Marks and Spencer: Current Issues in Company Reporting

VerifiedAdded on 2020/09/17

|14

|3708

|32

Report

AI Summary

This report delves into the current issues impacting company reporting techniques, with a specific focus on Marks and Spencer. It begins by analyzing the company's financial position, considering the influence of UK legal and regulatory frameworks. The report then explores the requirements of UK IFRS and GAAP reporting standards, comparing and contrasting their applications. It investigates the IFRS and GAAP standards suitable for international organizational reporting harmonization. Section 2 evaluates non-financial reporting indicators, such as balance scorecards and consumer reviews, to assess organizational performance beyond financial metrics. The final section examines forecasting techniques relevant to Marks and Spencer. The report highlights the importance of these techniques for informed decision-making, profitability, and stakeholder value, and provides a comprehensive overview of financial reporting practices, international accounting standards, and non-financial performance indicators.

Current Issues In

Company Reporting

Company Reporting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

SECTION 1......................................................................................................................................1

1 Analysing the financial position of Marks and Spencer with considering UK legal and

regulatory influences in reporting techniques.............................................................................1

2 Determining the requirements of UK IFRS GAAP reporting in referenced with Marks and

Spencer's data..............................................................................................................................2

3 Ascertaining the IFRS and GAAP standards which suits the international harmonisation of

organisational reporting..............................................................................................................4

SECTION 2......................................................................................................................................5

4 Evaluation of the non-financial reporting indicators for Marks and Spencer..........................5

SECTION 3......................................................................................................................................6

5 Ascertaining the forecasting techniques for Marks and Spencer.............................................6

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

SECTION 1......................................................................................................................................1

1 Analysing the financial position of Marks and Spencer with considering UK legal and

regulatory influences in reporting techniques.............................................................................1

2 Determining the requirements of UK IFRS GAAP reporting in referenced with Marks and

Spencer's data..............................................................................................................................2

3 Ascertaining the IFRS and GAAP standards which suits the international harmonisation of

organisational reporting..............................................................................................................4

SECTION 2......................................................................................................................................5

4 Evaluation of the non-financial reporting indicators for Marks and Spencer..........................5

SECTION 3......................................................................................................................................6

5 Ascertaining the forecasting techniques for Marks and Spencer.............................................6

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................11

INTRODUCTION

To ascertain the current issues in the company's reporting techniques which are affecting

the operational aspects as well as market value. In the following study there will be analysis and

theoretical observation over the universal financial reporting techniques such as GAAP, IFRS

and FRS techniques. The reporting concepts and principles will be implied over Marks and

Spencer to determine their responsibility in presenting the effective information to the users of

such data set. Te study will present favourable and beneficial terms which are need to be

implicated by the organisation as to have increment in the performance as well as rise in the

share value of the firm. There will be discussion over qualitative and quantitative techniques

with their advantages and disadvantages as to ascertain their importance in future growth.

SECTION 1

1 Analysing the financial position of Marks and Spencer with considering UK legal and

regulatory influences in reporting techniques

To demonstrate the financial position of Marks and Spencer in accordance with the

various legal and regulatory factors which determines in the reporting methods of this entity.

Therefore, this organisation is one of the leading brand in UK which provides clothes, foods,

products etc. Thus, in accordance with the same there will be requirement of well managed

financial data set with consideration of all the legal method of preparing it. In relation with the

UK's legal environment where the focus of government in having appropriate disclosure of all

the financial accounts from every organisation (Bonsall IV and et.al., 2017). There are various

organisation which in turn facilitating the appropriate guidance and funnelling to the accounting

professionals in context with preparing and presenting the financial reports. The aim of financial

reporting council (FRC) is to funnel and guide the organisations to properly use reporting

techniques as well as make the best quality of corporate governance.

Financial reporting council (FRC)

This is the independent regulatory framework of Ireland and UK which function with the

motive of facilitating the best corporate governance in each organisation. It guides the managers,

accounting professionals as well as auditors to make and present the adequate reports in the

market. Thus, on which they would become to gather the large numbers of shareholders

(Guidance on the Strategic Report, 2014). In addition, the influence of three committees such

1

To ascertain the current issues in the company's reporting techniques which are affecting

the operational aspects as well as market value. In the following study there will be analysis and

theoretical observation over the universal financial reporting techniques such as GAAP, IFRS

and FRS techniques. The reporting concepts and principles will be implied over Marks and

Spencer to determine their responsibility in presenting the effective information to the users of

such data set. Te study will present favourable and beneficial terms which are need to be

implicated by the organisation as to have increment in the performance as well as rise in the

share value of the firm. There will be discussion over qualitative and quantitative techniques

with their advantages and disadvantages as to ascertain their importance in future growth.

SECTION 1

1 Analysing the financial position of Marks and Spencer with considering UK legal and

regulatory influences in reporting techniques

To demonstrate the financial position of Marks and Spencer in accordance with the

various legal and regulatory factors which determines in the reporting methods of this entity.

Therefore, this organisation is one of the leading brand in UK which provides clothes, foods,

products etc. Thus, in accordance with the same there will be requirement of well managed

financial data set with consideration of all the legal method of preparing it. In relation with the

UK's legal environment where the focus of government in having appropriate disclosure of all

the financial accounts from every organisation (Bonsall IV and et.al., 2017). There are various

organisation which in turn facilitating the appropriate guidance and funnelling to the accounting

professionals in context with preparing and presenting the financial reports. The aim of financial

reporting council (FRC) is to funnel and guide the organisations to properly use reporting

techniques as well as make the best quality of corporate governance.

Financial reporting council (FRC)

This is the independent regulatory framework of Ireland and UK which function with the

motive of facilitating the best corporate governance in each organisation. It guides the managers,

accounting professionals as well as auditors to make and present the adequate reports in the

market. Thus, on which they would become to gather the large numbers of shareholders

(Guidance on the Strategic Report, 2014). In addition, the influence of three committees such

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

add executive, conduct and codes & standard committees there has implementation of various

codes and ethics as well as guidance to perform the better funnelling among stakeholders.

Changes in the financial reporting in last few years:

There has been changes in the operations of the making and presenting the reports among

the stakeholders of Marks and Spencer. Therefore, IAS/IFRS has the main provocation in

accordance with having the quality reports made from each business unit. Therefore, such

information will be helpful to the market and stakeholders associated with the company. They

will easily analyse and demonstrate the growth of business in making profitable payments of

dividends (Johnston and Petacchi, 2017). On the European countries are provoking the quality

financial reporting technique must be implied over all the countries as a general rule. Therefore,

there has been various debates and discussion over the preparation of such reporting techniques

as well as setting the rules and regulations.

2 Determining the requirements of UK IFRS GAAP reporting in referenced with Marks and

Spencer's data

There are various reporting technique which will be used universally as to have

appropriate reporting of the financial condition of an organisation. Therefore, the presentation of

the financial reports of the organisation is on the basis of providing information to all the users as

well as have stable capital structure. Marks and Spencer will have sufficient amount of funds for

the operation as well as they can become able to make utilisation of the resources in appropriate

manner (Cohen, Krishnamoorthy and Wright, 2017). There will be increment in the numbers of

shareholders as the market value of the entity will be reflect in the internal trade market which in

turn will be attractive to the shareholder's.

International Financial Reporting Standards:

This is the reporting standard which in turn helpful for providing the fruitful guidance to

the accounting professionals in terms of following the universally accepted method of presenting

reports. Thus, the standard which will be helpful for each individual in understanding the

financial criteria of the business (Abdullah, Naser and Al-Duwaila, 2017). It is universally be

proven and accepted that the revenue must be listed in the income statements, assets and

liabilities will be in balance sheet etc.

2

codes and ethics as well as guidance to perform the better funnelling among stakeholders.

Changes in the financial reporting in last few years:

There has been changes in the operations of the making and presenting the reports among

the stakeholders of Marks and Spencer. Therefore, IAS/IFRS has the main provocation in

accordance with having the quality reports made from each business unit. Therefore, such

information will be helpful to the market and stakeholders associated with the company. They

will easily analyse and demonstrate the growth of business in making profitable payments of

dividends (Johnston and Petacchi, 2017). On the European countries are provoking the quality

financial reporting technique must be implied over all the countries as a general rule. Therefore,

there has been various debates and discussion over the preparation of such reporting techniques

as well as setting the rules and regulations.

2 Determining the requirements of UK IFRS GAAP reporting in referenced with Marks and

Spencer's data

There are various reporting technique which will be used universally as to have

appropriate reporting of the financial condition of an organisation. Therefore, the presentation of

the financial reports of the organisation is on the basis of providing information to all the users as

well as have stable capital structure. Marks and Spencer will have sufficient amount of funds for

the operation as well as they can become able to make utilisation of the resources in appropriate

manner (Cohen, Krishnamoorthy and Wright, 2017). There will be increment in the numbers of

shareholders as the market value of the entity will be reflect in the internal trade market which in

turn will be attractive to the shareholder's.

International Financial Reporting Standards:

This is the reporting standard which in turn helpful for providing the fruitful guidance to

the accounting professionals in terms of following the universally accepted method of presenting

reports. Thus, the standard which will be helpful for each individual in understanding the

financial criteria of the business (Abdullah, Naser and Al-Duwaila, 2017). It is universally be

proven and accepted that the revenue must be listed in the income statements, assets and

liabilities will be in balance sheet etc.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

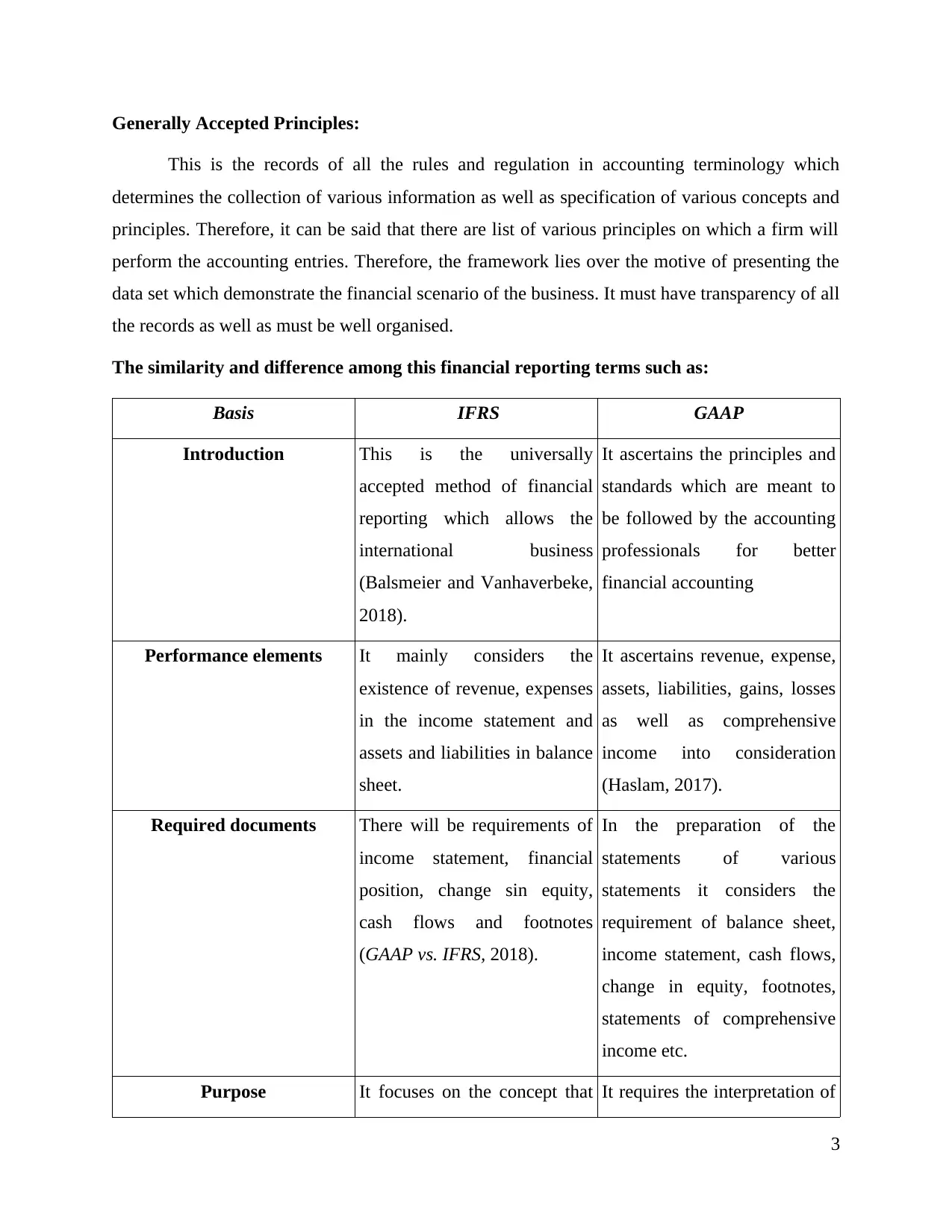

Generally Accepted Principles:

This is the records of all the rules and regulation in accounting terminology which

determines the collection of various information as well as specification of various concepts and

principles. Therefore, it can be said that there are list of various principles on which a firm will

perform the accounting entries. Therefore, the framework lies over the motive of presenting the

data set which demonstrate the financial scenario of the business. It must have transparency of all

the records as well as must be well organised.

The similarity and difference among this financial reporting terms such as:

Basis IFRS GAAP

Introduction This is the universally

accepted method of financial

reporting which allows the

international business

(Balsmeier and Vanhaverbeke,

2018).

It ascertains the principles and

standards which are meant to

be followed by the accounting

professionals for better

financial accounting

Performance elements It mainly considers the

existence of revenue, expenses

in the income statement and

assets and liabilities in balance

sheet.

It ascertains revenue, expense,

assets, liabilities, gains, losses

as well as comprehensive

income into consideration

(Haslam, 2017).

Required documents There will be requirements of

income statement, financial

position, change sin equity,

cash flows and footnotes

(GAAP vs. IFRS, 2018).

In the preparation of the

statements of various

statements it considers the

requirement of balance sheet,

income statement, cash flows,

change in equity, footnotes,

statements of comprehensive

income etc.

Purpose It focuses on the concept that It requires the interpretation of

3

This is the records of all the rules and regulation in accounting terminology which

determines the collection of various information as well as specification of various concepts and

principles. Therefore, it can be said that there are list of various principles on which a firm will

perform the accounting entries. Therefore, the framework lies over the motive of presenting the

data set which demonstrate the financial scenario of the business. It must have transparency of all

the records as well as must be well organised.

The similarity and difference among this financial reporting terms such as:

Basis IFRS GAAP

Introduction This is the universally

accepted method of financial

reporting which allows the

international business

(Balsmeier and Vanhaverbeke,

2018).

It ascertains the principles and

standards which are meant to

be followed by the accounting

professionals for better

financial accounting

Performance elements It mainly considers the

existence of revenue, expenses

in the income statement and

assets and liabilities in balance

sheet.

It ascertains revenue, expense,

assets, liabilities, gains, losses

as well as comprehensive

income into consideration

(Haslam, 2017).

Required documents There will be requirements of

income statement, financial

position, change sin equity,

cash flows and footnotes

(GAAP vs. IFRS, 2018).

In the preparation of the

statements of various

statements it considers the

requirement of balance sheet,

income statement, cash flows,

change in equity, footnotes,

statements of comprehensive

income etc.

Purpose It focuses on the concept that It requires the interpretation of

3

each and every issues in the

financial data set must be

resolved in accordance with

the IFRS framework and

standards.

the issues with proper

interpretation of such factor.

There will be no provision

which required to be

considered by the managers.

Objectives It specifies the terms that all

the information will be used

and understand by the user on

the wide segmentation. The

same set of rule will be

applicable to both business and

non- business enterprises.

It also provides the

information to the stakeholder

at wide segmentation which

has the separate objectives of

each business (Bonsall IV and

et.al., 2017).

3 Ascertaining the IFRS and GAAP standards which suits the international harmonisation of

organisational reporting

In relation with harmonising the GAAP and IFRS standards in international financial

market. The argument lies in between the international accounting harmonization which will be

helpful in accepting the countries' convergence in monumental tasks. There has been various

generic barriers in the same concept. There are still some places where the barriers like language,

educational level as well as economical level (Johnston and Petacchi, 2017). Therefore, the main

motive of IFRS is to present the accurate standards for all categories of businesses. In order to

harmonize the world with these two principles and standards there is need to have appropriate

promotion of such methods of preparing statements.

Conclusion:

In accordance with the concept of GAAP and IFRS techniques which will result in

providing the accurate framework of recording the financial data in a summarized from.

Therefore, the standard presented by IFRS are the main funnelling module on which a firm can

easily have sufficient amount of funds from the national as well as international investors

(Cohen, Krishnamoorthy and Wright, 2017). On the other side, GAAP provides the guidelines

for accounting concepts and terms which are to be used by the firm on daily basis. Therefore, the

4

financial data set must be

resolved in accordance with

the IFRS framework and

standards.

the issues with proper

interpretation of such factor.

There will be no provision

which required to be

considered by the managers.

Objectives It specifies the terms that all

the information will be used

and understand by the user on

the wide segmentation. The

same set of rule will be

applicable to both business and

non- business enterprises.

It also provides the

information to the stakeholder

at wide segmentation which

has the separate objectives of

each business (Bonsall IV and

et.al., 2017).

3 Ascertaining the IFRS and GAAP standards which suits the international harmonisation of

organisational reporting

In relation with harmonising the GAAP and IFRS standards in international financial

market. The argument lies in between the international accounting harmonization which will be

helpful in accepting the countries' convergence in monumental tasks. There has been various

generic barriers in the same concept. There are still some places where the barriers like language,

educational level as well as economical level (Johnston and Petacchi, 2017). Therefore, the main

motive of IFRS is to present the accurate standards for all categories of businesses. In order to

harmonize the world with these two principles and standards there is need to have appropriate

promotion of such methods of preparing statements.

Conclusion:

In accordance with the concept of GAAP and IFRS techniques which will result in

providing the accurate framework of recording the financial data in a summarized from.

Therefore, the standard presented by IFRS are the main funnelling module on which a firm can

easily have sufficient amount of funds from the national as well as international investors

(Cohen, Krishnamoorthy and Wright, 2017). On the other side, GAAP provides the guidelines

for accounting concepts and terms which are to be used by the firm on daily basis. Therefore, the

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

influence of both the terms in preparing the financial accounts of the business is quite necessary

in terms of decisions making, analysing the profitability, efficiency, liquidity and ability to meet

the debts in a required time.

SECTION 2

4 Evaluation of the non-financial reporting indicators for Marks and Spencer

In relation with the other methods than the financial terms of presenting the

organisational performances. There are various techniques and terms which will be presented by

the professionals in relation with analysing performance of organisation as well as the utilisation

of the resources (Abdullah, Naser and Al-Duwaila, 2017). Thus, the non-financial factors which

will be best of reporting the business reports such as:

Balance scorecard: This is the strategic planning and management system which is

being implicated by various entities as to have adequate analysis over the organisational as well

as employee performance. Marks and Spencer will be helpful in making the appropriate

management of work and workforce by this technique (Balsmeier and Vanhaverbeke, 2018).

There will have effective control over the operations of business activities such as prioritising the

projects, services and products. Similarly, the managers in the organisation at various

departments prepare the scorecard on which they mention small targets and time limits which

provokes the men-force to make efforts in attaining them.

Benchmarking: This is the technique which is also helpful for performance analysis. Iot

ascertain the process of the company in operating under the projected plans. It supports the

selection, planning and completion of the projects. It also demonstrates the total utilisation of the

quality, costs and time over the project which is need to be controlled and overcome by the

professionals as to have appropriate analysis of organisational performance.

Consumer reviews:The feedbacks or reviews from consumers is the right method of

analysing the loopholes in the products and services. It helps in decision making and bringing

innovative changes in the products and services (Haslam, 2017). The designing of the operations

will be helpful in bringing sufficient satisfaction to the consumers.

Industry news: The industry news will be useful in demonstrating the challenges and

competitive needs in the business. Therefore, to retain the shareholders and consumers there is

5

in terms of decisions making, analysing the profitability, efficiency, liquidity and ability to meet

the debts in a required time.

SECTION 2

4 Evaluation of the non-financial reporting indicators for Marks and Spencer

In relation with the other methods than the financial terms of presenting the

organisational performances. There are various techniques and terms which will be presented by

the professionals in relation with analysing performance of organisation as well as the utilisation

of the resources (Abdullah, Naser and Al-Duwaila, 2017). Thus, the non-financial factors which

will be best of reporting the business reports such as:

Balance scorecard: This is the strategic planning and management system which is

being implicated by various entities as to have adequate analysis over the organisational as well

as employee performance. Marks and Spencer will be helpful in making the appropriate

management of work and workforce by this technique (Balsmeier and Vanhaverbeke, 2018).

There will have effective control over the operations of business activities such as prioritising the

projects, services and products. Similarly, the managers in the organisation at various

departments prepare the scorecard on which they mention small targets and time limits which

provokes the men-force to make efforts in attaining them.

Benchmarking: This is the technique which is also helpful for performance analysis. Iot

ascertain the process of the company in operating under the projected plans. It supports the

selection, planning and completion of the projects. It also demonstrates the total utilisation of the

quality, costs and time over the project which is need to be controlled and overcome by the

professionals as to have appropriate analysis of organisational performance.

Consumer reviews:The feedbacks or reviews from consumers is the right method of

analysing the loopholes in the products and services. It helps in decision making and bringing

innovative changes in the products and services (Haslam, 2017). The designing of the operations

will be helpful in bringing sufficient satisfaction to the consumers.

Industry news: The industry news will be useful in demonstrating the challenges and

competitive needs in the business. Therefore, to retain the shareholders and consumers there is

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

need to have dynamic ability in the operations (Bonsall IV and et.al., 2017). There must be

innovative changes In the product line as well as changes in the dividend policies.

CSR: The corporate social responsibility helps in creating the environmental awareness

in the business. Therefore, Marks and Spencer will have profitable market value in the internal

financial market which will be fruitful for creating the unique identity.

Staff turnover: This is the most effective technique which is helpful in making the

adequate analysis over the numbers of employees hired by the organisation as well as numbers of

employees left the organisation. It will be used in examining the turnover reason on which

business demonstrate the accurate reasons behind the job left by the professionals. Marks and

Spencer will be helpful as if they make adequate records of all the information such as improving

the pay slip, reducing the work load, implicating training and development etc.

Public image: This technique helps in determining the brand image in the market. It can

be seen at the platform like social media as well as through indirect approach such as analysing

the sales and provide gathered by the firms (Cohen, Krishnamoorthy and Wright, 2017). To build

a good image in the external environment which will have positive impacts over the business

growth.

Staff development: The performance of Marks and Spencer or any entity lies over the

efforts made by their workforce. Thus, in relation with having appropriate operational gains there

is need to have proper training and educational session which in turn helps in guiding the

employees to perform accurately (Johnston and Petacchi, 2017).

SECTION 3

5 Ascertaining the forecasting techniques for Marks and Spencer

Qualitative techniques:

Market research

This is effective technique which help Marks and Spencer to assess consumer preferences

and needs in the best possible way. Moreover, target markets can be easily analysed and

customer-oriented goods may be supplied quite effectually.

Advantages:

6

innovative changes In the product line as well as changes in the dividend policies.

CSR: The corporate social responsibility helps in creating the environmental awareness

in the business. Therefore, Marks and Spencer will have profitable market value in the internal

financial market which will be fruitful for creating the unique identity.

Staff turnover: This is the most effective technique which is helpful in making the

adequate analysis over the numbers of employees hired by the organisation as well as numbers of

employees left the organisation. It will be used in examining the turnover reason on which

business demonstrate the accurate reasons behind the job left by the professionals. Marks and

Spencer will be helpful as if they make adequate records of all the information such as improving

the pay slip, reducing the work load, implicating training and development etc.

Public image: This technique helps in determining the brand image in the market. It can

be seen at the platform like social media as well as through indirect approach such as analysing

the sales and provide gathered by the firms (Cohen, Krishnamoorthy and Wright, 2017). To build

a good image in the external environment which will have positive impacts over the business

growth.

Staff development: The performance of Marks and Spencer or any entity lies over the

efforts made by their workforce. Thus, in relation with having appropriate operational gains there

is need to have proper training and educational session which in turn helps in guiding the

employees to perform accurately (Johnston and Petacchi, 2017).

SECTION 3

5 Ascertaining the forecasting techniques for Marks and Spencer

Qualitative techniques:

Market research

This is effective technique which help Marks and Spencer to assess consumer preferences

and needs in the best possible way. Moreover, target markets can be easily analysed and

customer-oriented goods may be supplied quite effectually.

Advantages:

6

1. Product planning can be easily done by marketing research and Marks and Spencer

may sell luxury goods to customers.

2. Advertising programmes can be established with the help of marketing research. Thus,

optimum utilisation of resources may be attained (Chand).

Limitations:

1. It is not suitable as it is based on human behaviour which is ever-changing.

2. This technique is unsuitable for forecasting as there are intervening factors analysed

between market research findings and complexity of market forces.

Delphi method

It is effectual forecasting technique which is derived by structured views of panel of

experts. Appropriate decisions are taken by panel of experts of Marks and Spencer quite

effectively.

Advantages:

1. It is quite useful as more number of experts can easily participate.

2. This method allows assessing and identifying priorities which Marks and Spencer

requires ultimately.

Limitations:

1. Data analysis is a tedious task and more rounds are taken to arrive at decision

(Anderson and et.al, 2018).

2. This is time-consuming process and reporting can be biased as per the preferences of

experts. Reliability is completely lost.

Historical analogy

This is another qualitative forecasting technique which is used to forecast sales of similar

product in the near future as well. This method is quite useful for predicting sales on the basis of

historical data.

Advantages:

7

may sell luxury goods to customers.

2. Advertising programmes can be established with the help of marketing research. Thus,

optimum utilisation of resources may be attained (Chand).

Limitations:

1. It is not suitable as it is based on human behaviour which is ever-changing.

2. This technique is unsuitable for forecasting as there are intervening factors analysed

between market research findings and complexity of market forces.

Delphi method

It is effectual forecasting technique which is derived by structured views of panel of

experts. Appropriate decisions are taken by panel of experts of Marks and Spencer quite

effectively.

Advantages:

1. It is quite useful as more number of experts can easily participate.

2. This method allows assessing and identifying priorities which Marks and Spencer

requires ultimately.

Limitations:

1. Data analysis is a tedious task and more rounds are taken to arrive at decision

(Anderson and et.al, 2018).

2. This is time-consuming process and reporting can be biased as per the preferences of

experts. Reliability is completely lost.

Historical analogy

This is another qualitative forecasting technique which is used to forecast sales of similar

product in the near future as well. This method is quite useful for predicting sales on the basis of

historical data.

Advantages:

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1. It is simple forecasting technique which is easy to interpret results in the best possible

way.

2. It saves time for management as it is aligned with past figures and estimation can be

made with much ease about the future (Finn, Goodfellow and Levine, 2016).

Limitations:

1. Historical analogy is unsuitable as it is based on historical data and facts which may be

subject to change in the future.

2. This forecasting technique is not useful as complete estimation is not made and same

predictions are made for new similar product.

Quantitative techniques

Time serve analysis

Time serve analysis is useful technique based on forecasting business sales and behaviour

in the future. This method is quite effective as various time series charts such as line charts can

be prepared with much ease.

Advantages:

1. Historical data is helpful for firm to forecast sales behaviour quite effectively. Line

charts are useful for reliability purpose.

2. Future growth and trend of Marks and Spencer may be analysed. Thus, trend can be

forecasted easily (Mun, 2017).

Limitations:

1. This method is purely based on statistical tools and there are other attributes which are

relevant but ignored.

2. Single events cannot be identified and its impact is difficult to analyse as well.

Net Present Value (NPV):

NPV is useful forecasting technique which is useful for Marks and Spencer to assess

attractiveness of new project and eventually investment may be made in it. Profitability aspect is

8

way.

2. It saves time for management as it is aligned with past figures and estimation can be

made with much ease about the future (Finn, Goodfellow and Levine, 2016).

Limitations:

1. Historical analogy is unsuitable as it is based on historical data and facts which may be

subject to change in the future.

2. This forecasting technique is not useful as complete estimation is not made and same

predictions are made for new similar product.

Quantitative techniques

Time serve analysis

Time serve analysis is useful technique based on forecasting business sales and behaviour

in the future. This method is quite effective as various time series charts such as line charts can

be prepared with much ease.

Advantages:

1. Historical data is helpful for firm to forecast sales behaviour quite effectively. Line

charts are useful for reliability purpose.

2. Future growth and trend of Marks and Spencer may be analysed. Thus, trend can be

forecasted easily (Mun, 2017).

Limitations:

1. This method is purely based on statistical tools and there are other attributes which are

relevant but ignored.

2. Single events cannot be identified and its impact is difficult to analyse as well.

Net Present Value (NPV):

NPV is useful forecasting technique which is useful for Marks and Spencer to assess

attractiveness of new project and eventually investment may be made in it. Profitability aspect is

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

provided by analysing and differencing net present value of cash inflows and outflows (Kuo,

Tseng and Chen, 2016).

Advantages:

1. It is simple to calculate and cost of capital is considered while evaluating effectiveness

of project.

2. It considers time value of money concept and correct value of profitability is assessed.

Limitations:

1. NPV lays emphasis on profitability aspect but ignores quantum of time that will be

taken by project to yield maximum returns.

2. Cost of capital is complex to arrive at and good investments might be ignored.

Internal Rate of Return (IRR):

IRR is another capital investment technique which is basically discount rate makes NPV

of cash flows from project to zero. Thus, this technique is interrelated to NPV and judges

profitability of potential investment.

Advantages:

1. IRR lays emphasis on time value of money concept. Thus, correct profitability of

project is ascertained (Huan-Niemi and et.al, 2016).

2. It is simple to compute and derive conclusion with much ease.

Limitations:

1. IRR is not useful when there are two mutually exclusive projects of different size and

time duration.

2. The concept of economies of scale is completely ignored which is required to obtain

benefits out of project.

CONCLUSION

Hereby it can be concluded that company requires adopting quantitative and qualitative

techniques of forecasting. This will help it to estimate sales and profit behaviour in the best

possible way. Quantitative methods discussed are important so that Marks and Spencer may

9

Tseng and Chen, 2016).

Advantages:

1. It is simple to calculate and cost of capital is considered while evaluating effectiveness

of project.

2. It considers time value of money concept and correct value of profitability is assessed.

Limitations:

1. NPV lays emphasis on profitability aspect but ignores quantum of time that will be

taken by project to yield maximum returns.

2. Cost of capital is complex to arrive at and good investments might be ignored.

Internal Rate of Return (IRR):

IRR is another capital investment technique which is basically discount rate makes NPV

of cash flows from project to zero. Thus, this technique is interrelated to NPV and judges

profitability of potential investment.

Advantages:

1. IRR lays emphasis on time value of money concept. Thus, correct profitability of

project is ascertained (Huan-Niemi and et.al, 2016).

2. It is simple to compute and derive conclusion with much ease.

Limitations:

1. IRR is not useful when there are two mutually exclusive projects of different size and

time duration.

2. The concept of economies of scale is completely ignored which is required to obtain

benefits out of project.

CONCLUSION

Hereby it can be concluded that company requires adopting quantitative and qualitative

techniques of forecasting. This will help it to estimate sales and profit behaviour in the best

possible way. Quantitative methods discussed are important so that Marks and Spencer may

9

invest in high yielding project which yields maximum returns to it. Thus, overall sales may be

injected and profit can be maximised. On the other hand, qualitative techniques are also

important as past trends may be assessed and future forecast may be made in accordance to

customers' preferences.

10

injected and profit can be maximised. On the other hand, qualitative techniques are also

important as past trends may be assessed and future forecast may be made in accordance to

customers' preferences.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.