Financial Accounting: Qualitative Characteristics and Materiality

VerifiedAdded on 2021/04/16

|6

|1347

|146

Report

AI Summary

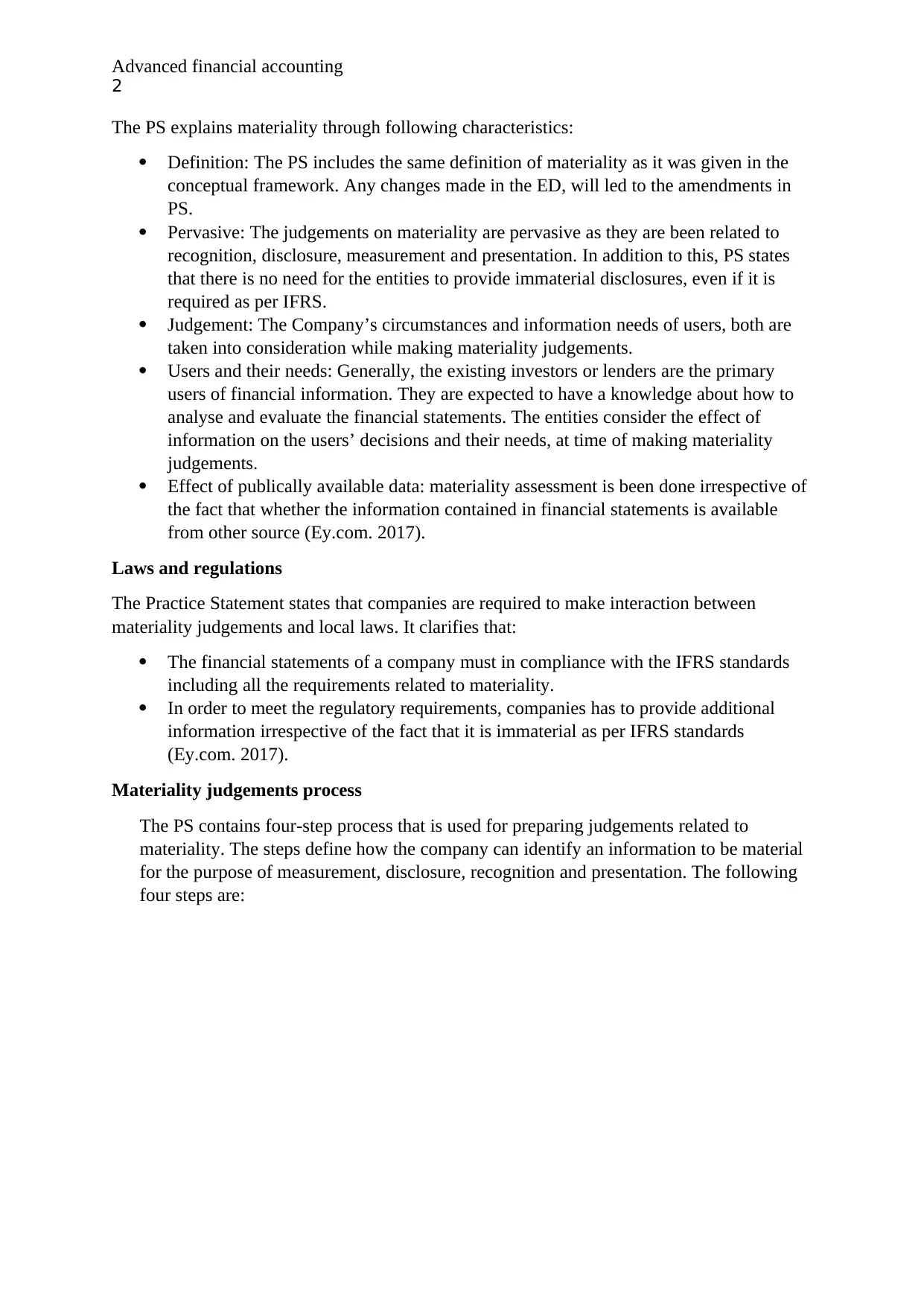

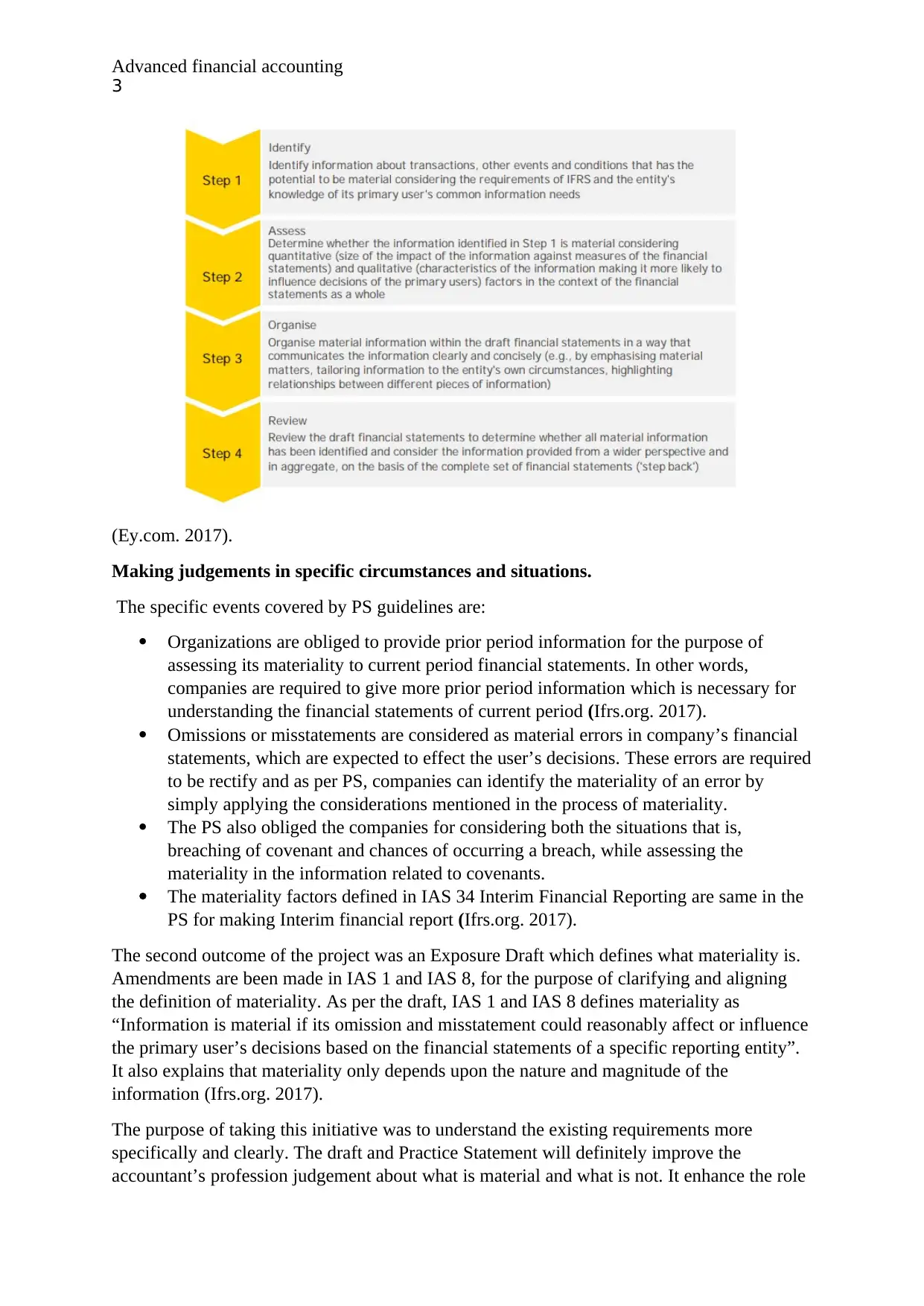

This report delves into the concept of materiality within the framework of advanced financial accounting. It begins by defining materiality as a key aspect of relevance, emphasizing its role in influencing the decisions of financial statement users. The report references IAS 1 and IAS 8 to underscore the importance of data that can alter user decisions. It then examines the IFRS Practice Statement 2 and Exposure Draft on materiality, detailing the characteristics, including definition, pervasiveness, and the role of judgment. The report outlines the four-step process for making materiality judgments, covering specific situations like prior period information and errors. It also touches upon the amendments to IAS 1 and IAS 8, which aim to clarify the definition of materiality. The report concludes by highlighting the benefits of these initiatives, such as improved accountant judgment and enhanced decision-making for stakeholders.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.