Financial Planning Fundamentals: Strategy Paper for Brendon McDougall

VerifiedAdded on 2022/11/13

|9

|1455

|117

Practical Assignment

AI Summary

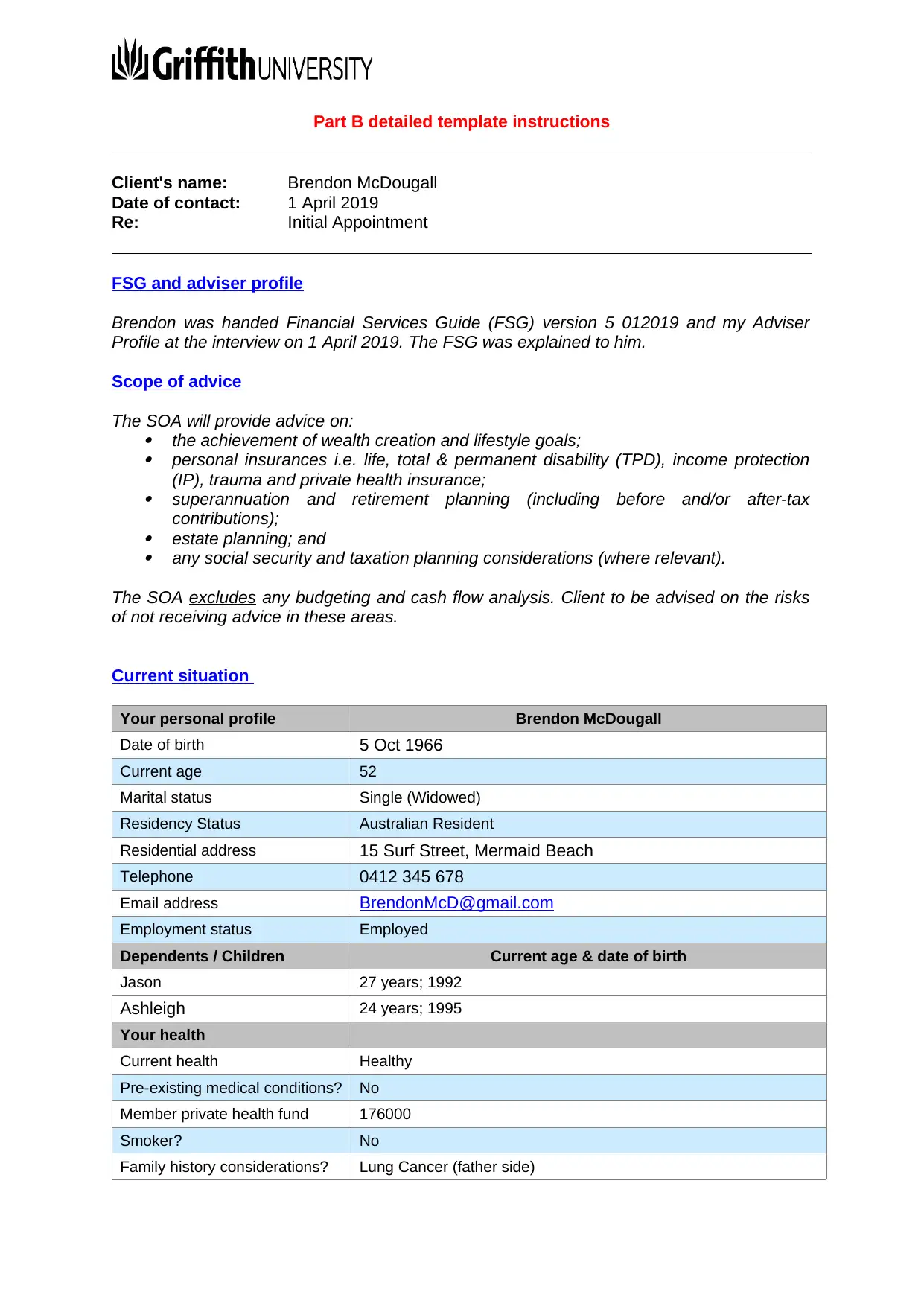

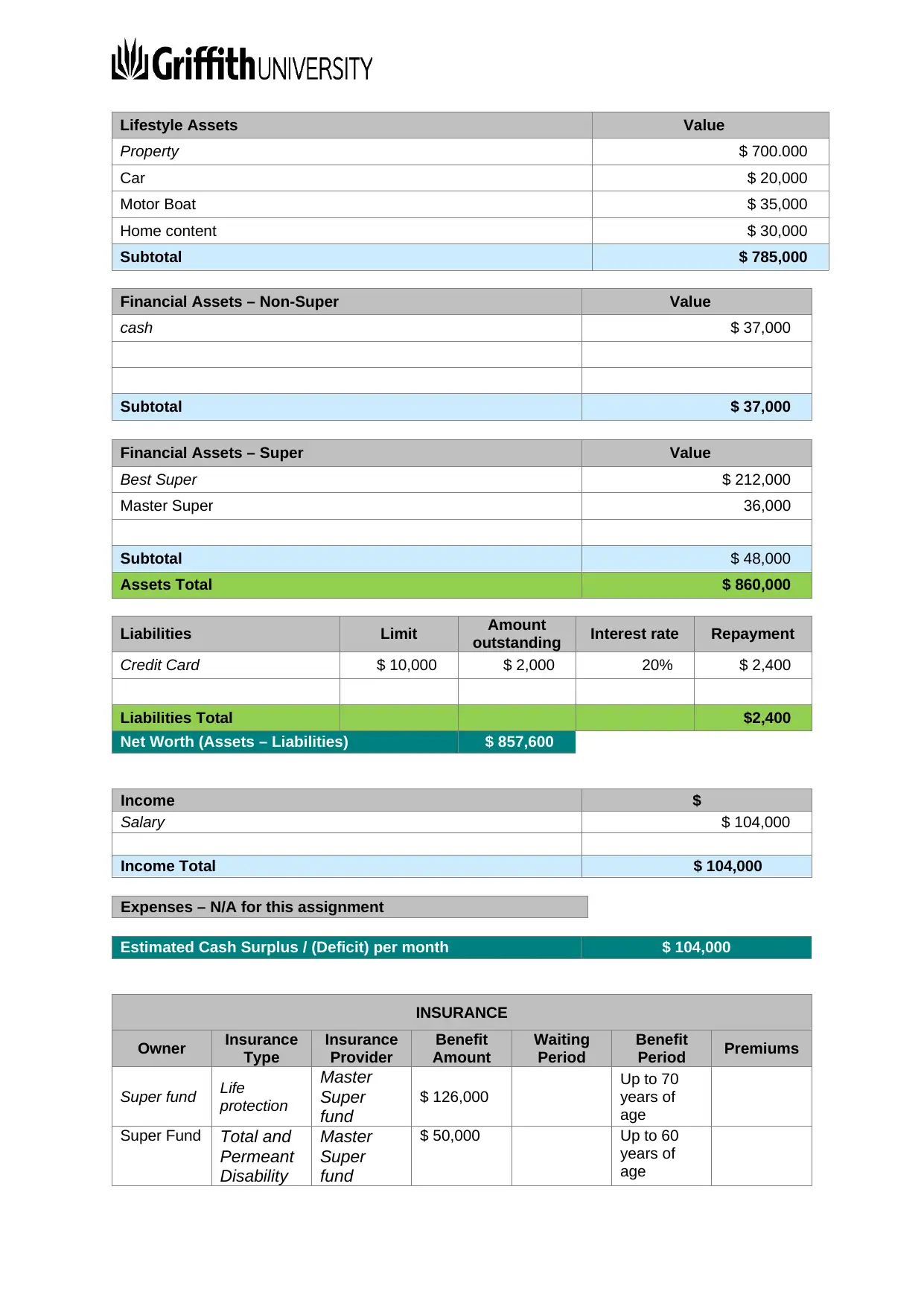

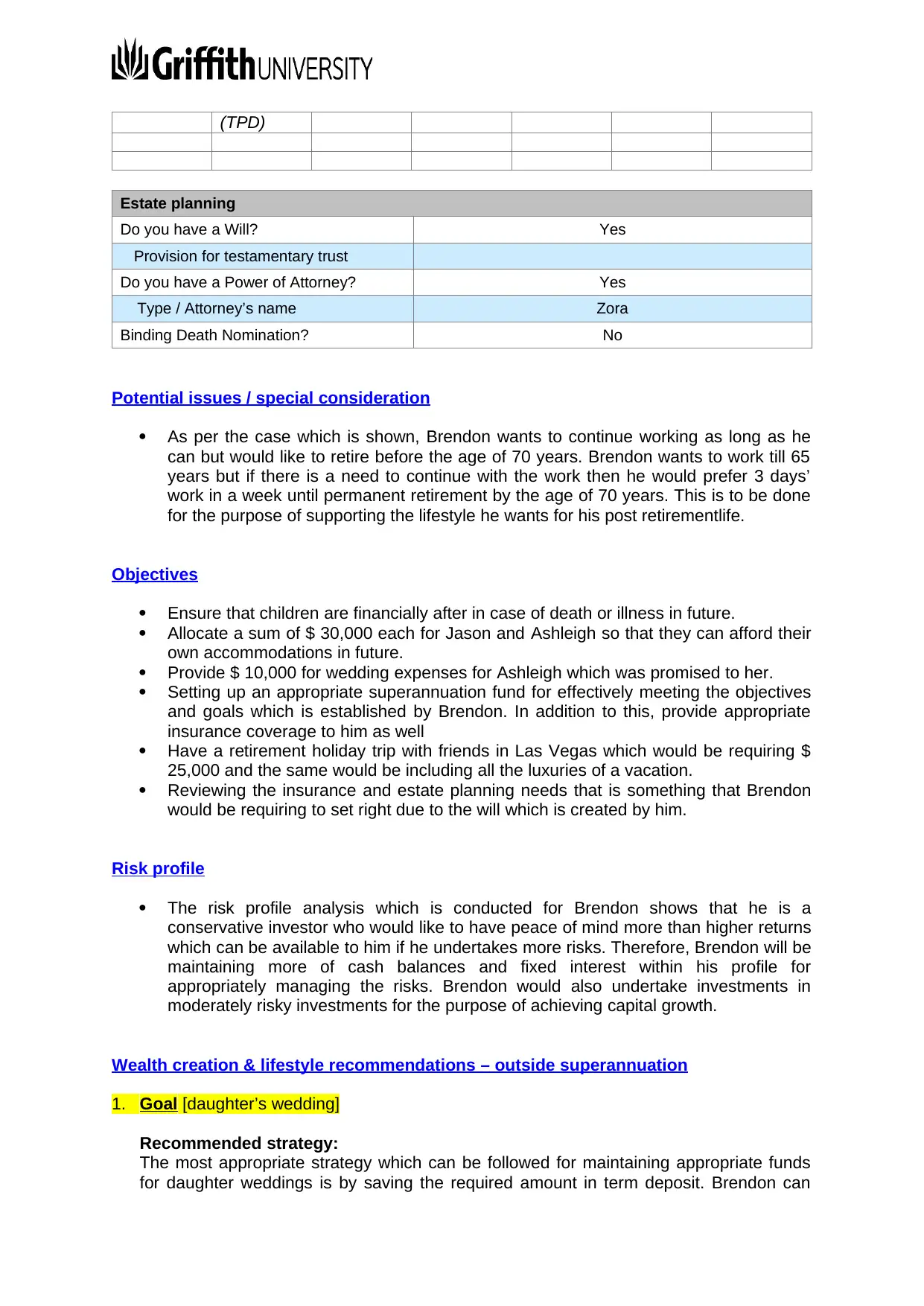

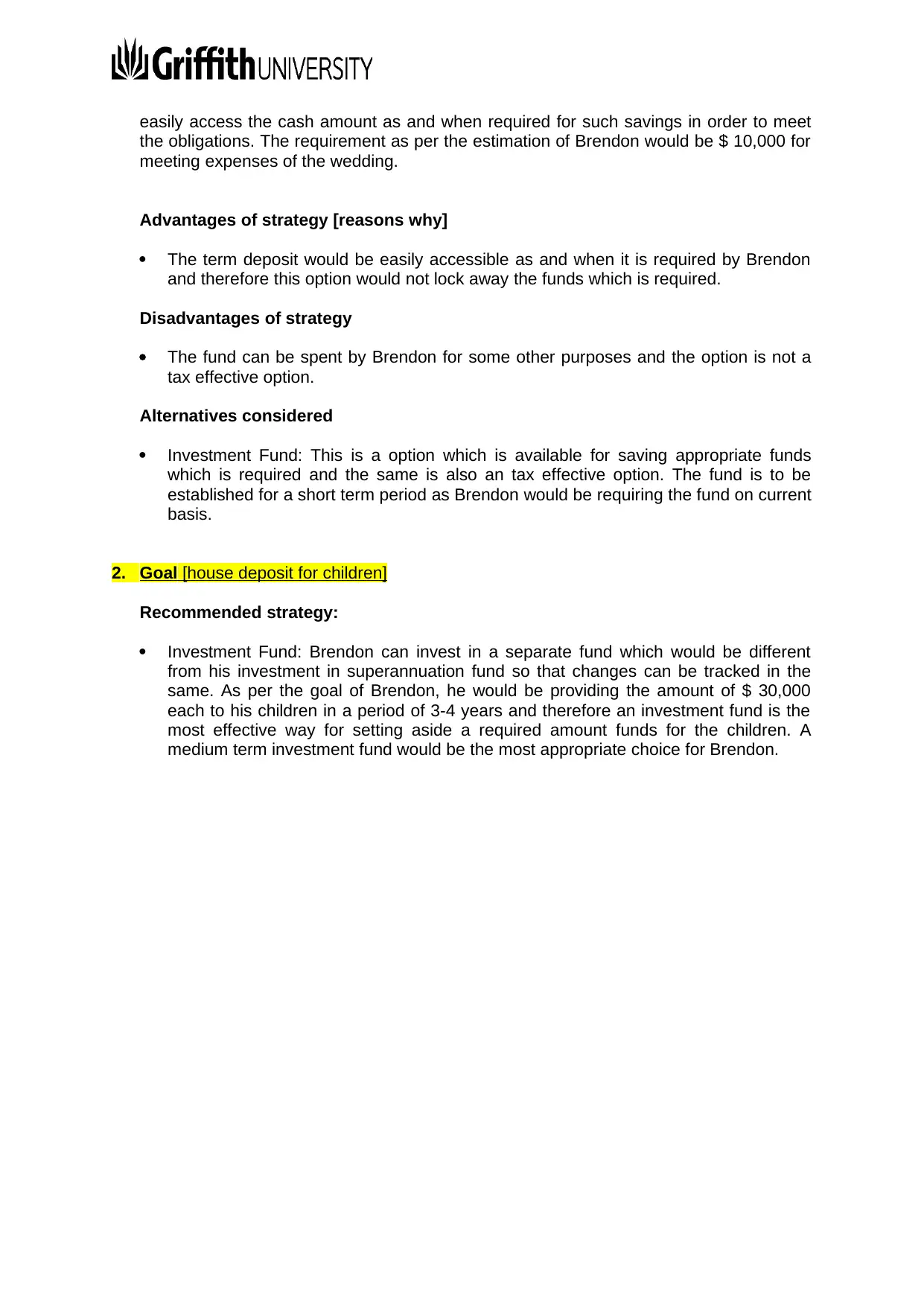

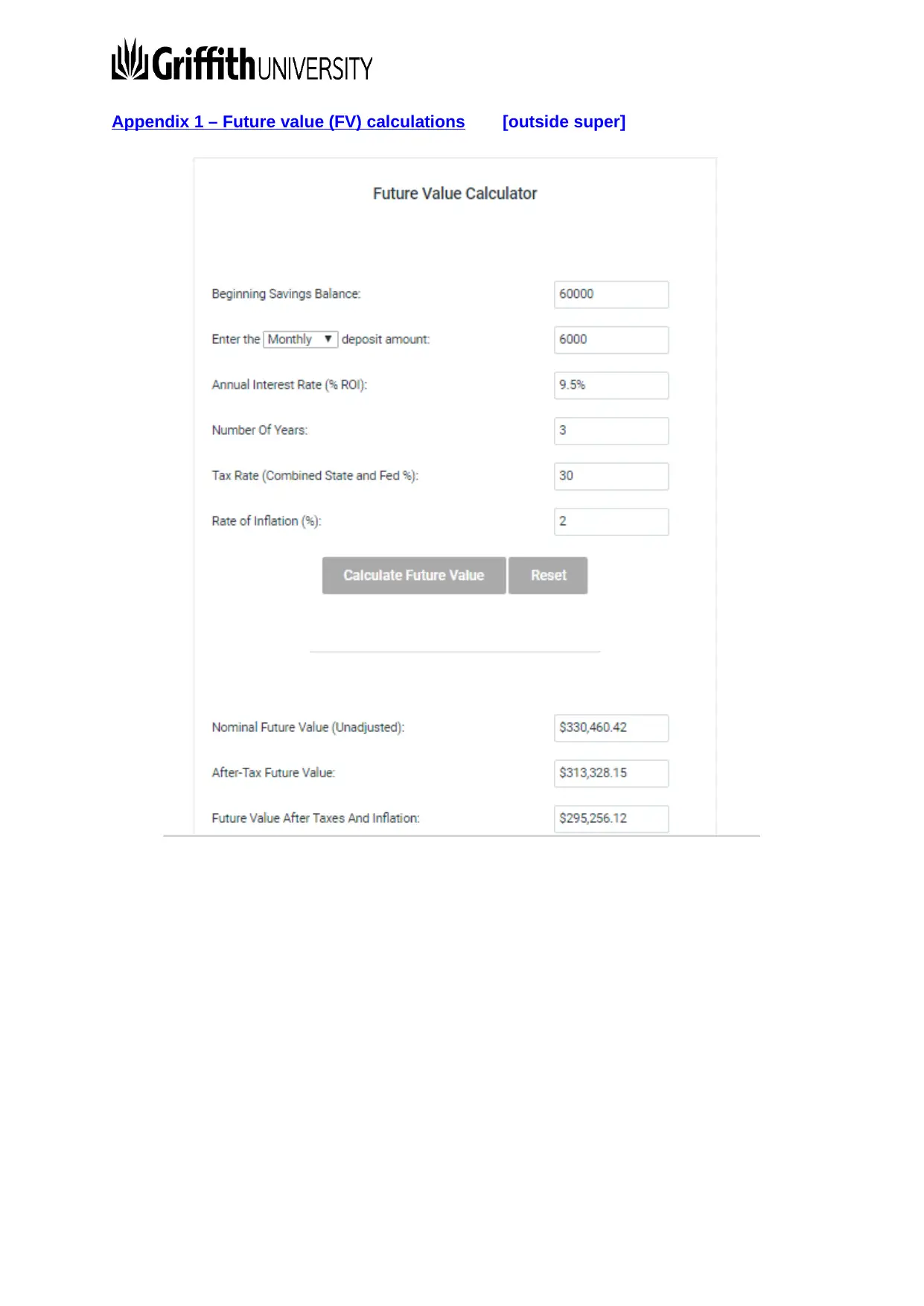

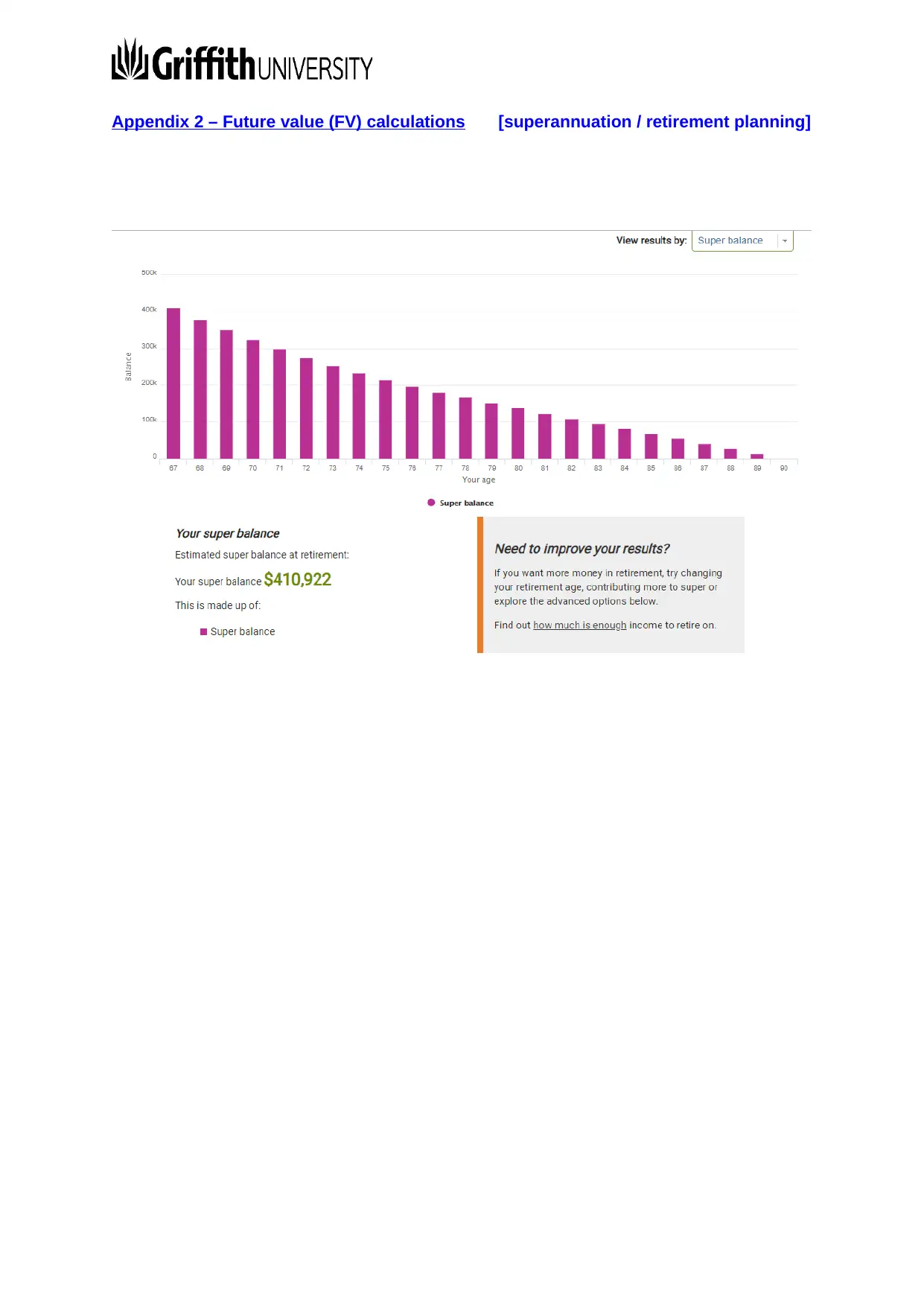

This assignment presents a detailed financial plan for Brendon McDougall, a 52-year-old single (widowed) Australian resident. The plan addresses his wealth creation and lifestyle goals, including providing for his children, funding a holiday, and ensuring a comfortable retirement. It covers various aspects such as personal insurances (life, TPD, income protection, trauma, and private health), superannuation and retirement planning, and estate planning. The analysis includes a review of his current assets, liabilities, income, and expenses, along with his risk profile as a conservative investor. The assignment offers strategic recommendations for wealth creation both inside and outside superannuation, including investment funds and share portfolios, as well as superannuation strategies. It also suggests wealth protection measures through various insurance policies and estate planning considerations, such as preparing a will. The document outlines potential issues and special considerations, such as Brendon's desire to retire before age 70, and provides future value calculations to support the recommendations. The assignment aims to create a comprehensive financial strategy tailored to Brendon's specific needs and objectives.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.