Financial Performance Analysis: Tesco vs. Sainsbury - MBA Assignment

VerifiedAdded on 2023/01/17

|34

|6180

|26

Report

AI Summary

This MBA assignment analyzes the financial performance of Tesco and Sainsbury over a five-year period. The report begins with an introduction, followed by a background of both companies within the UK retail industry and their competitive positions. Section 2 conducts a comparative financial performance analysis using profitability, liquidity, and debt management ratios. Section 3 summarizes the analysis, concluding which company is financially stronger and justifying an investment recommendation. Finally, Section 4 identifies the limitations of the ratio analysis and assumptions made. The analysis includes asset utilization, margin analysis, returns, acid test ratio, cash ratio, current ratio, inventory period, accounts receivable period, accounts payable period, gearing ratio, and asset financing ratio. The report aims to provide a comprehensive understanding of the financial health of both companies to make informed investment decisions.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: MBA-FINANCIAL ANALYSIS AND MANAGEMENT

MBA-Financial Analysis and Management

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

MBA-Financial Analysis and Management

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1MBA-FINANCIAL ANALYSIS AND MANAGEMENT

Table of Contents

Introduction:....................................................................................................................................2

Section 1: Background of company and position in the industry in respect to its competitors.......2

Section 2: Five-year comparative financial performance analysis using ratios1............................3

Section 3: Summary analysis of which company is financially stronger; state and justify which

company’s shares would you buy..................................................................................................18

Section 4: Identify problems/limitations of the ratio analysis and assumptions you made in

comparative analysis......................................................................................................................20

Conclusion:....................................................................................................................................21

Reference and Bibliography:.........................................................................................................22

Appendices:...................................................................................................................................25

Table of Contents

Introduction:....................................................................................................................................2

Section 1: Background of company and position in the industry in respect to its competitors.......2

Section 2: Five-year comparative financial performance analysis using ratios1............................3

Section 3: Summary analysis of which company is financially stronger; state and justify which

company’s shares would you buy..................................................................................................18

Section 4: Identify problems/limitations of the ratio analysis and assumptions you made in

comparative analysis......................................................................................................................20

Conclusion:....................................................................................................................................21

Reference and Bibliography:.........................................................................................................22

Appendices:...................................................................................................................................25

2MBA-FINANCIAL ANALYSIS AND MANAGEMENT

Introduction:

The overall assessment mainly evaluates the financial performance of Tesco and

Sainsbury for the past five financial years. Adequate background evaluation has been conducted

for both the companies in respect to the industry and competitors. The background analysis

directly helps directly helps in detecting competitiveness of both the organization in the current

market. Furthermore, relevant ratios are used for identifying the current financial position of the

company and detect which organization is more profitable. This detection of the adequate

financial position of the organization would eventually help in determining the best investment

option. Lastly, relevant Limitations of the financial ratios are adequately depicted in the

assessment.

Section 1: Background of company and position in the industry in respect to its

competitors

The retail sector of the United Kingdom is considered to be one the major industries,

which can help in generating high level of income from operations. Moreover, Sainsbury and

Tesco are mainly considered to be one of the major players in the retail industry, as their

operations are worldwide and generate high level of income from operations. The British

multinational groceries and general merchandise retailer was founded 100 years ago and has

been successfully operating since. The company has been making adequate profits from

operations, which led to 1,208 million in 2018 (About.sainsburys.co.uk 2019). Sainsbury is

considered to be the third largest chain of supermarkets in United Kingdom, where the overall

operations has been conducted for the past 150 years. The company operations have been

Introduction:

The overall assessment mainly evaluates the financial performance of Tesco and

Sainsbury for the past five financial years. Adequate background evaluation has been conducted

for both the companies in respect to the industry and competitors. The background analysis

directly helps directly helps in detecting competitiveness of both the organization in the current

market. Furthermore, relevant ratios are used for identifying the current financial position of the

company and detect which organization is more profitable. This detection of the adequate

financial position of the organization would eventually help in determining the best investment

option. Lastly, relevant Limitations of the financial ratios are adequately depicted in the

assessment.

Section 1: Background of company and position in the industry in respect to its

competitors

The retail sector of the United Kingdom is considered to be one the major industries,

which can help in generating high level of income from operations. Moreover, Sainsbury and

Tesco are mainly considered to be one of the major players in the retail industry, as their

operations are worldwide and generate high level of income from operations. The British

multinational groceries and general merchandise retailer was founded 100 years ago and has

been successfully operating since. The company has been making adequate profits from

operations, which led to 1,208 million in 2018 (About.sainsburys.co.uk 2019). Sainsbury is

considered to be the third largest chain of supermarkets in United Kingdom, where the overall

operations has been conducted for the past 150 years. The company operations have been

3MBA-FINANCIAL ANALYSIS AND MANAGEMENT

increasing over time, where the current net income for the organisation was at the level of 309

million (Tesco plc 2019).

Both the companies have been one of the major contributors in the retail industry, where

the operations are increasing over the period of time. Hence, from the evaluation, it can be

detected that both the companies are giants in the retail industry where Tesco leads the market

with higher market share and profitability. On the other hand, Sainsbury was the largest retailer

in UK until Tesco gradually started to conquer the market in the late 1990s. The changing

business environment has mainly increased the possibility of new retail companies to flourish,

while both Tesco and Sainsbury has moved their operations from actual retail shop to the virtual

world such a websites and mobile applications.

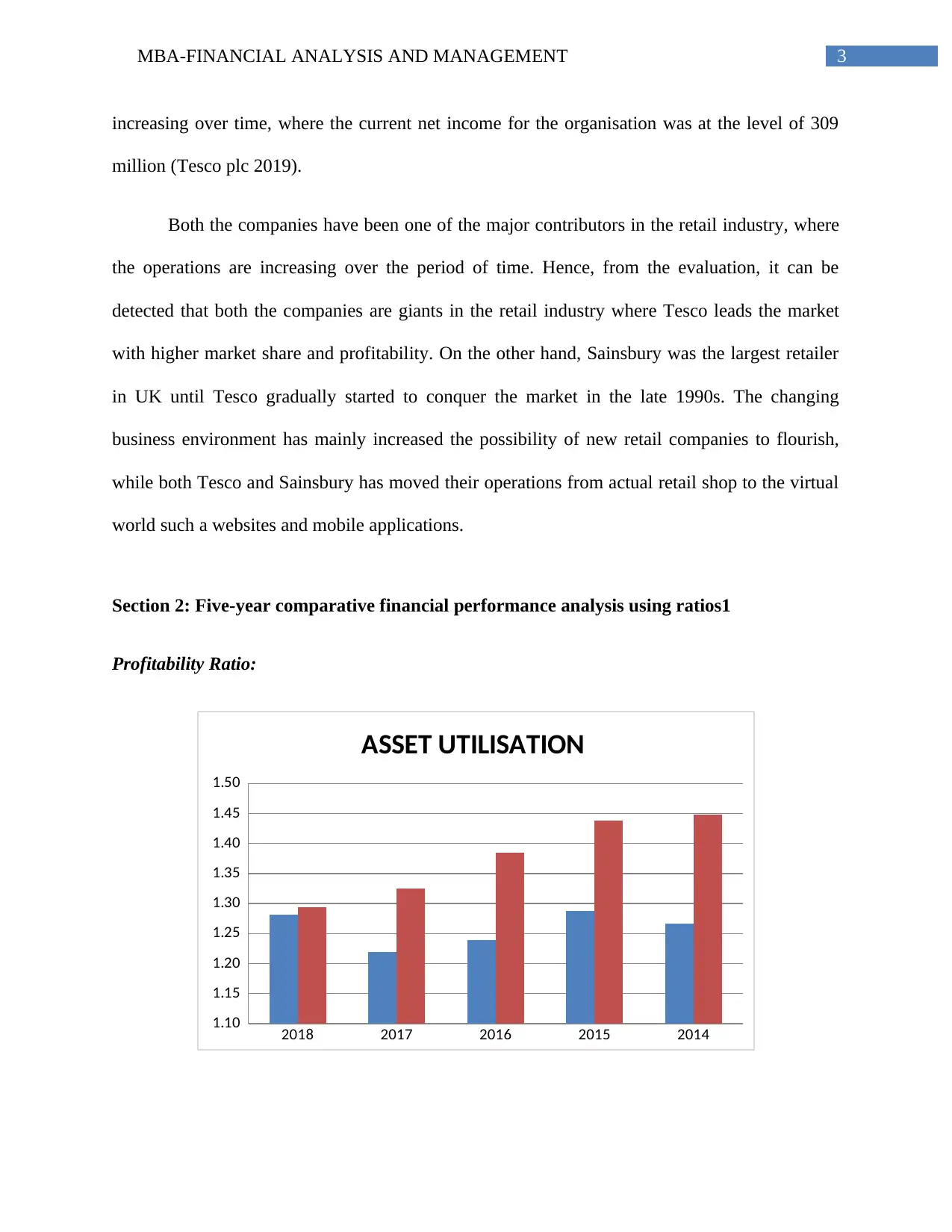

Section 2: Five-year comparative financial performance analysis using ratios1

Profitability Ratio:

2018 2017 2016 2015 2014

1.10

1.15

1.20

1.25

1.30

1.35

1.40

1.45

1.50

ASSET UTILISATION

increasing over time, where the current net income for the organisation was at the level of 309

million (Tesco plc 2019).

Both the companies have been one of the major contributors in the retail industry, where

the operations are increasing over the period of time. Hence, from the evaluation, it can be

detected that both the companies are giants in the retail industry where Tesco leads the market

with higher market share and profitability. On the other hand, Sainsbury was the largest retailer

in UK until Tesco gradually started to conquer the market in the late 1990s. The changing

business environment has mainly increased the possibility of new retail companies to flourish,

while both Tesco and Sainsbury has moved their operations from actual retail shop to the virtual

world such a websites and mobile applications.

Section 2: Five-year comparative financial performance analysis using ratios1

Profitability Ratio:

2018 2017 2016 2015 2014

1.10

1.15

1.20

1.25

1.30

1.35

1.40

1.45

1.50

ASSET UTILISATION

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4MBA-FINANCIAL ANALYSIS AND MANAGEMENT

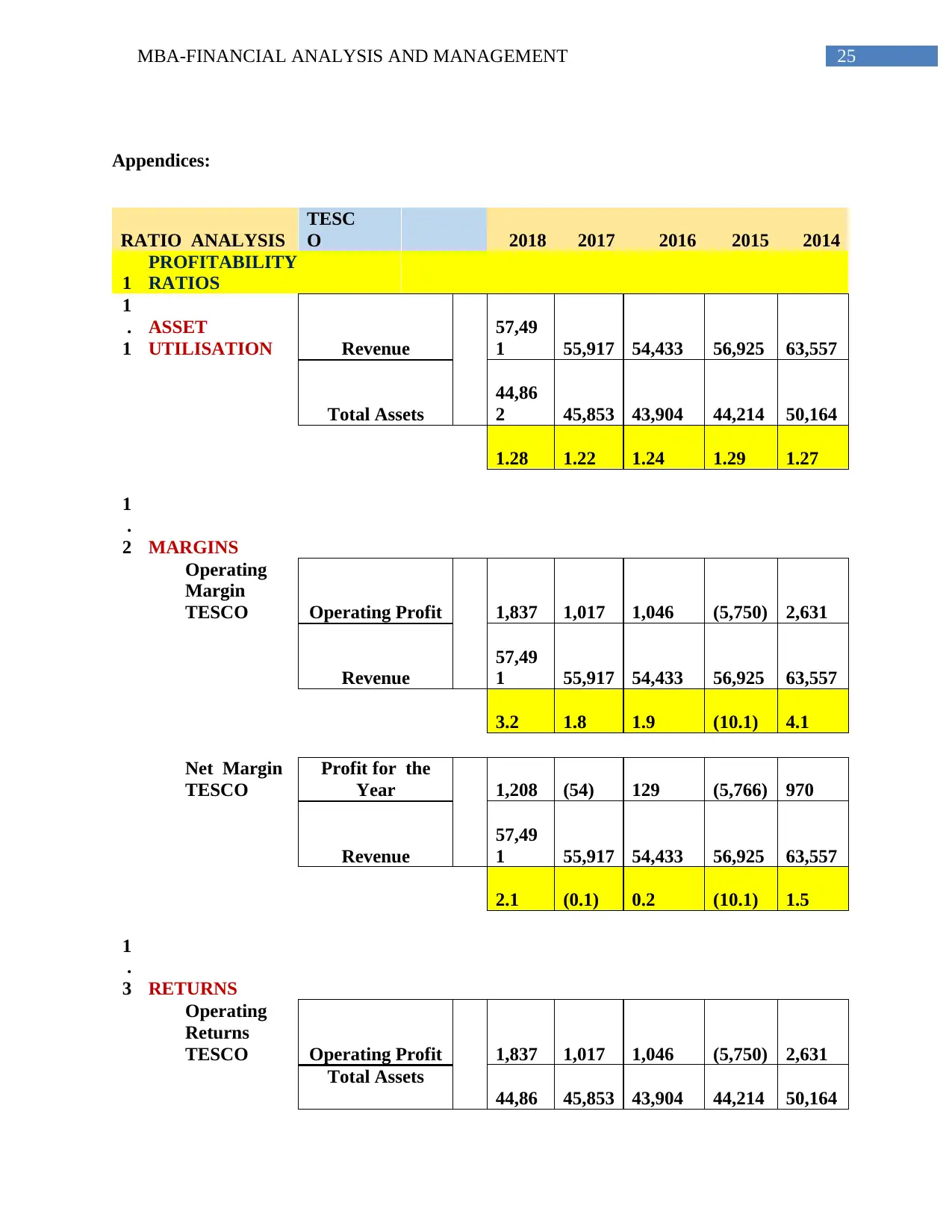

The Asset utilization of Tesco has relatively improved during the past 5 years from the

levels of 1.27 in 2014 to 1.28 in 2018. This improvement in the ratio is derived from the

declining values of total assets in comparison to its revenue. On the other hand, the overall asset

utilization of Sainsbury has declined from the level of 1.45 to 1.29 in 2018. Therefore, it could

be identified that Tesco’s management has effectively used their resource to generate high

revenue from operations. Atoom, Malkawi and Al (2017) stated that with the help of asset

utilization ratio investor able to understand the current management efficiency and utilizing the

available resources to maximize the revenues generated from operations.

2018 2017 2016 2015 2014

(12.0)

(10.0)

(8.0)

(6.0)

(4.0)

(2.0)

-

2.0

4.0

6.0

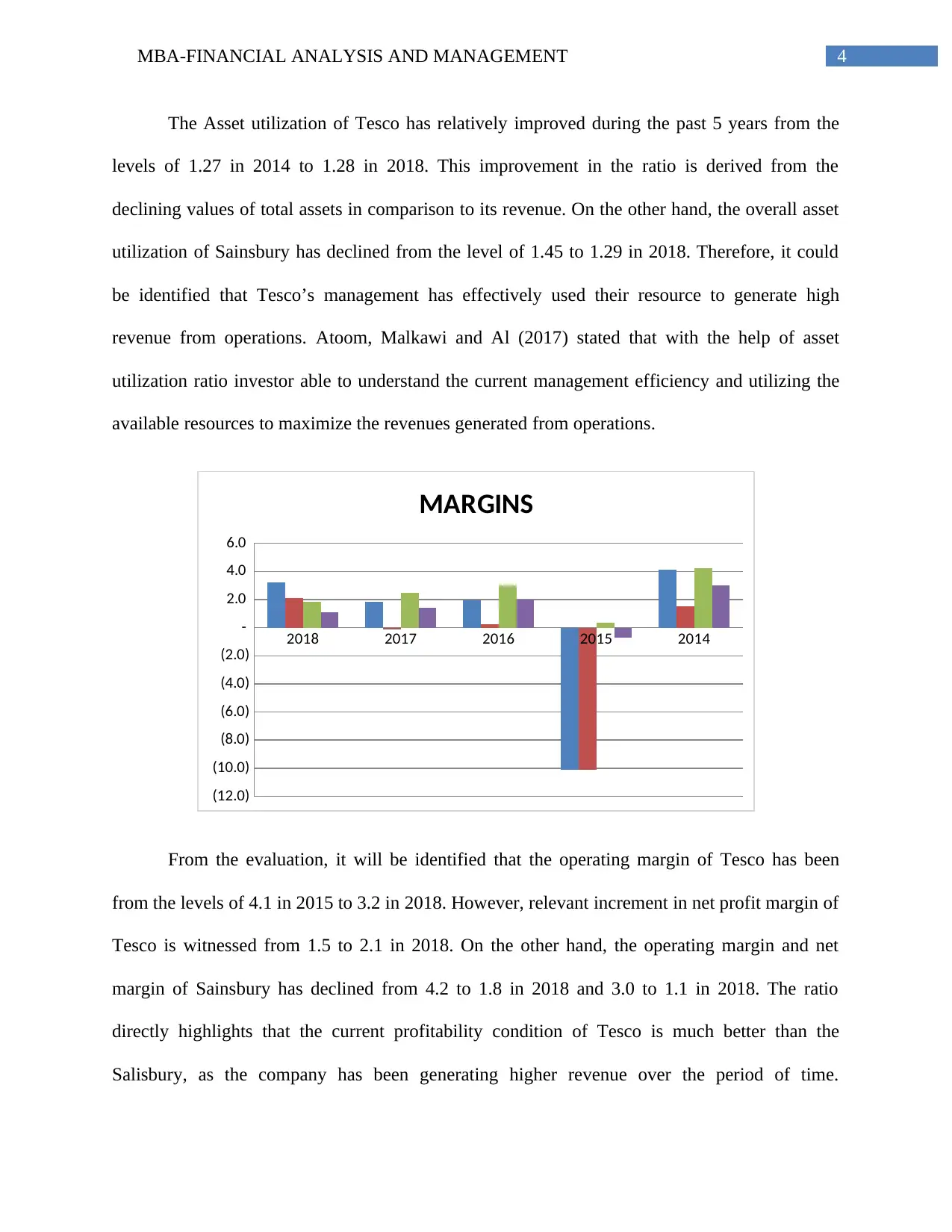

MARGINS

From the evaluation, it will be identified that the operating margin of Tesco has been

from the levels of 4.1 in 2015 to 3.2 in 2018. However, relevant increment in net profit margin of

Tesco is witnessed from 1.5 to 2.1 in 2018. On the other hand, the operating margin and net

margin of Sainsbury has declined from 4.2 to 1.8 in 2018 and 3.0 to 1.1 in 2018. The ratio

directly highlights that the current profitability condition of Tesco is much better than the

Salisbury, as the company has been generating higher revenue over the period of time.

The Asset utilization of Tesco has relatively improved during the past 5 years from the

levels of 1.27 in 2014 to 1.28 in 2018. This improvement in the ratio is derived from the

declining values of total assets in comparison to its revenue. On the other hand, the overall asset

utilization of Sainsbury has declined from the level of 1.45 to 1.29 in 2018. Therefore, it could

be identified that Tesco’s management has effectively used their resource to generate high

revenue from operations. Atoom, Malkawi and Al (2017) stated that with the help of asset

utilization ratio investor able to understand the current management efficiency and utilizing the

available resources to maximize the revenues generated from operations.

2018 2017 2016 2015 2014

(12.0)

(10.0)

(8.0)

(6.0)

(4.0)

(2.0)

-

2.0

4.0

6.0

MARGINS

From the evaluation, it will be identified that the operating margin of Tesco has been

from the levels of 4.1 in 2015 to 3.2 in 2018. However, relevant increment in net profit margin of

Tesco is witnessed from 1.5 to 2.1 in 2018. On the other hand, the operating margin and net

margin of Sainsbury has declined from 4.2 to 1.8 in 2018 and 3.0 to 1.1 in 2018. The ratio

directly highlights that the current profitability condition of Tesco is much better than the

Salisbury, as the company has been generating higher revenue over the period of time.

5MBA-FINANCIAL ANALYSIS AND MANAGEMENT

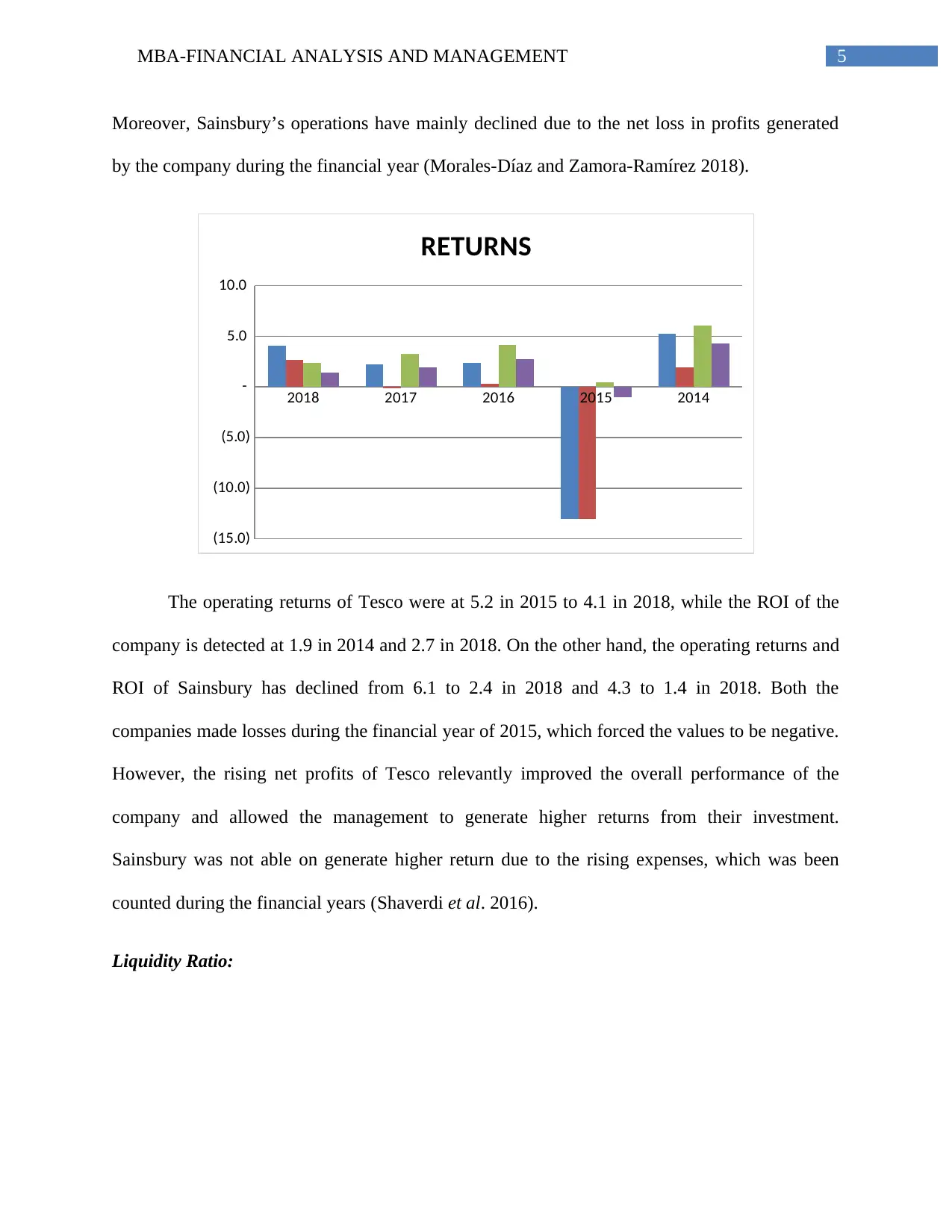

Moreover, Sainsbury’s operations have mainly declined due to the net loss in profits generated

by the company during the financial year (Morales-Díaz and Zamora-Ramírez 2018).

2018 2017 2016 2015 2014

(15.0)

(10.0)

(5.0)

-

5.0

10.0

RETURNS

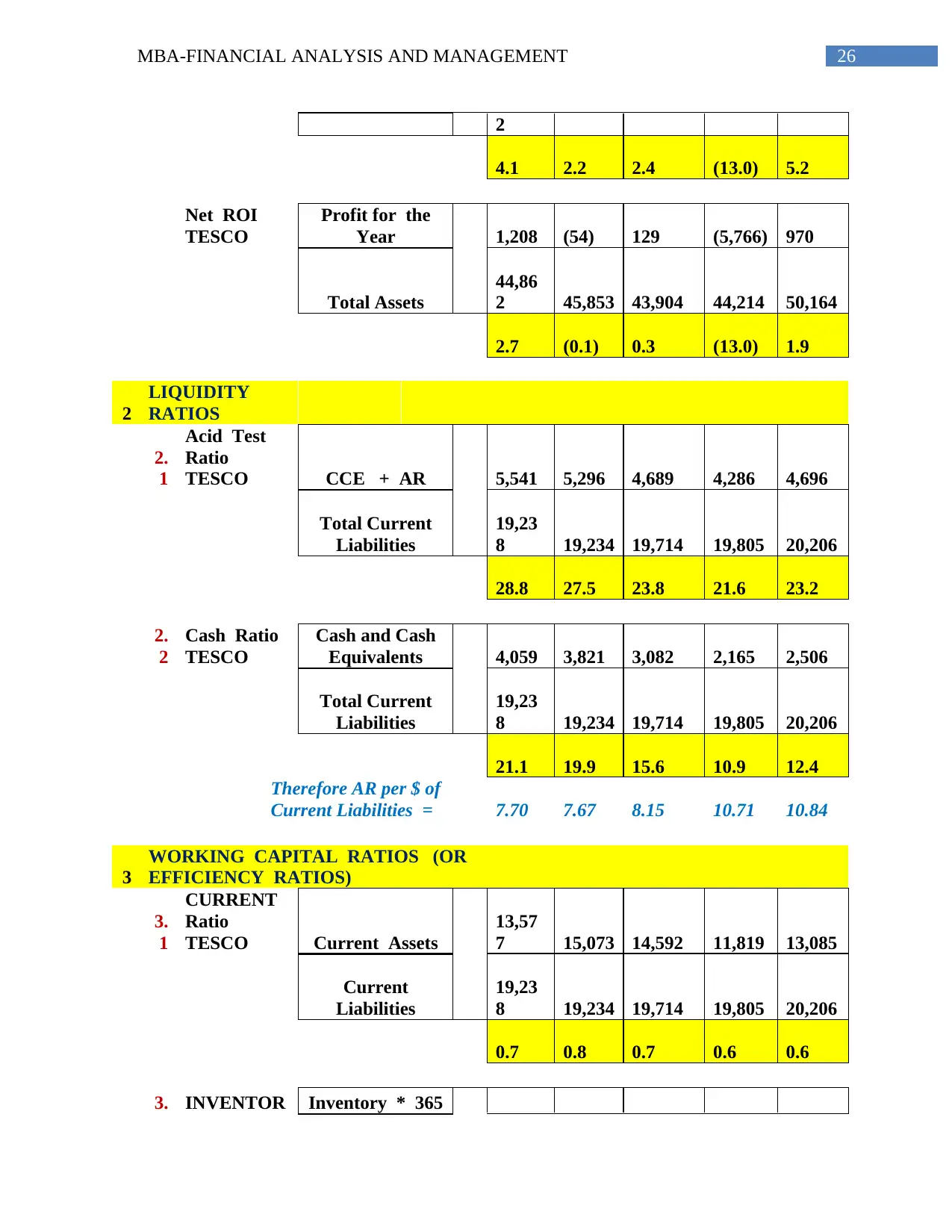

The operating returns of Tesco were at 5.2 in 2015 to 4.1 in 2018, while the ROI of the

company is detected at 1.9 in 2014 and 2.7 in 2018. On the other hand, the operating returns and

ROI of Sainsbury has declined from 6.1 to 2.4 in 2018 and 4.3 to 1.4 in 2018. Both the

companies made losses during the financial year of 2015, which forced the values to be negative.

However, the rising net profits of Tesco relevantly improved the overall performance of the

company and allowed the management to generate higher returns from their investment.

Sainsbury was not able on generate higher return due to the rising expenses, which was been

counted during the financial years (Shaverdi et al. 2016).

Liquidity Ratio:

Moreover, Sainsbury’s operations have mainly declined due to the net loss in profits generated

by the company during the financial year (Morales-Díaz and Zamora-Ramírez 2018).

2018 2017 2016 2015 2014

(15.0)

(10.0)

(5.0)

-

5.0

10.0

RETURNS

The operating returns of Tesco were at 5.2 in 2015 to 4.1 in 2018, while the ROI of the

company is detected at 1.9 in 2014 and 2.7 in 2018. On the other hand, the operating returns and

ROI of Sainsbury has declined from 6.1 to 2.4 in 2018 and 4.3 to 1.4 in 2018. Both the

companies made losses during the financial year of 2015, which forced the values to be negative.

However, the rising net profits of Tesco relevantly improved the overall performance of the

company and allowed the management to generate higher returns from their investment.

Sainsbury was not able on generate higher return due to the rising expenses, which was been

counted during the financial years (Shaverdi et al. 2016).

Liquidity Ratio:

6MBA-FINANCIAL ANALYSIS AND MANAGEMENT

2018 2017 2016 2015 2014

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

Acid Test Ratio

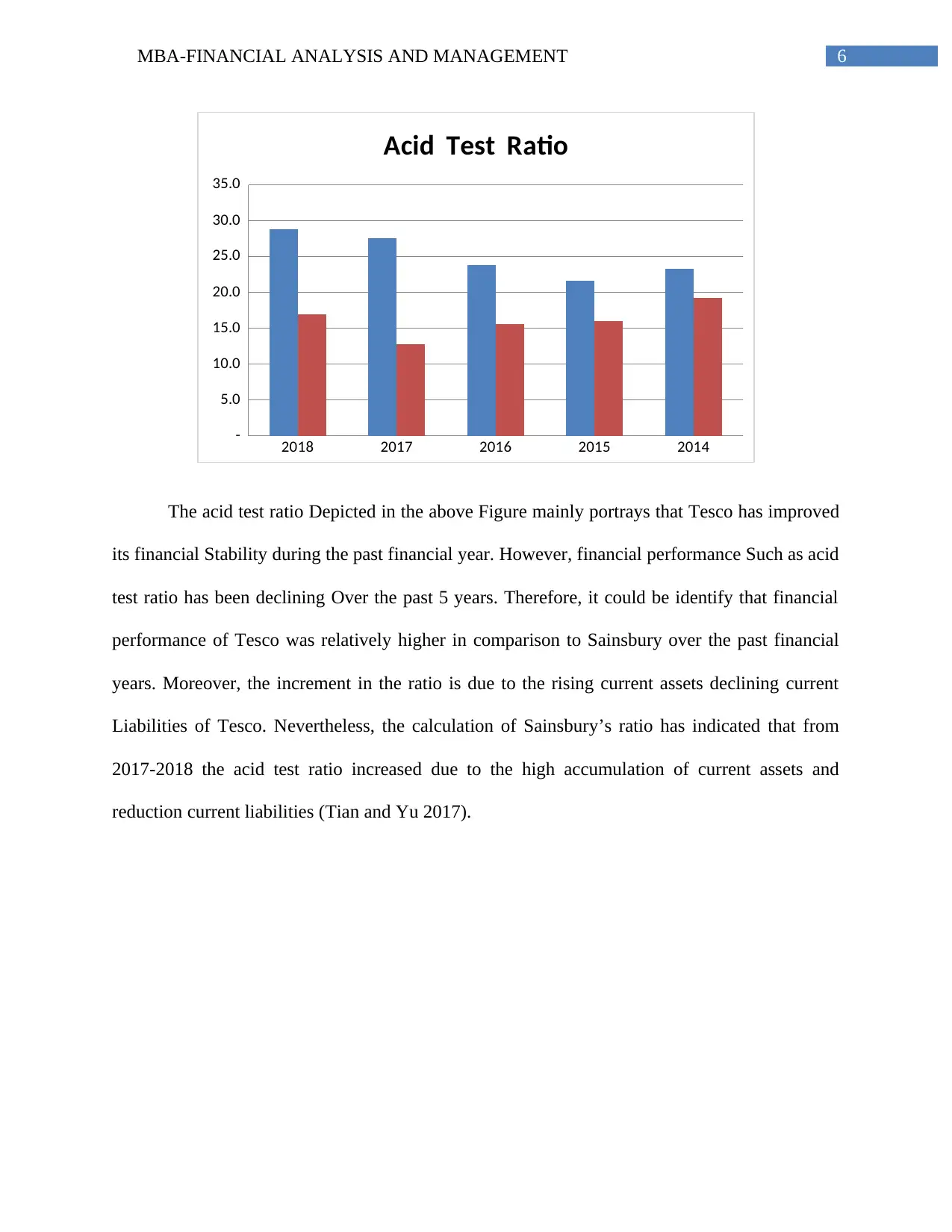

The acid test ratio Depicted in the above Figure mainly portrays that Tesco has improved

its financial Stability during the past financial year. However, financial performance Such as acid

test ratio has been declining Over the past 5 years. Therefore, it could be identify that financial

performance of Tesco was relatively higher in comparison to Sainsbury over the past financial

years. Moreover, the increment in the ratio is due to the rising current assets declining current

Liabilities of Tesco. Nevertheless, the calculation of Sainsbury’s ratio has indicated that from

2017-2018 the acid test ratio increased due to the high accumulation of current assets and

reduction current liabilities (Tian and Yu 2017).

2018 2017 2016 2015 2014

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

Acid Test Ratio

The acid test ratio Depicted in the above Figure mainly portrays that Tesco has improved

its financial Stability during the past financial year. However, financial performance Such as acid

test ratio has been declining Over the past 5 years. Therefore, it could be identify that financial

performance of Tesco was relatively higher in comparison to Sainsbury over the past financial

years. Moreover, the increment in the ratio is due to the rising current assets declining current

Liabilities of Tesco. Nevertheless, the calculation of Sainsbury’s ratio has indicated that from

2017-2018 the acid test ratio increased due to the high accumulation of current assets and

reduction current liabilities (Tian and Yu 2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MBA-FINANCIAL ANALYSIS AND MANAGEMENT

2018 2017 2016 2015 2014

-

5.0

10.0

15.0

20.0

25.0

Cash Ratio

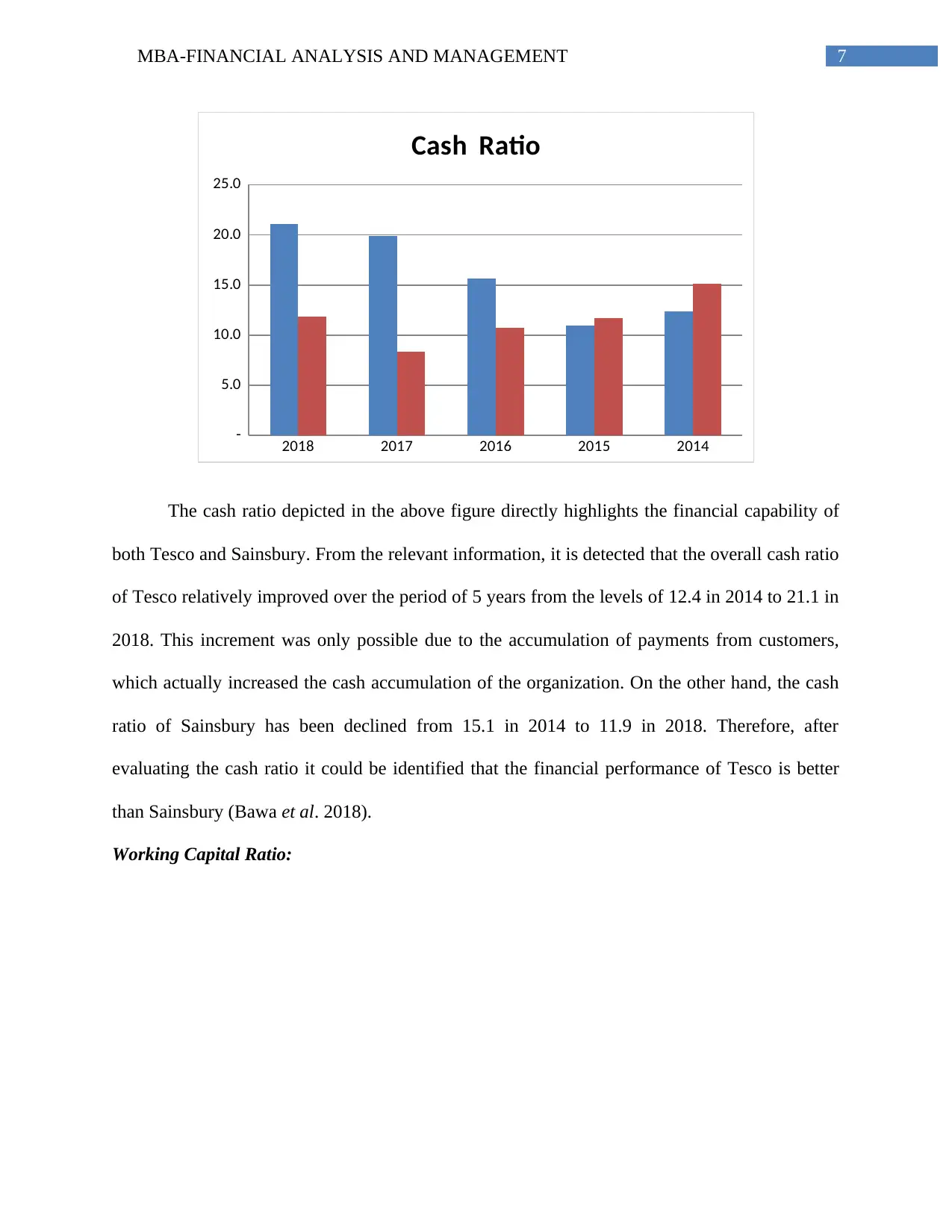

The cash ratio depicted in the above figure directly highlights the financial capability of

both Tesco and Sainsbury. From the relevant information, it is detected that the overall cash ratio

of Tesco relatively improved over the period of 5 years from the levels of 12.4 in 2014 to 21.1 in

2018. This increment was only possible due to the accumulation of payments from customers,

which actually increased the cash accumulation of the organization. On the other hand, the cash

ratio of Sainsbury has been declined from 15.1 in 2014 to 11.9 in 2018. Therefore, after

evaluating the cash ratio it could be identified that the financial performance of Tesco is better

than Sainsbury (Bawa et al. 2018).

Working Capital Ratio:

2018 2017 2016 2015 2014

-

5.0

10.0

15.0

20.0

25.0

Cash Ratio

The cash ratio depicted in the above figure directly highlights the financial capability of

both Tesco and Sainsbury. From the relevant information, it is detected that the overall cash ratio

of Tesco relatively improved over the period of 5 years from the levels of 12.4 in 2014 to 21.1 in

2018. This increment was only possible due to the accumulation of payments from customers,

which actually increased the cash accumulation of the organization. On the other hand, the cash

ratio of Sainsbury has been declined from 15.1 in 2014 to 11.9 in 2018. Therefore, after

evaluating the cash ratio it could be identified that the financial performance of Tesco is better

than Sainsbury (Bawa et al. 2018).

Working Capital Ratio:

8MBA-FINANCIAL ANALYSIS AND MANAGEMENT

2018 2017 2016 2015 2014

-

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

Current Ratio

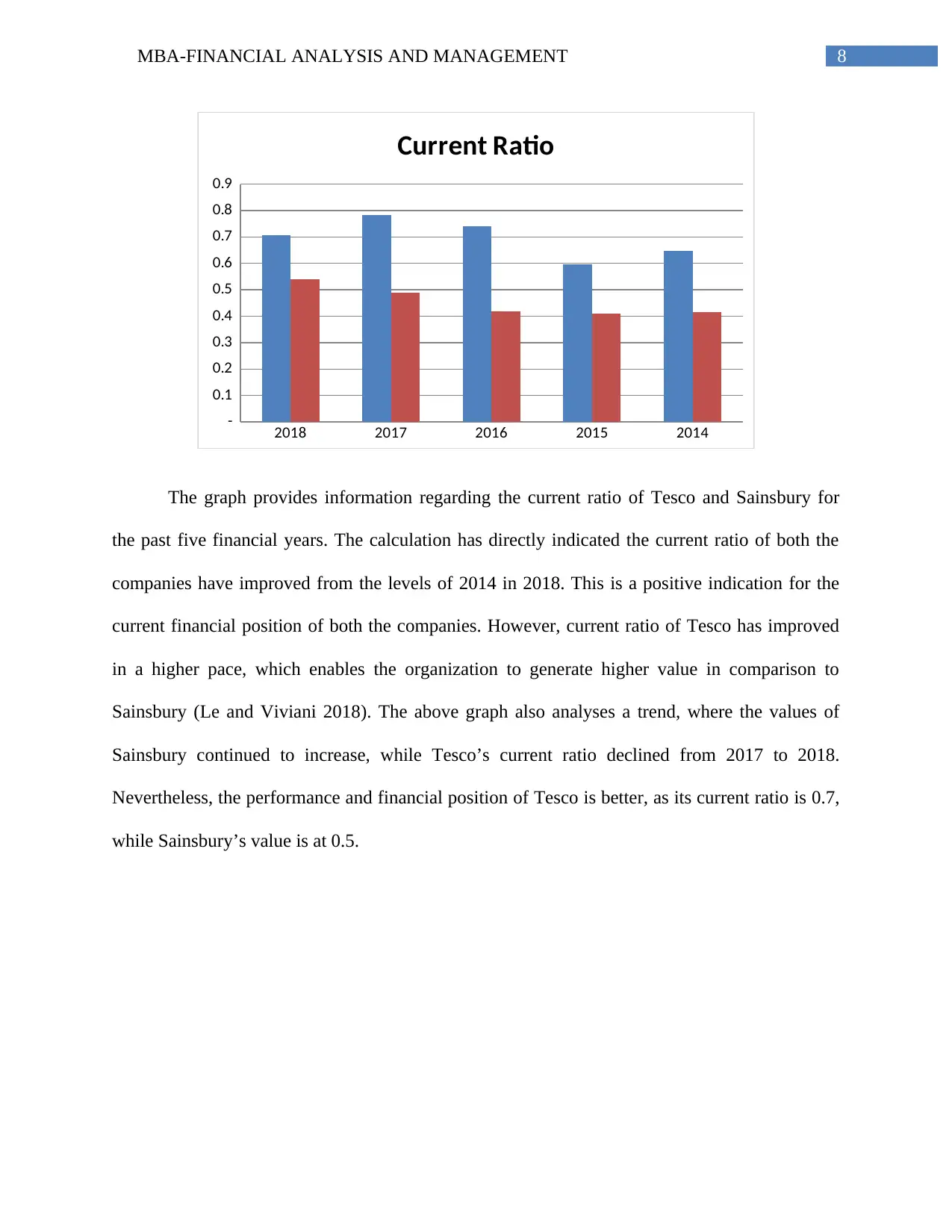

The graph provides information regarding the current ratio of Tesco and Sainsbury for

the past five financial years. The calculation has directly indicated the current ratio of both the

companies have improved from the levels of 2014 in 2018. This is a positive indication for the

current financial position of both the companies. However, current ratio of Tesco has improved

in a higher pace, which enables the organization to generate higher value in comparison to

Sainsbury (Le and Viviani 2018). The above graph also analyses a trend, where the values of

Sainsbury continued to increase, while Tesco’s current ratio declined from 2017 to 2018.

Nevertheless, the performance and financial position of Tesco is better, as its current ratio is 0.7,

while Sainsbury’s value is at 0.5.

2018 2017 2016 2015 2014

-

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

Current Ratio

The graph provides information regarding the current ratio of Tesco and Sainsbury for

the past five financial years. The calculation has directly indicated the current ratio of both the

companies have improved from the levels of 2014 in 2018. This is a positive indication for the

current financial position of both the companies. However, current ratio of Tesco has improved

in a higher pace, which enables the organization to generate higher value in comparison to

Sainsbury (Le and Viviani 2018). The above graph also analyses a trend, where the values of

Sainsbury continued to increase, while Tesco’s current ratio declined from 2017 to 2018.

Nevertheless, the performance and financial position of Tesco is better, as its current ratio is 0.7,

while Sainsbury’s value is at 0.5.

9MBA-FINANCIAL ANALYSIS AND MANAGEMENT

2018 2017 2016 2015 2014

-

5.0

10.0

15.0

20.0

25.0

30.0

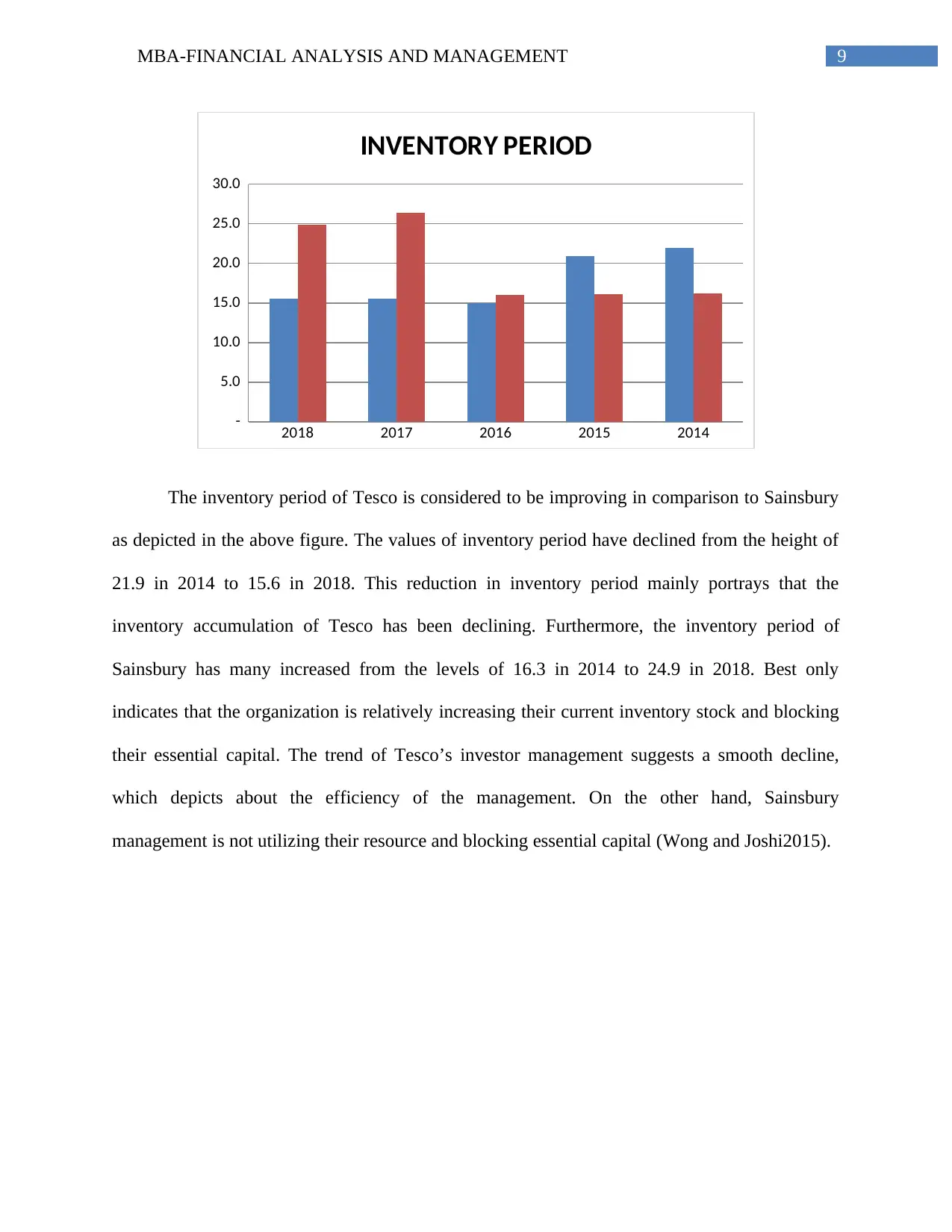

INVENTORY PERIOD

The inventory period of Tesco is considered to be improving in comparison to Sainsbury

as depicted in the above figure. The values of inventory period have declined from the height of

21.9 in 2014 to 15.6 in 2018. This reduction in inventory period mainly portrays that the

inventory accumulation of Tesco has been declining. Furthermore, the inventory period of

Sainsbury has many increased from the levels of 16.3 in 2014 to 24.9 in 2018. Best only

indicates that the organization is relatively increasing their current inventory stock and blocking

their essential capital. The trend of Tesco’s investor management suggests a smooth decline,

which depicts about the efficiency of the management. On the other hand, Sainsbury

management is not utilizing their resource and blocking essential capital (Wong and Joshi2015).

2018 2017 2016 2015 2014

-

5.0

10.0

15.0

20.0

25.0

30.0

INVENTORY PERIOD

The inventory period of Tesco is considered to be improving in comparison to Sainsbury

as depicted in the above figure. The values of inventory period have declined from the height of

21.9 in 2014 to 15.6 in 2018. This reduction in inventory period mainly portrays that the

inventory accumulation of Tesco has been declining. Furthermore, the inventory period of

Sainsbury has many increased from the levels of 16.3 in 2014 to 24.9 in 2018. Best only

indicates that the organization is relatively increasing their current inventory stock and blocking

their essential capital. The trend of Tesco’s investor management suggests a smooth decline,

which depicts about the efficiency of the management. On the other hand, Sainsbury

management is not utilizing their resource and blocking essential capital (Wong and Joshi2015).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10MBA-FINANCIAL ANALYSIS AND MANAGEMENT

2018 2017 2016 2015 2014

-

1,000.0

2,000.0

3,000.0

4,000.0

5,000.0

6,000.0

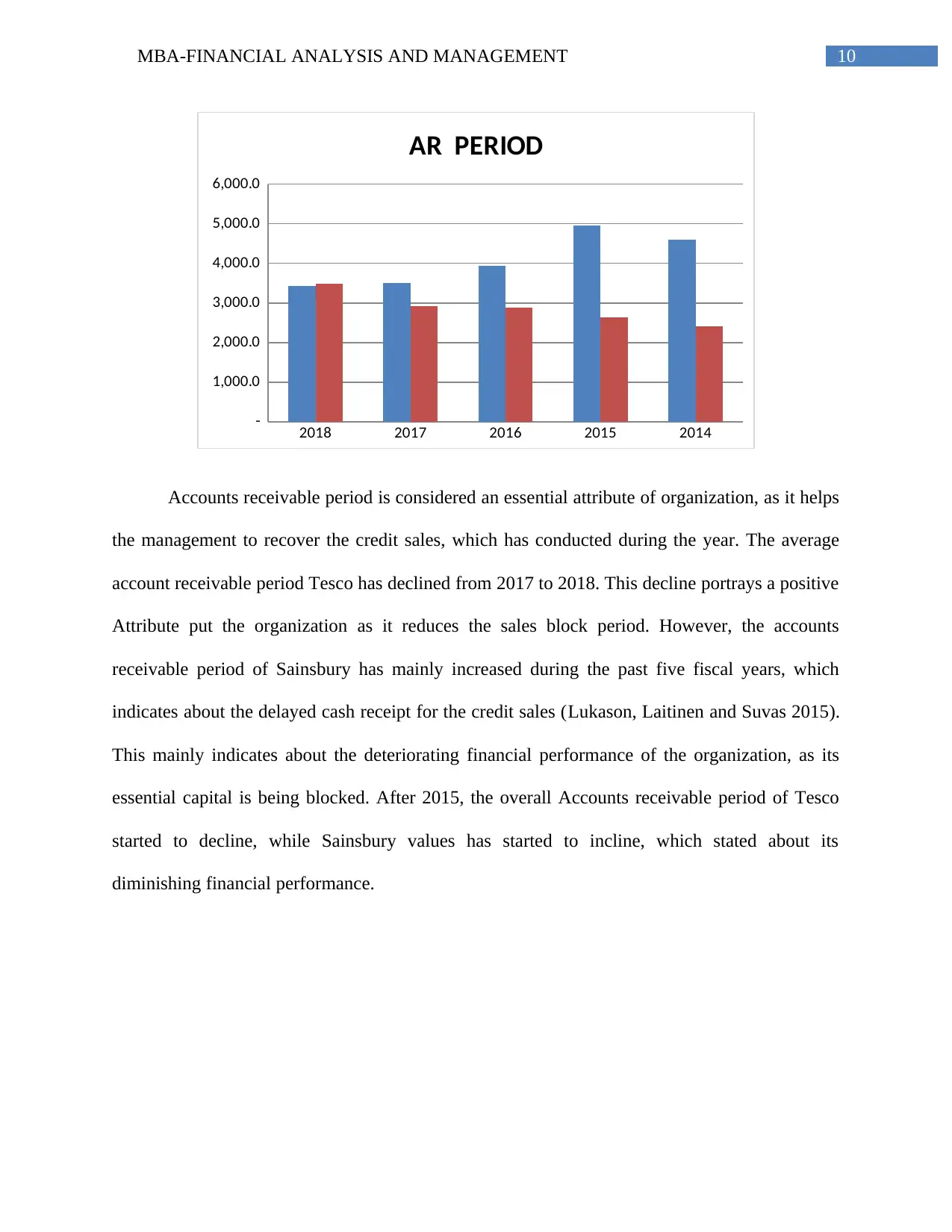

AR PERIOD

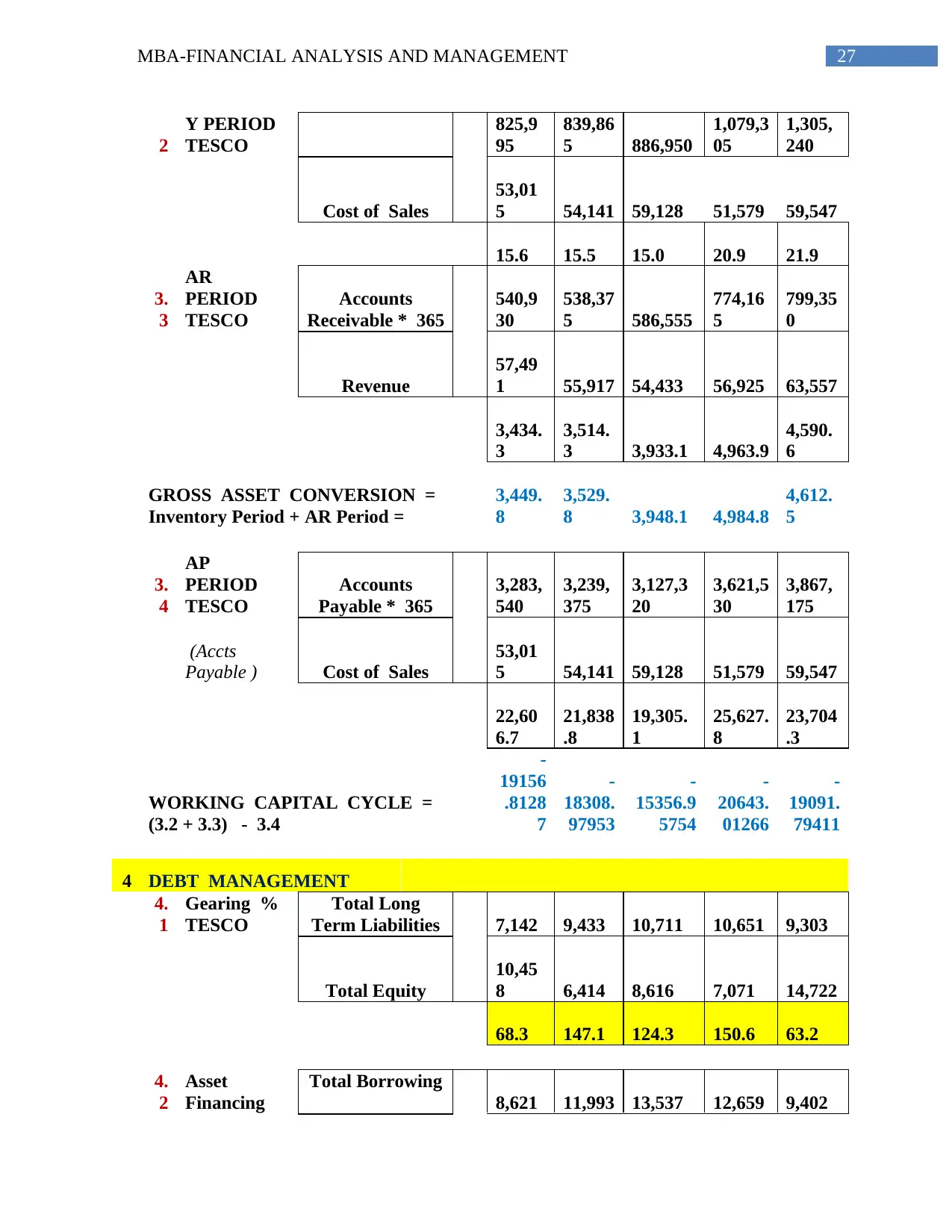

Accounts receivable period is considered an essential attribute of organization, as it helps

the management to recover the credit sales, which has conducted during the year. The average

account receivable period Tesco has declined from 2017 to 2018. This decline portrays a positive

Attribute put the organization as it reduces the sales block period. However, the accounts

receivable period of Sainsbury has mainly increased during the past five fiscal years, which

indicates about the delayed cash receipt for the credit sales (Lukason, Laitinen and Suvas 2015).

This mainly indicates about the deteriorating financial performance of the organization, as its

essential capital is being blocked. After 2015, the overall Accounts receivable period of Tesco

started to decline, while Sainsbury values has started to incline, which stated about its

diminishing financial performance.

2018 2017 2016 2015 2014

-

1,000.0

2,000.0

3,000.0

4,000.0

5,000.0

6,000.0

AR PERIOD

Accounts receivable period is considered an essential attribute of organization, as it helps

the management to recover the credit sales, which has conducted during the year. The average

account receivable period Tesco has declined from 2017 to 2018. This decline portrays a positive

Attribute put the organization as it reduces the sales block period. However, the accounts

receivable period of Sainsbury has mainly increased during the past five fiscal years, which

indicates about the delayed cash receipt for the credit sales (Lukason, Laitinen and Suvas 2015).

This mainly indicates about the deteriorating financial performance of the organization, as its

essential capital is being blocked. After 2015, the overall Accounts receivable period of Tesco

started to decline, while Sainsbury values has started to incline, which stated about its

diminishing financial performance.

11MBA-FINANCIAL ANALYSIS AND MANAGEMENT

2018 2017 2016 2015 2014

-

5,000.0

10,000.0

15,000.0

20,000.0

25,000.0

30,000.0

AP PERIOD

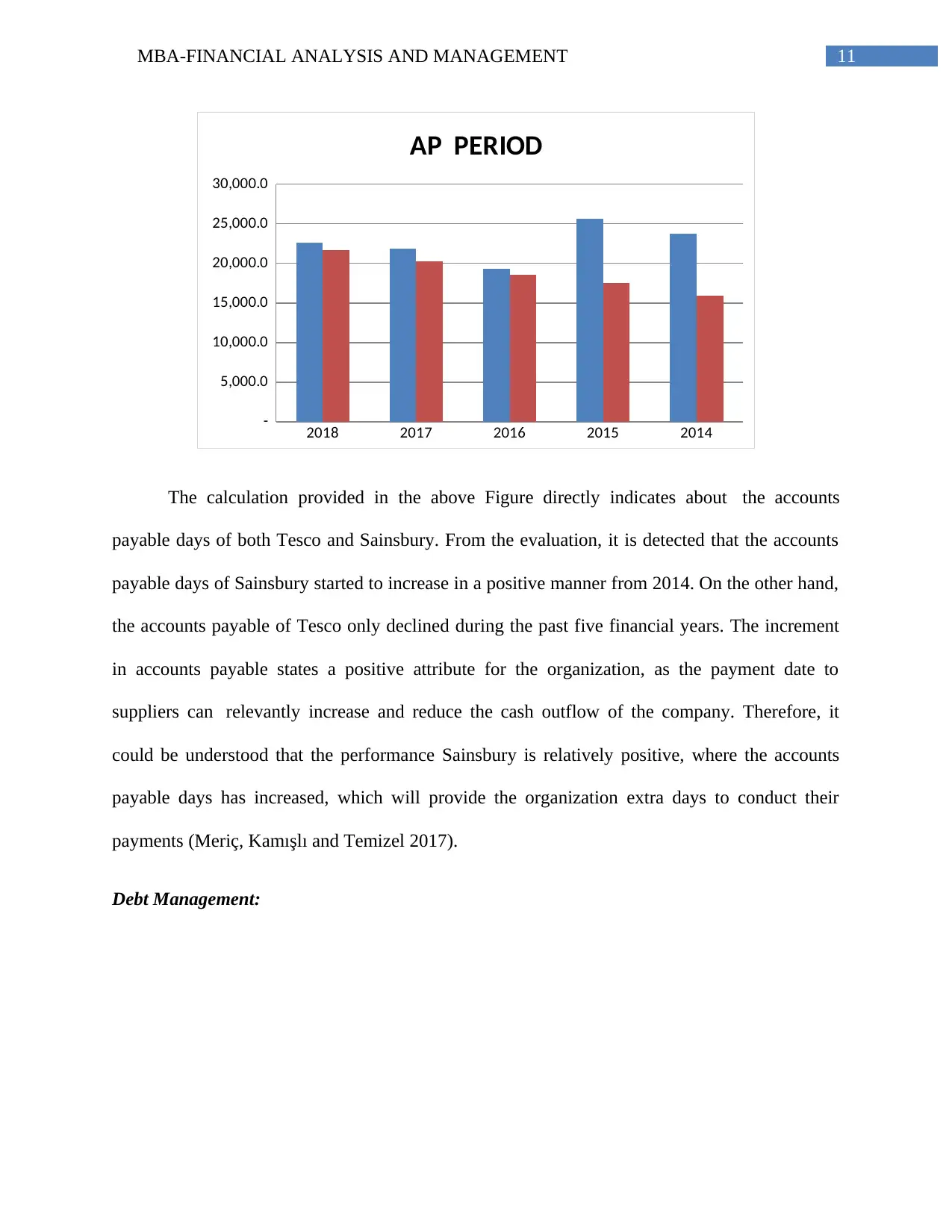

The calculation provided in the above Figure directly indicates about the accounts

payable days of both Tesco and Sainsbury. From the evaluation, it is detected that the accounts

payable days of Sainsbury started to increase in a positive manner from 2014. On the other hand,

the accounts payable of Tesco only declined during the past five financial years. The increment

in accounts payable states a positive attribute for the organization, as the payment date to

suppliers can relevantly increase and reduce the cash outflow of the company. Therefore, it

could be understood that the performance Sainsbury is relatively positive, where the accounts

payable days has increased, which will provide the organization extra days to conduct their

payments (Meriç, Kamışlı and Temizel 2017).

Debt Management:

2018 2017 2016 2015 2014

-

5,000.0

10,000.0

15,000.0

20,000.0

25,000.0

30,000.0

AP PERIOD

The calculation provided in the above Figure directly indicates about the accounts

payable days of both Tesco and Sainsbury. From the evaluation, it is detected that the accounts

payable days of Sainsbury started to increase in a positive manner from 2014. On the other hand,

the accounts payable of Tesco only declined during the past five financial years. The increment

in accounts payable states a positive attribute for the organization, as the payment date to

suppliers can relevantly increase and reduce the cash outflow of the company. Therefore, it

could be understood that the performance Sainsbury is relatively positive, where the accounts

payable days has increased, which will provide the organization extra days to conduct their

payments (Meriç, Kamışlı and Temizel 2017).

Debt Management:

12MBA-FINANCIAL ANALYSIS AND MANAGEMENT

2018 2017 2016 2015 2014

-

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

Gearing %

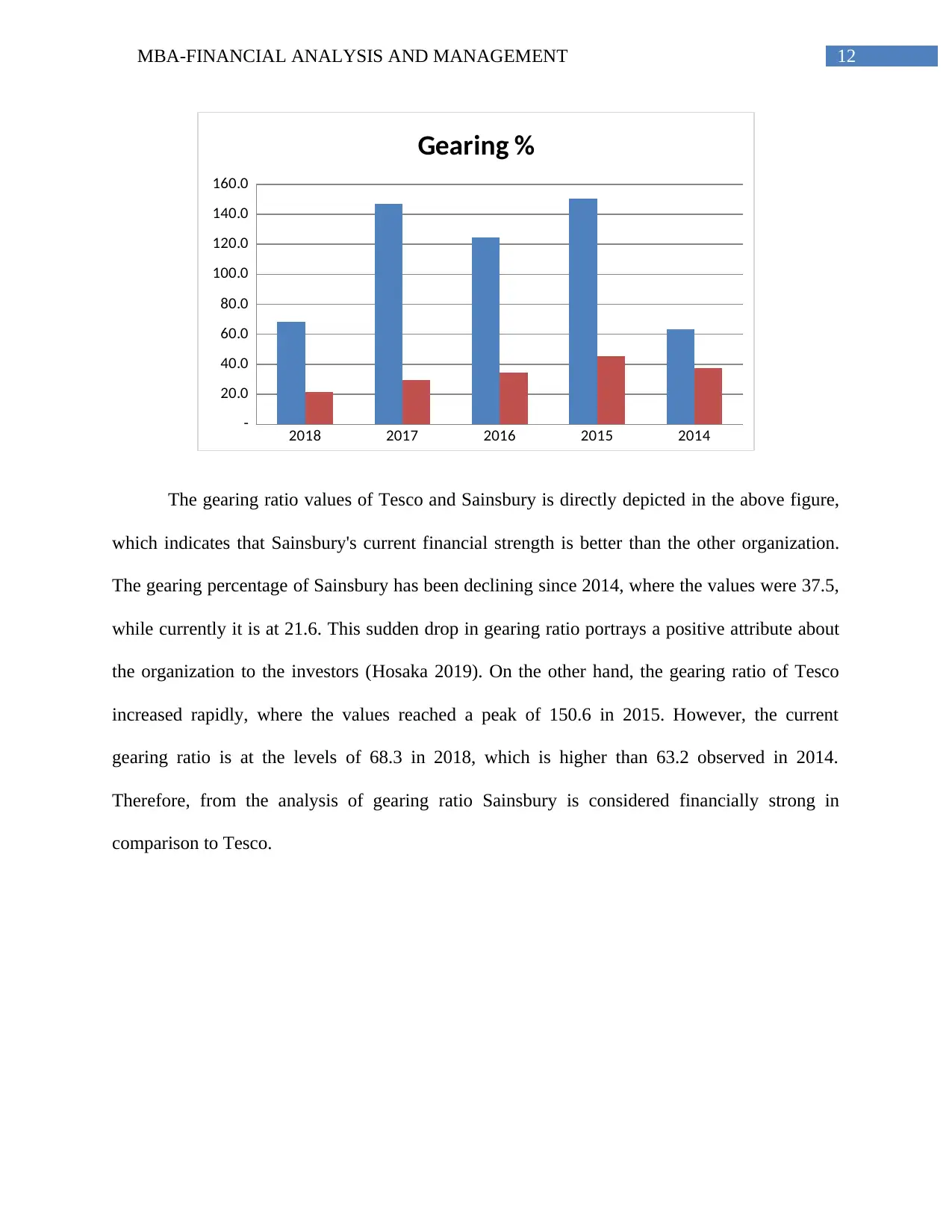

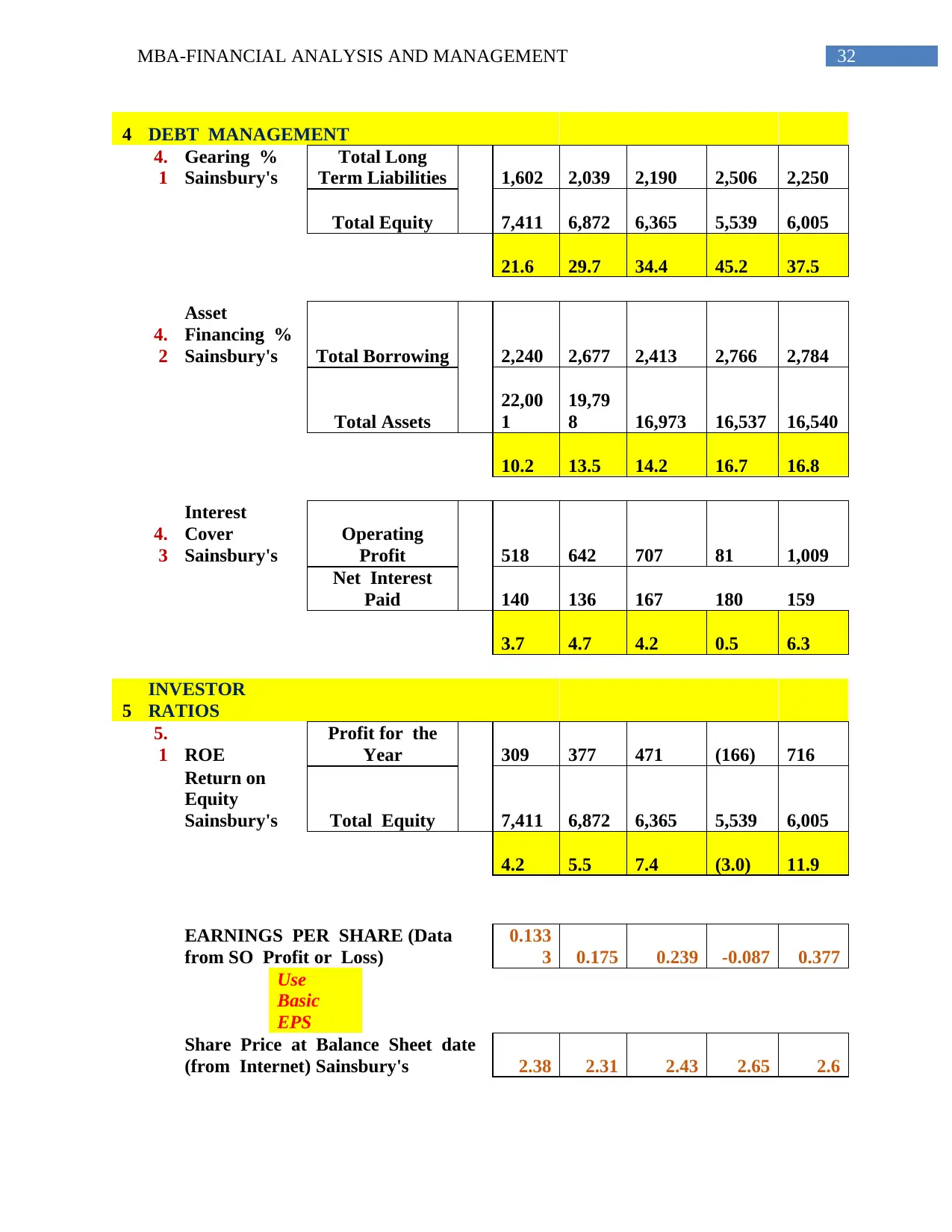

The gearing ratio values of Tesco and Sainsbury is directly depicted in the above figure,

which indicates that Sainsbury's current financial strength is better than the other organization.

The gearing percentage of Sainsbury has been declining since 2014, where the values were 37.5,

while currently it is at 21.6. This sudden drop in gearing ratio portrays a positive attribute about

the organization to the investors (Hosaka 2019). On the other hand, the gearing ratio of Tesco

increased rapidly, where the values reached a peak of 150.6 in 2015. However, the current

gearing ratio is at the levels of 68.3 in 2018, which is higher than 63.2 observed in 2014.

Therefore, from the analysis of gearing ratio Sainsbury is considered financially strong in

comparison to Tesco.

2018 2017 2016 2015 2014

-

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

Gearing %

The gearing ratio values of Tesco and Sainsbury is directly depicted in the above figure,

which indicates that Sainsbury's current financial strength is better than the other organization.

The gearing percentage of Sainsbury has been declining since 2014, where the values were 37.5,

while currently it is at 21.6. This sudden drop in gearing ratio portrays a positive attribute about

the organization to the investors (Hosaka 2019). On the other hand, the gearing ratio of Tesco

increased rapidly, where the values reached a peak of 150.6 in 2015. However, the current

gearing ratio is at the levels of 68.3 in 2018, which is higher than 63.2 observed in 2014.

Therefore, from the analysis of gearing ratio Sainsbury is considered financially strong in

comparison to Tesco.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13MBA-FINANCIAL ANALYSIS AND MANAGEMENT

2018 2017 2016 2015 2014

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

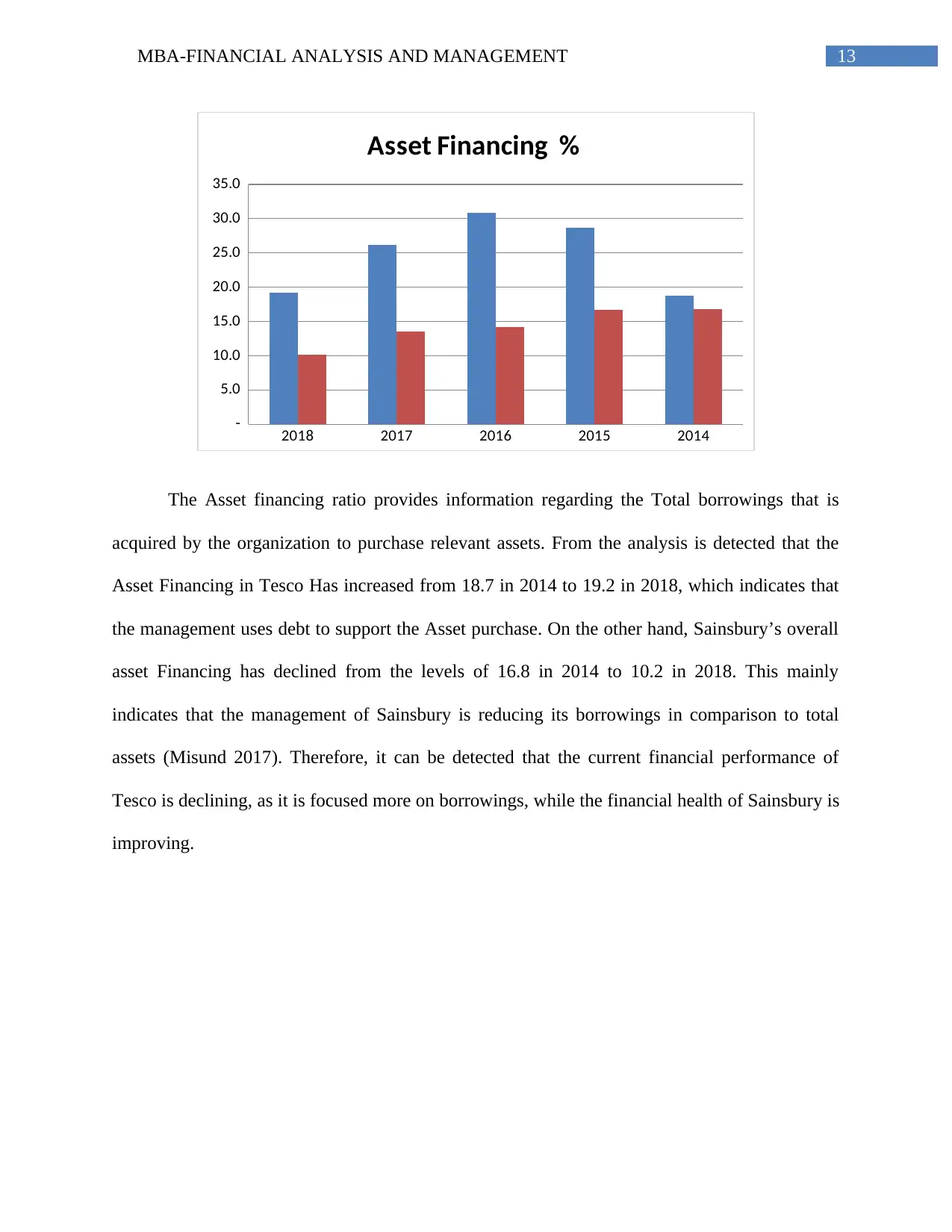

Asset Financing %

The Asset financing ratio provides information regarding the Total borrowings that is

acquired by the organization to purchase relevant assets. From the analysis is detected that the

Asset Financing in Tesco Has increased from 18.7 in 2014 to 19.2 in 2018, which indicates that

the management uses debt to support the Asset purchase. On the other hand, Sainsbury’s overall

asset Financing has declined from the levels of 16.8 in 2014 to 10.2 in 2018. This mainly

indicates that the management of Sainsbury is reducing its borrowings in comparison to total

assets (Misund 2017). Therefore, it can be detected that the current financial performance of

Tesco is declining, as it is focused more on borrowings, while the financial health of Sainsbury is

improving.

2018 2017 2016 2015 2014

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

Asset Financing %

The Asset financing ratio provides information regarding the Total borrowings that is

acquired by the organization to purchase relevant assets. From the analysis is detected that the

Asset Financing in Tesco Has increased from 18.7 in 2014 to 19.2 in 2018, which indicates that

the management uses debt to support the Asset purchase. On the other hand, Sainsbury’s overall

asset Financing has declined from the levels of 16.8 in 2014 to 10.2 in 2018. This mainly

indicates that the management of Sainsbury is reducing its borrowings in comparison to total

assets (Misund 2017). Therefore, it can be detected that the current financial performance of

Tesco is declining, as it is focused more on borrowings, while the financial health of Sainsbury is

improving.

14MBA-FINANCIAL ANALYSIS AND MANAGEMENT

2018 2017 2016 2015 2014

(10.0)

(8.0)

(6.0)

(4.0)

(2.0)

-

2.0

4.0

6.0

8.0

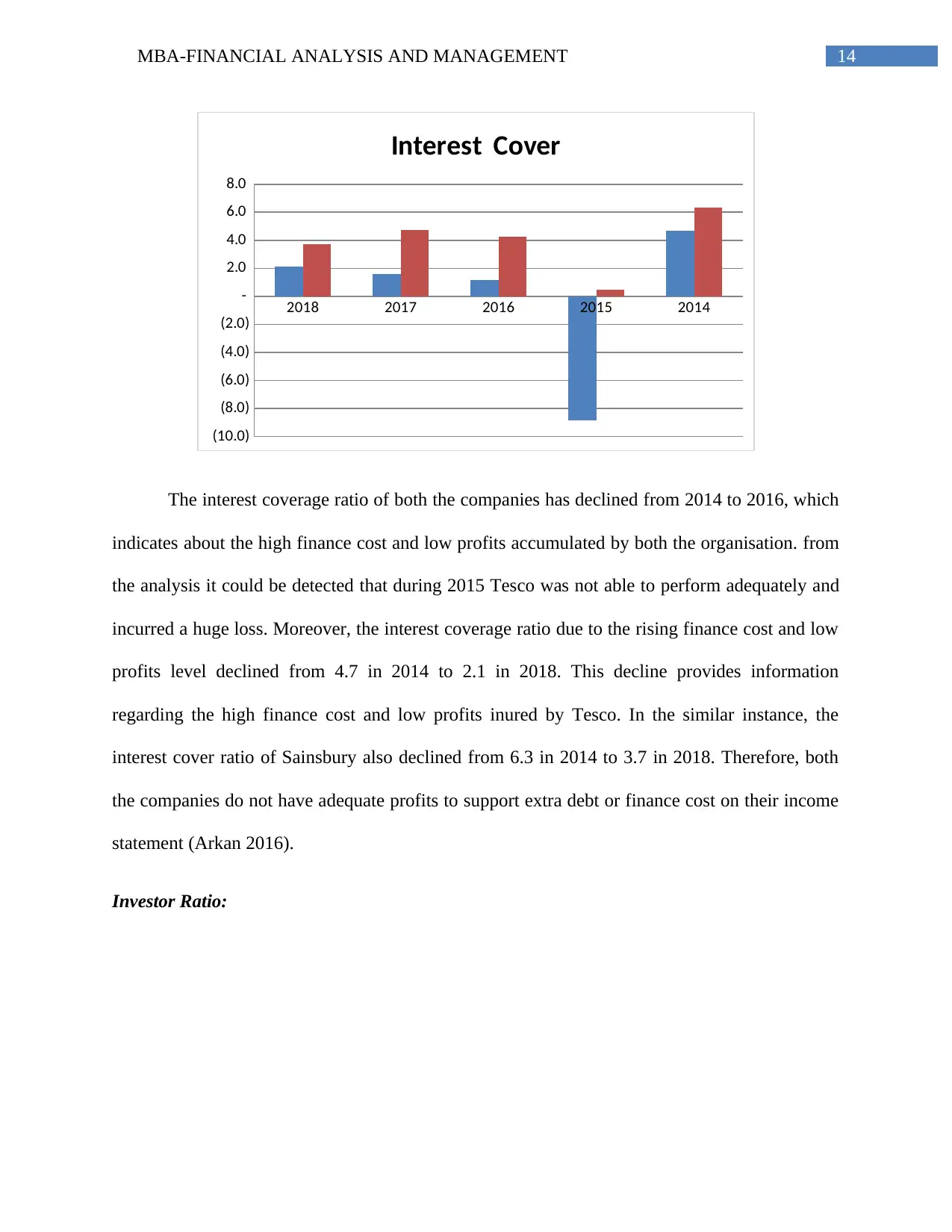

Interest Cover

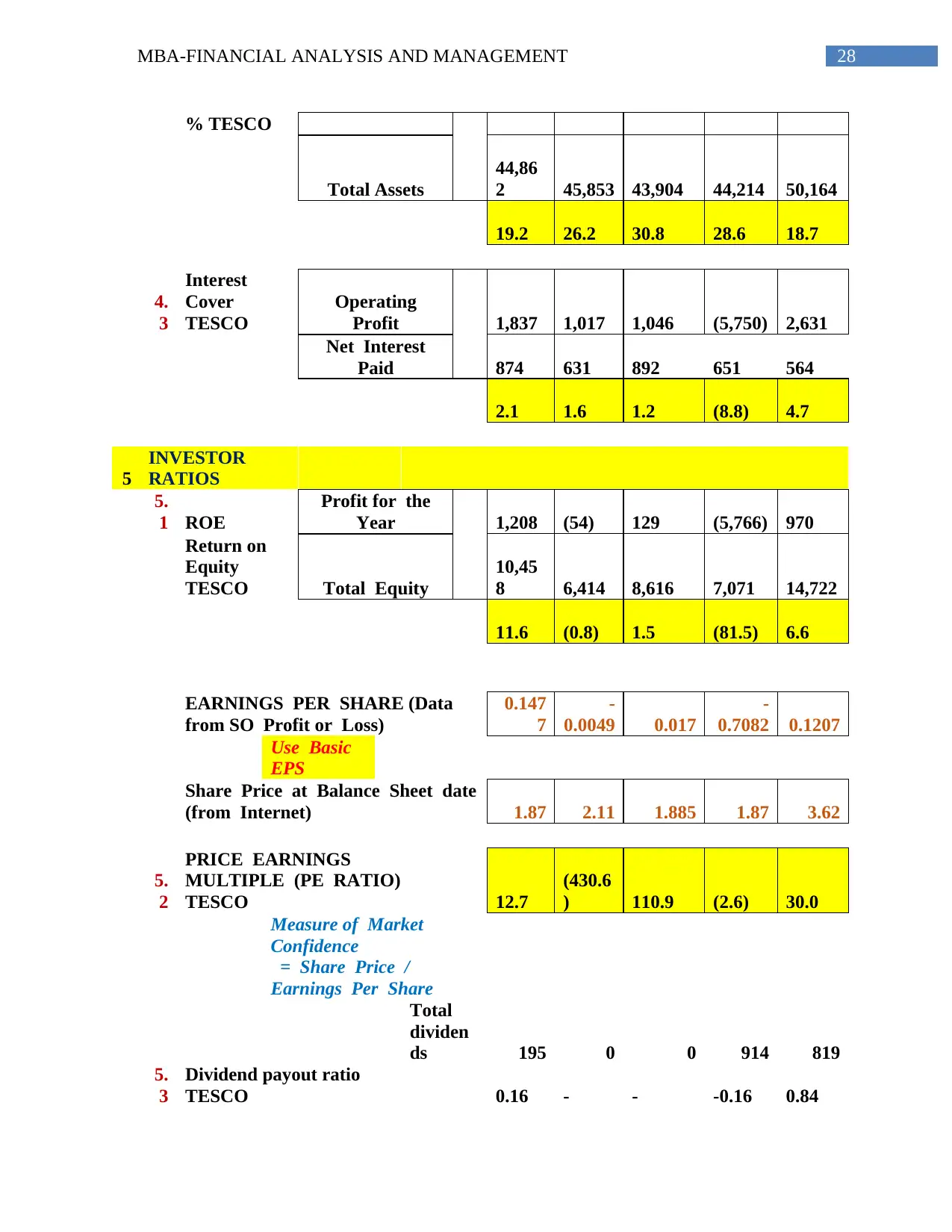

The interest coverage ratio of both the companies has declined from 2014 to 2016, which

indicates about the high finance cost and low profits accumulated by both the organisation. from

the analysis it could be detected that during 2015 Tesco was not able to perform adequately and

incurred a huge loss. Moreover, the interest coverage ratio due to the rising finance cost and low

profits level declined from 4.7 in 2014 to 2.1 in 2018. This decline provides information

regarding the high finance cost and low profits inured by Tesco. In the similar instance, the

interest cover ratio of Sainsbury also declined from 6.3 in 2014 to 3.7 in 2018. Therefore, both

the companies do not have adequate profits to support extra debt or finance cost on their income

statement (Arkan 2016).

Investor Ratio:

2018 2017 2016 2015 2014

(10.0)

(8.0)

(6.0)

(4.0)

(2.0)

-

2.0

4.0

6.0

8.0

Interest Cover

The interest coverage ratio of both the companies has declined from 2014 to 2016, which

indicates about the high finance cost and low profits accumulated by both the organisation. from

the analysis it could be detected that during 2015 Tesco was not able to perform adequately and

incurred a huge loss. Moreover, the interest coverage ratio due to the rising finance cost and low

profits level declined from 4.7 in 2014 to 2.1 in 2018. This decline provides information

regarding the high finance cost and low profits inured by Tesco. In the similar instance, the

interest cover ratio of Sainsbury also declined from 6.3 in 2014 to 3.7 in 2018. Therefore, both

the companies do not have adequate profits to support extra debt or finance cost on their income

statement (Arkan 2016).

Investor Ratio:

15MBA-FINANCIAL ANALYSIS AND MANAGEMENT

2018 2017 2016 2015 2014

(100.0)

(80.0)

(60.0)

(40.0)

(20.0)

-

20.0

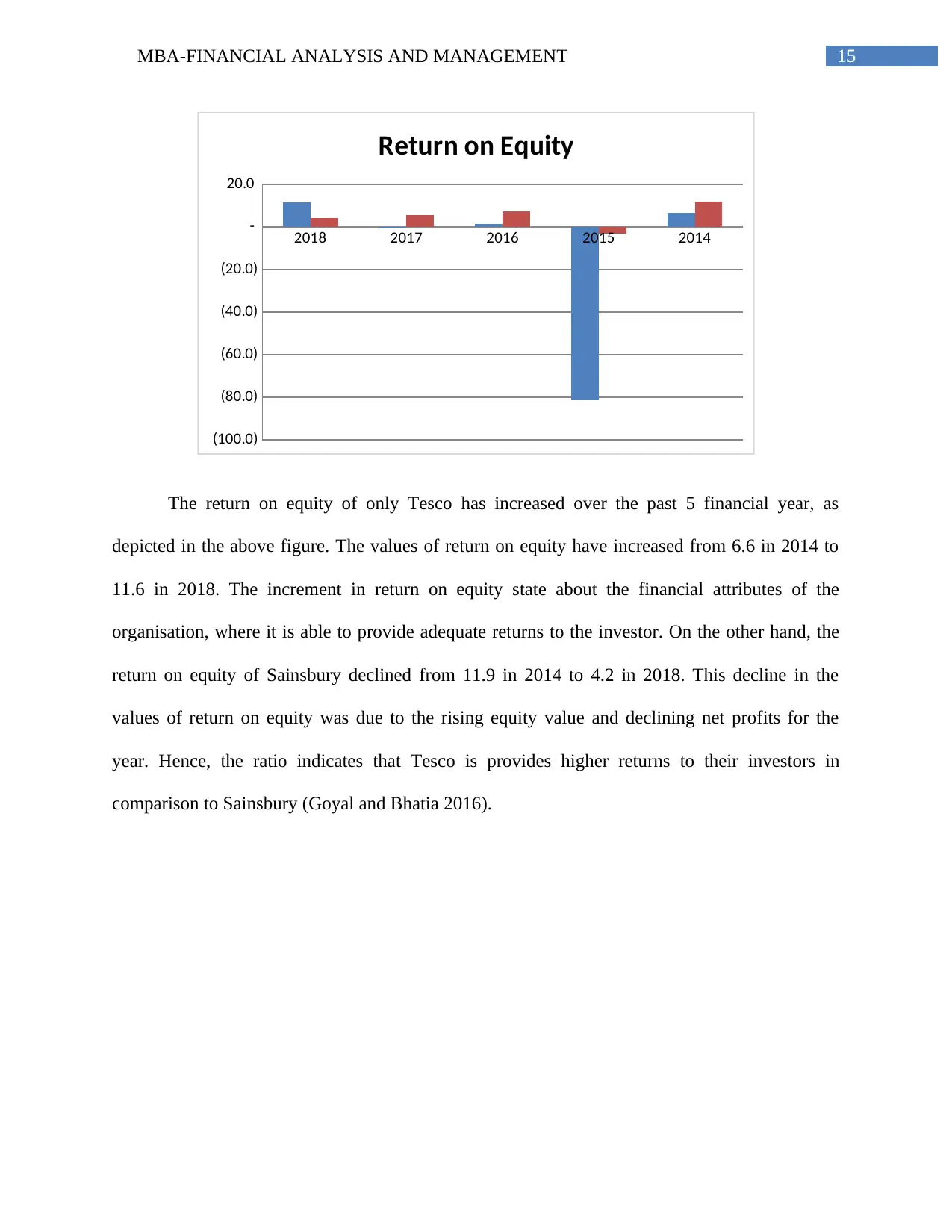

Return on Equity

The return on equity of only Tesco has increased over the past 5 financial year, as

depicted in the above figure. The values of return on equity have increased from 6.6 in 2014 to

11.6 in 2018. The increment in return on equity state about the financial attributes of the

organisation, where it is able to provide adequate returns to the investor. On the other hand, the

return on equity of Sainsbury declined from 11.9 in 2014 to 4.2 in 2018. This decline in the

values of return on equity was due to the rising equity value and declining net profits for the

year. Hence, the ratio indicates that Tesco is provides higher returns to their investors in

comparison to Sainsbury (Goyal and Bhatia 2016).

2018 2017 2016 2015 2014

(100.0)

(80.0)

(60.0)

(40.0)

(20.0)

-

20.0

Return on Equity

The return on equity of only Tesco has increased over the past 5 financial year, as

depicted in the above figure. The values of return on equity have increased from 6.6 in 2014 to

11.6 in 2018. The increment in return on equity state about the financial attributes of the

organisation, where it is able to provide adequate returns to the investor. On the other hand, the

return on equity of Sainsbury declined from 11.9 in 2014 to 4.2 in 2018. This decline in the

values of return on equity was due to the rising equity value and declining net profits for the

year. Hence, the ratio indicates that Tesco is provides higher returns to their investors in

comparison to Sainsbury (Goyal and Bhatia 2016).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16MBA-FINANCIAL ANALYSIS AND MANAGEMENT

2018 2017 2016 2015 2014

(500.0)

(400.0)

(300.0)

(200.0)

(100.0)

-

100.0

200.0

EARNINGS PER SHARE

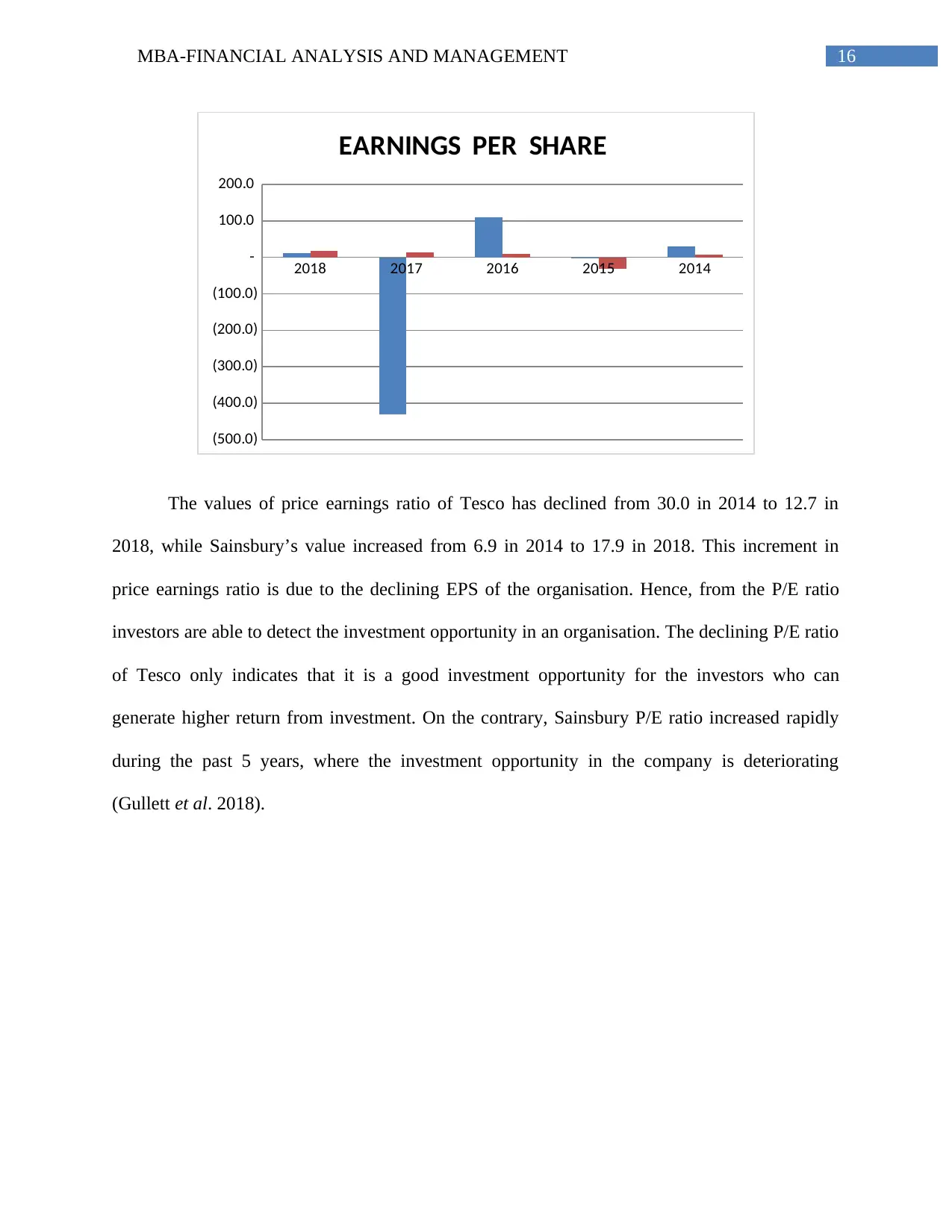

The values of price earnings ratio of Tesco has declined from 30.0 in 2014 to 12.7 in

2018, while Sainsbury’s value increased from 6.9 in 2014 to 17.9 in 2018. This increment in

price earnings ratio is due to the declining EPS of the organisation. Hence, from the P/E ratio

investors are able to detect the investment opportunity in an organisation. The declining P/E ratio

of Tesco only indicates that it is a good investment opportunity for the investors who can

generate higher return from investment. On the contrary, Sainsbury P/E ratio increased rapidly

during the past 5 years, where the investment opportunity in the company is deteriorating

(Gullett et al. 2018).

2018 2017 2016 2015 2014

(500.0)

(400.0)

(300.0)

(200.0)

(100.0)

-

100.0

200.0

EARNINGS PER SHARE

The values of price earnings ratio of Tesco has declined from 30.0 in 2014 to 12.7 in

2018, while Sainsbury’s value increased from 6.9 in 2014 to 17.9 in 2018. This increment in

price earnings ratio is due to the declining EPS of the organisation. Hence, from the P/E ratio

investors are able to detect the investment opportunity in an organisation. The declining P/E ratio

of Tesco only indicates that it is a good investment opportunity for the investors who can

generate higher return from investment. On the contrary, Sainsbury P/E ratio increased rapidly

during the past 5 years, where the investment opportunity in the company is deteriorating

(Gullett et al. 2018).

17MBA-FINANCIAL ANALYSIS AND MANAGEMENT

2018 2017 2016 2015 2014

(2.50)

(2.00)

(1.50)

(1.00)

(0.50)

-

0.50

1.00

1.50

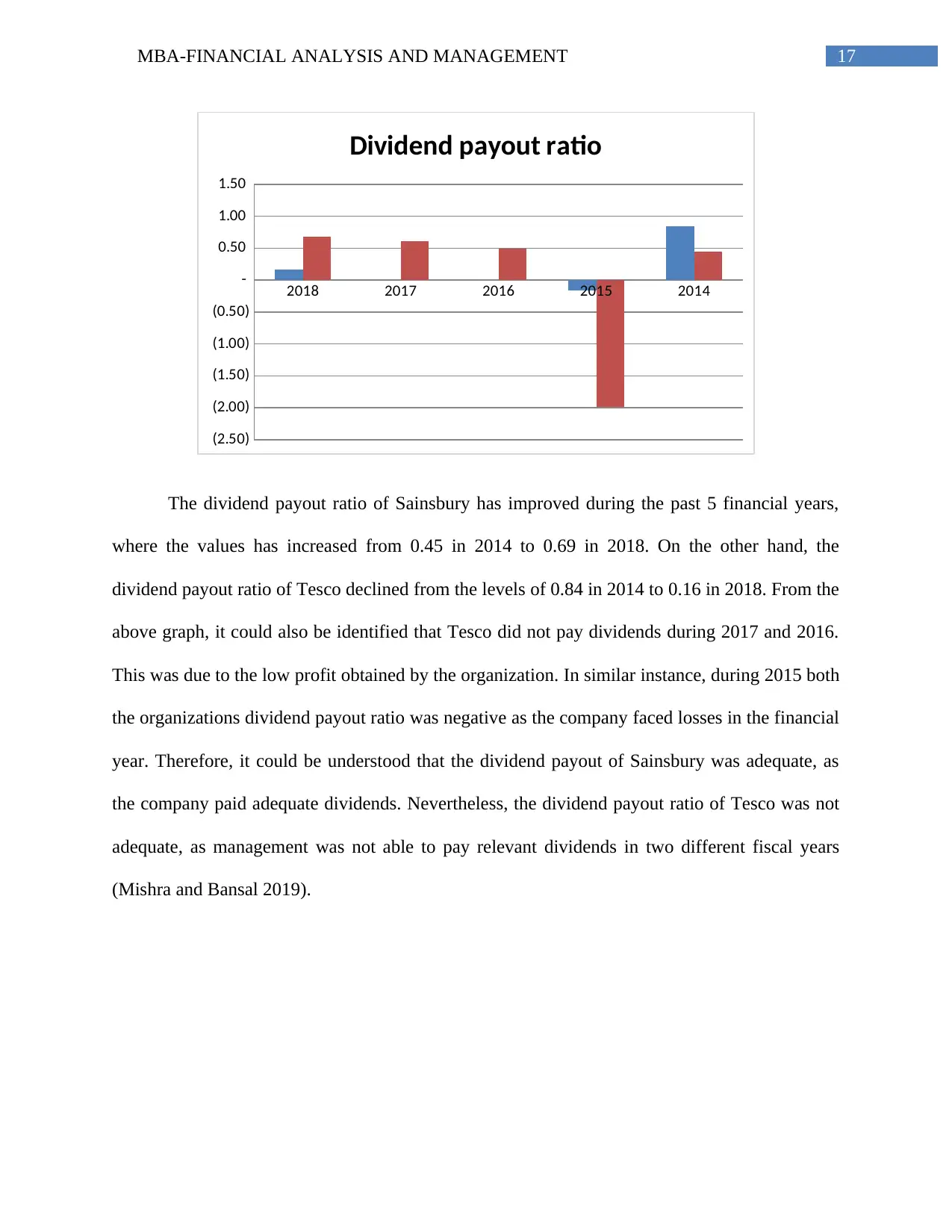

Dividend payout ratio

The dividend payout ratio of Sainsbury has improved during the past 5 financial years,

where the values has increased from 0.45 in 2014 to 0.69 in 2018. On the other hand, the

dividend payout ratio of Tesco declined from the levels of 0.84 in 2014 to 0.16 in 2018. From the

above graph, it could also be identified that Tesco did not pay dividends during 2017 and 2016.

This was due to the low profit obtained by the organization. In similar instance, during 2015 both

the organizations dividend payout ratio was negative as the company faced losses in the financial

year. Therefore, it could be understood that the dividend payout of Sainsbury was adequate, as

the company paid adequate dividends. Nevertheless, the dividend payout ratio of Tesco was not

adequate, as management was not able to pay relevant dividends in two different fiscal years

(Mishra and Bansal 2019).

2018 2017 2016 2015 2014

(2.50)

(2.00)

(1.50)

(1.00)

(0.50)

-

0.50

1.00

1.50

Dividend payout ratio

The dividend payout ratio of Sainsbury has improved during the past 5 financial years,

where the values has increased from 0.45 in 2014 to 0.69 in 2018. On the other hand, the

dividend payout ratio of Tesco declined from the levels of 0.84 in 2014 to 0.16 in 2018. From the

above graph, it could also be identified that Tesco did not pay dividends during 2017 and 2016.

This was due to the low profit obtained by the organization. In similar instance, during 2015 both

the organizations dividend payout ratio was negative as the company faced losses in the financial

year. Therefore, it could be understood that the dividend payout of Sainsbury was adequate, as

the company paid adequate dividends. Nevertheless, the dividend payout ratio of Tesco was not

adequate, as management was not able to pay relevant dividends in two different fiscal years

(Mishra and Bansal 2019).

18MBA-FINANCIAL ANALYSIS AND MANAGEMENT

2018 2017 2016 2015 2014

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

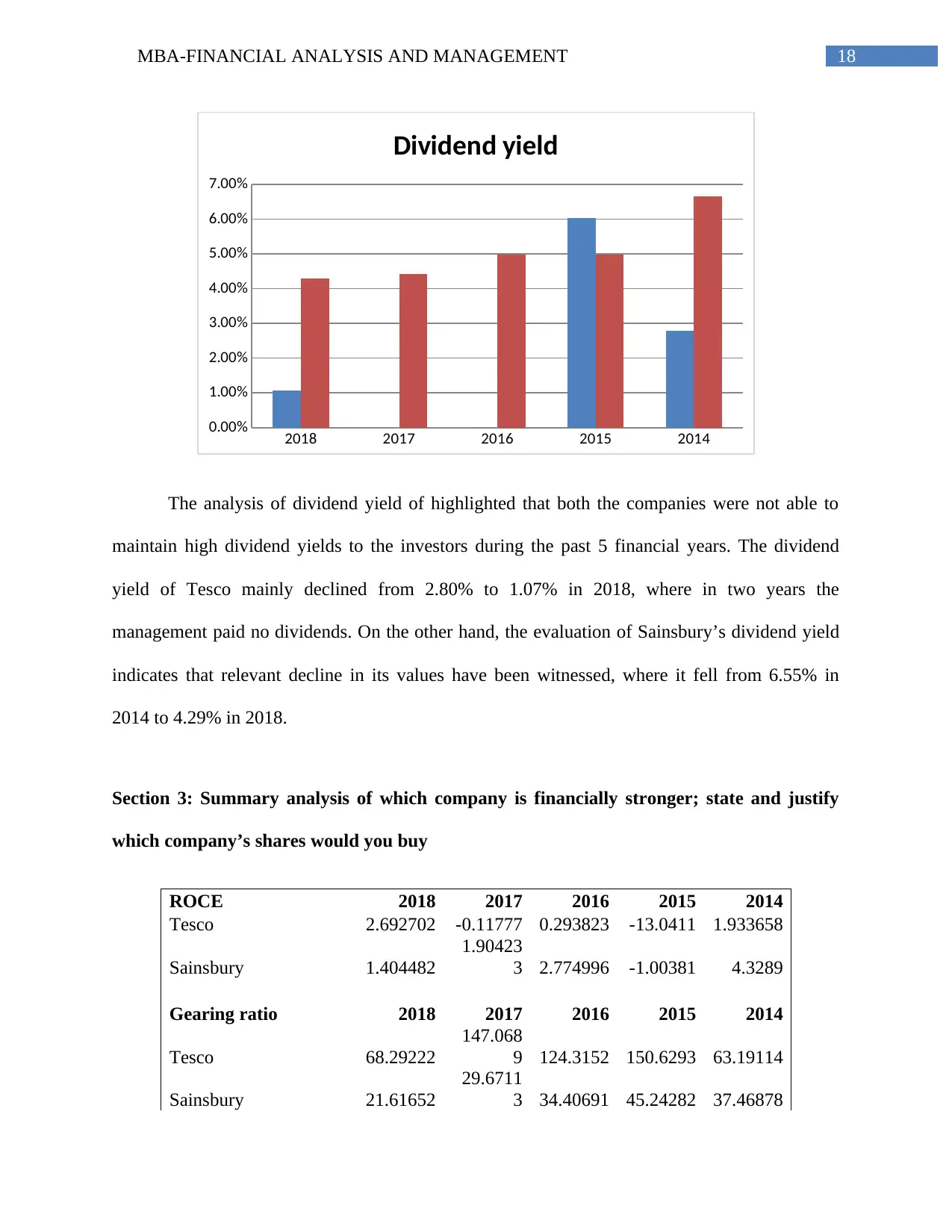

Dividend yield

The analysis of dividend yield of highlighted that both the companies were not able to

maintain high dividend yields to the investors during the past 5 financial years. The dividend

yield of Tesco mainly declined from 2.80% to 1.07% in 2018, where in two years the

management paid no dividends. On the other hand, the evaluation of Sainsbury’s dividend yield

indicates that relevant decline in its values have been witnessed, where it fell from 6.55% in

2014 to 4.29% in 2018.

Section 3: Summary analysis of which company is financially stronger; state and justify

which company’s shares would you buy

ROCE 2018 2017 2016 2015 2014

Tesco 2.692702 -0.11777 0.293823 -13.0411 1.933658

Sainsbury 1.404482

1.90423

3 2.774996 -1.00381 4.3289

Gearing ratio 2018 2017 2016 2015 2014

Tesco 68.29222

147.068

9 124.3152 150.6293 63.19114

Sainsbury 21.61652

29.6711

3 34.40691 45.24282 37.46878

2018 2017 2016 2015 2014

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

Dividend yield

The analysis of dividend yield of highlighted that both the companies were not able to

maintain high dividend yields to the investors during the past 5 financial years. The dividend

yield of Tesco mainly declined from 2.80% to 1.07% in 2018, where in two years the

management paid no dividends. On the other hand, the evaluation of Sainsbury’s dividend yield

indicates that relevant decline in its values have been witnessed, where it fell from 6.55% in

2014 to 4.29% in 2018.

Section 3: Summary analysis of which company is financially stronger; state and justify

which company’s shares would you buy

ROCE 2018 2017 2016 2015 2014

Tesco 2.692702 -0.11777 0.293823 -13.0411 1.933658

Sainsbury 1.404482

1.90423

3 2.774996 -1.00381 4.3289

Gearing ratio 2018 2017 2016 2015 2014

Tesco 68.29222

147.068

9 124.3152 150.6293 63.19114

Sainsbury 21.61652

29.6711

3 34.40691 45.24282 37.46878

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

19MBA-FINANCIAL ANALYSIS AND MANAGEMENT

ROE 2018 2017 2016 2015 2014

Tesco 11.55097 -0.84191 1.497214 -81.5443 6.588779

Sainsbury 4.169478 5.48603 7.399843 -2.99693 11.9234

EPS 2018 2017 2016 2015 2014

Tesco 0.1477 -0.0049 0.017 -0.7082 0.1207

Sainsbury 0.1333 0.175 0.239 -0.087 0.377

P/E 2018 2017 2016 2015 2014

Tesco 12.6608 -430.612 110.8824 -2.6405 29.99171

Sainsbury 17.85446 13.2 10.16736 -30.4598 6.896552

Share price movement 2018 2017 2016 2015 2014

Tesco 1.87 2.11 1.885 1.87 3.62

Sainsbury 2.38 2.31 2.43 2.65 2.6

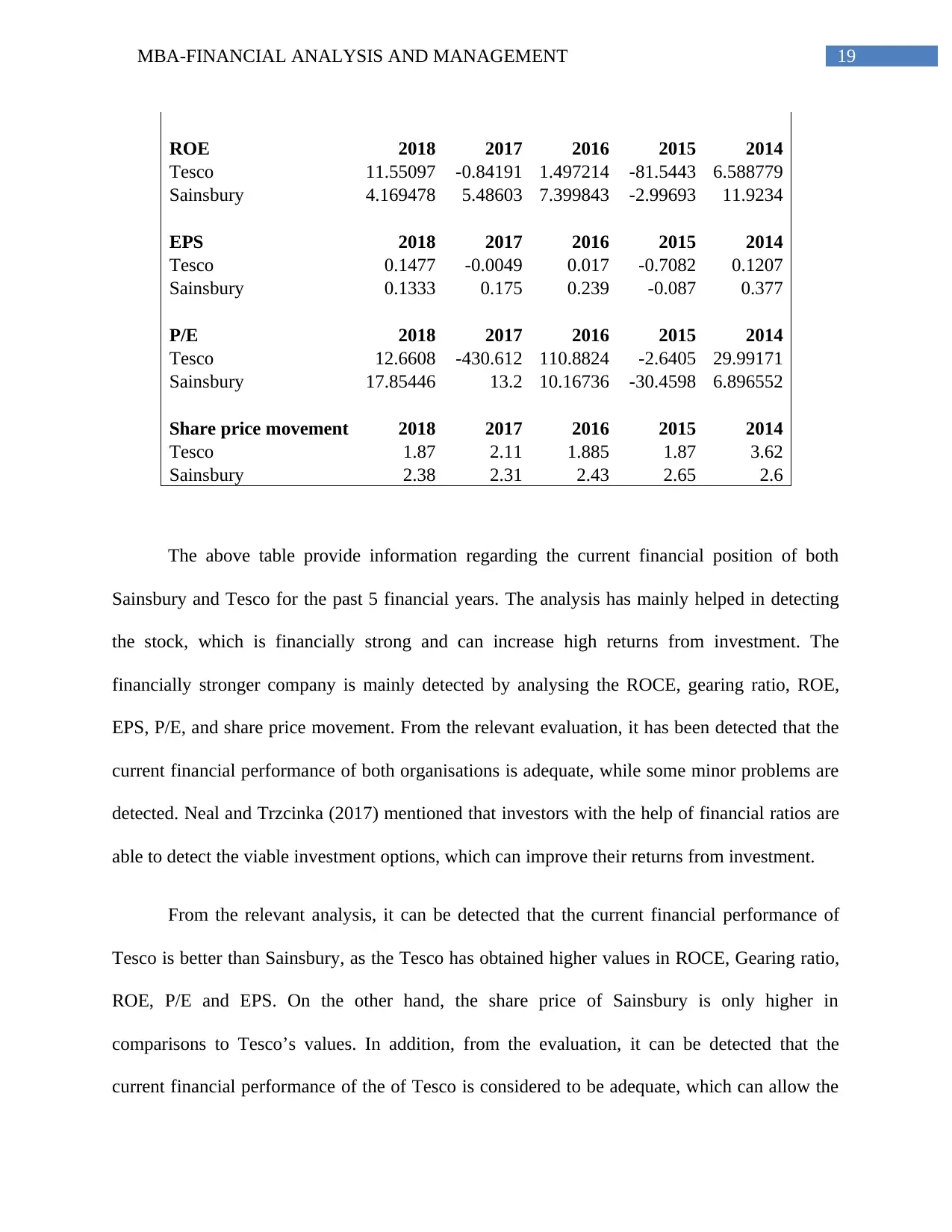

The above table provide information regarding the current financial position of both

Sainsbury and Tesco for the past 5 financial years. The analysis has mainly helped in detecting

the stock, which is financially strong and can increase high returns from investment. The

financially stronger company is mainly detected by analysing the ROCE, gearing ratio, ROE,

EPS, P/E, and share price movement. From the relevant evaluation, it has been detected that the

current financial performance of both organisations is adequate, while some minor problems are

detected. Neal and Trzcinka (2017) mentioned that investors with the help of financial ratios are

able to detect the viable investment options, which can improve their returns from investment.

From the relevant analysis, it can be detected that the current financial performance of

Tesco is better than Sainsbury, as the Tesco has obtained higher values in ROCE, Gearing ratio,

ROE, P/E and EPS. On the other hand, the share price of Sainsbury is only higher in

comparisons to Tesco’s values. In addition, from the evaluation, it can be detected that the

current financial performance of the of Tesco is considered to be adequate, which can allow the

ROE 2018 2017 2016 2015 2014

Tesco 11.55097 -0.84191 1.497214 -81.5443 6.588779

Sainsbury 4.169478 5.48603 7.399843 -2.99693 11.9234

EPS 2018 2017 2016 2015 2014

Tesco 0.1477 -0.0049 0.017 -0.7082 0.1207

Sainsbury 0.1333 0.175 0.239 -0.087 0.377

P/E 2018 2017 2016 2015 2014

Tesco 12.6608 -430.612 110.8824 -2.6405 29.99171

Sainsbury 17.85446 13.2 10.16736 -30.4598 6.896552

Share price movement 2018 2017 2016 2015 2014

Tesco 1.87 2.11 1.885 1.87 3.62

Sainsbury 2.38 2.31 2.43 2.65 2.6

The above table provide information regarding the current financial position of both

Sainsbury and Tesco for the past 5 financial years. The analysis has mainly helped in detecting

the stock, which is financially strong and can increase high returns from investment. The

financially stronger company is mainly detected by analysing the ROCE, gearing ratio, ROE,

EPS, P/E, and share price movement. From the relevant evaluation, it has been detected that the

current financial performance of both organisations is adequate, while some minor problems are

detected. Neal and Trzcinka (2017) mentioned that investors with the help of financial ratios are

able to detect the viable investment options, which can improve their returns from investment.

From the relevant analysis, it can be detected that the current financial performance of

Tesco is better than Sainsbury, as the Tesco has obtained higher values in ROCE, Gearing ratio,

ROE, P/E and EPS. On the other hand, the share price of Sainsbury is only higher in

comparisons to Tesco’s values. In addition, from the evaluation, it can be detected that the

current financial performance of the of Tesco is considered to be adequate, which can allow the

20MBA-FINANCIAL ANALYSIS AND MANAGEMENT

investor to generate high level of income from operations. However, the share price of Sainsbury

is considered to be high in comparison to Tesco, which indicates that the investors would

increase their investment value.

Section 4: Identify problems/limitations of the ratio analysis and assumptions you made in

comparative analysis

There are relevant problems that can be identified for the ratio analysis, which have

negative impact on the overall investment options of the investors. The financial performance of

the organisation is mainly derived from relevant ratios, which can be maintained by the wrong

information presented in the annual report. There are many instances, where the organisation has

presented manipulative annual report to project higher financial performance to their

investments. In this instance the investors are not able to gather the required information

regarding the current financial performance of the company, which helps in their investment

decisions. Moreover, the major limitation of the financial ratios is that it can evaluate the

historical performance of the company and do not provide relevant information on the future

prospects of the company (Ozturk and Serçemeli 2016). The financial ratios are not able to

analyse all the relevant information of and organisation to detect its future growth, whereas the

trend analysis does not present the actual fluctuations in profitability that would be maintained

by the company under different economic and global conditions. Hence, investors can use both

fundamental and technical analysis to determine the overall financial performance of the

organisation, which could help in generating high level of income from investment.

investor to generate high level of income from operations. However, the share price of Sainsbury

is considered to be high in comparison to Tesco, which indicates that the investors would

increase their investment value.

Section 4: Identify problems/limitations of the ratio analysis and assumptions you made in

comparative analysis

There are relevant problems that can be identified for the ratio analysis, which have

negative impact on the overall investment options of the investors. The financial performance of

the organisation is mainly derived from relevant ratios, which can be maintained by the wrong

information presented in the annual report. There are many instances, where the organisation has

presented manipulative annual report to project higher financial performance to their

investments. In this instance the investors are not able to gather the required information

regarding the current financial performance of the company, which helps in their investment

decisions. Moreover, the major limitation of the financial ratios is that it can evaluate the

historical performance of the company and do not provide relevant information on the future

prospects of the company (Ozturk and Serçemeli 2016). The financial ratios are not able to

analyse all the relevant information of and organisation to detect its future growth, whereas the

trend analysis does not present the actual fluctuations in profitability that would be maintained

by the company under different economic and global conditions. Hence, investors can use both

fundamental and technical analysis to determine the overall financial performance of the

organisation, which could help in generating high level of income from investment.

21MBA-FINANCIAL ANALYSIS AND MANAGEMENT

Conclusion:

The overall financial performance of Tesco and Sainsbury is mainly evaluated in the

above assessment, which can eventually help in determining the accurate financial performance.

From the relevant analysis, it can be detected that the current financial performance of the both

Tesco and Sainsbury have depicted about the most viable investment option. Therefore, from the

relevant information, it can be detected that the current financial performance of the of Tesco is

much better than Sainsbury, which can allow the investor to generate higher returns on

investment. Hence, investment needs to be conducted in Tesco plc, while no investment in

Sainsbury.

Conclusion:

The overall financial performance of Tesco and Sainsbury is mainly evaluated in the

above assessment, which can eventually help in determining the accurate financial performance.

From the relevant analysis, it can be detected that the current financial performance of the both

Tesco and Sainsbury have depicted about the most viable investment option. Therefore, from the

relevant information, it can be detected that the current financial performance of the of Tesco is

much better than Sainsbury, which can allow the investor to generate higher returns on

investment. Hence, investment needs to be conducted in Tesco plc, while no investment in

Sainsbury.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

22MBA-FINANCIAL ANALYSIS AND MANAGEMENT

Reference and Bibliography:

About.sainsburys.co.uk. 2019. Welcome to Sainsburys Home. [online] Available at:

https://www.about.sainsburys.co.uk/ [Accessed 17 Apr. 2019].

Arkan, T., 2016. The importance of financial ratios in predicting stock price trends: A case study

in emerging markets. Finanse, Rynki Finansowe, Ubezpieczenia, 79(1), pp.13-26.

Atoom, R., Malkawi, E. and Al Share, B., 2017. Utilizing Australian Shareholders' Association

(ASA): Fifteen Top Financial Ratios to Evaluate Jordanian Banks' Performance. Journal of

Applied Finance and Banking, 7(1), p.119.

Bawa, J.K., Goyal, V., Mitra, S.K. and Basu, S., 2018. An analysis of NPAs of Indian banks:

Using a comprehensive framework of 31 financial ratios. IIMB Management Review.

Chiaramonte, L. and Casu, B., 2017. Capital and liquidity ratios and financial distress. Evidence

from the European banking industry. The British Accounting Review, 49(2), pp.138-161.

Goyal, S. and Bhatia, A., 2016. Analysis of Financial Ratios for Measuring Performance of

Indian Public Sector Banks. International Journal of Engineering and Management Research

(IJEMR), 6(2), pp.152-162.

Gullett, N.S., Kilgore, R.W. and Geddie, M.F., 2018. Use of Financial Ratios to Measure the

Quality of Earnings. Academy of Accounting and Financial Studies Journal.

Haskins, M.E. and Haskins, M.E., 2017. Remington, Inc.: Instant Insights for Financial

Ratios. Darden Business Publishing Cases, pp.1-7.

Reference and Bibliography:

About.sainsburys.co.uk. 2019. Welcome to Sainsburys Home. [online] Available at:

https://www.about.sainsburys.co.uk/ [Accessed 17 Apr. 2019].

Arkan, T., 2016. The importance of financial ratios in predicting stock price trends: A case study

in emerging markets. Finanse, Rynki Finansowe, Ubezpieczenia, 79(1), pp.13-26.

Atoom, R., Malkawi, E. and Al Share, B., 2017. Utilizing Australian Shareholders' Association

(ASA): Fifteen Top Financial Ratios to Evaluate Jordanian Banks' Performance. Journal of

Applied Finance and Banking, 7(1), p.119.

Bawa, J.K., Goyal, V., Mitra, S.K. and Basu, S., 2018. An analysis of NPAs of Indian banks:

Using a comprehensive framework of 31 financial ratios. IIMB Management Review.

Chiaramonte, L. and Casu, B., 2017. Capital and liquidity ratios and financial distress. Evidence

from the European banking industry. The British Accounting Review, 49(2), pp.138-161.

Goyal, S. and Bhatia, A., 2016. Analysis of Financial Ratios for Measuring Performance of

Indian Public Sector Banks. International Journal of Engineering and Management Research

(IJEMR), 6(2), pp.152-162.

Gullett, N.S., Kilgore, R.W. and Geddie, M.F., 2018. Use of Financial Ratios to Measure the

Quality of Earnings. Academy of Accounting and Financial Studies Journal.

Haskins, M.E. and Haskins, M.E., 2017. Remington, Inc.: Instant Insights for Financial

Ratios. Darden Business Publishing Cases, pp.1-7.

23MBA-FINANCIAL ANALYSIS AND MANAGEMENT

Hosaka, T., 2019. Bankruptcy prediction using imaged financial ratios and convolutional neural

networks. Expert Systems with Applications, 117, pp.287-299.

Le, H.H. and Viviani, J.L., 2018. Predicting bank failure: An improvement by implementing a

machine-learning approach to classical financial ratios. Research in International Business and

Finance, 44, pp.16-25.

Lukason, O., Laitinen, E.K. and Suvas, A., 2015. Growth patterns of small manufacturing firms

before failure: interconnections with financial ratios and nonfinancial variables. International

Journal of Industrial Engineering and Management, 6(2), pp.59-66.

Meriç, E., Kamışlı, M. and Temizel, F., 2017. Interactions among Stock Price and Financial

Ratios: The Case of Turkish Banking Sector. Applied Economics and Finance, 4(6), pp.107-115.

Mishra, S. and Bansal, R., 2019. Credit Rating and Its Interaction With Financial Ratios: A

Study of BSE 500 Companies. In Behavioral Finance and Decision-Making Models (pp. 251-

268). IGI Global.

Misund, B., 2017. Financial ratios and prediction on corporate bankruptcy in the Atlantic salmon

industry. Aquaculture economics & management, 21(2), pp.241-260.

Morales-Díaz, J. and Zamora-Ramírez, C., 2018. The impact of IFRS 16 on key financial ratios:

a new methodological approach. Accounting in Europe, 15(1), pp.105-133.

Neal, R.S. and Trzcinka, C., 2016. Financial markets 2017: Make P/E ratios great again. Indiana

Business Review, 91(4), pp.1-4.

Neal, R.S. and Trzcinka, C., 2017. Financial markets 2018: P/E ratios are great again. Indiana

Business Review, 92(4), pp.1-4.

Hosaka, T., 2019. Bankruptcy prediction using imaged financial ratios and convolutional neural

networks. Expert Systems with Applications, 117, pp.287-299.

Le, H.H. and Viviani, J.L., 2018. Predicting bank failure: An improvement by implementing a

machine-learning approach to classical financial ratios. Research in International Business and

Finance, 44, pp.16-25.

Lukason, O., Laitinen, E.K. and Suvas, A., 2015. Growth patterns of small manufacturing firms

before failure: interconnections with financial ratios and nonfinancial variables. International

Journal of Industrial Engineering and Management, 6(2), pp.59-66.

Meriç, E., Kamışlı, M. and Temizel, F., 2017. Interactions among Stock Price and Financial

Ratios: The Case of Turkish Banking Sector. Applied Economics and Finance, 4(6), pp.107-115.

Mishra, S. and Bansal, R., 2019. Credit Rating and Its Interaction With Financial Ratios: A

Study of BSE 500 Companies. In Behavioral Finance and Decision-Making Models (pp. 251-

268). IGI Global.

Misund, B., 2017. Financial ratios and prediction on corporate bankruptcy in the Atlantic salmon

industry. Aquaculture economics & management, 21(2), pp.241-260.

Morales-Díaz, J. and Zamora-Ramírez, C., 2018. The impact of IFRS 16 on key financial ratios:

a new methodological approach. Accounting in Europe, 15(1), pp.105-133.

Neal, R.S. and Trzcinka, C., 2016. Financial markets 2017: Make P/E ratios great again. Indiana

Business Review, 91(4), pp.1-4.

Neal, R.S. and Trzcinka, C., 2017. Financial markets 2018: P/E ratios are great again. Indiana

Business Review, 92(4), pp.1-4.

24MBA-FINANCIAL ANALYSIS AND MANAGEMENT

Nia, S.H., 2015. Financial ratios between fraudulent and non-fraudulent firms: Evidence from

Tehran Stock Exchange. Journal of Accounting and Taxation, 7(3), pp.38-44.

Nuryani, N., Heng, T.T. and Juliesta, N., 2015. Capitalization of Operating Lease and Its Impact

on Firm's Financial Ratios. Procedia-Social and Behavioral Sciences, 211, pp.268-276.

Öztürk, M. and Serçemeli, M., 2016. Impact of New Standard" IFRS 16 Leases" on Statement of

Financial Position and Key Ratios: A Case Study on an Airline Company in Turkey. Business

and Economics Research Journal, 7(4), p.143.

Shaverdi, M., Ramezani, I., Tahmasebi, R. and Rostamy, A.A.A., 2016. Combining fuzzy AHP

and fuzzy TOPSIS with financial ratios to design a novel performance evaluation

model. International Journal of Fuzzy Systems, 18(2), pp.248-262.

Tesco plc. 2019. Tesco PLC. [online] Available at: https://www.tescoplc.com/ [Accessed 17 Apr.

2019].

Tian, S. and Yu, Y., 2017. Financial ratios and bankruptcy predictions: An international

evidence. International Review of Economics & Finance, 51, pp.510-526.

Wong, K. and Joshi, M., 2015. The impact of lease capitalisation on financial statements and key

ratios: Evidence from Australia. Australasian Accounting, Business and Finance Journal, 9(3),

pp.27-44.

Nia, S.H., 2015. Financial ratios between fraudulent and non-fraudulent firms: Evidence from

Tehran Stock Exchange. Journal of Accounting and Taxation, 7(3), pp.38-44.

Nuryani, N., Heng, T.T. and Juliesta, N., 2015. Capitalization of Operating Lease and Its Impact

on Firm's Financial Ratios. Procedia-Social and Behavioral Sciences, 211, pp.268-276.

Öztürk, M. and Serçemeli, M., 2016. Impact of New Standard" IFRS 16 Leases" on Statement of

Financial Position and Key Ratios: A Case Study on an Airline Company in Turkey. Business

and Economics Research Journal, 7(4), p.143.

Shaverdi, M., Ramezani, I., Tahmasebi, R. and Rostamy, A.A.A., 2016. Combining fuzzy AHP

and fuzzy TOPSIS with financial ratios to design a novel performance evaluation

model. International Journal of Fuzzy Systems, 18(2), pp.248-262.

Tesco plc. 2019. Tesco PLC. [online] Available at: https://www.tescoplc.com/ [Accessed 17 Apr.

2019].

Tian, S. and Yu, Y., 2017. Financial ratios and bankruptcy predictions: An international

evidence. International Review of Economics & Finance, 51, pp.510-526.

Wong, K. and Joshi, M., 2015. The impact of lease capitalisation on financial statements and key

ratios: Evidence from Australia. Australasian Accounting, Business and Finance Journal, 9(3),

pp.27-44.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

25MBA-FINANCIAL ANALYSIS AND MANAGEMENT

Appendices:

RATIO ANALYSIS

TESC

O 2018 2017 2016 2015 2014

1

PROFITABILITY

RATIOS

1

.

1

ASSET

UTILISATION Revenue

57,49

1 55,917 54,433 56,925 63,557

Total Assets

44,86

2 45,853 43,904 44,214 50,164

1.28 1.22 1.24 1.29 1.27

1

.

2 MARGINS

Operating

Margin

TESCO Operating Profit 1,837 1,017 1,046 (5,750) 2,631

Revenue

57,49

1 55,917 54,433 56,925 63,557

3.2 1.8 1.9 (10.1) 4.1

Net Margin

TESCO

Profit for the

Year 1,208 (54) 129 (5,766) 970

Revenue

57,49

1 55,917 54,433 56,925 63,557

2.1 (0.1) 0.2 (10.1) 1.5

1

.

3 RETURNS

Operating

Returns

TESCO Operating Profit 1,837 1,017 1,046 (5,750) 2,631

Total Assets

44,86 45,853 43,904 44,214 50,164

Appendices:

RATIO ANALYSIS

TESC

O 2018 2017 2016 2015 2014

1

PROFITABILITY

RATIOS

1

.

1

ASSET

UTILISATION Revenue

57,49

1 55,917 54,433 56,925 63,557

Total Assets

44,86

2 45,853 43,904 44,214 50,164

1.28 1.22 1.24 1.29 1.27

1

.

2 MARGINS

Operating

Margin

TESCO Operating Profit 1,837 1,017 1,046 (5,750) 2,631

Revenue

57,49

1 55,917 54,433 56,925 63,557

3.2 1.8 1.9 (10.1) 4.1

Net Margin

TESCO

Profit for the

Year 1,208 (54) 129 (5,766) 970

Revenue

57,49

1 55,917 54,433 56,925 63,557

2.1 (0.1) 0.2 (10.1) 1.5

1

.

3 RETURNS

Operating

Returns

TESCO Operating Profit 1,837 1,017 1,046 (5,750) 2,631

Total Assets

44,86 45,853 43,904 44,214 50,164

26MBA-FINANCIAL ANALYSIS AND MANAGEMENT

2

4.1 2.2 2.4 (13.0) 5.2

Net ROI

TESCO

Profit for the

Year 1,208 (54) 129 (5,766) 970

Total Assets

44,86

2 45,853 43,904 44,214 50,164

2.7 (0.1) 0.3 (13.0) 1.9

2

LIQUIDITY

RATIOS

2.

1

Acid Test

Ratio

TESCO CCE + AR 5,541 5,296 4,689 4,286 4,696

Total Current

Liabilities

19,23

8 19,234 19,714 19,805 20,206

28.8 27.5 23.8 21.6 23.2

2.

2

Cash Ratio

TESCO

Cash and Cash

Equivalents 4,059 3,821 3,082 2,165 2,506

Total Current

Liabilities

19,23

8 19,234 19,714 19,805 20,206

21.1 19.9 15.6 10.9 12.4

Therefore AR per $ of

Current Liabilities = 7.70 7.67 8.15 10.71 10.84

3

WORKING CAPITAL RATIOS (OR

EFFICIENCY RATIOS)

3.

1

CURRENT

Ratio

TESCO Current Assets

13,57

7 15,073 14,592 11,819 13,085

Current

Liabilities

19,23

8 19,234 19,714 19,805 20,206

0.7 0.8 0.7 0.6 0.6

3. INVENTOR Inventory * 365

2

4.1 2.2 2.4 (13.0) 5.2

Net ROI

TESCO

Profit for the

Year 1,208 (54) 129 (5,766) 970

Total Assets

44,86

2 45,853 43,904 44,214 50,164

2.7 (0.1) 0.3 (13.0) 1.9

2

LIQUIDITY

RATIOS

2.

1

Acid Test

Ratio

TESCO CCE + AR 5,541 5,296 4,689 4,286 4,696

Total Current

Liabilities

19,23

8 19,234 19,714 19,805 20,206

28.8 27.5 23.8 21.6 23.2

2.

2

Cash Ratio

TESCO

Cash and Cash

Equivalents 4,059 3,821 3,082 2,165 2,506

Total Current

Liabilities

19,23

8 19,234 19,714 19,805 20,206

21.1 19.9 15.6 10.9 12.4

Therefore AR per $ of

Current Liabilities = 7.70 7.67 8.15 10.71 10.84

3

WORKING CAPITAL RATIOS (OR

EFFICIENCY RATIOS)

3.

1

CURRENT

Ratio

TESCO Current Assets

13,57

7 15,073 14,592 11,819 13,085

Current

Liabilities

19,23

8 19,234 19,714 19,805 20,206

0.7 0.8 0.7 0.6 0.6

3. INVENTOR Inventory * 365

27MBA-FINANCIAL ANALYSIS AND MANAGEMENT

2

Y PERIOD

TESCO

825,9

95

839,86

5 886,950

1,079,3

05

1,305,

240

Cost of Sales

53,01

5 54,141 59,128 51,579 59,547

15.6 15.5 15.0 20.9 21.9

3.

3

AR

PERIOD

TESCO

Accounts

Receivable * 365

540,9

30

538,37

5 586,555

774,16

5

799,35

0

Revenue

57,49

1 55,917 54,433 56,925 63,557

3,434.

3

3,514.

3 3,933.1 4,963.9

4,590.

6

GROSS ASSET CONVERSION =

Inventory Period + AR Period =

3,449.

8

3,529.

8 3,948.1 4,984.8

4,612.

5

3.

4

AP

PERIOD

TESCO

Accounts

Payable * 365

3,283,

540

3,239,

375

3,127,3

20

3,621,5

30

3,867,

175

(Accts

Payable ) Cost of Sales

53,01

5 54,141 59,128 51,579 59,547

22,60

6.7

21,838

.8

19,305.

1

25,627.

8

23,704

.3

WORKING CAPITAL CYCLE =

(3.2 + 3.3) - 3.4

-

19156

.8128

7

-

18308.

97953

-

15356.9

5754

-

20643.

01266

-

19091.

79411

4 DEBT MANAGEMENT

4.

1

Gearing %

TESCO

Total Long

Term Liabilities 7,142 9,433 10,711 10,651 9,303

Total Equity

10,45

8 6,414 8,616 7,071 14,722

68.3 147.1 124.3 150.6 63.2

4.

2

Asset

Financing

Total Borrowing

8,621 11,993 13,537 12,659 9,402

2

Y PERIOD

TESCO

825,9

95

839,86

5 886,950

1,079,3

05

1,305,

240

Cost of Sales

53,01

5 54,141 59,128 51,579 59,547

15.6 15.5 15.0 20.9 21.9

3.

3

AR

PERIOD

TESCO

Accounts

Receivable * 365

540,9

30

538,37

5 586,555

774,16

5

799,35

0

Revenue

57,49

1 55,917 54,433 56,925 63,557

3,434.

3

3,514.

3 3,933.1 4,963.9

4,590.

6

GROSS ASSET CONVERSION =

Inventory Period + AR Period =

3,449.

8

3,529.

8 3,948.1 4,984.8

4,612.

5

3.

4

AP

PERIOD

TESCO

Accounts

Payable * 365

3,283,

540

3,239,

375

3,127,3

20

3,621,5

30

3,867,

175

(Accts

Payable ) Cost of Sales

53,01

5 54,141 59,128 51,579 59,547

22,60

6.7

21,838

.8

19,305.

1

25,627.

8

23,704

.3

WORKING CAPITAL CYCLE =

(3.2 + 3.3) - 3.4

-

19156

.8128

7

-

18308.

97953

-

15356.9

5754

-

20643.

01266

-

19091.

79411

4 DEBT MANAGEMENT

4.

1

Gearing %

TESCO

Total Long

Term Liabilities 7,142 9,433 10,711 10,651 9,303

Total Equity

10,45

8 6,414 8,616 7,071 14,722

68.3 147.1 124.3 150.6 63.2

4.

2

Asset

Financing

Total Borrowing

8,621 11,993 13,537 12,659 9,402

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

28MBA-FINANCIAL ANALYSIS AND MANAGEMENT

% TESCO

Total Assets

44,86

2 45,853 43,904 44,214 50,164

19.2 26.2 30.8 28.6 18.7

4.

3

Interest

Cover

TESCO

Operating

Profit 1,837 1,017 1,046 (5,750) 2,631

Net Interest

Paid 874 631 892 651 564

2.1 1.6 1.2 (8.8) 4.7

5

INVESTOR

RATIOS

5.

1 ROE

Profit for the

Year 1,208 (54) 129 (5,766) 970

Return on

Equity

TESCO Total Equity

10,45

8 6,414 8,616 7,071 14,722

11.6 (0.8) 1.5 (81.5) 6.6

EARNINGS PER SHARE (Data

from SO Profit or Loss)

0.147

7

-

0.0049 0.017

-

0.7082 0.1207

Use Basic

EPS

Share Price at Balance Sheet date

(from Internet) 1.87 2.11 1.885 1.87 3.62

5.

2

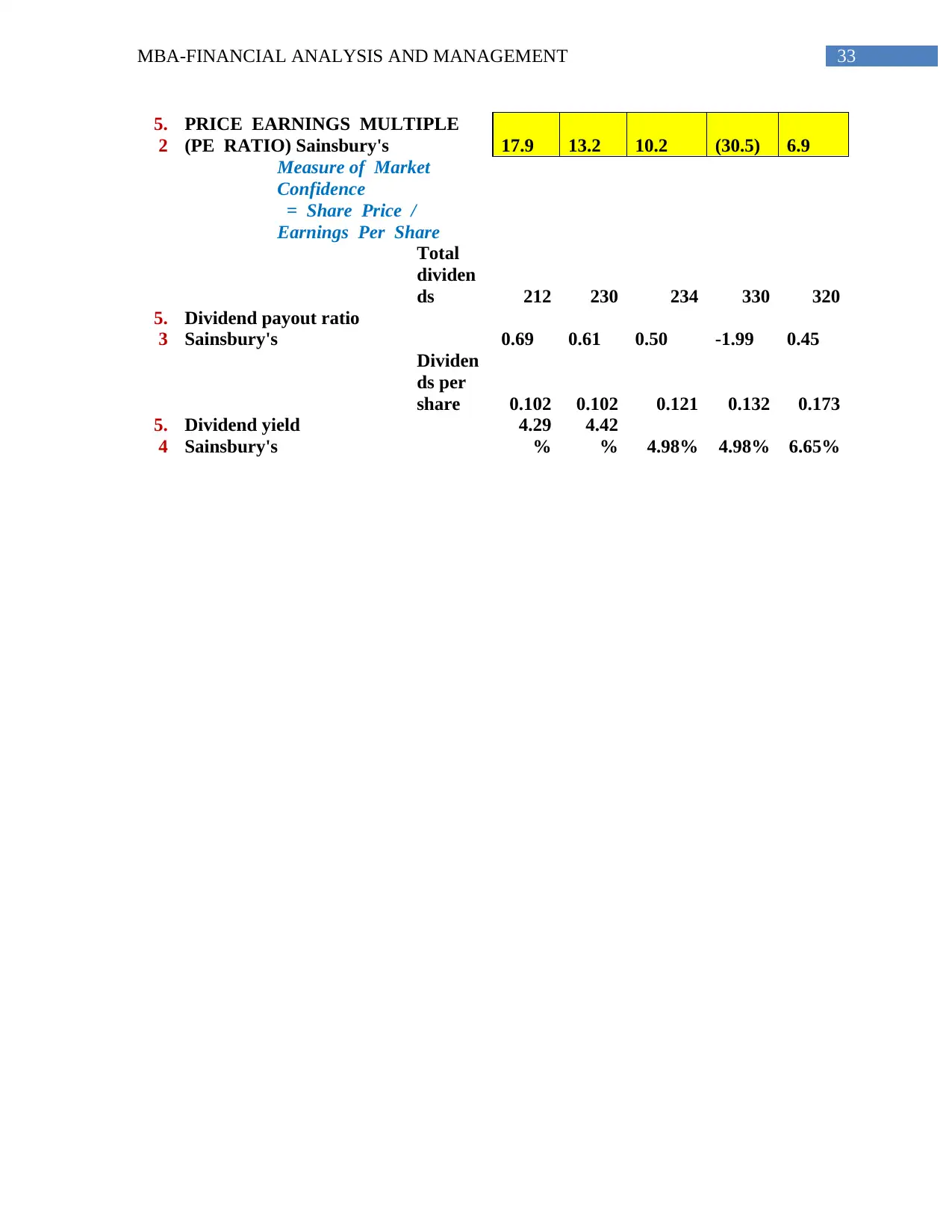

PRICE EARNINGS

MULTIPLE (PE RATIO)

TESCO 12.7

(430.6

) 110.9 (2.6) 30.0

Measure of Market

Confidence

= Share Price /

Earnings Per Share

Total

dividen

ds 195 0 0 914 819

5.

3

Dividend payout ratio

TESCO 0.16 - - -0.16 0.84

% TESCO

Total Assets

44,86

2 45,853 43,904 44,214 50,164

19.2 26.2 30.8 28.6 18.7

4.

3

Interest

Cover

TESCO

Operating

Profit 1,837 1,017 1,046 (5,750) 2,631

Net Interest

Paid 874 631 892 651 564

2.1 1.6 1.2 (8.8) 4.7

5

INVESTOR

RATIOS

5.

1 ROE

Profit for the

Year 1,208 (54) 129 (5,766) 970

Return on

Equity

TESCO Total Equity

10,45

8 6,414 8,616 7,071 14,722

11.6 (0.8) 1.5 (81.5) 6.6

EARNINGS PER SHARE (Data

from SO Profit or Loss)

0.147

7

-

0.0049 0.017

-

0.7082 0.1207

Use Basic

EPS

Share Price at Balance Sheet date

(from Internet) 1.87 2.11 1.885 1.87 3.62

5.

2

PRICE EARNINGS

MULTIPLE (PE RATIO)

TESCO 12.7

(430.6

) 110.9 (2.6) 30.0

Measure of Market

Confidence

= Share Price /

Earnings Per Share

Total

dividen

ds 195 0 0 914 819

5.

3

Dividend payout ratio

TESCO 0.16 - - -0.16 0.84

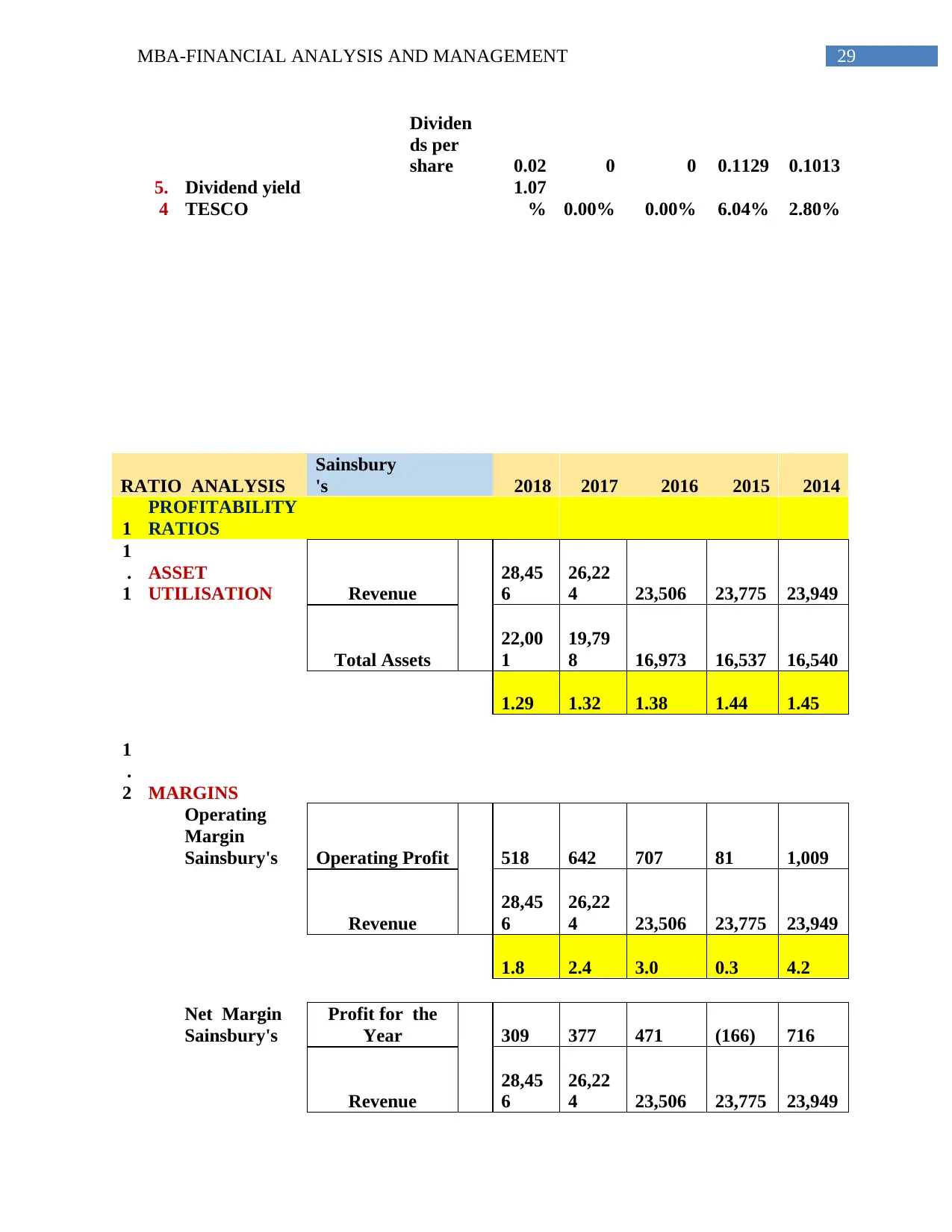

29MBA-FINANCIAL ANALYSIS AND MANAGEMENT

Dividen

ds per

share 0.02 0 0 0.1129 0.1013

5.

4

Dividend yield

TESCO

1.07

% 0.00% 0.00% 6.04% 2.80%

RATIO ANALYSIS

Sainsbury

's 2018 2017 2016 2015 2014

1

PROFITABILITY

RATIOS

1

.

1

ASSET

UTILISATION Revenue

28,45

6

26,22

4 23,506 23,775 23,949

Total Assets

22,00

1

19,79

8 16,973 16,537 16,540

1.29 1.32 1.38 1.44 1.45

1

.

2 MARGINS

Operating

Margin

Sainsbury's Operating Profit 518 642 707 81 1,009

Revenue

28,45

6

26,22

4 23,506 23,775 23,949

1.8 2.4 3.0 0.3 4.2

Net Margin

Sainsbury's

Profit for the

Year 309 377 471 (166) 716

Revenue

28,45

6

26,22

4 23,506 23,775 23,949

Dividen

ds per

share 0.02 0 0 0.1129 0.1013

5.

4

Dividend yield

TESCO

1.07

% 0.00% 0.00% 6.04% 2.80%

RATIO ANALYSIS

Sainsbury

's 2018 2017 2016 2015 2014

1

PROFITABILITY

RATIOS

1

.

1

ASSET

UTILISATION Revenue

28,45

6

26,22

4 23,506 23,775 23,949

Total Assets

22,00

1

19,79

8 16,973 16,537 16,540

1.29 1.32 1.38 1.44 1.45

1

.

2 MARGINS

Operating

Margin

Sainsbury's Operating Profit 518 642 707 81 1,009

Revenue

28,45

6

26,22

4 23,506 23,775 23,949

1.8 2.4 3.0 0.3 4.2

Net Margin

Sainsbury's

Profit for the

Year 309 377 471 (166) 716

Revenue

28,45

6

26,22

4 23,506 23,775 23,949

30MBA-FINANCIAL ANALYSIS AND MANAGEMENT

1.1 1.4 2.0 (0.7) 3.0

1

.

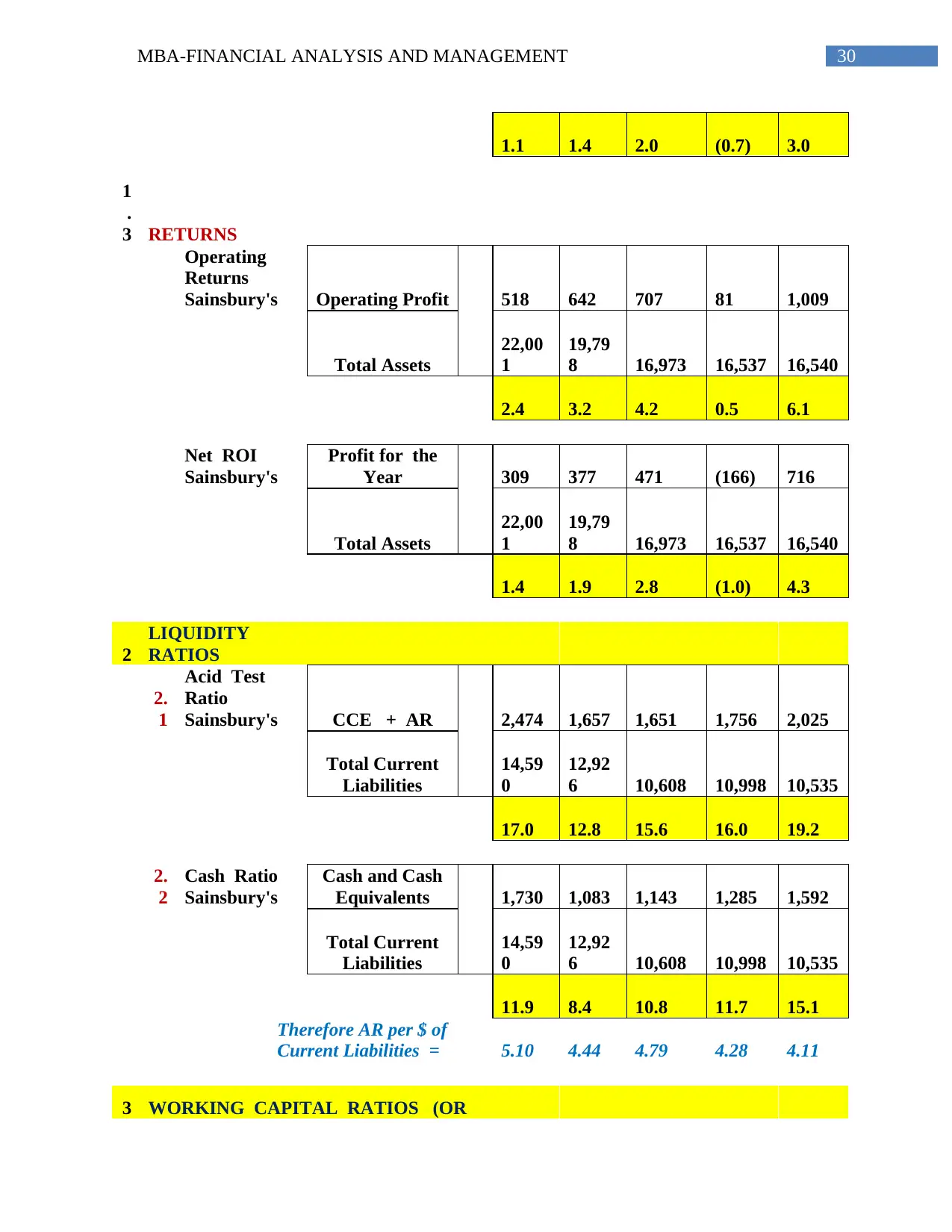

3 RETURNS

Operating

Returns

Sainsbury's Operating Profit 518 642 707 81 1,009

Total Assets

22,00

1

19,79

8 16,973 16,537 16,540

2.4 3.2 4.2 0.5 6.1

Net ROI

Sainsbury's

Profit for the

Year 309 377 471 (166) 716

Total Assets

22,00

1

19,79

8 16,973 16,537 16,540

1.4 1.9 2.8 (1.0) 4.3

2

LIQUIDITY

RATIOS

2.

1

Acid Test

Ratio

Sainsbury's CCE + AR 2,474 1,657 1,651 1,756 2,025

Total Current

Liabilities

14,59

0

12,92

6 10,608 10,998 10,535

17.0 12.8 15.6 16.0 19.2

2.

2

Cash Ratio

Sainsbury's

Cash and Cash

Equivalents 1,730 1,083 1,143 1,285 1,592

Total Current

Liabilities

14,59

0

12,92

6 10,608 10,998 10,535

11.9 8.4 10.8 11.7 15.1

Therefore AR per $ of

Current Liabilities = 5.10 4.44 4.79 4.28 4.11

3 WORKING CAPITAL RATIOS (OR

1.1 1.4 2.0 (0.7) 3.0

1

.

3 RETURNS

Operating

Returns

Sainsbury's Operating Profit 518 642 707 81 1,009

Total Assets

22,00

1

19,79

8 16,973 16,537 16,540

2.4 3.2 4.2 0.5 6.1

Net ROI

Sainsbury's

Profit for the

Year 309 377 471 (166) 716

Total Assets

22,00

1

19,79

8 16,973 16,537 16,540

1.4 1.9 2.8 (1.0) 4.3

2

LIQUIDITY

RATIOS

2.

1

Acid Test

Ratio

Sainsbury's CCE + AR 2,474 1,657 1,651 1,756 2,025

Total Current

Liabilities

14,59

0

12,92

6 10,608 10,998 10,535

17.0 12.8 15.6 16.0 19.2

2.

2

Cash Ratio

Sainsbury's

Cash and Cash

Equivalents 1,730 1,083 1,143 1,285 1,592

Total Current

Liabilities

14,59

0

12,92

6 10,608 10,998 10,535

11.9 8.4 10.8 11.7 15.1

Therefore AR per $ of

Current Liabilities = 5.10 4.44 4.79 4.28 4.11

3 WORKING CAPITAL RATIOS (OR

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

31MBA-FINANCIAL ANALYSIS AND MANAGEMENT

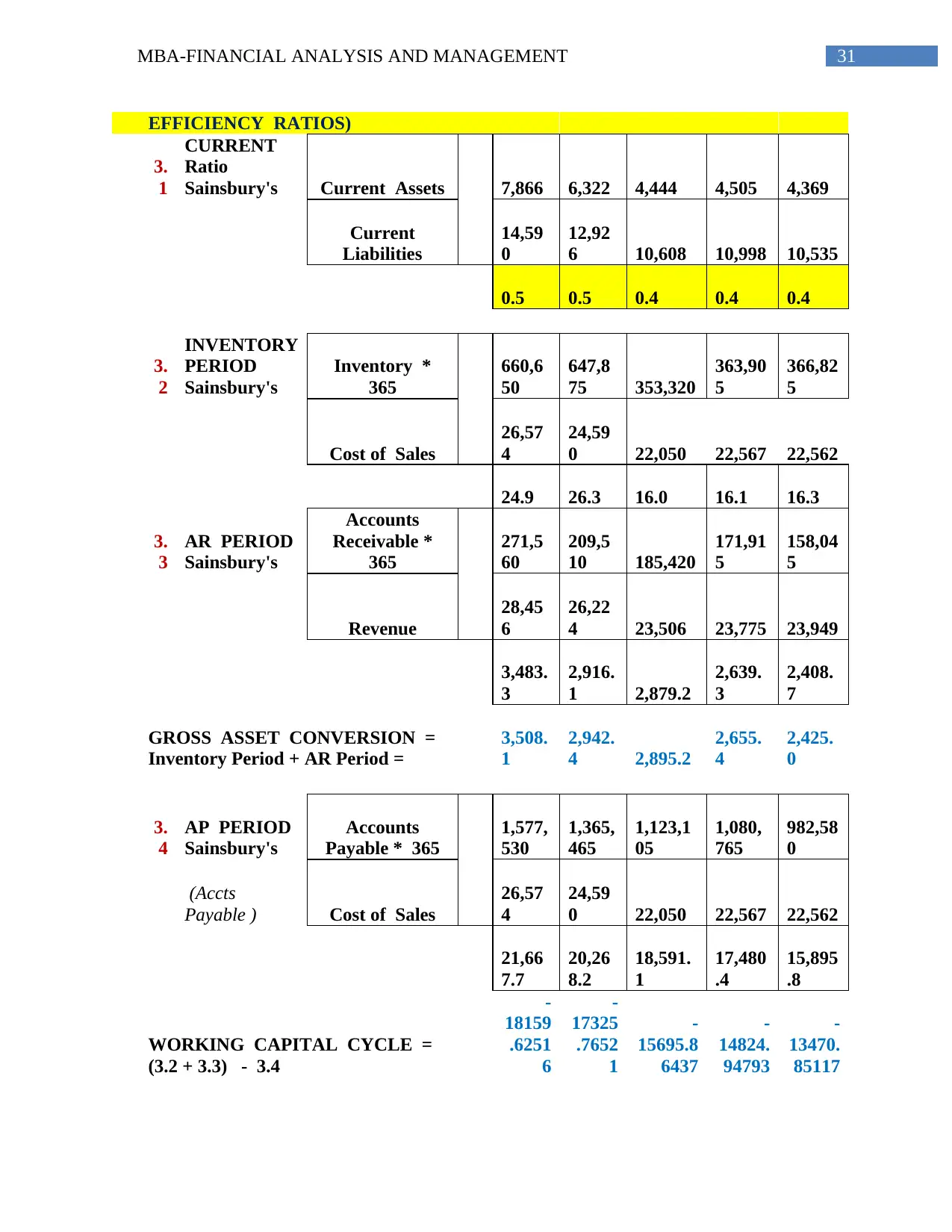

EFFICIENCY RATIOS)

3.

1

CURRENT

Ratio

Sainsbury's Current Assets 7,866 6,322 4,444 4,505 4,369

Current

Liabilities

14,59

0

12,92

6 10,608 10,998 10,535

0.5 0.5 0.4 0.4 0.4

3.

2

INVENTORY

PERIOD

Sainsbury's

Inventory *

365

660,6

50

647,8

75 353,320

363,90

5

366,82

5

Cost of Sales

26,57

4

24,59

0 22,050 22,567 22,562

24.9 26.3 16.0 16.1 16.3

3.

3

AR PERIOD

Sainsbury's

Accounts

Receivable *

365

271,5

60

209,5

10 185,420

171,91

5

158,04

5

Revenue

28,45

6

26,22

4 23,506 23,775 23,949

3,483.

3

2,916.

1 2,879.2

2,639.

3

2,408.

7

GROSS ASSET CONVERSION =

Inventory Period + AR Period =

3,508.

1

2,942.

4 2,895.2

2,655.

4

2,425.

0

3.

4

AP PERIOD

Sainsbury's

Accounts

Payable * 365

1,577,

530

1,365,

465

1,123,1

05

1,080,

765

982,58

0

(Accts

Payable ) Cost of Sales

26,57

4

24,59

0 22,050 22,567 22,562

21,66

7.7

20,26

8.2

18,591.

1

17,480

.4

15,895

.8

WORKING CAPITAL CYCLE =

(3.2 + 3.3) - 3.4

-

18159

.6251

6

-

17325

.7652

1

-

15695.8

6437

-

14824.

94793

-

13470.

85117

EFFICIENCY RATIOS)

3.

1

CURRENT

Ratio

Sainsbury's Current Assets 7,866 6,322 4,444 4,505 4,369

Current

Liabilities

14,59

0

12,92

6 10,608 10,998 10,535

0.5 0.5 0.4 0.4 0.4

3.

2

INVENTORY

PERIOD

Sainsbury's

Inventory *

365

660,6

50

647,8

75 353,320

363,90

5

366,82

5

Cost of Sales

26,57

4

24,59

0 22,050 22,567 22,562

24.9 26.3 16.0 16.1 16.3

3.

3

AR PERIOD

Sainsbury's

Accounts

Receivable *

365

271,5

60

209,5

10 185,420

171,91

5

158,04

5

Revenue

28,45

6

26,22

4 23,506 23,775 23,949

3,483.

3

2,916.

1 2,879.2

2,639.

3

2,408.

7

GROSS ASSET CONVERSION =

Inventory Period + AR Period =

3,508.

1

2,942.

4 2,895.2

2,655.

4

2,425.

0

3.

4

AP PERIOD

Sainsbury's

Accounts

Payable * 365

1,577,

530

1,365,

465

1,123,1

05

1,080,

765

982,58

0

(Accts

Payable ) Cost of Sales

26,57

4

24,59

0 22,050 22,567 22,562

21,66

7.7

20,26

8.2

18,591.

1

17,480

.4

15,895

.8

WORKING CAPITAL CYCLE =

(3.2 + 3.3) - 3.4

-

18159

.6251

6

-

17325

.7652

1

-

15695.8

6437

-

14824.

94793

-

13470.

85117

32MBA-FINANCIAL ANALYSIS AND MANAGEMENT

4 DEBT MANAGEMENT

4.

1

Gearing %

Sainsbury's

Total Long

Term Liabilities 1,602 2,039 2,190 2,506 2,250

Total Equity 7,411 6,872 6,365 5,539 6,005

21.6 29.7 34.4 45.2 37.5