University Finance Module: Managing Financial Resources Report

VerifiedAdded on 2020/05/16

|29

|6242

|74

Report

AI Summary

This report provides a comprehensive analysis of financial resource management and decision-making, focusing on Marks & Spencer as a case study. It examines short-term and long-term sources of finance, including trade credit, bank loans, and equity financing, along with their implications and associated costs. The report delves into the importance of financial planning, the information needs of various decision-makers within the company, and the impact of financial decisions on financial statements. It also addresses cash budgeting, unit cost calculations, pricing decisions, and the application of investment appraisal techniques. Furthermore, the report compares financial statements of different business structures, evaluates Marks & Spencer's financial performance using various ratios, and provides recommendations for financial strategies. The report covers a wide array of topics related to financial management and decision-making, making it a valuable resource for students studying finance.

Running head: MANAGING FINANCIAL RESOURCES AND DECISIONS

Managing Financial Resources and Decisions

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Managing Financial Resources and Decisions

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGING FINANCIAL RESOURCES AND DECISIONS

Table of Contents

Task 1:.............................................................................................................................................3

AC 1.1 Short and medium term sources of finance available to Marks & Spencer:...................3

AC 1.2 Implications of the different sources of finance identified in the above section:...........4

AC 1.3 Appropriate sources of finance for a long-term project and recommendation of the

sources to be selected for Marks & Spencer:...............................................................................5

Task 2:.............................................................................................................................................7

AC 2.1 Costs of the different sources of finance identified in the above section:......................7

AC 2.2 Importance of financial planning to Marks & Spencer:..................................................8

AC 2.3 Information needs of different decision makers in Marks and Spencer:........................9

AC 2.4 Impact of the chosen sources of finance on the financial statements with reference to

Marks & Spencer:......................................................................................................................10

Task 3:...........................................................................................................................................11

AC 3.1 Problem identification and remedies to eliminate the problems in cash budget while

highlighting the importance of preparing cash budgets for decision-making in Croydon M&S

Store:..........................................................................................................................................11

AC 3.2 Calculation of unit costs and making pricing decisions:...............................................13

AC 3.3 Assessment of the viability of the two projects using investment appraisal techniques

in the context of Marks & Spencer:...........................................................................................15

Task 4:...........................................................................................................................................16

Table of Contents

Task 1:.............................................................................................................................................3

AC 1.1 Short and medium term sources of finance available to Marks & Spencer:...................3

AC 1.2 Implications of the different sources of finance identified in the above section:...........4

AC 1.3 Appropriate sources of finance for a long-term project and recommendation of the

sources to be selected for Marks & Spencer:...............................................................................5

Task 2:.............................................................................................................................................7

AC 2.1 Costs of the different sources of finance identified in the above section:......................7

AC 2.2 Importance of financial planning to Marks & Spencer:..................................................8

AC 2.3 Information needs of different decision makers in Marks and Spencer:........................9

AC 2.4 Impact of the chosen sources of finance on the financial statements with reference to

Marks & Spencer:......................................................................................................................10

Task 3:...........................................................................................................................................11

AC 3.1 Problem identification and remedies to eliminate the problems in cash budget while

highlighting the importance of preparing cash budgets for decision-making in Croydon M&S

Store:..........................................................................................................................................11

AC 3.2 Calculation of unit costs and making pricing decisions:...............................................13

AC 3.3 Assessment of the viability of the two projects using investment appraisal techniques

in the context of Marks & Spencer:...........................................................................................15

Task 4:...........................................................................................................................................16

2MANAGING FINANCIAL RESOURCES AND DECISIONS

AC 4.1 Main financial statements used in a business:...............................................................16

AC 4.2 Comparison of financial statements of a sole trader with those of a Public Limited

Company:...................................................................................................................................17

AC 4.3 Financial performance of Marks & Spencer by evaluating various ratios:...................18

References:....................................................................................................................................23

Appendices:...................................................................................................................................27

AC 4.1 Main financial statements used in a business:...............................................................16

AC 4.2 Comparison of financial statements of a sole trader with those of a Public Limited

Company:...................................................................................................................................17

AC 4.3 Financial performance of Marks & Spencer by evaluating various ratios:...................18

References:....................................................................................................................................23

Appendices:...................................................................................................................................27

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGING FINANCIAL RESOURCES AND DECISIONS

Task 1:

AC 1.1 Short and medium term sources of finance available to Marks & Spencer:

The sources of finance are both medium term and short term and these are available to

Marks & Spencer in the following:

Trade credit:

Trade credit is the fund received from the suppliers over the period between the delivery

of products and the successive account settlement made on the part of the recipient (Balaban,

Župljanin and Ivanović 2017). One method through which Marks & Spencer could express the

credit term is “2/10: net 30”. This denotes that 2% discount would be provided on the part of the

supplier; in case, the amount is paid back. In opposition, the organisation needs to make the

entire payment within 30 days. The trade credit length is reliant on various influential dynamics

such as industrial practices and customers, kind of products and relative bargaining power.

Bank credit and overdrafts:

The bank lending to the organisations is predominantly short-term; however, it is now

available in the form of medium-term source of finance as well. On the other hand, overdrafts

signify the amount that an organisation might withdraw as cash or cheques (Baños-Caballero,

García-Teruel and Martínez-Solano 2014). The bank normally takes security in the form of fixed

charge or floating charge. Fixed charge could be defined as the situation, in which there is

security of overdraft against particular asset, while floating charge provides security on all the

assets of the business.

Hire purchase:

Task 1:

AC 1.1 Short and medium term sources of finance available to Marks & Spencer:

The sources of finance are both medium term and short term and these are available to

Marks & Spencer in the following:

Trade credit:

Trade credit is the fund received from the suppliers over the period between the delivery

of products and the successive account settlement made on the part of the recipient (Balaban,

Župljanin and Ivanović 2017). One method through which Marks & Spencer could express the

credit term is “2/10: net 30”. This denotes that 2% discount would be provided on the part of the

supplier; in case, the amount is paid back. In opposition, the organisation needs to make the

entire payment within 30 days. The trade credit length is reliant on various influential dynamics

such as industrial practices and customers, kind of products and relative bargaining power.

Bank credit and overdrafts:

The bank lending to the organisations is predominantly short-term; however, it is now

available in the form of medium-term source of finance as well. On the other hand, overdrafts

signify the amount that an organisation might withdraw as cash or cheques (Baños-Caballero,

García-Teruel and Martínez-Solano 2014). The bank normally takes security in the form of fixed

charge or floating charge. Fixed charge could be defined as the situation, in which there is

security of overdraft against particular asset, while floating charge provides security on all the

assets of the business.

Hire purchase:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGING FINANCIAL RESOURCES AND DECISIONS

Hire purchase could be described as hiring with the alternative to buy. When the final

instalment is paid, the asset ownership is transferred to the buyer. Thus, with the help of inland

revenues, Marks & Spencer would be able to claim as well as retain capital allowances that the

purchase fee option is lower in contrast to the market value after the expiry of the term contract.

Leasing:

In the words of Benedettini, Swink and Neely (2015), leasing transaction is a commercial

contract, in which the owner of equipment has the right of using the same in exchange for

payment on the part of the equipment user of a particular rental over a pre-agreed timeframe.

AC 1.2 Implications of the different sources of finance identified in the above section:

As assessed above, various sources of funding are available to Marks & Spencer. By

listing each source of finance, the implications at the business cost could be evaluated. In the

initial stage, all organisations need short-term funding for covering daily running cost. Short-

term and medium-term sources of finance help in providing the primary working capital to

Marks & Spencer. The implications of these sources of finance are discussed as follows:

Trade credit:

Trade credit is the credit allowed in relation to the raw materials that the manufacturers

use in producing the products purchased for resale on the part of the retailer. When Marks &

Spencer purchases products from its suppliers, payment is not made instantly. In this period, the

purchaser owes an outstanding debt to the supplier before the payment is due. This outstanding

debt is reported in the liability side of the balance sheet statement of the organisation under

accounts receivable.

Hire purchase could be described as hiring with the alternative to buy. When the final

instalment is paid, the asset ownership is transferred to the buyer. Thus, with the help of inland

revenues, Marks & Spencer would be able to claim as well as retain capital allowances that the

purchase fee option is lower in contrast to the market value after the expiry of the term contract.

Leasing:

In the words of Benedettini, Swink and Neely (2015), leasing transaction is a commercial

contract, in which the owner of equipment has the right of using the same in exchange for

payment on the part of the equipment user of a particular rental over a pre-agreed timeframe.

AC 1.2 Implications of the different sources of finance identified in the above section:

As assessed above, various sources of funding are available to Marks & Spencer. By

listing each source of finance, the implications at the business cost could be evaluated. In the

initial stage, all organisations need short-term funding for covering daily running cost. Short-

term and medium-term sources of finance help in providing the primary working capital to

Marks & Spencer. The implications of these sources of finance are discussed as follows:

Trade credit:

Trade credit is the credit allowed in relation to the raw materials that the manufacturers

use in producing the products purchased for resale on the part of the retailer. When Marks &

Spencer purchases products from its suppliers, payment is not made instantly. In this period, the

purchaser owes an outstanding debt to the supplier before the payment is due. This outstanding

debt is reported in the liability side of the balance sheet statement of the organisation under

accounts receivable.

5MANAGING FINANCIAL RESOURCES AND DECISIONS

Bank credit and overdrafts:

As an organisation could pass through liquidity shortage, it might borrow funds for a

short time span of six months from the banks having surplus liquidity. Based on the amount and

period of the borrowed amount, there is variation in the rate of interest, which Marks & Spencer

need to bear for continuing its business operations.

Hire purchase and leasing:

The organisation could acquire the asset on lease from the lessor rather than procuring

funds in order to buy equipments. For hire purchase, the acquisition of asset is made on credit

and the payment is made on the terms and conditions, which are laid out in the agreement of hire

purchase.

AC 1.3 Appropriate sources of finance for a long-term project and recommendation of the

sources to be selected for Marks & Spencer:

The kind of finance selected relies on the size and nature of an organisation (Benson, Faff

and Smith 2014). For selecting the kind of financing alternative, an effective source of finance is

significant. The sources of finance could be internal as well as external sources. The internal

sources of finance for the long-term project of Marks & Spencer include the following:

Owner’s investment:

It denotes the amount that is generated from the personal savings of the owner (Biddle

2015). This is a long-term source of finance, which is used as start-up capital for investing in the

desired project.

Sale of stock:

Bank credit and overdrafts:

As an organisation could pass through liquidity shortage, it might borrow funds for a

short time span of six months from the banks having surplus liquidity. Based on the amount and

period of the borrowed amount, there is variation in the rate of interest, which Marks & Spencer

need to bear for continuing its business operations.

Hire purchase and leasing:

The organisation could acquire the asset on lease from the lessor rather than procuring

funds in order to buy equipments. For hire purchase, the acquisition of asset is made on credit

and the payment is made on the terms and conditions, which are laid out in the agreement of hire

purchase.

AC 1.3 Appropriate sources of finance for a long-term project and recommendation of the

sources to be selected for Marks & Spencer:

The kind of finance selected relies on the size and nature of an organisation (Benson, Faff

and Smith 2014). For selecting the kind of financing alternative, an effective source of finance is

significant. The sources of finance could be internal as well as external sources. The internal

sources of finance for the long-term project of Marks & Spencer include the following:

Owner’s investment:

It denotes the amount that is generated from the personal savings of the owner (Biddle

2015). This is a long-term source of finance, which is used as start-up capital for investing in the

desired project.

Sale of stock:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGING FINANCIAL RESOURCES AND DECISIONS

Profit could be generated from selling the unsold stock and it is ploughed back into the

business for expansion projects. Hence, by selling a part of its stock, Marks & Spencer could

raise funds for financing its long-term project.

Debt collection:

Marks & Spencer has a number of debtors, who owe money to the organisation. Thus, in

order to raise funds for funding long-term project, the organisation could minimise the debtor

terms, which would help in increasing its working capital base. The amount collected could be

used for funding a portion of its long-term project.

Marks & Spencer could raise funds from various external sources, which are depicted as

follows:

Debt financing:

In order to fund long-term project, Marks & Spencer could obtain long-term loan from

the banks at a certain rate of interest. In this case, the organisation needs to pay a certain amount

in the form of interest, which would be reported in the cash flow statement as repayment of

borrowings (Churet and Eccles 2014).

Equity financing:

Marks & Spencer could issue additional equity shares in the market for raising funds in

order to finance its long-term project. This source of funding is less risky for the organisation,

since the liability burden of the organisation would not increase.

Profit could be generated from selling the unsold stock and it is ploughed back into the

business for expansion projects. Hence, by selling a part of its stock, Marks & Spencer could

raise funds for financing its long-term project.

Debt collection:

Marks & Spencer has a number of debtors, who owe money to the organisation. Thus, in

order to raise funds for funding long-term project, the organisation could minimise the debtor

terms, which would help in increasing its working capital base. The amount collected could be

used for funding a portion of its long-term project.

Marks & Spencer could raise funds from various external sources, which are depicted as

follows:

Debt financing:

In order to fund long-term project, Marks & Spencer could obtain long-term loan from

the banks at a certain rate of interest. In this case, the organisation needs to pay a certain amount

in the form of interest, which would be reported in the cash flow statement as repayment of

borrowings (Churet and Eccles 2014).

Equity financing:

Marks & Spencer could issue additional equity shares in the market for raising funds in

order to finance its long-term project. This source of funding is less risky for the organisation,

since the liability burden of the organisation would not increase.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGING FINANCIAL RESOURCES AND DECISIONS

Hence, the appropriate sources of finance for Marks & Spencer include retained earnings,

bank loans and issuance of equity shares and these could be used for funding its long-term

project.

Task 2:

AC 2.1 Costs of the different sources of finance identified in the above section:

Marks & Spencer could use retained earnings, bank loans and issuance of equity shares in

order to undertake its long-term project. Hence, these sources of finance would impose financial

and opportunity cost on the organisation. Both these costs have significant effects on the

profitability and growth of the organisation and these are described briefly as follows:

Financial cost:

Various financial institutions and banks might impose greater financial cost in front of

Marks & Spencer. These institutions and banks charge increased rate of interest against the loans

provided (Clark, Feiner and Viehs 2015). In addition, the organisation is needed to repay the loan

amount in instalments, which would have direct influence on its profitability and liquidity

aspects. The interest expense would rise for the organisation and hence, this would result in

minimised profit before tax and net income. On the other hand, Marks & Spencer might have to

use its cash base for repaying interest loans and as a result, the current asset base would fall. As

the debt burden of Marks & Spencer increases, the organisation would have to use its asset base

for discharging such obligations. I

Opportunity cost:

Hence, the appropriate sources of finance for Marks & Spencer include retained earnings,

bank loans and issuance of equity shares and these could be used for funding its long-term

project.

Task 2:

AC 2.1 Costs of the different sources of finance identified in the above section:

Marks & Spencer could use retained earnings, bank loans and issuance of equity shares in

order to undertake its long-term project. Hence, these sources of finance would impose financial

and opportunity cost on the organisation. Both these costs have significant effects on the

profitability and growth of the organisation and these are described briefly as follows:

Financial cost:

Various financial institutions and banks might impose greater financial cost in front of

Marks & Spencer. These institutions and banks charge increased rate of interest against the loans

provided (Clark, Feiner and Viehs 2015). In addition, the organisation is needed to repay the loan

amount in instalments, which would have direct influence on its profitability and liquidity

aspects. The interest expense would rise for the organisation and hence, this would result in

minimised profit before tax and net income. On the other hand, Marks & Spencer might have to

use its cash base for repaying interest loans and as a result, the current asset base would fall. As

the debt burden of Marks & Spencer increases, the organisation would have to use its asset base

for discharging such obligations. I

Opportunity cost:

8MANAGING FINANCIAL RESOURCES AND DECISIONS

Opportunity cost is the loss that a business incurs while selecting any other option. If

Marks & Spencer is involved in using the retained earnings, it might hinder its ability to pay

dividends to the shareholders or grabbing future opportunities. As a result, an unstable position

would be formed in the eyes of the shareholders (DeFusco et al. 2015). Furthermore, it would

become difficult for the organisation to combat with the sudden contingencies that might happen

in future.

AC 2.2 Importance of financial planning to Marks & Spencer:

Financial planning could be defined as a procedure, which helps a firm to make different

profitable and sensible decisions. Marks & Spencer could be able to distribute funds effectively

in all the departments by planning the financial activities. As a result, the organisation would be

steered towards growth and development. The importance of financial planning to Marks &

Spencer is represented as follows:

With the help of financial planning, all the business activities could be controlled that

happen within an organisation (Finkler et al. 2016). Thus, Marks & Spencer would be

able to obtain deeper knowledge regarding funds, which is available within the

organisation for fulfilling its daily needs.

Financial planning helps the organisation in using the available resources fully through

which it could be able to minimise the wastage of resources.

Financial planning assists Marks & Spencer in relation to the fund, which the

organisation raises against the sources of funds.

If the financial activities are planned, they could help Marks & Spencer to fulfil the future

needs. Along with this, the organisation would be able to overcome the different

contingencies, which could occur when sales are anticipated.

Opportunity cost is the loss that a business incurs while selecting any other option. If

Marks & Spencer is involved in using the retained earnings, it might hinder its ability to pay

dividends to the shareholders or grabbing future opportunities. As a result, an unstable position

would be formed in the eyes of the shareholders (DeFusco et al. 2015). Furthermore, it would

become difficult for the organisation to combat with the sudden contingencies that might happen

in future.

AC 2.2 Importance of financial planning to Marks & Spencer:

Financial planning could be defined as a procedure, which helps a firm to make different

profitable and sensible decisions. Marks & Spencer could be able to distribute funds effectively

in all the departments by planning the financial activities. As a result, the organisation would be

steered towards growth and development. The importance of financial planning to Marks &

Spencer is represented as follows:

With the help of financial planning, all the business activities could be controlled that

happen within an organisation (Finkler et al. 2016). Thus, Marks & Spencer would be

able to obtain deeper knowledge regarding funds, which is available within the

organisation for fulfilling its daily needs.

Financial planning helps the organisation in using the available resources fully through

which it could be able to minimise the wastage of resources.

Financial planning assists Marks & Spencer in relation to the fund, which the

organisation raises against the sources of funds.

If the financial activities are planned, they could help Marks & Spencer to fulfil the future

needs. Along with this, the organisation would be able to overcome the different

contingencies, which could occur when sales are anticipated.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGING FINANCIAL RESOURCES AND DECISIONS

AC 2.3 Information needs of different decision makers in Marks and Spencer:

Various decision makers or stakeholders need various kinds of information for making

useful decisions. Hence, some of the information that the various stakeholders needs is described

as follows:

Managers:

The managers review the income statement and the cash flow statement of Marks &

Spencer for assessing its liquidity position. The managers of the organisation prefer the balance

sheet statement as well for obtaining wider insights about its financial performance in a specific

period (Fullerton, Kennedy and Widener 2014).

Investors:

The investors primarily prefer the income statement and balance sheet statement of the

organisation for determining whether Marks & Spencer is in a position to provide them with

increased rate of return. Along with this, the investors prefer these statements for evaluating the

financial position of the organisation for making investment-related decisions.

Staffs:

Staffs are the persons involved in working for the betterment of the organisation (Gitman,

Juchau and Flanagan 2015). The staffs of Marks & Spencer desire for fair salary, incentives and

bonus, in lieu of which they want to assess the income statement of the organisation, in lieu of

which the staffs are required to view the income statement of the organisation. In addition, this

statement is preferred for determining the profitability aspects of the organisation.

Suppliers:

AC 2.3 Information needs of different decision makers in Marks and Spencer:

Various decision makers or stakeholders need various kinds of information for making

useful decisions. Hence, some of the information that the various stakeholders needs is described

as follows:

Managers:

The managers review the income statement and the cash flow statement of Marks &

Spencer for assessing its liquidity position. The managers of the organisation prefer the balance

sheet statement as well for obtaining wider insights about its financial performance in a specific

period (Fullerton, Kennedy and Widener 2014).

Investors:

The investors primarily prefer the income statement and balance sheet statement of the

organisation for determining whether Marks & Spencer is in a position to provide them with

increased rate of return. Along with this, the investors prefer these statements for evaluating the

financial position of the organisation for making investment-related decisions.

Staffs:

Staffs are the persons involved in working for the betterment of the organisation (Gitman,

Juchau and Flanagan 2015). The staffs of Marks & Spencer desire for fair salary, incentives and

bonus, in lieu of which they want to assess the income statement of the organisation, in lieu of

which the staffs are required to view the income statement of the organisation. In addition, this

statement is preferred for determining the profitability aspects of the organisation.

Suppliers:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGING FINANCIAL RESOURCES AND DECISIONS

In the words of Kajola, Adewumi and Oworu (2015), suppliers are those that provide raw

materials to the organisation for manufacturing finished products. These decision-makers would

be interested in the income statement and cash flow statement of Marks & Spencer for

ascertaining whether the organisation is in a position to pay them timely for the materials

supplied.

Government:

Since the intention of the UK government is to ensure the welfare of the society, it wants

each organisation to grow while generating additional employment opportunities. In addition, the

government wants Marks & Spencer to pay its corporate tax within time. Hence, it prefers the

income statement and balance sheet statement of the organisation.

AC 2.4 Impact of the chosen sources of finance on the financial statements with reference

to Marks & Spencer:

It has been observed that various sources of finance have different effects on the financial

statements of an organisation (Karadag 2015). Each source that the organisation uses has direct

impact on the financial statements. Thus, in lieu of which the organisation is needed to choose

the sources of funding by keeping in mind the influence of these sources on the financial

statements. Marks & Spencer prefer retained earnings, bank loan and issuance of equity shares

for raising funds for its long-term project. For instance, it is assumed that Marks & Spencer has

obtained bank loan of £400,000 at 10% interest rate per annum. In this scenario, the bank loan

has effect on both income statement and balance sheet statement of the organisation.

In the words of Kajola, Adewumi and Oworu (2015), suppliers are those that provide raw

materials to the organisation for manufacturing finished products. These decision-makers would

be interested in the income statement and cash flow statement of Marks & Spencer for

ascertaining whether the organisation is in a position to pay them timely for the materials

supplied.

Government:

Since the intention of the UK government is to ensure the welfare of the society, it wants

each organisation to grow while generating additional employment opportunities. In addition, the

government wants Marks & Spencer to pay its corporate tax within time. Hence, it prefers the

income statement and balance sheet statement of the organisation.

AC 2.4 Impact of the chosen sources of finance on the financial statements with reference

to Marks & Spencer:

It has been observed that various sources of finance have different effects on the financial

statements of an organisation (Karadag 2015). Each source that the organisation uses has direct

impact on the financial statements. Thus, in lieu of which the organisation is needed to choose

the sources of funding by keeping in mind the influence of these sources on the financial

statements. Marks & Spencer prefer retained earnings, bank loan and issuance of equity shares

for raising funds for its long-term project. For instance, it is assumed that Marks & Spencer has

obtained bank loan of £400,000 at 10% interest rate per annum. In this scenario, the bank loan

has effect on both income statement and balance sheet statement of the organisation.

11MANAGING FINANCIAL RESOURCES AND DECISIONS

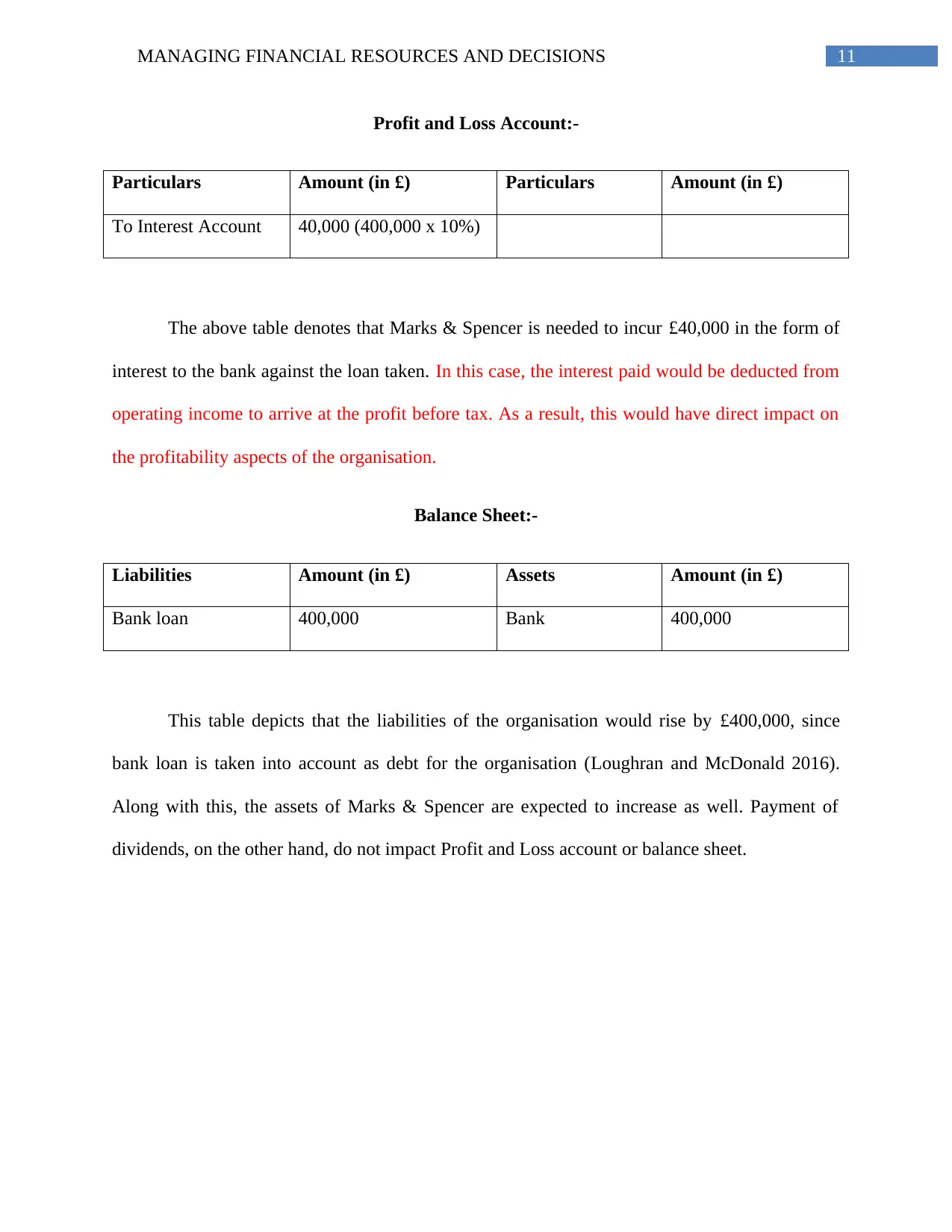

Profit and Loss Account:-

Particulars Amount (in £) Particulars Amount (in £)

To Interest Account 40,000 (400,000 x 10%)

The above table denotes that Marks & Spencer is needed to incur £40,000 in the form of

interest to the bank against the loan taken. In this case, the interest paid would be deducted from

operating income to arrive at the profit before tax. As a result, this would have direct impact on

the profitability aspects of the organisation.

Balance Sheet:-

Liabilities Amount (in £) Assets Amount (in £)

Bank loan 400,000 Bank 400,000

This table depicts that the liabilities of the organisation would rise by £400,000, since

bank loan is taken into account as debt for the organisation (Loughran and McDonald 2016).

Along with this, the assets of Marks & Spencer are expected to increase as well. Payment of

dividends, on the other hand, do not impact Profit and Loss account or balance sheet.

Profit and Loss Account:-

Particulars Amount (in £) Particulars Amount (in £)

To Interest Account 40,000 (400,000 x 10%)

The above table denotes that Marks & Spencer is needed to incur £40,000 in the form of

interest to the bank against the loan taken. In this case, the interest paid would be deducted from

operating income to arrive at the profit before tax. As a result, this would have direct impact on

the profitability aspects of the organisation.

Balance Sheet:-

Liabilities Amount (in £) Assets Amount (in £)

Bank loan 400,000 Bank 400,000

This table depicts that the liabilities of the organisation would rise by £400,000, since

bank loan is taken into account as debt for the organisation (Loughran and McDonald 2016).

Along with this, the assets of Marks & Spencer are expected to increase as well. Payment of

dividends, on the other hand, do not impact Profit and Loss account or balance sheet.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 29

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.