MarketLine Industry Profile: Consumer Electronics in Europe - Analysis

VerifiedAdded on 2021/09/08

|39

|13122

|171

Report

AI Summary

This MarketLine industry profile provides a comprehensive analysis of the consumer electronics market in Europe. It details the market value, which reached $275.1 billion in 2018 and is forecasted to reach $318.0 billion by 2023, with a CAGR of 2.9% between 2018 and 2023. The report segments the market by category and geography, highlighting household appliances as the largest segment and Germany as the largest geographic market. It examines market rivalry and the competitive landscape, including the influence of online retailers like Amazon. The analysis includes market data, a five forces analysis, and profiles of key companies such as Amazon.com, MediaMarktSaturn Retail Group, and Dixons Carphone plc. Macroeconomic indicators and the impact of Brexit on the UK and Ireland are also discussed. The report provides valuable insights into market trends, drivers, and challenges within the European consumer electronics sector.

© MARKETLINE THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 1

MarketLine Industry Profile

Consumer Electronics in Europe

March 2020

Reference Code: 0201-2033

Publication Date: March 2020

WWW.MARKETLINE.COM

MARKETLINE. THIS PROFILE IS A LICENSED PRODUCT

AND IS NOT TO BE PHOTOCOPIED

MarketLine Industry Profile

Consumer Electronics in Europe

March 2020

Reference Code: 0201-2033

Publication Date: March 2020

WWW.MARKETLINE.COM

MARKETLINE. THIS PROFILE IS A LICENSED PRODUCT

AND IS NOT TO BE PHOTOCOPIED

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Consumer Electronics in Europe

Industry Profiles

© MARKETLINE THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 2

1. Executive Summary

1.1. Market value

The European consumer electronics market grew by 2.8% in 2018 to reach a value of $275,134.6 million.

1.2. Market value forecast

In 2023, the European consumer electronics market is forecast to have a value of $318,010.4 million, an increase of

15.6% since 2018.

1.3. Category segmentation

Household appliances is the largest segment of the consumer electronics market in Europe, accounting for 29.3% of

the market's total value.

1.4. Geography segmentation

Germany accounts for 21.2% of the European consumer electronics market value.

1.5. Market rivalry

The consumer electronics retail market has several large chain players coexisting with small independents. It is

relatively easy for a company to step up its sales volume in response to market conditions, easing rivalry.

1.6. Competitive Landscape

Europe is home to the world's largest and longest-established specialist retail conglomerates in the consumer

electronics sphere, but has felt the impact of Amazon's rise acutely. Two of its traditional heavyweights have however

formed a European Retail Alliance, and attitudes towards big ecommerce in the region are tending towards

protectionism.

Industry Profiles

© MARKETLINE THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 2

1. Executive Summary

1.1. Market value

The European consumer electronics market grew by 2.8% in 2018 to reach a value of $275,134.6 million.

1.2. Market value forecast

In 2023, the European consumer electronics market is forecast to have a value of $318,010.4 million, an increase of

15.6% since 2018.

1.3. Category segmentation

Household appliances is the largest segment of the consumer electronics market in Europe, accounting for 29.3% of

the market's total value.

1.4. Geography segmentation

Germany accounts for 21.2% of the European consumer electronics market value.

1.5. Market rivalry

The consumer electronics retail market has several large chain players coexisting with small independents. It is

relatively easy for a company to step up its sales volume in response to market conditions, easing rivalry.

1.6. Competitive Landscape

Europe is home to the world's largest and longest-established specialist retail conglomerates in the consumer

electronics sphere, but has felt the impact of Amazon's rise acutely. Two of its traditional heavyweights have however

formed a European Retail Alliance, and attitudes towards big ecommerce in the region are tending towards

protectionism.

Consumer Electronics in Europe

Industry Profiles

© MARKETLINE THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 3

TABLE OF CONTENTS

1. Executive Summary 2

1.1. Market value.................................................................................................................................2

1.2. Market value forecast ...................................................................................................................2

1.3. Category segmentation ................................................................................................................2

1.4. Geography segmentation .............................................................................................................2

1.5. Market rivalry................................................................................................................................2

1.6. Competitive Landscape................................................................................................................2

2. Market Overview 7

2.1. Market definition ...........................................................................................................................7

2.2. Market analysis ............................................................................................................................7

3. Market Data 9

3.1. Market value.................................................................................................................................9

4. Market Segmentation 10

4.1. Category segmentation ..............................................................................................................10

4.2. Geography segmentation ...........................................................................................................11

4.3. Market distribution ......................................................................................................................12

5. Market Outlook 13

5.1. Market value forecast .................................................................................................................13

6. Five Forces Analysis 14

6.1. Summary .................................................................................................................................... 14

6.2. Buyer power ...............................................................................................................................16

6.3. Supplier power ...........................................................................................................................17

6.4. New entrants ..............................................................................................................................19

6.5. Threat of substitutes...................................................................................................................21

6.6. Degree of rivalry .........................................................................................................................22

7. Competitive Landscape 23

Industry Profiles

© MARKETLINE THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 3

TABLE OF CONTENTS

1. Executive Summary 2

1.1. Market value.................................................................................................................................2

1.2. Market value forecast ...................................................................................................................2

1.3. Category segmentation ................................................................................................................2

1.4. Geography segmentation .............................................................................................................2

1.5. Market rivalry................................................................................................................................2

1.6. Competitive Landscape................................................................................................................2

2. Market Overview 7

2.1. Market definition ...........................................................................................................................7

2.2. Market analysis ............................................................................................................................7

3. Market Data 9

3.1. Market value.................................................................................................................................9

4. Market Segmentation 10

4.1. Category segmentation ..............................................................................................................10

4.2. Geography segmentation ...........................................................................................................11

4.3. Market distribution ......................................................................................................................12

5. Market Outlook 13

5.1. Market value forecast .................................................................................................................13

6. Five Forces Analysis 14

6.1. Summary .................................................................................................................................... 14

6.2. Buyer power ...............................................................................................................................16

6.3. Supplier power ...........................................................................................................................17

6.4. New entrants ..............................................................................................................................19

6.5. Threat of substitutes...................................................................................................................21

6.6. Degree of rivalry .........................................................................................................................22

7. Competitive Landscape 23

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Consumer Electronics in Europe

Industry Profiles

© MARKETLINE THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 4

7.1. Who are the leading players?.....................................................................................................23

7.2. How are multichannel players dealing with competition from online pureplay? .........................23

7.3. What might prevent Amazon from making further entries into European markets?...................24

8. Company Profiles 25

8.1. Amazon.com, Inc........................................................................................................................25

8.2. MediaMarktSaturn Retail Group.................................................................................................29

8.3. Dixons Carphone plc ..................................................................................................................32

9. Macroeconomic Indicators 35

9.1. Country data...............................................................................................................................35

Appendix 37

Methodology ............................................................................................................................................ 37

9.2. Industry associations..................................................................................................................38

9.3. Related MarketLine research .....................................................................................................38

About MarketLine ....................................................................................................................................39

Industry Profiles

© MARKETLINE THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 4

7.1. Who are the leading players?.....................................................................................................23

7.2. How are multichannel players dealing with competition from online pureplay? .........................23

7.3. What might prevent Amazon from making further entries into European markets?...................24

8. Company Profiles 25

8.1. Amazon.com, Inc........................................................................................................................25

8.2. MediaMarktSaturn Retail Group.................................................................................................29

8.3. Dixons Carphone plc ..................................................................................................................32

9. Macroeconomic Indicators 35

9.1. Country data...............................................................................................................................35

Appendix 37

Methodology ............................................................................................................................................ 37

9.2. Industry associations..................................................................................................................38

9.3. Related MarketLine research .....................................................................................................38

About MarketLine ....................................................................................................................................39

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Consumer Electronics in Europe

Industry Profiles

© MARKETLINE THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 5

LIST OF TABLES

Table 1: Europe consumer electronics market value: $ million, 2014–18 9

Table 2: Europe consumer electronics market category segmentation: $ million, 2018 10

Table 3: Europe consumer electronics market geography segmentation: $ million, 2018 11

Table 4: Europe consumer electronics market distribution: % share, by value, 2018 12

Table 5: Europe consumer electronics market value forecast: $ million, 2018–23 13

Table 6: Amazon.com, Inc.: key facts 25

Table 7: Amazon.com, Inc.: Annual Financial Ratios 27

Table 8: Amazon.com, Inc.: Key Employees 28

Table 9: MediaMarktSaturn Retail Group: key facts 29

Table 10: MediaMarktSaturn Retail Group: Key Employees 31

Table 11: Dixons Carphone plc: key facts 32

Table 12: Dixons Carphone plc: Annual Financial Ratios 33

Table 13: Dixons Carphone plc: Key Employees 34

Table 14: Europe size of population (million), 2014–18 35

Table 15: Europe gdp (constant 2005 prices, $ billion), 2014–18 35

Table 16: Europe gdp (current prices, $ billion), 2014–18 35

Table 17: Europe inflation, 2014–18 35

Table 18: Europe consumer price index (absolute), 2014–18 36

Table 19: Europe exchange rate, 2014–18 36

Industry Profiles

© MARKETLINE THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 5

LIST OF TABLES

Table 1: Europe consumer electronics market value: $ million, 2014–18 9

Table 2: Europe consumer electronics market category segmentation: $ million, 2018 10

Table 3: Europe consumer electronics market geography segmentation: $ million, 2018 11

Table 4: Europe consumer electronics market distribution: % share, by value, 2018 12

Table 5: Europe consumer electronics market value forecast: $ million, 2018–23 13

Table 6: Amazon.com, Inc.: key facts 25

Table 7: Amazon.com, Inc.: Annual Financial Ratios 27

Table 8: Amazon.com, Inc.: Key Employees 28

Table 9: MediaMarktSaturn Retail Group: key facts 29

Table 10: MediaMarktSaturn Retail Group: Key Employees 31

Table 11: Dixons Carphone plc: key facts 32

Table 12: Dixons Carphone plc: Annual Financial Ratios 33

Table 13: Dixons Carphone plc: Key Employees 34

Table 14: Europe size of population (million), 2014–18 35

Table 15: Europe gdp (constant 2005 prices, $ billion), 2014–18 35

Table 16: Europe gdp (current prices, $ billion), 2014–18 35

Table 17: Europe inflation, 2014–18 35

Table 18: Europe consumer price index (absolute), 2014–18 36

Table 19: Europe exchange rate, 2014–18 36

Consumer Electronics in Europe

Industry Profiles

© MARKETLINE THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 6

LIST OF FIGURES

Figure 1: Europe consumer electronics market value: $ million, 2014–18 9

Figure 2: Europe consumer electronics market category segmentation: % share, by value, 2018 10

Figure 3: Europe consumer electronics market geography segmentation: % share, by value, 2018 11

Figure 4: Europe consumer electronics market distribution: % share, by value, 2018 12

Figure 5: Europe consumer electronics market value forecast: $ million, 2018–23 13

Figure 6: Forces driving competition in the consumer electronics market in Europe, 2018 14

Figure 7: Drivers of buyer power in the consumer electronics market in Europe, 2018 16

Figure 8: Drivers of supplier power in the consumer electronics market in Europe, 2018 17

Figure 9: Factors influencing the likelihood of new entrants in the consumer electronics market in Europe,

2018 19

Figure 10: Factors influencing the threat of substitutes in the consumer electronics market in Europe, 201821

Figure 11: Drivers of degree of rivalry in the consumer electronics market in Europe, 2018 22

Industry Profiles

© MARKETLINE THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 6

LIST OF FIGURES

Figure 1: Europe consumer electronics market value: $ million, 2014–18 9

Figure 2: Europe consumer electronics market category segmentation: % share, by value, 2018 10

Figure 3: Europe consumer electronics market geography segmentation: % share, by value, 2018 11

Figure 4: Europe consumer electronics market distribution: % share, by value, 2018 12

Figure 5: Europe consumer electronics market value forecast: $ million, 2018–23 13

Figure 6: Forces driving competition in the consumer electronics market in Europe, 2018 14

Figure 7: Drivers of buyer power in the consumer electronics market in Europe, 2018 16

Figure 8: Drivers of supplier power in the consumer electronics market in Europe, 2018 17

Figure 9: Factors influencing the likelihood of new entrants in the consumer electronics market in Europe,

2018 19

Figure 10: Factors influencing the threat of substitutes in the consumer electronics market in Europe, 201821

Figure 11: Drivers of degree of rivalry in the consumer electronics market in Europe, 2018 22

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Consumer Electronics in Europe

Industry Profiles

© MARKETLINE THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 7

2. Market Overview

2.1. Market definition

The Electrical and Electronics Retail market is comprised of the sales of communications equipment, computer

hardware and software, consumer electronics, household appliances, and photographic equipment. Communications

equipment includes retail sales only of answer machines, fax machines, fixed-line telephones, mobile phone

accessories and mobile phones. Computer hardware and software includes retail sales only of desktops and laptop

computers, software, memory sticks, CD packs, hard disks and other data storage devices, computer peripherals,

PDAs, organizers, calculators, and satellite navigation systems. Consumer electronics includes retail sales of CD

players, DVD players and recorders, hi-fi systems, home theatres, in-car entertainment systems, portable digital

radios, radios, televisions and video recorders, home use and portable games consoles. Household appliances includes

major domestic appliances (air conditioners, dishwashers, dryers, freezers, hobs and extractors, microwave ovens,

refrigerators, stoves, vacuum cleaners and washing machines) plus minor domestic appliances (blenders, coffee

machines, deep fryers, food processors, grills, hair products, hair trimmers, curling tongs, razors, hand-held mixers,

irons, juicers, kettles, stand mixers, toasters, sun lamps and fans). Photographic equipment includes camcorders,

cameras, projectors, camera and camcorder accessories, binoculars and telescopes. The market is valued at retail

selling price (RSP) with any currency conversions calculated using constant 2018 annual average exchange rates.

For the purposes of this report, the global market consists of North America, South America, Europe, Asia-Pacific,

Middle East, South Africa and Nigeria.

North America consists of Canada, Mexico, and the United States.

South America comprises Argentina, Brazil, Chile, Colombia, and Peru.

Europe comprises Austria, Belgium, the Czech Republic, Denmark, Finland, France, Germany, Greece, Ireland, Italy,

Netherlands, Norway, Poland, Portugal, Russia, Spain, Sweden, Switzerland, Turkey, and the United Kingdom.

Scandinavia comprises Denmark, Finland, Norway, and Sweden.

Asia-Pacific comprises Australia, China, Hong Kong, India, Indonesia, Kazakhstan, Japan, Malaysia, New Zealand,

Pakistan, Philippines, Singapore, South Korea, Taiwan, Thailand, and Vietnam.

Middle East comprises Egypt, Israel, Saudi Arabia, and United Arab Emirates.

2.2. Market analysis

The European consumer electronics market remained on a fairly slow but steady trajectory of growth in 2018, which is

expected to continue through the forecast period.

Three key trends have been characteristic of Europe’s biggest markets, Germany, France and the UK. Firstly, online

pureplay has grown faster than any other distribution channel; smartphones in particular have been the major sales-

drivers for both online and brick-and-mortar stores; and finally, the latter type of store has struggled especially in

these countries to compete with the online pureplay giant Amazon.

The market had total revenues of $275.1bn in 2018, representing a compound annual growth rate (CAGR) of 2.5%

between 2014 and 2018. In comparison, the German and UK markets grew with CAGRs of 2.6% and 0.7% respectively,

over the same period, to reach respective values of $58.2bn and $27.4bn in 2018.

Varying macroeconomic conditions have been at play across European markets. For example, levels of unemployment

in France continued to experience a progressive downward trend, which combined with an improving average wage

has seen consumer confidence increase. This has sustained the steady, albeit very slow growth of France’s consumer

electronics market. Gains for online pureplay retailers have, however, had an overall constraining effect on this

growth, as physical retailers struggle to compete.

Industry Profiles

© MARKETLINE THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 7

2. Market Overview

2.1. Market definition

The Electrical and Electronics Retail market is comprised of the sales of communications equipment, computer

hardware and software, consumer electronics, household appliances, and photographic equipment. Communications

equipment includes retail sales only of answer machines, fax machines, fixed-line telephones, mobile phone

accessories and mobile phones. Computer hardware and software includes retail sales only of desktops and laptop

computers, software, memory sticks, CD packs, hard disks and other data storage devices, computer peripherals,

PDAs, organizers, calculators, and satellite navigation systems. Consumer electronics includes retail sales of CD

players, DVD players and recorders, hi-fi systems, home theatres, in-car entertainment systems, portable digital

radios, radios, televisions and video recorders, home use and portable games consoles. Household appliances includes

major domestic appliances (air conditioners, dishwashers, dryers, freezers, hobs and extractors, microwave ovens,

refrigerators, stoves, vacuum cleaners and washing machines) plus minor domestic appliances (blenders, coffee

machines, deep fryers, food processors, grills, hair products, hair trimmers, curling tongs, razors, hand-held mixers,

irons, juicers, kettles, stand mixers, toasters, sun lamps and fans). Photographic equipment includes camcorders,

cameras, projectors, camera and camcorder accessories, binoculars and telescopes. The market is valued at retail

selling price (RSP) with any currency conversions calculated using constant 2018 annual average exchange rates.

For the purposes of this report, the global market consists of North America, South America, Europe, Asia-Pacific,

Middle East, South Africa and Nigeria.

North America consists of Canada, Mexico, and the United States.

South America comprises Argentina, Brazil, Chile, Colombia, and Peru.

Europe comprises Austria, Belgium, the Czech Republic, Denmark, Finland, France, Germany, Greece, Ireland, Italy,

Netherlands, Norway, Poland, Portugal, Russia, Spain, Sweden, Switzerland, Turkey, and the United Kingdom.

Scandinavia comprises Denmark, Finland, Norway, and Sweden.

Asia-Pacific comprises Australia, China, Hong Kong, India, Indonesia, Kazakhstan, Japan, Malaysia, New Zealand,

Pakistan, Philippines, Singapore, South Korea, Taiwan, Thailand, and Vietnam.

Middle East comprises Egypt, Israel, Saudi Arabia, and United Arab Emirates.

2.2. Market analysis

The European consumer electronics market remained on a fairly slow but steady trajectory of growth in 2018, which is

expected to continue through the forecast period.

Three key trends have been characteristic of Europe’s biggest markets, Germany, France and the UK. Firstly, online

pureplay has grown faster than any other distribution channel; smartphones in particular have been the major sales-

drivers for both online and brick-and-mortar stores; and finally, the latter type of store has struggled especially in

these countries to compete with the online pureplay giant Amazon.

The market had total revenues of $275.1bn in 2018, representing a compound annual growth rate (CAGR) of 2.5%

between 2014 and 2018. In comparison, the German and UK markets grew with CAGRs of 2.6% and 0.7% respectively,

over the same period, to reach respective values of $58.2bn and $27.4bn in 2018.

Varying macroeconomic conditions have been at play across European markets. For example, levels of unemployment

in France continued to experience a progressive downward trend, which combined with an improving average wage

has seen consumer confidence increase. This has sustained the steady, albeit very slow growth of France’s consumer

electronics market. Gains for online pureplay retailers have, however, had an overall constraining effect on this

growth, as physical retailers struggle to compete.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Consumer Electronics in Europe

Industry Profiles

© MARKETLINE THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 8

The UK is Europe’s third-biggest retail market, but its rate of growth is well below both the European and the world

average. The stagnant performance of high street retailers, with multiple high-profile closures over the last several

years, is particularly to blame, and can in turn be attributed to the rise of ecommerce.

Portugal’s growth is slightly above the European average, and the rapid growth of online pureplay at the expense of

declining specialist stores would appear to put it on a similar trajectory to more mature markets such as the UK.

However, whilst Portuguese consumers have been shopping through the Spanish Amazon site since 2011, specialists

with physical and online stores retain a larger and still-growing market share. The resulting diversity of players is

enabling particularly healthy overall growth.

The household appliances segment was the market's most lucrative in 2018, with total revenues of $80.5bn,

equivalent to 29.3% of the market's overall value. The communications equipment segment contributed revenues of

$72.1bn in 2018, equating to 26.2% of the market's aggregate value.

The maturity of this market in Scandinavia has been partly to blame for that area’s slow development in 2018, even in

the online pureplay channel. In Sweden, high levels of internet penetration and the eight-highest per capita income in

the world made for an early uptake of ecommerce options, at the point when players in that sphere had not had time

for consolidation. The early success of this channel created a diverse playing field that has dampened rivalry whilst

bringing revenue growth to maturity quickly. The presence of five Swedish-based ecommerce sites in 2018’s top six by

revenue is illustrative of these conditions.

The performance of the market is forecast to accelerate, with an anticipated CAGR of 2.9% for the five-year period

2018 - 2023, which is expected to drive the market to a value of $318.0bn by the end of 2023. Comparatively, the

German and UK markets will grow with CAGRs of 2.6% and 1.2% respectively, over the same period, to reach

respective values of $66.3bn and $29.0bn in 2023.

Europe is waiting with apprehension for the UK’s departure from the EU, which will have an impact on the UK’s

trading partners. Most pronounced will be the effect on electronics retail in Ireland. Whilst changes in the sterling-

euro exchange rate have been progressively more favorable to Irish consumers shopping through UK ecommerce

sites, there is uncertainty over the economic outcome of a no-deal Brexit and the financial impact on consumers. The

volume of trade between Ireland and the UK and fears of political instability stemming from the notorious ‘backstop’

issue around the Irish-UK border are the leading factors here. Higher tariffs and regulatory checks on goods moving

across the border will impact retailers and consumers alike.

Industry Profiles

© MARKETLINE THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 8

The UK is Europe’s third-biggest retail market, but its rate of growth is well below both the European and the world

average. The stagnant performance of high street retailers, with multiple high-profile closures over the last several

years, is particularly to blame, and can in turn be attributed to the rise of ecommerce.

Portugal’s growth is slightly above the European average, and the rapid growth of online pureplay at the expense of

declining specialist stores would appear to put it on a similar trajectory to more mature markets such as the UK.

However, whilst Portuguese consumers have been shopping through the Spanish Amazon site since 2011, specialists

with physical and online stores retain a larger and still-growing market share. The resulting diversity of players is

enabling particularly healthy overall growth.

The household appliances segment was the market's most lucrative in 2018, with total revenues of $80.5bn,

equivalent to 29.3% of the market's overall value. The communications equipment segment contributed revenues of

$72.1bn in 2018, equating to 26.2% of the market's aggregate value.

The maturity of this market in Scandinavia has been partly to blame for that area’s slow development in 2018, even in

the online pureplay channel. In Sweden, high levels of internet penetration and the eight-highest per capita income in

the world made for an early uptake of ecommerce options, at the point when players in that sphere had not had time

for consolidation. The early success of this channel created a diverse playing field that has dampened rivalry whilst

bringing revenue growth to maturity quickly. The presence of five Swedish-based ecommerce sites in 2018’s top six by

revenue is illustrative of these conditions.

The performance of the market is forecast to accelerate, with an anticipated CAGR of 2.9% for the five-year period

2018 - 2023, which is expected to drive the market to a value of $318.0bn by the end of 2023. Comparatively, the

German and UK markets will grow with CAGRs of 2.6% and 1.2% respectively, over the same period, to reach

respective values of $66.3bn and $29.0bn in 2023.

Europe is waiting with apprehension for the UK’s departure from the EU, which will have an impact on the UK’s

trading partners. Most pronounced will be the effect on electronics retail in Ireland. Whilst changes in the sterling-

euro exchange rate have been progressively more favorable to Irish consumers shopping through UK ecommerce

sites, there is uncertainty over the economic outcome of a no-deal Brexit and the financial impact on consumers. The

volume of trade between Ireland and the UK and fears of political instability stemming from the notorious ‘backstop’

issue around the Irish-UK border are the leading factors here. Higher tariffs and regulatory checks on goods moving

across the border will impact retailers and consumers alike.

Consumer Electronics in Europe

Industry Profiles

© MARKETLINE THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 9

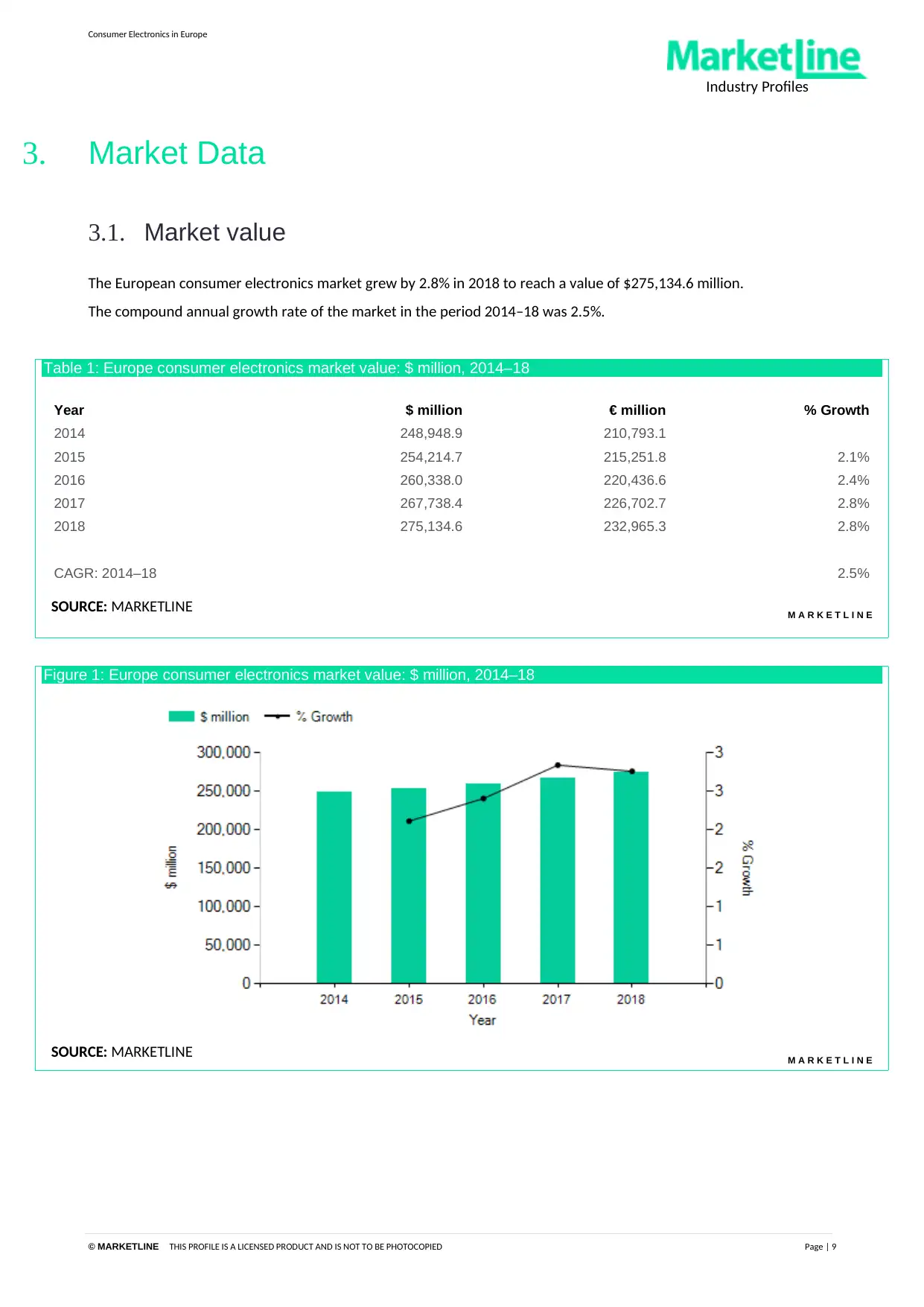

3. Market Data

3.1. Market value

The European consumer electronics market grew by 2.8% in 2018 to reach a value of $275,134.6 million.

The compound annual growth rate of the market in the period 2014–18 was 2.5%.

Table 1: Europe consumer electronics market value: $ million, 2014–18

Year $ million € million % Growth

2014 248,948.9 210,793.1

2015 254,214.7 215,251.8 2.1%

2016 260,338.0 220,436.6 2.4%

2017 267,738.4 226,702.7 2.8%

2018 275,134.6 232,965.3 2.8%

CAGR: 2014–18 2.5%

SOURCE: MARKETLINE M A R K E T L I N E

Figure 1: Europe consumer electronics market value: $ million, 2014–18

SOURCE: MARKETLINE M A R K E T L I N E

Industry Profiles

© MARKETLINE THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 9

3. Market Data

3.1. Market value

The European consumer electronics market grew by 2.8% in 2018 to reach a value of $275,134.6 million.

The compound annual growth rate of the market in the period 2014–18 was 2.5%.

Table 1: Europe consumer electronics market value: $ million, 2014–18

Year $ million € million % Growth

2014 248,948.9 210,793.1

2015 254,214.7 215,251.8 2.1%

2016 260,338.0 220,436.6 2.4%

2017 267,738.4 226,702.7 2.8%

2018 275,134.6 232,965.3 2.8%

CAGR: 2014–18 2.5%

SOURCE: MARKETLINE M A R K E T L I N E

Figure 1: Europe consumer electronics market value: $ million, 2014–18

SOURCE: MARKETLINE M A R K E T L I N E

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Consumer Electronics in Europe

Industry Profiles

© MARKETLINE THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 10

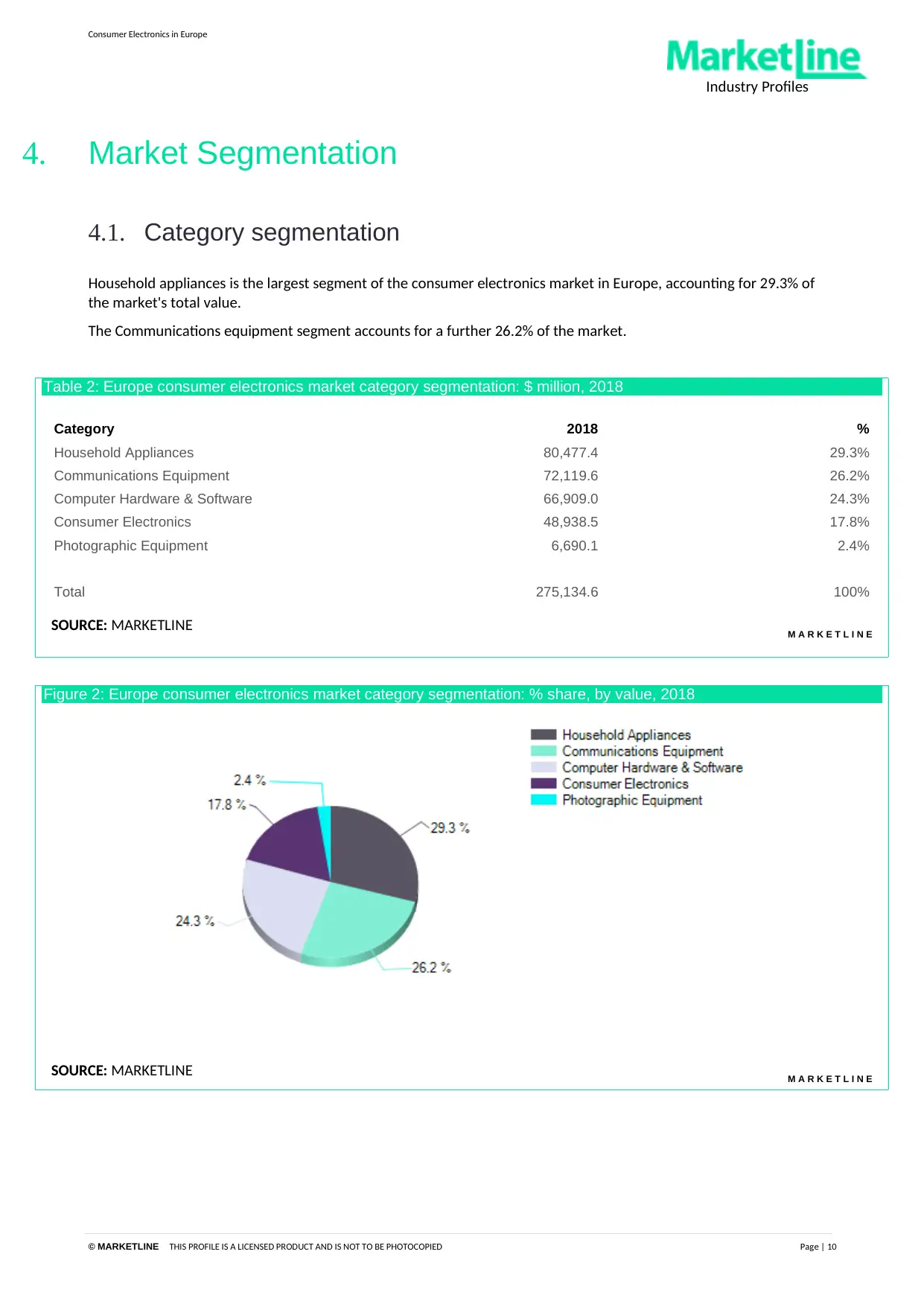

4. Market Segmentation

4.1. Category segmentation

Household appliances is the largest segment of the consumer electronics market in Europe, accounting for 29.3% of

the market's total value.

The Communications equipment segment accounts for a further 26.2% of the market.

Table 2: Europe consumer electronics market category segmentation: $ million, 2018

Category 2018 %

Household Appliances 80,477.4 29.3%

Communications Equipment 72,119.6 26.2%

Computer Hardware & Software 66,909.0 24.3%

Consumer Electronics 48,938.5 17.8%

Photographic Equipment 6,690.1 2.4%

Total 275,134.6 100%

SOURCE: MARKETLINE M A R K E T L I N E

Figure 2: Europe consumer electronics market category segmentation: % share, by value, 2018

SOURCE: MARKETLINE M A R K E T L I N E

Industry Profiles

© MARKETLINE THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 10

4. Market Segmentation

4.1. Category segmentation

Household appliances is the largest segment of the consumer electronics market in Europe, accounting for 29.3% of

the market's total value.

The Communications equipment segment accounts for a further 26.2% of the market.

Table 2: Europe consumer electronics market category segmentation: $ million, 2018

Category 2018 %

Household Appliances 80,477.4 29.3%

Communications Equipment 72,119.6 26.2%

Computer Hardware & Software 66,909.0 24.3%

Consumer Electronics 48,938.5 17.8%

Photographic Equipment 6,690.1 2.4%

Total 275,134.6 100%

SOURCE: MARKETLINE M A R K E T L I N E

Figure 2: Europe consumer electronics market category segmentation: % share, by value, 2018

SOURCE: MARKETLINE M A R K E T L I N E

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Consumer Electronics in Europe

Industry Profiles

© MARKETLINE THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 11

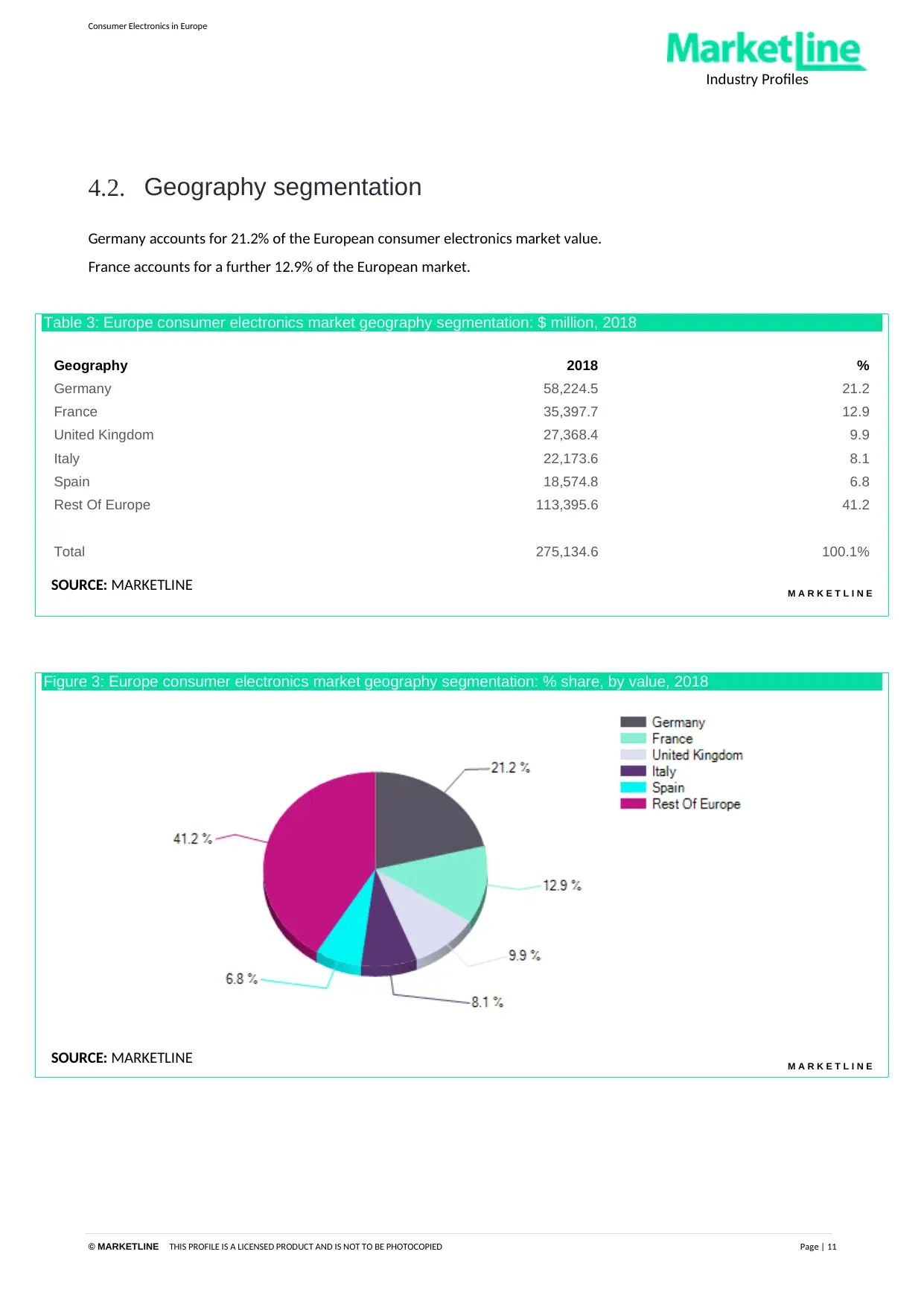

4.2. Geography segmentation

Germany accounts for 21.2% of the European consumer electronics market value.

France accounts for a further 12.9% of the European market.

Table 3: Europe consumer electronics market geography segmentation: $ million, 2018

Geography 2018 %

Germany 58,224.5 21.2

France 35,397.7 12.9

United Kingdom 27,368.4 9.9

Italy 22,173.6 8.1

Spain 18,574.8 6.8

Rest Of Europe 113,395.6 41.2

Total 275,134.6 100.1%

SOURCE: MARKETLINE M A R K E T L I N E

Figure 3: Europe consumer electronics market geography segmentation: % share, by value, 2018

SOURCE: MARKETLINE M A R K E T L I N E

Industry Profiles

© MARKETLINE THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 11

4.2. Geography segmentation

Germany accounts for 21.2% of the European consumer electronics market value.

France accounts for a further 12.9% of the European market.

Table 3: Europe consumer electronics market geography segmentation: $ million, 2018

Geography 2018 %

Germany 58,224.5 21.2

France 35,397.7 12.9

United Kingdom 27,368.4 9.9

Italy 22,173.6 8.1

Spain 18,574.8 6.8

Rest Of Europe 113,395.6 41.2

Total 275,134.6 100.1%

SOURCE: MARKETLINE M A R K E T L I N E

Figure 3: Europe consumer electronics market geography segmentation: % share, by value, 2018

SOURCE: MARKETLINE M A R K E T L I N E

Consumer Electronics in Europe

Industry Profiles

© MARKETLINE THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 12

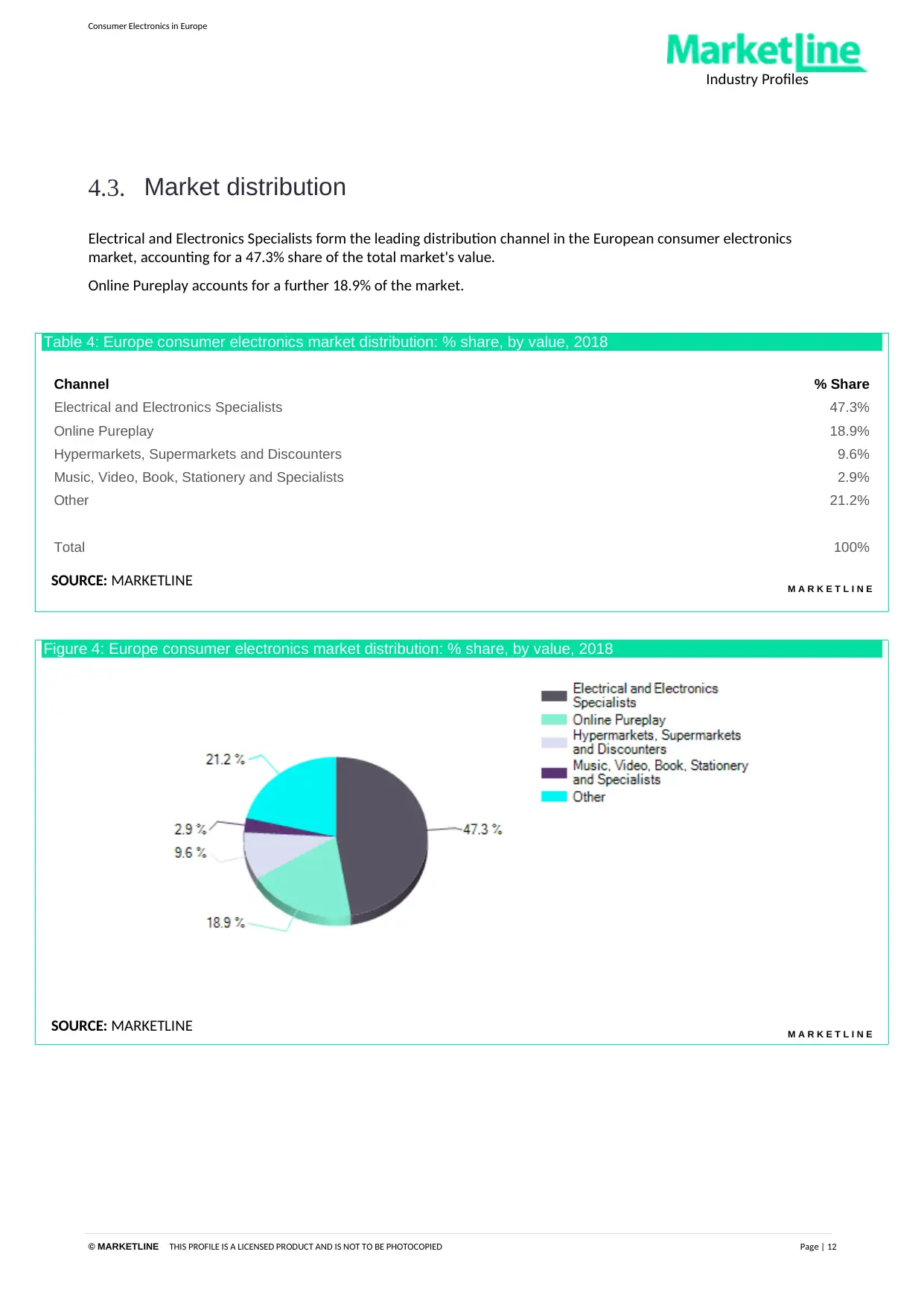

4.3. Market distribution

Electrical and Electronics Specialists form the leading distribution channel in the European consumer electronics

market, accounting for a 47.3% share of the total market's value.

Online Pureplay accounts for a further 18.9% of the market.

Table 4: Europe consumer electronics market distribution: % share, by value, 2018

Channel % Share

Electrical and Electronics Specialists 47.3%

Online Pureplay 18.9%

Hypermarkets, Supermarkets and Discounters 9.6%

Music, Video, Book, Stationery and Specialists 2.9%

Other 21.2%

Total 100%

SOURCE: MARKETLINE M A R K E T L I N E

Figure 4: Europe consumer electronics market distribution: % share, by value, 2018

SOURCE: MARKETLINE M A R K E T L I N E

Industry Profiles

© MARKETLINE THIS PROFILE IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED Page | 12

4.3. Market distribution

Electrical and Electronics Specialists form the leading distribution channel in the European consumer electronics

market, accounting for a 47.3% share of the total market's value.

Online Pureplay accounts for a further 18.9% of the market.

Table 4: Europe consumer electronics market distribution: % share, by value, 2018

Channel % Share

Electrical and Electronics Specialists 47.3%

Online Pureplay 18.9%

Hypermarkets, Supermarkets and Discounters 9.6%

Music, Video, Book, Stationery and Specialists 2.9%

Other 21.2%

Total 100%

SOURCE: MARKETLINE M A R K E T L I N E

Figure 4: Europe consumer electronics market distribution: % share, by value, 2018

SOURCE: MARKETLINE M A R K E T L I N E

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 39

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.