Financial Management Analysis: Marks and Spencer Group Plc Report

VerifiedAdded on 2023/06/03

|15

|4035

|106

Report

AI Summary

This report provides a comprehensive financial analysis of Marks and Spencer Group Plc, covering a five-year period. It assesses liquidity through current and quick ratios, revealing a potential liquidity crisis. Profitability is examined using net, operating, and gross profit margins, indicating declining profitability trends. The report also touches upon efficiency ratios such as inventory, receivable, and payable turnover. Capital structure management and stock market performance are briefly discussed. The analysis identifies limitations and offers recommendations for improvement. Desklib provides access to similar solved assignments and study resources for students.

ANALYSIS OF BUSINESS OF MARKS AND SPENCER

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Content

Purpose of Report.................................................................................................................................3

Introduction...........................................................................................................................................3

Products................................................................................................................................................4

Key Personnel........................................................................................................................................4

Liquidity Analysis...................................................................................................................................4

Current Ratio.........................................................................................................................................5

Quick Ratio............................................................................................................................................6

Profitability Analysis..............................................................................................................................7

Net Profit Margin...................................................................................................................................7

Operating Profit Margin........................................................................................................................8

Gross Profit Margin...............................................................................................................................9

Inventory Turnover ratio.....................................................................................................................10

Receivable Turnover ratio...................................................................................................................11

Payable Turnover ratio........................................................................................................................12

Capital Structure Management...........................................................................................................12

Stock Market Performance..................................................................................................................13

Problems and Limitations....................................................................................................................13

Recommendation for Improvements..................................................................................................14

References:..........................................................................................................................................14

Purpose of Report.................................................................................................................................3

Introduction...........................................................................................................................................3

Products................................................................................................................................................4

Key Personnel........................................................................................................................................4

Liquidity Analysis...................................................................................................................................4

Current Ratio.........................................................................................................................................5

Quick Ratio............................................................................................................................................6

Profitability Analysis..............................................................................................................................7

Net Profit Margin...................................................................................................................................7

Operating Profit Margin........................................................................................................................8

Gross Profit Margin...............................................................................................................................9

Inventory Turnover ratio.....................................................................................................................10

Receivable Turnover ratio...................................................................................................................11

Payable Turnover ratio........................................................................................................................12

Capital Structure Management...........................................................................................................12

Stock Market Performance..................................................................................................................13

Problems and Limitations....................................................................................................................13

Recommendation for Improvements..................................................................................................14

References:..........................................................................................................................................14

Purpose of Report

The report has been prepared to analyse the business of Marks and Spencer and involves

analysis of business prospect over a period of 5 years with focus on the following segments:

(a) Liquidity analysis involving computation of Current Ratio and Quick Ratio;

(b) Profitability analysis involving computation of Gross Profit Margin, Net Profit Margin

and Operating Profit Margin;

(c) Working Capital Margin Analysis involving computation of Cash Conversion Cycle;

(d) Capital Structure Management analysis involving computation of debt to equity ratio

and capital gearing ratio;

(e) Stock Market Performance and involves computation of Price to Equity Ratio

Post above, the report deals with the limitation of analysis and recommendation for

improvement of analysis.

Introduction

Marks and Spencer Group Plc is a listed entity in London Stock Exchange with principal

operations under the retail segment. (Reuters.com, 2018)The company makes its presence

The report has been prepared to analyse the business of Marks and Spencer and involves

analysis of business prospect over a period of 5 years with focus on the following segments:

(a) Liquidity analysis involving computation of Current Ratio and Quick Ratio;

(b) Profitability analysis involving computation of Gross Profit Margin, Net Profit Margin

and Operating Profit Margin;

(c) Working Capital Margin Analysis involving computation of Cash Conversion Cycle;

(d) Capital Structure Management analysis involving computation of debt to equity ratio

and capital gearing ratio;

(e) Stock Market Performance and involves computation of Price to Equity Ratio

Post above, the report deals with the limitation of analysis and recommendation for

improvement of analysis.

Introduction

Marks and Spencer Group Plc is a listed entity in London Stock Exchange with principal

operations under the retail segment. (Reuters.com, 2018)The company makes its presence

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

pan world with more than 1380 stores globally. Marks has two segments of operation one is

domestic and other is international. Under the domestic segment it operated through its own

stores and through franchisee. The product dealt include food, clothing and home products. It

marks it presence digitally too. (Anon., n.d.) The company is headquartered in London. The

price of the shares quoted on London Stock Exchange on 6:09 AM EDT is 286.10 GBP.

Products

The company deals in following products and businesses:

(a) Food Industry: The Company has 696 food stores and contributes to 61% of UK

Revenue of the company. (Anon., 2018)

(b) Clothing and Home Sector: The company has 11.1 M Sqft clothing space in UK and the

business accounts for 39% of UK revenue of the company. (Anon., 2018)

Key Personnel

The key Personnel of the company along with a brief description of their profile is given

here-in-below:

(a) Archie Norman: Mr. Archie is the chairman of the company since September 2017. He

had prior stint in ITV, Lazard UK, Asda etc. He has a long track of creating value in

companies and changeover of many British Companies.

(b) Steve Rowe: Mr. Steve is the Chief Executive and Executive Director of the company

and has been since 2016. He is a veteran in e-commerce and retail business and he has

worked in all the areas of business.

(c) Humphrey Singer: He is Chief Financial Officer of the company and has been since

2018. He has past stint with Dixons Carphone Plc. He has played key roles in Finance

in various companies.

(d) Amanda Mellor: She is Group Secretary and group head of Corporate Governance of

the company. She has been since 2004 with the company and has diverse knowledge.

Her past stint was with James Capel, Robert Fleming etc.

(e) Katie Bickerstaffe: She is Non-Executive director of the company and has a diversified

knowledge in finance. She had a bright career with Ernst and Young, big four Audit

Company of the world. (Reuters.com, 2018)

Other directors include Pip McCrostie, Alison Brittain, Andrew Fisher, Andrew Halford.

Liquidity Analysis

This analysis measure the ability of the company to repays its liabilities in a timely manner as

and when due. The analysis is crucial to determine the company financial position in short

term and whether the company shall repay its debt in a timely manner. This ratio impact the

financial liquidity of the company and continuity of day-to-day operations of the company.

These analysis is based on items present in statement of financial position.

domestic and other is international. Under the domestic segment it operated through its own

stores and through franchisee. The product dealt include food, clothing and home products. It

marks it presence digitally too. (Anon., n.d.) The company is headquartered in London. The

price of the shares quoted on London Stock Exchange on 6:09 AM EDT is 286.10 GBP.

Products

The company deals in following products and businesses:

(a) Food Industry: The Company has 696 food stores and contributes to 61% of UK

Revenue of the company. (Anon., 2018)

(b) Clothing and Home Sector: The company has 11.1 M Sqft clothing space in UK and the

business accounts for 39% of UK revenue of the company. (Anon., 2018)

Key Personnel

The key Personnel of the company along with a brief description of their profile is given

here-in-below:

(a) Archie Norman: Mr. Archie is the chairman of the company since September 2017. He

had prior stint in ITV, Lazard UK, Asda etc. He has a long track of creating value in

companies and changeover of many British Companies.

(b) Steve Rowe: Mr. Steve is the Chief Executive and Executive Director of the company

and has been since 2016. He is a veteran in e-commerce and retail business and he has

worked in all the areas of business.

(c) Humphrey Singer: He is Chief Financial Officer of the company and has been since

2018. He has past stint with Dixons Carphone Plc. He has played key roles in Finance

in various companies.

(d) Amanda Mellor: She is Group Secretary and group head of Corporate Governance of

the company. She has been since 2004 with the company and has diverse knowledge.

Her past stint was with James Capel, Robert Fleming etc.

(e) Katie Bickerstaffe: She is Non-Executive director of the company and has a diversified

knowledge in finance. She had a bright career with Ernst and Young, big four Audit

Company of the world. (Reuters.com, 2018)

Other directors include Pip McCrostie, Alison Brittain, Andrew Fisher, Andrew Halford.

Liquidity Analysis

This analysis measure the ability of the company to repays its liabilities in a timely manner as

and when due. The analysis is crucial to determine the company financial position in short

term and whether the company shall repay its debt in a timely manner. This ratio impact the

financial liquidity of the company and continuity of day-to-day operations of the company.

These analysis is based on items present in statement of financial position.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Current Ratio

This ratio is one of the simplest and most common tool of analysis used for analysis the

current asset and liability position of the company. The idle ratio is 2:1. However, the same is

not guarantee that company shall meet its short term obligations. (Accounting Coach, 2018)

The formula for computation of Current ratio has been detailed here-in-below:

Current Ratio: Current Asset/ Current Liability

The data has been used for past 5 years to analyse the current ratio of the company. The table

has been enumerated here-in-below:

Current Ratio

('000)

Sl

No Particulars Current Asset (A) Current Liability (B) Current Ratio (A/B)

1 2018 1317900 1826000 0.722

2 2017 1723300 2368000 0.728

3 2016 1461400 2104800 0.694

4 2015 1455000 2111600 0.689

5 2014 1368500 2349300 0.583

This ratio is one of the simplest and most common tool of analysis used for analysis the

current asset and liability position of the company. The idle ratio is 2:1. However, the same is

not guarantee that company shall meet its short term obligations. (Accounting Coach, 2018)

The formula for computation of Current ratio has been detailed here-in-below:

Current Ratio: Current Asset/ Current Liability

The data has been used for past 5 years to analyse the current ratio of the company. The table

has been enumerated here-in-below:

Current Ratio

('000)

Sl

No Particulars Current Asset (A) Current Liability (B) Current Ratio (A/B)

1 2018 1317900 1826000 0.722

2 2017 1723300 2368000 0.728

3 2016 1461400 2104800 0.694

4 2015 1455000 2111600 0.689

5 2014 1368500 2349300 0.583

On perusal of the above table, it shall be seen that company’s current ratio is below 2 over the

period of 5 years and has been gradually improving over the years which is a good sign but

the company suffers from acute liquidity crisis as understandable from low current ratio and

has only 72 cents assets for 1 GBP of liability which is not good and is impacting the

financial position of the company (Anon., 2018)

Quick Ratio

Quick Ratio is also a significant tool for analysing the liquidity position of the company. The

major difference between current ratio and quick ratio is that it goes for further in depth

analysis and excludes inventory and prepaid expense from current asset for computation of

ratio. (Investing Answers, 2018) The idle quick ratio is 1:1.The formula for computation of

quick ratio has been detailed here-in-below

Quick Ratio: (Current Asset- Inventory- Prepaid Expense)/Current Liability

The data has been used for past 5 years to analyse the quick ratio of the company. The table

has been enumerated here-in-below:

Quick Ratio

('000)

Sl No Particulars Quick Asset (A) Current Liability (B) Quick Ratio (A/B)

1 2018 536900 1826000 0.294

2 2017 964800 2368000 0.407

3 2016 661500 2104800 0.314

4 2015 657200 2111600 0.311

5 2014 523000 2349300 0.223

2013 2014 2015 2016 2017 2018 2019

0.000

0.100

0.200

0.300

0.400

0.500

0.600

0.700

0.800 0.7220.728

0.6940.689

0.583

Current Ratio (A/B)

Current Ratio (A/B)

period of 5 years and has been gradually improving over the years which is a good sign but

the company suffers from acute liquidity crisis as understandable from low current ratio and

has only 72 cents assets for 1 GBP of liability which is not good and is impacting the

financial position of the company (Anon., 2018)

Quick Ratio

Quick Ratio is also a significant tool for analysing the liquidity position of the company. The

major difference between current ratio and quick ratio is that it goes for further in depth

analysis and excludes inventory and prepaid expense from current asset for computation of

ratio. (Investing Answers, 2018) The idle quick ratio is 1:1.The formula for computation of

quick ratio has been detailed here-in-below

Quick Ratio: (Current Asset- Inventory- Prepaid Expense)/Current Liability

The data has been used for past 5 years to analyse the quick ratio of the company. The table

has been enumerated here-in-below:

Quick Ratio

('000)

Sl No Particulars Quick Asset (A) Current Liability (B) Quick Ratio (A/B)

1 2018 536900 1826000 0.294

2 2017 964800 2368000 0.407

3 2016 661500 2104800 0.314

4 2015 657200 2111600 0.311

5 2014 523000 2349300 0.223

2013 2014 2015 2016 2017 2018 2019

0.000

0.100

0.200

0.300

0.400

0.500

0.600

0.700

0.800 0.7220.728

0.6940.689

0.583

Current Ratio (A/B)

Current Ratio (A/B)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

On perusal of the above table, it shall be seen that company’s quick ratio is below 1 over the

period of 5 years and has been gradually improving over the years which is a good sign but

the company suffers from acute liquidity crisis as understandable from low quick ratio and

has only 30 cents assets for 1 GBP of liability which is not good and is impacting the

financial position of the company. It is also evident that inventory forms a major chunk of

current asset of the company which is not a positive signal in short term. (Anon., 2018)

Further, the cash reserves of the company are acute low.

Profitability Analysis

The second segment of analysis is based on profitability of the company. It is an important

for a company to earn profit for sustaining the business and expanding in future. The key

ratios that has been analysed to understand the profitability of the company include (a) Net

Profit Margin, (b) Gross Profit Margin, (c) Operating profit Margin

Net Profit Margin

This is a significant tool in analysing the profitability that is in hand of the company post tax

and meeting expenses of the company. This profit is available for distribution to equity and

preference shareholders. Further, the higher the margin the better the owners of the company

are taken care of. The ratio is computed by using the following formula:

Net Profit Margin= (Net Profit/ Sales)

The data has been used for past 5 years to analyse the net profit margin of the company. The

table has been enumerated here-in-below:

Net Profit Margin

('000)

Sl No Particulars Net Profit (A) Sales (B) Net Profit Margin (A/B)

1 2018 25700 10698200 0.2%

2 2017 117100 10622000 1.1%

3 2016 406900 10555400 3.9%

4 2015 486500 10311400 4.7%

5 2014 506000 10309700 4.9%

2013.5 2014 2014.5 2015 2015.5 2016 2016.5 2017 2017.5 2018 2018.5

0.000

0.050

0.100

0.150

0.200

0.250

0.300

0.350

0.400

0.450

0.294

0.407

0.3140.311

0.223

Quick Ratio

Series2

period of 5 years and has been gradually improving over the years which is a good sign but

the company suffers from acute liquidity crisis as understandable from low quick ratio and

has only 30 cents assets for 1 GBP of liability which is not good and is impacting the

financial position of the company. It is also evident that inventory forms a major chunk of

current asset of the company which is not a positive signal in short term. (Anon., 2018)

Further, the cash reserves of the company are acute low.

Profitability Analysis

The second segment of analysis is based on profitability of the company. It is an important

for a company to earn profit for sustaining the business and expanding in future. The key

ratios that has been analysed to understand the profitability of the company include (a) Net

Profit Margin, (b) Gross Profit Margin, (c) Operating profit Margin

Net Profit Margin

This is a significant tool in analysing the profitability that is in hand of the company post tax

and meeting expenses of the company. This profit is available for distribution to equity and

preference shareholders. Further, the higher the margin the better the owners of the company

are taken care of. The ratio is computed by using the following formula:

Net Profit Margin= (Net Profit/ Sales)

The data has been used for past 5 years to analyse the net profit margin of the company. The

table has been enumerated here-in-below:

Net Profit Margin

('000)

Sl No Particulars Net Profit (A) Sales (B) Net Profit Margin (A/B)

1 2018 25700 10698200 0.2%

2 2017 117100 10622000 1.1%

3 2016 406900 10555400 3.9%

4 2015 486500 10311400 4.7%

5 2014 506000 10309700 4.9%

2013.5 2014 2014.5 2015 2015.5 2016 2016.5 2017 2017.5 2018 2018.5

0.000

0.050

0.100

0.150

0.200

0.250

0.300

0.350

0.400

0.450

0.294

0.407

0.3140.311

0.223

Quick Ratio

Series2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

On perusal of the above table, it shall be seen that company’s Net Profit margin has been very

low over the years and has reached bottom in 2018 as reflected in the curve above. Thus, it

can be inferred that company has not been generating significant profits from its two

divisions and is not providing fair return to its investors. Further, a lower profit margin shall

impact the future business of the company a turnover strategy is must. Accordingly, a new

chairman with experience in turnaround strategies has been seated. (Anon., 2018)

Operating Profit Margin

This is also a significant tool for analysing the profitability of the company. The ratio takes

into account the profitability of the company from its continuous operations before tax and

finance cost. The higher the operating margin the better the investors are taken care of. The

formula for computation of margin has been detailed here-in-below:\

Operating Profit Margin=Operating Profit/Sales

The data has been used for past 5 years to analyse the operating profit margin of the

company. The table has been enumerated here-in-below:

2013.5 2014 2014.5 2015 2015.5 2016 2016.5 2017 2017.5 2018 2018.5

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

0.2%

1.1%

3.9%

4.7%

4.9%

Net Profit Margin

Series2

low over the years and has reached bottom in 2018 as reflected in the curve above. Thus, it

can be inferred that company has not been generating significant profits from its two

divisions and is not providing fair return to its investors. Further, a lower profit margin shall

impact the future business of the company a turnover strategy is must. Accordingly, a new

chairman with experience in turnaround strategies has been seated. (Anon., 2018)

Operating Profit Margin

This is also a significant tool for analysing the profitability of the company. The ratio takes

into account the profitability of the company from its continuous operations before tax and

finance cost. The higher the operating margin the better the investors are taken care of. The

formula for computation of margin has been detailed here-in-below:\

Operating Profit Margin=Operating Profit/Sales

The data has been used for past 5 years to analyse the operating profit margin of the

company. The table has been enumerated here-in-below:

2013.5 2014 2014.5 2015 2015.5 2016 2016.5 2017 2017.5 2018 2018.5

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

0.2%

1.1%

3.9%

4.7%

4.9%

Net Profit Margin

Series2

Operating Profit Margin

('000)

Sl

No Particulars Operating Profit (A) Sales (B) Operating Profit Margin (A/B)

1 2018 29100 10698200 0.272%

2 2017 115700 10622000 1.089%

3 2016 404400 10555400 3.831%

4 2015 481700 10311400 4.672%

5 2014 694500 10309700 6.736%

On perusal of the above table, it shall be seen that company’s Operating Profit margin has

been very low over the years and has reached bottom in 2018 as reflected in the curve above.

Thus, it can be inferred that company has not been generating significant profits from its two

divisions and is not providing fair return to its investors. Further, a lower profit margin shall

impact the future business of the company a turnover strategy is must. Accordingly, a new

chairman with experience in turnaround strategies has been seated.

Gross Profit Margin

Gross Profit Margin is an indicator of profit earned after deducting direct expense incurred

for earning such profit. The ratio is significant for analysing the profit earned by the company

from its business before reduction of any indirect expense. The higher the gross profit margin

the better the investors are taken care of. The formula for computation of margin has been

detailed here-in-below:

Gross Profit Margin=Gross Profit/Sales

The data has been used for past 5 years to analyse the gross profit margin of the company.

The table has been enumerated here-in-below:

2013.5 2014 2014.5 2015 2015.5 2016 2016.5 2017 2017.5 2018 2018.5

0.000%

1.000%

2.000%

3.000%

4.000%

5.000%

6.000%

7.000%

8.000%

0.272%

1.089%

3.831%

4.672%

6.736%

Operating Profit Margin

Series2

('000)

Sl

No Particulars Operating Profit (A) Sales (B) Operating Profit Margin (A/B)

1 2018 29100 10698200 0.272%

2 2017 115700 10622000 1.089%

3 2016 404400 10555400 3.831%

4 2015 481700 10311400 4.672%

5 2014 694500 10309700 6.736%

On perusal of the above table, it shall be seen that company’s Operating Profit margin has

been very low over the years and has reached bottom in 2018 as reflected in the curve above.

Thus, it can be inferred that company has not been generating significant profits from its two

divisions and is not providing fair return to its investors. Further, a lower profit margin shall

impact the future business of the company a turnover strategy is must. Accordingly, a new

chairman with experience in turnaround strategies has been seated.

Gross Profit Margin

Gross Profit Margin is an indicator of profit earned after deducting direct expense incurred

for earning such profit. The ratio is significant for analysing the profit earned by the company

from its business before reduction of any indirect expense. The higher the gross profit margin

the better the investors are taken care of. The formula for computation of margin has been

detailed here-in-below:

Gross Profit Margin=Gross Profit/Sales

The data has been used for past 5 years to analyse the gross profit margin of the company.

The table has been enumerated here-in-below:

2013.5 2014 2014.5 2015 2015.5 2016 2016.5 2017 2017.5 2018 2018.5

0.000%

1.000%

2.000%

3.000%

4.000%

5.000%

6.000%

7.000%

8.000%

0.272%

1.089%

3.831%

4.672%

6.736%

Operating Profit Margin

Series2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Gross Profit Margin

('000)

Sl No Particulars Gross Profit (A) Sales (B) Gross Profit Margin (A/B)

1 2018 3952600 10698200 36.95%

2 2017 3992700 10622000 37.59%

3 2016 4028900 10555400 38.17%

4 2015 3880600 10311400 37.63%

5 2014 3870700 10309700 37.54%

On perusal of the above table, it shall be seen that company’s Gross Profit margin has been

good over the years and has reached bottom in 2018 as reflected in the curve above. Despite

that the net profit and operating profit of the company has been low on account of significant

indirect expense of the company. (Anon., 2018)

Efficiency Ratio

These ratio analyse the effectiveness of the company to manage its asset and liability in a

prudent manner. Further, it also analyse the efficiency of the company to utilise the assets to

generate revenue. (MyAccountingCourse.com, 2018)

The ratios that have been analysed includes inventory turnover ratio, receivable turnover ratio and

Account payable turnover ratio.

2013.5 2014 2014.5 2015 2015.5 2016 2016.5 2017 2017.5 2018 2018.5

36.00%

36.50%

37.00%

37.50%

38.00%

38.50%

36.95%

37.59%

38.17%

37.63%

37.54%

Gross Profit Margin

Series2

('000)

Sl No Particulars Gross Profit (A) Sales (B) Gross Profit Margin (A/B)

1 2018 3952600 10698200 36.95%

2 2017 3992700 10622000 37.59%

3 2016 4028900 10555400 38.17%

4 2015 3880600 10311400 37.63%

5 2014 3870700 10309700 37.54%

On perusal of the above table, it shall be seen that company’s Gross Profit margin has been

good over the years and has reached bottom in 2018 as reflected in the curve above. Despite

that the net profit and operating profit of the company has been low on account of significant

indirect expense of the company. (Anon., 2018)

Efficiency Ratio

These ratio analyse the effectiveness of the company to manage its asset and liability in a

prudent manner. Further, it also analyse the efficiency of the company to utilise the assets to

generate revenue. (MyAccountingCourse.com, 2018)

The ratios that have been analysed includes inventory turnover ratio, receivable turnover ratio and

Account payable turnover ratio.

2013.5 2014 2014.5 2015 2015.5 2016 2016.5 2017 2017.5 2018 2018.5

36.00%

36.50%

37.00%

37.50%

38.00%

38.50%

36.95%

37.59%

38.17%

37.63%

37.54%

Gross Profit Margin

Series2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

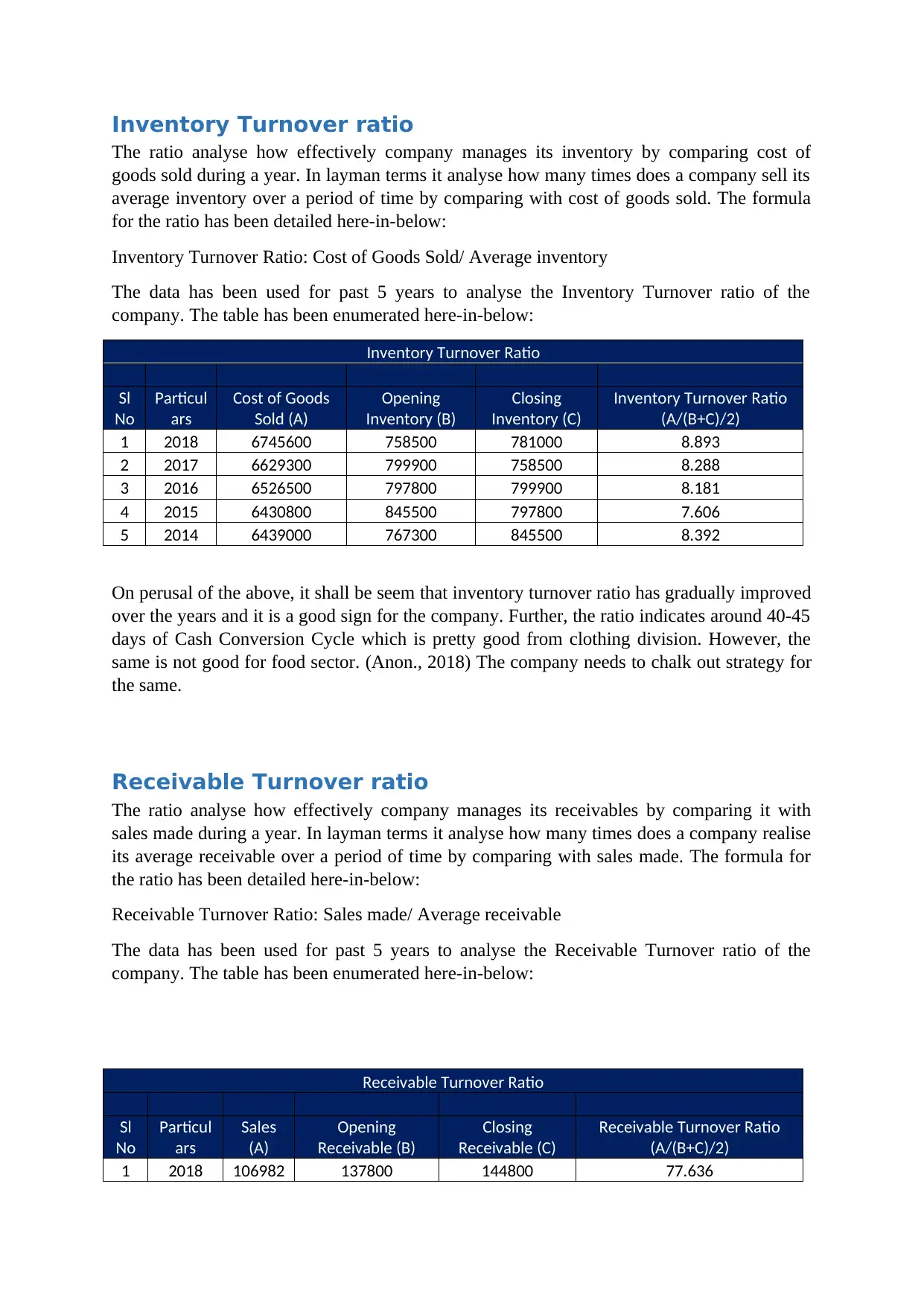

Inventory Turnover ratio

The ratio analyse how effectively company manages its inventory by comparing cost of

goods sold during a year. In layman terms it analyse how many times does a company sell its

average inventory over a period of time by comparing with cost of goods sold. The formula

for the ratio has been detailed here-in-below:

Inventory Turnover Ratio: Cost of Goods Sold/ Average inventory

The data has been used for past 5 years to analyse the Inventory Turnover ratio of the

company. The table has been enumerated here-in-below:

Inventory Turnover Ratio

Sl

No

Particul

ars

Cost of Goods

Sold (A)

Opening

Inventory (B)

Closing

Inventory (C)

Inventory Turnover Ratio

(A/(B+C)/2)

1 2018 6745600 758500 781000 8.893

2 2017 6629300 799900 758500 8.288

3 2016 6526500 797800 799900 8.181

4 2015 6430800 845500 797800 7.606

5 2014 6439000 767300 845500 8.392

On perusal of the above, it shall be seem that inventory turnover ratio has gradually improved

over the years and it is a good sign for the company. Further, the ratio indicates around 40-45

days of Cash Conversion Cycle which is pretty good from clothing division. However, the

same is not good for food sector. (Anon., 2018) The company needs to chalk out strategy for

the same.

Receivable Turnover ratio

The ratio analyse how effectively company manages its receivables by comparing it with

sales made during a year. In layman terms it analyse how many times does a company realise

its average receivable over a period of time by comparing with sales made. The formula for

the ratio has been detailed here-in-below:

Receivable Turnover Ratio: Sales made/ Average receivable

The data has been used for past 5 years to analyse the Receivable Turnover ratio of the

company. The table has been enumerated here-in-below:

Receivable Turnover Ratio

Sl

No

Particul

ars

Sales

(A)

Opening

Receivable (B)

Closing

Receivable (C)

Receivable Turnover Ratio

(A/(B+C)/2)

1 2018 106982 137800 144800 77.636

The ratio analyse how effectively company manages its inventory by comparing cost of

goods sold during a year. In layman terms it analyse how many times does a company sell its

average inventory over a period of time by comparing with cost of goods sold. The formula

for the ratio has been detailed here-in-below:

Inventory Turnover Ratio: Cost of Goods Sold/ Average inventory

The data has been used for past 5 years to analyse the Inventory Turnover ratio of the

company. The table has been enumerated here-in-below:

Inventory Turnover Ratio

Sl

No

Particul

ars

Cost of Goods

Sold (A)

Opening

Inventory (B)

Closing

Inventory (C)

Inventory Turnover Ratio

(A/(B+C)/2)

1 2018 6745600 758500 781000 8.893

2 2017 6629300 799900 758500 8.288

3 2016 6526500 797800 799900 8.181

4 2015 6430800 845500 797800 7.606

5 2014 6439000 767300 845500 8.392

On perusal of the above, it shall be seem that inventory turnover ratio has gradually improved

over the years and it is a good sign for the company. Further, the ratio indicates around 40-45

days of Cash Conversion Cycle which is pretty good from clothing division. However, the

same is not good for food sector. (Anon., 2018) The company needs to chalk out strategy for

the same.

Receivable Turnover ratio

The ratio analyse how effectively company manages its receivables by comparing it with

sales made during a year. In layman terms it analyse how many times does a company realise

its average receivable over a period of time by comparing with sales made. The formula for

the ratio has been detailed here-in-below:

Receivable Turnover Ratio: Sales made/ Average receivable

The data has been used for past 5 years to analyse the Receivable Turnover ratio of the

company. The table has been enumerated here-in-below:

Receivable Turnover Ratio

Sl

No

Particul

ars

Sales

(A)

Opening

Receivable (B)

Closing

Receivable (C)

Receivable Turnover Ratio

(A/(B+C)/2)

1 2018 106982 137800 144800 77.636

Receivable Turnover Ratio

00

2 2017

106220

00 167800 137800 63.302

3 2016

105554

00 177000 167800 59.635

4 2015

103114

00 309500 177000 33.316

5 2014

103097

00 245000 309500 42.080

On perusal of the above, it shall be seem that receivable turnover ratio has gradually

improved over the years and it is a good sign for the company. Further, the ratio indicates

around 5- 10 days of Cash Conversion Cycle which is pretty good and shows the

effectiveness of management in marinating its working capital.

Payable Turnover ratio

The ratio analyse how effectively company manages its payables by comparing it with

purchases made during a year. In layman terms it analyse how many times does a company

pays its average payable over a period of time by comparing with purchases made. The

formula for the ratio has been detailed here-in-below:

Purchase Turnover Ratio: Purchases made/ Average payable

Purchases: Cost of goods sold +Opening Stock- Closing Stock

The data has been used for past 5 years to analyse the Receivable Turnover ratio of the

company. The table has been enumerated here-in-below:

Payable Turnover Ratio

Sl

No

Particul

ars

Purchases

(A)

Opening

Payable (B)

Closing

Receivable (C)

Payable Turnover Ratio

(A/(B+C)/2)

1 2018 6768100 967500 872900 6.995

2 2017 6587900 1021900 967500 6.447

3 2016 6528600 967600 1021900 6.747

4 2015 6383100 1692800 967600 3.771

5 2014 6517200 1503800 1692800 4.334

The company has been very slow in making payment to its creditors as indicated by a low

turnover ratio. The same justifies the reason for lower current ratio and quick ratio. However,

a lower ratio is also an indicator of a weaker bargaining power in the hands of the company.

The average payment days lies between 80-90 days resulting in a negative cash conversion

cycle.

00

2 2017

106220

00 167800 137800 63.302

3 2016

105554

00 177000 167800 59.635

4 2015

103114

00 309500 177000 33.316

5 2014

103097

00 245000 309500 42.080

On perusal of the above, it shall be seem that receivable turnover ratio has gradually

improved over the years and it is a good sign for the company. Further, the ratio indicates

around 5- 10 days of Cash Conversion Cycle which is pretty good and shows the

effectiveness of management in marinating its working capital.

Payable Turnover ratio

The ratio analyse how effectively company manages its payables by comparing it with

purchases made during a year. In layman terms it analyse how many times does a company

pays its average payable over a period of time by comparing with purchases made. The

formula for the ratio has been detailed here-in-below:

Purchase Turnover Ratio: Purchases made/ Average payable

Purchases: Cost of goods sold +Opening Stock- Closing Stock

The data has been used for past 5 years to analyse the Receivable Turnover ratio of the

company. The table has been enumerated here-in-below:

Payable Turnover Ratio

Sl

No

Particul

ars

Purchases

(A)

Opening

Payable (B)

Closing

Receivable (C)

Payable Turnover Ratio

(A/(B+C)/2)

1 2018 6768100 967500 872900 6.995

2 2017 6587900 1021900 967500 6.447

3 2016 6528600 967600 1021900 6.747

4 2015 6383100 1692800 967600 3.771

5 2014 6517200 1503800 1692800 4.334

The company has been very slow in making payment to its creditors as indicated by a low

turnover ratio. The same justifies the reason for lower current ratio and quick ratio. However,

a lower ratio is also an indicator of a weaker bargaining power in the hands of the company.

The average payment days lies between 80-90 days resulting in a negative cash conversion

cycle.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.