Managerial Finance Report: Matheson Electronics Case Study Analysis

VerifiedAdded on 2023/03/30

|18

|3462

|484

Report

AI Summary

This report analyzes the financial feasibility of Matheson Electronics launching a new electronic device. It employs various investment appraisal techniques such as Net Present Value (NPV), Payback Method, Internal Rate of Return (IRR), and Accounting Rate of Return (ARR) to evaluate the project's profitability. The report also explores sources of finance, breakeven analysis, margin of safety, and cash budgeting to assess the financial risks and returns. Furthermore, it includes performance evaluations, and considers other crucial issues. The analysis reveals a negative NPV, indicating the project's potential unprofitability, though ARR suggests some returns. The report also includes detailed calculations and interpretations of each financial metric, providing a comprehensive overview of the project's financial implications and recommendations.

Running Head: Managerial Finance

Managerial Finance

Contents

Managerial Finance

Contents

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Managerial Finance

1. Executive Summary....................................................................................................................2

2. Introduction..................................................................................................................................2

3. Investment Appraisal Technique...............................................................................................2

3.1 Net Present Value (NPV)...................................................................................................2

3.2 Payback Method..................................................................................................................3

3.3 Internal Rate of Return (IRR).............................................................................................4

3.4 Accounting Rate of Return (ARR).....................................................................................4

4. Sources of Finance.....................................................................................................................5

4.1 Personal Finance.....................................................................................................................5

4.2 Internal Source of Finance......................................................................................................5

4.3 External Source of Finance.....................................................................................................5

a) Equity Financing..................................................................................................................5

b) Debt Financing....................................................................................................................5

5. Breakeven Analysis....................................................................................................................6

5.1 Margin of Safety..................................................................................................................6

6. Cash Budget................................................................................................................................6

7. Performance Evaluation of Lily Wholesale Company............................................................7

8. Issues to be considered by Matheson Electronics.................................................................8

9. Conclusion...................................................................................................................................8

10. References.............................................................................................................................10

11. Appendix................................................................................................................................11

11.1 Calculation of Net Present Value.......................................................................................11

11.2 Payback Method...................................................................................................................12

11.3 Internal Rate of Return........................................................................................................13

11.4 Accounting Rate of Return..................................................................................................13

11.5 Breakeven Analysis.............................................................................................................14

11.6 Margin of Safety...................................................................................................................14

11.7 Cash Budget.........................................................................................................................15

11.8 Income Statement................................................................................................................16

1

1. Executive Summary....................................................................................................................2

2. Introduction..................................................................................................................................2

3. Investment Appraisal Technique...............................................................................................2

3.1 Net Present Value (NPV)...................................................................................................2

3.2 Payback Method..................................................................................................................3

3.3 Internal Rate of Return (IRR).............................................................................................4

3.4 Accounting Rate of Return (ARR).....................................................................................4

4. Sources of Finance.....................................................................................................................5

4.1 Personal Finance.....................................................................................................................5

4.2 Internal Source of Finance......................................................................................................5

4.3 External Source of Finance.....................................................................................................5

a) Equity Financing..................................................................................................................5

b) Debt Financing....................................................................................................................5

5. Breakeven Analysis....................................................................................................................6

5.1 Margin of Safety..................................................................................................................6

6. Cash Budget................................................................................................................................6

7. Performance Evaluation of Lily Wholesale Company............................................................7

8. Issues to be considered by Matheson Electronics.................................................................8

9. Conclusion...................................................................................................................................8

10. References.............................................................................................................................10

11. Appendix................................................................................................................................11

11.1 Calculation of Net Present Value.......................................................................................11

11.2 Payback Method...................................................................................................................12

11.3 Internal Rate of Return........................................................................................................13

11.4 Accounting Rate of Return..................................................................................................13

11.5 Breakeven Analysis.............................................................................................................14

11.6 Margin of Safety...................................................................................................................14

11.7 Cash Budget.........................................................................................................................15

11.8 Income Statement................................................................................................................16

1

Managerial Finance

1. Executive Summary

This project is prepared to assist Matheson Electronics with the decision of selecting

or rejecting the project of launching a new electronic device which could measure

miles an automobile could cover in per gallon of gasoline. Analysis has shown that

company could launch the project as a result of positive NPV and acceptable level of

Accounting Rate of Return. The other reason of selecting the project is that it would

help company in reaping more profit because there are no competitors in the market.

2. Introduction

Every business needs capital to meet its long term needs like expansion, acquisition

of another company or to enter all new market. These funds are required for meeting

the needs arising in day to day business operations which are considered as short-

term needs. So now when the fund is so important for any business organisation,

they think twice before investing in any project. To avoid the risk of loss arising from

the investment done in the project the company employs the investment appraisal

techniques like NPV, IRR, and Payback Period etc. to check the profitability of the

project. To avoid the risk associated with the sales and market variability the

company often carries out the breakeven analysis and calculates margin of safety.

3. Investment Appraisal Technique

3.1 Net Present Value (NPV)

Net Present value is usually employed in the investment industry to make a

proper valuation of the project (Bell, 2017).NPV is used to estimate the return

on the amount invested in the project and then the return is converted into

dollar value of today. This helps the company in understanding whether the

project worth the investment or not. It helps the company in knowing whether

the investment would actually increase the value of the firm or not. The best

part of using NPV as an investment appraisal technique is it consider time

value of money, all the cash flows and also the risks associated with the

future cash flows. There are certain reasons which make the NPV less

attractive. The calculations involved in the NPV are very complex in nature

like estimation of cost of capital. There are certain assumptions which are

2

1. Executive Summary

This project is prepared to assist Matheson Electronics with the decision of selecting

or rejecting the project of launching a new electronic device which could measure

miles an automobile could cover in per gallon of gasoline. Analysis has shown that

company could launch the project as a result of positive NPV and acceptable level of

Accounting Rate of Return. The other reason of selecting the project is that it would

help company in reaping more profit because there are no competitors in the market.

2. Introduction

Every business needs capital to meet its long term needs like expansion, acquisition

of another company or to enter all new market. These funds are required for meeting

the needs arising in day to day business operations which are considered as short-

term needs. So now when the fund is so important for any business organisation,

they think twice before investing in any project. To avoid the risk of loss arising from

the investment done in the project the company employs the investment appraisal

techniques like NPV, IRR, and Payback Period etc. to check the profitability of the

project. To avoid the risk associated with the sales and market variability the

company often carries out the breakeven analysis and calculates margin of safety.

3. Investment Appraisal Technique

3.1 Net Present Value (NPV)

Net Present value is usually employed in the investment industry to make a

proper valuation of the project (Bell, 2017).NPV is used to estimate the return

on the amount invested in the project and then the return is converted into

dollar value of today. This helps the company in understanding whether the

project worth the investment or not. It helps the company in knowing whether

the investment would actually increase the value of the firm or not. The best

part of using NPV as an investment appraisal technique is it consider time

value of money, all the cash flows and also the risks associated with the

future cash flows. There are certain reasons which make the NPV less

attractive. The calculations involved in the NPV are very complex in nature

like estimation of cost of capital. There are certain assumptions which are

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Managerial Finance

taken while computing NPV of any project. Management of the company

needs to take the assumptions in respect of dollar amount as well as timing of

the future cash flows related with the project. Interest rates for the project’s

duration are also assumed. The problem lies in the fact that these

assumptions could or could not be realistic in nature.

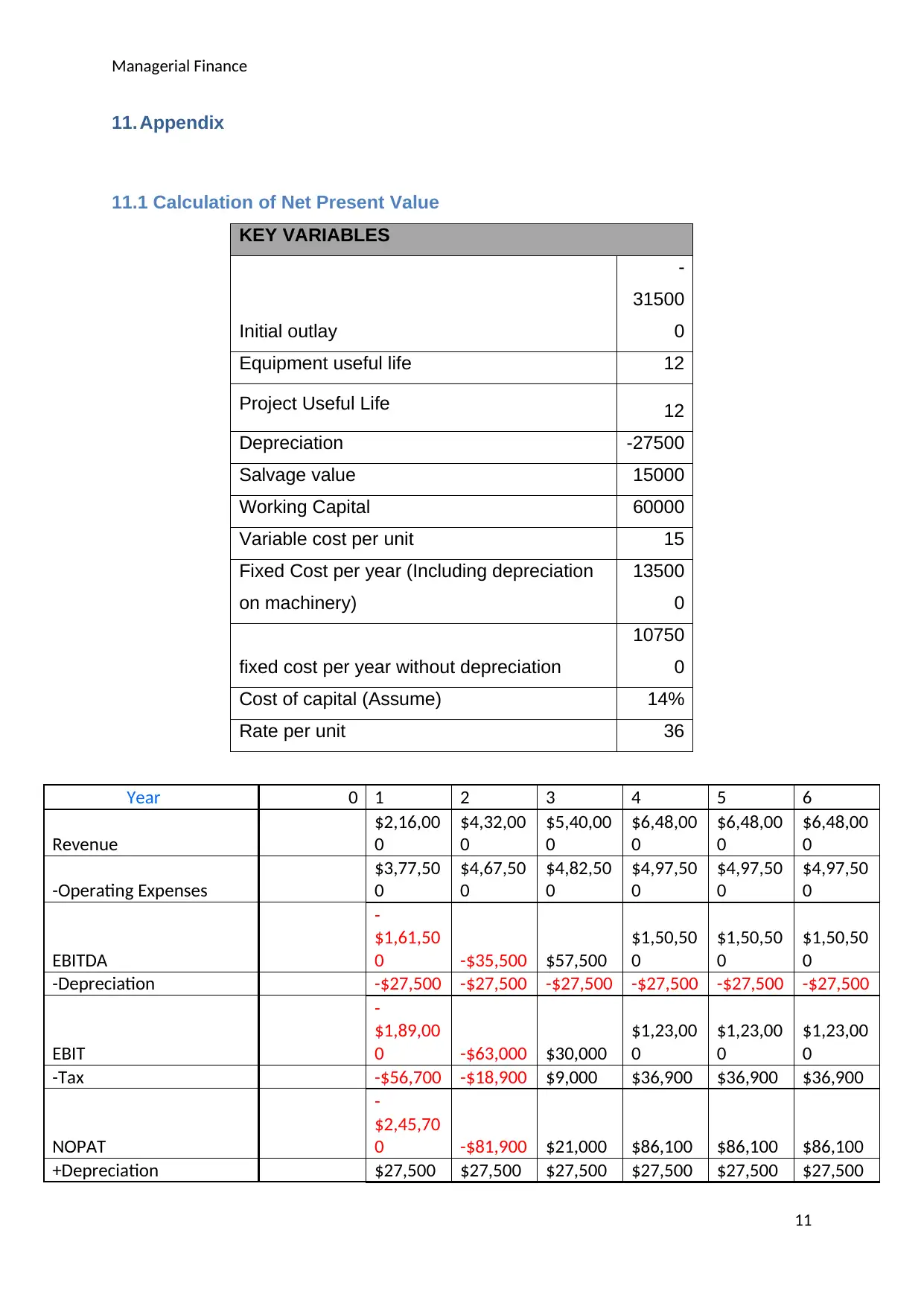

The net present value of the project stands at $-180688 (Appendix

11.1).Since, NPV of the project of launching an electronic device of the

company Matheson Electronics is negative we may interpret that the cash

inflow or the revenues to be generated from the project will be lower than the

cost incurred on the project execution. So, the company should not go ahead

with the project launch.

The Matheson Electronics may also go for other methods like Payback

method, Accounting Rate of Return and Internal Rate of return for the project

evaluation.

3.2 Payback Method

The payback period is a very appropriate measure to know about the

duration of time the invested amount in the project would stay at risk. It is

time period in which the investment done in the asset or in a project starts

giving the return. The projects with a shorter payback period are usually

considered and those with longer payback period are rejected.

In case of Matheson Electronics the payback period is coming out to be 7.75

years (Appendix 11.2) which means the amount invested in the launch of new

electronic device will start giving returns after 7.75 years.

However there are certain drawbacks of using this method. First, it does not

consider the life span of the asset and therefore the investor does not come

to know about whether payback period is just before the expiry of asset’s life

or just after the asset’s useful life. The main motive of investment is to earn

profit and every investor wants to know about whether the investment will be

profitable or not. Payback only considers the time period in which the initial

investment will be return by the project but it ignores the element of overall

profitability.

3

taken while computing NPV of any project. Management of the company

needs to take the assumptions in respect of dollar amount as well as timing of

the future cash flows related with the project. Interest rates for the project’s

duration are also assumed. The problem lies in the fact that these

assumptions could or could not be realistic in nature.

The net present value of the project stands at $-180688 (Appendix

11.1).Since, NPV of the project of launching an electronic device of the

company Matheson Electronics is negative we may interpret that the cash

inflow or the revenues to be generated from the project will be lower than the

cost incurred on the project execution. So, the company should not go ahead

with the project launch.

The Matheson Electronics may also go for other methods like Payback

method, Accounting Rate of Return and Internal Rate of return for the project

evaluation.

3.2 Payback Method

The payback period is a very appropriate measure to know about the

duration of time the invested amount in the project would stay at risk. It is

time period in which the investment done in the asset or in a project starts

giving the return. The projects with a shorter payback period are usually

considered and those with longer payback period are rejected.

In case of Matheson Electronics the payback period is coming out to be 7.75

years (Appendix 11.2) which means the amount invested in the launch of new

electronic device will start giving returns after 7.75 years.

However there are certain drawbacks of using this method. First, it does not

consider the life span of the asset and therefore the investor does not come

to know about whether payback period is just before the expiry of asset’s life

or just after the asset’s useful life. The main motive of investment is to earn

profit and every investor wants to know about whether the investment will be

profitable or not. Payback only considers the time period in which the initial

investment will be return by the project but it ignores the element of overall

profitability.

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Managerial Finance

3.3 Internal Rate of Return (IRR)

The calculation of internal rate of Return is one of the significant tools used

for project selection. It computes the amount of profit that a company would

generate in future course taking time value of money into consideration.

Internal Rate of Return tries to find the discount rate at which the present

value of cash flows relating to future will become zero (Bizfluent, 2017).

Higher the IRR of any project better is the probability of the business to be

successful.

Now, looking at the Matheson Electronics’ IRR, then it is 9% (Appendix 11.3).

Interpreting the project solely on the basis of IRR is never a good idea as it

may lead the investor to invest in a wrong project. For example, there are two

projects, Project A of one year with IRR 20% and Project B of 15years with

IRR of 15%. If the investor will consider the selection or rejection of any

project basing on IRR then he would definitely choose Project A as it has a

greater IRR than Project B. But, if we look at the time duration of both the

project then Project A will last only for one year thereby will give a return of

20% only for a year however Project B is for 13 years which would give the

investor a return of 13% for 13 years. Such facts are not considered in the

IRR calculation (Harvard Business Review, 2016).

3.4 Accounting Rate of Return (ARR)

In the Accounting rate of return (ARR), the project is selected or rejected on

the basis of net income from the projects rather than basing the decision

upon cash flows from the projects (Cengage, n.d.). Average Rate of return

tells the investor about the return given by the project on every dollar

invested.

The project with which Matheson Electronics’ wants to proceed with has an

Average rate of return of 15% (Appendix 11.4). It means for every dollar

invested by the company into this project will get a return of 15%.

The problem with Average accounting return is it does not consider the time

value of money. It also ignores the timings of profit as it uses the profit

average while making calculation (Scottish Qualifications Authority,n.d.).

4

3.3 Internal Rate of Return (IRR)

The calculation of internal rate of Return is one of the significant tools used

for project selection. It computes the amount of profit that a company would

generate in future course taking time value of money into consideration.

Internal Rate of Return tries to find the discount rate at which the present

value of cash flows relating to future will become zero (Bizfluent, 2017).

Higher the IRR of any project better is the probability of the business to be

successful.

Now, looking at the Matheson Electronics’ IRR, then it is 9% (Appendix 11.3).

Interpreting the project solely on the basis of IRR is never a good idea as it

may lead the investor to invest in a wrong project. For example, there are two

projects, Project A of one year with IRR 20% and Project B of 15years with

IRR of 15%. If the investor will consider the selection or rejection of any

project basing on IRR then he would definitely choose Project A as it has a

greater IRR than Project B. But, if we look at the time duration of both the

project then Project A will last only for one year thereby will give a return of

20% only for a year however Project B is for 13 years which would give the

investor a return of 13% for 13 years. Such facts are not considered in the

IRR calculation (Harvard Business Review, 2016).

3.4 Accounting Rate of Return (ARR)

In the Accounting rate of return (ARR), the project is selected or rejected on

the basis of net income from the projects rather than basing the decision

upon cash flows from the projects (Cengage, n.d.). Average Rate of return

tells the investor about the return given by the project on every dollar

invested.

The project with which Matheson Electronics’ wants to proceed with has an

Average rate of return of 15% (Appendix 11.4). It means for every dollar

invested by the company into this project will get a return of 15%.

The problem with Average accounting return is it does not consider the time

value of money. It also ignores the timings of profit as it uses the profit

average while making calculation (Scottish Qualifications Authority,n.d.).

4

Managerial Finance

4. Sources of Finance

In order to run the business successfully the companies are required to meet their

working capital needs and also their long term needs for which they require a

extensive amount of capital. There are various ways and sources through which the

companies fulfil their needs of meeting the capital needs.

4.1 Personal Finance

The first thing and first source of finance which every business owner could find is

his own funds. Most of the start-up companies choose to finance their business with

the amount they have with them as their savings. Personal finance also includes the

borrowed funds from friends, relatives, personal loans from financial institutions etc.

4.2 Internal Source of Finance

Internal Source of finance is nothing but the accumulated funds maintained by the

company in the form of retained earnings, depreciation provisions, deferred taxation

etc.

4.3 External Source of Finance

There are usually two external sources of finance, one is the debt financing and the

other is equity financing. These two sources very popular sources of finance and are

also used very frequently and extensively by the business firms.

a) Equity Financing

Equity financing refers to the process of raising funds through the issue of shares to

the persons who are contributing funds and they are known as shareholders of the

company. They enjoy the ownership of the company to the extent of share held by

them. The shareholders receive the dividend at the time when company earns the

profit. However, company is not liable to pay dividends to the shareholders in case of

low profit or at the time it incurred loss.

b) Debt Financing

There are times when the business entities with good record of earnings over the

year and with good market reputation and goodwill often search for raising money

through outside sources in order to meet their capital needs. For meeting this need

companies issue debentures to the persons who lend money and for this lent

amount the company is liable to pay a fixed rate of interest to the debenture holders

5

4. Sources of Finance

In order to run the business successfully the companies are required to meet their

working capital needs and also their long term needs for which they require a

extensive amount of capital. There are various ways and sources through which the

companies fulfil their needs of meeting the capital needs.

4.1 Personal Finance

The first thing and first source of finance which every business owner could find is

his own funds. Most of the start-up companies choose to finance their business with

the amount they have with them as their savings. Personal finance also includes the

borrowed funds from friends, relatives, personal loans from financial institutions etc.

4.2 Internal Source of Finance

Internal Source of finance is nothing but the accumulated funds maintained by the

company in the form of retained earnings, depreciation provisions, deferred taxation

etc.

4.3 External Source of Finance

There are usually two external sources of finance, one is the debt financing and the

other is equity financing. These two sources very popular sources of finance and are

also used very frequently and extensively by the business firms.

a) Equity Financing

Equity financing refers to the process of raising funds through the issue of shares to

the persons who are contributing funds and they are known as shareholders of the

company. They enjoy the ownership of the company to the extent of share held by

them. The shareholders receive the dividend at the time when company earns the

profit. However, company is not liable to pay dividends to the shareholders in case of

low profit or at the time it incurred loss.

b) Debt Financing

There are times when the business entities with good record of earnings over the

year and with good market reputation and goodwill often search for raising money

through outside sources in order to meet their capital needs. For meeting this need

companies issue debentures to the persons who lend money and for this lent

amount the company is liable to pay a fixed rate of interest to the debenture holders

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Managerial Finance

irrespective of whether the firm has earned profit or has incurred loss (Business

Management Ideas, n.d.).

5. Breakeven Analysis

Breakeven Analysis is the tool usually employed by the management of the company

and the management accountants. It gives them an idea about the level of sale at

which the income of the project equals the cost incurred on the project (Business,

2018). The breakeven analysis for the Matheson Electronics had been shown in

Appendix 11.5. From the table we could see that when the company will sell

5119(approx.) units of the electronic device (Device which Matheson Electronic is

planning to launch) then it will be able to cover its total costs which stand at

$184285.7.

5.1 Margin of Safety

The margin of safety is calculated to quantify business risk. It shows the

percentage by which the company could witness a drop in its sales figure before

it actually starts to incur losses. Higher Margin of Safety is considered good as it

shows the capability of the company to withstand the changes taking place in

sales. In case the company’s sale would fall below the margin of safety then it

would have to face net loss for that particular year or period.

The Margin of Safety for the Matheson Electronics had been computed in

Appendix 11.6. From the table we could see the company would not face the loss

related to the sales variability till it produces and sells 189881 units of the

electronic device. Up to this unit the company is free from the risk. So if the

company will produce more than 189881 units then the company could witness

3% drop in its sales before it starts facing the loss.

6. Cash Budget

Cash Budget reflects the future cash position of the business organisation. It reflects

the future sources of receipts and also the prospect areas where the company would

require paying cash. For any business organisation liquidity matters the most even

more than earning profit. Usually the forecast made in the cash budget is for a period

6

irrespective of whether the firm has earned profit or has incurred loss (Business

Management Ideas, n.d.).

5. Breakeven Analysis

Breakeven Analysis is the tool usually employed by the management of the company

and the management accountants. It gives them an idea about the level of sale at

which the income of the project equals the cost incurred on the project (Business,

2018). The breakeven analysis for the Matheson Electronics had been shown in

Appendix 11.5. From the table we could see that when the company will sell

5119(approx.) units of the electronic device (Device which Matheson Electronic is

planning to launch) then it will be able to cover its total costs which stand at

$184285.7.

5.1 Margin of Safety

The margin of safety is calculated to quantify business risk. It shows the

percentage by which the company could witness a drop in its sales figure before

it actually starts to incur losses. Higher Margin of Safety is considered good as it

shows the capability of the company to withstand the changes taking place in

sales. In case the company’s sale would fall below the margin of safety then it

would have to face net loss for that particular year or period.

The Margin of Safety for the Matheson Electronics had been computed in

Appendix 11.6. From the table we could see the company would not face the loss

related to the sales variability till it produces and sells 189881 units of the

electronic device. Up to this unit the company is free from the risk. So if the

company will produce more than 189881 units then the company could witness

3% drop in its sales before it starts facing the loss.

6. Cash Budget

Cash Budget reflects the future cash position of the business organisation. It reflects

the future sources of receipts and also the prospect areas where the company would

require paying cash. For any business organisation liquidity matters the most even

more than earning profit. Usually the forecast made in the cash budget is for a period

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Managerial Finance

of one year however it is usually broken down in months or weeks which facilitates in

adding the variations taking place frequently (Financial Accountancy,n.d.).

There are certain advantages of cash budget like it helps the management in

meeting the future cash requirement, helps in taking the benefit of cash discount as

a result of making early payments due on accounts payable etc.

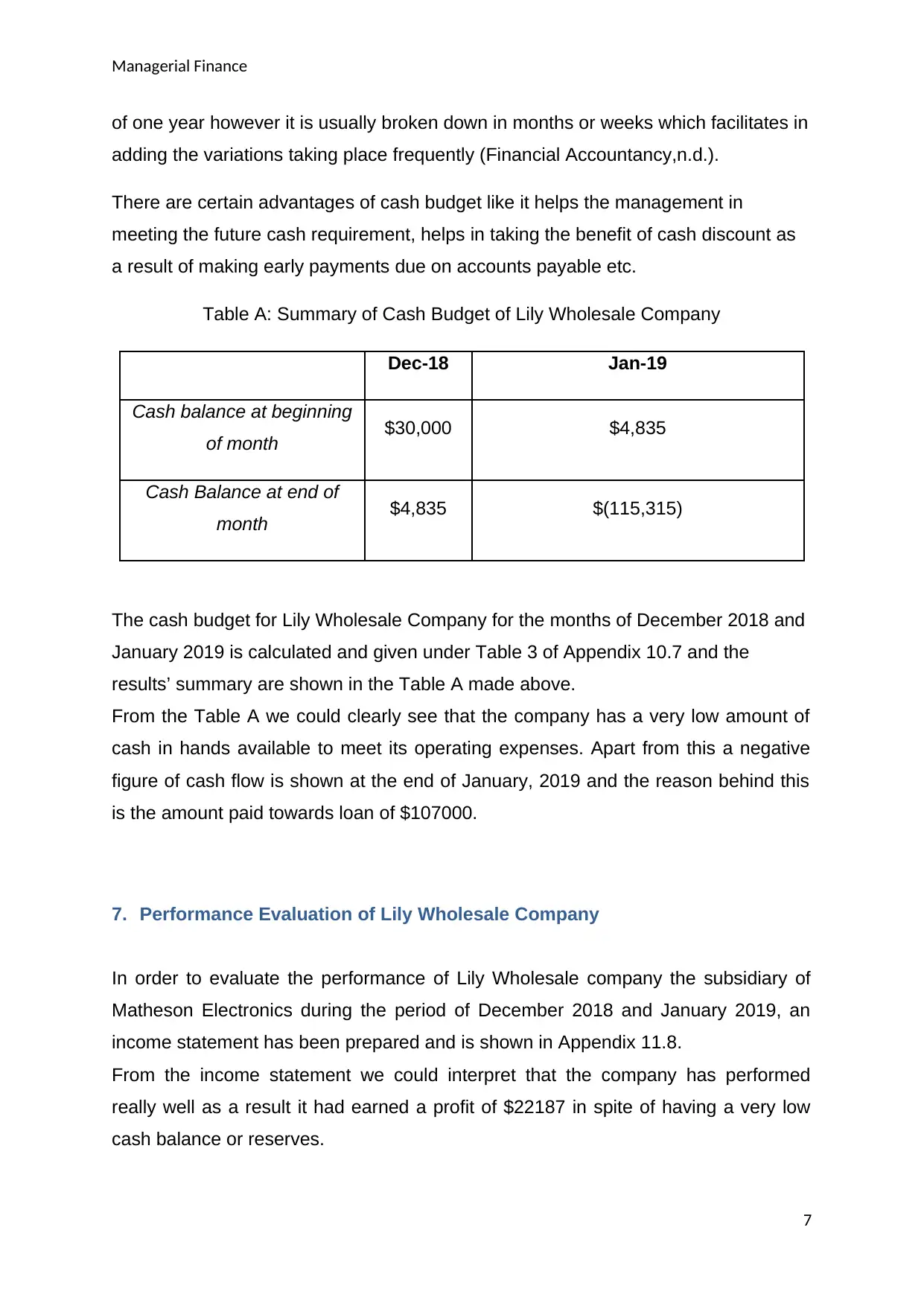

Table A: Summary of Cash Budget of Lily Wholesale Company

Dec-18 Jan-19

Cash balance at beginning

of month $30,000 $4,835

Cash Balance at end of

month $4,835 $(115,315)

The cash budget for Lily Wholesale Company for the months of December 2018 and

January 2019 is calculated and given under Table 3 of Appendix 10.7 and the

results’ summary are shown in the Table A made above.

From the Table A we could clearly see that the company has a very low amount of

cash in hands available to meet its operating expenses. Apart from this a negative

figure of cash flow is shown at the end of January, 2019 and the reason behind this

is the amount paid towards loan of $107000.

7. Performance Evaluation of Lily Wholesale Company

In order to evaluate the performance of Lily Wholesale company the subsidiary of

Matheson Electronics during the period of December 2018 and January 2019, an

income statement has been prepared and is shown in Appendix 11.8.

From the income statement we could interpret that the company has performed

really well as a result it had earned a profit of $22187 in spite of having a very low

cash balance or reserves.

7

of one year however it is usually broken down in months or weeks which facilitates in

adding the variations taking place frequently (Financial Accountancy,n.d.).

There are certain advantages of cash budget like it helps the management in

meeting the future cash requirement, helps in taking the benefit of cash discount as

a result of making early payments due on accounts payable etc.

Table A: Summary of Cash Budget of Lily Wholesale Company

Dec-18 Jan-19

Cash balance at beginning

of month $30,000 $4,835

Cash Balance at end of

month $4,835 $(115,315)

The cash budget for Lily Wholesale Company for the months of December 2018 and

January 2019 is calculated and given under Table 3 of Appendix 10.7 and the

results’ summary are shown in the Table A made above.

From the Table A we could clearly see that the company has a very low amount of

cash in hands available to meet its operating expenses. Apart from this a negative

figure of cash flow is shown at the end of January, 2019 and the reason behind this

is the amount paid towards loan of $107000.

7. Performance Evaluation of Lily Wholesale Company

In order to evaluate the performance of Lily Wholesale company the subsidiary of

Matheson Electronics during the period of December 2018 and January 2019, an

income statement has been prepared and is shown in Appendix 11.8.

From the income statement we could interpret that the company has performed

really well as a result it had earned a profit of $22187 in spite of having a very low

cash balance or reserves.

7

Managerial Finance

8. Issues to be considered by Matheson Electronics

The electronic device which Matheson Electronics is planning to produce and launch

in the market facilitates the driver in knowing about the number of miles the

automobile is able to travel per gallon of gasoline. The market would get such a

product for the first time so Matheson Electronics could charge a good sum for the

unique and innovative device and could earn a good amount of return.

Next, since the product is new in the market and there are no competitors selling the

same product in the market, Matheson Electronics could use it as its competitive

advantage.

Matheson Electronics could also employ the cost leadership strategy. At the start the

company will not have any competitor as a result it could sell the device at a higher

price in order to earn more profit. However, since it does not takes time for other

companies to copy the technology so by that time Matheson Electronics could go for

producing the device at a larger scale and earn the economies of scale which would

lower the cost incurred on producing each device. This would help the company in

selling the device at a lower price than that of their competitors and earn profit

Other way is the company could focus on increasing the market share with the help

of reduced price. Increasing the market share would result in reduced cost and

increased profit.

If Matheson Electronics would apply the above stated cost leadership strategy

successfully then it would get other benefits like capital would be easily accessible in

order to invest in technology.

Matheson Electronics is coming with a completely unique product which shows that

the company has employed differentiation strategy. However, to remain competitive

in the market the company is required to remain focussed on the continuous

development of the device or else the risk of competitor would go high.

9. Conclusion

So Matheson Electronics should not proceed with the project of launching the type of

electronic device which could assist driver in understanding the number of miles the

8

8. Issues to be considered by Matheson Electronics

The electronic device which Matheson Electronics is planning to produce and launch

in the market facilitates the driver in knowing about the number of miles the

automobile is able to travel per gallon of gasoline. The market would get such a

product for the first time so Matheson Electronics could charge a good sum for the

unique and innovative device and could earn a good amount of return.

Next, since the product is new in the market and there are no competitors selling the

same product in the market, Matheson Electronics could use it as its competitive

advantage.

Matheson Electronics could also employ the cost leadership strategy. At the start the

company will not have any competitor as a result it could sell the device at a higher

price in order to earn more profit. However, since it does not takes time for other

companies to copy the technology so by that time Matheson Electronics could go for

producing the device at a larger scale and earn the economies of scale which would

lower the cost incurred on producing each device. This would help the company in

selling the device at a lower price than that of their competitors and earn profit

Other way is the company could focus on increasing the market share with the help

of reduced price. Increasing the market share would result in reduced cost and

increased profit.

If Matheson Electronics would apply the above stated cost leadership strategy

successfully then it would get other benefits like capital would be easily accessible in

order to invest in technology.

Matheson Electronics is coming with a completely unique product which shows that

the company has employed differentiation strategy. However, to remain competitive

in the market the company is required to remain focussed on the continuous

development of the device or else the risk of competitor would go high.

9. Conclusion

So Matheson Electronics should not proceed with the project of launching the type of

electronic device which could assist driver in understanding the number of miles the

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Managerial Finance

automobile could travel per gallon of gasoline because it has a negative NPV which

is considered to be very important for project selection and then it has a very long

payback period of approximately 8 years where the project life is itself 12 years. Now

talking about the performance of Lily Wholesale Company which is the subsidiary of

Matheson Electronics then it has performed well as a result of which in spite of

having a low cash balance it managed to generate profit.

9

automobile could travel per gallon of gasoline because it has a negative NPV which

is considered to be very important for project selection and then it has a very long

payback period of approximately 8 years where the project life is itself 12 years. Now

talking about the performance of Lily Wholesale Company which is the subsidiary of

Matheson Electronics then it has performed well as a result of which in spite of

having a low cash balance it managed to generate profit.

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Managerial Finance

10. References

Business.(2018).Break even analysis.[Online].Available 2 June, 2019

https://www.business.gov.au/planning/business-plans/writing-a-business-plan/break-

even-analysis.

Bell, P.(2017).Introducing the Net Present Value Profile.[Online].Available 2 June,

2019 https://mpra.ub.uni-muenchen.de/79764/1/MPRA_paper_79764.pdf.

Bizfluent.(2017).The Advantages & Disadvantages of the Internal Rate of Return

Method.[Online].Available 2 June, 2019 https://bizfluent.com/info-8564382-

advantages-internal-rate-return-method.html.

Business Management Ideas.(n.d.).Sources of Finance:Internal and External

Industries.[Online].Available 2 June, 2019

http://www.businessmanagementideas.com/financial-management/sources-of-

finance-internal-and-external-industries/10548.

Cengage.(n.d.).The Accounting Rate of Return (ARR).[Online].Available 2 June,

2019

http://www.cengage.com/resource_uploads/downloads/0324594690_163041.pdf.

Financial Accountancy.(2018).Break even analysis.[Online].Available 2 June, 2019

http://www.financialaccountancy.org/management-of-cash-budgets/introduction-to-

cash-budget/.

Harvard Business Review.(2016).A Refresher on Internal Rate of Return.

[Online].Available 2 June, 2019 https://hbr.org/2016/03/a-refresher-on-internal-rate-

of-return.

Scottish Qualifications Authority.(n.d.).Capital Investment Appraisal- Advantages &

Disadvantage of Different Methods.[Online].Available 2 June, 2019

https://cn.sqa.org.uk/files/professional-development-conference-2017/day2/

MangementAccountingDecisionMakingPack3ChrisAtkinson.pdf.

10

10. References

Business.(2018).Break even analysis.[Online].Available 2 June, 2019

https://www.business.gov.au/planning/business-plans/writing-a-business-plan/break-

even-analysis.

Bell, P.(2017).Introducing the Net Present Value Profile.[Online].Available 2 June,

2019 https://mpra.ub.uni-muenchen.de/79764/1/MPRA_paper_79764.pdf.

Bizfluent.(2017).The Advantages & Disadvantages of the Internal Rate of Return

Method.[Online].Available 2 June, 2019 https://bizfluent.com/info-8564382-

advantages-internal-rate-return-method.html.

Business Management Ideas.(n.d.).Sources of Finance:Internal and External

Industries.[Online].Available 2 June, 2019

http://www.businessmanagementideas.com/financial-management/sources-of-

finance-internal-and-external-industries/10548.

Cengage.(n.d.).The Accounting Rate of Return (ARR).[Online].Available 2 June,

2019

http://www.cengage.com/resource_uploads/downloads/0324594690_163041.pdf.

Financial Accountancy.(2018).Break even analysis.[Online].Available 2 June, 2019

http://www.financialaccountancy.org/management-of-cash-budgets/introduction-to-

cash-budget/.

Harvard Business Review.(2016).A Refresher on Internal Rate of Return.

[Online].Available 2 June, 2019 https://hbr.org/2016/03/a-refresher-on-internal-rate-

of-return.

Scottish Qualifications Authority.(n.d.).Capital Investment Appraisal- Advantages &

Disadvantage of Different Methods.[Online].Available 2 June, 2019

https://cn.sqa.org.uk/files/professional-development-conference-2017/day2/

MangementAccountingDecisionMakingPack3ChrisAtkinson.pdf.

10

Managerial Finance

11. Appendix

11.1 Calculation of Net Present Value

KEY VARIABLES

Initial outlay

-

31500

0

Equipment useful life 12

Project Useful Life 12

Depreciation -27500

Salvage value 15000

Working Capital 60000

Variable cost per unit 15

Fixed Cost per year (Including depreciation

on machinery)

13500

0

fixed cost per year without depreciation

10750

0

Cost of capital (Assume) 14%

Rate per unit 36

Year 0 1 2 3 4 5 6

Revenue

$2,16,00

0

$4,32,00

0

$5,40,00

0

$6,48,00

0

$6,48,00

0

$6,48,00

0

-Operating Expenses

$3,77,50

0

$4,67,50

0

$4,82,50

0

$4,97,50

0

$4,97,50

0

$4,97,50

0

EBITDA

-

$1,61,50

0 -$35,500 $57,500

$1,50,50

0

$1,50,50

0

$1,50,50

0

-Depreciation -$27,500 -$27,500 -$27,500 -$27,500 -$27,500 -$27,500

EBIT

-

$1,89,00

0 -$63,000 $30,000

$1,23,00

0

$1,23,00

0

$1,23,00

0

-Tax -$56,700 -$18,900 $9,000 $36,900 $36,900 $36,900

NOPAT

-

$2,45,70

0 -$81,900 $21,000 $86,100 $86,100 $86,100

+Depreciation $27,500 $27,500 $27,500 $27,500 $27,500 $27,500

11

11. Appendix

11.1 Calculation of Net Present Value

KEY VARIABLES

Initial outlay

-

31500

0

Equipment useful life 12

Project Useful Life 12

Depreciation -27500

Salvage value 15000

Working Capital 60000

Variable cost per unit 15

Fixed Cost per year (Including depreciation

on machinery)

13500

0

fixed cost per year without depreciation

10750

0

Cost of capital (Assume) 14%

Rate per unit 36

Year 0 1 2 3 4 5 6

Revenue

$2,16,00

0

$4,32,00

0

$5,40,00

0

$6,48,00

0

$6,48,00

0

$6,48,00

0

-Operating Expenses

$3,77,50

0

$4,67,50

0

$4,82,50

0

$4,97,50

0

$4,97,50

0

$4,97,50

0

EBITDA

-

$1,61,50

0 -$35,500 $57,500

$1,50,50

0

$1,50,50

0

$1,50,50

0

-Depreciation -$27,500 -$27,500 -$27,500 -$27,500 -$27,500 -$27,500

EBIT

-

$1,89,00

0 -$63,000 $30,000

$1,23,00

0

$1,23,00

0

$1,23,00

0

-Tax -$56,700 -$18,900 $9,000 $36,900 $36,900 $36,900

NOPAT

-

$2,45,70

0 -$81,900 $21,000 $86,100 $86,100 $86,100

+Depreciation $27,500 $27,500 $27,500 $27,500 $27,500 $27,500

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.