Management Accounting Report: Cost Analysis at Marks and Spencer

VerifiedAdded on 2022/12/07

|15

|4228

|283

Report

AI Summary

This report provides an in-depth analysis of management accounting principles and practices, using Marks and Spencer (M&S) as a case study. It begins with an explanation of management accounting, its essential requirements, and a comparison with financial accounting, highlighting the primary users of management accounting information within M&S. The report then delves into various management accounting systems employed, including cost accounting, inventory management, and job costing systems, along with the process of accounting reporting, covering budget reports, cost managerial accounting reports, performance reports, and account receivable aging reports. Furthermore, the report explores cost analysis techniques, calculating costs using both marginal and absorption costing methods, and includes income statements under both costing approaches. The report also discusses the advantages and disadvantages of different planning tools used for budgetary control. Finally, it compares how organizations, specifically M&S, adapt their management accounting systems to respond to financial problems, offering insights into strategic decision-making in response to financial challenges.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................2

P1 Explanation of management accounting and providing the essential requirements of

different types of management accounting systems...............................................................2

P2 Explanation of various methods which are used for management accounting reporting. 4

TASK 2............................................................................................................................................5

P3 Calculation of costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs......................................................................5

TASK 3............................................................................................................................................9

P4 Explanation of the advantages and disadvantages of various types of planning tools used

for budgetary control..............................................................................................................9

TASK 4..........................................................................................................................................11

P5 Comparison of how organizations are adapting management accounting systems to

respond to financial problems..............................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................2

P1 Explanation of management accounting and providing the essential requirements of

different types of management accounting systems...............................................................2

P2 Explanation of various methods which are used for management accounting reporting. 4

TASK 2............................................................................................................................................5

P3 Calculation of costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs......................................................................5

TASK 3............................................................................................................................................9

P4 Explanation of the advantages and disadvantages of various types of planning tools used

for budgetary control..............................................................................................................9

TASK 4..........................................................................................................................................11

P5 Comparison of how organizations are adapting management accounting systems to

respond to financial problems..............................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

For the purpose of preparing reports of business operations it is necessary for organization to

follow a prescribed accounting system full stop Management Accounting system is one of the

forces from them. It helps the organization in taking short and long term decisions as it provide

various censorious informations to the management regarding the decision making in the

operations of business. It is used find a performance with the help of financial and managerial

data of organization. On the basis of Management Accounting system various organizations

make decisions regarding their running activities. Report is based on Marks and Spencer which

is a UK based multinational company dealing in food products, clothing, home products and

footwear having headquarter in London, England, UK. This report include various concepts of

Management Accounting such as types of Management Accounting system, method use for

accounting reporting, various techniques of cost analysis, advantages and disadvantages of

various types of planning tools and many more.

1

For the purpose of preparing reports of business operations it is necessary for organization to

follow a prescribed accounting system full stop Management Accounting system is one of the

forces from them. It helps the organization in taking short and long term decisions as it provide

various censorious informations to the management regarding the decision making in the

operations of business. It is used find a performance with the help of financial and managerial

data of organization. On the basis of Management Accounting system various organizations

make decisions regarding their running activities. Report is based on Marks and Spencer which

is a UK based multinational company dealing in food products, clothing, home products and

footwear having headquarter in London, England, UK. This report include various concepts of

Management Accounting such as types of Management Accounting system, method use for

accounting reporting, various techniques of cost analysis, advantages and disadvantages of

various types of planning tools and many more.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 1

P1 Explanation of management accounting and providing the essential requirements of different

types of management accounting systems

Management Accounting can be defined as a process of using the various information of

organization including variance analysis budget report inventory report and many more for the

purpose of creating statistical and financial data which is very useful in the process of making

decisions for the purpose of running the operational activities of organization (Bailey, W.J. and

Samuels, J.A., 2018). Some time it becomes a confusing topic about Management Accounting

and financial accounting which are totally different from each other. The difference between

Management Accounting and financial accounting are given below:

Basis Financial Accounting Management Accounting

Users of data Financial data is used by

various external stakeholders

which include creditors,

suppliers and general public.

It focus on the diverse range of

information related to the

organization which is useful for

both internal as well as external

stakeholders. Management

accounting information is acquired

by financial accounting (Baker,

C.R., 2019).

Purpose Financial accounting focuses on

the measurement of profitability

and efficiency of complete

organization.

Management accounting focuses on

the measurement of disadvantages

of organization by developing

budget and variance analysis.

Report display It’s report can be seen by

income statement and balance

sheet.

It’s report can be seen by predicting

future making decisions obtained

from the financial accounting from

cash flow statement, budgetary

statement, financial report and fund

flow statements.

2

P1 Explanation of management accounting and providing the essential requirements of different

types of management accounting systems

Management Accounting can be defined as a process of using the various information of

organization including variance analysis budget report inventory report and many more for the

purpose of creating statistical and financial data which is very useful in the process of making

decisions for the purpose of running the operational activities of organization (Bailey, W.J. and

Samuels, J.A., 2018). Some time it becomes a confusing topic about Management Accounting

and financial accounting which are totally different from each other. The difference between

Management Accounting and financial accounting are given below:

Basis Financial Accounting Management Accounting

Users of data Financial data is used by

various external stakeholders

which include creditors,

suppliers and general public.

It focus on the diverse range of

information related to the

organization which is useful for

both internal as well as external

stakeholders. Management

accounting information is acquired

by financial accounting (Baker,

C.R., 2019).

Purpose Financial accounting focuses on

the measurement of profitability

and efficiency of complete

organization.

Management accounting focuses on

the measurement of disadvantages

of organization by developing

budget and variance analysis.

Report display It’s report can be seen by

income statement and balance

sheet.

It’s report can be seen by predicting

future making decisions obtained

from the financial accounting from

cash flow statement, budgetary

statement, financial report and fund

flow statements.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Primary users of management accounting information: Personnel management, shareholders,

employees and investors of organization are the primary users of management accounting in

Marks and Spencer (Bassani, G. and Cattaneo, C., 2017).

Management Accounting System: It can be defined as a process of analyzing both

financial as well as non financial information which plays an important role while planning and

decision making in an organization.

Principle of management accounting: Following are some principles of management

accounting which are considered by Marks and Spencer organization:

Various information which are related to the evidence, statement, accounting and

reports are collected with the help of information of past and present with the

purpose of predicting future.

It also help the organization in the calculation of return on investment.

For the purpose of running the management of organization, all the required

information can be integrated by management accounting.

Management Accounting System

Cost accounting system: Marks and Spencer uses this system in order to find out the Per unit

cost of product. According to this they set the selling prices of products. In the process of cost

accounting system all the records related to the business operations are recorded which include

direct as well as indirect cost.

Inventory management system: this system is used for the purpose of evaluating the materials in

inventory by using various processes which include FIFO, AVCO and LIFO. It is beneficial for

Marks and Spencer organization as it involve the identification of selling prices, requirements of

products and any loss of products.

Job costing system: through this system data related to the cost of production is identified by the

organization for stop Marks and Spencer use this data for the purpose of identifying the accuracy

of its estimation process, any reimbursement for customers, setting prices of products and many

more (Bösch and et. al., 2019).

Price Optimisation system: this system is used for the purpose of identifying the demand of

customers as well as the most possible prices of product. It is analyzed that marks and Spencer

can increase the prices of their product based on increasing margin profit which is beneficial for

the system.

3

employees and investors of organization are the primary users of management accounting in

Marks and Spencer (Bassani, G. and Cattaneo, C., 2017).

Management Accounting System: It can be defined as a process of analyzing both

financial as well as non financial information which plays an important role while planning and

decision making in an organization.

Principle of management accounting: Following are some principles of management

accounting which are considered by Marks and Spencer organization:

Various information which are related to the evidence, statement, accounting and

reports are collected with the help of information of past and present with the

purpose of predicting future.

It also help the organization in the calculation of return on investment.

For the purpose of running the management of organization, all the required

information can be integrated by management accounting.

Management Accounting System

Cost accounting system: Marks and Spencer uses this system in order to find out the Per unit

cost of product. According to this they set the selling prices of products. In the process of cost

accounting system all the records related to the business operations are recorded which include

direct as well as indirect cost.

Inventory management system: this system is used for the purpose of evaluating the materials in

inventory by using various processes which include FIFO, AVCO and LIFO. It is beneficial for

Marks and Spencer organization as it involve the identification of selling prices, requirements of

products and any loss of products.

Job costing system: through this system data related to the cost of production is identified by the

organization for stop Marks and Spencer use this data for the purpose of identifying the accuracy

of its estimation process, any reimbursement for customers, setting prices of products and many

more (Bösch and et. al., 2019).

Price Optimisation system: this system is used for the purpose of identifying the demand of

customers as well as the most possible prices of product. It is analyzed that marks and Spencer

can increase the prices of their product based on increasing margin profit which is beneficial for

the system.

3

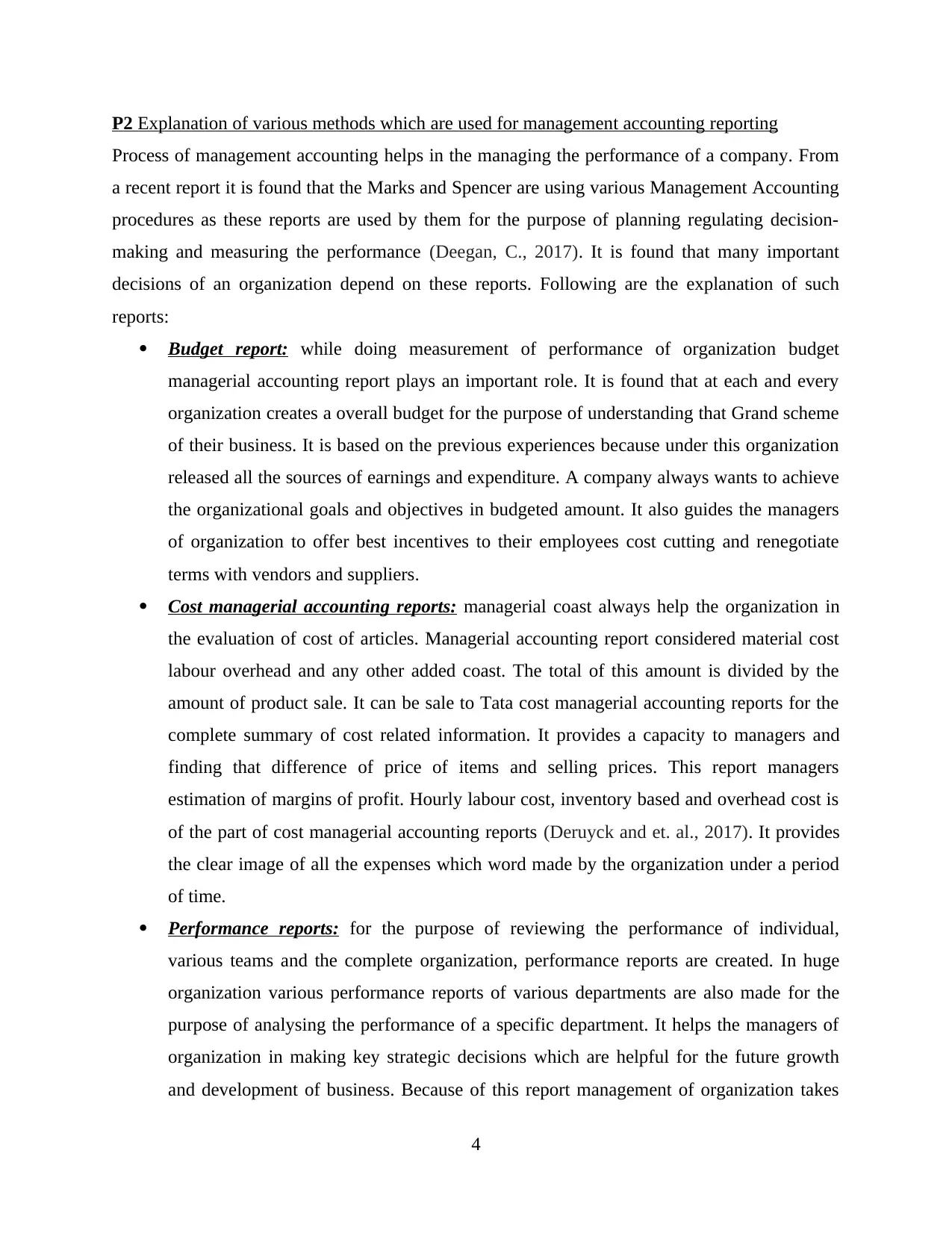

P2 Explanation of various methods which are used for management accounting reporting

Process of management accounting helps in the managing the performance of a company. From

a recent report it is found that the Marks and Spencer are using various Management Accounting

procedures as these reports are used by them for the purpose of planning regulating decision-

making and measuring the performance (Deegan, C., 2017). It is found that many important

decisions of an organization depend on these reports. Following are the explanation of such

reports:

Budget report: while doing measurement of performance of organization budget

managerial accounting report plays an important role. It is found that at each and every

organization creates a overall budget for the purpose of understanding that Grand scheme

of their business. It is based on the previous experiences because under this organization

released all the sources of earnings and expenditure. A company always wants to achieve

the organizational goals and objectives in budgeted amount. It also guides the managers

of organization to offer best incentives to their employees cost cutting and renegotiate

terms with vendors and suppliers.

Cost managerial accounting reports: managerial coast always help the organization in

the evaluation of cost of articles. Managerial accounting report considered material cost

labour overhead and any other added coast. The total of this amount is divided by the

amount of product sale. It can be sale to Tata cost managerial accounting reports for the

complete summary of cost related information. It provides a capacity to managers and

finding that difference of price of items and selling prices. This report managers

estimation of margins of profit. Hourly labour cost, inventory based and overhead cost is

of the part of cost managerial accounting reports (Deruyck and et. al., 2017). It provides

the clear image of all the expenses which word made by the organization under a period

of time.

Performance reports: for the purpose of reviewing the performance of individual,

various teams and the complete organization, performance reports are created. In huge

organization various performance reports of various departments are also made for the

purpose of analysing the performance of a specific department. It helps the managers of

organization in making key strategic decisions which are helpful for the future growth

and development of business. Because of this report management of organization takes

4

Process of management accounting helps in the managing the performance of a company. From

a recent report it is found that the Marks and Spencer are using various Management Accounting

procedures as these reports are used by them for the purpose of planning regulating decision-

making and measuring the performance (Deegan, C., 2017). It is found that many important

decisions of an organization depend on these reports. Following are the explanation of such

reports:

Budget report: while doing measurement of performance of organization budget

managerial accounting report plays an important role. It is found that at each and every

organization creates a overall budget for the purpose of understanding that Grand scheme

of their business. It is based on the previous experiences because under this organization

released all the sources of earnings and expenditure. A company always wants to achieve

the organizational goals and objectives in budgeted amount. It also guides the managers

of organization to offer best incentives to their employees cost cutting and renegotiate

terms with vendors and suppliers.

Cost managerial accounting reports: managerial coast always help the organization in

the evaluation of cost of articles. Managerial accounting report considered material cost

labour overhead and any other added coast. The total of this amount is divided by the

amount of product sale. It can be sale to Tata cost managerial accounting reports for the

complete summary of cost related information. It provides a capacity to managers and

finding that difference of price of items and selling prices. This report managers

estimation of margins of profit. Hourly labour cost, inventory based and overhead cost is

of the part of cost managerial accounting reports (Deruyck and et. al., 2017). It provides

the clear image of all the expenses which word made by the organization under a period

of time.

Performance reports: for the purpose of reviewing the performance of individual,

various teams and the complete organization, performance reports are created. In huge

organization various performance reports of various departments are also made for the

purpose of analysing the performance of a specific department. It helps the managers of

organization in making key strategic decisions which are helpful for the future growth

and development of business. Because of this report management of organization takes

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the decision of rewarding and incentive for employees on the basis of their performance.

Performance report helps the organization in differentiating the employees on the basis of

their performance. According to this, management of organization also arrange training

and development program for low performing employees (Duff and et. al., 2020). The

role of this report is vital for an organization to keep an accurate measure of its strategy

towards is its mission.

Account receivable aging report: if any business organization is depend on the extending

credit then account receivable aging report plays an important role in their operations as it

helps the organization in recognising the defaulters by breaking down the clients

remaining balances into a specific period of time. It also finds various issues in process of

collection of a business organization. If the company found a number of defaulters in

account receivable aging report then the organization have to complete transformation to

tighter credit policies as cash flows in critical to the operation of an e-business. The

accountant will return of all the bad that of the organization. It is necessary for an

organization to know about who owns the money of organization.

Other managerial accounting reports: along with above mentioned report some reports

are are also important for every business organization which include project reports,

order Information Report, competitor analysis, and many other. These reports are made

by professionals (Fiorillo and et. al., 2019). If the organization is going to take decisions

it is necessary for them to take a site on accounting reports so that they can make and

develop Strategies and decisions in an effective and efficient manner.

TASK 2

P3 Calculation of costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs.

Below mentioned table shows the complete calculation of per unit cost for westfield

company. The data or amounts showing in the table are self sourced as an example.

Particulars Variable Cost Absorption

Cost

Direct material £ 270 £ 270

Direct Labour £ 47 £ 47

5

Performance report helps the organization in differentiating the employees on the basis of

their performance. According to this, management of organization also arrange training

and development program for low performing employees (Duff and et. al., 2020). The

role of this report is vital for an organization to keep an accurate measure of its strategy

towards is its mission.

Account receivable aging report: if any business organization is depend on the extending

credit then account receivable aging report plays an important role in their operations as it

helps the organization in recognising the defaulters by breaking down the clients

remaining balances into a specific period of time. It also finds various issues in process of

collection of a business organization. If the company found a number of defaulters in

account receivable aging report then the organization have to complete transformation to

tighter credit policies as cash flows in critical to the operation of an e-business. The

accountant will return of all the bad that of the organization. It is necessary for an

organization to know about who owns the money of organization.

Other managerial accounting reports: along with above mentioned report some reports

are are also important for every business organization which include project reports,

order Information Report, competitor analysis, and many other. These reports are made

by professionals (Fiorillo and et. al., 2019). If the organization is going to take decisions

it is necessary for them to take a site on accounting reports so that they can make and

develop Strategies and decisions in an effective and efficient manner.

TASK 2

P3 Calculation of costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs.

Below mentioned table shows the complete calculation of per unit cost for westfield

company. The data or amounts showing in the table are self sourced as an example.

Particulars Variable Cost Absorption

Cost

Direct material £ 270 £ 270

Direct Labour £ 47 £ 47

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

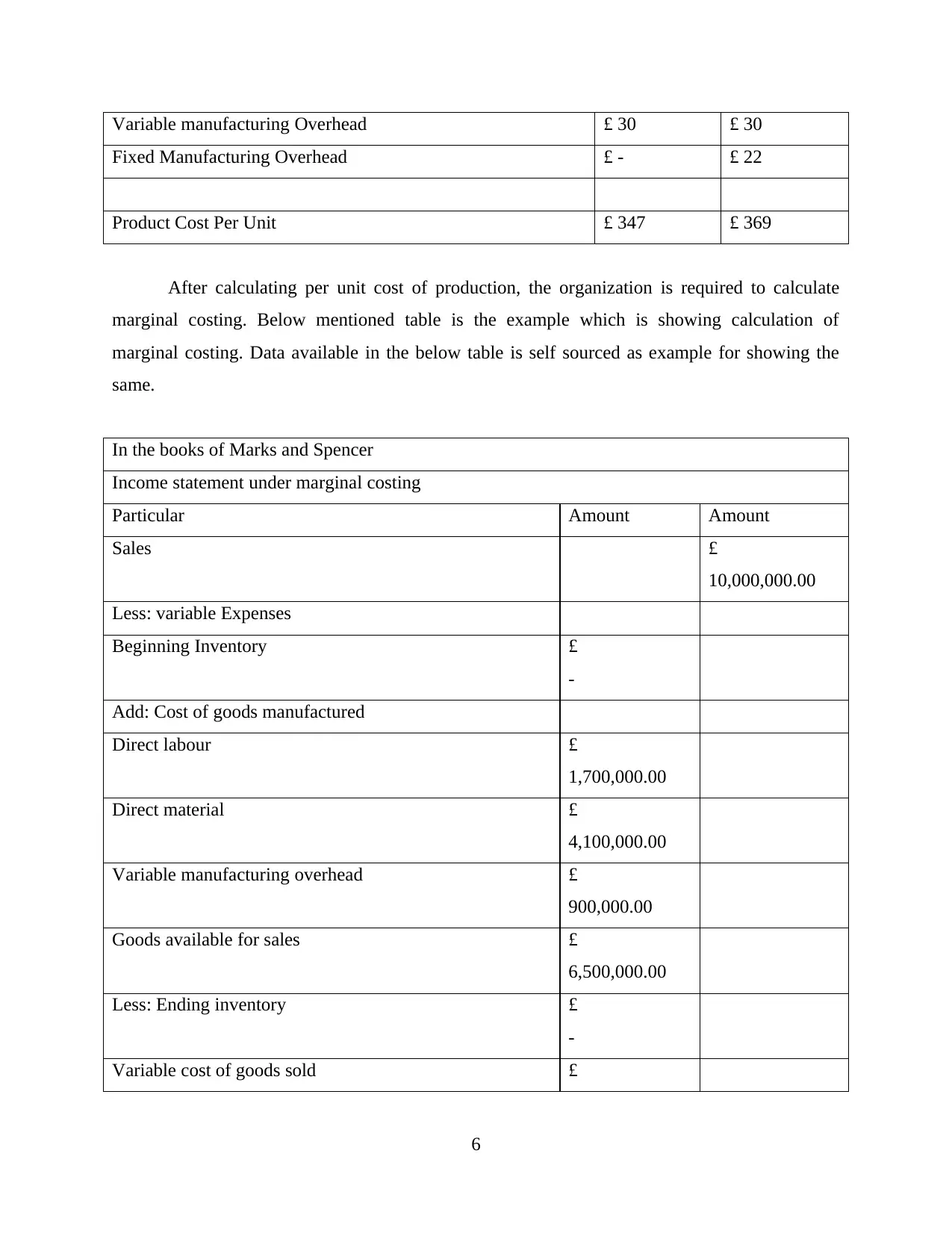

Variable manufacturing Overhead £ 30 £ 30

Fixed Manufacturing Overhead £ - £ 22

Product Cost Per Unit £ 347 £ 369

After calculating per unit cost of production, the organization is required to calculate

marginal costing. Below mentioned table is the example which is showing calculation of

marginal costing. Data available in the below table is self sourced as example for showing the

same.

In the books of Marks and Spencer

Income statement under marginal costing

Particular Amount Amount

Sales £

10,000,000.00

Less: variable Expenses

Beginning Inventory £

-

Add: Cost of goods manufactured

Direct labour £

1,700,000.00

Direct material £

4,100,000.00

Variable manufacturing overhead £

900,000.00

Goods available for sales £

6,500,000.00

Less: Ending inventory £

-

Variable cost of goods sold £

6

Fixed Manufacturing Overhead £ - £ 22

Product Cost Per Unit £ 347 £ 369

After calculating per unit cost of production, the organization is required to calculate

marginal costing. Below mentioned table is the example which is showing calculation of

marginal costing. Data available in the below table is self sourced as example for showing the

same.

In the books of Marks and Spencer

Income statement under marginal costing

Particular Amount Amount

Sales £

10,000,000.00

Less: variable Expenses

Beginning Inventory £

-

Add: Cost of goods manufactured

Direct labour £

1,700,000.00

Direct material £

4,100,000.00

Variable manufacturing overhead £

900,000.00

Goods available for sales £

6,500,000.00

Less: Ending inventory £

-

Variable cost of goods sold £

6

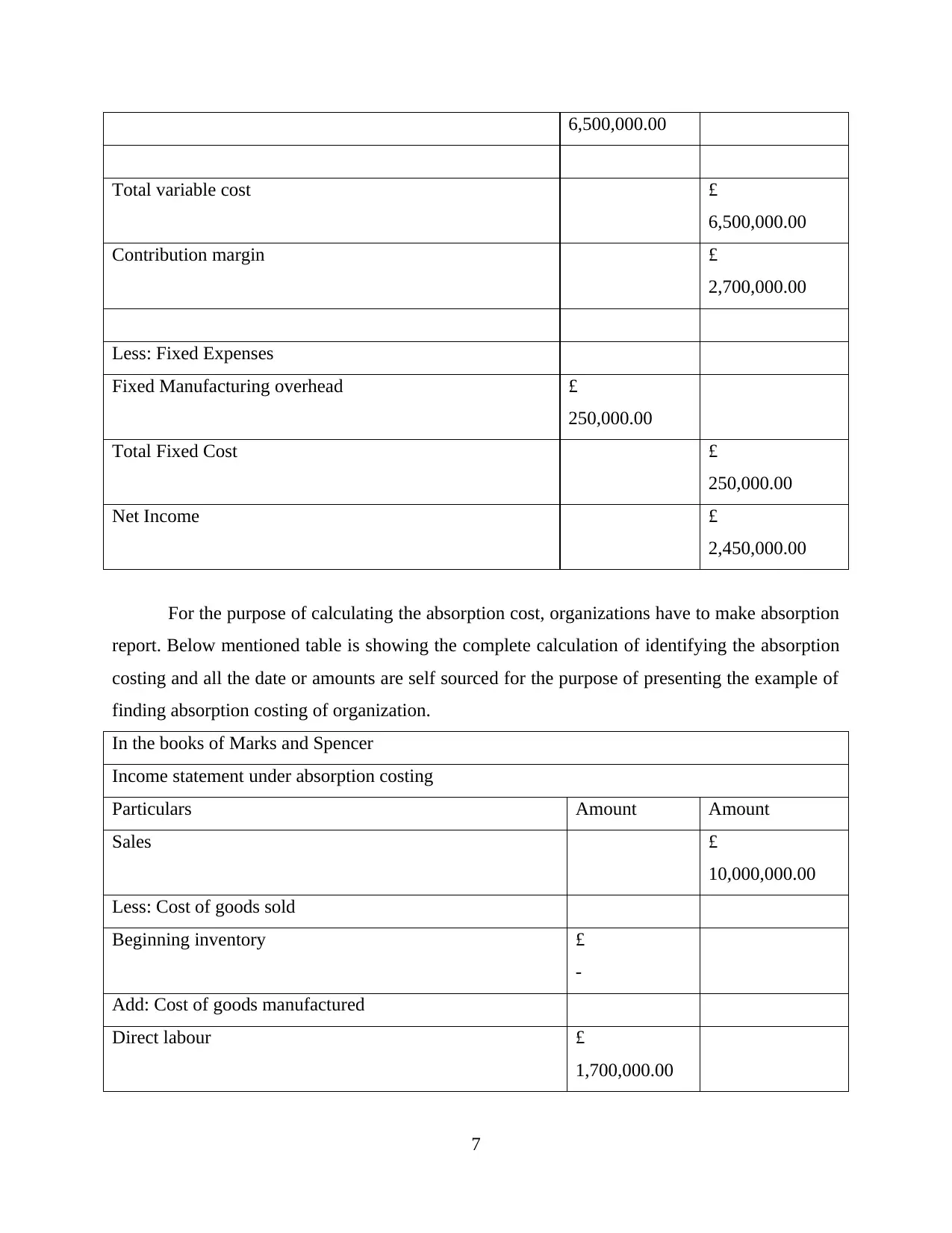

6,500,000.00

Total variable cost £

6,500,000.00

Contribution margin £

2,700,000.00

Less: Fixed Expenses

Fixed Manufacturing overhead £

250,000.00

Total Fixed Cost £

250,000.00

Net Income £

2,450,000.00

For the purpose of calculating the absorption cost, organizations have to make absorption

report. Below mentioned table is showing the complete calculation of identifying the absorption

costing and all the date or amounts are self sourced for the purpose of presenting the example of

finding absorption costing of organization.

In the books of Marks and Spencer

Income statement under absorption costing

Particulars Amount Amount

Sales £

10,000,000.00

Less: Cost of goods sold

Beginning inventory £

-

Add: Cost of goods manufactured

Direct labour £

1,700,000.00

7

Total variable cost £

6,500,000.00

Contribution margin £

2,700,000.00

Less: Fixed Expenses

Fixed Manufacturing overhead £

250,000.00

Total Fixed Cost £

250,000.00

Net Income £

2,450,000.00

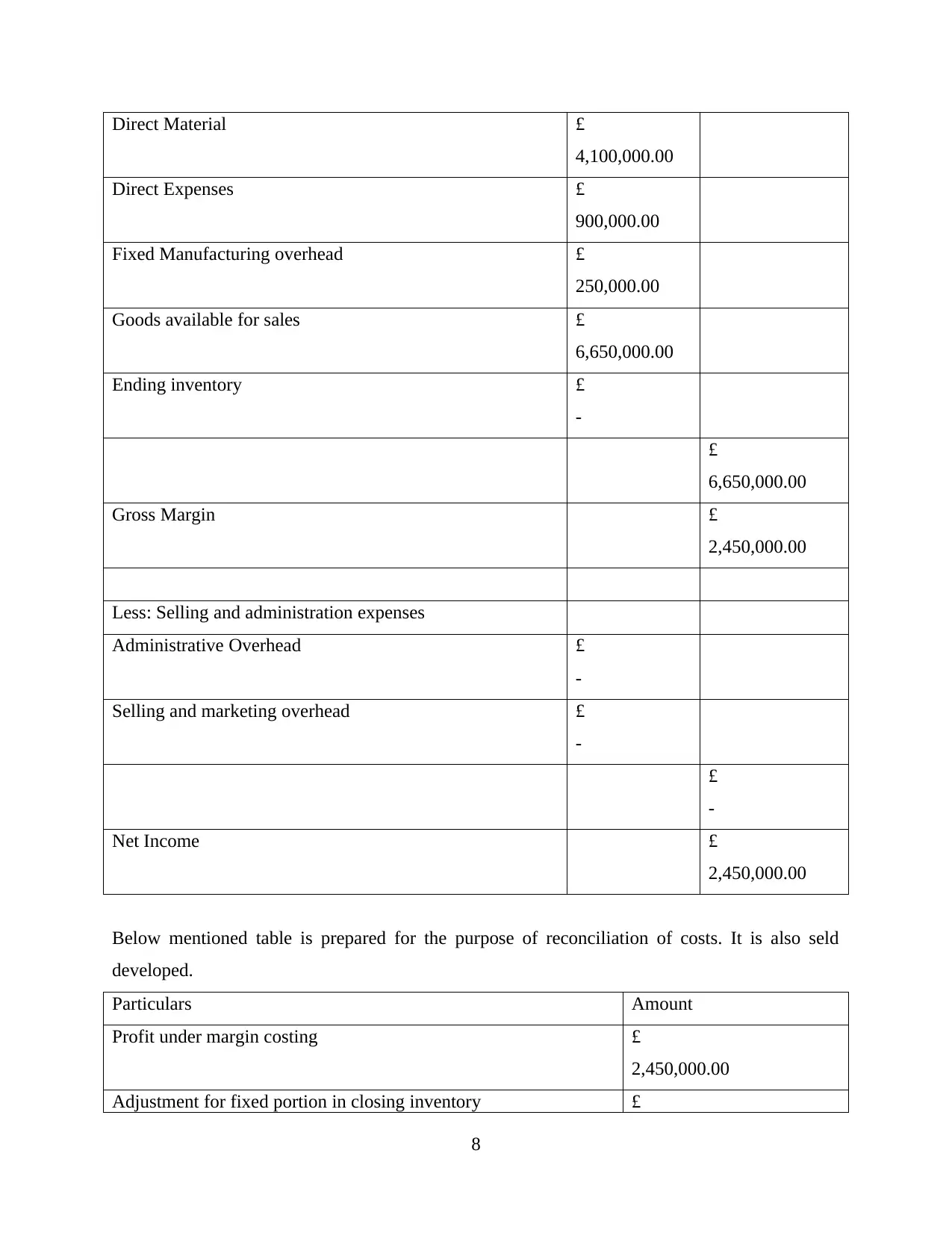

For the purpose of calculating the absorption cost, organizations have to make absorption

report. Below mentioned table is showing the complete calculation of identifying the absorption

costing and all the date or amounts are self sourced for the purpose of presenting the example of

finding absorption costing of organization.

In the books of Marks and Spencer

Income statement under absorption costing

Particulars Amount Amount

Sales £

10,000,000.00

Less: Cost of goods sold

Beginning inventory £

-

Add: Cost of goods manufactured

Direct labour £

1,700,000.00

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Direct Material £

4,100,000.00

Direct Expenses £

900,000.00

Fixed Manufacturing overhead £

250,000.00

Goods available for sales £

6,650,000.00

Ending inventory £

-

£

6,650,000.00

Gross Margin £

2,450,000.00

Less: Selling and administration expenses

Administrative Overhead £

-

Selling and marketing overhead £

-

£

-

Net Income £

2,450,000.00

Below mentioned table is prepared for the purpose of reconciliation of costs. It is also seld

developed.

Particulars Amount

Profit under margin costing £

2,450,000.00

Adjustment for fixed portion in closing inventory £

8

4,100,000.00

Direct Expenses £

900,000.00

Fixed Manufacturing overhead £

250,000.00

Goods available for sales £

6,650,000.00

Ending inventory £

-

£

6,650,000.00

Gross Margin £

2,450,000.00

Less: Selling and administration expenses

Administrative Overhead £

-

Selling and marketing overhead £

-

£

-

Net Income £

2,450,000.00

Below mentioned table is prepared for the purpose of reconciliation of costs. It is also seld

developed.

Particulars Amount

Profit under margin costing £

2,450,000.00

Adjustment for fixed portion in closing inventory £

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

-

Profit under absorption costing £

2,450,000.00

From the above taken example, it is found that, there is no closing inventory in the organization

which state that there is no any adjustment is made related to the fixed cost portion in the

inventory (Hasibuan, R.P.S. and Syahrial, H., 2019). Along with his, it is also found that the

profit under marginal costing and absorption costing are evaluated as same because of the

absence of closing inventory. So, it is suggested to the organization to do prepare budget on he

basis of their costs. The costing is also showing that the organization is highly successful. The

sales made the organization are highly targeted For the purpose of compensating the values

assigned towards the profit which will help in the generation of high sales of products in the long

run.

TASK 3

P4 Explanation of the advantages and disadvantages of various types of planning tools used for

budgetary control.

A budget approximately estimate the results of future of a business with the financial

position of firm for a specific period of time or it can be said at one or more financial year. In

simple words a family is stated that the budgets are prepared for estimating the future for making

Future Plans performance measurement needs controlling process and making innovative ideas

regarding the new products and services (Johanson and et. al., 2019). It also enables the business

in knowing about the financial needs according to time. The organization who is already

reviewing their budgets they are required to keep close eye on the reality so that they can assist

the variances in the actual result as earlier planned. Budgetary control has both advantages and

disadvantages on organization. Some of or advantages of budgetary control on Marks and

Spencer are given below:

Advantages

Maximization of profit: main focus of budgetary control is only on the maximization of profit of

the business organization. For the purpose of achieving objectives, it is necessary for

9

Profit under absorption costing £

2,450,000.00

From the above taken example, it is found that, there is no closing inventory in the organization

which state that there is no any adjustment is made related to the fixed cost portion in the

inventory (Hasibuan, R.P.S. and Syahrial, H., 2019). Along with his, it is also found that the

profit under marginal costing and absorption costing are evaluated as same because of the

absence of closing inventory. So, it is suggested to the organization to do prepare budget on he

basis of their costs. The costing is also showing that the organization is highly successful. The

sales made the organization are highly targeted For the purpose of compensating the values

assigned towards the profit which will help in the generation of high sales of products in the long

run.

TASK 3

P4 Explanation of the advantages and disadvantages of various types of planning tools used for

budgetary control.

A budget approximately estimate the results of future of a business with the financial

position of firm for a specific period of time or it can be said at one or more financial year. In

simple words a family is stated that the budgets are prepared for estimating the future for making

Future Plans performance measurement needs controlling process and making innovative ideas

regarding the new products and services (Johanson and et. al., 2019). It also enables the business

in knowing about the financial needs according to time. The organization who is already

reviewing their budgets they are required to keep close eye on the reality so that they can assist

the variances in the actual result as earlier planned. Budgetary control has both advantages and

disadvantages on organization. Some of or advantages of budgetary control on Marks and

Spencer are given below:

Advantages

Maximization of profit: main focus of budgetary control is only on the maximization of profit of

the business organization. For the purpose of achieving objectives, it is necessary for

9

organization to do proper planning and coordination between various departments so that they

can perform the functions in an effective and efficient manner. Because of budgetary control the

organization have proper control on capital and revenue expenditure as. Because of this they can

use resources in a proper and best possible way.

Coordination: budgetary control creates outline for All the departments working in an

organization. If the organization want to achieves the the desired goals and objectives so it is

necessary for them to do the work with the proper coordination of department (Jordão, R.V.D.,

2017). For the purpose of achieving budgetary target of organization it is necessary for all the

executive and subordinate to co-ordinate with one another.

Specific aim: top management makes and develop plans, policies and goals of organization. It is

necessary for organization to put all the efforts together to reach on the common goal of

organization. Every department makes sure that their target should be achieved in an effective

and efficient manner. The efforts put by various departments are only with the purpose of

achieving some specific aims. There is no any specific aim then the efforts of the complete

organization will be counted as waste.

Disadvantages

Uncertain future: budgets are always future oriented. But it can be used limitation for the

organization as the future prediction may not always comes true. The future is uncertain and the

situation which is assumed to prevail in future make change (Modell, S., 2019). A little bit

change in the future conditions can destroy the whole budget of organization. It may also destroy

all the preparations which were made by organization for the purpose of achieving their desired

goals and objectives. It is also found the Tata feature and certain it is decreased the utility of a

budgetary control system.

Discourage efficient persons: every employee or person of organization has assigned some

targets under the budgetary control system. Achieving the target is the only tendency of people

of organization. There are various efficient person in the organization which can exit the targets

but it will also make feel them content by reaching the target (Oesterreich, T.D. and Teuteberg,

F., 2019). So it can we say that budgets serve as constraints on managerial initiatives.

Conflict among different departments: sometimes it is also found at budgetary control system is

related to the creation of various conflicts among the functional departments of organization.

Every department think only about their department goal but not about the business goal. For the

10

can perform the functions in an effective and efficient manner. Because of budgetary control the

organization have proper control on capital and revenue expenditure as. Because of this they can

use resources in a proper and best possible way.

Coordination: budgetary control creates outline for All the departments working in an

organization. If the organization want to achieves the the desired goals and objectives so it is

necessary for them to do the work with the proper coordination of department (Jordão, R.V.D.,

2017). For the purpose of achieving budgetary target of organization it is necessary for all the

executive and subordinate to co-ordinate with one another.

Specific aim: top management makes and develop plans, policies and goals of organization. It is

necessary for organization to put all the efforts together to reach on the common goal of

organization. Every department makes sure that their target should be achieved in an effective

and efficient manner. The efforts put by various departments are only with the purpose of

achieving some specific aims. There is no any specific aim then the efforts of the complete

organization will be counted as waste.

Disadvantages

Uncertain future: budgets are always future oriented. But it can be used limitation for the

organization as the future prediction may not always comes true. The future is uncertain and the

situation which is assumed to prevail in future make change (Modell, S., 2019). A little bit

change in the future conditions can destroy the whole budget of organization. It may also destroy

all the preparations which were made by organization for the purpose of achieving their desired

goals and objectives. It is also found the Tata feature and certain it is decreased the utility of a

budgetary control system.

Discourage efficient persons: every employee or person of organization has assigned some

targets under the budgetary control system. Achieving the target is the only tendency of people

of organization. There are various efficient person in the organization which can exit the targets

but it will also make feel them content by reaching the target (Oesterreich, T.D. and Teuteberg,

F., 2019). So it can we say that budgets serve as constraints on managerial initiatives.

Conflict among different departments: sometimes it is also found at budgetary control system is

related to the creation of various conflicts among the functional departments of organization.

Every department think only about their department goal but not about the business goal. For the

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.