MBA 6100 Spring 2019 Block 1: CVP Analysis Case Study

VerifiedAdded on 2023/04/26

|8

|1079

|495

Case Study

AI Summary

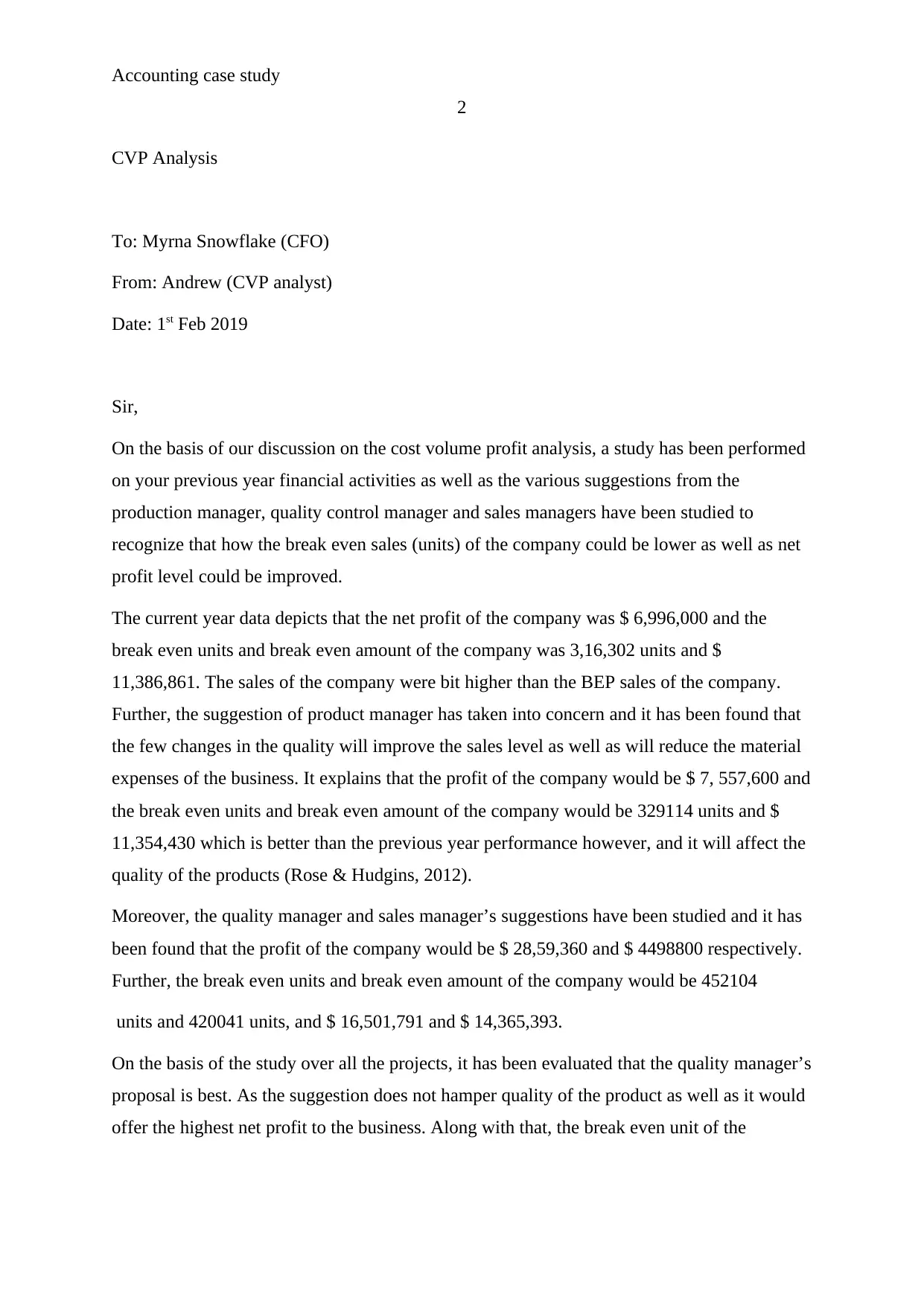

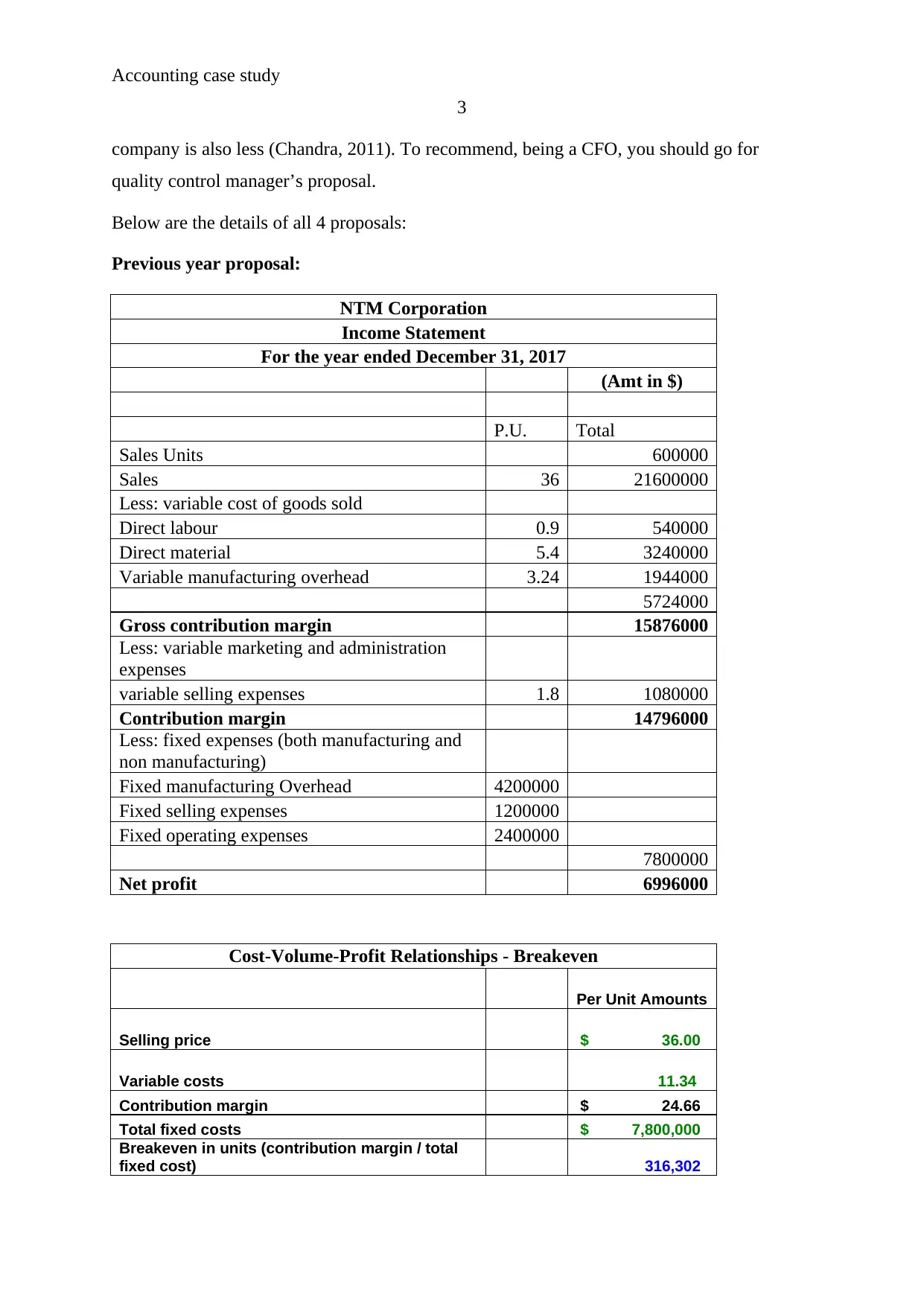

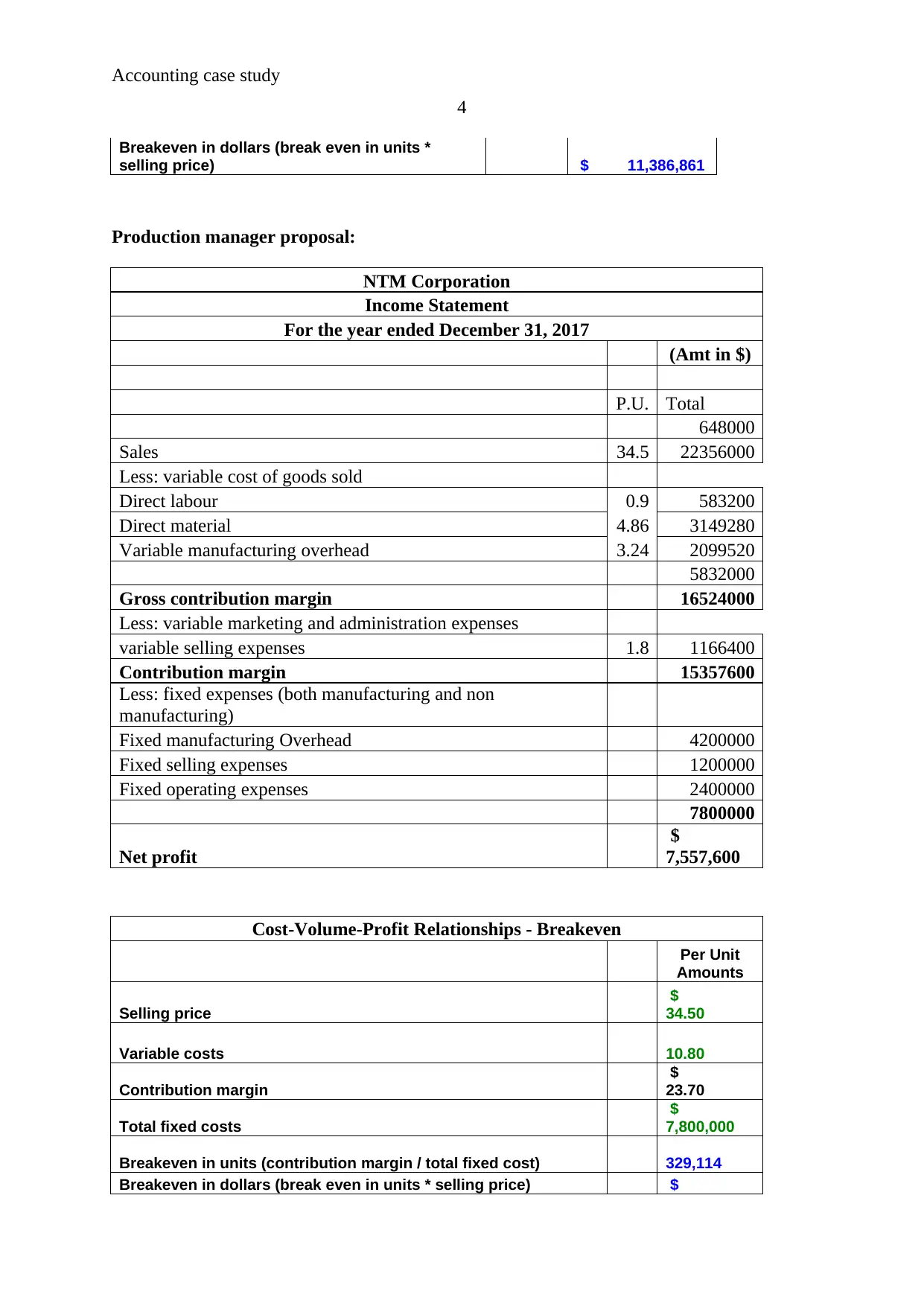

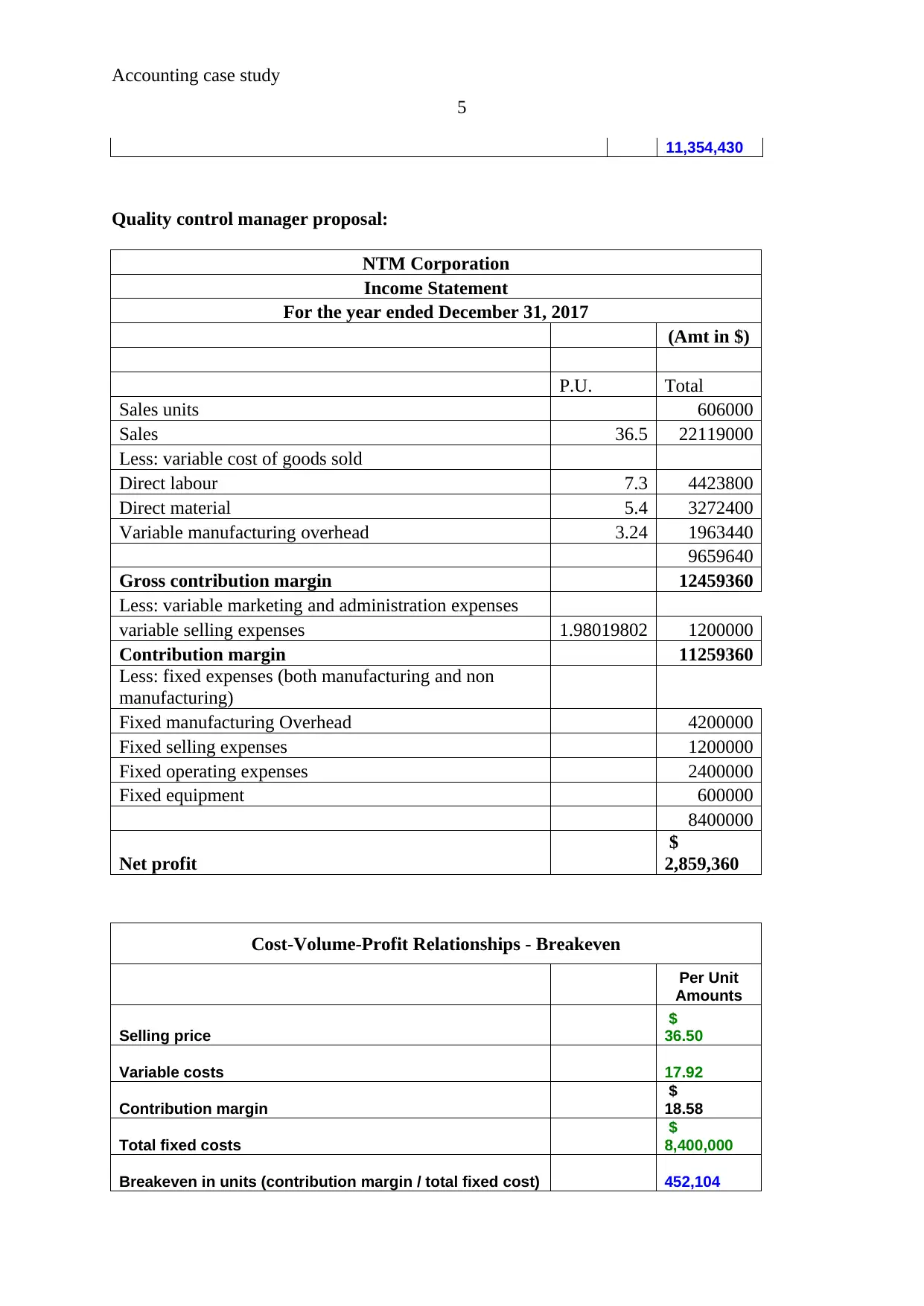

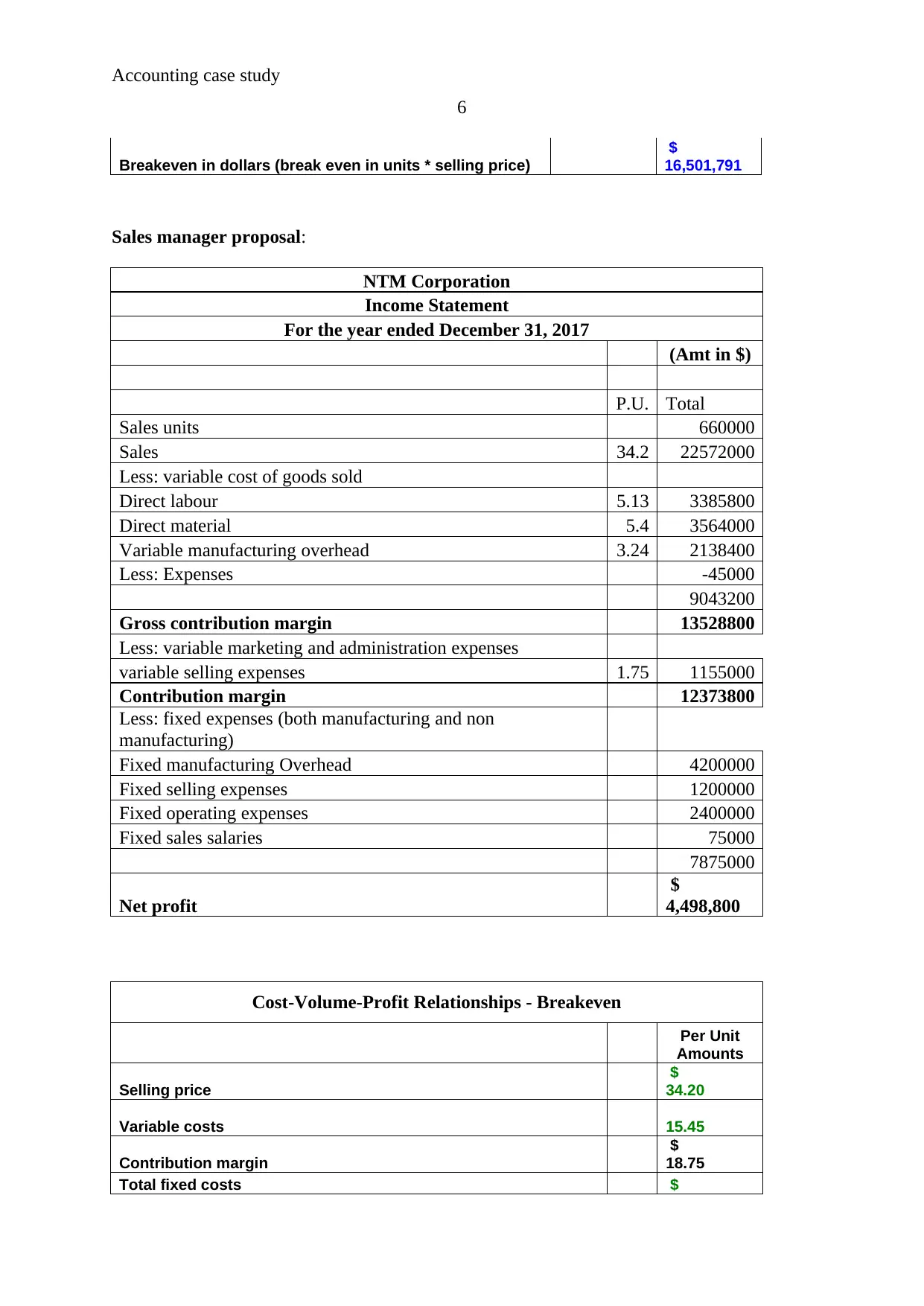

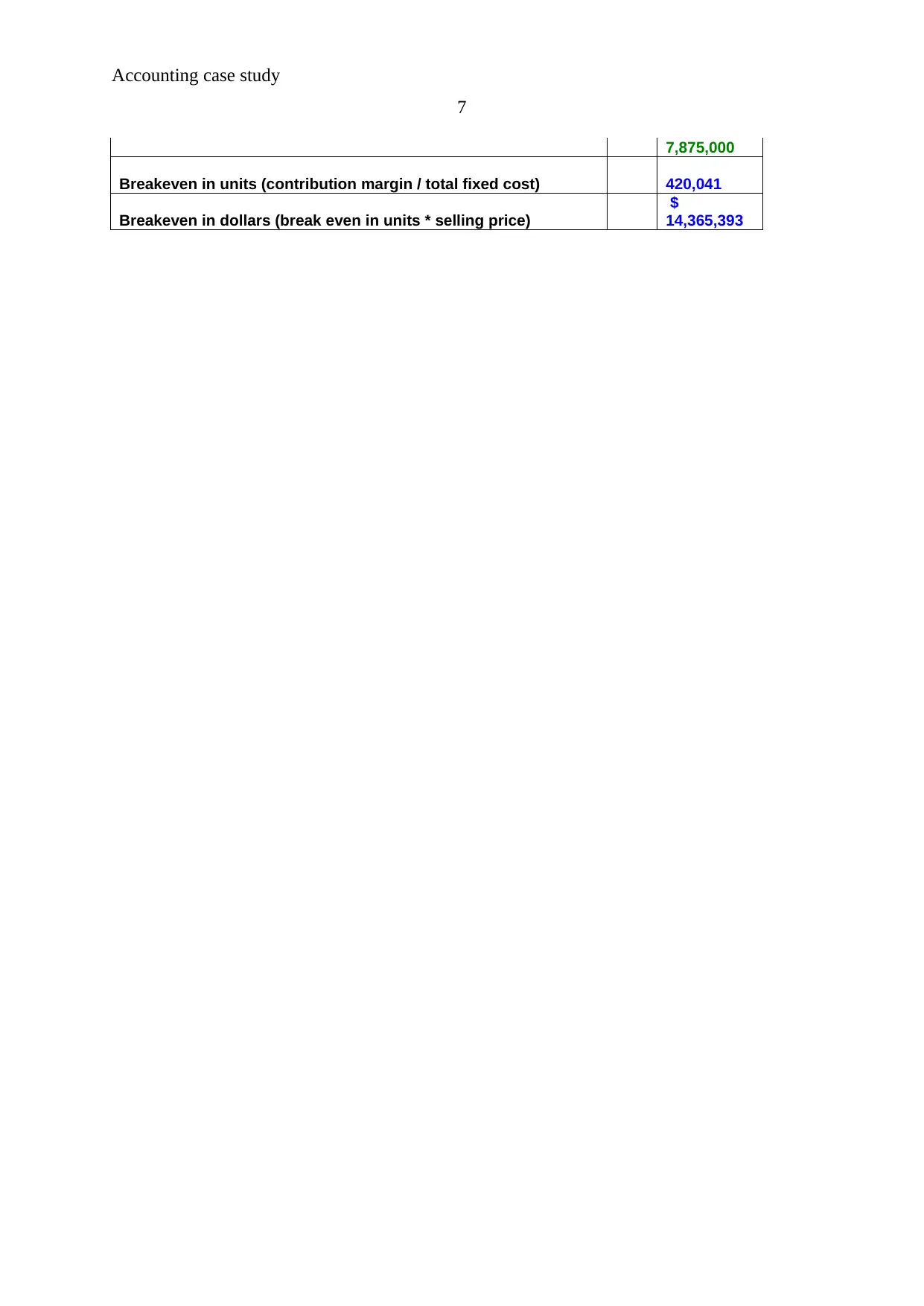

This case study report analyzes the cost-volume-profit (CVP) of NTM Corporation to determine strategies for increasing profitability. The analysis includes the preparation of a contribution format income statement for 2017, calculating break-even sales in units and dollars. The report then evaluates proposals from the Production Manager, Quality Control Manager, and Sales Manager, each suggesting changes to reduce costs or increase sales volume. The Production Manager's proposal involves reducing material costs and lowering sales price. The Quality Control Manager's proposal focuses on improving sales volume, and the Sales Manager's proposal focuses on increasing sales volume. The report calculates the financial impact, break-even points, and net profit for each proposal. The analysis concludes that the Quality Control Manager's proposal is the most beneficial, recommending its implementation to the CFO, Myrna Snowflake, based on its positive impact on profitability and break-even units. The report also provides detailed income statements and calculations for each scenario, including references to relevant financial management texts.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.