The Role of Accounting Standards: A Research on Maybank's Performance

VerifiedAdded on 2023/01/13

|28

|7042

|55

Homework Assignment

AI Summary

This assignment delves into the critical role of accounting standards, using Maybank, a prominent Malaysian bank, as a case study. The research investigates the significance of accounting rules and standards in shaping a company's financial performance and the preparation of accurate annual reports. The study examines the importance of valuable accounting policies for Maybank and their impact on various stakeholders. Furthermore, it explores the consequences of non-compliance with accounting standards. The methodology includes a literature review, research approach, and data collection methods, with an emphasis on ethical considerations. The analysis aims to ascertain the impact of accounting standards on decision-making for shareholders and provide recommendations. The assignment covers the identification and definition of the problem, supported by facts, figures, and evidence. It also outlines research questions, objectives, and the justification for conducting the research, referencing relevant and up-to-date sources.

Research methodology

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

METHODOLOGY..........................................................................................................................1

CHAPTER 2: LITERATURE REVIEW.........................................................................................3

Role of accounting rules and standard for a company...........................................................3

Importance of valuable accounting policies and standard for Maybank which support in

preparing appropriate annual reports for various parties:.......................................................4

Consequences of non Compliance of accounting standards:.................................................5

CHAPTER 3: RESEARCH METHODOLOGY.............................................................................7

Type of Investigation..............................................................................................................7

Research Approach.................................................................................................................7

Research Philosophy..............................................................................................................7

Data collection........................................................................................................................8

Sampling.................................................................................................................................8

Data analysis...........................................................................................................................8

Ethical consideration..............................................................................................................9

CHAPTER 4: DATA ANALYSIS................................................................................................10

CHAPTER 5: Recommendation & Reflection .............................................................................21

Recommendations................................................................................................................21

Reflection.............................................................................................................................22

CHAPTER 6: Conclusion..............................................................................................................23

REFERENCES..............................................................................................................................24

INTRODUCTION...........................................................................................................................1

METHODOLOGY..........................................................................................................................1

CHAPTER 2: LITERATURE REVIEW.........................................................................................3

Role of accounting rules and standard for a company...........................................................3

Importance of valuable accounting policies and standard for Maybank which support in

preparing appropriate annual reports for various parties:.......................................................4

Consequences of non Compliance of accounting standards:.................................................5

CHAPTER 3: RESEARCH METHODOLOGY.............................................................................7

Type of Investigation..............................................................................................................7

Research Approach.................................................................................................................7

Research Philosophy..............................................................................................................7

Data collection........................................................................................................................8

Sampling.................................................................................................................................8

Data analysis...........................................................................................................................8

Ethical consideration..............................................................................................................9

CHAPTER 4: DATA ANALYSIS................................................................................................10

CHAPTER 5: Recommendation & Reflection .............................................................................21

Recommendations................................................................................................................21

Reflection.............................................................................................................................22

CHAPTER 6: Conclusion..............................................................................................................23

REFERENCES..............................................................................................................................24

TASK 1

TOPIC: Role of accounting standards. A case study on Maybank.

POINT 1: INTRODUCTION

In present time, it is necessary for every company to follow and implement the

appropriate accounting standard while preparing valuable reports (Cai, Rahman and Courtenay,

2014). This is because it helps to clearly define the actual financial position of company during

that year and determined the areas which needed to be modified. Accounting standards keep

investors on the same page, business owners and regulators. It is easier to assess the results when

all companies adopt the same accounting practices. The regulations often prohibit businesses

from using the accounting areas to their own benefit. In this research Maybank is selected which

is a leading bank of Malaysia and provide number of banking and insurance services to large

number of people. The same would only be achieved if there is clear criteria for determining the

practices are adopted within Maybank. The all transactions of entities must then be reported in a

uniform manner when they comply with such issued accounting standards. Accounting Practices

have set out various standards, laws and legislation to be followed by businesses in accounting

procedures. These rules and guidelines must be adopted by every organization. This controls the

whole manner in which financial requirements are planned and delivered. Therefore, if auditors

believe that entity has met with accounting standards and rules specified, they will easily check

that all fiscal practises are fair and accurate. . In the semi-probability screening process, samples

are collected in this kind of way that some people are randomly selected as a part of investigation

which are further support in making valuable decision. In respect to complete the particular

research 30 respondent are selected randomly those are working for different job position in

Maybank. This help in defining the correct information about the understanding and use

accounting standard while preparing annual statement.

POINT 2: Identification and definition of the problem

“To recognise the importance of various accounting standard on the performance and

authenticity of company.” Study related with Maybank.

Problem statement

Is implementation of appropriate accounting standard while preparing annual statement

are helpful in decision making for different shareholder?

POINT 3: Facts, figures or evidence

TOPIC: Role of accounting standards. A case study on Maybank.

POINT 1: INTRODUCTION

In present time, it is necessary for every company to follow and implement the

appropriate accounting standard while preparing valuable reports (Cai, Rahman and Courtenay,

2014). This is because it helps to clearly define the actual financial position of company during

that year and determined the areas which needed to be modified. Accounting standards keep

investors on the same page, business owners and regulators. It is easier to assess the results when

all companies adopt the same accounting practices. The regulations often prohibit businesses

from using the accounting areas to their own benefit. In this research Maybank is selected which

is a leading bank of Malaysia and provide number of banking and insurance services to large

number of people. The same would only be achieved if there is clear criteria for determining the

practices are adopted within Maybank. The all transactions of entities must then be reported in a

uniform manner when they comply with such issued accounting standards. Accounting Practices

have set out various standards, laws and legislation to be followed by businesses in accounting

procedures. These rules and guidelines must be adopted by every organization. This controls the

whole manner in which financial requirements are planned and delivered. Therefore, if auditors

believe that entity has met with accounting standards and rules specified, they will easily check

that all fiscal practises are fair and accurate. . In the semi-probability screening process, samples

are collected in this kind of way that some people are randomly selected as a part of investigation

which are further support in making valuable decision. In respect to complete the particular

research 30 respondent are selected randomly those are working for different job position in

Maybank. This help in defining the correct information about the understanding and use

accounting standard while preparing annual statement.

POINT 2: Identification and definition of the problem

“To recognise the importance of various accounting standard on the performance and

authenticity of company.” Study related with Maybank.

Problem statement

Is implementation of appropriate accounting standard while preparing annual statement

are helpful in decision making for different shareholder?

POINT 3: Facts, figures or evidence

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

For the researcher, ethical considerations are important when studying principles of ethics to

support better outcomes. Ethics must improve the thesis to discourage participants from

promoting unethical behaviour. When focusing at morality, the speaker cannot provide the

viewer with misleading facts that improves the integrity and sense of research. All the

participants are kept safe and protected by the investigator in existing research so each

participant is helpful for the research projects. All data necessary to lead to analysis must be

preserved secure and avoid abuse and exploitation in the light of the study topic. It is the process

of gathering information on specific factors with the aim of analysing the data. An investigator

will be able to examine their hypotheses based on the data and information collected. Types of

data collection are of two different types, namely primary and secondary. In respect to complete

the particular research primary method is used to which is effective in collecting the desirable

information about the research topic. Researcher develop appropriate question which are asked

to specific audience in order to determine their understanding and knowledge about particular

topic. Moreover appropriate statistical test are performed in order to detect the accuracy of

gathered information so that crucial decision are made for future effectiveness.

POINT 4: Research questions and objectives

Objectives

To ascertain the role of accounting rules and standard for a company.

To detect the importance of valuable accounting policies and standard for Maybank

which support in preparing appropriate annual reports for various parties?

To determine the consequences of noncompliance of accounting standard

Questions

What is the main role of accounting rules and standard for a company?

What are the importance of valuable accounting policies and standard for Maybank

which support in preparing appropriate annual reports for various parties?

What happen in case if company do not follow appropriate accounting standards?

Methods of research refer to processes which are mainly used to gather information and

data for effective business decisions. It is considered by systematic and objective methods of

searching for solution to problems that arise as a search for the knowledge. There are two

different research methods which are qualitative and quantitative (Fatima, Abdullah and

Sulaiman, 2015).

support better outcomes. Ethics must improve the thesis to discourage participants from

promoting unethical behaviour. When focusing at morality, the speaker cannot provide the

viewer with misleading facts that improves the integrity and sense of research. All the

participants are kept safe and protected by the investigator in existing research so each

participant is helpful for the research projects. All data necessary to lead to analysis must be

preserved secure and avoid abuse and exploitation in the light of the study topic. It is the process

of gathering information on specific factors with the aim of analysing the data. An investigator

will be able to examine their hypotheses based on the data and information collected. Types of

data collection are of two different types, namely primary and secondary. In respect to complete

the particular research primary method is used to which is effective in collecting the desirable

information about the research topic. Researcher develop appropriate question which are asked

to specific audience in order to determine their understanding and knowledge about particular

topic. Moreover appropriate statistical test are performed in order to detect the accuracy of

gathered information so that crucial decision are made for future effectiveness.

POINT 4: Research questions and objectives

Objectives

To ascertain the role of accounting rules and standard for a company.

To detect the importance of valuable accounting policies and standard for Maybank

which support in preparing appropriate annual reports for various parties?

To determine the consequences of noncompliance of accounting standard

Questions

What is the main role of accounting rules and standard for a company?

What are the importance of valuable accounting policies and standard for Maybank

which support in preparing appropriate annual reports for various parties?

What happen in case if company do not follow appropriate accounting standards?

Methods of research refer to processes which are mainly used to gather information and

data for effective business decisions. It is considered by systematic and objective methods of

searching for solution to problems that arise as a search for the knowledge. There are two

different research methods which are qualitative and quantitative (Fatima, Abdullah and

Sulaiman, 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

POINT 5: Justification for doing the research

In order to perform this research quantitative approach is used because which provides

the suitable understanding about the facts and reality to the research topic. This method is also

supportive to extract large number of data in shorter period that saves times and cost.

Data collection- It is the process of gathering information on specific factors with the aim

of analysing the data. An investigator will be able to examine their hypotheses based on the data

and information collected. Types of data collection are of two different types, namely primary

and secondary. In respect to complete the particular research primary method is used to which is

effective in collecting the desirable information about the research topic. Researcher develop

appropriate question which are asked to specific audience in order to determine their

understanding and knowledge about particular topic. Moreover appropriate statistical test are

performed in order to detect the accuracy of gathered information so that crucial decision are

made for future effectiveness.

POINT 6: Appropriate and latest references and citations

Cai, L., Rahman, A. and Courtenay, S., 2014. The effect of IFRS adoption conditional upon the

level of pre-adoption divergence. The International Journal of Accounting. 49(2).

pp.147-178.

Fatima, A. H., Abdullah, N. and Sulaiman, M., 2015. Environmental disclosure quality:

examining the impact of the stock exchange of Malaysia’s listing requirements. Social

Responsibility Journal.

Goh, C. F. and Rasli, A., 2014. CEO duality, board independence, corporate governance and

firm performance in family firms: Evidence from the manufacturing industry in

Malaysia. Asian Business & Management. 13(4). pp.333-357.

Haji, A. A., 2014. The relationship between corporate governance attributes and firm

performance before and after the revised code. International Journal of Commerce and

Management.

Haron, R. and Ibrahim, K., 2012. Target capital structure and speed of adjustment: Panel data

evidence on Malaysia Shariah compliant securities. International Journal of Economics,

Management and Accounting. 20(2).

Hassan, Z. and Diallo, M. M., 2013. Cross-cultural adjustments and expatriate’s job

performance: a study on Malaysia. International journal of accounting and business

management. 1(1), pp.8-23.

In order to perform this research quantitative approach is used because which provides

the suitable understanding about the facts and reality to the research topic. This method is also

supportive to extract large number of data in shorter period that saves times and cost.

Data collection- It is the process of gathering information on specific factors with the aim

of analysing the data. An investigator will be able to examine their hypotheses based on the data

and information collected. Types of data collection are of two different types, namely primary

and secondary. In respect to complete the particular research primary method is used to which is

effective in collecting the desirable information about the research topic. Researcher develop

appropriate question which are asked to specific audience in order to determine their

understanding and knowledge about particular topic. Moreover appropriate statistical test are

performed in order to detect the accuracy of gathered information so that crucial decision are

made for future effectiveness.

POINT 6: Appropriate and latest references and citations

Cai, L., Rahman, A. and Courtenay, S., 2014. The effect of IFRS adoption conditional upon the

level of pre-adoption divergence. The International Journal of Accounting. 49(2).

pp.147-178.

Fatima, A. H., Abdullah, N. and Sulaiman, M., 2015. Environmental disclosure quality:

examining the impact of the stock exchange of Malaysia’s listing requirements. Social

Responsibility Journal.

Goh, C. F. and Rasli, A., 2014. CEO duality, board independence, corporate governance and

firm performance in family firms: Evidence from the manufacturing industry in

Malaysia. Asian Business & Management. 13(4). pp.333-357.

Haji, A. A., 2014. The relationship between corporate governance attributes and firm

performance before and after the revised code. International Journal of Commerce and

Management.

Haron, R. and Ibrahim, K., 2012. Target capital structure and speed of adjustment: Panel data

evidence on Malaysia Shariah compliant securities. International Journal of Economics,

Management and Accounting. 20(2).

Hassan, Z. and Diallo, M. M., 2013. Cross-cultural adjustments and expatriate’s job

performance: a study on Malaysia. International journal of accounting and business

management. 1(1), pp.8-23.

TASK 2:

POINT 1: Introduction

In present time, it is necessary for every company to follow and implement the

appropriate accounting standard while preparing valuable reports. This is because it helps to

clearly define the actual financial position of company during that year and determined the areas

which needed to be modified. Accounting standards keep investors on the same page, business

owners and regulators. It is easier to assess the results when all companies adopt the same

accounting practices. The regulations often prohibit businesses from using the accounting areas

to their own benefit. In this research Maybank is selected which is a leading bank of Malaysia

and provide number of banking and insurance services to large number of people.

Problem statement.

Is implementation of appropriate accounting standard while preparing annual statement are

helpful in decision making for different shareholder.

Objective

To ascertain the role of accounting rules and standard for a company.

To detect the importance of valuable accounting policies and standard for Maybank which

support in preparing appropriate annual reports for various parties?

To determine the consequences of noncompliance of accounting standard

Point 2 Literature review

Role of accounting rules and standard for a company

According to Muniandy and Ali, (2012) accounting rules and standards are regarded as

core and essential regulative framework for formation of effective fiscal reports as well as

sequent auditing of same (Muniandy, and Ali, 2012). Accounting rules are common guidelines

issued by relevant regulatory authority. Some guidelines may be compulsory to follow and

several may be just advisory. These rules contain some specific guidelines that assist accounting

personnel in reporting financial information. They are made available by means of a number of

important reports on the knowledge and reporting of special types of legal process, happenings

as well as other expenses. Accounting rules are designed to provide valuable information to

various users of financial statements, like stakeholders, lenders, borrowers, managers, investment

providers, suppliers, competitive companies, researchers, regulatory body. In reality, these

POINT 1: Introduction

In present time, it is necessary for every company to follow and implement the

appropriate accounting standard while preparing valuable reports. This is because it helps to

clearly define the actual financial position of company during that year and determined the areas

which needed to be modified. Accounting standards keep investors on the same page, business

owners and regulators. It is easier to assess the results when all companies adopt the same

accounting practices. The regulations often prohibit businesses from using the accounting areas

to their own benefit. In this research Maybank is selected which is a leading bank of Malaysia

and provide number of banking and insurance services to large number of people.

Problem statement.

Is implementation of appropriate accounting standard while preparing annual statement are

helpful in decision making for different shareholder.

Objective

To ascertain the role of accounting rules and standard for a company.

To detect the importance of valuable accounting policies and standard for Maybank which

support in preparing appropriate annual reports for various parties?

To determine the consequences of noncompliance of accounting standard

Point 2 Literature review

Role of accounting rules and standard for a company

According to Muniandy and Ali, (2012) accounting rules and standards are regarded as

core and essential regulative framework for formation of effective fiscal reports as well as

sequent auditing of same (Muniandy, and Ali, 2012). Accounting rules are common guidelines

issued by relevant regulatory authority. Some guidelines may be compulsory to follow and

several may be just advisory. These rules contain some specific guidelines that assist accounting

personnel in reporting financial information. They are made available by means of a number of

important reports on the knowledge and reporting of special types of legal process, happenings

as well as other expenses. Accounting rules are designed to provide valuable information to

various users of financial statements, like stakeholders, lenders, borrowers, managers, investment

providers, suppliers, competitive companies, researchers, regulatory body. In reality, these

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

assertions are scheduled and recommended in order to enhance & baseline quality of fiscal

coverage. The rapid growth of global trade agreements trade agreements trade as well as the

internationalisation of enterprises, the introduction of latest communication technologies as well

as the emergence of international challenging forces are disrupting the fiscal environment to

large extent. In current global business circumstances, the locals of business community are in

serious want of common financial reporting language which should be used by all.

As per Salleh and Stewart, (2012) an international financial reporting structure is a

necessity to entice both overseas and current and current or future investors, which should be

accomplished through the harmonisation of accounting rules/standards (Salleh and Stewart,

2012). Accounting Standards refers to policy texts (unbiased statements for best financial

reporting practices) issued by specialist accounting authorities on various elements of

measurement, managing and confidentiality of accounting operations and concerns. As regards

the enactment of Malaysian GAAP, These are demonstrated as imperatives of accounting

reforms and trends, by codes or guidelines on how items that are to be drawn up in accounts

should be removed from accounts and described in annual reports of Maybank. The aim of

developing standards in context of Maybank is ensuring consistency in entire process of financial

reporting as well as to ensure quality and compatibility in information published by corporations.

MFRS include presentation, measurement, treatment, identification and disclosure elements of

accounting operations related to financial statements that are published policy documents

provided by a professional accounting officer or by government or other administrative

authority. Accounting rules / principles make it easy for stakeholders to analyses businesses

easily by evaluating their financial reports. If investors/stakeholders are divided among two

businesses in same field, investor can evaluate their corresponding statements to decide who is

performing a better way of generating sales and handling cash-flows. These also allows

corporations gain insight and transparency into own practices and results (Goh and Rasli, 2014).

In fact, these minimize the possibility of inaccurate financial reporting through having multiple

monitors and safeguarding.

Importance of valuable accounting policies and standard for Maybank which support in

preparing appropriate annual reports for various parties:

As pet the views of Kasim, (2012) accounting policies relates to basic standards and

processes set in place by the governing staff of the corporation which are utilized to compile its

coverage. The rapid growth of global trade agreements trade agreements trade as well as the

internationalisation of enterprises, the introduction of latest communication technologies as well

as the emergence of international challenging forces are disrupting the fiscal environment to

large extent. In current global business circumstances, the locals of business community are in

serious want of common financial reporting language which should be used by all.

As per Salleh and Stewart, (2012) an international financial reporting structure is a

necessity to entice both overseas and current and current or future investors, which should be

accomplished through the harmonisation of accounting rules/standards (Salleh and Stewart,

2012). Accounting Standards refers to policy texts (unbiased statements for best financial

reporting practices) issued by specialist accounting authorities on various elements of

measurement, managing and confidentiality of accounting operations and concerns. As regards

the enactment of Malaysian GAAP, These are demonstrated as imperatives of accounting

reforms and trends, by codes or guidelines on how items that are to be drawn up in accounts

should be removed from accounts and described in annual reports of Maybank. The aim of

developing standards in context of Maybank is ensuring consistency in entire process of financial

reporting as well as to ensure quality and compatibility in information published by corporations.

MFRS include presentation, measurement, treatment, identification and disclosure elements of

accounting operations related to financial statements that are published policy documents

provided by a professional accounting officer or by government or other administrative

authority. Accounting rules / principles make it easy for stakeholders to analyses businesses

easily by evaluating their financial reports. If investors/stakeholders are divided among two

businesses in same field, investor can evaluate their corresponding statements to decide who is

performing a better way of generating sales and handling cash-flows. These also allows

corporations gain insight and transparency into own practices and results (Goh and Rasli, 2014).

In fact, these minimize the possibility of inaccurate financial reporting through having multiple

monitors and safeguarding.

Importance of valuable accounting policies and standard for Maybank which support in

preparing appropriate annual reports for various parties:

As pet the views of Kasim, (2012) accounting policies relates to basic standards and

processes set in place by the governing staff of the corporation which are utilized to compile its

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

annual or periodic financial statements and reports (Kasim, 2012). They comprise all accounting

methods, assessment structures and disclosures. As in Malaysia for banking corporation, Central

Bank of Malaya (Bank Negara Tanah Melayu) form policies for banks with respect to

accounting, finance and other banking operations. This is the major regulating body which is

responsible for regulating banks and financial institutions like Maybank. Entities specially

banking corporations are usually expected to file their annual financial-statements in compliance

with Malaysian Financial Reporting Standards (MFRS) similar to IFRSs, except for independent

private entities which fail to comply with Private Entity Reporting Standards (PERS) for annual-

financial statements with periods starting before 1, Jan. 2016 and Malaysian Private Entities

Reporting Standard (MPERS-almost identical). Their primary goal is to maintain effective

transparency, reliability, credibility and comparability of financial reports and statements. They

do this by streamlining the nations economy's accounting practices and values (Haji, 2014).

Companies like Maybank are not permitted to manage and file their records as per their own

desires or preferences, or are unable to produce financial statements/reports for various groups

concerned. A large-scale global enterprise such as Maybank needs a solid infrastructure to meet

its clients’ expectations. One element is a powerful database developed by company that shares

‘best practice’ information with all its offices around the world. Client is also harnessing all

available technology to ensure any of their advisers can work with their clients anywhere in the

world, allowing them to be fully effective in serving the clients’ needs immediately.

Mukhlisin, Hudaib and Azid, (2015) expressed views on this topic that Accounting is

commonly used as a specific language of business, because it expresses the actual financial

position of company to others (Mukhlisin, Hudaib and Azid, 2015). But as each language has

some syntax, as well as rules of grammar are same here. The key role in context of Maybank is

to increase the consistency and credit-ability of financial statements. Once financial statements

need to be produced in compliance with the guidelines, consumers will depend on them. As they

are aware that failure to comply with these requirements can have significant consequences for

businesses. Then there's comparability. Such criteria would enable for inter-firm as well as intra-

firm contrasts. This helps us to track the growth of product and its place in market. This also

aims to lay down a collection of accounting rules that involve the required reporting

requirements and assessment methods for different financial activities. Accounting standards

allow auditing personnel to fulfil their roles and duties. It simplifies the responsibilities and

methods, assessment structures and disclosures. As in Malaysia for banking corporation, Central

Bank of Malaya (Bank Negara Tanah Melayu) form policies for banks with respect to

accounting, finance and other banking operations. This is the major regulating body which is

responsible for regulating banks and financial institutions like Maybank. Entities specially

banking corporations are usually expected to file their annual financial-statements in compliance

with Malaysian Financial Reporting Standards (MFRS) similar to IFRSs, except for independent

private entities which fail to comply with Private Entity Reporting Standards (PERS) for annual-

financial statements with periods starting before 1, Jan. 2016 and Malaysian Private Entities

Reporting Standard (MPERS-almost identical). Their primary goal is to maintain effective

transparency, reliability, credibility and comparability of financial reports and statements. They

do this by streamlining the nations economy's accounting practices and values (Haji, 2014).

Companies like Maybank are not permitted to manage and file their records as per their own

desires or preferences, or are unable to produce financial statements/reports for various groups

concerned. A large-scale global enterprise such as Maybank needs a solid infrastructure to meet

its clients’ expectations. One element is a powerful database developed by company that shares

‘best practice’ information with all its offices around the world. Client is also harnessing all

available technology to ensure any of their advisers can work with their clients anywhere in the

world, allowing them to be fully effective in serving the clients’ needs immediately.

Mukhlisin, Hudaib and Azid, (2015) expressed views on this topic that Accounting is

commonly used as a specific language of business, because it expresses the actual financial

position of company to others (Mukhlisin, Hudaib and Azid, 2015). But as each language has

some syntax, as well as rules of grammar are same here. The key role in context of Maybank is

to increase the consistency and credit-ability of financial statements. Once financial statements

need to be produced in compliance with the guidelines, consumers will depend on them. As they

are aware that failure to comply with these requirements can have significant consequences for

businesses. Then there's comparability. Such criteria would enable for inter-firm as well as intra-

firm contrasts. This helps us to track the growth of product and its place in market. This also

aims to lay down a collection of accounting rules that involve the required reporting

requirements and assessment methods for different financial activities. Accounting standards

allow auditing personnel to fulfil their roles and duties. It simplifies the responsibilities and

making it simple for such personnel to fulfil roles. Streamlining all accounting and financial

information is crucial role of accounting standards. This sets out standard guidelines for every

fiscal and accounting transaction. This eliminates all the uncertainty of accounting operation

(Haron and Ibrahim, 2012).

Consequences of non Compliance of accounting standards:

According to Mohdali, Isa and Yusoff, (2014) Malaysia is very lucky that it have made

quantum leaps in process of convergence to IFRS (Mohdali, Isa and Yusoff, 2014). Aside from

the disagreement with treatment of Islamic based banking and finance including its relationship

to measurements, disclosures and acknowledgements based on Syariah as well as MFRS

frameworks. Malaysia is quite stable and on right track to convergence to IFRS as there no major

problems of non-compliances with MFRS, this is also recognized that Malaysia has adopted as

well as over time developed effective national accounting and reporting policies, combined with

sufficient funding to as well as from MASB. Malaysia's educational system, theoretically is quite

much in compliance with current trends in accounting and corporate fraternity, so there's no

shortage of local ability in terms of educational and trainings, and bookkeepers in training are

quite well ready to join the job market to large extent (Hassan and Diallo, 2013). In Malaysia, for

banking corporation like Maybank it is required to follow accounting standards as the non-

compliance of accounting standard leads to penalties as specified. Also those banks which are

not following accounting standards comes in radar of regulatory authorities and auditing

personnels. Also in general public credibility or creditworthiness of bank also may decline as

non-compliance of accounting standards can reduce the relevancy of reported financial

statements for stakeholders and other interested parties. In order to make sure that reporting

entities in country are MFRS compliant, such entities should carry out a systematic, thorough

and accurate analysis of their corporation's readiness to comply with MFRS in order to prevent

any inquiry by authority owing to non-compliance after grace period for complete adoption.

As per Yusof, Ling and Wah, (2014) unless Malaysia winds up cutting its MFRS as

compatibility system that can be tailored to local requirements as well as not single size fits all

collection of standards, since full acceptance requires countries to sacrifice their sovereignty,

Country will have serious problems and will encounter difficulty to be accepted as a nation that

meets complete IFRS adoption (Yusof, Ling and Wah, 2014). The most concrete effect is that

when the company fails to follow new standards, it might be at risk of non-compliance as well as

information is crucial role of accounting standards. This sets out standard guidelines for every

fiscal and accounting transaction. This eliminates all the uncertainty of accounting operation

(Haron and Ibrahim, 2012).

Consequences of non Compliance of accounting standards:

According to Mohdali, Isa and Yusoff, (2014) Malaysia is very lucky that it have made

quantum leaps in process of convergence to IFRS (Mohdali, Isa and Yusoff, 2014). Aside from

the disagreement with treatment of Islamic based banking and finance including its relationship

to measurements, disclosures and acknowledgements based on Syariah as well as MFRS

frameworks. Malaysia is quite stable and on right track to convergence to IFRS as there no major

problems of non-compliances with MFRS, this is also recognized that Malaysia has adopted as

well as over time developed effective national accounting and reporting policies, combined with

sufficient funding to as well as from MASB. Malaysia's educational system, theoretically is quite

much in compliance with current trends in accounting and corporate fraternity, so there's no

shortage of local ability in terms of educational and trainings, and bookkeepers in training are

quite well ready to join the job market to large extent (Hassan and Diallo, 2013). In Malaysia, for

banking corporation like Maybank it is required to follow accounting standards as the non-

compliance of accounting standard leads to penalties as specified. Also those banks which are

not following accounting standards comes in radar of regulatory authorities and auditing

personnels. Also in general public credibility or creditworthiness of bank also may decline as

non-compliance of accounting standards can reduce the relevancy of reported financial

statements for stakeholders and other interested parties. In order to make sure that reporting

entities in country are MFRS compliant, such entities should carry out a systematic, thorough

and accurate analysis of their corporation's readiness to comply with MFRS in order to prevent

any inquiry by authority owing to non-compliance after grace period for complete adoption.

As per Yusof, Ling and Wah, (2014) unless Malaysia winds up cutting its MFRS as

compatibility system that can be tailored to local requirements as well as not single size fits all

collection of standards, since full acceptance requires countries to sacrifice their sovereignty,

Country will have serious problems and will encounter difficulty to be accepted as a nation that

meets complete IFRS adoption (Yusof, Ling and Wah, 2014). The most concrete effect is that

when the company fails to follow new standards, it might be at risk of non-compliance as well as

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

competitors of bank can gain competitive advantages. Non compliance of accounting standards

is directly linked with its shareholder's trust. Also non compliance can result in legal proceedings

against bank. Further, for effective reporting of information and results is also good for bank's

personal growth. Non-compliance act as a direct message for shareholders and other stakeholders

like customers, lenders etc. that bank are hiding truth or there may be chances of fraud or

mismanagement. Accounting standards ensures that proper disclosures are made in financial

statements so users can easily understand what is going on within Maybank but due to non-

compliances if bank not make adequate disclosures then it can hurt the sentiments of users of

financial statements. Further at global level non-compliances of IFRS or MFRS can also impact

the image of bank in global market-place. Thus it is duty of each corporation to follow

accounting standards appropriately and prevent all such direct and indirect consequences

(Siswantoro and Ibrahim, 2017).

Point 3: Presentation of theoretical framework

The method for the gradual assessment used throughout the research is recognized as

survey methodology. RM is commonly defined as the essential component of several research

projects offering an adequate statutory and specific framework for the conducting of study.

Methodologically relevant and accurate actual facts can be used primarily to help answer

hypotheses or to explain why concerns are raised specifically in the analysis (Razak and

Mustapha, 2013). It acts as a roadmap for the prosecutor to draw a specific decision on a decided

problem for a study. Some important components of RM are discussed underneath:

Type of Investigation

Research methods apply to systems adopted primarily to obtain data and information in

order to make innovative business judgements (Mohamed and Daud, 2012). The quest for

solutions to problems occurring in the search for meaning is regarded through systematic and

analytical means. To complete the following research project quantitative method is

implemented as it is helpful in delivering the suitable understanding to all facts and figure

relevant to particular research. The concept of quantitative research is really the systematic way

of gathering evidence to be pursued to obtain more accurate results.

Research Approach

The systematic process which includes various theories and procedures for data

collection, interpretation and comprehension which are stated as research mechanism or

is directly linked with its shareholder's trust. Also non compliance can result in legal proceedings

against bank. Further, for effective reporting of information and results is also good for bank's

personal growth. Non-compliance act as a direct message for shareholders and other stakeholders

like customers, lenders etc. that bank are hiding truth or there may be chances of fraud or

mismanagement. Accounting standards ensures that proper disclosures are made in financial

statements so users can easily understand what is going on within Maybank but due to non-

compliances if bank not make adequate disclosures then it can hurt the sentiments of users of

financial statements. Further at global level non-compliances of IFRS or MFRS can also impact

the image of bank in global market-place. Thus it is duty of each corporation to follow

accounting standards appropriately and prevent all such direct and indirect consequences

(Siswantoro and Ibrahim, 2017).

Point 3: Presentation of theoretical framework

The method for the gradual assessment used throughout the research is recognized as

survey methodology. RM is commonly defined as the essential component of several research

projects offering an adequate statutory and specific framework for the conducting of study.

Methodologically relevant and accurate actual facts can be used primarily to help answer

hypotheses or to explain why concerns are raised specifically in the analysis (Razak and

Mustapha, 2013). It acts as a roadmap for the prosecutor to draw a specific decision on a decided

problem for a study. Some important components of RM are discussed underneath:

Type of Investigation

Research methods apply to systems adopted primarily to obtain data and information in

order to make innovative business judgements (Mohamed and Daud, 2012). The quest for

solutions to problems occurring in the search for meaning is regarded through systematic and

analytical means. To complete the following research project quantitative method is

implemented as it is helpful in delivering the suitable understanding to all facts and figure

relevant to particular research. The concept of quantitative research is really the systematic way

of gathering evidence to be pursued to obtain more accurate results.

Research Approach

The systematic process which includes various theories and procedures for data

collection, interpretation and comprehension which are stated as research mechanism or

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

approach. Some of crucial techniques for study are inductive, abductive and deductive. In this

research approach of inductive reasoning is starts with hypothesis formulation and completing

testing for the successful results. This means researcher can take with a broad range of

possibilities. The assumptions they make from the evidence collected or a specific data series

are virtually unlimited. Inductive reasoning, though, offers researcher a reference point for

narrowing its conclusions and drawing a rational inference.

Research Philosophy

The accurate way of assessing collection of the scientific information is known as a

research philosophy by consideration of key sources, knowledge and understanding. The beliefs,

views, ideas and assumptions that are formed are those that are based on evidence to be gathered

or the information to be taken (Ng, Chong and Ismail, 2013). This describes the data related to a

particular event as well as the details obtained, analysed and is used to accomplish the study aim.

This particular study uses the theory of positivism, that actually accepts that perhaps the forces

and structures go further than reality and laws occur and are real. It notes some theory and any

certain methodology of science which can not be rejected by the scientific method.

Sampling

In general, sampling may be defined as gathering some sections of the sample from broad

population and making results based on their responses in the context of study needs. Moreover,

researcher used to make the assumption that weather people are aware or not about the research

topic from the understanding and response of selected people (Lahsasna, 2014).

Data analysis

The most important part of a detailed research is to promote the use of mathematical

instruments and procedures in order to assess and explain the information gathered. This

approach should be used in the framework of analysis to provide the correct interpretation for

relevant content. In addition, quantitative method of collecting data is effective in ascertaining

the in-depth knowledge of selected candidate relevance to research topic. Qualitative data

analysis is also effective in determining the theoretical concept which ease the understanding of

accounting rules and regulation that are valuable in preparing statement.

Point 4 Research methods

Questionnaire

research approach of inductive reasoning is starts with hypothesis formulation and completing

testing for the successful results. This means researcher can take with a broad range of

possibilities. The assumptions they make from the evidence collected or a specific data series

are virtually unlimited. Inductive reasoning, though, offers researcher a reference point for

narrowing its conclusions and drawing a rational inference.

Research Philosophy

The accurate way of assessing collection of the scientific information is known as a

research philosophy by consideration of key sources, knowledge and understanding. The beliefs,

views, ideas and assumptions that are formed are those that are based on evidence to be gathered

or the information to be taken (Ng, Chong and Ismail, 2013). This describes the data related to a

particular event as well as the details obtained, analysed and is used to accomplish the study aim.

This particular study uses the theory of positivism, that actually accepts that perhaps the forces

and structures go further than reality and laws occur and are real. It notes some theory and any

certain methodology of science which can not be rejected by the scientific method.

Sampling

In general, sampling may be defined as gathering some sections of the sample from broad

population and making results based on their responses in the context of study needs. Moreover,

researcher used to make the assumption that weather people are aware or not about the research

topic from the understanding and response of selected people (Lahsasna, 2014).

Data analysis

The most important part of a detailed research is to promote the use of mathematical

instruments and procedures in order to assess and explain the information gathered. This

approach should be used in the framework of analysis to provide the correct interpretation for

relevant content. In addition, quantitative method of collecting data is effective in ascertaining

the in-depth knowledge of selected candidate relevance to research topic. Qualitative data

analysis is also effective in determining the theoretical concept which ease the understanding of

accounting rules and regulation that are valuable in preparing statement.

Point 4 Research methods

Questionnaire

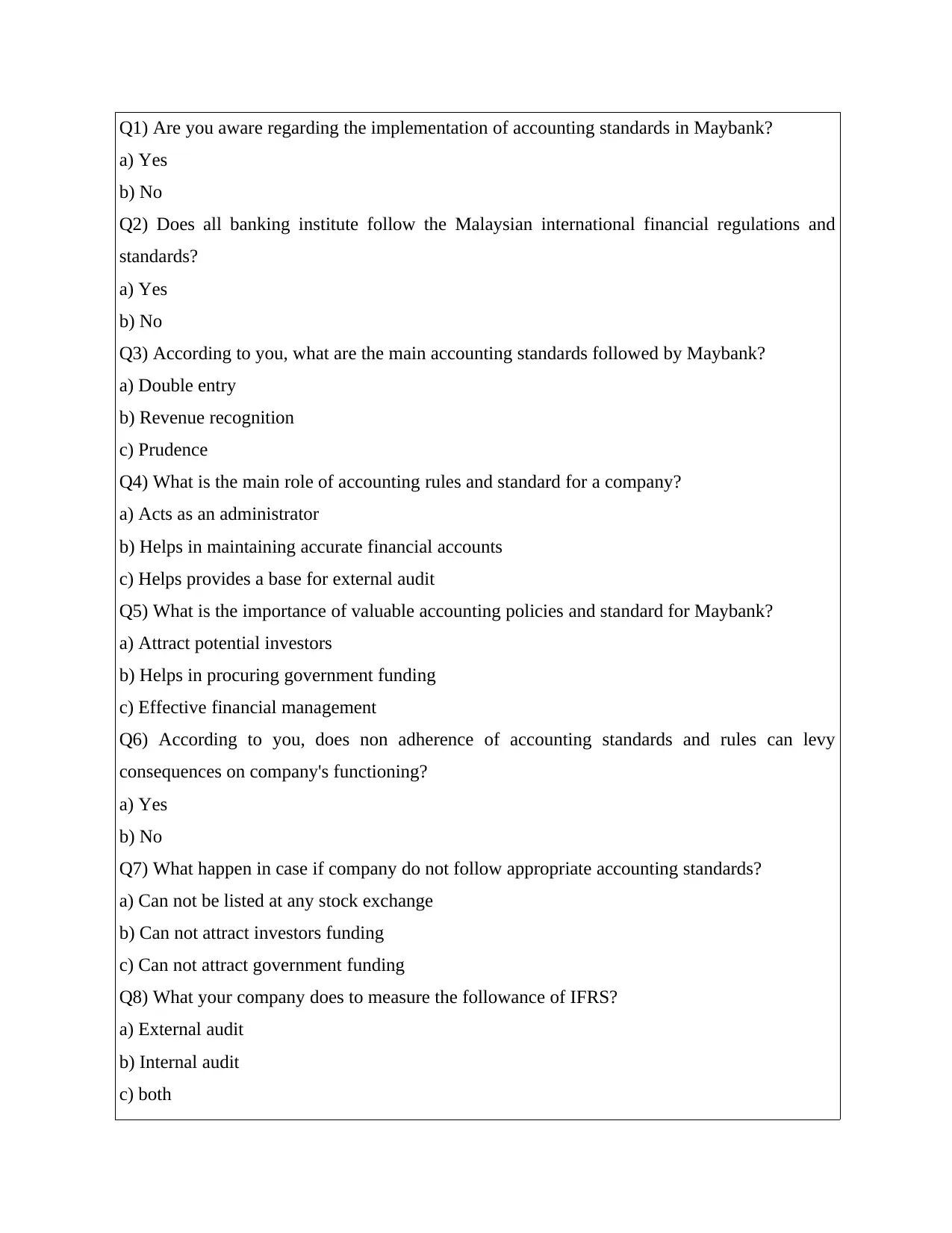

Q1) Are you aware regarding the implementation of accounting standards in Maybank?

a) Yes

b) No

Q2) Does all banking institute follow the Malaysian international financial regulations and

standards?

a) Yes

b) No

Q3) According to you, what are the main accounting standards followed by Maybank?

a) Double entry

b) Revenue recognition

c) Prudence

Q4) What is the main role of accounting rules and standard for a company?

a) Acts as an administrator

b) Helps in maintaining accurate financial accounts

c) Helps provides a base for external audit

Q5) What is the importance of valuable accounting policies and standard for Maybank?

a) Attract potential investors

b) Helps in procuring government funding

c) Effective financial management

Q6) According to you, does non adherence of accounting standards and rules can levy

consequences on company's functioning?

a) Yes

b) No

Q7) What happen in case if company do not follow appropriate accounting standards?

a) Can not be listed at any stock exchange

b) Can not attract investors funding

c) Can not attract government funding

Q8) What your company does to measure the followance of IFRS?

a) External audit

b) Internal audit

c) both

a) Yes

b) No

Q2) Does all banking institute follow the Malaysian international financial regulations and

standards?

a) Yes

b) No

Q3) According to you, what are the main accounting standards followed by Maybank?

a) Double entry

b) Revenue recognition

c) Prudence

Q4) What is the main role of accounting rules and standard for a company?

a) Acts as an administrator

b) Helps in maintaining accurate financial accounts

c) Helps provides a base for external audit

Q5) What is the importance of valuable accounting policies and standard for Maybank?

a) Attract potential investors

b) Helps in procuring government funding

c) Effective financial management

Q6) According to you, does non adherence of accounting standards and rules can levy

consequences on company's functioning?

a) Yes

b) No

Q7) What happen in case if company do not follow appropriate accounting standards?

a) Can not be listed at any stock exchange

b) Can not attract investors funding

c) Can not attract government funding

Q8) What your company does to measure the followance of IFRS?

a) External audit

b) Internal audit

c) both

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 28

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.