McDonald's Expansion: Financial Plan and Analysis Report

VerifiedAdded on 2020/11/12

|14

|4324

|54

Report

AI Summary

This report provides a detailed financial analysis of McDonald's expansion plans in Coventry High Street. It includes an overview of the company's vision and mission, followed by a comprehensive financial plan. The financial plan encompasses breakeven analysis for burgers and beverages, projected profit and loss statements, cash flow projections, and balance sheets for three years (2018-2020). The analysis also includes key financial ratios to assess the financial health and performance of the expansion. The report aims to forecast financial requirements and operational changes necessary for successful business growth, providing valuable insights into the financial feasibility and potential profitability of the expansion project. The report also contains interpretation of data, and the financial statements included are the income statement, cash flow statement, and balance sheet.

FINANCE IN

MANAGEMENT AND

LEADERSHIP

MANAGEMENT AND

LEADERSHIP

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

Overview................................................................................................................................1

Vision and Mission.................................................................................................................1

FINANCIAL PLAN.........................................................................................................................2

Breakeven Analysis................................................................................................................2

Projected Profit and Loss........................................................................................................4

Projected Cash flow................................................................................................................5

Projected Balance sheet..........................................................................................................7

Financial ratios.......................................................................................................................8

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

Overview................................................................................................................................1

Vision and Mission.................................................................................................................1

FINANCIAL PLAN.........................................................................................................................2

Breakeven Analysis................................................................................................................2

Projected Profit and Loss........................................................................................................4

Projected Cash flow................................................................................................................5

Projected Balance sheet..........................................................................................................7

Financial ratios.......................................................................................................................8

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Expansion and developing newer ideas are main perceptions which have been used by

various organisations with motive of creating new opportunities as well as Improving business

on new platform. It enhances the operational activities as well as performance of entity in large

scale. In the present report there has been discussion based on expanding the McDonald’s

business in Coventry High Street. Along, with this there will be discussion based on various

financial requirements and changes in operations which can be needful in forecasting cash

requirements.

Overview

McDonald’s has been known as world’s largest food chain restaurant which serves in

many countries or locations. The satisfaction it brings to consumers are based on convenience in

cost as well as quality. The large varieties of burgers as well as various fast food dishes has been

presented by McDonald’s with considering proper quality of products (Chen and et.al., 2018). In

approach with same firm plans to make expansion of its operations which comprises of various

processes such as serving varieties of burgers, beverages and various fast food dishes.

Managerial professionals have been thought about making expansion of operations which

will be helpful in leading firm on right direction. They have selected Coventry High street as a

new location which has been analysed as the most convenient and profitable area for

McDonald’s to have successful business (Easton and Monahan, 2016). The motive of industry is

for serving students, workers and local citizens in location with good food quality as well as with

lower prices.

Vision and Mission

In terms of analysing objectives and motive of business on which it can be said that there will

be need of having adequate operational increments as well as development of brand image in the

market (Ruginski and et.al., 2016). Considering the most convenient prices which will be

charged by McDonald’s on its food and beverages with the motive of having higher sales in each

period. Therefore, expansion of operations will lead firm in widening operational area as well as

generating adequate revenue through activities. There has been various objective which have

been undertaken by the professionals such as:

1

Expansion and developing newer ideas are main perceptions which have been used by

various organisations with motive of creating new opportunities as well as Improving business

on new platform. It enhances the operational activities as well as performance of entity in large

scale. In the present report there has been discussion based on expanding the McDonald’s

business in Coventry High Street. Along, with this there will be discussion based on various

financial requirements and changes in operations which can be needful in forecasting cash

requirements.

Overview

McDonald’s has been known as world’s largest food chain restaurant which serves in

many countries or locations. The satisfaction it brings to consumers are based on convenience in

cost as well as quality. The large varieties of burgers as well as various fast food dishes has been

presented by McDonald’s with considering proper quality of products (Chen and et.al., 2018). In

approach with same firm plans to make expansion of its operations which comprises of various

processes such as serving varieties of burgers, beverages and various fast food dishes.

Managerial professionals have been thought about making expansion of operations which

will be helpful in leading firm on right direction. They have selected Coventry High street as a

new location which has been analysed as the most convenient and profitable area for

McDonald’s to have successful business (Easton and Monahan, 2016). The motive of industry is

for serving students, workers and local citizens in location with good food quality as well as with

lower prices.

Vision and Mission

In terms of analysing objectives and motive of business on which it can be said that there will

be need of having adequate operational increments as well as development of brand image in the

market (Ruginski and et.al., 2016). Considering the most convenient prices which will be

charged by McDonald’s on its food and beverages with the motive of having higher sales in each

period. Therefore, expansion of operations will lead firm in widening operational area as well as

generating adequate revenue through activities. There has been various objective which have

been undertaken by the professionals such as:

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Developing good consumer’s relationship which will be beneficial in retaining them as

well as rising the level of sales in each year.

Increasing profitability of firm that will be adequate and helpful as per meeting the goals

as well as retaining earning for better financial strength.

Satisfying the large number of buyers with convenient costs, prices and location of

operations.

FINANCIAL PLAN

As per making qualitative development and rise in the operational level in business there

will be need of making effective operational efficiency and gains (Xu and Tang, 2015). It

comprises execution of all the transactional activities as well as management of funds in the

right direction that will be helpful in managing issues and various activities of McDonald’s.

Thus, as per analysing the feasibility and capabilities of firm in meeting the debts on the right

time there will be estimation of various financials in upcoming 3 years. However, with respect to

analyse strength of firm there will be determination of break even analysis, balance sheet,

income statement, cash flow statement and financial analysis.

Breakeven Analysis

It is the main difference between demand incurred in a market from a particular brand or

product as well as efficiency of business in supplying such products. Thus, Goods which are

aimed by McDonald’s in relation with selling in market, weekly, monthly and annually has been

analysed (Zeff, 2016). However, this estimation has been based on determining the selling price

per unit, variable as well as fixed costs. The estimation of data set can be analysed for the period

2018, 2019 and 2020.

Break-Even analysis (Burgers)

Particulars Formula 2018 (In £)

2019

(In £)

2020

(In £)

Selling price per unit 10.5 10.5 10.5

Variable cost per unit 0.3 0.2 0.1

Contribution per unit

Selling price per unit -

variable cost per unit 10.2 10.3 10.4

2

well as rising the level of sales in each year.

Increasing profitability of firm that will be adequate and helpful as per meeting the goals

as well as retaining earning for better financial strength.

Satisfying the large number of buyers with convenient costs, prices and location of

operations.

FINANCIAL PLAN

As per making qualitative development and rise in the operational level in business there

will be need of making effective operational efficiency and gains (Xu and Tang, 2015). It

comprises execution of all the transactional activities as well as management of funds in the

right direction that will be helpful in managing issues and various activities of McDonald’s.

Thus, as per analysing the feasibility and capabilities of firm in meeting the debts on the right

time there will be estimation of various financials in upcoming 3 years. However, with respect to

analyse strength of firm there will be determination of break even analysis, balance sheet,

income statement, cash flow statement and financial analysis.

Breakeven Analysis

It is the main difference between demand incurred in a market from a particular brand or

product as well as efficiency of business in supplying such products. Thus, Goods which are

aimed by McDonald’s in relation with selling in market, weekly, monthly and annually has been

analysed (Zeff, 2016). However, this estimation has been based on determining the selling price

per unit, variable as well as fixed costs. The estimation of data set can be analysed for the period

2018, 2019 and 2020.

Break-Even analysis (Burgers)

Particulars Formula 2018 (In £)

2019

(In £)

2020

(In £)

Selling price per unit 10.5 10.5 10.5

Variable cost per unit 0.3 0.2 0.1

Contribution per unit

Selling price per unit -

variable cost per unit 10.2 10.3 10.4

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

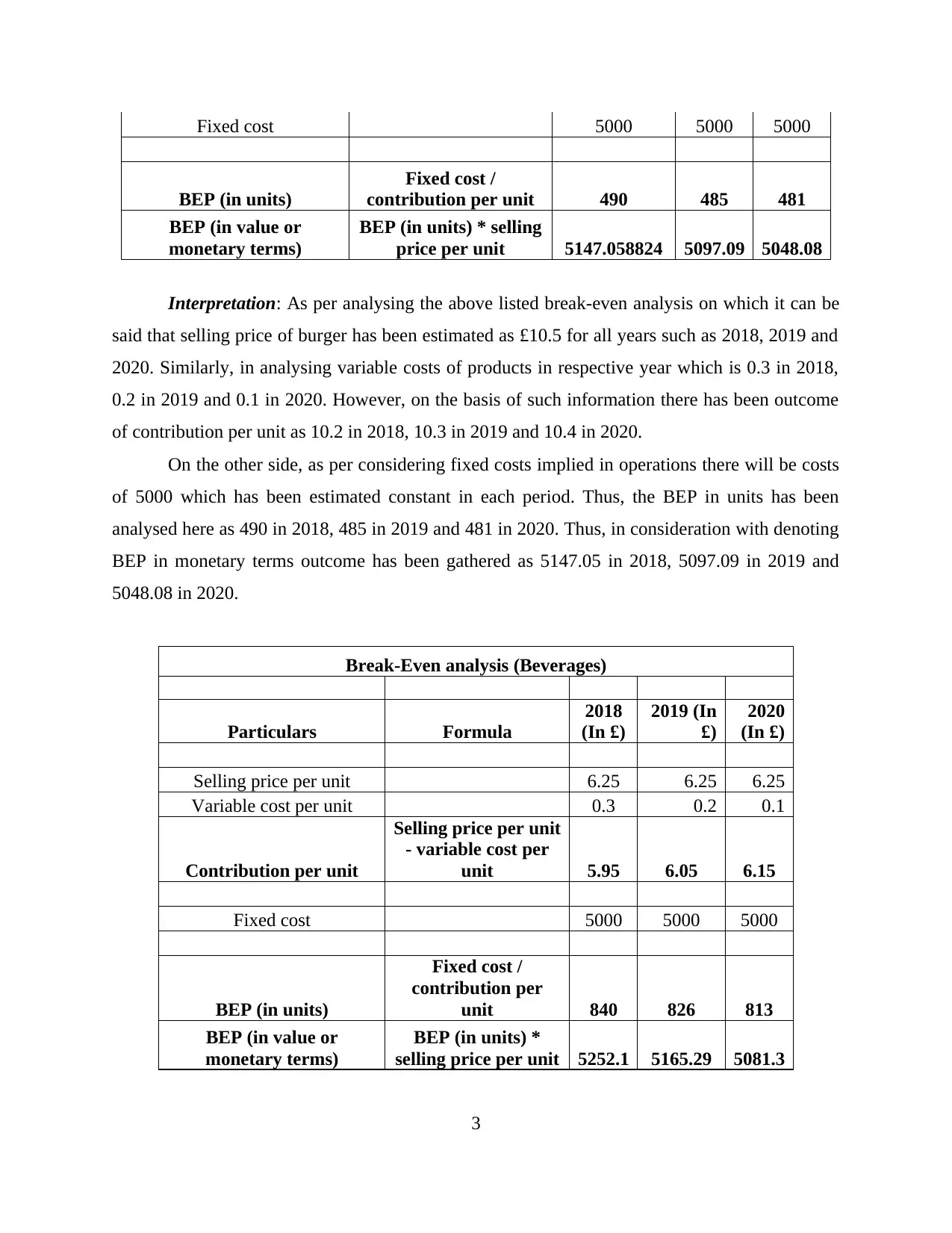

Fixed cost 5000 5000 5000

BEP (in units)

Fixed cost /

contribution per unit 490 485 481

BEP (in value or

monetary terms)

BEP (in units) * selling

price per unit 5147.058824 5097.09 5048.08

Interpretation: As per analysing the above listed break-even analysis on which it can be

said that selling price of burger has been estimated as £10.5 for all years such as 2018, 2019 and

2020. Similarly, in analysing variable costs of products in respective year which is 0.3 in 2018,

0.2 in 2019 and 0.1 in 2020. However, on the basis of such information there has been outcome

of contribution per unit as 10.2 in 2018, 10.3 in 2019 and 10.4 in 2020.

On the other side, as per considering fixed costs implied in operations there will be costs

of 5000 which has been estimated constant in each period. Thus, the BEP in units has been

analysed here as 490 in 2018, 485 in 2019 and 481 in 2020. Thus, in consideration with denoting

BEP in monetary terms outcome has been gathered as 5147.05 in 2018, 5097.09 in 2019 and

5048.08 in 2020.

Break-Even analysis (Beverages)

Particulars Formula

2018

(In £)

2019 (In

£)

2020

(In £)

Selling price per unit 6.25 6.25 6.25

Variable cost per unit 0.3 0.2 0.1

Contribution per unit

Selling price per unit

- variable cost per

unit 5.95 6.05 6.15

Fixed cost 5000 5000 5000

BEP (in units)

Fixed cost /

contribution per

unit 840 826 813

BEP (in value or

monetary terms)

BEP (in units) *

selling price per unit 5252.1 5165.29 5081.3

3

BEP (in units)

Fixed cost /

contribution per unit 490 485 481

BEP (in value or

monetary terms)

BEP (in units) * selling

price per unit 5147.058824 5097.09 5048.08

Interpretation: As per analysing the above listed break-even analysis on which it can be

said that selling price of burger has been estimated as £10.5 for all years such as 2018, 2019 and

2020. Similarly, in analysing variable costs of products in respective year which is 0.3 in 2018,

0.2 in 2019 and 0.1 in 2020. However, on the basis of such information there has been outcome

of contribution per unit as 10.2 in 2018, 10.3 in 2019 and 10.4 in 2020.

On the other side, as per considering fixed costs implied in operations there will be costs

of 5000 which has been estimated constant in each period. Thus, the BEP in units has been

analysed here as 490 in 2018, 485 in 2019 and 481 in 2020. Thus, in consideration with denoting

BEP in monetary terms outcome has been gathered as 5147.05 in 2018, 5097.09 in 2019 and

5048.08 in 2020.

Break-Even analysis (Beverages)

Particulars Formula

2018

(In £)

2019 (In

£)

2020

(In £)

Selling price per unit 6.25 6.25 6.25

Variable cost per unit 0.3 0.2 0.1

Contribution per unit

Selling price per unit

- variable cost per

unit 5.95 6.05 6.15

Fixed cost 5000 5000 5000

BEP (in units)

Fixed cost /

contribution per

unit 840 826 813

BEP (in value or

monetary terms)

BEP (in units) *

selling price per unit 5252.1 5165.29 5081.3

3

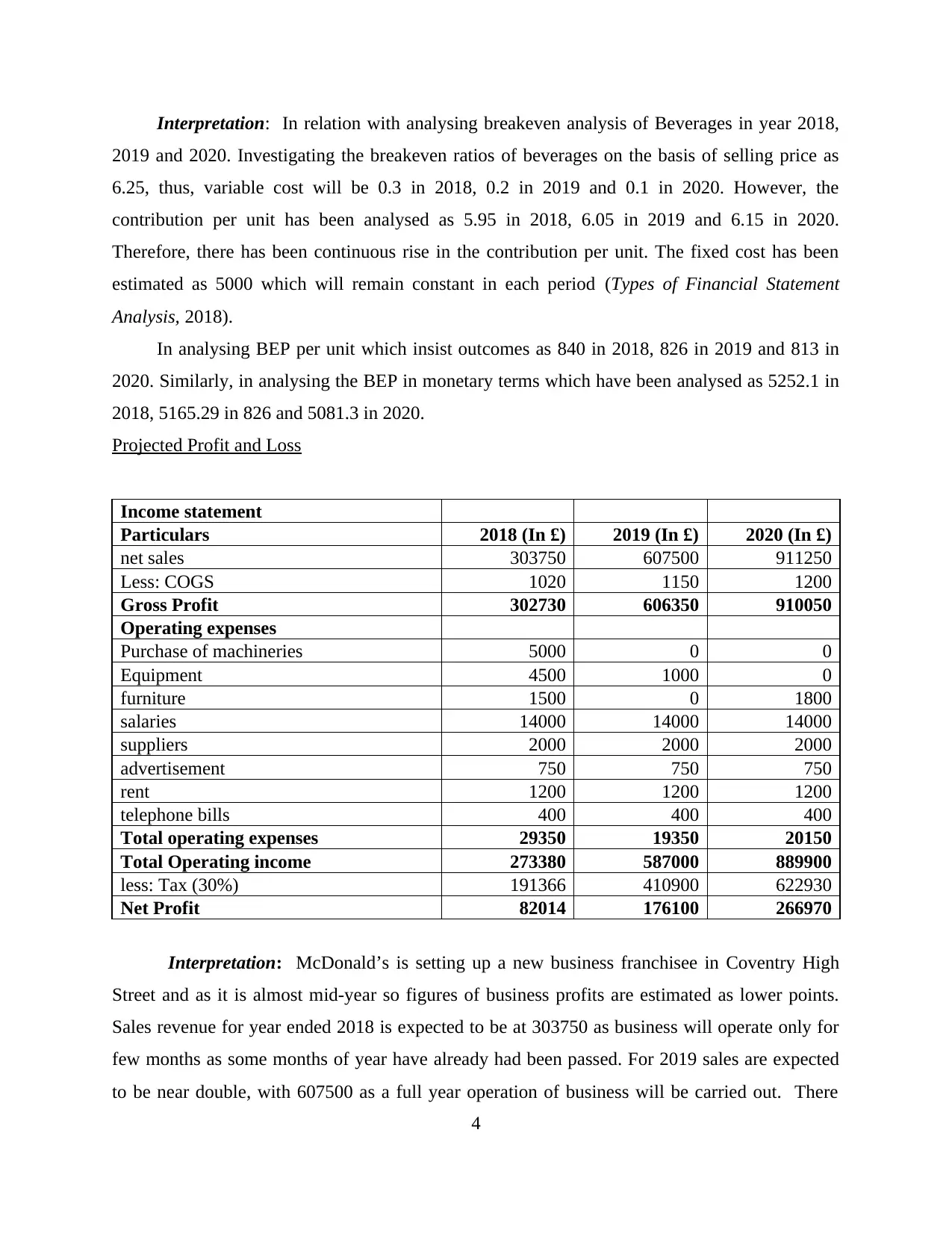

Interpretation: In relation with analysing breakeven analysis of Beverages in year 2018,

2019 and 2020. Investigating the breakeven ratios of beverages on the basis of selling price as

6.25, thus, variable cost will be 0.3 in 2018, 0.2 in 2019 and 0.1 in 2020. However, the

contribution per unit has been analysed as 5.95 in 2018, 6.05 in 2019 and 6.15 in 2020.

Therefore, there has been continuous rise in the contribution per unit. The fixed cost has been

estimated as 5000 which will remain constant in each period (Types of Financial Statement

Analysis, 2018).

In analysing BEP per unit which insist outcomes as 840 in 2018, 826 in 2019 and 813 in

2020. Similarly, in analysing the BEP in monetary terms which have been analysed as 5252.1 in

2018, 5165.29 in 826 and 5081.3 in 2020.

Projected Profit and Loss

Income statement

Particulars 2018 (In £) 2019 (In £) 2020 (In £)

net sales 303750 607500 911250

Less: COGS 1020 1150 1200

Gross Profit 302730 606350 910050

Operating expenses

Purchase of machineries 5000 0 0

Equipment 4500 1000 0

furniture 1500 0 1800

salaries 14000 14000 14000

suppliers 2000 2000 2000

advertisement 750 750 750

rent 1200 1200 1200

telephone bills 400 400 400

Total operating expenses 29350 19350 20150

Total Operating income 273380 587000 889900

less: Tax (30%) 191366 410900 622930

Net Profit 82014 176100 266970

Interpretation: McDonald’s is setting up a new business franchisee in Coventry High

Street and as it is almost mid-year so figures of business profits are estimated as lower points.

Sales revenue for year ended 2018 is expected to be at 303750 as business will operate only for

few months as some months of year have already had been passed. For 2019 sales are expected

to be near double, with 607500 as a full year operation of business will be carried out. There

4

2019 and 2020. Investigating the breakeven ratios of beverages on the basis of selling price as

6.25, thus, variable cost will be 0.3 in 2018, 0.2 in 2019 and 0.1 in 2020. However, the

contribution per unit has been analysed as 5.95 in 2018, 6.05 in 2019 and 6.15 in 2020.

Therefore, there has been continuous rise in the contribution per unit. The fixed cost has been

estimated as 5000 which will remain constant in each period (Types of Financial Statement

Analysis, 2018).

In analysing BEP per unit which insist outcomes as 840 in 2018, 826 in 2019 and 813 in

2020. Similarly, in analysing the BEP in monetary terms which have been analysed as 5252.1 in

2018, 5165.29 in 826 and 5081.3 in 2020.

Projected Profit and Loss

Income statement

Particulars 2018 (In £) 2019 (In £) 2020 (In £)

net sales 303750 607500 911250

Less: COGS 1020 1150 1200

Gross Profit 302730 606350 910050

Operating expenses

Purchase of machineries 5000 0 0

Equipment 4500 1000 0

furniture 1500 0 1800

salaries 14000 14000 14000

suppliers 2000 2000 2000

advertisement 750 750 750

rent 1200 1200 1200

telephone bills 400 400 400

Total operating expenses 29350 19350 20150

Total Operating income 273380 587000 889900

less: Tax (30%) 191366 410900 622930

Net Profit 82014 176100 266970

Interpretation: McDonald’s is setting up a new business franchisee in Coventry High

Street and as it is almost mid-year so figures of business profits are estimated as lower points.

Sales revenue for year ended 2018 is expected to be at 303750 as business will operate only for

few months as some months of year have already had been passed. For 2019 sales are expected

to be near double, with 607500 as a full year operation of business will be carried out. There

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

will be an increase in cost of goods sold but continuous efforts and measurements will be taken

to have a control over administrative and operational cost so percentage increase in this cost is

lesser than percentage increase in sales revenue (Barron, Byard and Yu, 2017). For year end

2020 sales will rise with higher pace and are expected to reach at 911250. in this year there will

be no purchase of machinery, equipment or furniture. This will reduce the operating expenses of

business, hence an increment in net profits are estimated at a better rate.

For the year end 2018 earnings of business is expecting to earn net profits of 82014 with total

expense of 221736, and in this initial revenue expenses are estimated for purchase of machinery,

equipment and furniture. For 2019 profits are estimated to rise to 176100, as full year sales of

foods and beverages will be made so revenue will be collected for whole year, with sales

revenue, expenses related to investment for store will also reduce, as only a machinery of 1000 is

purchased in this year, so a good net profit margin is expected to earn in 2019.

With an increase in sales revenue the tax will also increase, which will increase their

operating expense so to compensate this a significant control over operating cost will be maintain

profitability of business at higher percentage.

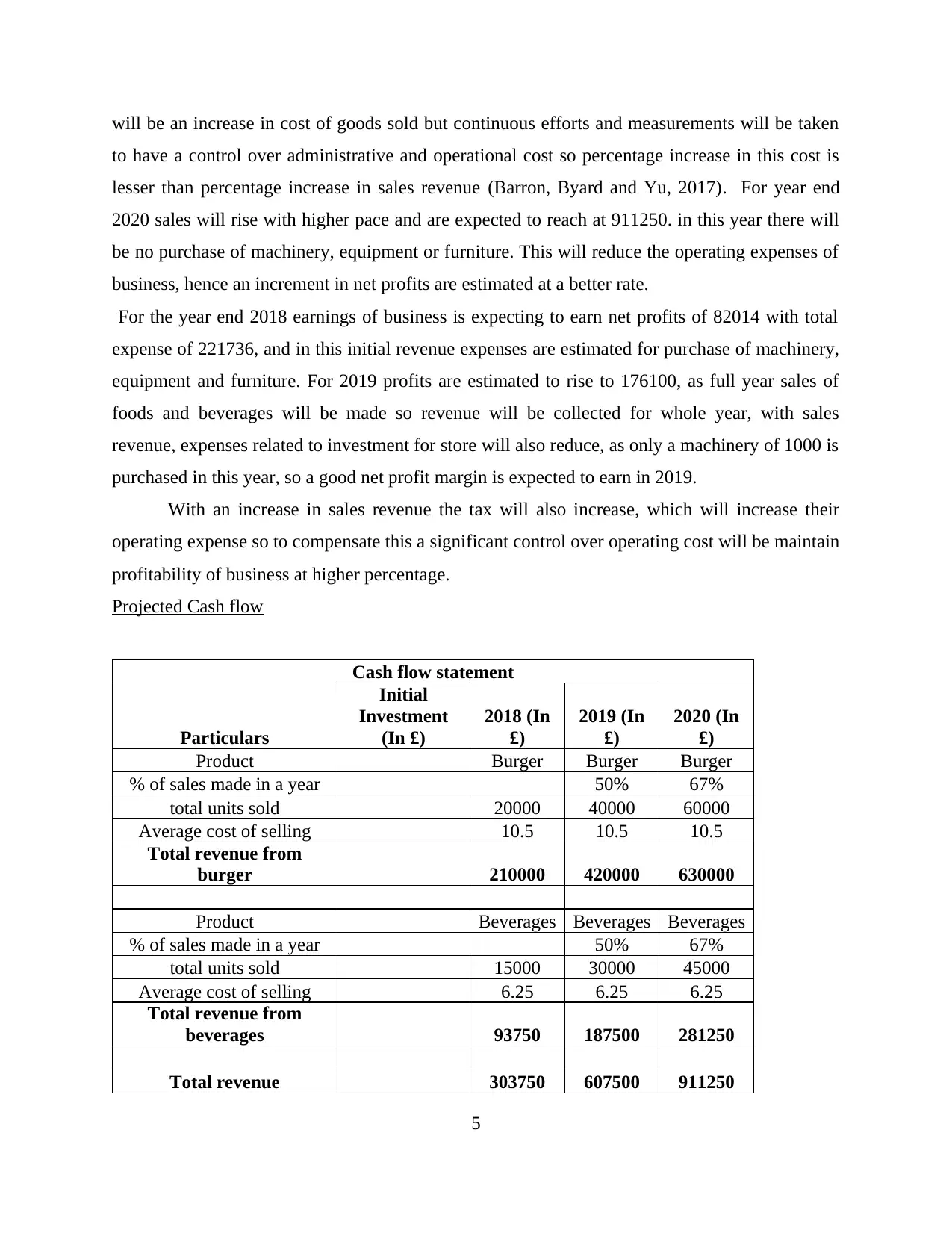

Projected Cash flow

Cash flow statement

Particulars

Initial

Investment

(In £)

2018 (In

£)

2019 (In

£)

2020 (In

£)

Product Burger Burger Burger

% of sales made in a year 50% 67%

total units sold 20000 40000 60000

Average cost of selling 10.5 10.5 10.5

Total revenue from

burger 210000 420000 630000

Product Beverages Beverages Beverages

% of sales made in a year 50% 67%

total units sold 15000 30000 45000

Average cost of selling 6.25 6.25 6.25

Total revenue from

beverages 93750 187500 281250

Total revenue 303750 607500 911250

5

to have a control over administrative and operational cost so percentage increase in this cost is

lesser than percentage increase in sales revenue (Barron, Byard and Yu, 2017). For year end

2020 sales will rise with higher pace and are expected to reach at 911250. in this year there will

be no purchase of machinery, equipment or furniture. This will reduce the operating expenses of

business, hence an increment in net profits are estimated at a better rate.

For the year end 2018 earnings of business is expecting to earn net profits of 82014 with total

expense of 221736, and in this initial revenue expenses are estimated for purchase of machinery,

equipment and furniture. For 2019 profits are estimated to rise to 176100, as full year sales of

foods and beverages will be made so revenue will be collected for whole year, with sales

revenue, expenses related to investment for store will also reduce, as only a machinery of 1000 is

purchased in this year, so a good net profit margin is expected to earn in 2019.

With an increase in sales revenue the tax will also increase, which will increase their

operating expense so to compensate this a significant control over operating cost will be maintain

profitability of business at higher percentage.

Projected Cash flow

Cash flow statement

Particulars

Initial

Investment

(In £)

2018 (In

£)

2019 (In

£)

2020 (In

£)

Product Burger Burger Burger

% of sales made in a year 50% 67%

total units sold 20000 40000 60000

Average cost of selling 10.5 10.5 10.5

Total revenue from

burger 210000 420000 630000

Product Beverages Beverages Beverages

% of sales made in a year 50% 67%

total units sold 15000 30000 45000

Average cost of selling 6.25 6.25 6.25

Total revenue from

beverages 93750 187500 281250

Total revenue 303750 607500 911250

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

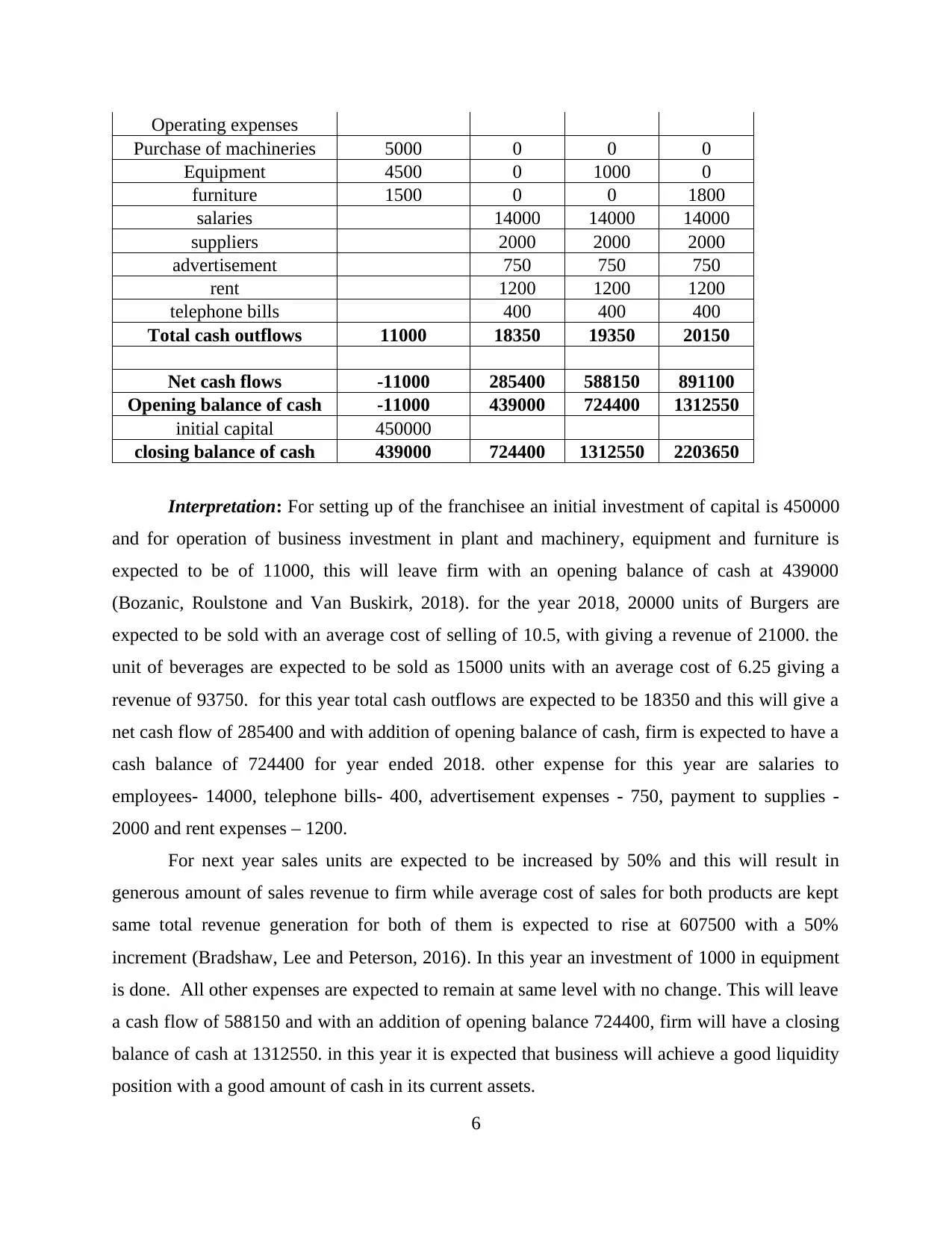

Operating expenses

Purchase of machineries 5000 0 0 0

Equipment 4500 0 1000 0

furniture 1500 0 0 1800

salaries 14000 14000 14000

suppliers 2000 2000 2000

advertisement 750 750 750

rent 1200 1200 1200

telephone bills 400 400 400

Total cash outflows 11000 18350 19350 20150

Net cash flows -11000 285400 588150 891100

Opening balance of cash -11000 439000 724400 1312550

initial capital 450000

closing balance of cash 439000 724400 1312550 2203650

Interpretation: For setting up of the franchisee an initial investment of capital is 450000

and for operation of business investment in plant and machinery, equipment and furniture is

expected to be of 11000, this will leave firm with an opening balance of cash at 439000

(Bozanic, Roulstone and Van Buskirk, 2018). for the year 2018, 20000 units of Burgers are

expected to be sold with an average cost of selling of 10.5, with giving a revenue of 21000. the

unit of beverages are expected to be sold as 15000 units with an average cost of 6.25 giving a

revenue of 93750. for this year total cash outflows are expected to be 18350 and this will give a

net cash flow of 285400 and with addition of opening balance of cash, firm is expected to have a

cash balance of 724400 for year ended 2018. other expense for this year are salaries to

employees- 14000, telephone bills- 400, advertisement expenses - 750, payment to supplies -

2000 and rent expenses – 1200.

For next year sales units are expected to be increased by 50% and this will result in

generous amount of sales revenue to firm while average cost of sales for both products are kept

same total revenue generation for both of them is expected to rise at 607500 with a 50%

increment (Bradshaw, Lee and Peterson, 2016). In this year an investment of 1000 in equipment

is done. All other expenses are expected to remain at same level with no change. This will leave

a cash flow of 588150 and with an addition of opening balance 724400, firm will have a closing

balance of cash at 1312550. in this year it is expected that business will achieve a good liquidity

position with a good amount of cash in its current assets.

6

Purchase of machineries 5000 0 0 0

Equipment 4500 0 1000 0

furniture 1500 0 0 1800

salaries 14000 14000 14000

suppliers 2000 2000 2000

advertisement 750 750 750

rent 1200 1200 1200

telephone bills 400 400 400

Total cash outflows 11000 18350 19350 20150

Net cash flows -11000 285400 588150 891100

Opening balance of cash -11000 439000 724400 1312550

initial capital 450000

closing balance of cash 439000 724400 1312550 2203650

Interpretation: For setting up of the franchisee an initial investment of capital is 450000

and for operation of business investment in plant and machinery, equipment and furniture is

expected to be of 11000, this will leave firm with an opening balance of cash at 439000

(Bozanic, Roulstone and Van Buskirk, 2018). for the year 2018, 20000 units of Burgers are

expected to be sold with an average cost of selling of 10.5, with giving a revenue of 21000. the

unit of beverages are expected to be sold as 15000 units with an average cost of 6.25 giving a

revenue of 93750. for this year total cash outflows are expected to be 18350 and this will give a

net cash flow of 285400 and with addition of opening balance of cash, firm is expected to have a

cash balance of 724400 for year ended 2018. other expense for this year are salaries to

employees- 14000, telephone bills- 400, advertisement expenses - 750, payment to supplies -

2000 and rent expenses – 1200.

For next year sales units are expected to be increased by 50% and this will result in

generous amount of sales revenue to firm while average cost of sales for both products are kept

same total revenue generation for both of them is expected to rise at 607500 with a 50%

increment (Bradshaw, Lee and Peterson, 2016). In this year an investment of 1000 in equipment

is done. All other expenses are expected to remain at same level with no change. This will leave

a cash flow of 588150 and with an addition of opening balance 724400, firm will have a closing

balance of cash at 1312550. in this year it is expected that business will achieve a good liquidity

position with a good amount of cash in its current assets.

6

For year 2020, sales of both burgers and beverages are expected to rise by 67% and sales

cost are kept constant which will lead to increase in total sales revenue of business from 607500

to 911250. Furniture purchase of 1800 is forecasted for this year. Other operating expenses such

as rent, telephone bill, advertisement expanses, electricity and salary expenses are estimated to

be constant. This will give net cash flow of 891100 and with an addition of opening g balance,

for year end 2020 firm is expected to have a cash balance of 2203650.

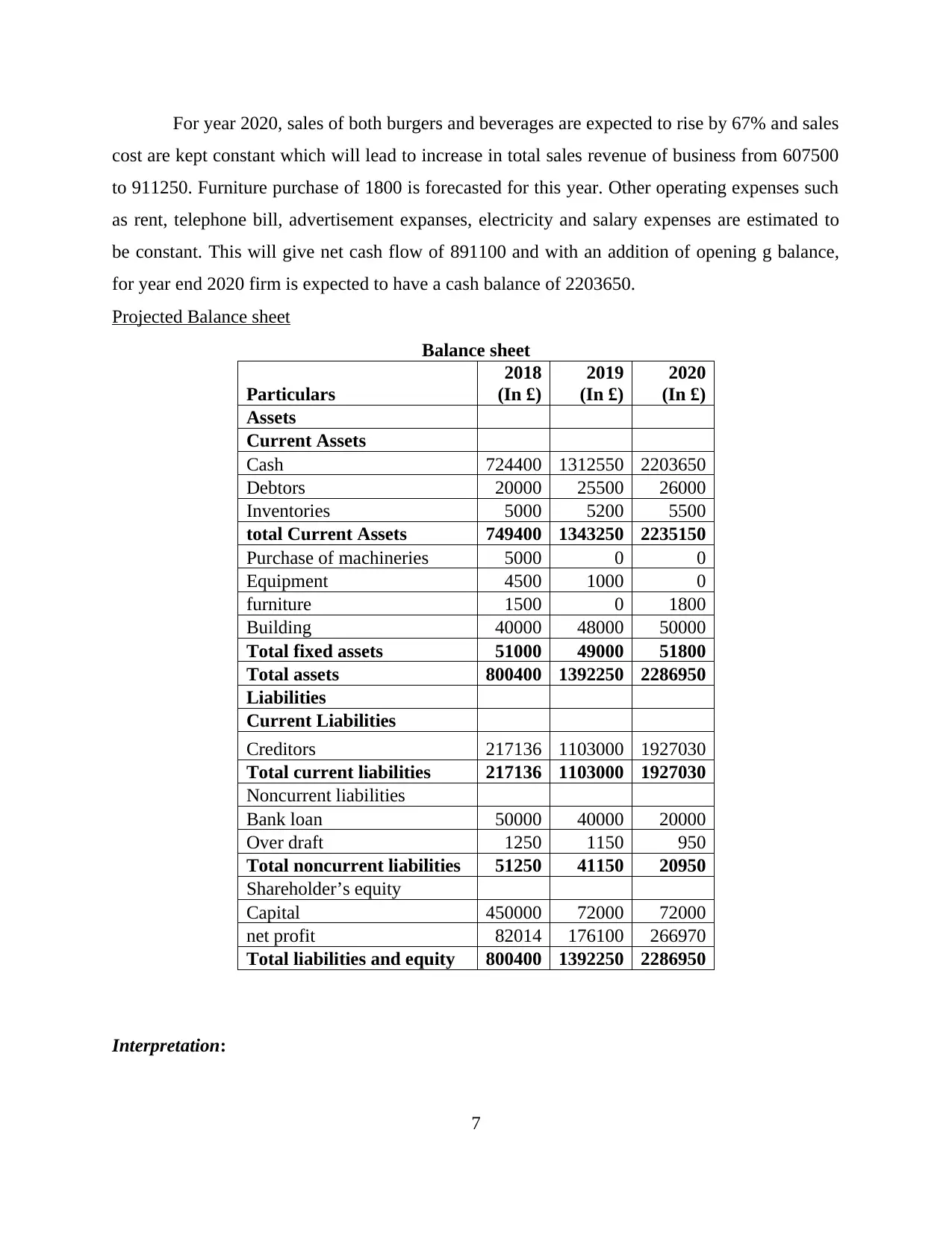

Projected Balance sheet

Balance sheet

Particulars

2018

(In £)

2019

(In £)

2020

(In £)

Assets

Current Assets

Cash 724400 1312550 2203650

Debtors 20000 25500 26000

Inventories 5000 5200 5500

total Current Assets 749400 1343250 2235150

Purchase of machineries 5000 0 0

Equipment 4500 1000 0

furniture 1500 0 1800

Building 40000 48000 50000

Total fixed assets 51000 49000 51800

Total assets 800400 1392250 2286950

Liabilities

Current Liabilities

Creditors 217136 1103000 1927030

Total current liabilities 217136 1103000 1927030

Noncurrent liabilities

Bank loan 50000 40000 20000

Over draft 1250 1150 950

Total noncurrent liabilities 51250 41150 20950

Shareholder’s equity

Capital 450000 72000 72000

net profit 82014 176100 266970

Total liabilities and equity 800400 1392250 2286950

Interpretation:

7

cost are kept constant which will lead to increase in total sales revenue of business from 607500

to 911250. Furniture purchase of 1800 is forecasted for this year. Other operating expenses such

as rent, telephone bill, advertisement expanses, electricity and salary expenses are estimated to

be constant. This will give net cash flow of 891100 and with an addition of opening g balance,

for year end 2020 firm is expected to have a cash balance of 2203650.

Projected Balance sheet

Balance sheet

Particulars

2018

(In £)

2019

(In £)

2020

(In £)

Assets

Current Assets

Cash 724400 1312550 2203650

Debtors 20000 25500 26000

Inventories 5000 5200 5500

total Current Assets 749400 1343250 2235150

Purchase of machineries 5000 0 0

Equipment 4500 1000 0

furniture 1500 0 1800

Building 40000 48000 50000

Total fixed assets 51000 49000 51800

Total assets 800400 1392250 2286950

Liabilities

Current Liabilities

Creditors 217136 1103000 1927030

Total current liabilities 217136 1103000 1927030

Noncurrent liabilities

Bank loan 50000 40000 20000

Over draft 1250 1150 950

Total noncurrent liabilities 51250 41150 20950

Shareholder’s equity

Capital 450000 72000 72000

net profit 82014 176100 266970

Total liabilities and equity 800400 1392250 2286950

Interpretation:

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

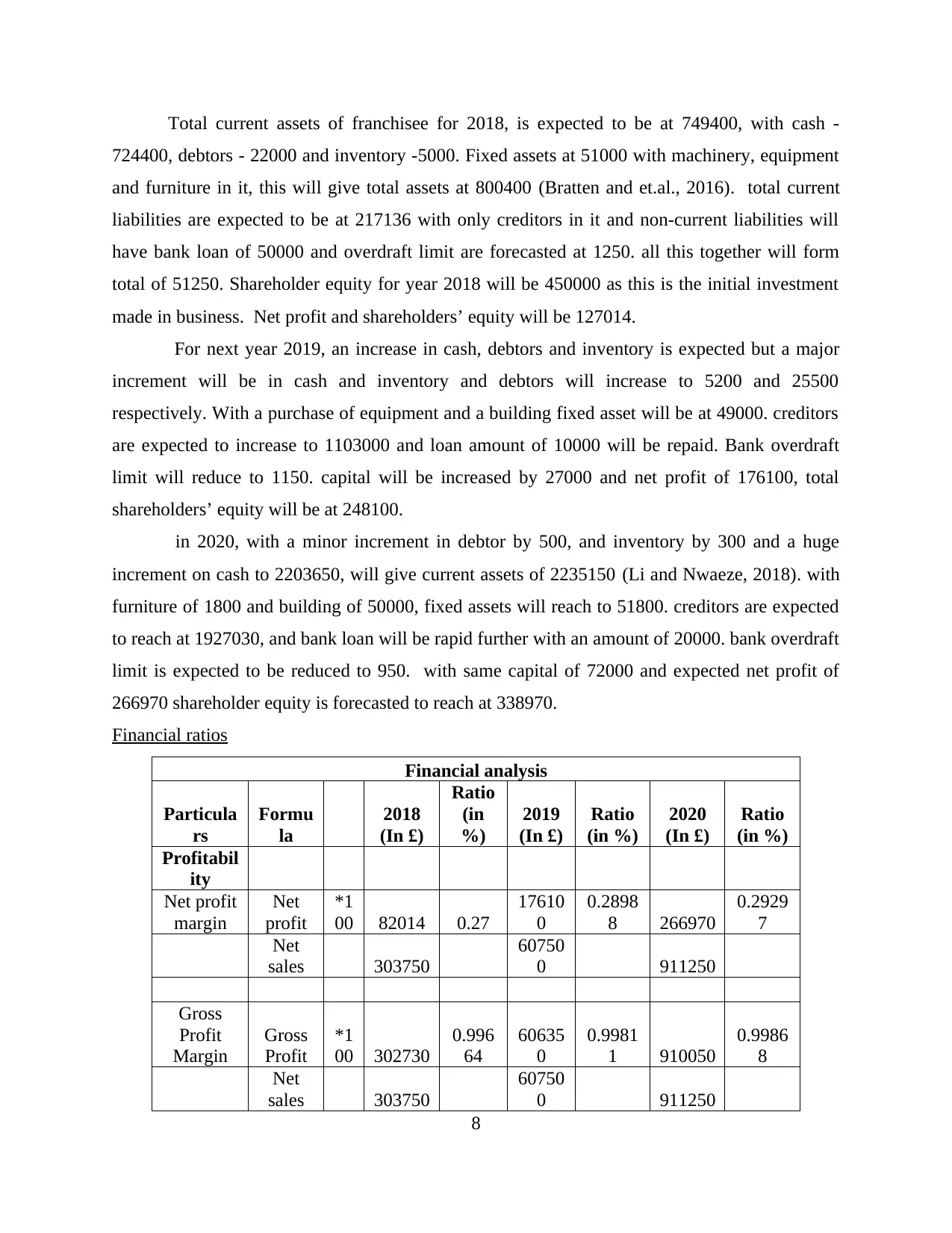

Total current assets of franchisee for 2018, is expected to be at 749400, with cash -

724400, debtors - 22000 and inventory -5000. Fixed assets at 51000 with machinery, equipment

and furniture in it, this will give total assets at 800400 (Bratten and et.al., 2016). total current

liabilities are expected to be at 217136 with only creditors in it and non-current liabilities will

have bank loan of 50000 and overdraft limit are forecasted at 1250. all this together will form

total of 51250. Shareholder equity for year 2018 will be 450000 as this is the initial investment

made in business. Net profit and shareholders’ equity will be 127014.

For next year 2019, an increase in cash, debtors and inventory is expected but a major

increment will be in cash and inventory and debtors will increase to 5200 and 25500

respectively. With a purchase of equipment and a building fixed asset will be at 49000. creditors

are expected to increase to 1103000 and loan amount of 10000 will be repaid. Bank overdraft

limit will reduce to 1150. capital will be increased by 27000 and net profit of 176100, total

shareholders’ equity will be at 248100.

in 2020, with a minor increment in debtor by 500, and inventory by 300 and a huge

increment on cash to 2203650, will give current assets of 2235150 (Li and Nwaeze, 2018). with

furniture of 1800 and building of 50000, fixed assets will reach to 51800. creditors are expected

to reach at 1927030, and bank loan will be rapid further with an amount of 20000. bank overdraft

limit is expected to be reduced to 950. with same capital of 72000 and expected net profit of

266970 shareholder equity is forecasted to reach at 338970.

Financial ratios

Financial analysis

Particula

rs

Formu

la

2018

(In £)

Ratio

(in

%)

2019

(In £)

Ratio

(in %)

2020

(In £)

Ratio

(in %)

Profitabil

ity

Net profit

margin

Net

profit

*1

00 82014 0.27

17610

0

0.2898

8 266970

0.2929

7

Net

sales 303750

60750

0 911250

Gross

Profit

Margin

Gross

Profit

*1

00 302730

0.996

64

60635

0

0.9981

1 910050

0.9986

8

Net

sales 303750

60750

0 911250

8

724400, debtors - 22000 and inventory -5000. Fixed assets at 51000 with machinery, equipment

and furniture in it, this will give total assets at 800400 (Bratten and et.al., 2016). total current

liabilities are expected to be at 217136 with only creditors in it and non-current liabilities will

have bank loan of 50000 and overdraft limit are forecasted at 1250. all this together will form

total of 51250. Shareholder equity for year 2018 will be 450000 as this is the initial investment

made in business. Net profit and shareholders’ equity will be 127014.

For next year 2019, an increase in cash, debtors and inventory is expected but a major

increment will be in cash and inventory and debtors will increase to 5200 and 25500

respectively. With a purchase of equipment and a building fixed asset will be at 49000. creditors

are expected to increase to 1103000 and loan amount of 10000 will be repaid. Bank overdraft

limit will reduce to 1150. capital will be increased by 27000 and net profit of 176100, total

shareholders’ equity will be at 248100.

in 2020, with a minor increment in debtor by 500, and inventory by 300 and a huge

increment on cash to 2203650, will give current assets of 2235150 (Li and Nwaeze, 2018). with

furniture of 1800 and building of 50000, fixed assets will reach to 51800. creditors are expected

to reach at 1927030, and bank loan will be rapid further with an amount of 20000. bank overdraft

limit is expected to be reduced to 950. with same capital of 72000 and expected net profit of

266970 shareholder equity is forecasted to reach at 338970.

Financial ratios

Financial analysis

Particula

rs

Formu

la

2018

(In £)

Ratio

(in

%)

2019

(In £)

Ratio

(in %)

2020

(In £)

Ratio

(in %)

Profitabil

ity

Net profit

margin

Net

profit

*1

00 82014 0.27

17610

0

0.2898

8 266970

0.2929

7

Net

sales 303750

60750

0 911250

Gross

Profit

Margin

Gross

Profit

*1

00 302730

0.996

64

60635

0

0.9981

1 910050

0.9986

8

Net

sales 303750

60750

0 911250

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

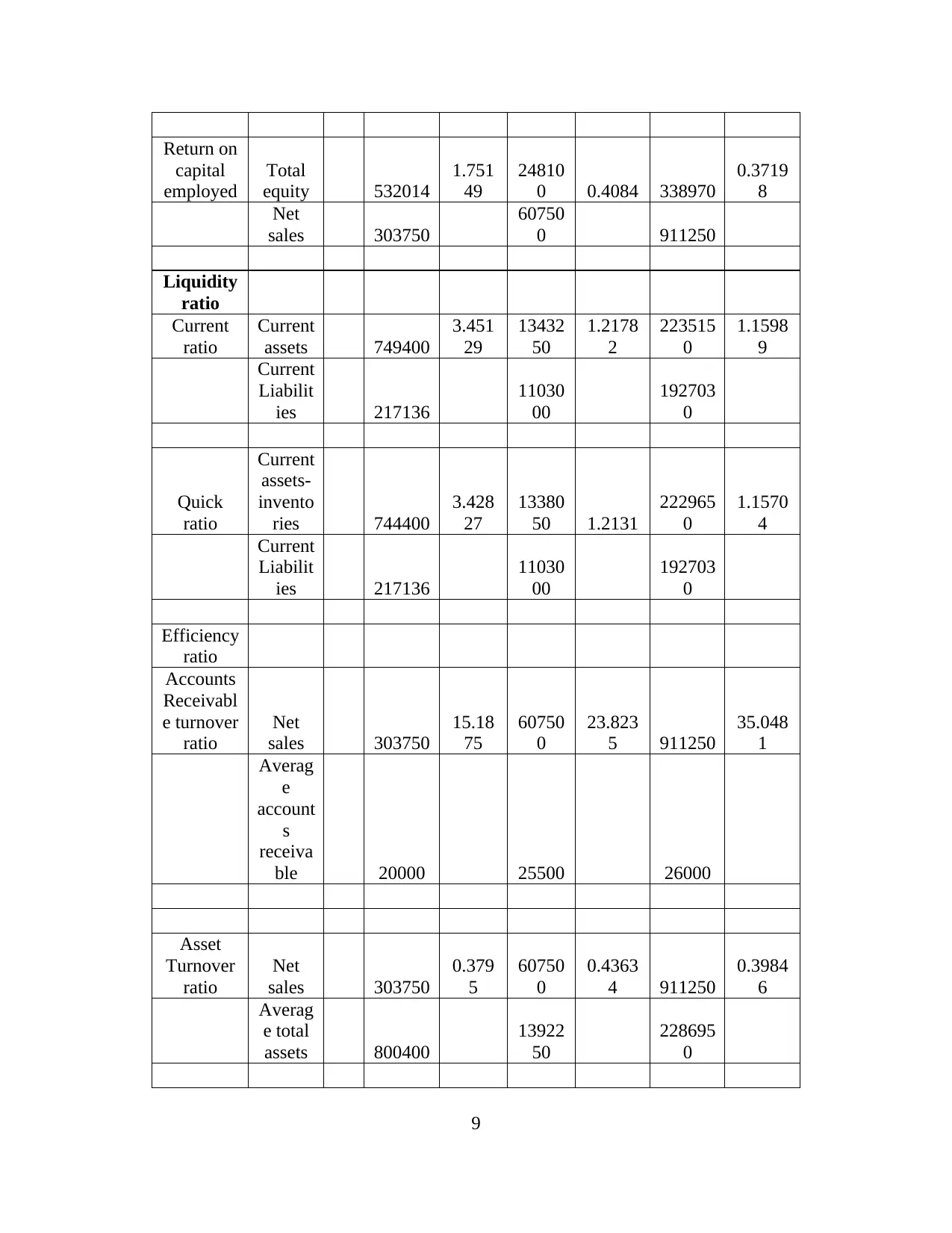

Return on

capital

employed

Total

equity 532014

1.751

49

24810

0 0.4084 338970

0.3719

8

Net

sales 303750

60750

0 911250

Liquidity

ratio

Current

ratio

Current

assets 749400

3.451

29

13432

50

1.2178

2

223515

0

1.1598

9

Current

Liabilit

ies 217136

11030

00

192703

0

Quick

ratio

Current

assets-

invento

ries 744400

3.428

27

13380

50 1.2131

222965

0

1.1570

4

Current

Liabilit

ies 217136

11030

00

192703

0

Efficiency

ratio

Accounts

Receivabl

e turnover

ratio

Net

sales 303750

15.18

75

60750

0

23.823

5 911250

35.048

1

Averag

e

account

s

receiva

ble 20000 25500 26000

Asset

Turnover

ratio

Net

sales 303750

0.379

5

60750

0

0.4363

4 911250

0.3984

6

Averag

e total

assets 800400

13922

50

228695

0

9

capital

employed

Total

equity 532014

1.751

49

24810

0 0.4084 338970

0.3719

8

Net

sales 303750

60750

0 911250

Liquidity

ratio

Current

ratio

Current

assets 749400

3.451

29

13432

50

1.2178

2

223515

0

1.1598

9

Current

Liabilit

ies 217136

11030

00

192703

0

Quick

ratio

Current

assets-

invento

ries 744400

3.428

27

13380

50 1.2131

222965

0

1.1570

4

Current

Liabilit

ies 217136

11030

00

192703

0

Efficiency

ratio

Accounts

Receivabl

e turnover

ratio

Net

sales 303750

15.18

75

60750

0

23.823

5 911250

35.048

1

Averag

e

account

s

receiva

ble 20000 25500 26000

Asset

Turnover

ratio

Net

sales 303750

0.379

5

60750

0

0.4363

4 911250

0.3984

6

Averag

e total

assets 800400

13922

50

228695

0

9

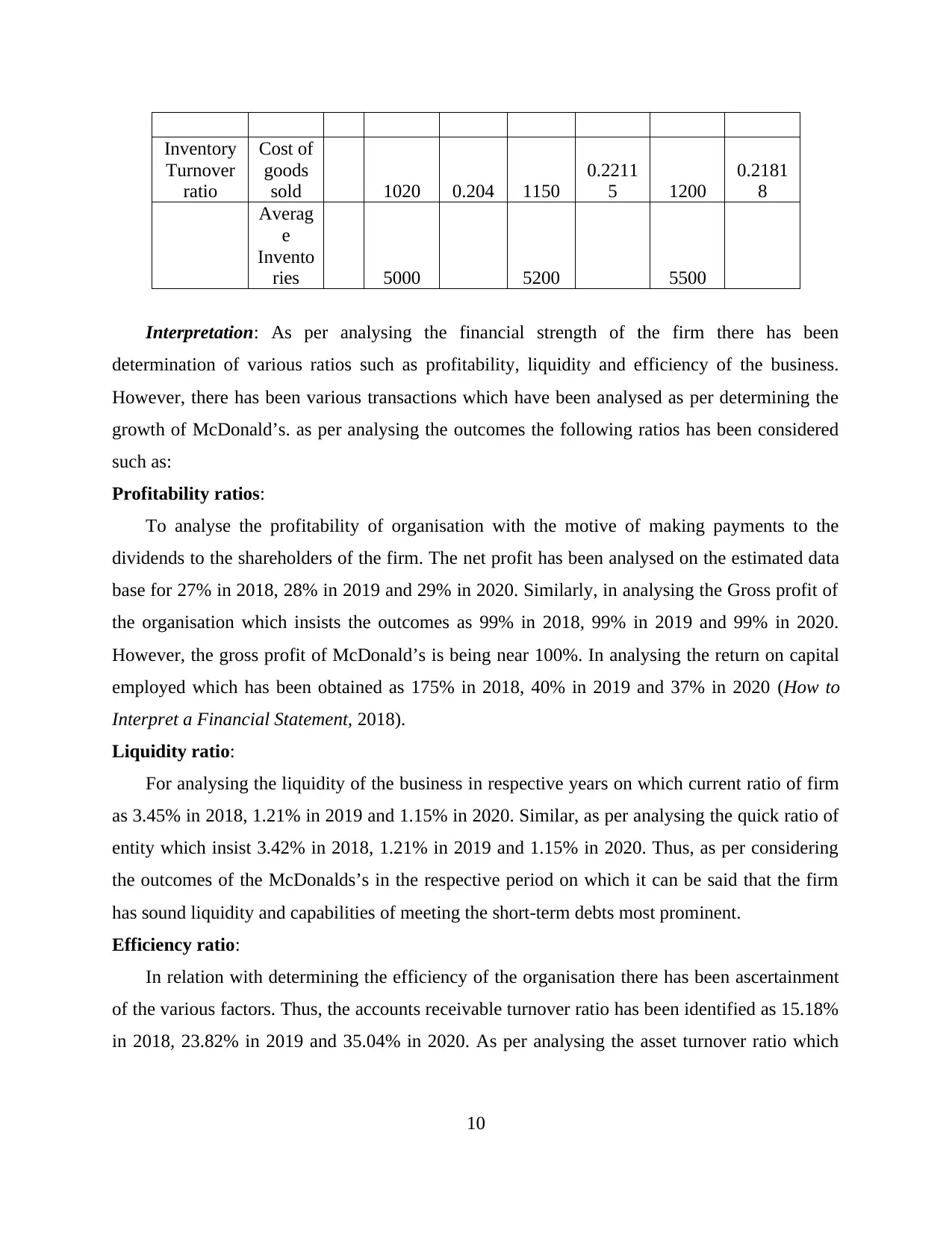

Inventory

Turnover

ratio

Cost of

goods

sold 1020 0.204 1150

0.2211

5 1200

0.2181

8

Averag

e

Invento

ries 5000 5200 5500

Interpretation: As per analysing the financial strength of the firm there has been

determination of various ratios such as profitability, liquidity and efficiency of the business.

However, there has been various transactions which have been analysed as per determining the

growth of McDonald’s. as per analysing the outcomes the following ratios has been considered

such as:

Profitability ratios:

To analyse the profitability of organisation with the motive of making payments to the

dividends to the shareholders of the firm. The net profit has been analysed on the estimated data

base for 27% in 2018, 28% in 2019 and 29% in 2020. Similarly, in analysing the Gross profit of

the organisation which insists the outcomes as 99% in 2018, 99% in 2019 and 99% in 2020.

However, the gross profit of McDonald’s is being near 100%. In analysing the return on capital

employed which has been obtained as 175% in 2018, 40% in 2019 and 37% in 2020 (How to

Interpret a Financial Statement, 2018).

Liquidity ratio:

For analysing the liquidity of the business in respective years on which current ratio of firm

as 3.45% in 2018, 1.21% in 2019 and 1.15% in 2020. Similar, as per analysing the quick ratio of

entity which insist 3.42% in 2018, 1.21% in 2019 and 1.15% in 2020. Thus, as per considering

the outcomes of the McDonalds’s in the respective period on which it can be said that the firm

has sound liquidity and capabilities of meeting the short-term debts most prominent.

Efficiency ratio:

In relation with determining the efficiency of the organisation there has been ascertainment

of the various factors. Thus, the accounts receivable turnover ratio has been identified as 15.18%

in 2018, 23.82% in 2019 and 35.04% in 2020. As per analysing the asset turnover ratio which

10

Turnover

ratio

Cost of

goods

sold 1020 0.204 1150

0.2211

5 1200

0.2181

8

Averag

e

Invento

ries 5000 5200 5500

Interpretation: As per analysing the financial strength of the firm there has been

determination of various ratios such as profitability, liquidity and efficiency of the business.

However, there has been various transactions which have been analysed as per determining the

growth of McDonald’s. as per analysing the outcomes the following ratios has been considered

such as:

Profitability ratios:

To analyse the profitability of organisation with the motive of making payments to the

dividends to the shareholders of the firm. The net profit has been analysed on the estimated data

base for 27% in 2018, 28% in 2019 and 29% in 2020. Similarly, in analysing the Gross profit of

the organisation which insists the outcomes as 99% in 2018, 99% in 2019 and 99% in 2020.

However, the gross profit of McDonald’s is being near 100%. In analysing the return on capital

employed which has been obtained as 175% in 2018, 40% in 2019 and 37% in 2020 (How to

Interpret a Financial Statement, 2018).

Liquidity ratio:

For analysing the liquidity of the business in respective years on which current ratio of firm

as 3.45% in 2018, 1.21% in 2019 and 1.15% in 2020. Similar, as per analysing the quick ratio of

entity which insist 3.42% in 2018, 1.21% in 2019 and 1.15% in 2020. Thus, as per considering

the outcomes of the McDonalds’s in the respective period on which it can be said that the firm

has sound liquidity and capabilities of meeting the short-term debts most prominent.

Efficiency ratio:

In relation with determining the efficiency of the organisation there has been ascertainment

of the various factors. Thus, the accounts receivable turnover ratio has been identified as 15.18%

in 2018, 23.82% in 2019 and 35.04% in 2020. As per analysing the asset turnover ratio which

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.