Medibank Limited: Advance Financial Accounting Report - HA3011

VerifiedAdded on 2022/10/19

|11

|3589

|214

Report

AI Summary

This report provides a comprehensive analysis of Medibank Private Limited's financial accounting practices, based on its 2018 annual report. It identifies the accounting standards employed, primarily adhering to Australian Accounting Standards (AASB) and International Financial Reporting Standards (IFRS). The report delves into the application of these standards, including the measurement of financial assets at fair value and the valuation of claims and liabilities. A significant portion of the report is dedicated to the new accounting standard for leases, AASB 16, explaining the changes incorporated and their impact on Medibank's financial statements. The discussion includes the disclosure requirements related to leases, such as operating lease commitments and payments receivable. The report also examines the transitional provisions and the effects of transitioning from AASB 117 to AASB 16, outlining the implications for Medibank's financial reporting, including the adoption of either the complete or modified retrospective approach. The report aims to provide a clear understanding of Medibank's financial position and the evolving landscape of accounting standards, offering valuable insights for investors and stakeholders.

Running head: ADVANCE FINANCIAL ACCOUNTING

Advance Financial Accounting

Name of the student

Name of the university

Author note

Advance Financial Accounting

Name of the student

Name of the university

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ADVANCE FINANCIAL ACCOUNTING

Table of Contents

Introduction......................................................................................................................................3

Discussion........................................................................................................................................3

Conclusion.......................................................................................................................................8

References......................................................................................................................................10

Table of Contents

Introduction......................................................................................................................................3

Discussion........................................................................................................................................3

Conclusion.......................................................................................................................................8

References......................................................................................................................................10

2ADVANCE FINANCIAL ACCOUNTING

Introduction

The Medibank private limited is a particular firm, which provide insurance for good

physical condition and management of disease. Medibank also provide preventive and better

non-segregated primary health care and after hours physical support. The company provide

service to the peoples of Australia. The headquarters of the company is located in Melbourne,

Australia. The company operates in the physical fitness insurance service sector. The company is

the second largest service provider of physical fitness insurance in Australia. The revenue earn

by the company is AUD $6,319.5 million at the end of the year 2018. The firm earns a total

income of $ 445.1 for the year 2018. The company had 3.7 million consumers and the additional

amount that have been committed to the consumers if of $35 million. The reported market share

of the company is 26.85% for the year 2018 (Medibank, 2019). This firm is listed in the

Australian stock exchange (ASX). The purpose of this entity is to provide better health service to

the peoples of the Australia (Xu, Davidson and Cheong, 2017). The strategy of this entity is to

take responsibility for providing better health by playing an active role in helping the customers

to take a better control of health and wellbeing of the people (Bugeja, Czernkowski and Moran,

2015). The motive of this report is to examine the annual report of the company and to describe

and identify the accounting standards used by the company for preparing the monetary statement

of the entity. The changed incorporated in this new accounting standard for lease AASB 16 by

entity have also been stated in the report.

Discussion

The monetary statements of the firm have been put together by succeding the Australian

Accounting Standards AASB, International Financial Reporting Standard (IFRS). These

standards of accounting have been offered by the International Accounting standard board and

the company’s act 2001. The statement have been put together under the historical cost

agreement. The financial assets of companies have been calculated at a fair value

(www.aasb.gov.au, 2019). The profit and loss records and the plant and machinery of this entity

also measured at its fair worth. The claims and the liabilities of the entity are measured by at the

current worth of the presumed time to come payments of the company. The amounts of the

financial records are introduced in Australian dollars, this is the practical and presenting currency

Introduction

The Medibank private limited is a particular firm, which provide insurance for good

physical condition and management of disease. Medibank also provide preventive and better

non-segregated primary health care and after hours physical support. The company provide

service to the peoples of Australia. The headquarters of the company is located in Melbourne,

Australia. The company operates in the physical fitness insurance service sector. The company is

the second largest service provider of physical fitness insurance in Australia. The revenue earn

by the company is AUD $6,319.5 million at the end of the year 2018. The firm earns a total

income of $ 445.1 for the year 2018. The company had 3.7 million consumers and the additional

amount that have been committed to the consumers if of $35 million. The reported market share

of the company is 26.85% for the year 2018 (Medibank, 2019). This firm is listed in the

Australian stock exchange (ASX). The purpose of this entity is to provide better health service to

the peoples of the Australia (Xu, Davidson and Cheong, 2017). The strategy of this entity is to

take responsibility for providing better health by playing an active role in helping the customers

to take a better control of health and wellbeing of the people (Bugeja, Czernkowski and Moran,

2015). The motive of this report is to examine the annual report of the company and to describe

and identify the accounting standards used by the company for preparing the monetary statement

of the entity. The changed incorporated in this new accounting standard for lease AASB 16 by

entity have also been stated in the report.

Discussion

The monetary statements of the firm have been put together by succeding the Australian

Accounting Standards AASB, International Financial Reporting Standard (IFRS). These

standards of accounting have been offered by the International Accounting standard board and

the company’s act 2001. The statement have been put together under the historical cost

agreement. The financial assets of companies have been calculated at a fair value

(www.aasb.gov.au, 2019). The profit and loss records and the plant and machinery of this entity

also measured at its fair worth. The claims and the liabilities of the entity are measured by at the

current worth of the presumed time to come payments of the company. The amounts of the

financial records are introduced in Australian dollars, this is the practical and presenting currency

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ADVANCE FINANCIAL ACCOUNTING

of the firm Medibank. The amount balances have been aggregated in following with ASIC

Corporations implement to the closest hundred thousand dollars. The company have adopted all

the new accounting standard that have been become mandatory for preparing financial

statements for the time period of 30th June 2018. The new accounting standard that have been

adopted by the company do not create any effect on the monetary statements for the reporting

period of 30th June 2018. The profits from the selling of monetary assets and the acquirer of

monetary assets in the consolidated income statement of cash flows have been again classified.

This results of a change in presenting of these items in the recent reporting period. This change

does not make an effect on the total cash flow from the investing activities (Cotton, Schneider

and McCarthy, 2013).

The objective for the disclosure in lease is as because for better understanding of monetary

position of the firm. The users of the monetary records require in understanding the timing, the

amount and unpredictability of cash flows growing from leases (Parker, 2013). The company

should disclose the cost of the financial lease. The lessee need to disclose the short term costs of

lease eliminating the expenses of the lease that need to be disclosed. The sublease income on a

gross basis also have to disclose in the annual report. The net gain and the loss also have to

disclose. The transactions that are practically related to the measurements he to be disclosed.

This includes the package of practical expedients, that give the access to lessee not to reappraise

any contracts, existing or expired that contain leases (Öztürk and Serçemeli, 2016). According to

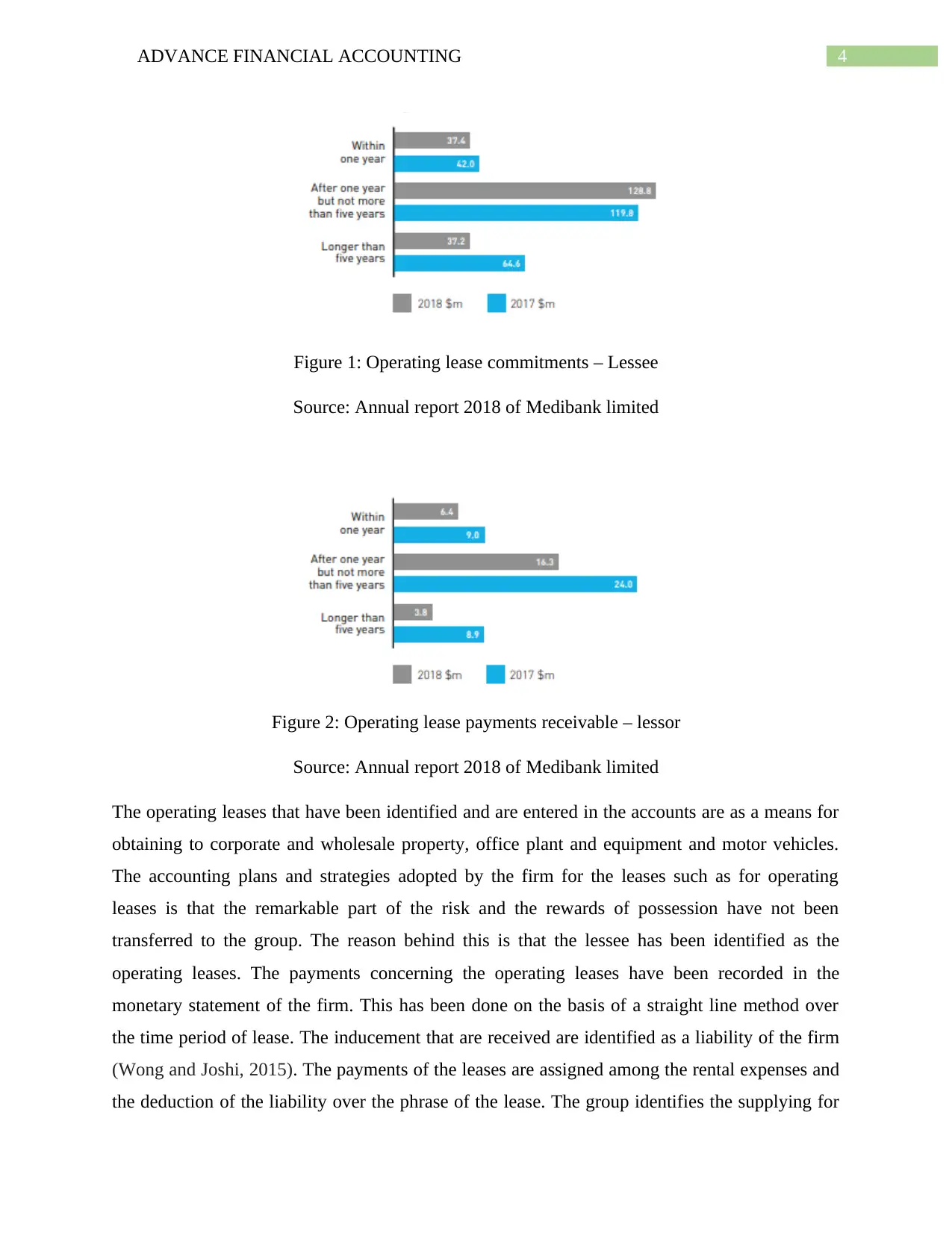

annual report provided by the entity for the year of 2018, the operating commitments of lease

within one year is $37.4million, for more than one year it is $128.8 million and the lease

commitments, that are longer than five years are $37.2 million. The lease operating payments

receivable within one year are $6.4 million, for more than year the amount is $16.3 million and

the lease payments that are receivable for more five years is $3.8 million. The above mentioned

amount of operational lease commitments and the lease payments receivable are all less than the

previous year. The graphs have been showed below

of the firm Medibank. The amount balances have been aggregated in following with ASIC

Corporations implement to the closest hundred thousand dollars. The company have adopted all

the new accounting standard that have been become mandatory for preparing financial

statements for the time period of 30th June 2018. The new accounting standard that have been

adopted by the company do not create any effect on the monetary statements for the reporting

period of 30th June 2018. The profits from the selling of monetary assets and the acquirer of

monetary assets in the consolidated income statement of cash flows have been again classified.

This results of a change in presenting of these items in the recent reporting period. This change

does not make an effect on the total cash flow from the investing activities (Cotton, Schneider

and McCarthy, 2013).

The objective for the disclosure in lease is as because for better understanding of monetary

position of the firm. The users of the monetary records require in understanding the timing, the

amount and unpredictability of cash flows growing from leases (Parker, 2013). The company

should disclose the cost of the financial lease. The lessee need to disclose the short term costs of

lease eliminating the expenses of the lease that need to be disclosed. The sublease income on a

gross basis also have to disclose in the annual report. The net gain and the loss also have to

disclose. The transactions that are practically related to the measurements he to be disclosed.

This includes the package of practical expedients, that give the access to lessee not to reappraise

any contracts, existing or expired that contain leases (Öztürk and Serçemeli, 2016). According to

annual report provided by the entity for the year of 2018, the operating commitments of lease

within one year is $37.4million, for more than one year it is $128.8 million and the lease

commitments, that are longer than five years are $37.2 million. The lease operating payments

receivable within one year are $6.4 million, for more than year the amount is $16.3 million and

the lease payments that are receivable for more five years is $3.8 million. The above mentioned

amount of operational lease commitments and the lease payments receivable are all less than the

previous year. The graphs have been showed below

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ADVANCE FINANCIAL ACCOUNTING

Figure 1: Operating lease commitments – Lessee

Source: Annual report 2018 of Medibank limited

Figure 2: Operating lease payments receivable – lessor

Source: Annual report 2018 of Medibank limited

The operating leases that have been identified and are entered in the accounts are as a means for

obtaining to corporate and wholesale property, office plant and equipment and motor vehicles.

The accounting plans and strategies adopted by the firm for the leases such as for operating

leases is that the remarkable part of the risk and the rewards of possession have not been

transferred to the group. The reason behind this is that the lessee has been identified as the

operating leases. The payments concerning the operating leases have been recorded in the

monetary statement of the firm. This has been done on the basis of a straight line method over

the time period of lease. The inducement that are received are identified as a liability of the firm

(Wong and Joshi, 2015). The payments of the leases are assigned among the rental expenses and

the deduction of the liability over the phrase of the lease. The group identifies the supplying for

Figure 1: Operating lease commitments – Lessee

Source: Annual report 2018 of Medibank limited

Figure 2: Operating lease payments receivable – lessor

Source: Annual report 2018 of Medibank limited

The operating leases that have been identified and are entered in the accounts are as a means for

obtaining to corporate and wholesale property, office plant and equipment and motor vehicles.

The accounting plans and strategies adopted by the firm for the leases such as for operating

leases is that the remarkable part of the risk and the rewards of possession have not been

transferred to the group. The reason behind this is that the lessee has been identified as the

operating leases. The payments concerning the operating leases have been recorded in the

monetary statement of the firm. This has been done on the basis of a straight line method over

the time period of lease. The inducement that are received are identified as a liability of the firm

(Wong and Joshi, 2015). The payments of the leases are assigned among the rental expenses and

the deduction of the liability over the phrase of the lease. The group identifies the supplying for

5ADVANCE FINANCIAL ACCOUNTING

losses on the contracts of the lease. The unavoidable lowest total value of meeting the

commitment down the agreement surpass the profitable advantages to be received under it.

The company has not resolute the transition approach to similar for the new accounting standard

(Henderson et.al, 2015). However the company can utilize the complete retrospective approach

or the modified retrospective approach at the time of transition. The impact of transition based on

the complete retrospective approach will be that the lease liability identified on the start off date

of lease is by using rate of interest. However, if the rate cannot be resolute then the rate of

incremental borrowing in used for discounting (Australian Accounting Standards Board, 2016).

The firm have to provide a third income records of monetary position as at the beginning of the

earliest period. This is done to minimum the comparative financial records of the firm (Joubert,

Garvie and Parle, 2017). The impact of transition based on the modified retrospective approach

will be the effective date of the beginning application will be from 1st April 2019 for the financial

year 19-20. The liability of lease is measured at the current worth of the remaining clearance of

lease. The discounting is done in this approach is used by the rate of incremental borrowing. The

right use of asset that have been identified and is valued at an equal amount to the lease liability

and discounted by using rate of incremental borrowing. The difference between the right of

usable asset and the liability of lease is identified in the beginning retained earnings on the initial

application. The Australian Accounting standards Board (AASB) expand, matter and maintains

the accounting standard of Australia involving the interpretation. The accounting standard AASB

117 which is based on the International standard IFRS 117 and is provided by the international

accounting standard board (IASB). This distinguishes among the finance and the operating leases

(Peytcheva, Wright and Majoor 2014). The classification of the particular ease that is it a

financial or an operating is found on the possibility of risk and reward to possession of a leased

asset lie with the lessor or the lessee. However, if it moves substantially the risk and rewards to

the possession from the lessor to lessee then it will be financial otherwise not. According to the

accounting standard AASB 117 the payment of the lease under an operating lease will be

recognized as expenses on the basis of a straight line method (Australian Accounting Standard

Board, 2007). AASB 16 is new accounting standard, which affects the way of operating leases

that are considered on the monetary records of the firm. The procedures and the accounting

systems have been started serving the changes (Hana and Patrik, 2017). This accounting standard

replaces the old standard that is AASB 117. According to the accounting standard AASB 117 the

losses on the contracts of the lease. The unavoidable lowest total value of meeting the

commitment down the agreement surpass the profitable advantages to be received under it.

The company has not resolute the transition approach to similar for the new accounting standard

(Henderson et.al, 2015). However the company can utilize the complete retrospective approach

or the modified retrospective approach at the time of transition. The impact of transition based on

the complete retrospective approach will be that the lease liability identified on the start off date

of lease is by using rate of interest. However, if the rate cannot be resolute then the rate of

incremental borrowing in used for discounting (Australian Accounting Standards Board, 2016).

The firm have to provide a third income records of monetary position as at the beginning of the

earliest period. This is done to minimum the comparative financial records of the firm (Joubert,

Garvie and Parle, 2017). The impact of transition based on the modified retrospective approach

will be the effective date of the beginning application will be from 1st April 2019 for the financial

year 19-20. The liability of lease is measured at the current worth of the remaining clearance of

lease. The discounting is done in this approach is used by the rate of incremental borrowing. The

right use of asset that have been identified and is valued at an equal amount to the lease liability

and discounted by using rate of incremental borrowing. The difference between the right of

usable asset and the liability of lease is identified in the beginning retained earnings on the initial

application. The Australian Accounting standards Board (AASB) expand, matter and maintains

the accounting standard of Australia involving the interpretation. The accounting standard AASB

117 which is based on the International standard IFRS 117 and is provided by the international

accounting standard board (IASB). This distinguishes among the finance and the operating leases

(Peytcheva, Wright and Majoor 2014). The classification of the particular ease that is it a

financial or an operating is found on the possibility of risk and reward to possession of a leased

asset lie with the lessor or the lessee. However, if it moves substantially the risk and rewards to

the possession from the lessor to lessee then it will be financial otherwise not. According to the

accounting standard AASB 117 the payment of the lease under an operating lease will be

recognized as expenses on the basis of a straight line method (Australian Accounting Standard

Board, 2007). AASB 16 is new accounting standard, which affects the way of operating leases

that are considered on the monetary records of the firm. The procedures and the accounting

systems have been started serving the changes (Hana and Patrik, 2017). This accounting standard

replaces the old standard that is AASB 117. According to the accounting standard AASB 117 the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ADVANCE FINANCIAL ACCOUNTING

income statement of company do not require to include the commitment to make future

payments of the firm. This means that the monetary statement prepared by the firm will not be

effective and precisely consider the monetary position of the firm. This new standard have been

introduced by the accounting boards to completely review the firm’s liabilities by giving clarity

of the leasing activities, the financial leverage of a lessee and the employed capital. This new

standard is validate, more precise and understandable monetary statements. This will be very

helpful for the investors, shareholder of the company (Medibank, 2018). This is because they can

compare the financial position of the company’s that borrows to purchase asset among the

companies that lease assets. The business that follows the Australian accounting standards will

be affected by this new standard of accounting. This new standard will have an effect on

company’s who are lessees of assets (Brumm and Liu, 2019). This is mandatory for those who

prepare monetary reports on a general basis. This new standard will be implied on the companies

with a 31st December year end reporting will be commencing on 1st January 2019. The

companies whose year end at 30th June, the first period relevant for them will be from 1st July

2019. The relevant changes are that the companies need to bring the majority of operating leases

on the income statement. The property and the equipment leases that have been identified before

off the balance sheet. This need to be accounted by the company for as a right of use asset

(Altamuro et.al, 2014). The liability of lease that will bring additional lucidity about the lease

obligation of a company. This will led to the changes in the key monetary metrics such as the

gearing ratio, asset turnover and EBITDA. The accounting of the lessor will be unchanged from

the recent leases standard of AASB 117 (IAS 117). The standard AASB 16 establish a single

lessee model of accounting that needs a lessee to identify the assets and liabilities for all the

leases with a term for more than twelve months besides the underlying asset is of low value. The

lessee should identify about utilization of assets and represent the utilization of the underlying

leased asset and a lease liability, which represents its commitment in paying of the lease. AASB

16 includes the revelation of the requirements of the lessees. The lessees will be required to

approach the judgment on deciding among the data and to be relevant the objective of providing

a basis for users of the monetary statement. The lessor need to classify the leases as an operating

lease and financial lease. The lessor also needs to prepare the accounts for this two lease

separately (Barone, Birt and Moya, 2014). According to AASB 16 the lessor need to provide a

detailed disclosure in the report. This will make better the data to be disclosed about the risk

income statement of company do not require to include the commitment to make future

payments of the firm. This means that the monetary statement prepared by the firm will not be

effective and precisely consider the monetary position of the firm. This new standard have been

introduced by the accounting boards to completely review the firm’s liabilities by giving clarity

of the leasing activities, the financial leverage of a lessee and the employed capital. This new

standard is validate, more precise and understandable monetary statements. This will be very

helpful for the investors, shareholder of the company (Medibank, 2018). This is because they can

compare the financial position of the company’s that borrows to purchase asset among the

companies that lease assets. The business that follows the Australian accounting standards will

be affected by this new standard of accounting. This new standard will have an effect on

company’s who are lessees of assets (Brumm and Liu, 2019). This is mandatory for those who

prepare monetary reports on a general basis. This new standard will be implied on the companies

with a 31st December year end reporting will be commencing on 1st January 2019. The

companies whose year end at 30th June, the first period relevant for them will be from 1st July

2019. The relevant changes are that the companies need to bring the majority of operating leases

on the income statement. The property and the equipment leases that have been identified before

off the balance sheet. This need to be accounted by the company for as a right of use asset

(Altamuro et.al, 2014). The liability of lease that will bring additional lucidity about the lease

obligation of a company. This will led to the changes in the key monetary metrics such as the

gearing ratio, asset turnover and EBITDA. The accounting of the lessor will be unchanged from

the recent leases standard of AASB 117 (IAS 117). The standard AASB 16 establish a single

lessee model of accounting that needs a lessee to identify the assets and liabilities for all the

leases with a term for more than twelve months besides the underlying asset is of low value. The

lessee should identify about utilization of assets and represent the utilization of the underlying

leased asset and a lease liability, which represents its commitment in paying of the lease. AASB

16 includes the revelation of the requirements of the lessees. The lessees will be required to

approach the judgment on deciding among the data and to be relevant the objective of providing

a basis for users of the monetary statement. The lessor need to classify the leases as an operating

lease and financial lease. The lessor also needs to prepare the accounts for this two lease

separately (Barone, Birt and Moya, 2014). According to AASB 16 the lessor need to provide a

detailed disclosure in the report. This will make better the data to be disclosed about the risk

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ADVANCE FINANCIAL ACCOUNTING

exposure of the lessor. This recent standard will have a notable affect on the monetary statement

of the company. These changes in the lease standard will led to enlarge the level of complication

and risk in the financial reporting. This new standard will make changes in the outline of

expenditure alternately being as a straight line rental expenditure. The companies after the

implementation of this new standard, may potentially have huge changes in the financial

statement that is required to be explained to the investors and the stakeholder of the company

(Dakis, 2016). This will led to rise in assets and liabilities and decrease in equity of the monetary

records of the entity. The EBITDA and the monetary position of the firm will also increase and

the front end lease expenses and profit before of the company will decrease. The operating cash

flow statement of the firm will also increase and the financing cash flow statement of the firm

will decrease. These effect of may also create future affair with the working capital, bank

covenants, lease agreements and the requirements audit the financial statements. According to

the annual report for the year 2018 the Company has not implemented the changes. The group

has been planning to apply the AASB 16 for the annual period beginning from 1st July 2019. The

group have started to analyze the potential effect on the standard on the monetary records of the

entity based on the recent lease contract of the firm. The group identify the new assets and

liabilities for operating leases of corporate place of work and retail sites of the company. The

nature of expenditure on the leases will also have the relevant changes. This is because the new

accounting standard will take the place of the straight line operating lease expenditure with a

charge of depreciation for the right use of assets. This has been identified that the operating cash

flows will rise under AASB16 the cash paid attributable for the repayment of principal amount

will be involved in monitoring the cash flow. The net rise and fall of the cash and the cash

equivalent balances will be remain same. The group has quantified the impact of AASB 16 that

is based on the recent lease portfolio. The group had not been await a material impact on the

monetary records and income of the firm in the year of application of this recent accounting

standard.

Conclusion

This can be concluded from the above discussion is that Medibank private limited is an

organization that provides physical insurance, travelling insurance, life insurance, animal related

insurance and health management to the people of Australia. The annual report of the firm have

exposure of the lessor. This recent standard will have a notable affect on the monetary statement

of the company. These changes in the lease standard will led to enlarge the level of complication

and risk in the financial reporting. This new standard will make changes in the outline of

expenditure alternately being as a straight line rental expenditure. The companies after the

implementation of this new standard, may potentially have huge changes in the financial

statement that is required to be explained to the investors and the stakeholder of the company

(Dakis, 2016). This will led to rise in assets and liabilities and decrease in equity of the monetary

records of the entity. The EBITDA and the monetary position of the firm will also increase and

the front end lease expenses and profit before of the company will decrease. The operating cash

flow statement of the firm will also increase and the financing cash flow statement of the firm

will decrease. These effect of may also create future affair with the working capital, bank

covenants, lease agreements and the requirements audit the financial statements. According to

the annual report for the year 2018 the Company has not implemented the changes. The group

has been planning to apply the AASB 16 for the annual period beginning from 1st July 2019. The

group have started to analyze the potential effect on the standard on the monetary records of the

entity based on the recent lease contract of the firm. The group identify the new assets and

liabilities for operating leases of corporate place of work and retail sites of the company. The

nature of expenditure on the leases will also have the relevant changes. This is because the new

accounting standard will take the place of the straight line operating lease expenditure with a

charge of depreciation for the right use of assets. This has been identified that the operating cash

flows will rise under AASB16 the cash paid attributable for the repayment of principal amount

will be involved in monitoring the cash flow. The net rise and fall of the cash and the cash

equivalent balances will be remain same. The group has quantified the impact of AASB 16 that

is based on the recent lease portfolio. The group had not been await a material impact on the

monetary records and income of the firm in the year of application of this recent accounting

standard.

Conclusion

This can be concluded from the above discussion is that Medibank private limited is an

organization that provides physical insurance, travelling insurance, life insurance, animal related

insurance and health management to the people of Australia. The annual report of the firm have

8ADVANCE FINANCIAL ACCOUNTING

been analyzed. According to that it have been identified that the company is following the

Australian standard of accounting for preparing the monetary records of the entity. The entity

have followed all the required accounting concepts and standard that are needed to prepare the

monetary statement provided by the company. The annual report that have been analyzed is for

the year 2018 the financial statements have not been affected for the recent accounting standard.

The new standard ASSB 16 that have been introduced by the Australian accounting standard

board will be adopted by the company for the financial year 2019-2020. This recent standard of

accounting for lease AASB 16 have been replaced AASB 117. The new accounting standard that

have been introduced has a better understanding and replaces the disadvantages of the previous

accounting standard for the lease. The other benefits are that the quality and the comparability of

the monetary statements for the companies will improve. The utilizers of the annual report can

compare the reports of the company and can do a better analysis. The identification of all the

assets and liabilities for all the leases is also improves. The company have analyzed the relevant

changes and the relevant impacts for the new accounting standard. The company have not

planned for any transitional approach for the recent accounting standard that have been

introduced by the Australian accounting standard board.

been analyzed. According to that it have been identified that the company is following the

Australian standard of accounting for preparing the monetary records of the entity. The entity

have followed all the required accounting concepts and standard that are needed to prepare the

monetary statement provided by the company. The annual report that have been analyzed is for

the year 2018 the financial statements have not been affected for the recent accounting standard.

The new standard ASSB 16 that have been introduced by the Australian accounting standard

board will be adopted by the company for the financial year 2019-2020. This recent standard of

accounting for lease AASB 16 have been replaced AASB 117. The new accounting standard that

have been introduced has a better understanding and replaces the disadvantages of the previous

accounting standard for the lease. The other benefits are that the quality and the comparability of

the monetary statements for the companies will improve. The utilizers of the annual report can

compare the reports of the company and can do a better analysis. The identification of all the

assets and liabilities for all the leases is also improves. The company have analyzed the relevant

changes and the relevant impacts for the new accounting standard. The company have not

planned for any transitional approach for the recent accounting standard that have been

introduced by the Australian accounting standard board.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ADVANCE FINANCIAL ACCOUNTING

References

Altamuro, J., Johnston, R., Pandit, S. and Zhang, H., 2014. Operating leases and credit

assessments. Contemporary Accounting Research, 31(2), pp.551-580.

Australian Accounting Standard Board, 2007. AASB117. [ebook] Australia: Australian

Accounting Standard Board. Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB117_07-04_COMPapr07_07-07.pdf

[Accessed 19 Sep. 2019].

Australian Accounting Standards Board, 2016. AASB 16. [ebook] Australia: Australian

Accounting Standards Board, p.67. Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB16_02-16.pdf [Accessed 19 Sep.

2019].

Barone, E., Birt, J. and Moya, S., 2014. Lease accounting: A review of recent

literature. Accounting in Europe, 11(1), pp.35-54.

Brumm, L. and Liu, J., 2019. New leasing accounting standard. Taxation in Australia, 53(8),

p.449.

Bugeja, M., Czernkowski, R. and Moran, D., 2015. The impact of the management approach on

segment reporting. Journal of Business Finance & Accounting, 42(3-4), pp.310-366.

Cotten, B., Schneider, D.K. and McCarthy, M.G., 2013. Capitalisation of operating leases and

credit ratings. Journal of Applied Research in Accounting and Finance (JARAF), 8(1).

Dakis, G.S., 2016. Upcoming changes to contributions and leasing standards. Governance

Directions, 68(2), p.99.

Hana, B. and Patrik, S., 2017. Will the amendments to the IAS 16 and IAS 41 influence the value

of biological assets?. Agricultural Economics, 63(2), pp.53-64.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial accounting.

Pearson Higher Education AU.

References

Altamuro, J., Johnston, R., Pandit, S. and Zhang, H., 2014. Operating leases and credit

assessments. Contemporary Accounting Research, 31(2), pp.551-580.

Australian Accounting Standard Board, 2007. AASB117. [ebook] Australia: Australian

Accounting Standard Board. Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB117_07-04_COMPapr07_07-07.pdf

[Accessed 19 Sep. 2019].

Australian Accounting Standards Board, 2016. AASB 16. [ebook] Australia: Australian

Accounting Standards Board, p.67. Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB16_02-16.pdf [Accessed 19 Sep.

2019].

Barone, E., Birt, J. and Moya, S., 2014. Lease accounting: A review of recent

literature. Accounting in Europe, 11(1), pp.35-54.

Brumm, L. and Liu, J., 2019. New leasing accounting standard. Taxation in Australia, 53(8),

p.449.

Bugeja, M., Czernkowski, R. and Moran, D., 2015. The impact of the management approach on

segment reporting. Journal of Business Finance & Accounting, 42(3-4), pp.310-366.

Cotten, B., Schneider, D.K. and McCarthy, M.G., 2013. Capitalisation of operating leases and

credit ratings. Journal of Applied Research in Accounting and Finance (JARAF), 8(1).

Dakis, G.S., 2016. Upcoming changes to contributions and leasing standards. Governance

Directions, 68(2), p.99.

Hana, B. and Patrik, S., 2017. Will the amendments to the IAS 16 and IAS 41 influence the value

of biological assets?. Agricultural Economics, 63(2), pp.53-64.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial accounting.

Pearson Higher Education AU.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ADVANCE FINANCIAL ACCOUNTING

Joubert, M., Garvie, L. and Parle, G., 2017. Implications of the New Accounting Standard for

Leases AASB 16 (IFRS 16) with the Inclusion of Operating Leases in the Balance Sheet. The

Journal of New Business Ideas & Trends, 15(2), pp.1-11.

Medibank, 2018. Annual report 2018. [ebook] Australia: Medibank, p.136. Available at:

https://www.medibank.com.au/content/dam/retail/about-assets/pdfs/investor-centre/annual-

reports/Medibank_Annual_Report_2018.pdf [Accessed 19 Sep. 2019].

Medibank, 2019. Medibank Private Health Insurance | For Better Health | Medibank. [online]

Medibank. Available at: https://www.medibank.com.au/ [Accessed 19 Sep. 2019].

Öztürk, M. and Serçemeli, M., 2016. Impact of New Standard" IFRS 16 Leases" on Statement of

Financial Position and Key Ratios: A Case Study on an Airline Company in Turkey. Business

and Economics Research Journal, 7(4), p.143.Brown, A.M., 2016. The financial milieu of the

IASB and AASB. Australian Accounting Review, 16(38), pp.85-95.

Parker, R.H. ed., 2013. Accounting in Australia (RLE Accounting): Historical Essays. Routledge.

Peytcheva, M., Wright, A.M. and Majoor, B., 2014. The impact of principles-based versus rules-

based accounting standards on auditors' motivations and evidence demands. Behavioral

Research in Accounting, 26(2), pp.51-72.

Wong, K. and Joshi, M., 2015. The impact of lease capitalisation on financial statements and key

ratios: Evidence from Australia. Australasian Accounting, Business and Finance Journal, 9(3),

pp.27-44.

www.aasb.gov.au 2019. Australian Accounting Standards Board (AASB) - Home. [online]

Aasb.gov.au. Available at: https://www.aasb.gov.au/ [Accessed 12 Sep. 2019].

Xu, W., Davidson, R.A. and Cheong, C.S., 2017. Converting financial statements: operating to

capitalised leases. Pacific accounting review, 29(1), pp.34-54.

Joubert, M., Garvie, L. and Parle, G., 2017. Implications of the New Accounting Standard for

Leases AASB 16 (IFRS 16) with the Inclusion of Operating Leases in the Balance Sheet. The

Journal of New Business Ideas & Trends, 15(2), pp.1-11.

Medibank, 2018. Annual report 2018. [ebook] Australia: Medibank, p.136. Available at:

https://www.medibank.com.au/content/dam/retail/about-assets/pdfs/investor-centre/annual-

reports/Medibank_Annual_Report_2018.pdf [Accessed 19 Sep. 2019].

Medibank, 2019. Medibank Private Health Insurance | For Better Health | Medibank. [online]

Medibank. Available at: https://www.medibank.com.au/ [Accessed 19 Sep. 2019].

Öztürk, M. and Serçemeli, M., 2016. Impact of New Standard" IFRS 16 Leases" on Statement of

Financial Position and Key Ratios: A Case Study on an Airline Company in Turkey. Business

and Economics Research Journal, 7(4), p.143.Brown, A.M., 2016. The financial milieu of the

IASB and AASB. Australian Accounting Review, 16(38), pp.85-95.

Parker, R.H. ed., 2013. Accounting in Australia (RLE Accounting): Historical Essays. Routledge.

Peytcheva, M., Wright, A.M. and Majoor, B., 2014. The impact of principles-based versus rules-

based accounting standards on auditors' motivations and evidence demands. Behavioral

Research in Accounting, 26(2), pp.51-72.

Wong, K. and Joshi, M., 2015. The impact of lease capitalisation on financial statements and key

ratios: Evidence from Australia. Australasian Accounting, Business and Finance Journal, 9(3),

pp.27-44.

www.aasb.gov.au 2019. Australian Accounting Standards Board (AASB) - Home. [online]

Aasb.gov.au. Available at: https://www.aasb.gov.au/ [Accessed 12 Sep. 2019].

Xu, W., Davidson, R.A. and Cheong, C.S., 2017. Converting financial statements: operating to

capitalised leases. Pacific accounting review, 29(1), pp.34-54.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.