Financial Reporting: Marks and Spencer's Performance and Analysis

VerifiedAdded on 2020/12/23

|11

|2877

|264

Report

AI Summary

This report provides a comprehensive analysis of financial reporting, focusing on Marks and Spencer. It begins with an introduction to financial reporting, its purpose, and core concepts. The report then delves into the conceptual and regulatory frameworks, highlighting the importance of IFRS and IAS. It identifies key stakeholders, including management, employees, customers, and shareholders, and explains their needs for financial information. The analysis evaluates the value of financial reporting in meeting organizational objectives and growth, and discusses the benefits of international accounting standards. The report also applies financial reporting theories, such as residual equity theory and legitimacy theory. Furthermore, it presents a financial ratio analysis of Marks and Spencer's performance, evaluating profitability, liquidity, solvency, and efficiency. The report concludes by addressing differences in financial reporting across the world and the degree of IFRS compliance.

FINANCIAL REPORTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION.......................................................................................................................................3

MAIN BODY..............................................................................................................................................3

1. Purpose and concept of financial reporting..........................................................................................3

2. Conceptual and regulatory framework of financial reporting.............................................................3

3. Key stakeholders of organization and their need of using financial reports.........................................4

4. Value of financial reporting for meeting organizational objectives and growth.................................5

5. International accounting standard and international financial reporting standard with their benefits...5

6. Evaluation of financial reporting through application of theories and models.....................................6

7. Differences in financial reporting across the world............................................................................8

8. Degree of compliance with IFRS across the world.............................................................................8

CONCLUSION...........................................................................................................................................9

REFERENCES..........................................................................................................................................10

INTRODUCTION.......................................................................................................................................3

MAIN BODY..............................................................................................................................................3

1. Purpose and concept of financial reporting..........................................................................................3

2. Conceptual and regulatory framework of financial reporting.............................................................3

3. Key stakeholders of organization and their need of using financial reports.........................................4

4. Value of financial reporting for meeting organizational objectives and growth.................................5

5. International accounting standard and international financial reporting standard with their benefits...5

6. Evaluation of financial reporting through application of theories and models.....................................6

7. Differences in financial reporting across the world............................................................................8

8. Degree of compliance with IFRS across the world.............................................................................8

CONCLUSION...........................................................................................................................................9

REFERENCES..........................................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial reporting refers to the system of recording the financial information in form of

statement in order to provide information to the stakeholders regarding the financial position and

performance of firm. In this study, Marks and Spencer will be consider which is involved in

fashion industry and provide clothing for men, women and kids. This assignment will include

the concept and purpose of financial reporting. Moreover, It will provide understanding about the

conceptual and regulatory framework of financial reporting. Also, it will contain information

about IFRS and IAS.

MAIN BODY

1. Purpose and concept of financial reporting

Financial Reporting is related to recording of financial information which assist in

providing useful information to the stakeholders for their decision making. The main purpose of

financial reporting is to provide accurate and useful information to the stakeholders. The purpose

of financial reporting is to record the various operations of business in the statement form. There

are different financial reporting statements which provide different information to the users. It

consists of income statement, balance sheet and cash flow statement.

The income statement consists of income and expenditure for a specified period which

provides understanding about the profitability of the firm by comparing the incomes with that of

expenses to identify the net income or loss for a period. Balance sheet is the statement which is

prepared to identify the financial position of the firm through use of the assets and liabilities to

identify the liquidity position of the company (Leuz and Wysocki, 2016 ). Cash flow statement

records the information n about the cash inflow and outflow for a period to identify the future

cash requirement of business. The purpose and concept of financial reporting is to provide

accurate information to the investors and other stakeholders to get understanding about the

company’s profitability and position for various decisions making.

2. Conceptual and regulatory framework of financial reporting

The conceptual framework of financial reporting is the set of fundamental concepts

which are used for reporting of information in the report formats. It assists in developing

accounting policies for companies. The conceptual framework provides the understanding about

objective of general purpose of financial reporting (Williams and Dobelman, 2017). Moreover, it

defines the qualitative characteristics of useful financial information. It defines the elements of

the various statement such as assets, liabilities, income, expense equity etc. Also, it defines

concepts regarding capital and capital maintenance. The regulatory framework of financial

reporting gives information about the regulatory standards which are made for the compliance of

International financial reporting framework. It means the financial reporting are regulated on the

Financial reporting refers to the system of recording the financial information in form of

statement in order to provide information to the stakeholders regarding the financial position and

performance of firm. In this study, Marks and Spencer will be consider which is involved in

fashion industry and provide clothing for men, women and kids. This assignment will include

the concept and purpose of financial reporting. Moreover, It will provide understanding about the

conceptual and regulatory framework of financial reporting. Also, it will contain information

about IFRS and IAS.

MAIN BODY

1. Purpose and concept of financial reporting

Financial Reporting is related to recording of financial information which assist in

providing useful information to the stakeholders for their decision making. The main purpose of

financial reporting is to provide accurate and useful information to the stakeholders. The purpose

of financial reporting is to record the various operations of business in the statement form. There

are different financial reporting statements which provide different information to the users. It

consists of income statement, balance sheet and cash flow statement.

The income statement consists of income and expenditure for a specified period which

provides understanding about the profitability of the firm by comparing the incomes with that of

expenses to identify the net income or loss for a period. Balance sheet is the statement which is

prepared to identify the financial position of the firm through use of the assets and liabilities to

identify the liquidity position of the company (Leuz and Wysocki, 2016 ). Cash flow statement

records the information n about the cash inflow and outflow for a period to identify the future

cash requirement of business. The purpose and concept of financial reporting is to provide

accurate information to the investors and other stakeholders to get understanding about the

company’s profitability and position for various decisions making.

2. Conceptual and regulatory framework of financial reporting

The conceptual framework of financial reporting is the set of fundamental concepts

which are used for reporting of information in the report formats. It assists in developing

accounting policies for companies. The conceptual framework provides the understanding about

objective of general purpose of financial reporting (Williams and Dobelman, 2017). Moreover, it

defines the qualitative characteristics of useful financial information. It defines the elements of

the various statement such as assets, liabilities, income, expense equity etc. Also, it defines

concepts regarding capital and capital maintenance. The regulatory framework of financial

reporting gives information about the regulatory standards which are made for the compliance of

International financial reporting framework. It means the financial reporting are regulated on the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

basis of standards provided by IASB. The principles of financial reporting include full

disclosure of accounting information.

Moreover, the principle of accounting is to provide true and fair view of accounting information.

The financial statements must be consistent in order to have comparison with the past years

financial statement or comparison with other companies. The main purpose of the financial

reporting principles to provide better and clear understanding to the stakeholder of company

regarding the financial performance and position of the firm (Ge and et.al., 2018). Principles are

required for treatment of various transactions and disclosure of the accounting information in

order to reduce the chance missing of information.

3. Key stakeholders of organization and their need of using financial reports

The key stakeholders of the marks and Spencer consist of internal stakeholders and external

stakeholders. Internal stakeholders of the firms are those which are present in the organization

and consist of the following:

Management: The managers are the internal stakeholders of the organization which uses the

financial information to make future decision for the firm in order to enhance the profitability

and performance of the company.

Employees : The employees in the organization uses the financial information to have their job

security by understanding the business profitability to make decision regarding their job.

Owners: the owners or the board of directors uses the financial information to identify their

business profit ability in order to make changes in their policies and their norms to enhance their

business performance.

External stakeholders of Marks and Spencer consist of those which are present outside the

organization and have their influence on business operations (Acharya and Ryan, 2016). The

following are the external stakeholders of Marks and Spencer:

Customers : They are the buyers of products and services of company. The company provide

their customers with the financial information in order to retain them in business by providing

true information regarding their performance in industry.

Suppliers: These are the individuals which provide the firm with the raw materials. They use the

financial stamen of company to identify the liquidity position of the firm to pay the obligation to

suppliers.

Government authorities: This uses the financial information to identify the tax liability of the

company so that the company pay the accurate amount of the tax liability.

disclosure of accounting information.

Moreover, the principle of accounting is to provide true and fair view of accounting information.

The financial statements must be consistent in order to have comparison with the past years

financial statement or comparison with other companies. The main purpose of the financial

reporting principles to provide better and clear understanding to the stakeholder of company

regarding the financial performance and position of the firm (Ge and et.al., 2018). Principles are

required for treatment of various transactions and disclosure of the accounting information in

order to reduce the chance missing of information.

3. Key stakeholders of organization and their need of using financial reports

The key stakeholders of the marks and Spencer consist of internal stakeholders and external

stakeholders. Internal stakeholders of the firms are those which are present in the organization

and consist of the following:

Management: The managers are the internal stakeholders of the organization which uses the

financial information to make future decision for the firm in order to enhance the profitability

and performance of the company.

Employees : The employees in the organization uses the financial information to have their job

security by understanding the business profitability to make decision regarding their job.

Owners: the owners or the board of directors uses the financial information to identify their

business profit ability in order to make changes in their policies and their norms to enhance their

business performance.

External stakeholders of Marks and Spencer consist of those which are present outside the

organization and have their influence on business operations (Acharya and Ryan, 2016). The

following are the external stakeholders of Marks and Spencer:

Customers : They are the buyers of products and services of company. The company provide

their customers with the financial information in order to retain them in business by providing

true information regarding their performance in industry.

Suppliers: These are the individuals which provide the firm with the raw materials. They use the

financial stamen of company to identify the liquidity position of the firm to pay the obligation to

suppliers.

Government authorities: This uses the financial information to identify the tax liability of the

company so that the company pay the accurate amount of the tax liability.

Shareholders: They are the people which have invested their money in the money to provide

them funds for their operations (Call and et.al., 2017). They use the financial information to

understand the firm’s capability to provide them higher returns on the funds invested by them.

4. Value of financial reporting for meeting organizational objectives and growth

Financial reporting is important for identifying the profitability of the firm which assist in

improving the future performance and profitability of the company. Financial reporting assist in

making financial planning of the business which creates value for the firm in the future by

enhancing performance of the company (Bushee, Goodman and Sunder, 2018). Financial

reporting assist in identifying the various areas which required close monitoring for improving

the productivity and performance of enterprise. Also, with the help of financial statement firm is

able to understand its profitability and assist in reducing the expenses of enterprise to increase

the net profitability of firm. Furthermore, financial statement assists in identifying the liquidity

position of the firm on the basis of assets and liabilities. Management by using the financial

statement is able to prepare the budgets which assist in gathering information regarding the

future profitability on the basis of past records. Financial statement provide better understanding

about the firm’s operation and on the basis of the statement the firm is able to make changes in

the operations and strategies to increase their profitability (Lang and Stice-Lawrence, 2015).

With the help of financial statement the firms is able increase its value of goodwill which assist

in attracting more customers towards organization. In addition, financial statement of the

company provides assistance to its investors to make decision regarding investment in the

company for performing their business operations.

5. International accounting standard and international financial reporting standard with their

benefits

International accounting standard are the older accounting standards which were replaced

in the years 2001 by international financial reporting standards. This standards were issued by

international accounting standard committee. Whereas IFRS is the international financial

reporting standards which are issued by the international accounting standards board it is new

accounting standards which were adopted in 2001 by replacing the international accounting

standards. IFRS is the set of rules which are use for reporting of financial information. They

provide standards for companies to maintain and report their accounts. This standards are framed

in order to make the financial statements consistent, transparent and comparable around the

world. There are various benefits of international accounting standards which are as follows :

Firms by using the international accounting standards are able to facilitate ethical

compliance of the standards.

They are globally comparable accounting standards which assist in providing flexibility

and transparency.

them funds for their operations (Call and et.al., 2017). They use the financial information to

understand the firm’s capability to provide them higher returns on the funds invested by them.

4. Value of financial reporting for meeting organizational objectives and growth

Financial reporting is important for identifying the profitability of the firm which assist in

improving the future performance and profitability of the company. Financial reporting assist in

making financial planning of the business which creates value for the firm in the future by

enhancing performance of the company (Bushee, Goodman and Sunder, 2018). Financial

reporting assist in identifying the various areas which required close monitoring for improving

the productivity and performance of enterprise. Also, with the help of financial statement firm is

able to understand its profitability and assist in reducing the expenses of enterprise to increase

the net profitability of firm. Furthermore, financial statement assists in identifying the liquidity

position of the firm on the basis of assets and liabilities. Management by using the financial

statement is able to prepare the budgets which assist in gathering information regarding the

future profitability on the basis of past records. Financial statement provide better understanding

about the firm’s operation and on the basis of the statement the firm is able to make changes in

the operations and strategies to increase their profitability (Lang and Stice-Lawrence, 2015).

With the help of financial statement the firms is able increase its value of goodwill which assist

in attracting more customers towards organization. In addition, financial statement of the

company provides assistance to its investors to make decision regarding investment in the

company for performing their business operations.

5. International accounting standard and international financial reporting standard with their

benefits

International accounting standard are the older accounting standards which were replaced

in the years 2001 by international financial reporting standards. This standards were issued by

international accounting standard committee. Whereas IFRS is the international financial

reporting standards which are issued by the international accounting standards board it is new

accounting standards which were adopted in 2001 by replacing the international accounting

standards. IFRS is the set of rules which are use for reporting of financial information. They

provide standards for companies to maintain and report their accounts. This standards are framed

in order to make the financial statements consistent, transparent and comparable around the

world. There are various benefits of international accounting standards which are as follows :

Firms by using the international accounting standards are able to facilitate ethical

compliance of the standards.

They are globally comparable accounting standards which assist in providing flexibility

and transparency.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

They provide better understanding to the investors and other market participants to make

informed decisions.

It also assist in reducing reporting and regulatory cost.

International financial reporting standards benefits :

It assists in increasing foreign capital flows to country by encouraging the international

investors to invest.

It improves the financial controls by standardizing the process of financial reporting.

IFRS assist in improving the day to day operations of the firms.

It reduces the cost of capital.

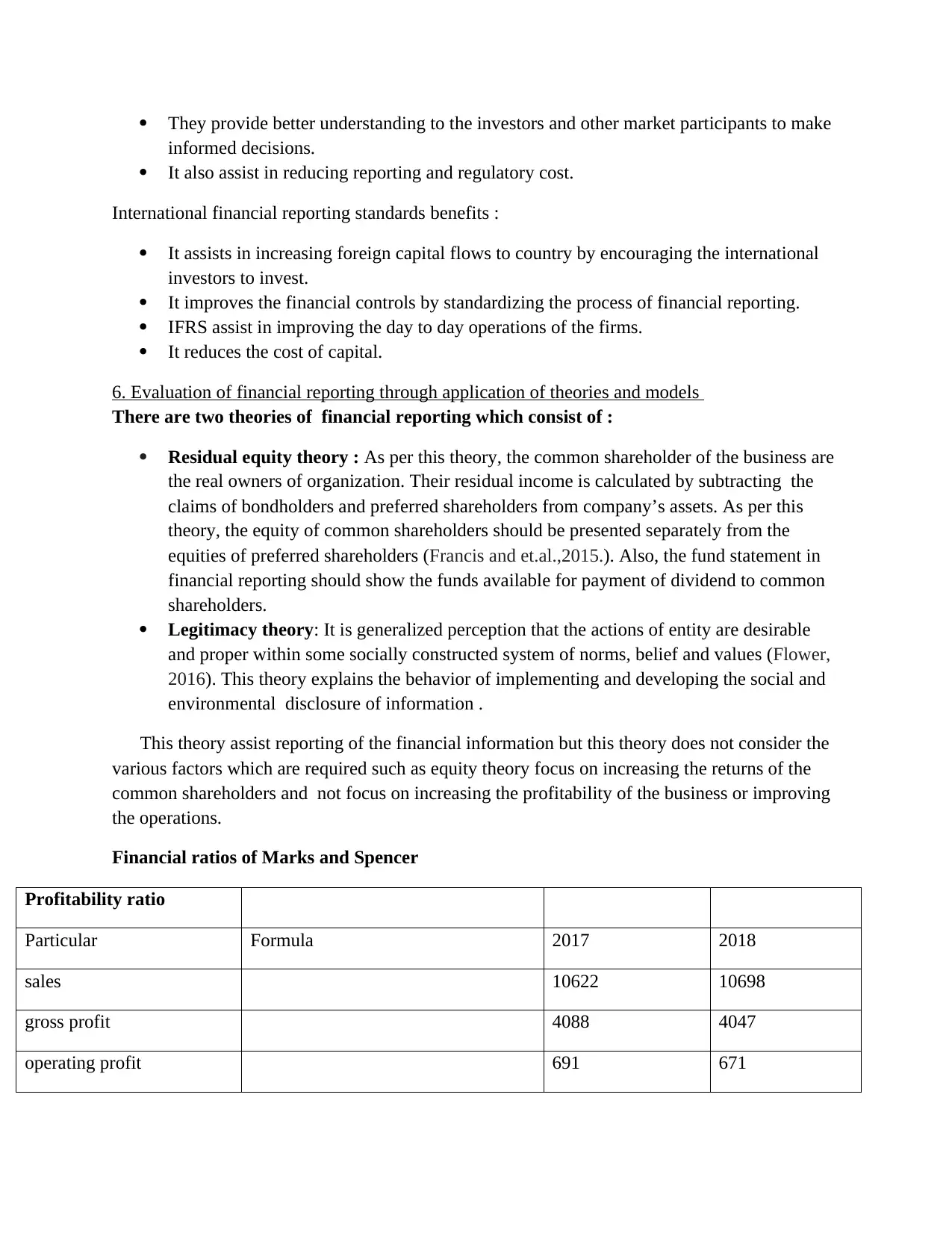

6. Evaluation of financial reporting through application of theories and models

There are two theories of financial reporting which consist of :

Residual equity theory : As per this theory, the common shareholder of the business are

the real owners of organization. Their residual income is calculated by subtracting the

claims of bondholders and preferred shareholders from company’s assets. As per this

theory, the equity of common shareholders should be presented separately from the

equities of preferred shareholders (Francis and et.al.,2015.). Also, the fund statement in

financial reporting should show the funds available for payment of dividend to common

shareholders.

Legitimacy theory: It is generalized perception that the actions of entity are desirable

and proper within some socially constructed system of norms, belief and values (Flower,

2016). This theory explains the behavior of implementing and developing the social and

environmental disclosure of information .

This theory assist reporting of the financial information but this theory does not consider the

various factors which are required such as equity theory focus on increasing the returns of the

common shareholders and not focus on increasing the profitability of the business or improving

the operations.

Financial ratios of Marks and Spencer

Profitability ratio

Particular Formula 2017 2018

sales 10622 10698

gross profit 4088 4047

operating profit 691 671

informed decisions.

It also assist in reducing reporting and regulatory cost.

International financial reporting standards benefits :

It assists in increasing foreign capital flows to country by encouraging the international

investors to invest.

It improves the financial controls by standardizing the process of financial reporting.

IFRS assist in improving the day to day operations of the firms.

It reduces the cost of capital.

6. Evaluation of financial reporting through application of theories and models

There are two theories of financial reporting which consist of :

Residual equity theory : As per this theory, the common shareholder of the business are

the real owners of organization. Their residual income is calculated by subtracting the

claims of bondholders and preferred shareholders from company’s assets. As per this

theory, the equity of common shareholders should be presented separately from the

equities of preferred shareholders (Francis and et.al.,2015.). Also, the fund statement in

financial reporting should show the funds available for payment of dividend to common

shareholders.

Legitimacy theory: It is generalized perception that the actions of entity are desirable

and proper within some socially constructed system of norms, belief and values (Flower,

2016). This theory explains the behavior of implementing and developing the social and

environmental disclosure of information .

This theory assist reporting of the financial information but this theory does not consider the

various factors which are required such as equity theory focus on increasing the returns of the

common shareholders and not focus on increasing the profitability of the business or improving

the operations.

Financial ratios of Marks and Spencer

Profitability ratio

Particular Formula 2017 2018

sales 10622 10698

gross profit 4088 4047

operating profit 691 671

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

gross profit ratio gross pofit / sales 38.5 37.8

operating profit ratio operating profit/sales 6.5 6.3

From the above ratio it can be interpreted about the profitability of marks and Spencer it

can said that the gross profitability of the company is reduced in 2018 which is equal to 37.8

which was 38.5 in 2017. Also, there net profitability of the firm is reduces in the years which

shows the overall profitability of the firm is less as compared to 2017.

Liquidity ratio 2017 2018

current assets 1723 1318

current liabilities 2368 1826

stock 759 781

current ratio current assets/ current liabilities 0.73 0.72

quick ratio currentassets- stock/ current liabilities 0.41 0.29

From the above calculation it can be interpreted about liquidity ratio which provide

understanding about the ability of the firm to pay out their debts. It can be interpreted that the

current ratio shows that company is not able to pay off their current liabilities with the current

assets . so , it is recommended to the firm to increase their current assets.

Solvecny ratio 2017 2018

total liabilitiy 1663 1623

operating profit ratio operating profit/sales 6.5 6.3

From the above ratio it can be interpreted about the profitability of marks and Spencer it

can said that the gross profitability of the company is reduced in 2018 which is equal to 37.8

which was 38.5 in 2017. Also, there net profitability of the firm is reduces in the years which

shows the overall profitability of the firm is less as compared to 2017.

Liquidity ratio 2017 2018

current assets 1723 1318

current liabilities 2368 1826

stock 759 781

current ratio current assets/ current liabilities 0.73 0.72

quick ratio currentassets- stock/ current liabilities 0.41 0.29

From the above calculation it can be interpreted about liquidity ratio which provide

understanding about the ability of the firm to pay out their debts. It can be interpreted that the

current ratio shows that company is not able to pay off their current liabilities with the current

assets . so , it is recommended to the firm to increase their current assets.

Solvecny ratio 2017 2018

total liabilitiy 1663 1623

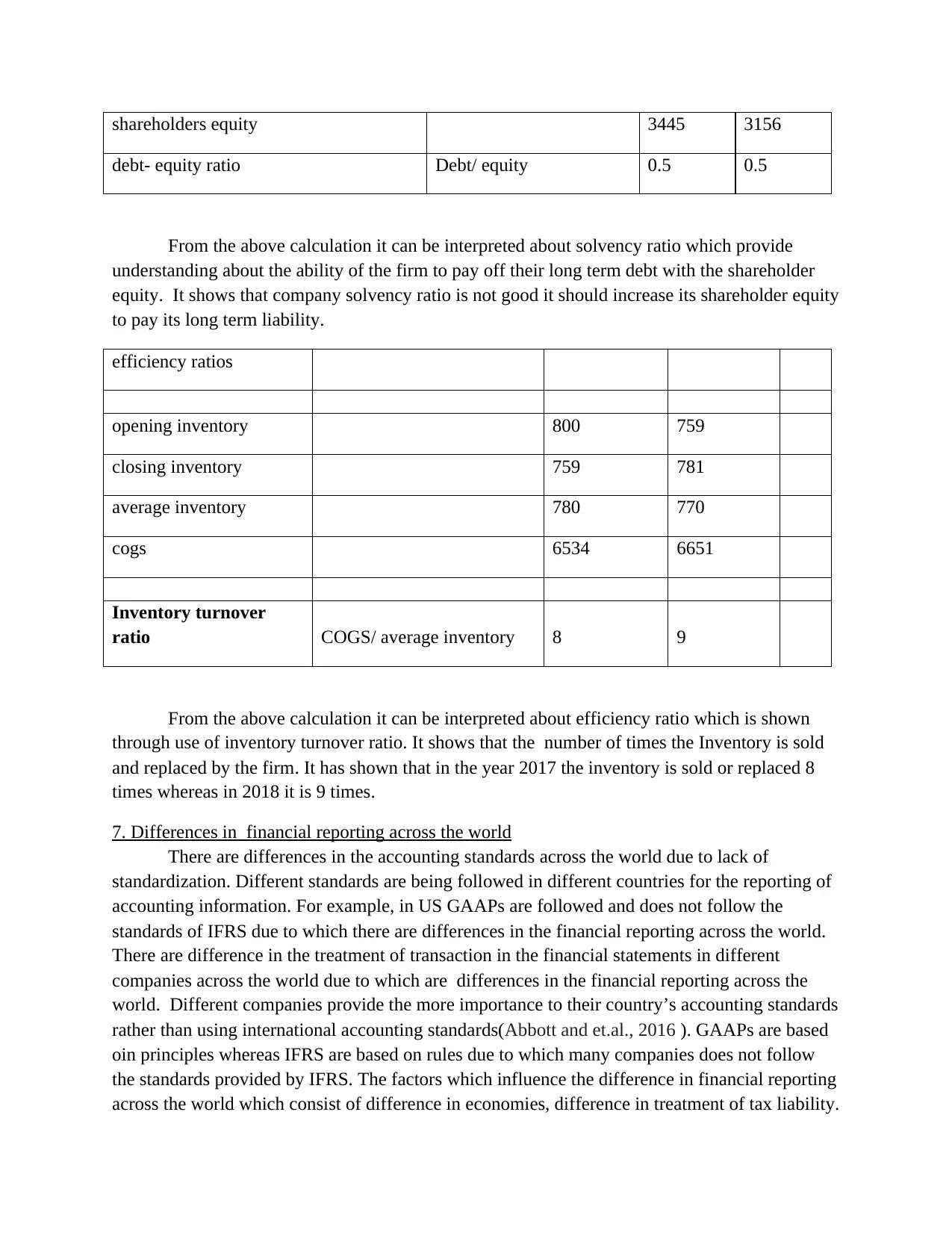

shareholders equity 3445 3156

debt- equity ratio Debt/ equity 0.5 0.5

From the above calculation it can be interpreted about solvency ratio which provide

understanding about the ability of the firm to pay off their long term debt with the shareholder

equity. It shows that company solvency ratio is not good it should increase its shareholder equity

to pay its long term liability.

efficiency ratios

opening inventory 800 759

closing inventory 759 781

average inventory 780 770

cogs 6534 6651

Inventory turnover

ratio COGS/ average inventory 8 9

From the above calculation it can be interpreted about efficiency ratio which is shown

through use of inventory turnover ratio. It shows that the number of times the Inventory is sold

and replaced by the firm. It has shown that in the year 2017 the inventory is sold or replaced 8

times whereas in 2018 it is 9 times.

7. Differences in financial reporting across the world

There are differences in the accounting standards across the world due to lack of

standardization. Different standards are being followed in different countries for the reporting of

accounting information. For example, in US GAAPs are followed and does not follow the

standards of IFRS due to which there are differences in the financial reporting across the world.

There are difference in the treatment of transaction in the financial statements in different

companies across the world due to which are differences in the financial reporting across the

world. Different companies provide the more importance to their country’s accounting standards

rather than using international accounting standards(Abbott and et.al., 2016 ). GAAPs are based

oin principles whereas IFRS are based on rules due to which many companies does not follow

the standards provided by IFRS. The factors which influence the difference in financial reporting

across the world which consist of difference in economies, difference in treatment of tax liability.

debt- equity ratio Debt/ equity 0.5 0.5

From the above calculation it can be interpreted about solvency ratio which provide

understanding about the ability of the firm to pay off their long term debt with the shareholder

equity. It shows that company solvency ratio is not good it should increase its shareholder equity

to pay its long term liability.

efficiency ratios

opening inventory 800 759

closing inventory 759 781

average inventory 780 770

cogs 6534 6651

Inventory turnover

ratio COGS/ average inventory 8 9

From the above calculation it can be interpreted about efficiency ratio which is shown

through use of inventory turnover ratio. It shows that the number of times the Inventory is sold

and replaced by the firm. It has shown that in the year 2017 the inventory is sold or replaced 8

times whereas in 2018 it is 9 times.

7. Differences in financial reporting across the world

There are differences in the accounting standards across the world due to lack of

standardization. Different standards are being followed in different countries for the reporting of

accounting information. For example, in US GAAPs are followed and does not follow the

standards of IFRS due to which there are differences in the financial reporting across the world.

There are difference in the treatment of transaction in the financial statements in different

companies across the world due to which are differences in the financial reporting across the

world. Different companies provide the more importance to their country’s accounting standards

rather than using international accounting standards(Abbott and et.al., 2016 ). GAAPs are based

oin principles whereas IFRS are based on rules due to which many companies does not follow

the standards provided by IFRS. The factors which influence the difference in financial reporting

across the world which consist of difference in economies, difference in treatment of tax liability.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

8. Degree of compliance with IFRS across the world

It refers to the compliance level of the companies with the IFRS standards across the world. Here

are different companies following different standards as per their consistency and simplicity.

IFRS standards are not complied by many organization due to various factors such as

profitability and other factors. Moreover, the compliance level of the firms with IFRS depend on

the benefits of IFRS to the companies with that of the standards adopted by them (Davidson,

Dey and Smith, 2015). Also, companies does not company with IFRS because of cost of

implementing the IFRS standards and changes in the treatment of operations in financial

reporting which reduces the chances of compliance with IFRS.

CONCLUSION

From the above study it has been concluded about financial reporting which is used to

report the financial information for making various decisions making. This assignment has

provided understanding about concept and purpose of financial reporting which is to provide

useful financial information to stakeholders for various decision making. Also, it has considered

the discussion on main stakeholders of company which consists of internal and external

stakeholders. Moreover, it has provided information about IFRS and IAS with they benefits.

It refers to the compliance level of the companies with the IFRS standards across the world. Here

are different companies following different standards as per their consistency and simplicity.

IFRS standards are not complied by many organization due to various factors such as

profitability and other factors. Moreover, the compliance level of the firms with IFRS depend on

the benefits of IFRS to the companies with that of the standards adopted by them (Davidson,

Dey and Smith, 2015). Also, companies does not company with IFRS because of cost of

implementing the IFRS standards and changes in the treatment of operations in financial

reporting which reduces the chances of compliance with IFRS.

CONCLUSION

From the above study it has been concluded about financial reporting which is used to

report the financial information for making various decisions making. This assignment has

provided understanding about concept and purpose of financial reporting which is to provide

useful financial information to stakeholders for various decision making. Also, it has considered

the discussion on main stakeholders of company which consists of internal and external

stakeholders. Moreover, it has provided information about IFRS and IAS with they benefits.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and journals

Leuz, C. and Wysocki, P. D., 2016. The economics of disclosure and financial reporting

regulation: Evidence and suggestions for future research. Journal of Accounting Research. 54(2).

pp.525-622.

Williams, E. E. and Dobelman, J. A., 2017. Financial statement analysis. World Scientific Book

Chapters. pp.109-169.

Ge, W. and et.al., 2018. When does internal control over financial reporting curb resource

extraction? Evidence from China. Evidence from China (March 30, 2018).

Acharya, V. V. and Ryan, S. G., 2016. Banks’ financial reporting and financial system

stability. Journal of Accounting Research. 54(2). pp.277-340.

Bushee, B. J., Goodman, T. H. and Sunder, S. V., 2018. Financial Reporting Quality, Investment

Horizon, and Institutional Investor Trading Strategies. The Accounting Review.

Francis, B. and et.al.,2015. Gender differences in financial reporting decision making: Evidence

from accounting conservatism. Contemporary Accounting Research. 32(3). pp.1285-1318.

Abbott, L.J. and et.al., 2016. Internal audit quality and financial reporting quality: The joint

importance of independence and competence. Journal of Accounting Research. 54(1). pp.3-40.

Davidson, R., Dey, A. and Smith, A., 2015. Executives'“off-the-job” behavior, corporate culture,

and financial reporting risk.Journal of Financial Economics, 117(1). pp.5-28.

Flower, J., 2016. European financial reporting: adapting to a changing world. Springer.

Lang, M. and Stice-Lawrence, L., 2015. Textual analysis and international financial reporting:

Large sample evidence.Journal of Accounting and Economics. 60(2-3). pp.110-135.

Call, A.C. and et.al., 2017. Employee quality and financial reporting outcomes.Journal of

Accounting and Economics. 64(1). pp.123-149.

Books and journals

Leuz, C. and Wysocki, P. D., 2016. The economics of disclosure and financial reporting

regulation: Evidence and suggestions for future research. Journal of Accounting Research. 54(2).

pp.525-622.

Williams, E. E. and Dobelman, J. A., 2017. Financial statement analysis. World Scientific Book

Chapters. pp.109-169.

Ge, W. and et.al., 2018. When does internal control over financial reporting curb resource

extraction? Evidence from China. Evidence from China (March 30, 2018).

Acharya, V. V. and Ryan, S. G., 2016. Banks’ financial reporting and financial system

stability. Journal of Accounting Research. 54(2). pp.277-340.

Bushee, B. J., Goodman, T. H. and Sunder, S. V., 2018. Financial Reporting Quality, Investment

Horizon, and Institutional Investor Trading Strategies. The Accounting Review.

Francis, B. and et.al.,2015. Gender differences in financial reporting decision making: Evidence

from accounting conservatism. Contemporary Accounting Research. 32(3). pp.1285-1318.

Abbott, L.J. and et.al., 2016. Internal audit quality and financial reporting quality: The joint

importance of independence and competence. Journal of Accounting Research. 54(1). pp.3-40.

Davidson, R., Dey, A. and Smith, A., 2015. Executives'“off-the-job” behavior, corporate culture,

and financial reporting risk.Journal of Financial Economics, 117(1). pp.5-28.

Flower, J., 2016. European financial reporting: adapting to a changing world. Springer.

Lang, M. and Stice-Lawrence, L., 2015. Textual analysis and international financial reporting:

Large sample evidence.Journal of Accounting and Economics. 60(2-3). pp.110-135.

Call, A.C. and et.al., 2017. Employee quality and financial reporting outcomes.Journal of

Accounting and Economics. 64(1). pp.123-149.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.