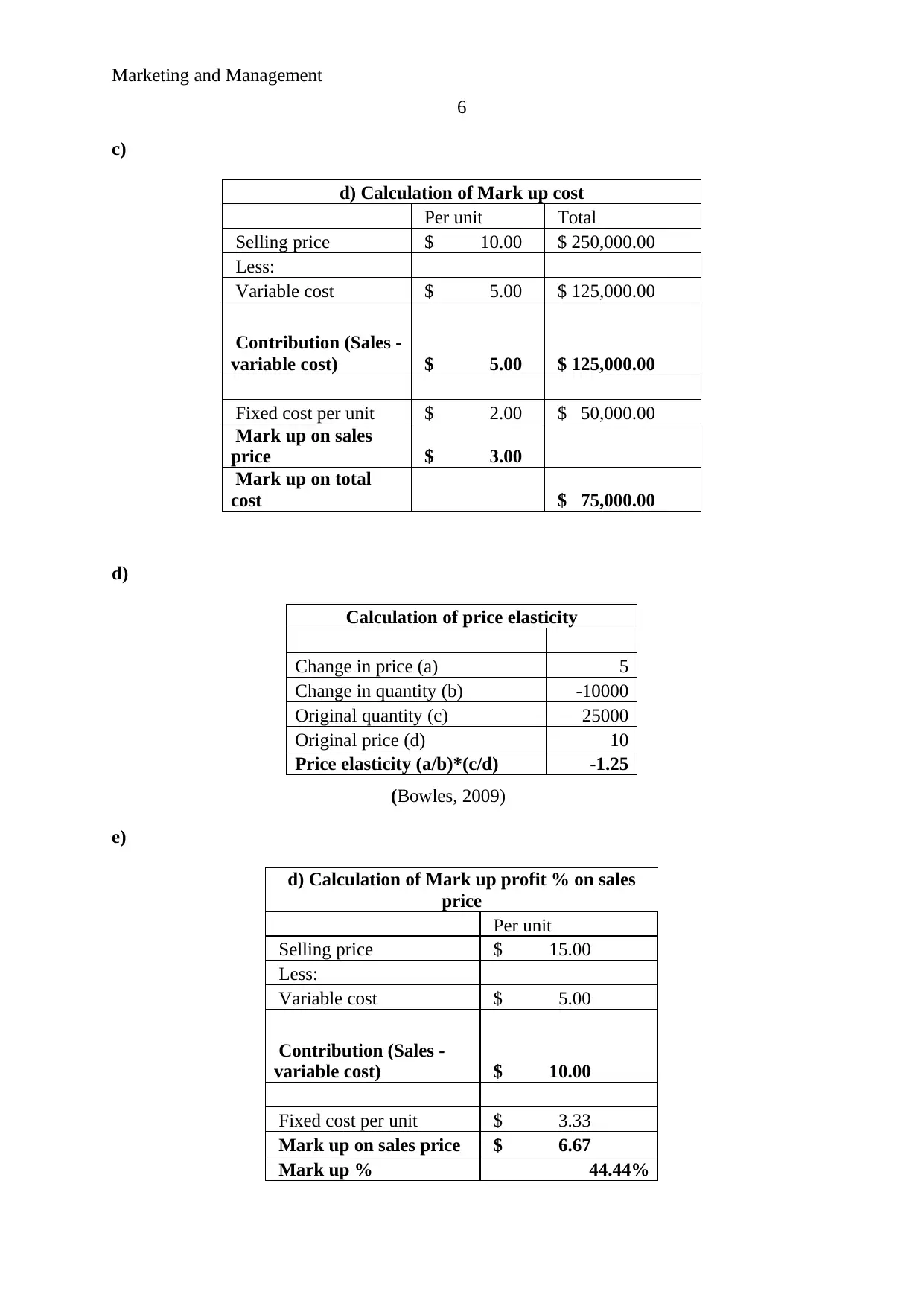

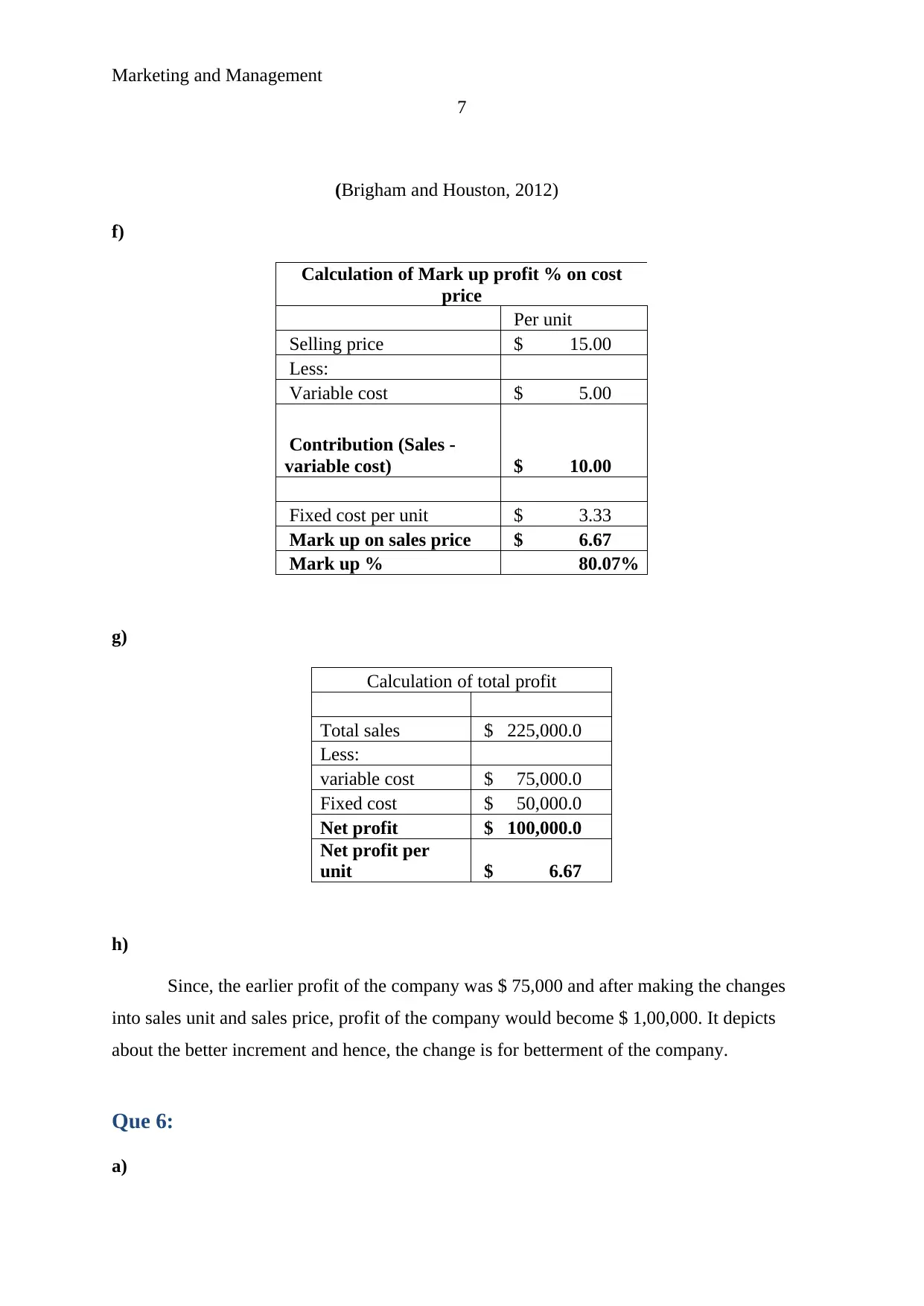

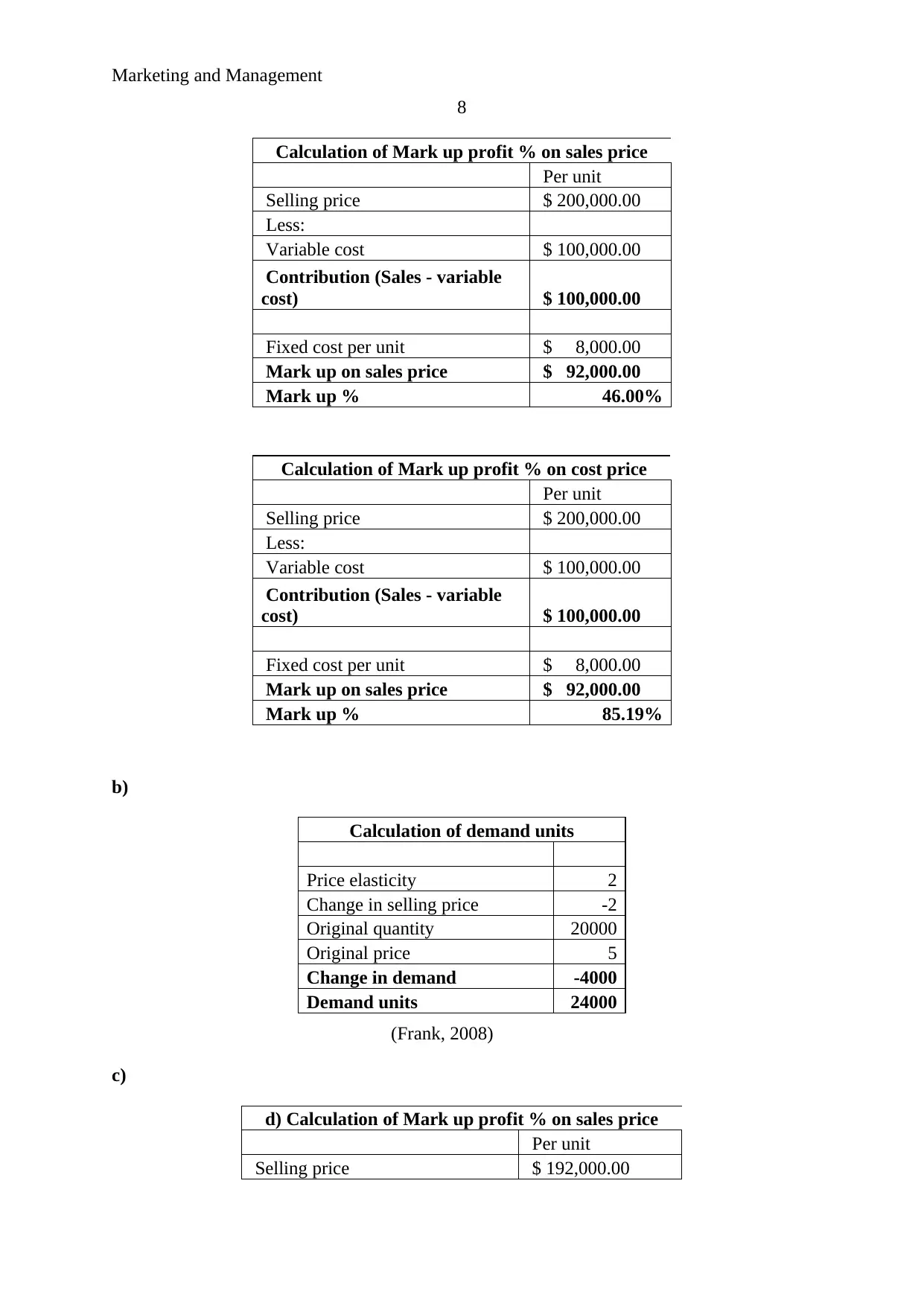

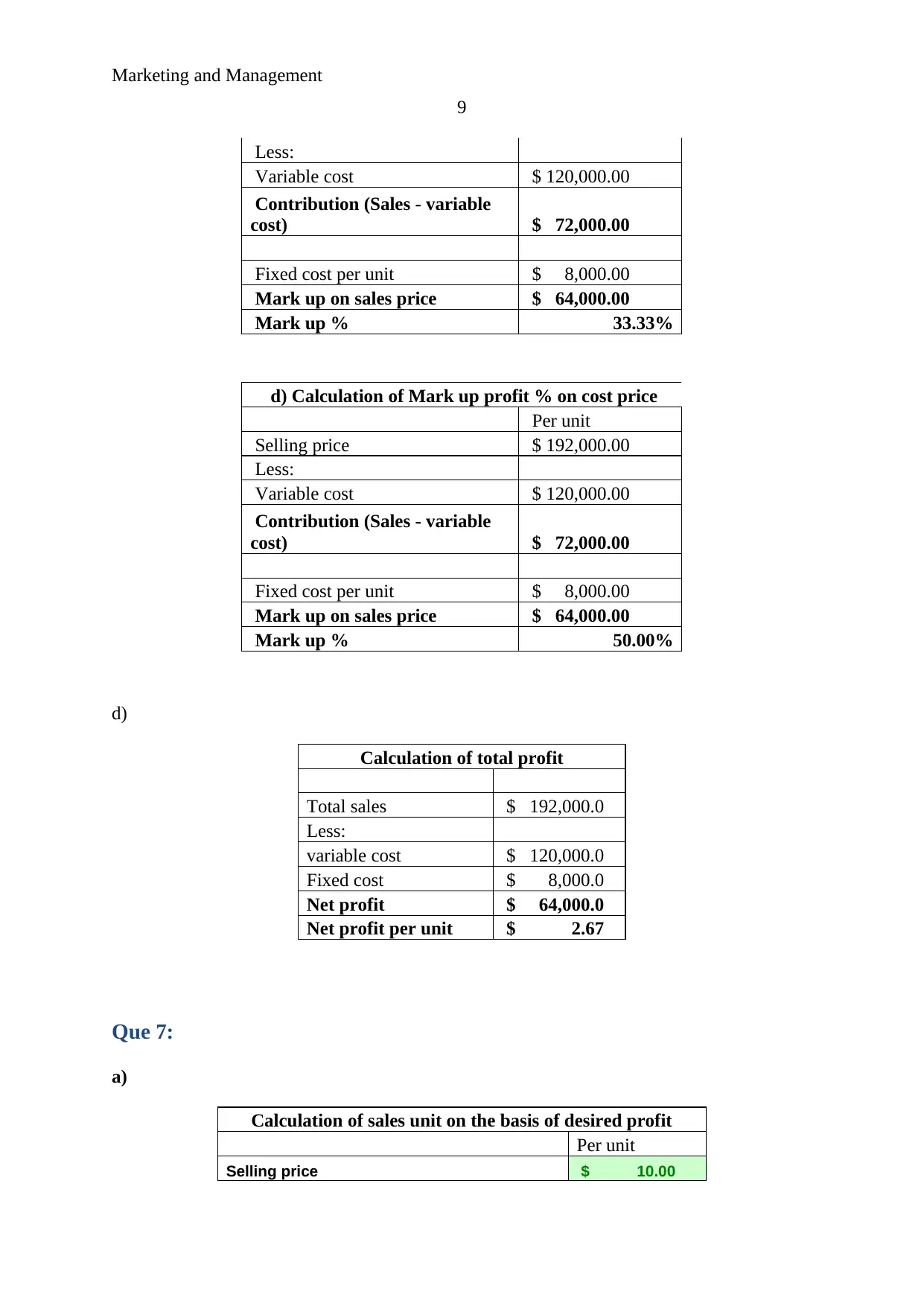

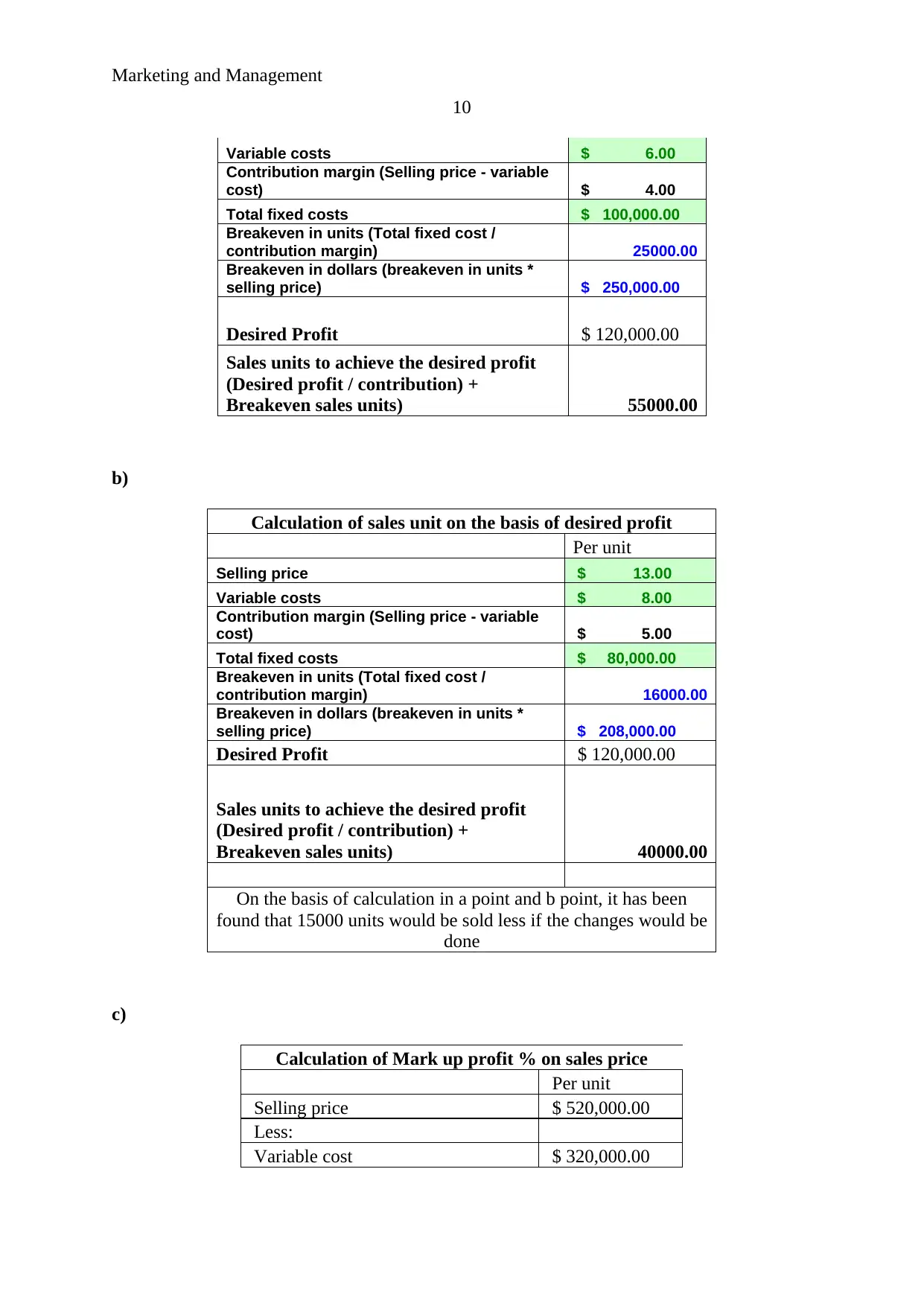

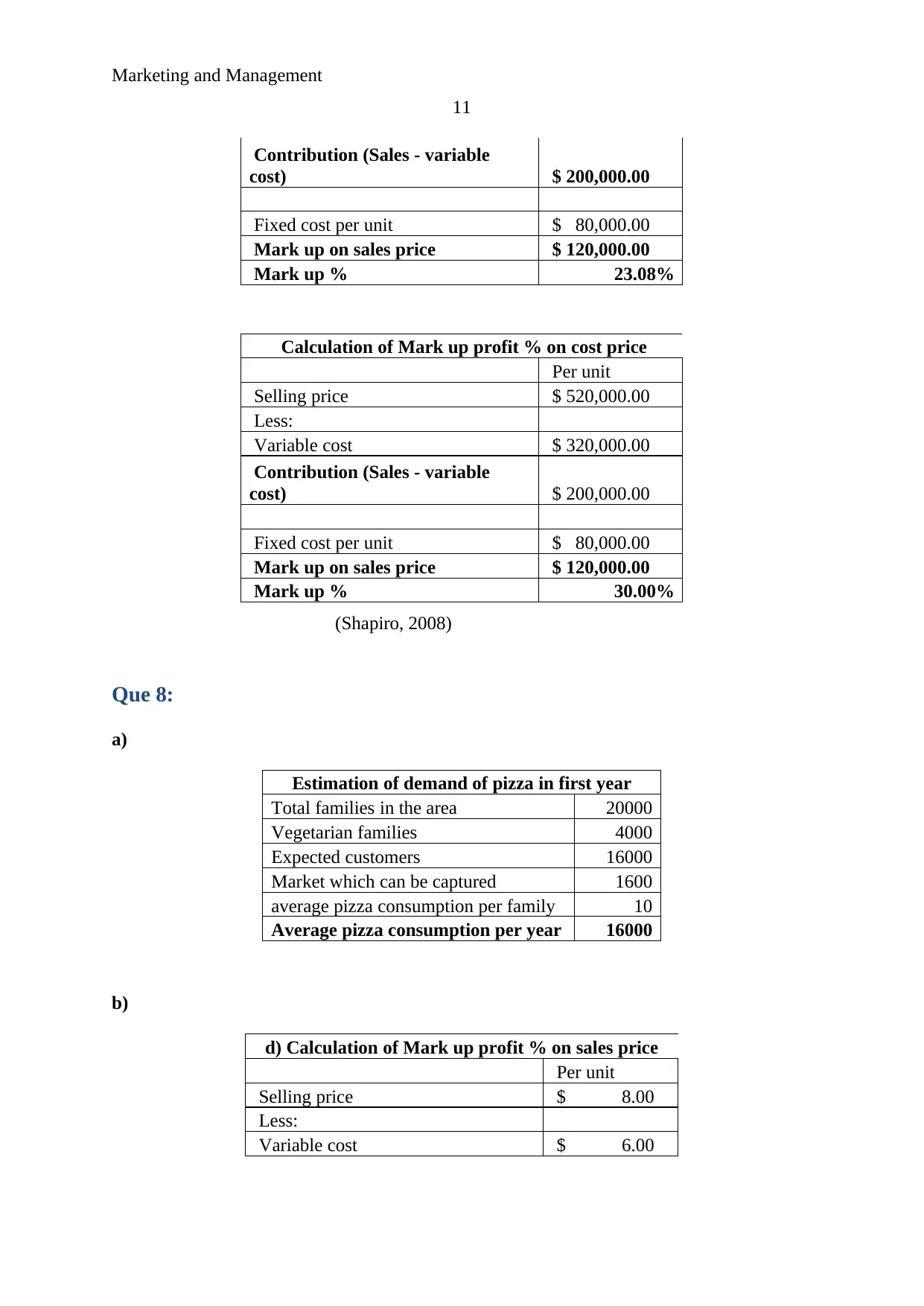

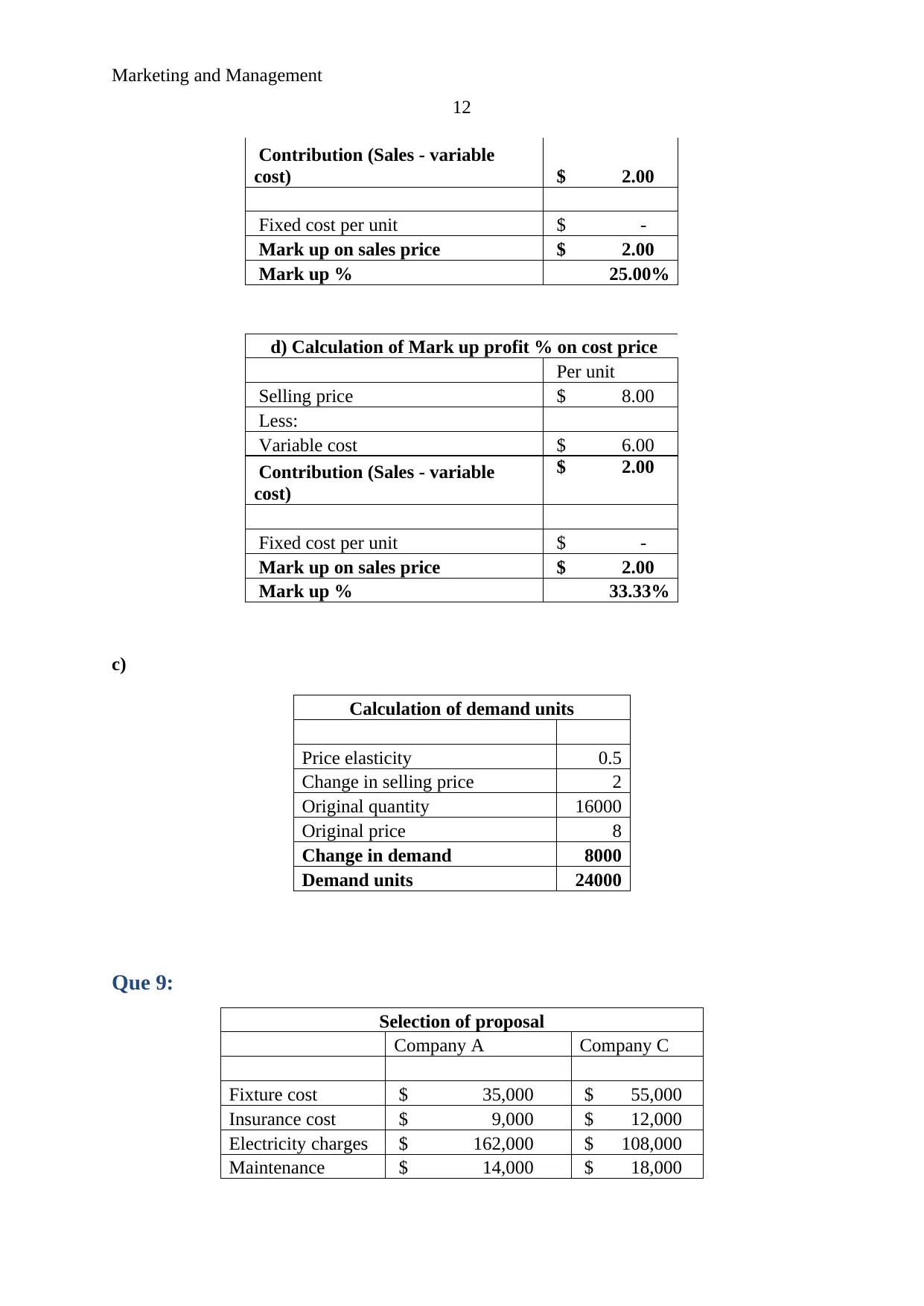

This assignment report provides detailed solutions to a marketing math problem set. The problems cover a range of topics including retail price calculations, margin analysis, and cost-volume-profit relationships. The first question involves calculating retail price and retailer margins given unit costs and desired margins. The second question delves into calculating contribution margin, breakeven points (in units and dollars), and the sales volume needed to achieve a specific profit target for a DVD manufacturer. Further questions explore market potential, sales volume, and market share calculations. The assignment also addresses markups, price elasticity, and profit analysis. The final sections include calculations of markups on sales and cost prices and an assessment of the impact of sales changes on profit. The report provides detailed calculations and analyses to demonstrate an understanding of marketing and management principles.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.