ACC621 Semester 2: Analyzing Issues & Materiality in Auditing Practice

VerifiedAdded on 2023/06/15

|12

|2473

|368

Report

AI Summary

This report provides an analysis of key issues in auditing practice, focusing on materiality and misstatements. It begins with a discussion of preliminary judgments for materiality, highlighting the importance of establishing a base for assessing misstatements and the impact of materiality levels on audit scope and budget. The report then examines analytical review procedures, including trend analysis, and identifies four accounts susceptible to material misstatement: sales, cost of sales, depreciation, and wages. For each account, the rationale for selection and relevant assertions are explained. The report recommends specific audit procedures for each account to prevent and detect misstatements. Finally, it addresses the auditor's responsibility in detecting fraud, emphasizing the need to evaluate both transactional data and behavioral patterns. Desklib offers a wealth of similar solved assignments and past papers to aid students in their studies.

Running head: ISSUES IN AUDITING PRACTICE

Issues in auditing practice

Name of the student

Name of the university

Student ID

Author note

Issues in auditing practice

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ISSUES IN AUDITING PRACTICE

Table of Contents

1.0 Preliminary judgement for materiality............................................................................2

2.0 Analytical review............................................................................................................3

3.0 Analytical review through trend analysis.............................................................................3

4.0 Accounts under material misstatement................................................................................4

4.1.1 First account selected – Sales........................................................................................4

4.1.2 Rational for selection....................................................................................................4

4.1.3 Assertion and explanation.............................................................................................4

4.2 Second account selected – Cost of sales......................................................................4

4.2.1 Rational for selection...............................................................................................4

4.2.2 Assertion and explanation........................................................................................5

4.3 Third account selected – Depreciation.............................................................................5

4.3.1 Rational for selection....................................................................................................5

4.3.2 Assertion and explanation.............................................................................................5

4.4 Fourth account selected – Wages.....................................................................................6

4.4.1 Rational for selection....................................................................................................6

4.4.2 Assertion and explanation.............................................................................................6

5.0 Recommended audit procedure............................................................................................6

5.1 Audit procedure – Sales...................................................................................................6

5.2 Audit procedure – Cost of sales.......................................................................................7

5.3 Audit procedure – Depreciation.......................................................................................7

Table of Contents

1.0 Preliminary judgement for materiality............................................................................2

2.0 Analytical review............................................................................................................3

3.0 Analytical review through trend analysis.............................................................................3

4.0 Accounts under material misstatement................................................................................4

4.1.1 First account selected – Sales........................................................................................4

4.1.2 Rational for selection....................................................................................................4

4.1.3 Assertion and explanation.............................................................................................4

4.2 Second account selected – Cost of sales......................................................................4

4.2.1 Rational for selection...............................................................................................4

4.2.2 Assertion and explanation........................................................................................5

4.3 Third account selected – Depreciation.............................................................................5

4.3.1 Rational for selection....................................................................................................5

4.3.2 Assertion and explanation.............................................................................................5

4.4 Fourth account selected – Wages.....................................................................................6

4.4.1 Rational for selection....................................................................................................6

4.4.2 Assertion and explanation.............................................................................................6

5.0 Recommended audit procedure............................................................................................6

5.1 Audit procedure – Sales...................................................................................................6

5.2 Audit procedure – Cost of sales.......................................................................................7

5.3 Audit procedure – Depreciation.......................................................................................7

2ISSUES IN AUDITING PRACTICE

5.4 Audit procedure – wages..................................................................................................7

6.0 Fraud....................................................................................................................................8

Reference....................................................................................................................................9

5.4 Audit procedure – wages..................................................................................................7

6.0 Fraud....................................................................................................................................8

Reference....................................................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ISSUES IN AUDITING PRACTICE

1.0 Preliminary judgement for materiality

Preliminary judgement is the maximum amount the auditor can accept the

misstatement that will not have material impact on the decision provided by the auditor for

the users of financial statements. As materiality is a relative factor it is important that it must

have a base to establish the fact that whether the misstatement is material or immaterial. Base

here is crucial as the users take their decisions based on that. Further, some of the

misstatements are more important as com-pared to others even if the amount is not big. For

instance, misstatements that involve fraud are likely to be more crucial to the users as

compared to the misstatement with regard to unintentional errors. However, the base varies

on the basis of business nature. Various bases used for establishing the level of materiality are

revenue, net income and total assets. Materiality level is established by taking into

consideration all the above mentioned factors (Eilifsen and Messier 2014).

If the quantitative factors are taken into consideration the materiality tolerance for

Cyclamen Enterprise will be 1% to 5% of sales that is $ 197,950 *1% = $ 1979.50 to $

197,950 * 5% = $ 9,897.51. Further, 50% to 75% of the materiality amount will be

considered as tolerable misstatement. Therefore, in case of Cyclamen Enterprise tolerable

misstatement will be amounted to around $ 5000. As per the auditor the preliminary

assessment for materiality shall be set at $ 15,000. However, as per the calculation the

materiality shall be set at $ 5,000 (Legoria, Melendrez and Reynolds 2013). If the materiality

level is reduced the auditor will have to check more items as per the level of tolerable

misstatement. Hence, with changes of materiality amount in case of Cyclamen Enterprise the

audit budget will increase as the auditor will be required to check more items.

1.0 Preliminary judgement for materiality

Preliminary judgement is the maximum amount the auditor can accept the

misstatement that will not have material impact on the decision provided by the auditor for

the users of financial statements. As materiality is a relative factor it is important that it must

have a base to establish the fact that whether the misstatement is material or immaterial. Base

here is crucial as the users take their decisions based on that. Further, some of the

misstatements are more important as com-pared to others even if the amount is not big. For

instance, misstatements that involve fraud are likely to be more crucial to the users as

compared to the misstatement with regard to unintentional errors. However, the base varies

on the basis of business nature. Various bases used for establishing the level of materiality are

revenue, net income and total assets. Materiality level is established by taking into

consideration all the above mentioned factors (Eilifsen and Messier 2014).

If the quantitative factors are taken into consideration the materiality tolerance for

Cyclamen Enterprise will be 1% to 5% of sales that is $ 197,950 *1% = $ 1979.50 to $

197,950 * 5% = $ 9,897.51. Further, 50% to 75% of the materiality amount will be

considered as tolerable misstatement. Therefore, in case of Cyclamen Enterprise tolerable

misstatement will be amounted to around $ 5000. As per the auditor the preliminary

assessment for materiality shall be set at $ 15,000. However, as per the calculation the

materiality shall be set at $ 5,000 (Legoria, Melendrez and Reynolds 2013). If the materiality

level is reduced the auditor will have to check more items as per the level of tolerable

misstatement. Hence, with changes of materiality amount in case of Cyclamen Enterprise the

audit budget will increase as the auditor will be required to check more items.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ISSUES IN AUDITING PRACTICE

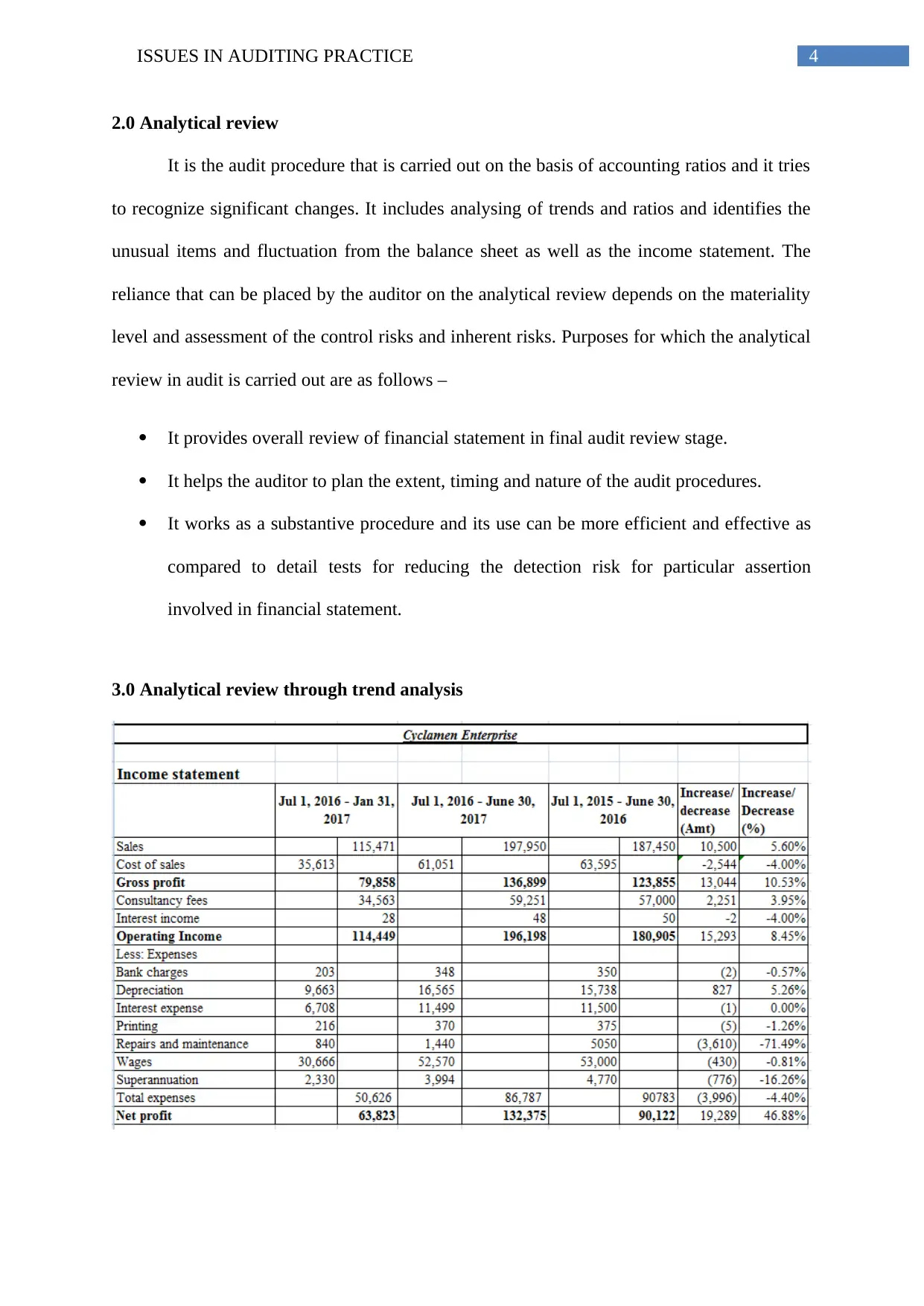

2.0 Analytical review

It is the audit procedure that is carried out on the basis of accounting ratios and it tries

to recognize significant changes. It includes analysing of trends and ratios and identifies the

unusual items and fluctuation from the balance sheet as well as the income statement. The

reliance that can be placed by the auditor on the analytical review depends on the materiality

level and assessment of the control risks and inherent risks. Purposes for which the analytical

review in audit is carried out are as follows –

It provides overall review of financial statement in final audit review stage.

It helps the auditor to plan the extent, timing and nature of the audit procedures.

It works as a substantive procedure and its use can be more efficient and effective as

compared to detail tests for reducing the detection risk for particular assertion

involved in financial statement.

3.0 Analytical review through trend analysis

2.0 Analytical review

It is the audit procedure that is carried out on the basis of accounting ratios and it tries

to recognize significant changes. It includes analysing of trends and ratios and identifies the

unusual items and fluctuation from the balance sheet as well as the income statement. The

reliance that can be placed by the auditor on the analytical review depends on the materiality

level and assessment of the control risks and inherent risks. Purposes for which the analytical

review in audit is carried out are as follows –

It provides overall review of financial statement in final audit review stage.

It helps the auditor to plan the extent, timing and nature of the audit procedures.

It works as a substantive procedure and its use can be more efficient and effective as

compared to detail tests for reducing the detection risk for particular assertion

involved in financial statement.

3.0 Analytical review through trend analysis

5ISSUES IN AUDITING PRACTICE

4.0 Accounts under material misstatement

4.1.1 First account selected – Sales

4.1.2 Rational for selection

Sales reflect the performance and activities of the company as the potential investors

and lenders assess the risks of their investments through the sales trends of the entity. In case

of Cyclamen Enterprise the sales revenue has been increased from $ 187,450 to $ 197,950

over last one year time period. Further, as different recognition method for sales revenue is

applied by different entities sales revenue must be verified for material misstatements.

4.1.3 Assertion and explanation

The auditor is mainly concerned about 3 types of material misstatements with regard

to sales – (i) sales made and recorded to the fictitious customers (ii) recognising the revenue

even if the goods have not yet been shipped or the service have not yet been provided and

(iii) goods are already shipped or the services are already provided but the revenue is not yet

recognized. The major assertion involves with the sales revenue transaction is accuracy

(Mock and Fukukawa 2015). The availability of authorized price list and trade terms

minimizes the inaccuracy risks. Therefore the assertion involve with sales revenue is that the

sales revenue transaction involves mathematical inaccuracy.

4.2 Second account selected – Cost of sales

4.2.1 Rational for selection

Cost of sales consumes maximum major proportion of the sales revenue. Further, the

other expenses of the entity are met from the amount left after meeting the cost of sales from

sales revenue. In case of Cyclamen Enterprise the cost of sales has been reduced from $

63,595 to $ 61,051 over last one year time period.

4.0 Accounts under material misstatement

4.1.1 First account selected – Sales

4.1.2 Rational for selection

Sales reflect the performance and activities of the company as the potential investors

and lenders assess the risks of their investments through the sales trends of the entity. In case

of Cyclamen Enterprise the sales revenue has been increased from $ 187,450 to $ 197,950

over last one year time period. Further, as different recognition method for sales revenue is

applied by different entities sales revenue must be verified for material misstatements.

4.1.3 Assertion and explanation

The auditor is mainly concerned about 3 types of material misstatements with regard

to sales – (i) sales made and recorded to the fictitious customers (ii) recognising the revenue

even if the goods have not yet been shipped or the service have not yet been provided and

(iii) goods are already shipped or the services are already provided but the revenue is not yet

recognized. The major assertion involves with the sales revenue transaction is accuracy

(Mock and Fukukawa 2015). The availability of authorized price list and trade terms

minimizes the inaccuracy risks. Therefore the assertion involve with sales revenue is that the

sales revenue transaction involves mathematical inaccuracy.

4.2 Second account selected – Cost of sales

4.2.1 Rational for selection

Cost of sales consumes maximum major proportion of the sales revenue. Further, the

other expenses of the entity are met from the amount left after meeting the cost of sales from

sales revenue. In case of Cyclamen Enterprise the cost of sales has been reduced from $

63,595 to $ 61,051 over last one year time period.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ISSUES IN AUDITING PRACTICE

4.2.2 Assertion and explanation

Generally, the cost of sales increases with the increase in sales revenue and number of

products or services sold and in the contrary it reduces with the reduction in sales revenue

and number of products or services sold. However, the situation may be changed if the

product or service selling prices have been enhanced or the company made any mistake in

recording the COGS under appropriate period (Antonio 2014). Therefore, the assertion

associated with COGS is cut-off that is the COGS is not recorded under correct accounting

period.

4.3 Third account selected – Depreciation

4.3.1 Rational for selection

Depreciation amount increases when the entity purchases any new asset or the entity

has changed the method of depreciation. It is found from the income statement of Cyclamen

Enterprise the cost of sales has been reduced from $ 63,595 to $ 61,051 over last one year

time period. However, no new purchase was found in case of the fixed asset from the trial

balance.

4.3.2 Assertion and explanation

As it is found that the depreciation is increased though any new asset has not been

purchased, likelihood is there that the company changed the depreciation charging method or

misstated the amount. Assertion may involve in case of depreciation is occurrence that is the

the depreciation recorded for all the assets are recorded for correct accounting period.

Another assertion involves here is cut-off that is the depreciation is charged for proper

accounts (Titera 2013).

4.2.2 Assertion and explanation

Generally, the cost of sales increases with the increase in sales revenue and number of

products or services sold and in the contrary it reduces with the reduction in sales revenue

and number of products or services sold. However, the situation may be changed if the

product or service selling prices have been enhanced or the company made any mistake in

recording the COGS under appropriate period (Antonio 2014). Therefore, the assertion

associated with COGS is cut-off that is the COGS is not recorded under correct accounting

period.

4.3 Third account selected – Depreciation

4.3.1 Rational for selection

Depreciation amount increases when the entity purchases any new asset or the entity

has changed the method of depreciation. It is found from the income statement of Cyclamen

Enterprise the cost of sales has been reduced from $ 63,595 to $ 61,051 over last one year

time period. However, no new purchase was found in case of the fixed asset from the trial

balance.

4.3.2 Assertion and explanation

As it is found that the depreciation is increased though any new asset has not been

purchased, likelihood is there that the company changed the depreciation charging method or

misstated the amount. Assertion may involve in case of depreciation is occurrence that is the

the depreciation recorded for all the assets are recorded for correct accounting period.

Another assertion involves here is cut-off that is the depreciation is charged for proper

accounts (Titera 2013).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ISSUES IN AUDITING PRACTICE

4.4 Fourth account selected – Wages

4.4.1 Rational for selection

As wages forms a major portion of the operating expenses in case of any entity, the

wages shall be analysed properly. Further, as the wages involve payment for the employees

those are generally in big numbers likelihood is there the payment is been misstated for one

or more employees. It is found from the income statement of Cyclamen Enterprise the wages

has been reduced from $ 53,000 to $ 52,570 over last one year time period.

4.4.2 Assertion and explanation

As wage involves payment to number of employees, advance payment made to them

and arrear payment due to them, it give ample chance to the management to misstate the

wage payment. Further, as the amount of wage has been reduced as compared to the previous

year likelihood is there that 1 or more employee retired during the year or payment to some

employees are due or the amount has been misstated (Lessambo 2018). Therefore, the

assertion involves here is accuracy that amounts and data associated to wage record have

been appropriately recorded.

5.0 Recommended audit procedure

5.1 Audit procedure – Sales

For preventing the fictitious sale the company shall segregate the duties including the

billing function, order entry and shipping function. Further, it must be verified that the sales

are recorded with approved shipping order and customer order (Ruhnke and Schmidt 2014).

Further, to minimize the accuracy misstatement sales invoice shall be matched with customer

order and shipping document with details like mathematical accuracy, price of the product

and quantity. The sales invoices shall be verified with the sales report on daily basis.

4.4 Fourth account selected – Wages

4.4.1 Rational for selection

As wages forms a major portion of the operating expenses in case of any entity, the

wages shall be analysed properly. Further, as the wages involve payment for the employees

those are generally in big numbers likelihood is there the payment is been misstated for one

or more employees. It is found from the income statement of Cyclamen Enterprise the wages

has been reduced from $ 53,000 to $ 52,570 over last one year time period.

4.4.2 Assertion and explanation

As wage involves payment to number of employees, advance payment made to them

and arrear payment due to them, it give ample chance to the management to misstate the

wage payment. Further, as the amount of wage has been reduced as compared to the previous

year likelihood is there that 1 or more employee retired during the year or payment to some

employees are due or the amount has been misstated (Lessambo 2018). Therefore, the

assertion involves here is accuracy that amounts and data associated to wage record have

been appropriately recorded.

5.0 Recommended audit procedure

5.1 Audit procedure – Sales

For preventing the fictitious sale the company shall segregate the duties including the

billing function, order entry and shipping function. Further, it must be verified that the sales

are recorded with approved shipping order and customer order (Ruhnke and Schmidt 2014).

Further, to minimize the accuracy misstatement sales invoice shall be matched with customer

order and shipping document with details like mathematical accuracy, price of the product

and quantity. The sales invoices shall be verified with the sales report on daily basis.

8ISSUES IN AUDITING PRACTICE

5.2 Audit procedure – Cost of sales

For auditing the COGS the auditor shall perform the predictive test for each product

line, business segments or divisions through reference of details with regard to the average

unit cost and units shipped. Investigation shall be made for any difference in recorded

amounts and predicted amounts. Vouchers related to COGS shall be traced through unit costs

used for releasing the inventory under the cost records (Kogan et al. 2014). Further, the

auditor shall check that the COGS have been charged to appropriate period under which the

sales are made.

5.3 Audit procedure – Depreciation

The auditor while auditing the depreciation must analyse the internal control related to

the assets on which the depreciations have been charged. The key controls those are

important for the auditors to check upon are the asset purchase authorisation procedure,

amount involved in purchasing the assets, selling procedure and authorisation for asset,

purchase date of asset and depreciation method used for the asset (Choudhary, Merkley and

Schipper 2018). Further, the auditor must use his professional scepticism and select few

sample calculation for depreciation to check that there is no computation error. The auditor

may recalculate the depreciation for sample items, if required.

5.4 Audit procedure – wages

While auditing for wages the wage payment shall be matched with the employee

register with details of their names, amount of monthly wages, advance payment made to

them and arrear payment made or due to any employee. The auditor shall verify the entire

payment voucher with the employee register (Christensen, Glover and Wood 2013). Further,

if any new employee is engaged or retired during the year payment made to the new

employee and stoppage of payment for retired employee shall be checked appropriately.

5.2 Audit procedure – Cost of sales

For auditing the COGS the auditor shall perform the predictive test for each product

line, business segments or divisions through reference of details with regard to the average

unit cost and units shipped. Investigation shall be made for any difference in recorded

amounts and predicted amounts. Vouchers related to COGS shall be traced through unit costs

used for releasing the inventory under the cost records (Kogan et al. 2014). Further, the

auditor shall check that the COGS have been charged to appropriate period under which the

sales are made.

5.3 Audit procedure – Depreciation

The auditor while auditing the depreciation must analyse the internal control related to

the assets on which the depreciations have been charged. The key controls those are

important for the auditors to check upon are the asset purchase authorisation procedure,

amount involved in purchasing the assets, selling procedure and authorisation for asset,

purchase date of asset and depreciation method used for the asset (Choudhary, Merkley and

Schipper 2018). Further, the auditor must use his professional scepticism and select few

sample calculation for depreciation to check that there is no computation error. The auditor

may recalculate the depreciation for sample items, if required.

5.4 Audit procedure – wages

While auditing for wages the wage payment shall be matched with the employee

register with details of their names, amount of monthly wages, advance payment made to

them and arrear payment made or due to any employee. The auditor shall verify the entire

payment voucher with the employee register (Christensen, Glover and Wood 2013). Further,

if any new employee is engaged or retired during the year payment made to the new

employee and stoppage of payment for retired employee shall be checked appropriately.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ISSUES IN AUDITING PRACTICE

6.0 Fraud

The auditor is responsible for planning and performing the audit for obtaining

reasonable assurance that the financial statements are free from the material misstatements

owing to fraud or error (Power 2013). Fraud is the intentional and purposeful misstatement

committed to obtain some personal target. Frauds are committed to hide any fraudulent

activities or getting higher amount of incentives. Fraud is not just identifying unusual

transaction, however, auditors are also responsible to evaluate the behavioural patterns of

management as well as employees to check if any indication is there that may have impact on

the financial statements (Boyle, DeZoort and Hermanson 2015). Therefore, even if the staffs

are faithful there always remains the likelihood of fraud and therefore, the audit partner’s

suggestion is not appropriate.

6.0 Fraud

The auditor is responsible for planning and performing the audit for obtaining

reasonable assurance that the financial statements are free from the material misstatements

owing to fraud or error (Power 2013). Fraud is the intentional and purposeful misstatement

committed to obtain some personal target. Frauds are committed to hide any fraudulent

activities or getting higher amount of incentives. Fraud is not just identifying unusual

transaction, however, auditors are also responsible to evaluate the behavioural patterns of

management as well as employees to check if any indication is there that may have impact on

the financial statements (Boyle, DeZoort and Hermanson 2015). Therefore, even if the staffs

are faithful there always remains the likelihood of fraud and therefore, the audit partner’s

suggestion is not appropriate.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ISSUES IN AUDITING PRACTICE

Reference

Antonio, G.R., 2014. Continuous auditing: Developing automated audit systems for fraud and

error detections. Journal of Economics, Business & Accountancy Ventura, 17(1), pp.127-144.

Boyle, D.M., DeZoort, F.T. and Hermanson, D.R., 2015. The effect of alternative fraud

model use on auditors’ fraud risk judgments. Journal of Accounting and Public Policy, 34(6),

pp.578-596.

Choudhary, P., Merkley, K.J. and Schipper, K., 2018. Auditors’ Quantitative Materiality

Judgments: Properties and Implications for Financial Reporting Reliability.

Christensen, B.E., Glover, S.M. and Wood, D.A., 2013. Extreme estimation uncertainty and

audit assurance. Current Issues in Auditing, 7(1), pp.P36-P42.

Eilifsen, A. and Messier Jr, W.F., 2014. Materiality guidance of the major public accounting

firms. Auditing: A Journal of Practice & Theory, 34(2), pp.3-26.

Kogan, A., Alles, M.G., Vasarhelyi, M.A. and Wu, J., 2014. Design and evaluation of a

continuous data level auditing system. Auditing: A Journal of Practice & Theory, 33(4),

pp.221-245.

Legoria, J., Melendrez, K.D. and Reynolds, J.K., 2013. Qualitative audit materiality and

earnings management. Review of Accounting Studies, 18(2), pp.414-442.

Lessambo, F.I., 2018. Audit Risks: Identification and Procedures. In Auditing, Assurance

Services, and Forensics(pp. 183-202). Palgrave Macmillan, Cham.

Mock, T.J. and Fukukawa, H., 2015. Auditors' risk assessments: The effects of elicitation

approach and assertion framing. Behavioral Research in Accounting, 28(2), pp.75-84.

Reference

Antonio, G.R., 2014. Continuous auditing: Developing automated audit systems for fraud and

error detections. Journal of Economics, Business & Accountancy Ventura, 17(1), pp.127-144.

Boyle, D.M., DeZoort, F.T. and Hermanson, D.R., 2015. The effect of alternative fraud

model use on auditors’ fraud risk judgments. Journal of Accounting and Public Policy, 34(6),

pp.578-596.

Choudhary, P., Merkley, K.J. and Schipper, K., 2018. Auditors’ Quantitative Materiality

Judgments: Properties and Implications for Financial Reporting Reliability.

Christensen, B.E., Glover, S.M. and Wood, D.A., 2013. Extreme estimation uncertainty and

audit assurance. Current Issues in Auditing, 7(1), pp.P36-P42.

Eilifsen, A. and Messier Jr, W.F., 2014. Materiality guidance of the major public accounting

firms. Auditing: A Journal of Practice & Theory, 34(2), pp.3-26.

Kogan, A., Alles, M.G., Vasarhelyi, M.A. and Wu, J., 2014. Design and evaluation of a

continuous data level auditing system. Auditing: A Journal of Practice & Theory, 33(4),

pp.221-245.

Legoria, J., Melendrez, K.D. and Reynolds, J.K., 2013. Qualitative audit materiality and

earnings management. Review of Accounting Studies, 18(2), pp.414-442.

Lessambo, F.I., 2018. Audit Risks: Identification and Procedures. In Auditing, Assurance

Services, and Forensics(pp. 183-202). Palgrave Macmillan, Cham.

Mock, T.J. and Fukukawa, H., 2015. Auditors' risk assessments: The effects of elicitation

approach and assertion framing. Behavioral Research in Accounting, 28(2), pp.75-84.

11ISSUES IN AUDITING PRACTICE

Power, M., 2013. The apparatus of fraud risk. Accounting, Organizations and Society, 38(6-

7), pp.525-543.

Ruhnke, K. and Schmidt, M., 2014. Misstatements in financial statements: The relationship

between inherent and control risk factors and audit adjustments. Auditing: A Journal of

Practice & Theory, 33(4), pp.247-269.

Titera, W.R., 2013. Updating audit standard—Enabling audit data analysis. Journal of

Information Systems, 27(1), pp.325-331.

Power, M., 2013. The apparatus of fraud risk. Accounting, Organizations and Society, 38(6-

7), pp.525-543.

Ruhnke, K. and Schmidt, M., 2014. Misstatements in financial statements: The relationship

between inherent and control risk factors and audit adjustments. Auditing: A Journal of

Practice & Theory, 33(4), pp.247-269.

Titera, W.R., 2013. Updating audit standard—Enabling audit data analysis. Journal of

Information Systems, 27(1), pp.325-331.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.