Report on Costs, Revenues, and Costing Systems at Marks and Spencer

VerifiedAdded on 2020/10/23

|18

|3394

|70

Report

AI Summary

This report provides a comprehensive analysis of costs and revenues within Marks and Spencer (M&S), a major British retailer. It begins by exploring the nature of costing systems, their role, and their significance within the organization, including internal reporting and different costing methods like historical, absorption, direct, and marginal costing. The report then evaluates cost information, including recording, analysis, and the different stages of inventory valuation using FIFO method. Furthermore, it examines cost apportionment, overhead costs, and calculation methods. The report also delves into budget deviations, variance analysis, and the presentation of information for budget holders. Finally, it assesses the application of costing systems in decision-making, including estimating future income and the impact of changing activity levels on unit costs, offering valuable insights into the financial operations of M&S.

COSTS AND REVENUES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

1. The nature of costing system and its role within Marks and Spencer.........................................1

1.1 Internal reporting and its purpose.....................................................................................1

1.2 Different costing systems and their relationships ............................................................1

1.3 Identification of responsibility, profit, investment and cost centres................................2

1.4 Classifications of cost and their uses................................................................................2

1.5 Marginal and absorption costing differences ..................................................................3

2. Cost information examination and recording .............................................................................3

2.1 Recording information......................................................................................................3

2.2 Analysis the cost information...........................................................................................4

2.3 Different stages in inventory ...........................................................................................4

2.4 Value inventory method...................................................................................................5

2.5 Cost behaviours................................................................................................................7

2.6 Costing systems and cost information..............................................................................8

3. Apportion cost..............................................................................................................................8

3.1 Describing overhead cost of production and service cost centre.....................................8

3.2 Calculating overhead absorption rates using methods....................................................8

3.3 Adjustments for overhead cost.......................................................................................10

3.4 Reviewing method of allocation, apportionments and absorption.................................10

3.5 Communicate when the queries in overhead..................................................................10

4. Deviation from the budget.........................................................................................................10

4.1 budget cost and actual cost and variances......................................................................11

4.2 analyse the variance .......................................................................................................11

4.3 Presenting the information for budget holder.................................................................11

4.4 management report.........................................................................................................11

5. Costing systems and decision-making.......................................................................................12

INTRODUCTION...........................................................................................................................1

1. The nature of costing system and its role within Marks and Spencer.........................................1

1.1 Internal reporting and its purpose.....................................................................................1

1.2 Different costing systems and their relationships ............................................................1

1.3 Identification of responsibility, profit, investment and cost centres................................2

1.4 Classifications of cost and their uses................................................................................2

1.5 Marginal and absorption costing differences ..................................................................3

2. Cost information examination and recording .............................................................................3

2.1 Recording information......................................................................................................3

2.2 Analysis the cost information...........................................................................................4

2.3 Different stages in inventory ...........................................................................................4

2.4 Value inventory method...................................................................................................5

2.5 Cost behaviours................................................................................................................7

2.6 Costing systems and cost information..............................................................................8

3. Apportion cost..............................................................................................................................8

3.1 Describing overhead cost of production and service cost centre.....................................8

3.2 Calculating overhead absorption rates using methods....................................................8

3.3 Adjustments for overhead cost.......................................................................................10

3.4 Reviewing method of allocation, apportionments and absorption.................................10

3.5 Communicate when the queries in overhead..................................................................10

4. Deviation from the budget.........................................................................................................10

4.1 budget cost and actual cost and variances......................................................................11

4.2 analyse the variance .......................................................................................................11

4.3 Presenting the information for budget holder.................................................................11

4.4 management report.........................................................................................................11

5. Costing systems and decision-making.......................................................................................12

5.1 Preparing the estimates of future income.......................................................................12

5.2 The impact of changing activity levels on unit costs.....................................................13

5.3 Calculate the effect of changing activity level...............................................................13

5.4 Impacts on short-term and long-term decision making..................................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

5.2 The impact of changing activity levels on unit costs.....................................................13

5.3 Calculate the effect of changing activity level...............................................................13

5.4 Impacts on short-term and long-term decision making..................................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

The below mentioned report identifies the significance of Costs and Revenues in context

of Marks and Spencer. Marks and Spencer is a major British multinational retailer specialising in

selling of luxury food products, home products and clothes. The report develops an

understanding of the nature of costing within the context of the chosen organisation. Also, it

understands their role and what significance they play within the organisational environment of

Marks and Spencer. The report briefly analyses and evaluates cost information. In the report, the

costs of apportion are explored as well. The proper usage of information gathered from costing

system in order provide an assistance in decision making for the organisation is briefly

evaluated. These evaluations will help in the determination the importance of revenue and cost

within Marks and Spencer.

1. The nature of costing system and its role within Marks and Spencer

1.1 Internal reporting and its purpose

Marks and Spencer is required to regularly compile the organisation's financial and

operational information in order to improve the value and performance of the organisation. The

process of internal reporting allows Marks and Spencer to compile this information and

distribute it to its stakeholders in order to make the necessary changes and improve the

organisation's performance (Capocchi, 2019). The report includes useful information such as

sales data, failure rates, expense trends etc. and are not meant to shared by the organisation to

any 3rd party.

Along with it, the generation of the accurate information helps Marks and Spencer to

make necessary assumptions and improve its performance. Accurate information will also help

the organisation to reach its required goals and objectives properly.

1.2 Different costing systems and their relationships

Historical Costing: The process of historical costing allows the costs to be established

after they are incurred. Marks and Spencer uses this costing system to analyse the actual incurred

costs.

1

The below mentioned report identifies the significance of Costs and Revenues in context

of Marks and Spencer. Marks and Spencer is a major British multinational retailer specialising in

selling of luxury food products, home products and clothes. The report develops an

understanding of the nature of costing within the context of the chosen organisation. Also, it

understands their role and what significance they play within the organisational environment of

Marks and Spencer. The report briefly analyses and evaluates cost information. In the report, the

costs of apportion are explored as well. The proper usage of information gathered from costing

system in order provide an assistance in decision making for the organisation is briefly

evaluated. These evaluations will help in the determination the importance of revenue and cost

within Marks and Spencer.

1. The nature of costing system and its role within Marks and Spencer

1.1 Internal reporting and its purpose

Marks and Spencer is required to regularly compile the organisation's financial and

operational information in order to improve the value and performance of the organisation. The

process of internal reporting allows Marks and Spencer to compile this information and

distribute it to its stakeholders in order to make the necessary changes and improve the

organisation's performance (Capocchi, 2019). The report includes useful information such as

sales data, failure rates, expense trends etc. and are not meant to shared by the organisation to

any 3rd party.

Along with it, the generation of the accurate information helps Marks and Spencer to

make necessary assumptions and improve its performance. Accurate information will also help

the organisation to reach its required goals and objectives properly.

1.2 Different costing systems and their relationships

Historical Costing: The process of historical costing allows the costs to be established

after they are incurred. Marks and Spencer uses this costing system to analyse the actual incurred

costs.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Absorption Costing: Marks and Spencer uses this system of costing to comprehend the

fixed manufacturing overheads. Such overheads are allocated by the organisation to its products

and are later used in its stock valuation.

Direct Costing: In the method of direct costing, the products of Marks and Spencer are

charged with the costs types that vary from the volume.

Marginal Costing: Marginal costing allows Marks and Spencer to classify its costs into

fixed and variable cost. Along with it, this costing is used for internal reporting.

The relationship between historical costing and absorption costing is that to understand

the manufacturing overheads in absorption costing it is important for the organisation to analyse

incurred costs which are done with the help of historical costing method. Also, it is important for

Marks and Spencer develop direct costing to develop marginal costing in order to complete the

process of internal reporting.

1.3 Identification of responsibility, profit, investment and cost centres

Below explored are types of centres such as responsibility, profit, investment and cost:

Responsibility centre: These centres are the organisational subunits in Marks and

Spencer. Small business divisions or groups are the kinds of subunits which are set up as

responsibility centres in the organisation.

Profit centres: A place where the identification of revenues and costs are done are

known as profit centres. In Marks and Spencer a profit centre varies from a particular team,

person, machine etc (Fitó Bertran, Llobet and Cuguero, 2018).

Investment centres: Investment centres the one in which costs, revenues, capital

investments are identified. The centres can be both subsidiary and division in Marks and

Spencer.

Cost centres: The place where costs are traced and segregated are known as cost centres

in Marks and Spencer.

1.4 Classifications of cost and their uses

Marks and Spencer used different costing methods to determine and understand different

organisational functions. Types of costs and their uses are:

2

fixed manufacturing overheads. Such overheads are allocated by the organisation to its products

and are later used in its stock valuation.

Direct Costing: In the method of direct costing, the products of Marks and Spencer are

charged with the costs types that vary from the volume.

Marginal Costing: Marginal costing allows Marks and Spencer to classify its costs into

fixed and variable cost. Along with it, this costing is used for internal reporting.

The relationship between historical costing and absorption costing is that to understand

the manufacturing overheads in absorption costing it is important for the organisation to analyse

incurred costs which are done with the help of historical costing method. Also, it is important for

Marks and Spencer develop direct costing to develop marginal costing in order to complete the

process of internal reporting.

1.3 Identification of responsibility, profit, investment and cost centres

Below explored are types of centres such as responsibility, profit, investment and cost:

Responsibility centre: These centres are the organisational subunits in Marks and

Spencer. Small business divisions or groups are the kinds of subunits which are set up as

responsibility centres in the organisation.

Profit centres: A place where the identification of revenues and costs are done are

known as profit centres. In Marks and Spencer a profit centre varies from a particular team,

person, machine etc (Fitó Bertran, Llobet and Cuguero, 2018).

Investment centres: Investment centres the one in which costs, revenues, capital

investments are identified. The centres can be both subsidiary and division in Marks and

Spencer.

Cost centres: The place where costs are traced and segregated are known as cost centres

in Marks and Spencer.

1.4 Classifications of cost and their uses

Marks and Spencer used different costing methods to determine and understand different

organisational functions. Types of costs and their uses are:

2

Fixed Costs: Costs which are used by Marks and Spencer to fix the used inputs in their

production process are Fixed costs. These costs do not vary while the production volume

changes (Ogungbade and Tabitha, 2018).

Variable Costs: The types of costs are used by Marks and Spencer to determine the

production variable inputs. These costs vary when production volume changes.

Semi-variable Costs: Semi-variable costs are fixed and variable as well. They do not

impact the production level directly but varies when there is a change observed in production

facilities, depreciation and administrative cost.

1.5 Marginal and absorption costing differences

Absorption Costing Marginal Costing

Absorption costing takes both fixed and

variable costing under account.

Marginal costing do not take the method of

fixed costing into account during the valuation

of the inventory and costing the product.

The classification of this costing is done in the

category of production, selling, administration,

and distribution (Uzaman and et.al., 2019).

Marginal costing classification is done in

variable and fixed costs.

The purpose of Absorption costing is to

provide the right evaluation of profits

generated.

The purpose of marginal costing is to bring

forth the product's cost contribution.

In costing, absorption costing is the method

one the most conventional methods and is seen

to be used in financial purpose and reporting of

taxes.

The marginal costing methods is not seen as a

conventional method as it involves numerous

data analysing.

2. Cost information examination and recording

2.1 Recording information

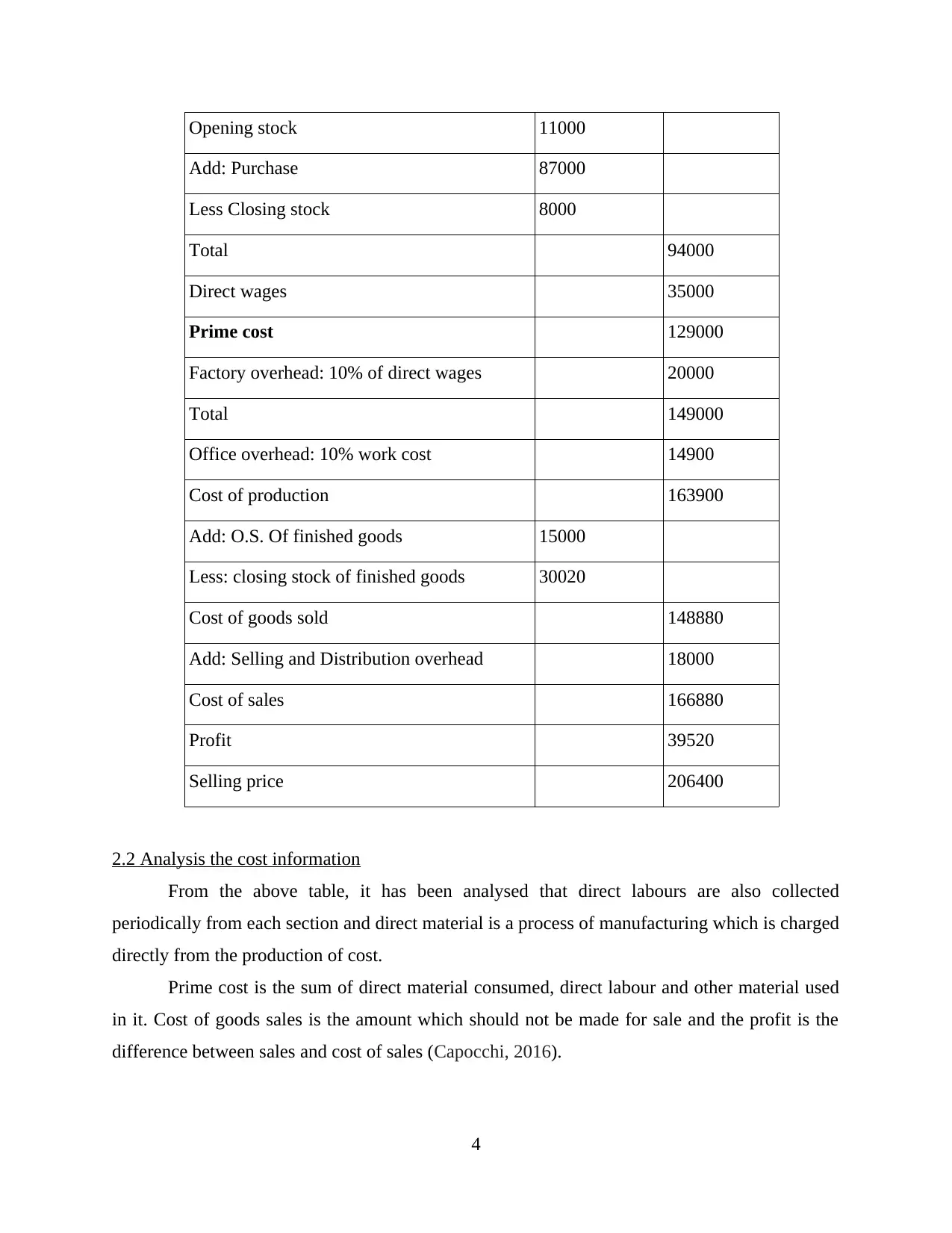

Cost sheet

Particulars Amount

3

production process are Fixed costs. These costs do not vary while the production volume

changes (Ogungbade and Tabitha, 2018).

Variable Costs: The types of costs are used by Marks and Spencer to determine the

production variable inputs. These costs vary when production volume changes.

Semi-variable Costs: Semi-variable costs are fixed and variable as well. They do not

impact the production level directly but varies when there is a change observed in production

facilities, depreciation and administrative cost.

1.5 Marginal and absorption costing differences

Absorption Costing Marginal Costing

Absorption costing takes both fixed and

variable costing under account.

Marginal costing do not take the method of

fixed costing into account during the valuation

of the inventory and costing the product.

The classification of this costing is done in the

category of production, selling, administration,

and distribution (Uzaman and et.al., 2019).

Marginal costing classification is done in

variable and fixed costs.

The purpose of Absorption costing is to

provide the right evaluation of profits

generated.

The purpose of marginal costing is to bring

forth the product's cost contribution.

In costing, absorption costing is the method

one the most conventional methods and is seen

to be used in financial purpose and reporting of

taxes.

The marginal costing methods is not seen as a

conventional method as it involves numerous

data analysing.

2. Cost information examination and recording

2.1 Recording information

Cost sheet

Particulars Amount

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Opening stock 11000

Add: Purchase 87000

Less Closing stock 8000

Total 94000

Direct wages 35000

Prime cost 129000

Factory overhead: 10% of direct wages 20000

Total 149000

Office overhead: 10% work cost 14900

Cost of production 163900

Add: O.S. Of finished goods 15000

Less: closing stock of finished goods 30020

Cost of goods sold 148880

Add: Selling and Distribution overhead 18000

Cost of sales 166880

Profit 39520

Selling price 206400

2.2 Analysis the cost information

From the above table, it has been analysed that direct labours are also collected

periodically from each section and direct material is a process of manufacturing which is charged

directly from the production of cost.

Prime cost is the sum of direct material consumed, direct labour and other material used

in it. Cost of goods sales is the amount which should not be made for sale and the profit is the

difference between sales and cost of sales (Capocchi, 2016).

4

Add: Purchase 87000

Less Closing stock 8000

Total 94000

Direct wages 35000

Prime cost 129000

Factory overhead: 10% of direct wages 20000

Total 149000

Office overhead: 10% work cost 14900

Cost of production 163900

Add: O.S. Of finished goods 15000

Less: closing stock of finished goods 30020

Cost of goods sold 148880

Add: Selling and Distribution overhead 18000

Cost of sales 166880

Profit 39520

Selling price 206400

2.2 Analysis the cost information

From the above table, it has been analysed that direct labours are also collected

periodically from each section and direct material is a process of manufacturing which is charged

directly from the production of cost.

Prime cost is the sum of direct material consumed, direct labour and other material used

in it. Cost of goods sales is the amount which should not be made for sale and the profit is the

difference between sales and cost of sales (Capocchi, 2016).

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

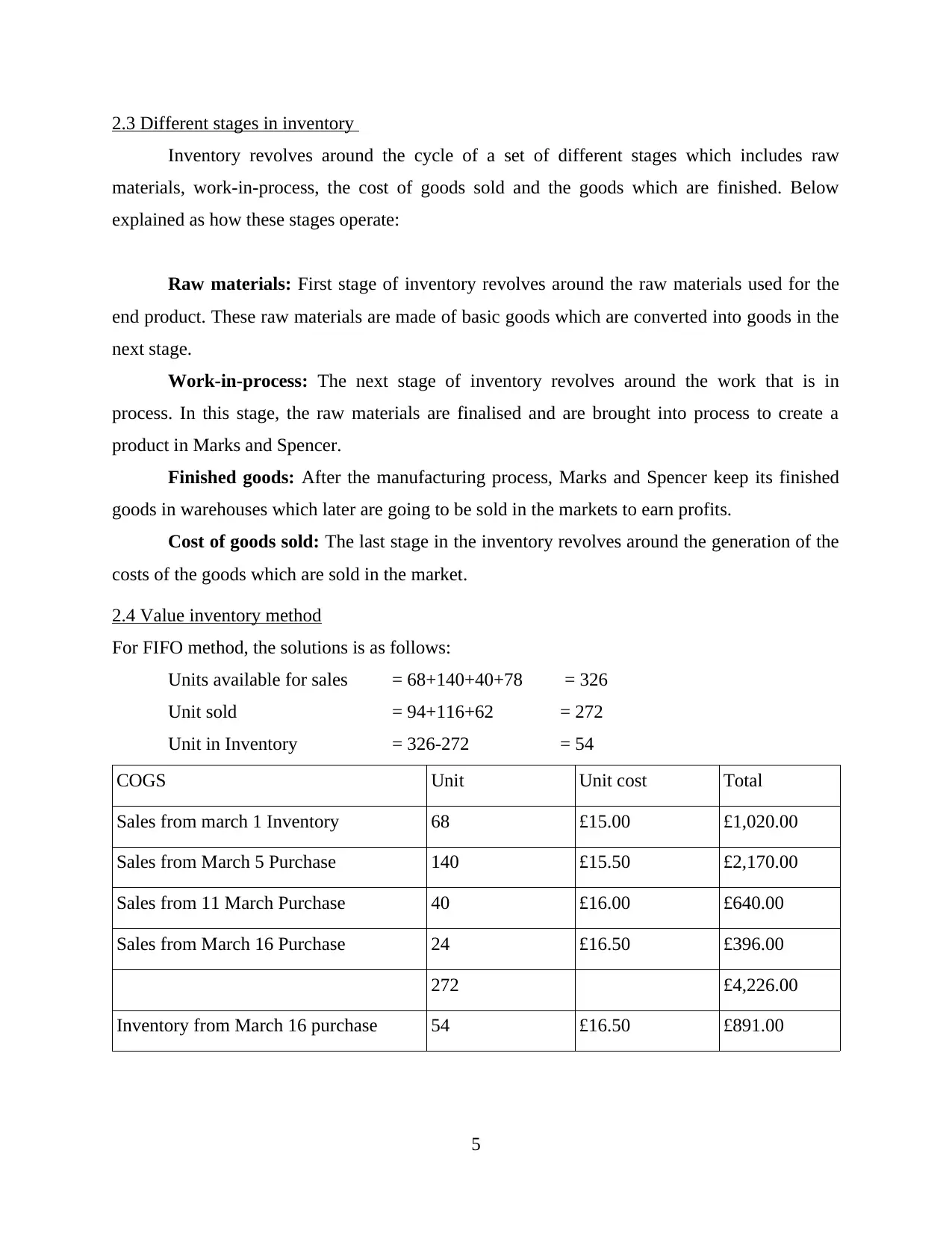

2.3 Different stages in inventory

Inventory revolves around the cycle of a set of different stages which includes raw

materials, work-in-process, the cost of goods sold and the goods which are finished. Below

explained as how these stages operate:

Raw materials: First stage of inventory revolves around the raw materials used for the

end product. These raw materials are made of basic goods which are converted into goods in the

next stage.

Work-in-process: The next stage of inventory revolves around the work that is in

process. In this stage, the raw materials are finalised and are brought into process to create a

product in Marks and Spencer.

Finished goods: After the manufacturing process, Marks and Spencer keep its finished

goods in warehouses which later are going to be sold in the markets to earn profits.

Cost of goods sold: The last stage in the inventory revolves around the generation of the

costs of the goods which are sold in the market.

2.4 Value inventory method

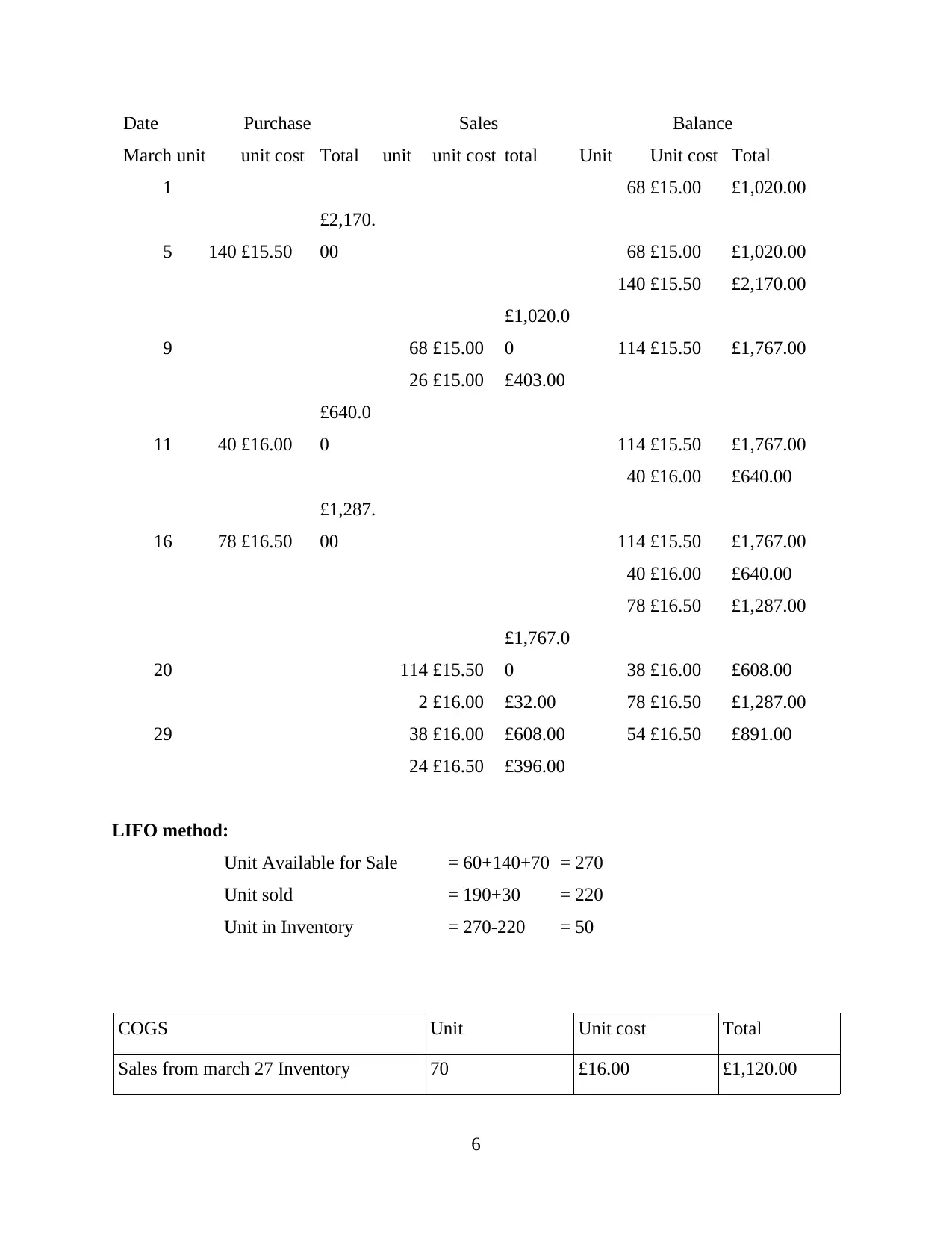

For FIFO method, the solutions is as follows:

Units available for sales = 68+140+40+78 = 326

Unit sold = 94+116+62 = 272

Unit in Inventory = 326-272 = 54

COGS Unit Unit cost Total

Sales from march 1 Inventory 68 £15.00 £1,020.00

Sales from March 5 Purchase 140 £15.50 £2,170.00

Sales from 11 March Purchase 40 £16.00 £640.00

Sales from March 16 Purchase 24 £16.50 £396.00

272 £4,226.00

Inventory from March 16 purchase 54 £16.50 £891.00

5

Inventory revolves around the cycle of a set of different stages which includes raw

materials, work-in-process, the cost of goods sold and the goods which are finished. Below

explained as how these stages operate:

Raw materials: First stage of inventory revolves around the raw materials used for the

end product. These raw materials are made of basic goods which are converted into goods in the

next stage.

Work-in-process: The next stage of inventory revolves around the work that is in

process. In this stage, the raw materials are finalised and are brought into process to create a

product in Marks and Spencer.

Finished goods: After the manufacturing process, Marks and Spencer keep its finished

goods in warehouses which later are going to be sold in the markets to earn profits.

Cost of goods sold: The last stage in the inventory revolves around the generation of the

costs of the goods which are sold in the market.

2.4 Value inventory method

For FIFO method, the solutions is as follows:

Units available for sales = 68+140+40+78 = 326

Unit sold = 94+116+62 = 272

Unit in Inventory = 326-272 = 54

COGS Unit Unit cost Total

Sales from march 1 Inventory 68 £15.00 £1,020.00

Sales from March 5 Purchase 140 £15.50 £2,170.00

Sales from 11 March Purchase 40 £16.00 £640.00

Sales from March 16 Purchase 24 £16.50 £396.00

272 £4,226.00

Inventory from March 16 purchase 54 £16.50 £891.00

5

Date Purchase Sales Balance

March unit unit cost Total unit unit cost total Unit Unit cost Total

1 68 £15.00 £1,020.00

5 140 £15.50

£2,170.

00 68 £15.00 £1,020.00

140 £15.50 £2,170.00

9 68 £15.00

£1,020.0

0 114 £15.50 £1,767.00

26 £15.00 £403.00

11 40 £16.00

£640.0

0 114 £15.50 £1,767.00

40 £16.00 £640.00

16 78 £16.50

£1,287.

00 114 £15.50 £1,767.00

40 £16.00 £640.00

78 £16.50 £1,287.00

20 114 £15.50

£1,767.0

0 38 £16.00 £608.00

2 £16.00 £32.00 78 £16.50 £1,287.00

29 38 £16.00 £608.00 54 £16.50 £891.00

24 £16.50 £396.00

LIFO method:

Unit Available for Sale = 60+140+70 = 270

Unit sold = 190+30 = 220

Unit in Inventory = 270-220 = 50

COGS Unit Unit cost Total

Sales from march 27 Inventory 70 £16.00 £1,120.00

6

March unit unit cost Total unit unit cost total Unit Unit cost Total

1 68 £15.00 £1,020.00

5 140 £15.50

£2,170.

00 68 £15.00 £1,020.00

140 £15.50 £2,170.00

9 68 £15.00

£1,020.0

0 114 £15.50 £1,767.00

26 £15.00 £403.00

11 40 £16.00

£640.0

0 114 £15.50 £1,767.00

40 £16.00 £640.00

16 78 £16.50

£1,287.

00 114 £15.50 £1,767.00

40 £16.00 £640.00

78 £16.50 £1,287.00

20 114 £15.50

£1,767.0

0 38 £16.00 £608.00

2 £16.00 £32.00 78 £16.50 £1,287.00

29 38 £16.00 £608.00 54 £16.50 £891.00

24 £16.50 £396.00

LIFO method:

Unit Available for Sale = 60+140+70 = 270

Unit sold = 190+30 = 220

Unit in Inventory = 270-220 = 50

COGS Unit Unit cost Total

Sales from march 27 Inventory 70 £16.00 £1,120.00

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

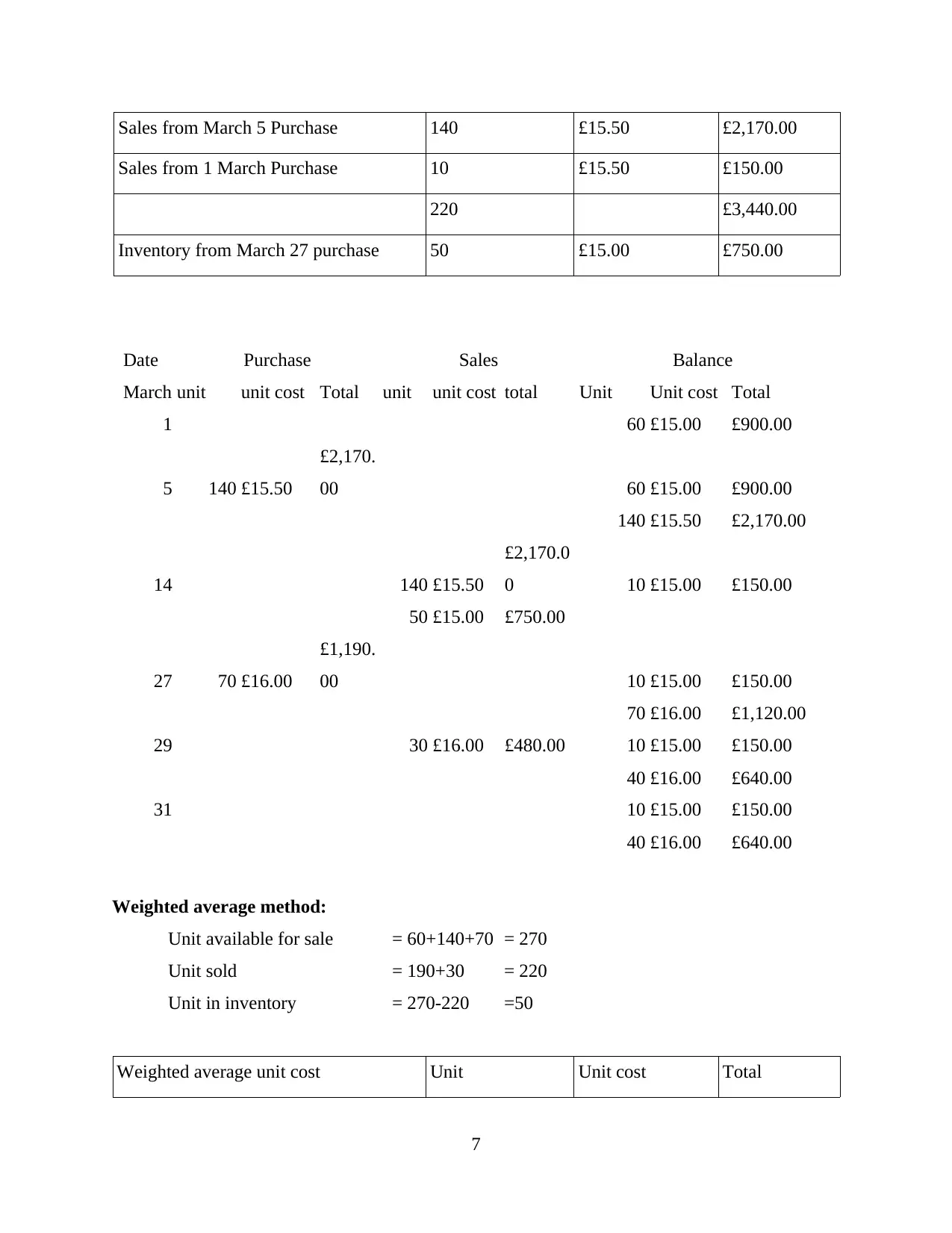

Sales from March 5 Purchase 140 £15.50 £2,170.00

Sales from 1 March Purchase 10 £15.50 £150.00

220 £3,440.00

Inventory from March 27 purchase 50 £15.00 £750.00

Date Purchase Sales Balance

March unit unit cost Total unit unit cost total Unit Unit cost Total

1 60 £15.00 £900.00

5 140 £15.50

£2,170.

00 60 £15.00 £900.00

140 £15.50 £2,170.00

14 140 £15.50

£2,170.0

0 10 £15.00 £150.00

50 £15.00 £750.00

27 70 £16.00

£1,190.

00 10 £15.00 £150.00

70 £16.00 £1,120.00

29 30 £16.00 £480.00 10 £15.00 £150.00

40 £16.00 £640.00

31 10 £15.00 £150.00

40 £16.00 £640.00

Weighted average method:

Unit available for sale = 60+140+70 = 270

Unit sold = 190+30 = 220

Unit in inventory = 270-220 =50

Weighted average unit cost Unit Unit cost Total

7

Sales from 1 March Purchase 10 £15.50 £150.00

220 £3,440.00

Inventory from March 27 purchase 50 £15.00 £750.00

Date Purchase Sales Balance

March unit unit cost Total unit unit cost total Unit Unit cost Total

1 60 £15.00 £900.00

5 140 £15.50

£2,170.

00 60 £15.00 £900.00

140 £15.50 £2,170.00

14 140 £15.50

£2,170.0

0 10 £15.00 £150.00

50 £15.00 £750.00

27 70 £16.00

£1,190.

00 10 £15.00 £150.00

70 £16.00 £1,120.00

29 30 £16.00 £480.00 10 £15.00 £150.00

40 £16.00 £640.00

31 10 £15.00 £150.00

40 £16.00 £640.00

Weighted average method:

Unit available for sale = 60+140+70 = 270

Unit sold = 190+30 = 220

Unit in inventory = 270-220 =50

Weighted average unit cost Unit Unit cost Total

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

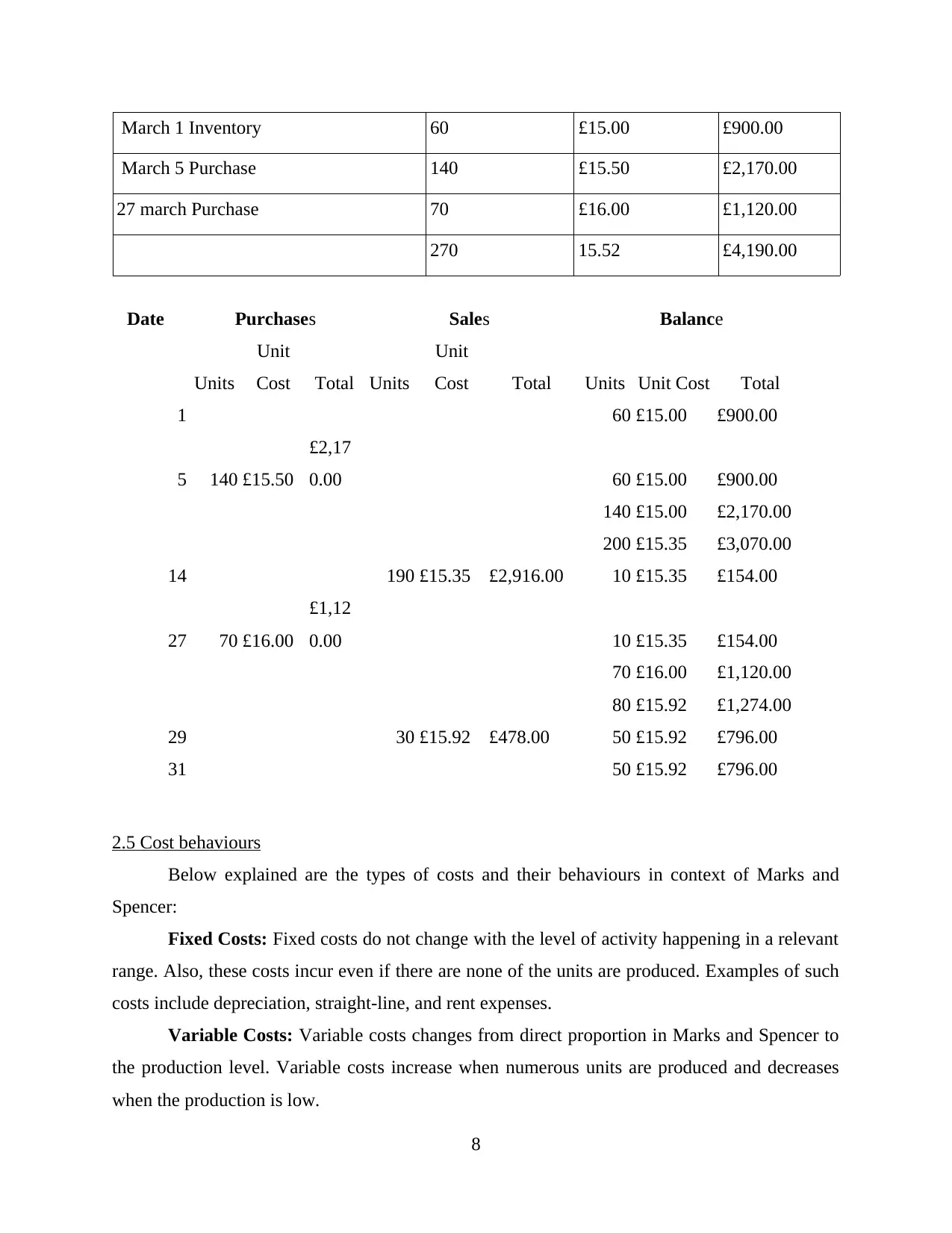

March 1 Inventory 60 £15.00 £900.00

March 5 Purchase 140 £15.50 £2,170.00

27 march Purchase 70 £16.00 £1,120.00

270 15.52 £4,190.00

Date Purchases Sales Balance

Units

Unit

Cost Total Units

Unit

Cost Total Units Unit Cost Total

1 60 £15.00 £900.00

5 140 £15.50

£2,17

0.00 60 £15.00 £900.00

140 £15.00 £2,170.00

200 £15.35 £3,070.00

14 190 £15.35 £2,916.00 10 £15.35 £154.00

27 70 £16.00

£1,12

0.00 10 £15.35 £154.00

70 £16.00 £1,120.00

80 £15.92 £1,274.00

29 30 £15.92 £478.00 50 £15.92 £796.00

31 50 £15.92 £796.00

2.5 Cost behaviours

Below explained are the types of costs and their behaviours in context of Marks and

Spencer:

Fixed Costs: Fixed costs do not change with the level of activity happening in a relevant

range. Also, these costs incur even if there are none of the units are produced. Examples of such

costs include depreciation, straight-line, and rent expenses.

Variable Costs: Variable costs changes from direct proportion in Marks and Spencer to

the production level. Variable costs increase when numerous units are produced and decreases

when the production is low.

8

March 5 Purchase 140 £15.50 £2,170.00

27 march Purchase 70 £16.00 £1,120.00

270 15.52 £4,190.00

Date Purchases Sales Balance

Units

Unit

Cost Total Units

Unit

Cost Total Units Unit Cost Total

1 60 £15.00 £900.00

5 140 £15.50

£2,17

0.00 60 £15.00 £900.00

140 £15.00 £2,170.00

200 £15.35 £3,070.00

14 190 £15.35 £2,916.00 10 £15.35 £154.00

27 70 £16.00

£1,12

0.00 10 £15.35 £154.00

70 £16.00 £1,120.00

80 £15.92 £1,274.00

29 30 £15.92 £478.00 50 £15.92 £796.00

31 50 £15.92 £796.00

2.5 Cost behaviours

Below explained are the types of costs and their behaviours in context of Marks and

Spencer:

Fixed Costs: Fixed costs do not change with the level of activity happening in a relevant

range. Also, these costs incur even if there are none of the units are produced. Examples of such

costs include depreciation, straight-line, and rent expenses.

Variable Costs: Variable costs changes from direct proportion in Marks and Spencer to

the production level. Variable costs increase when numerous units are produced and decreases

when the production is low.

8

Semi-variable Costs: Both fixed and variable costs components presence makes the

behavioural impact of semi-variable costs largely dependant on the side on which it is mostly

based upon in Marks and Spencer.

Step Costs: Step costs changes at discrete points rather than changing steadily at the

volume of activity happening within Marks and Spencer.

2.6 Costing systems and cost information

Below mentioned are the types of costing system and their cost informations:

Job costing: Job costing is known as a system that is used for tracking of the revenues

and job costs. It allows investigation which is standardized and job profitability as well.

Batch costing: In batch costing the items are generally stock manufactured. It allows

Marks and Spencer to understand the reaction of costs of manufactured items.

Unit costing: Unit costing revolves around expenditure that is total and Marks and

Spencer incurs to produce, store or sell single units of particular service or of its products.

Process costing: The method of process costing revolves around a simple method used to

collect and assign the produced units costs. In case when a number of identical units are

produced on large scale Marks and Spencer uses the method of process costing.

Service costing: Service costing method is used by Marks and Spencer when it is

providing services rather than producing goods.

3. Apportion cost

3.1 Describing overhead cost of production and service cost centre

Direct: It is the method under which the overhead cost are directly calculated such as

direct labour, cost and material.

Step down: It is the method that allocates the services cost to operate the departments in

well manner. This allocation is also start with the service department into the next highest cost.

3.2 Calculating overhead absorption rates using methods

1.Raw material cost basis:

Overhead absorption rate = Estimated FOH/ Estimated material cost * 100

= $150000/$110000*100

= $136.36% of direct material

Absorption of overhead on direct material cost:

9

behavioural impact of semi-variable costs largely dependant on the side on which it is mostly

based upon in Marks and Spencer.

Step Costs: Step costs changes at discrete points rather than changing steadily at the

volume of activity happening within Marks and Spencer.

2.6 Costing systems and cost information

Below mentioned are the types of costing system and their cost informations:

Job costing: Job costing is known as a system that is used for tracking of the revenues

and job costs. It allows investigation which is standardized and job profitability as well.

Batch costing: In batch costing the items are generally stock manufactured. It allows

Marks and Spencer to understand the reaction of costs of manufactured items.

Unit costing: Unit costing revolves around expenditure that is total and Marks and

Spencer incurs to produce, store or sell single units of particular service or of its products.

Process costing: The method of process costing revolves around a simple method used to

collect and assign the produced units costs. In case when a number of identical units are

produced on large scale Marks and Spencer uses the method of process costing.

Service costing: Service costing method is used by Marks and Spencer when it is

providing services rather than producing goods.

3. Apportion cost

3.1 Describing overhead cost of production and service cost centre

Direct: It is the method under which the overhead cost are directly calculated such as

direct labour, cost and material.

Step down: It is the method that allocates the services cost to operate the departments in

well manner. This allocation is also start with the service department into the next highest cost.

3.2 Calculating overhead absorption rates using methods

1.Raw material cost basis:

Overhead absorption rate = Estimated FOH/ Estimated material cost * 100

= $150000/$110000*100

= $136.36% of direct material

Absorption of overhead on direct material cost:

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.