Application of McKinsey's Valuation Tool: DMART in Emerging Markets

VerifiedAdded on 2022/10/13

|11

|2369

|495

Project

AI Summary

This project provides a comprehensive valuation of Avenue Supermarts Limited (DMART), a leading food and grocery retailer in India, within the context of an emerging market. The analysis incorporates the challenges inherent in emerging market valuations, such as macroeconomic uncertainties, political risks, and less stringent accounting standards. The project begins with a historical analysis of DMART's financial statements, followed by forecasting macroeconomic fundamentals, including revenue growth and store expansion plans. It addresses the incorporation of various risks through scenario analysis, utilizing a discounted cash flow approach to determine the intrinsic value of the stock. The study considers a base case and a distress scenario, estimating the probability of each. The cost of capital is estimated, incorporating factors such as inflation and leverage. The project concludes with the valuation results, comparing the intrinsic value with the current market price and providing relevant references. The analysis provides an in-depth understanding of financial modeling and valuation techniques applicable to emerging market companies.

VALUATION IN EMERGING MARKETS

Valuation in Emerging Markets

Valuation in Emerging Markets

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2VALUATION IN EMERGING MARKETS

Introduction

Valuation in emerging markets is comparatively more challenging due to the uncertainties in

macro-economic fundamentals, uncertain political risks, illiquid capital markets, control on

capital flows between the country and the other parts of globe and less stringent accounting

standards (McKinsey, Koller, Goedhart, & Wessels, 2010). The assignment serves to explain

incorporation of these uncertainties in valuation of Avenue Supermarts limited (National

Stock Exchange: DMART), which is a prominent food and grocery retailer in India (DMart,

2019).

Historical Analysis

Usually, in case of many emerging markets, the nation’s accounting standards are not very

stringent or detailed and differ vastly from IFRS. This leads to difficulty in comparing

companies following the local accounting standards with their international counterparts.

Here DMART’s financial statements are prepared in accordance with Indian Accounting

Standards. There is not much difference between IFRS and Indian AS (PWC, 2019). The

financial disclosures of DMART are quite detailed allowing for more accuracy in valuation.

Forecasting Macro-economic fundamentals

Over the past few years, India has become more stable on the political front. This has led to

smoother functioning of the government initiatives and regulations (Reserve Bank of India,

2019). The revenue forecasts reflect this stability. It is assumed that revenue growth for the

company would remain robust for the next five years on the back of high economic growth

brought about by positive reforms through a stable government. It is assumed that the

company will aggressively open stores within the next five years to combat the robust

demand brought about by growth in personal disposable income brought about by high GDP

growth and fall in unemployment, a strategic shift of people towards shopping from

Introduction

Valuation in emerging markets is comparatively more challenging due to the uncertainties in

macro-economic fundamentals, uncertain political risks, illiquid capital markets, control on

capital flows between the country and the other parts of globe and less stringent accounting

standards (McKinsey, Koller, Goedhart, & Wessels, 2010). The assignment serves to explain

incorporation of these uncertainties in valuation of Avenue Supermarts limited (National

Stock Exchange: DMART), which is a prominent food and grocery retailer in India (DMart,

2019).

Historical Analysis

Usually, in case of many emerging markets, the nation’s accounting standards are not very

stringent or detailed and differ vastly from IFRS. This leads to difficulty in comparing

companies following the local accounting standards with their international counterparts.

Here DMART’s financial statements are prepared in accordance with Indian Accounting

Standards. There is not much difference between IFRS and Indian AS (PWC, 2019). The

financial disclosures of DMART are quite detailed allowing for more accuracy in valuation.

Forecasting Macro-economic fundamentals

Over the past few years, India has become more stable on the political front. This has led to

smoother functioning of the government initiatives and regulations (Reserve Bank of India,

2019). The revenue forecasts reflect this stability. It is assumed that revenue growth for the

company would remain robust for the next five years on the back of high economic growth

brought about by positive reforms through a stable government. It is assumed that the

company will aggressively open stores within the next five years to combat the robust

demand brought about by growth in personal disposable income brought about by high GDP

growth and fall in unemployment, a strategic shift of people towards shopping from

3VALUATION IN EMERGING MARKETS

organized sector, and increased online grocery purchase preference by the tech savvy middle

class generation.

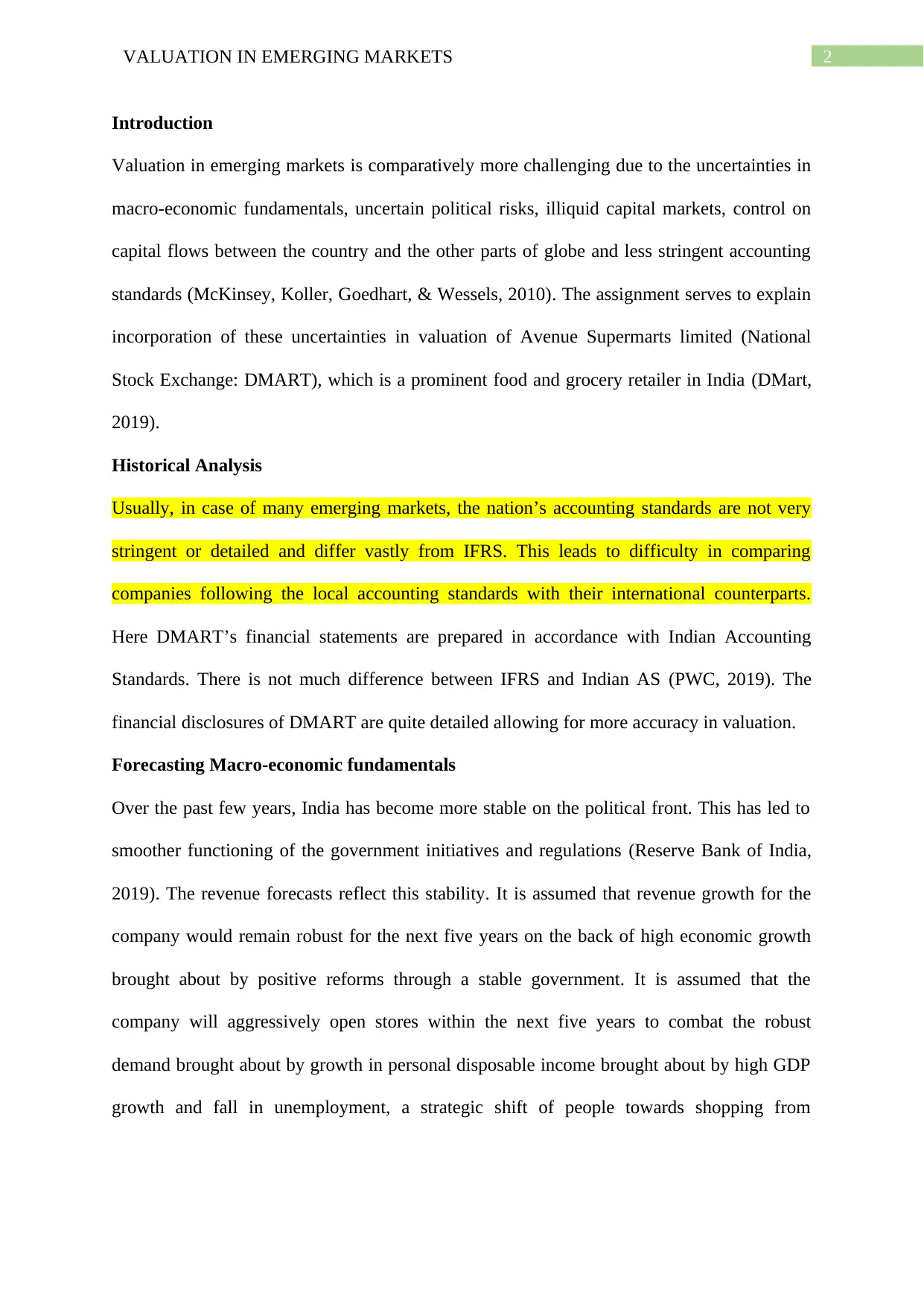

Here, while forecasting revenue under base case scenario, it is being considered that the same

store sales revenue growth would be around 20% for the next five years based on robust GDP

growth. Additionally, the company would continue to open 25 stores in FY20 and FY21, 24

stores in FY22, 23 stores in FY23 and 22 stores in FY24, to meet the high demand in the next

five years. It is also considered that the average area per new store would be same as the

average area of existing stores. It is also assumed that the company would witness 10%

growth in additional revenue per additional square feet added in the next five years.

While the inflation rate could inch up in forecasted years with rising GDP growth, the

monetary policy authority would definitely put a check on inflation through raising the

interest rates among other alternatives. The company’s interest costs would not be a cause of

worry since its debt equity ratio is significantly low and is not expected to reign on very high

territory. Further, considering a high interest coverage ratio, the company would not have

trouble refinancing its debt at attractive rates.

Considering fluctuations in exchange rate, it is assumed that in the long run, purchasing

power parity will hold. Inflation rate differential would lead to exchange rate adjustments and

hence, financial projections would not need tweaking for the same.

organized sector, and increased online grocery purchase preference by the tech savvy middle

class generation.

Here, while forecasting revenue under base case scenario, it is being considered that the same

store sales revenue growth would be around 20% for the next five years based on robust GDP

growth. Additionally, the company would continue to open 25 stores in FY20 and FY21, 24

stores in FY22, 23 stores in FY23 and 22 stores in FY24, to meet the high demand in the next

five years. It is also considered that the average area per new store would be same as the

average area of existing stores. It is also assumed that the company would witness 10%

growth in additional revenue per additional square feet added in the next five years.

While the inflation rate could inch up in forecasted years with rising GDP growth, the

monetary policy authority would definitely put a check on inflation through raising the

interest rates among other alternatives. The company’s interest costs would not be a cause of

worry since its debt equity ratio is significantly low and is not expected to reign on very high

territory. Further, considering a high interest coverage ratio, the company would not have

trouble refinancing its debt at attractive rates.

Considering fluctuations in exchange rate, it is assumed that in the long run, purchasing

power parity will hold. Inflation rate differential would lead to exchange rate adjustments and

hence, financial projections would not need tweaking for the same.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4VALUATION IN EMERGING MARKETS

Another area is the marginal tax rate that would be applicable to DMART. With increasing

political stability, the marginal tax rate for the company is expected to remain on the lower

side. The Indian government has recently lowered the effective tax rate for companies to

25.17%. For the next five years, it has been assumed that the effective tax rate would remain

the same.

Incorporation of Risks

There are possibilities that competitive environment may act as headwinds to its growth.

Adding to this, there could be political uncertainties if the current government does not

survive the next five years. Additionally, global slowdown could creep into Indian GDP

figures as well or there could be volatility in capital markets due to structural issues like the

current issues enveloping the non-performing assets of Indian banking sector. Furthermore,

any hike in oil prices due to rising tensions in middle east Asia in the coming years could

prove detrimental to the country’s fiscal deficit, thereby dampening the planned expenditure

of the Indian government resulting in growth slowdown in the country.

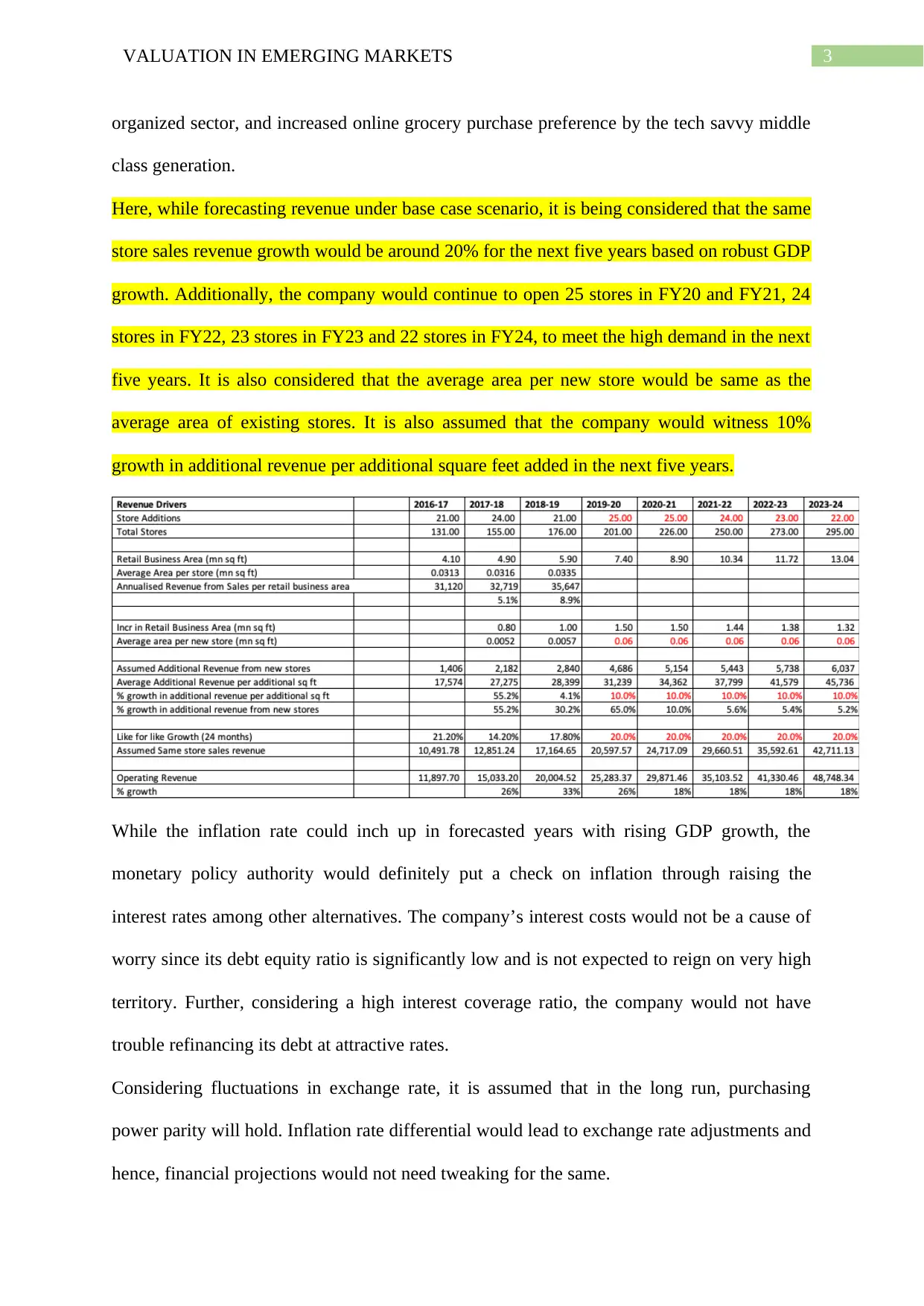

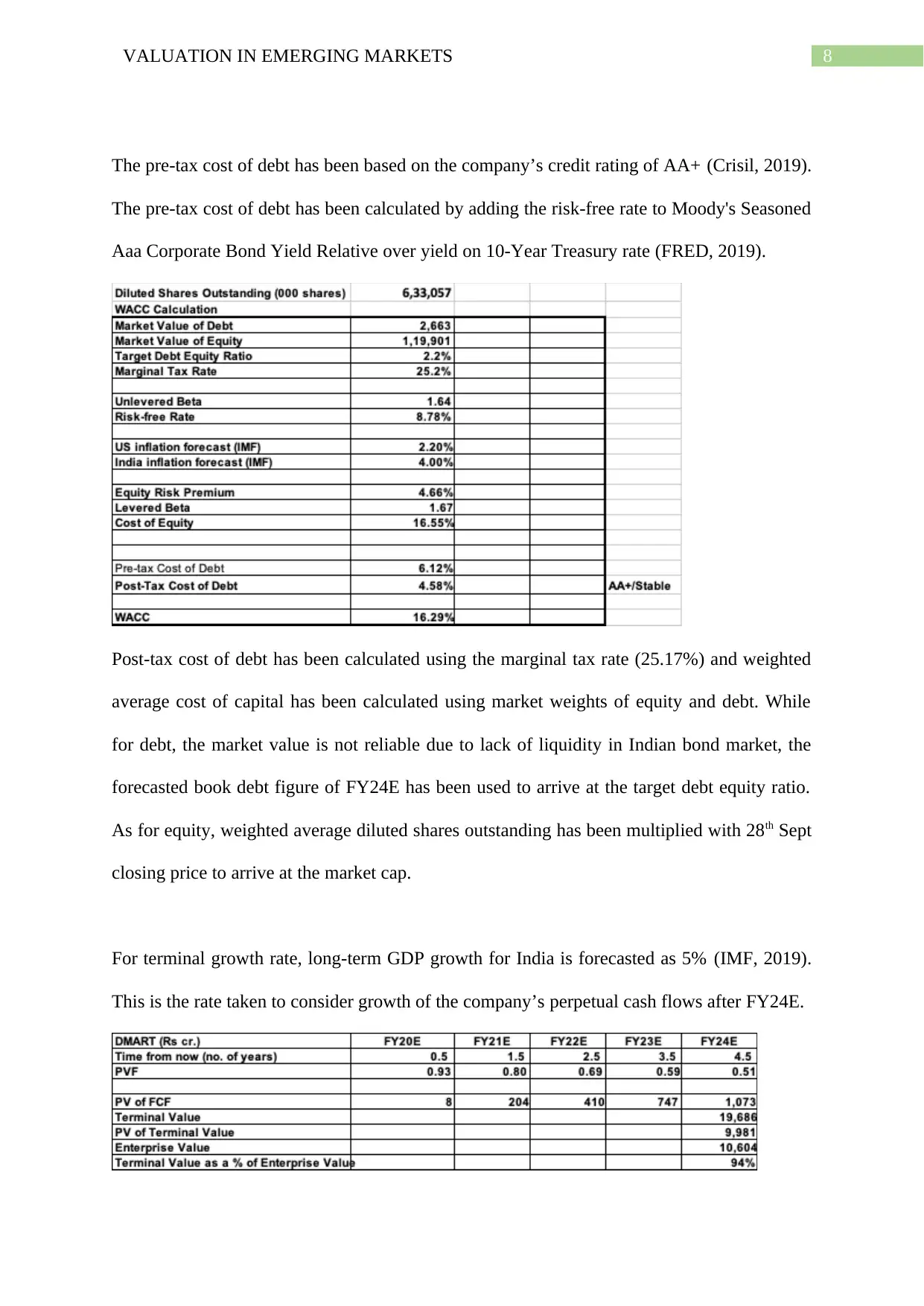

Scenario Discounted Cash Flow Approach

In this approach, various scenarios can be assumed and free cash flows computed accordingly

(McKinsey, Koller, Goedhart, & Wessels, 2010). Considering the existing scenario where

GDP growth is assumed to go up within next five years on the back of political stability and

low interest rate regime, the free cash flow table from FY20E-FY24E is estimated as follows

(terminal cash flows are expected to grow at terminal growth rate indefinitely):

Another area is the marginal tax rate that would be applicable to DMART. With increasing

political stability, the marginal tax rate for the company is expected to remain on the lower

side. The Indian government has recently lowered the effective tax rate for companies to

25.17%. For the next five years, it has been assumed that the effective tax rate would remain

the same.

Incorporation of Risks

There are possibilities that competitive environment may act as headwinds to its growth.

Adding to this, there could be political uncertainties if the current government does not

survive the next five years. Additionally, global slowdown could creep into Indian GDP

figures as well or there could be volatility in capital markets due to structural issues like the

current issues enveloping the non-performing assets of Indian banking sector. Furthermore,

any hike in oil prices due to rising tensions in middle east Asia in the coming years could

prove detrimental to the country’s fiscal deficit, thereby dampening the planned expenditure

of the Indian government resulting in growth slowdown in the country.

Scenario Discounted Cash Flow Approach

In this approach, various scenarios can be assumed and free cash flows computed accordingly

(McKinsey, Koller, Goedhart, & Wessels, 2010). Considering the existing scenario where

GDP growth is assumed to go up within next five years on the back of political stability and

low interest rate regime, the free cash flow table from FY20E-FY24E is estimated as follows

(terminal cash flows are expected to grow at terminal growth rate indefinitely):

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5VALUATION IN EMERGING MARKETS

Considering a scenario where slowdown in economic growth leads to realization of lower

same store sales growth (from 20% to 10%) and less addition of new stores (from 25 to 20 in

FY20E and FY21E; and 15 in FY22E-FY24E), the free cash flow table would be as follows:

It is being assumed here that average area per new store would be the same as the average

area for existing stores and additional revenue from new stores would witness growth of 10%

in spite of growth slowdown considering the fact that demand for food products and staples

remains stable irrespective of growth pangs. In fact, with the rising middle class and a general

inclination of people towards an organized retail sector for meeting their demands, the

company would continue to gain market share in a vastly unorganized retail market.

Furthermore, the company’s steps towards embracing e-commerce in an era of increasing

online retail purchases would also help it in safeguarding its existing market share. For the

last few years, the company has been very proactive in opening DMART Ready pick-up

points in various strategic locations for convenient shopping by customers round the clock as

well as on the move. Along with such an effective online shopping experience, attractive

discounts and home delivery at reasonable rates would help the company compete in the

market effectively even in periods of cyclical or structural growth slowdown.

Probability of Cash Flows

Considering the two cases- base case scenario and distress scenario, it is assumed that the

probability of company falling into distress scenario is currently 30%. This low percentage is

based on the premise that political environment is currently highly stable, reforms are in good

Considering a scenario where slowdown in economic growth leads to realization of lower

same store sales growth (from 20% to 10%) and less addition of new stores (from 25 to 20 in

FY20E and FY21E; and 15 in FY22E-FY24E), the free cash flow table would be as follows:

It is being assumed here that average area per new store would be the same as the average

area for existing stores and additional revenue from new stores would witness growth of 10%

in spite of growth slowdown considering the fact that demand for food products and staples

remains stable irrespective of growth pangs. In fact, with the rising middle class and a general

inclination of people towards an organized retail sector for meeting their demands, the

company would continue to gain market share in a vastly unorganized retail market.

Furthermore, the company’s steps towards embracing e-commerce in an era of increasing

online retail purchases would also help it in safeguarding its existing market share. For the

last few years, the company has been very proactive in opening DMART Ready pick-up

points in various strategic locations for convenient shopping by customers round the clock as

well as on the move. Along with such an effective online shopping experience, attractive

discounts and home delivery at reasonable rates would help the company compete in the

market effectively even in periods of cyclical or structural growth slowdown.

Probability of Cash Flows

Considering the two cases- base case scenario and distress scenario, it is assumed that the

probability of company falling into distress scenario is currently 30%. This low percentage is

based on the premise that political environment is currently highly stable, reforms are in good

6VALUATION IN EMERGING MARKETS

progress, high government expenditure on infrastructure development is expected to generate

growth in GDP and jobs and elevate the living standard of people.

The retail industry, especially food products and staples section, are relatively resilient from

economic growth irregularities due to the products being necessities in nature. The industry

has also been witnessing some structural shifts from unorganized to organized retail with

preference by Indian middle class to shop from organized retail segment. Additionally, the

industry is also seeing a spurt in online sales with rise in internet penetration, better

connectivity from 4G services, and higher usage of smartphones on the move.

As for the company, DMART is fundamentally very strong and has created a brand image of

being a retail chain offering reasonable discounts. A typical store contains a vast collection of

popular brands in almost every product category, thus, promising most customers with their

choice of brands. The company has also moved into e-commerce retail quite fast and quickly

growing its chain of Ready pick-up points in strategic locations.

The headwinds are growth slowdown due to global growth slowdown and high oil prices with

growing uncertainties in middle east Asia leading to higher fiscal deficit percentage for the

Indian government.

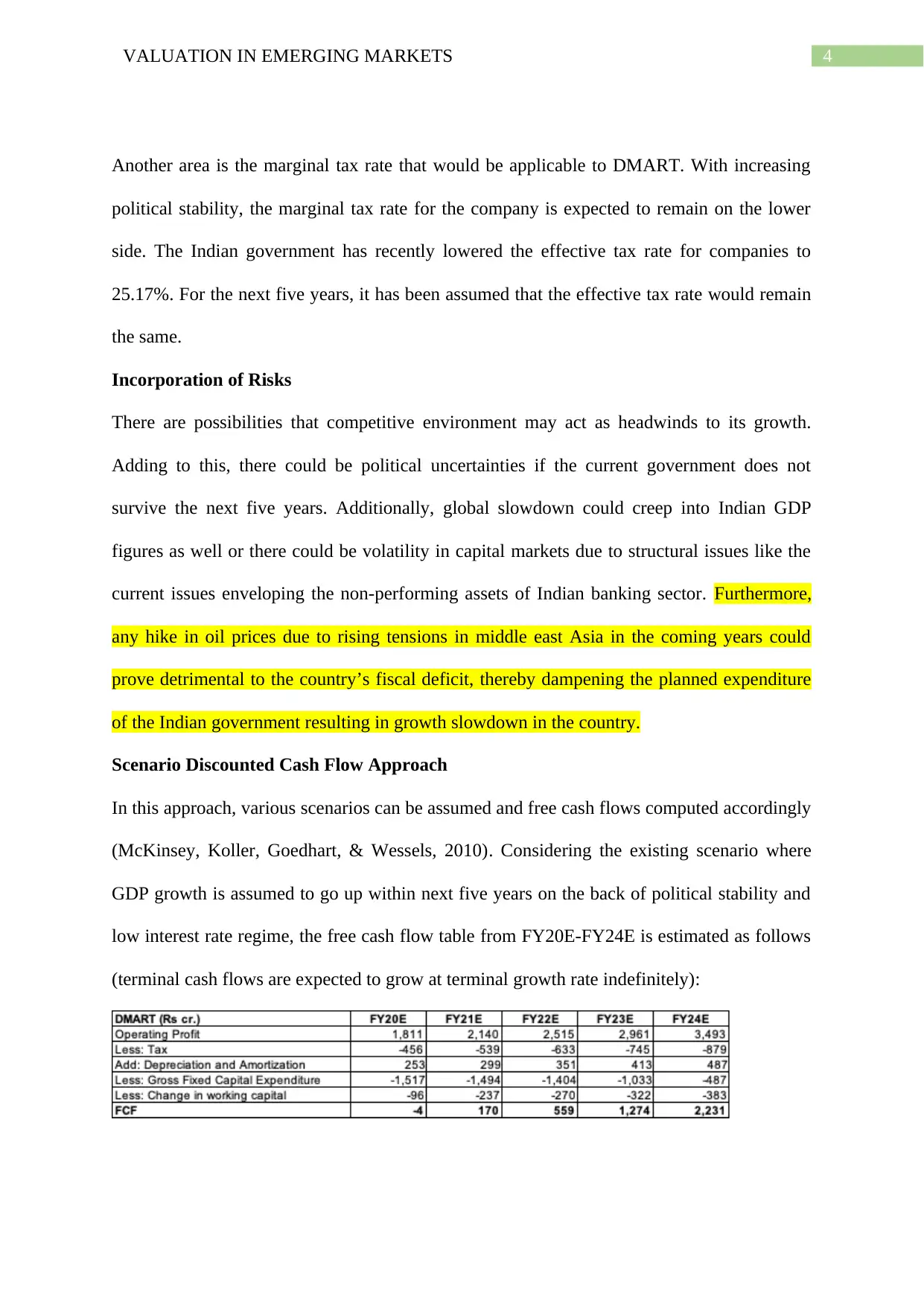

Based on the probabilities the expected Free cash flow table is as follows:

Estimating Cost of Capital

The average Indian investor cannot diversify globally because of capital controls. However,

the Indian capital market is well integrated with global markets and international investors

progress, high government expenditure on infrastructure development is expected to generate

growth in GDP and jobs and elevate the living standard of people.

The retail industry, especially food products and staples section, are relatively resilient from

economic growth irregularities due to the products being necessities in nature. The industry

has also been witnessing some structural shifts from unorganized to organized retail with

preference by Indian middle class to shop from organized retail segment. Additionally, the

industry is also seeing a spurt in online sales with rise in internet penetration, better

connectivity from 4G services, and higher usage of smartphones on the move.

As for the company, DMART is fundamentally very strong and has created a brand image of

being a retail chain offering reasonable discounts. A typical store contains a vast collection of

popular brands in almost every product category, thus, promising most customers with their

choice of brands. The company has also moved into e-commerce retail quite fast and quickly

growing its chain of Ready pick-up points in strategic locations.

The headwinds are growth slowdown due to global growth slowdown and high oil prices with

growing uncertainties in middle east Asia leading to higher fiscal deficit percentage for the

Indian government.

Based on the probabilities the expected Free cash flow table is as follows:

Estimating Cost of Capital

The average Indian investor cannot diversify globally because of capital controls. However,

the Indian capital market is well integrated with global markets and international investors

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7VALUATION IN EMERGING MARKETS

have easy access to the Indian market. It is expected that the integration will intensify in

future years allowing local investors to access the global markets freely. Considering the fact

that most country risks can be diversified by global investors, no additional country risk

premium has been added to the cost of capital. Additionally, in this case since probability

weights have been used, country risk premium has not been added as that would have lead to

double-counting.

The cost of capital, in case of DMART, can be estimated from a global cost of capital while

adjusting for inflation and leverage factor.

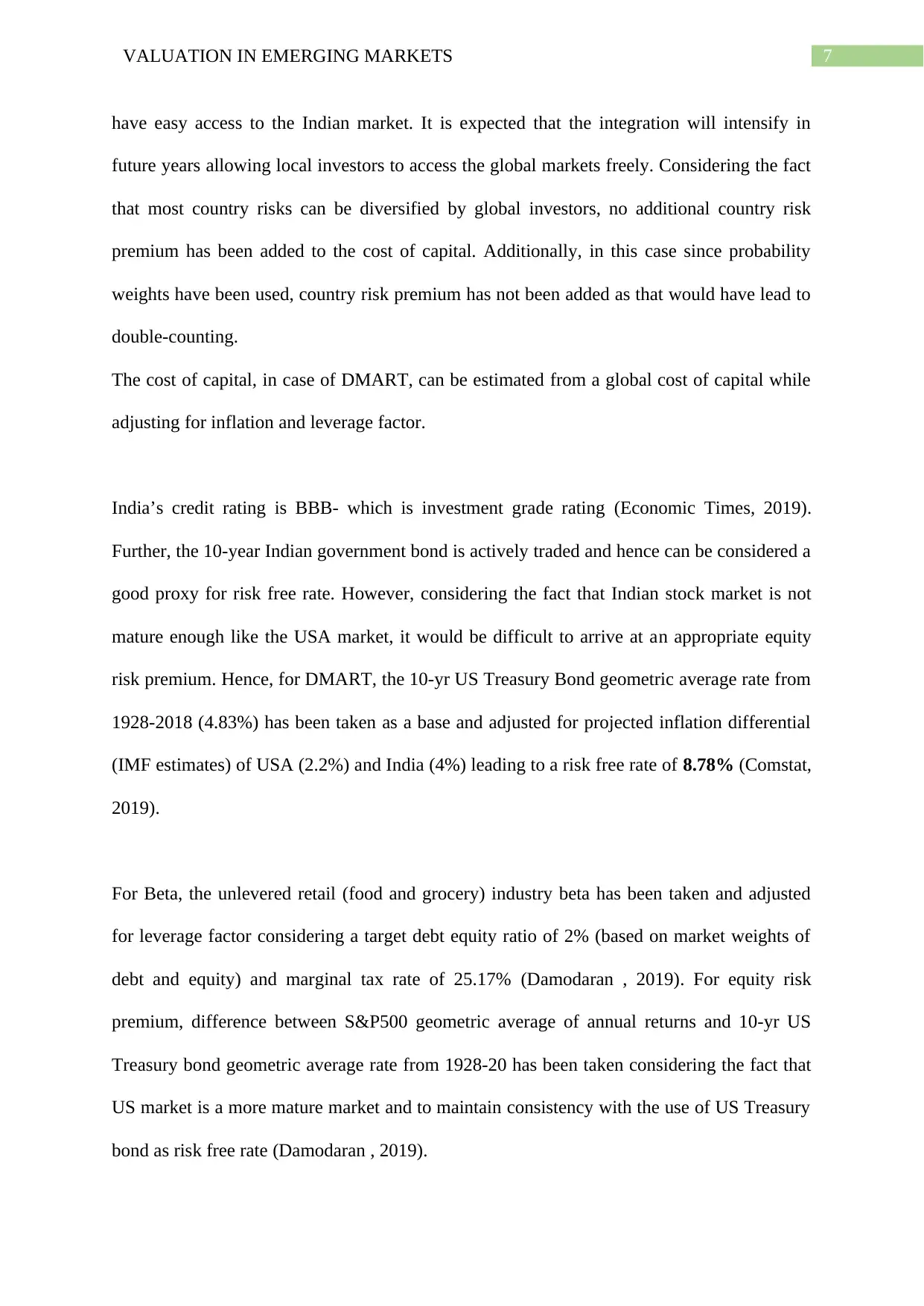

India’s credit rating is BBB- which is investment grade rating (Economic Times, 2019).

Further, the 10-year Indian government bond is actively traded and hence can be considered a

good proxy for risk free rate. However, considering the fact that Indian stock market is not

mature enough like the USA market, it would be difficult to arrive at an appropriate equity

risk premium. Hence, for DMART, the 10-yr US Treasury Bond geometric average rate from

1928-2018 (4.83%) has been taken as a base and adjusted for projected inflation differential

(IMF estimates) of USA (2.2%) and India (4%) leading to a risk free rate of 8.78% (Comstat,

2019).

For Beta, the unlevered retail (food and grocery) industry beta has been taken and adjusted

for leverage factor considering a target debt equity ratio of 2% (based on market weights of

debt and equity) and marginal tax rate of 25.17% (Damodaran , 2019). For equity risk

premium, difference between S&P500 geometric average of annual returns and 10-yr US

Treasury bond geometric average rate from 1928-20 has been taken considering the fact that

US market is a more mature market and to maintain consistency with the use of US Treasury

bond as risk free rate (Damodaran , 2019).

have easy access to the Indian market. It is expected that the integration will intensify in

future years allowing local investors to access the global markets freely. Considering the fact

that most country risks can be diversified by global investors, no additional country risk

premium has been added to the cost of capital. Additionally, in this case since probability

weights have been used, country risk premium has not been added as that would have lead to

double-counting.

The cost of capital, in case of DMART, can be estimated from a global cost of capital while

adjusting for inflation and leverage factor.

India’s credit rating is BBB- which is investment grade rating (Economic Times, 2019).

Further, the 10-year Indian government bond is actively traded and hence can be considered a

good proxy for risk free rate. However, considering the fact that Indian stock market is not

mature enough like the USA market, it would be difficult to arrive at an appropriate equity

risk premium. Hence, for DMART, the 10-yr US Treasury Bond geometric average rate from

1928-2018 (4.83%) has been taken as a base and adjusted for projected inflation differential

(IMF estimates) of USA (2.2%) and India (4%) leading to a risk free rate of 8.78% (Comstat,

2019).

For Beta, the unlevered retail (food and grocery) industry beta has been taken and adjusted

for leverage factor considering a target debt equity ratio of 2% (based on market weights of

debt and equity) and marginal tax rate of 25.17% (Damodaran , 2019). For equity risk

premium, difference between S&P500 geometric average of annual returns and 10-yr US

Treasury bond geometric average rate from 1928-20 has been taken considering the fact that

US market is a more mature market and to maintain consistency with the use of US Treasury

bond as risk free rate (Damodaran , 2019).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8VALUATION IN EMERGING MARKETS

The pre-tax cost of debt has been based on the company’s credit rating of AA+ (Crisil, 2019).

The pre-tax cost of debt has been calculated by adding the risk-free rate to Moody's Seasoned

Aaa Corporate Bond Yield Relative over yield on 10-Year Treasury rate (FRED, 2019).

Post-tax cost of debt has been calculated using the marginal tax rate (25.17%) and weighted

average cost of capital has been calculated using market weights of equity and debt. While

for debt, the market value is not reliable due to lack of liquidity in Indian bond market, the

forecasted book debt figure of FY24E has been used to arrive at the target debt equity ratio.

As for equity, weighted average diluted shares outstanding has been multiplied with 28th Sept

closing price to arrive at the market cap.

For terminal growth rate, long-term GDP growth for India is forecasted as 5% (IMF, 2019).

This is the rate taken to consider growth of the company’s perpetual cash flows after FY24E.

The pre-tax cost of debt has been based on the company’s credit rating of AA+ (Crisil, 2019).

The pre-tax cost of debt has been calculated by adding the risk-free rate to Moody's Seasoned

Aaa Corporate Bond Yield Relative over yield on 10-Year Treasury rate (FRED, 2019).

Post-tax cost of debt has been calculated using the marginal tax rate (25.17%) and weighted

average cost of capital has been calculated using market weights of equity and debt. While

for debt, the market value is not reliable due to lack of liquidity in Indian bond market, the

forecasted book debt figure of FY24E has been used to arrive at the target debt equity ratio.

As for equity, weighted average diluted shares outstanding has been multiplied with 28th Sept

closing price to arrive at the market cap.

For terminal growth rate, long-term GDP growth for India is forecasted as 5% (IMF, 2019).

This is the rate taken to consider growth of the company’s perpetual cash flows after FY24E.

9VALUATION IN EMERGING MARKETS

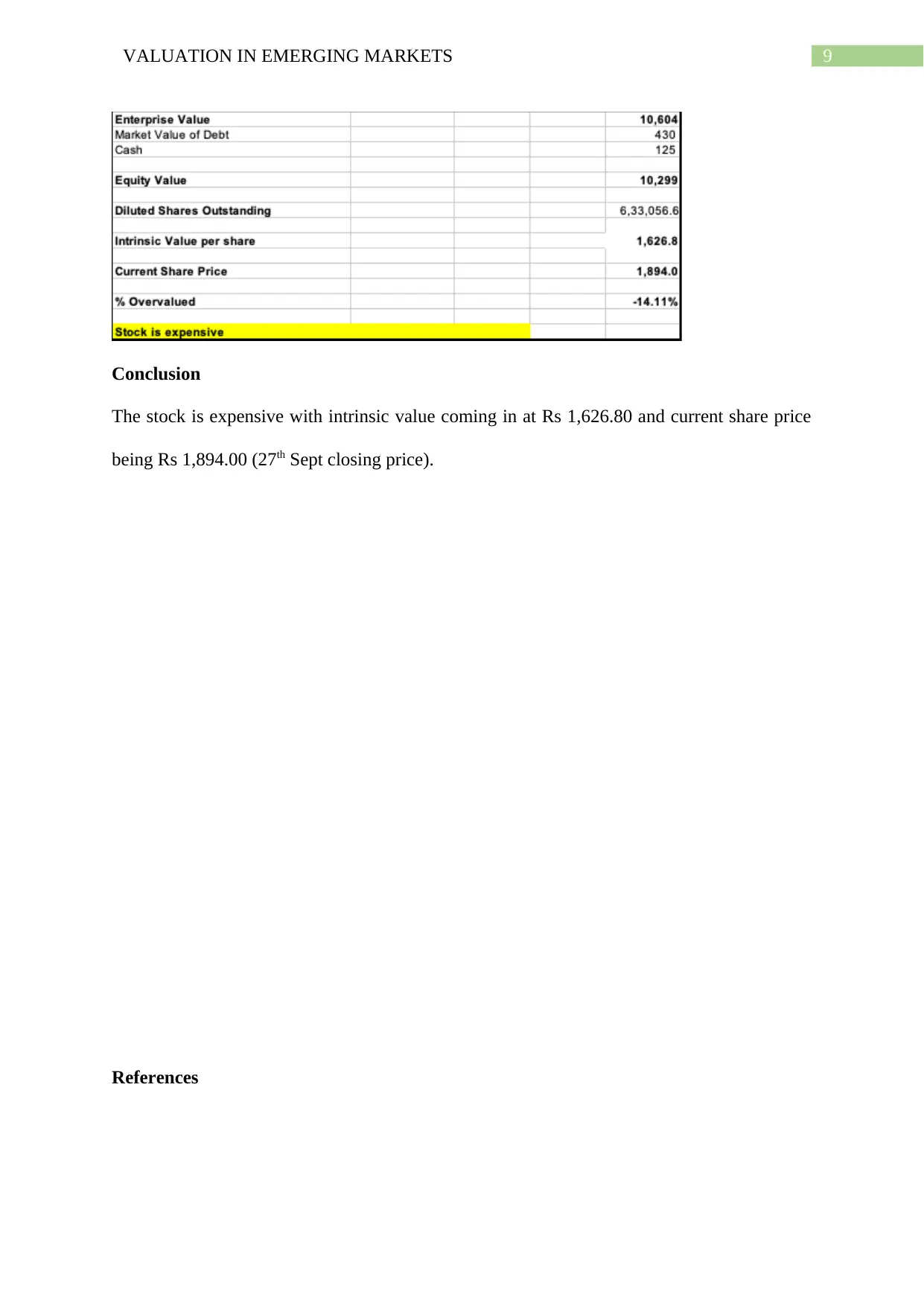

Conclusion

The stock is expensive with intrinsic value coming in at Rs 1,626.80 and current share price

being Rs 1,894.00 (27th Sept closing price).

References

Conclusion

The stock is expensive with intrinsic value coming in at Rs 1,626.80 and current share price

being Rs 1,894.00 (27th Sept closing price).

References

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10VALUATION IN EMERGING MARKETS

Comstat. (2019, Sept 28th). Comstat. Retrieved Sept 28th, 2019, from US Inflation Forecast

2019-2024 and up to 2060: http://comstat.comesa.int/kyaewad/us-inflation-forecast-

2019-2024-and-up-to-2060-data-and-charts?lang=en

Crisil. (2019, Sept 28th). Crisil. Retrieved Apr 26th, 2019, from Avenue Supermarts Limited:

https://www.crisil.com/mnt/winshare/Ratings/RatingList/RatingDocs/

Avenue_Supermarts_Limited_April_26_2019_RR.html

Damodaran . (2019, Sept 28th). New York University. Retrieved Jan 31st, 2019, from Data

Current: http://pages.stern.nyu.edu/~adamodar/New_Home_Page/datacurrent.html

DMart. (2019, Sept 28th). Annual Report. Retrieved Sept 28th, 2019, from D Mart:

https://www.dmartindia.com/investor-relationship

Economic Times. (2019, Sept 28th). Economic Times. Retrieved Nov 15th, 2018, from Fitch

keeps India rating unchanged for 12th year in a row:

https://economictimes.indiatimes.com/news/economy/indicators/fitch-keeps-indias-

sovereign-rating-unchanged/articleshow/66638115.cms?from=mdr

FRED. (2019, Sept 28th). FRED Economic Data. Retrieved Sept 28th, 2019, from Moody's

Seasoned Aaa Corporate Bond Yield Relative to Yield on 10-Year Treasury Constant

Maturity: https://fred.stlouisfed.org/series/AAA10Y

IMF. (2019, Sept 28th). International Monetary Fund. Retrieved Jul 23rd, 2019, from IMF

cuts India's FY20 growth forecast by 20 bps to 7%:

https://economictimes.indiatimes.com/news/economy/indicators/imf-cuts-indias-fy20-

growth-forecast-by-30-bps-to-7/articleshow/70348753.cms?from=mdr

McKinsey, Koller, T., Goedhart, M., & Wessels, D. (2010). Valuation: Measuring and

Managing the Value of Companies, University Edition. Hoboken: John Wiley and

Sons.

Comstat. (2019, Sept 28th). Comstat. Retrieved Sept 28th, 2019, from US Inflation Forecast

2019-2024 and up to 2060: http://comstat.comesa.int/kyaewad/us-inflation-forecast-

2019-2024-and-up-to-2060-data-and-charts?lang=en

Crisil. (2019, Sept 28th). Crisil. Retrieved Apr 26th, 2019, from Avenue Supermarts Limited:

https://www.crisil.com/mnt/winshare/Ratings/RatingList/RatingDocs/

Avenue_Supermarts_Limited_April_26_2019_RR.html

Damodaran . (2019, Sept 28th). New York University. Retrieved Jan 31st, 2019, from Data

Current: http://pages.stern.nyu.edu/~adamodar/New_Home_Page/datacurrent.html

DMart. (2019, Sept 28th). Annual Report. Retrieved Sept 28th, 2019, from D Mart:

https://www.dmartindia.com/investor-relationship

Economic Times. (2019, Sept 28th). Economic Times. Retrieved Nov 15th, 2018, from Fitch

keeps India rating unchanged for 12th year in a row:

https://economictimes.indiatimes.com/news/economy/indicators/fitch-keeps-indias-

sovereign-rating-unchanged/articleshow/66638115.cms?from=mdr

FRED. (2019, Sept 28th). FRED Economic Data. Retrieved Sept 28th, 2019, from Moody's

Seasoned Aaa Corporate Bond Yield Relative to Yield on 10-Year Treasury Constant

Maturity: https://fred.stlouisfed.org/series/AAA10Y

IMF. (2019, Sept 28th). International Monetary Fund. Retrieved Jul 23rd, 2019, from IMF

cuts India's FY20 growth forecast by 20 bps to 7%:

https://economictimes.indiatimes.com/news/economy/indicators/imf-cuts-indias-fy20-

growth-forecast-by-30-bps-to-7/articleshow/70348753.cms?from=mdr

McKinsey, Koller, T., Goedhart, M., & Wessels, D. (2010). Valuation: Measuring and

Managing the Value of Companies, University Edition. Hoboken: John Wiley and

Sons.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11VALUATION IN EMERGING MARKETS

PWC. (2019, Sept 28th). PWC. Retrieved Sept 28th, 2019, from IFRS, US GAAP, Ind AS

and Indian GAAP: https://www.pwc.in/assets/pdfs/publications/2017/ifrs-us-gaap-

ind-as-and-indian-gaap-similarities-and-differences.pdf

Reserve Bank of India. (2019, Sept 28th). Reserve Bank of India. Retrieved Sept 28th, 2019,

from Monetary Policy Report:

https://www.rbi.org.in/Scripts/HalfYearlyPublications.aspx?head=Monetary

%20Policy%20Report

PWC. (2019, Sept 28th). PWC. Retrieved Sept 28th, 2019, from IFRS, US GAAP, Ind AS

and Indian GAAP: https://www.pwc.in/assets/pdfs/publications/2017/ifrs-us-gaap-

ind-as-and-indian-gaap-similarities-and-differences.pdf

Reserve Bank of India. (2019, Sept 28th). Reserve Bank of India. Retrieved Sept 28th, 2019,

from Monetary Policy Report:

https://www.rbi.org.in/Scripts/HalfYearlyPublications.aspx?head=Monetary

%20Policy%20Report

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.