Stochastic Analysis Assignment: Martingales, Ito Integrals, Processes

VerifiedAdded on 2023/04/20

|3

|630

|284

Homework Assignment

AI Summary

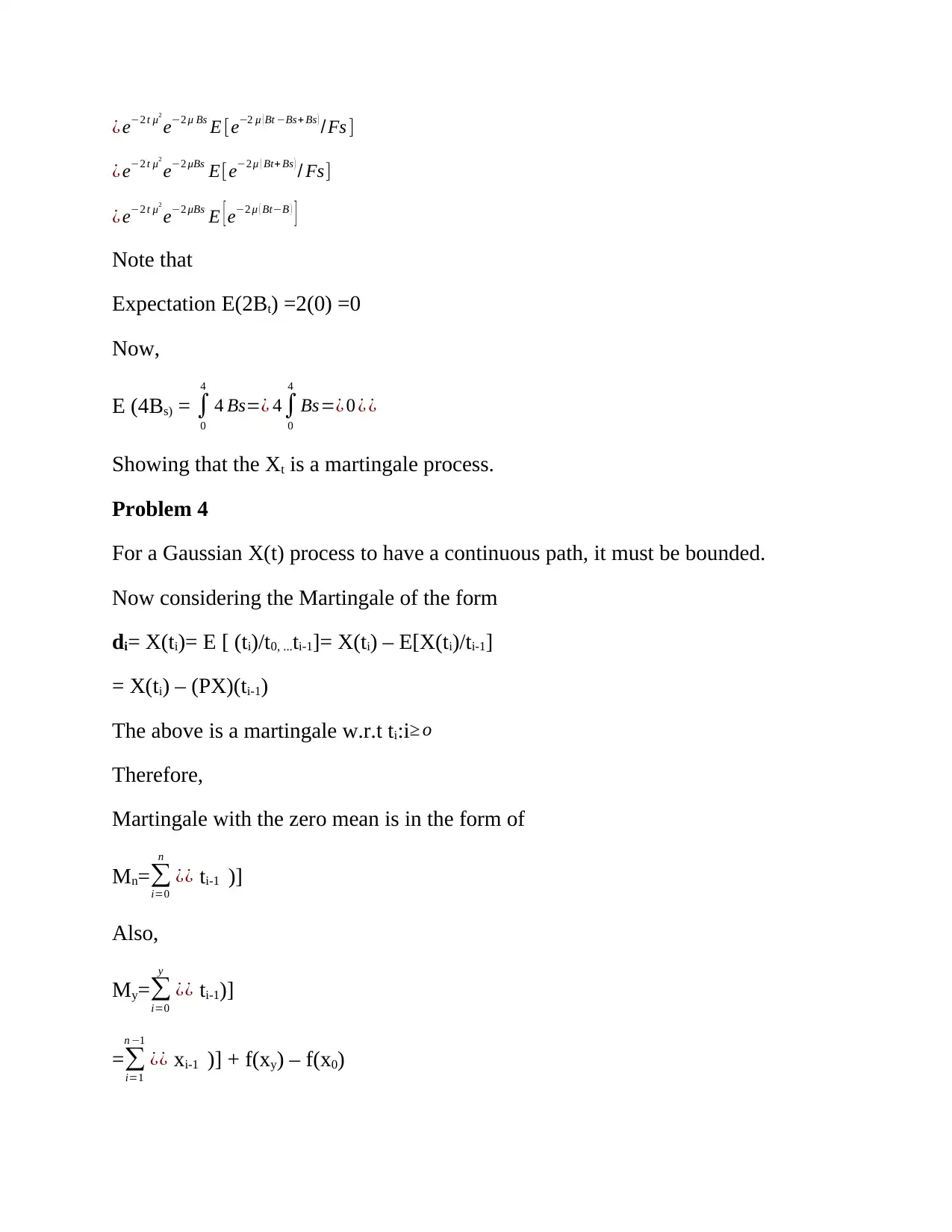

This assignment solution delves into stochastic analysis, addressing problems related to martingales, Ito integrals, and Brownian motion. It demonstrates that a given process is a martingale by showing that the conditional expectation satisfies the required property. The solution also explores the properties of Gaussian processes and their relationship to continuous paths, along with the mean and variance of Ito integrals, leveraging Ito's lemma for pathwise construction. The document also discusses the consistency of finite dimensional distributions in the context of stochastic processes. Desklib offers a wealth of similar solved assignments and study resources for students.

1 out of 3

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.