Management Accounting Report: Balanced Scorecard for McDonald's

VerifiedAdded on 2021/05/31

|17

|3937

|39

Report

AI Summary

This report evaluates the suitability of the Balanced Scorecard (BSC) method for McDonald's. It begins with an executive summary and table of contents, followed by an introduction to management accounting and the BSC concept. The report provides an overview of McDonald's, including its history and current operations, before detailing the four perspectives of the BSC: financial, customer, internal business processes, and learning and growth. It discusses the features of the BSC, such as financial evaluation, customer perspective measurement, internal business process classification, and learning and growth considerations. The report presents an example of a BSC applied to McDonald's, highlights the differences between traditional performance measurement systems and the BSC, and concludes with an assessment of the BSC's suitability for McDonald's. The analysis emphasizes how the BSC simplifies strategic goals, communicates vision and mission, refines metrics and measures, and enables performance analysis for the company. References are included at the end of the report.

Management Accounting

McDonald’s

[Type the phone number]

5 / 1 7 / 2 0 1 8

McDonald’s

[Type the phone number]

5 / 1 7 / 2 0 1 8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGEMENT ACCOUNTING 1

Executive Summary

This report is being prepared in order to identify whether Balanced Scorecard method is

suitable for McDonald's or not. In order to identify this, the report will highlight various

aspects like company's description, the concept of the balanced scorecard and its suitability in

the company.

Executive Summary

This report is being prepared in order to identify whether Balanced Scorecard method is

suitable for McDonald's or not. In order to identify this, the report will highlight various

aspects like company's description, the concept of the balanced scorecard and its suitability in

the company.

MANAGEMENT ACCOUNTING 2

Table of Contents

Executive Summary...................................................................................................................1

Introduction................................................................................................................................3

Overview of McDonald’s.......................................................................................................3

Balanced Scorecard................................................................................................................4

Four Legs of Balanced Scorecard......................................................................................5

Features of Balanced Scorecard.............................................................................................6

Financial Evaluation...........................................................................................................6

Measuring perspective of customers..................................................................................6

Classifying Internal Business Processes............................................................................6

Learning and growth..........................................................................................................7

Clarify the image of the company......................................................................................7

Flexibility...........................................................................................................................7

Example of the Balanced Scorecard in McDonald's..........................................................7

Difference between Traditional Performance Measurement systems and Balanced

Scorecard................................................................................................................................8

Suitability Balanced Scorecard for McDonald’s..................................................................11

Simplifies Strategic Goals................................................................................................11

Communicates Vision and Mission.................................................................................11

Refines Metrics and Measures.........................................................................................11

Enables Performance Analysis.........................................................................................12

Conclusion................................................................................................................................12

References................................................................................................................................13

Table of Contents

Executive Summary...................................................................................................................1

Introduction................................................................................................................................3

Overview of McDonald’s.......................................................................................................3

Balanced Scorecard................................................................................................................4

Four Legs of Balanced Scorecard......................................................................................5

Features of Balanced Scorecard.............................................................................................6

Financial Evaluation...........................................................................................................6

Measuring perspective of customers..................................................................................6

Classifying Internal Business Processes............................................................................6

Learning and growth..........................................................................................................7

Clarify the image of the company......................................................................................7

Flexibility...........................................................................................................................7

Example of the Balanced Scorecard in McDonald's..........................................................7

Difference between Traditional Performance Measurement systems and Balanced

Scorecard................................................................................................................................8

Suitability Balanced Scorecard for McDonald’s..................................................................11

Simplifies Strategic Goals................................................................................................11

Communicates Vision and Mission.................................................................................11

Refines Metrics and Measures.........................................................................................11

Enables Performance Analysis.........................................................................................12

Conclusion................................................................................................................................12

References................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGEMENT ACCOUNTING 3

Introduction

The procedure of recognizing, determining, examining, understanding and communicating

information for achieving goals of the organization is known as Management accounting

(Arora, 2012). This accounting branch is also called as cost accounting. The major difference

between financial accounting and managerial accounting is that information is focused

towards supporting administrators in the organization in making decisions, whereas financial

accounting is focused towards offering information to the partied outside the boundary of the

organization (Adler, 2013). This report is focused towards providing the information of one

of the information measurement system i.e. Balanced Scorecard which will be applied in the

McDonald's to identify whether it will be beneficial for the company or not. To do so report

will talk about balanced scorecard and its features. The overview of McDonald’s will be

given to know more about the company. Further, discussion of the difference between

balanced scorecard and traditional performance measurement system will be conducted and

in the end, whether balanced scorecard system is suitable for McDonald’s or not will be

discussed.

Overview of McDonald’s

McDonald’s is a fast food company of Australia which was established in 1940 by Maurice

and Richard McDonald in California, United States. They started the business as a hamburger

stand (McDonald’s, 2018). The first time the franchise of McDonald’s was in 1953 utilized

by Golden Arches logo in Phoenix, Arizona. Ray Kroc who is a famous businessman joined

the company in 1955, as an agent of the franchise and continued to buy the chain from the

McDonald's brother. The original headquarter of McDonald’s is in Illinois, however,

transferred the worldwide headquarter to Chicago in 2018.

Introduction

The procedure of recognizing, determining, examining, understanding and communicating

information for achieving goals of the organization is known as Management accounting

(Arora, 2012). This accounting branch is also called as cost accounting. The major difference

between financial accounting and managerial accounting is that information is focused

towards supporting administrators in the organization in making decisions, whereas financial

accounting is focused towards offering information to the partied outside the boundary of the

organization (Adler, 2013). This report is focused towards providing the information of one

of the information measurement system i.e. Balanced Scorecard which will be applied in the

McDonald's to identify whether it will be beneficial for the company or not. To do so report

will talk about balanced scorecard and its features. The overview of McDonald’s will be

given to know more about the company. Further, discussion of the difference between

balanced scorecard and traditional performance measurement system will be conducted and

in the end, whether balanced scorecard system is suitable for McDonald’s or not will be

discussed.

Overview of McDonald’s

McDonald’s is a fast food company of Australia which was established in 1940 by Maurice

and Richard McDonald in California, United States. They started the business as a hamburger

stand (McDonald’s, 2018). The first time the franchise of McDonald’s was in 1953 utilized

by Golden Arches logo in Phoenix, Arizona. Ray Kroc who is a famous businessman joined

the company in 1955, as an agent of the franchise and continued to buy the chain from the

McDonald's brother. The original headquarter of McDonald’s is in Illinois, however,

transferred the worldwide headquarter to Chicago in 2018.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGEMENT ACCOUNTING 4

McDonald’s is said to be the largest chain of the restaurant by revenue in the world, by

serving approx. 69 million consumers daily in about 100 countries with around 36,900 outlets

as of 2016 (McDonald’s, 2015). Though McDonald's is famous for its hamburgers, they also

sell cheeseburgers, French fries, soft drinks, chicken products, desserts, breakfast items,

wraps, and milkshakes. In order to deal with the changing taste of the customers and an

adverse reaction due to the unhealthy food, the company has added more items in its menu

i.e. fish, fruit, salads, and smoothies. The revenue of the McDonald’s Corporation is earned

from royalties, franchising fees, and rent, along with sales in the restaurants of the company.

As per the report of BCC of 2012, McDonald’s is the second-biggest private employer in the

world after Wal-Mart of 1.9 million employees, and from this 1.5 work for the franchises

(Myers, 2018).

In 1963, the McDonald’s public face was created with the establishment of a clown called

Ronald McDonald, although the dual arch “m” which is the symbol in 1962 became the

McDonald’s most lasting logo, long-lasting for lengthier than the big yellow arches that had

once ruled the previous restaurant rooftops. The products and symbols of the company define

the brand comprising The Egg McMuffin, Chicken Nuggets, Happy Meals, and the Big Mac.

The restaurant chain sustained to grow internationally and domestically, spreading business

in Canada in the year 1967, which resulted in touching the total of 10,000 restaurants in 1988

and functioning around 35,000 outlets in approx. 100 countries in the starting of the 21st

century. In the 1990s, the evolution was so rapid that people started saying that in every five

hours a new McDonald’s outlet is opened somewhere in the world. It efficiently became the

famous restaurant for family, highlighting reasonable food, flavors, and fun that seemed to

adults and children alike (McDonald’s, 2012).

McDonald’s is said to be the largest chain of the restaurant by revenue in the world, by

serving approx. 69 million consumers daily in about 100 countries with around 36,900 outlets

as of 2016 (McDonald’s, 2015). Though McDonald's is famous for its hamburgers, they also

sell cheeseburgers, French fries, soft drinks, chicken products, desserts, breakfast items,

wraps, and milkshakes. In order to deal with the changing taste of the customers and an

adverse reaction due to the unhealthy food, the company has added more items in its menu

i.e. fish, fruit, salads, and smoothies. The revenue of the McDonald’s Corporation is earned

from royalties, franchising fees, and rent, along with sales in the restaurants of the company.

As per the report of BCC of 2012, McDonald’s is the second-biggest private employer in the

world after Wal-Mart of 1.9 million employees, and from this 1.5 work for the franchises

(Myers, 2018).

In 1963, the McDonald’s public face was created with the establishment of a clown called

Ronald McDonald, although the dual arch “m” which is the symbol in 1962 became the

McDonald’s most lasting logo, long-lasting for lengthier than the big yellow arches that had

once ruled the previous restaurant rooftops. The products and symbols of the company define

the brand comprising The Egg McMuffin, Chicken Nuggets, Happy Meals, and the Big Mac.

The restaurant chain sustained to grow internationally and domestically, spreading business

in Canada in the year 1967, which resulted in touching the total of 10,000 restaurants in 1988

and functioning around 35,000 outlets in approx. 100 countries in the starting of the 21st

century. In the 1990s, the evolution was so rapid that people started saying that in every five

hours a new McDonald’s outlet is opened somewhere in the world. It efficiently became the

famous restaurant for family, highlighting reasonable food, flavors, and fun that seemed to

adults and children alike (McDonald’s, 2012).

MANAGEMENT ACCOUNTING 5

Balanced Scorecard

A performance metric utilizes in strategic management to recognize and enhance different

internal functions of the company and their resulting external consequences are known as

Balanced Scorecard (Rohm, 2017). It is utilized to evaluate and offer feedback to the

companies. Data collection is vital to provide quantitative outcomes, because the information

which is collected is understood by the executives and managers, and used to take improved

decisions for the company or organization (Johnson, 2018).

The Balanced Scorecard was established by Dr. Dravid Norton who is a theorist and by Dr.

Robert Kaplan who is an accounting academic. This system is utilized to strengthen good

behaviors in the company by dividing four distinct areas that should be examined. These four

areas are also said as a leg of this system and involve business processes, learning and

growth, finance, and customers. The balanced scorecard is utilized to achieve goals,

capacities, creativities and objectives that result from four key business functions. Business

can easily recognize factors hampering the performance of the company and plan strategic

variations tracked by future scorecards. It can also be used to execute strategy mapping to

look where the value is added to the company (Niven, 2010).

Four Legs of Balanced Scorecard

Information is gathered and evaluated from 4 business aspects. First is learning and growth

they are evaluated by the examination of knowledge and training resources. This leg

maintains how well data or information is taken and how efficiently staff members use the

information to make it a competitive advantage in the industry.

Second is a business process it is analyzed through examination of how well goods are

produced (50MINUTES, 2015). The operational administration is examined to identify any

delays, gaps, blockages, scarcities or waste.

Balanced Scorecard

A performance metric utilizes in strategic management to recognize and enhance different

internal functions of the company and their resulting external consequences are known as

Balanced Scorecard (Rohm, 2017). It is utilized to evaluate and offer feedback to the

companies. Data collection is vital to provide quantitative outcomes, because the information

which is collected is understood by the executives and managers, and used to take improved

decisions for the company or organization (Johnson, 2018).

The Balanced Scorecard was established by Dr. Dravid Norton who is a theorist and by Dr.

Robert Kaplan who is an accounting academic. This system is utilized to strengthen good

behaviors in the company by dividing four distinct areas that should be examined. These four

areas are also said as a leg of this system and involve business processes, learning and

growth, finance, and customers. The balanced scorecard is utilized to achieve goals,

capacities, creativities and objectives that result from four key business functions. Business

can easily recognize factors hampering the performance of the company and plan strategic

variations tracked by future scorecards. It can also be used to execute strategy mapping to

look where the value is added to the company (Niven, 2010).

Four Legs of Balanced Scorecard

Information is gathered and evaluated from 4 business aspects. First is learning and growth

they are evaluated by the examination of knowledge and training resources. This leg

maintains how well data or information is taken and how efficiently staff members use the

information to make it a competitive advantage in the industry.

Second is a business process it is analyzed through examination of how well goods are

produced (50MINUTES, 2015). The operational administration is examined to identify any

delays, gaps, blockages, scarcities or waste.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGEMENT ACCOUNTING 6

Third are customer perspectives these are gathered to measure the satisfaction of the

customers with prices, availability, and quality of products or services. Consumers provide

their feedback about whether their needs are fulfilled or not with the present products or

services (Pramudita, 2016).

Fourth, financial data like expenditures, income, and sales are utilized to known the financial

performance of the company. These metrics can comprise amounts in the dollar, budget

variances, financial ratios, or income targets. These four legs include the strategy and vision

of the company and need active management to examine the gathered data. Thus, the

balanced scorecard is mostly said as a tool of management, and not as a measurement tool

(Giannopoulos and Holt, 2013).

Features of Balanced Scorecard

Financial Evaluation – Financial evaluation is one of the traditional features of the balanced

scorecard. No single management employees will be concerned about balanced scorecard if it

does not involve this feature as it conducts with the profits, which are important for the goals

of making shareholder value. If possible, this feature must be considered equal same as other

features, however, other features are given more importance from this. This feature comprises

measures like return on assets, profit margins, and return on equity.

Measuring perspective of customers – Measuring perception of the customer's permits to

understand the organization as it exists due to the customers and for the customers, without

whom the company cannot survive. It is a not as much of an upfront feature as compared to

financial evaluation as it does not possess the similar static performance pointers. Perception

of the customers about a company is normally examined by surveys that confront customers

whether they life company or not and whether they can link the company with value or not.

Third are customer perspectives these are gathered to measure the satisfaction of the

customers with prices, availability, and quality of products or services. Consumers provide

their feedback about whether their needs are fulfilled or not with the present products or

services (Pramudita, 2016).

Fourth, financial data like expenditures, income, and sales are utilized to known the financial

performance of the company. These metrics can comprise amounts in the dollar, budget

variances, financial ratios, or income targets. These four legs include the strategy and vision

of the company and need active management to examine the gathered data. Thus, the

balanced scorecard is mostly said as a tool of management, and not as a measurement tool

(Giannopoulos and Holt, 2013).

Features of Balanced Scorecard

Financial Evaluation – Financial evaluation is one of the traditional features of the balanced

scorecard. No single management employees will be concerned about balanced scorecard if it

does not involve this feature as it conducts with the profits, which are important for the goals

of making shareholder value. If possible, this feature must be considered equal same as other

features, however, other features are given more importance from this. This feature comprises

measures like return on assets, profit margins, and return on equity.

Measuring perspective of customers – Measuring perception of the customer's permits to

understand the organization as it exists due to the customers and for the customers, without

whom the company cannot survive. It is a not as much of an upfront feature as compared to

financial evaluation as it does not possess the similar static performance pointers. Perception

of the customers about a company is normally examined by surveys that confront customers

whether they life company or not and whether they can link the company with value or not.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGEMENT ACCOUNTING 7

Classifying Internal Business Processes - To flourish, a company should know its main

competencies. A balanced scorecard recognizes internal processes of the business. This

comprises understanding which procedures are very important for an organization to get

success and assessing how the firm performs. The goal of this feature is to evaluate the

competence of the important operations of the company. Instances of processes comprise

distribution, manufacturing, and marketing.

Learning and growth – Businesses should regularly growth or the risk becoming obsolete.

Hence, learning and growth are involved in a balanced scorecard. This measures how a

company is capable to create new processes and knowledge and how it is capable to interpret

this into development and growth of the company (Clark, 2017).

Clarify the image of the company – Effective balanced scorecard help in defining the effect

and cause clearly about different objectives to the employees and stakeholder. The

explanation of the objective of the company and its target must be clearly explained to

decrease the chances of conflicts in the future.

Flexibility – A balanced scorecard must be very flexible. It should not create rigid

boundaries around the strategic objectives. In place of this, it permits the management to do

required changes whenever possible (Biazzo and Garengo, 2012).

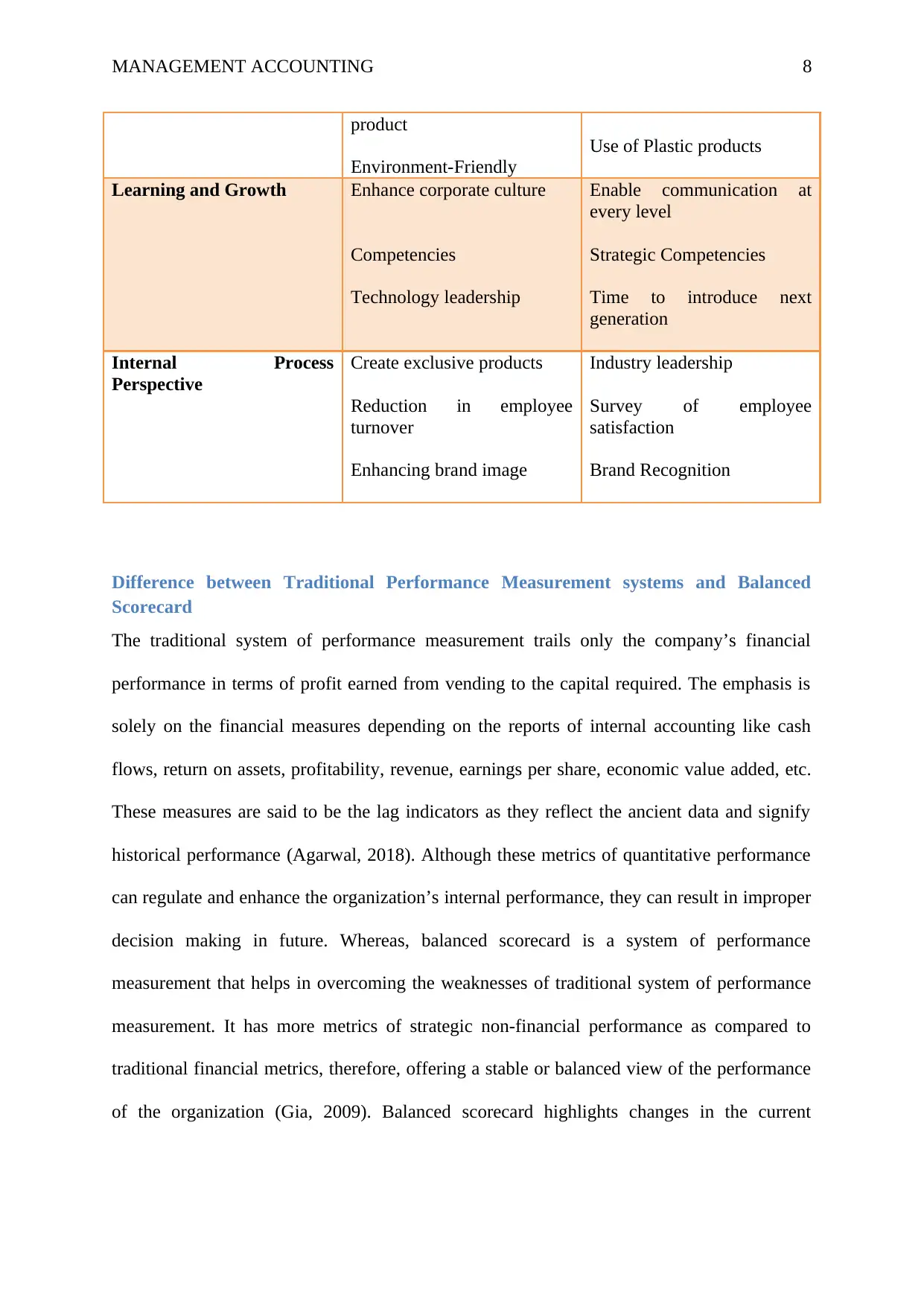

Example of the Balanced Scorecard in McDonald's

Perspectives Objectives Measures

Financial Perspective Market survival

Growth in Revenue

Enhance structure of cost

Cash Flow

Sales Volume

Actual Cost

Customer Perspective Effective service to the

customer

Enhance the quality of the

Satisfaction of customer

Increase in the number of

customers

Classifying Internal Business Processes - To flourish, a company should know its main

competencies. A balanced scorecard recognizes internal processes of the business. This

comprises understanding which procedures are very important for an organization to get

success and assessing how the firm performs. The goal of this feature is to evaluate the

competence of the important operations of the company. Instances of processes comprise

distribution, manufacturing, and marketing.

Learning and growth – Businesses should regularly growth or the risk becoming obsolete.

Hence, learning and growth are involved in a balanced scorecard. This measures how a

company is capable to create new processes and knowledge and how it is capable to interpret

this into development and growth of the company (Clark, 2017).

Clarify the image of the company – Effective balanced scorecard help in defining the effect

and cause clearly about different objectives to the employees and stakeholder. The

explanation of the objective of the company and its target must be clearly explained to

decrease the chances of conflicts in the future.

Flexibility – A balanced scorecard must be very flexible. It should not create rigid

boundaries around the strategic objectives. In place of this, it permits the management to do

required changes whenever possible (Biazzo and Garengo, 2012).

Example of the Balanced Scorecard in McDonald's

Perspectives Objectives Measures

Financial Perspective Market survival

Growth in Revenue

Enhance structure of cost

Cash Flow

Sales Volume

Actual Cost

Customer Perspective Effective service to the

customer

Enhance the quality of the

Satisfaction of customer

Increase in the number of

customers

MANAGEMENT ACCOUNTING 8

product

Environment-Friendly

Use of Plastic products

Learning and Growth Enhance corporate culture

Competencies

Technology leadership

Enable communication at

every level

Strategic Competencies

Time to introduce next

generation

Internal Process

Perspective

Create exclusive products

Reduction in employee

turnover

Enhancing brand image

Industry leadership

Survey of employee

satisfaction

Brand Recognition

Difference between Traditional Performance Measurement systems and Balanced

Scorecard

The traditional system of performance measurement trails only the company’s financial

performance in terms of profit earned from vending to the capital required. The emphasis is

solely on the financial measures depending on the reports of internal accounting like cash

flows, return on assets, profitability, revenue, earnings per share, economic value added, etc.

These measures are said to be the lag indicators as they reflect the ancient data and signify

historical performance (Agarwal, 2018). Although these metrics of quantitative performance

can regulate and enhance the organization’s internal performance, they can result in improper

decision making in future. Whereas, balanced scorecard is a system of performance

measurement that helps in overcoming the weaknesses of traditional system of performance

measurement. It has more metrics of strategic non-financial performance as compared to

traditional financial metrics, therefore, offering a stable or balanced view of the performance

of the organization (Gia, 2009). Balanced scorecard highlights changes in the current

product

Environment-Friendly

Use of Plastic products

Learning and Growth Enhance corporate culture

Competencies

Technology leadership

Enable communication at

every level

Strategic Competencies

Time to introduce next

generation

Internal Process

Perspective

Create exclusive products

Reduction in employee

turnover

Enhancing brand image

Industry leadership

Survey of employee

satisfaction

Brand Recognition

Difference between Traditional Performance Measurement systems and Balanced

Scorecard

The traditional system of performance measurement trails only the company’s financial

performance in terms of profit earned from vending to the capital required. The emphasis is

solely on the financial measures depending on the reports of internal accounting like cash

flows, return on assets, profitability, revenue, earnings per share, economic value added, etc.

These measures are said to be the lag indicators as they reflect the ancient data and signify

historical performance (Agarwal, 2018). Although these metrics of quantitative performance

can regulate and enhance the organization’s internal performance, they can result in improper

decision making in future. Whereas, balanced scorecard is a system of performance

measurement that helps in overcoming the weaknesses of traditional system of performance

measurement. It has more metrics of strategic non-financial performance as compared to

traditional financial metrics, therefore, offering a stable or balanced view of the performance

of the organization (Gia, 2009). Balanced scorecard highlights changes in the current

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGEMENT ACCOUNTING 9

competitive environment by considering the intangible assets that are now a key source of

competitive advantage (Schmeisser and Clausen, 2011).

The traditional system of performance measurement fundamentally dependent on the

financial metrics can inspire executives to take decisions that sacrifice long-term value

formation for the advantage of short-term performance. For instance, cost reduction can

upsurge profit in short-term, however simply at the loss of quality expense, customer base

loss or loss of expertise which all have long-run influences (Pourmoradi and Niknafs, 2016).

On the other hand, the balanced scorecard is an integrated system of strategic management

that supports activities of the business to the organization strategy by involving measurement

of performance with the strategic objectives of the company. It offers a framework to

interpret the strategy of the organization into precise assessable objectives of the performance

that can be measured (Yilmaz, 2013).

The financial performance is dependent on the historical data was adequate for the purpose of

decision making. But, the modern environment of business has shifted from bulk production

dependent industrial time to knowledge-based time period. This change has brought a

transformation from depending only on measuring tangible assets in the direction of valuing

of intangible assets like human capital, customer relationship, and intellectual capital, etc.

Therefore, in present competitive environment, single dependence on the financial measure is

unsuitable because this measure does not evaluate intangible assets, does not highlight the

competitive rivalry issues. Besides this, traditional performance measures are not related to

the strategy of the organization. Strategies are linked with the organization's long-run goals,

the organization's activity scope, the matching and allocation of organizational activities to its

resources ability and needs of the business, and consideration of the stakeholders of the

organization expectations and values. In another side, the objectives of the performance are

evaluated by using the four perspectives which are interconnected, i.e., the financial

competitive environment by considering the intangible assets that are now a key source of

competitive advantage (Schmeisser and Clausen, 2011).

The traditional system of performance measurement fundamentally dependent on the

financial metrics can inspire executives to take decisions that sacrifice long-term value

formation for the advantage of short-term performance. For instance, cost reduction can

upsurge profit in short-term, however simply at the loss of quality expense, customer base

loss or loss of expertise which all have long-run influences (Pourmoradi and Niknafs, 2016).

On the other hand, the balanced scorecard is an integrated system of strategic management

that supports activities of the business to the organization strategy by involving measurement

of performance with the strategic objectives of the company. It offers a framework to

interpret the strategy of the organization into precise assessable objectives of the performance

that can be measured (Yilmaz, 2013).

The financial performance is dependent on the historical data was adequate for the purpose of

decision making. But, the modern environment of business has shifted from bulk production

dependent industrial time to knowledge-based time period. This change has brought a

transformation from depending only on measuring tangible assets in the direction of valuing

of intangible assets like human capital, customer relationship, and intellectual capital, etc.

Therefore, in present competitive environment, single dependence on the financial measure is

unsuitable because this measure does not evaluate intangible assets, does not highlight the

competitive rivalry issues. Besides this, traditional performance measures are not related to

the strategy of the organization. Strategies are linked with the organization's long-run goals,

the organization's activity scope, the matching and allocation of organizational activities to its

resources ability and needs of the business, and consideration of the stakeholders of the

organization expectations and values. In another side, the objectives of the performance are

evaluated by using the four perspectives which are interconnected, i.e., the financial

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGEMENT ACCOUNTING 10

perspective, learning and growth perspective, customer perspective, and business processes

perspective.

Traditional performances systems concentrate on the short-run financial performance,

ensuing in sever between the long-run strategy of the company and short-run actions.

Organizations should evaluate performance in those methods that not just only imitate past

optimistic performance, but also inspire positive results of the future. Present, the

environment of business is considered by strong competitive rivalry and as an outcome

businesses need to be adaptive and flexible in order to gain and tolerate a competitive

advantage. The organization should outshine in other serious areas like service or product

quality, customer relationships, organizational flexibility, relationships with employees,

relationships with suppliers, knowledge of technology and processes, and innovation to

continue in the present competitive environment.

The Balanced scorecard measures the performance of the company from its four legs or

perspectives when metrics of performance are designed, analyzed and gathered relative to

every four perspectives. The evaluation of four perspectives has an inter-dependent

relationship among them. The perspective of learning and growth results in supplying high-

quality internal processes of business as employees will have grown correct competencies

(Striteska and Spickova, 2012). With effective internal processes of business, the company

will be capable to fulfill the needs of the customers and will increase customer loyalty and

market share for prospect business. The higher satisfaction of the customer can result in

enhancing the financial performance of the company. This reflects that the purpose in the

four perspectives is linked. Hence, if a company can outshine in every perspective of the

balanced scorecard, the company will have an improved long-run financial success.

perspective, learning and growth perspective, customer perspective, and business processes

perspective.

Traditional performances systems concentrate on the short-run financial performance,

ensuing in sever between the long-run strategy of the company and short-run actions.

Organizations should evaluate performance in those methods that not just only imitate past

optimistic performance, but also inspire positive results of the future. Present, the

environment of business is considered by strong competitive rivalry and as an outcome

businesses need to be adaptive and flexible in order to gain and tolerate a competitive

advantage. The organization should outshine in other serious areas like service or product

quality, customer relationships, organizational flexibility, relationships with employees,

relationships with suppliers, knowledge of technology and processes, and innovation to

continue in the present competitive environment.

The Balanced scorecard measures the performance of the company from its four legs or

perspectives when metrics of performance are designed, analyzed and gathered relative to

every four perspectives. The evaluation of four perspectives has an inter-dependent

relationship among them. The perspective of learning and growth results in supplying high-

quality internal processes of business as employees will have grown correct competencies

(Striteska and Spickova, 2012). With effective internal processes of business, the company

will be capable to fulfill the needs of the customers and will increase customer loyalty and

market share for prospect business. The higher satisfaction of the customer can result in

enhancing the financial performance of the company. This reflects that the purpose in the

four perspectives is linked. Hence, if a company can outshine in every perspective of the

balanced scorecard, the company will have an improved long-run financial success.

MANAGEMENT ACCOUNTING 11

Hence, it can be said that traditional performance measurement system which mainly

concentrates on the measures of financial performance are not suitable in this changing

environment. Whereas, balanced scorecard evaluates the performance of the company by

balancing between non-financial and financial measures. Progress is evaluated with

traditional financial measures, like loss and profit, with current non-financial measures like

employee’s retention, customer satisfaction, intellectual capital, market share, and brand

equity (Suvarna, 2012).

Suitability Balanced Scorecard for McDonald’s

McDonald’s can introduce a balanced scorecard in order to support all its activities of the

company. This framework of performance management will add measures of non-financial to

traditional financial metrics and will provide leaders of the company a stable view of how

things are going. By following non-financial measures, McDonald’s can confirm about

evaluating relationships with customers, employees, and suppliers and its capability to

preserve a sustainable business. Some of the points that will highlight the suitability of

balanced scorecard for McDonald’s are:

Simplifies Strategic Goals – A balanced scorecard will support McDonald's in creating

strategies for the organization by determining the priorities of the company. Program

operations, service delivery, and reporting production metrics support company in measuring

how positively company is performing and areas that need to be considered for changes,

depending on the mission and vision of the company. For instance, the satisfaction of the

customer is the priority.

Communicates Vision and Mission - A balanced scorecard supports managers to

communicate the same vision and mission in the company, at all the level. Prioritization and

decision making became simpler because the balanced scorecard introduces standards for the

Hence, it can be said that traditional performance measurement system which mainly

concentrates on the measures of financial performance are not suitable in this changing

environment. Whereas, balanced scorecard evaluates the performance of the company by

balancing between non-financial and financial measures. Progress is evaluated with

traditional financial measures, like loss and profit, with current non-financial measures like

employee’s retention, customer satisfaction, intellectual capital, market share, and brand

equity (Suvarna, 2012).

Suitability Balanced Scorecard for McDonald’s

McDonald’s can introduce a balanced scorecard in order to support all its activities of the

company. This framework of performance management will add measures of non-financial to

traditional financial metrics and will provide leaders of the company a stable view of how

things are going. By following non-financial measures, McDonald’s can confirm about

evaluating relationships with customers, employees, and suppliers and its capability to

preserve a sustainable business. Some of the points that will highlight the suitability of

balanced scorecard for McDonald’s are:

Simplifies Strategic Goals – A balanced scorecard will support McDonald's in creating

strategies for the organization by determining the priorities of the company. Program

operations, service delivery, and reporting production metrics support company in measuring

how positively company is performing and areas that need to be considered for changes,

depending on the mission and vision of the company. For instance, the satisfaction of the

customer is the priority.

Communicates Vision and Mission - A balanced scorecard supports managers to

communicate the same vision and mission in the company, at all the level. Prioritization and

decision making became simpler because the balanced scorecard introduces standards for the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.