Medibank & Conceptual Accounting Framework: A Compliance Report

VerifiedAdded on 2023/06/13

|14

|2803

|187

Report

AI Summary

This report provides a critical analysis of Medibank, an ASX Top 100 listed company, and its effectiveness in meeting the obligations of the accounting conceptual framework. It addresses the conceptual framework's objectives, recognition criteria for assets, liabilities, revenues, equity, and expenses, and qualitative aspects such as relevance, verifiability, timeliness, comparability, understandability, and faithful representation. The analysis considers Medibank's adherence to Australian Accounting Standards Board (AASB) regulations and the Corporations Act 2001. The report highlights areas where Medibank complies with the framework and identifies potential issues, such as disclosures related to health benefits fund acts and control over assets and liabilities. It also discusses the company's revenue recognition, expense realization, and equity segmentation. The audit report of Ernst and Young indicates that the financial statements of the corporate firm are represented faithfully that compiles with all the required accounting standards.

Running head: CONTEMPORARY ISSUES IN ACCOUNTING

Contemporary Issues in Accounting

Name of the University:

Name of the Student:

Authors Note:

Contemporary Issues in Accounting

Name of the University:

Name of the Student:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CONTEMPORARY ISSUES IN ACCOUNTING

Table of Contents

1. Introduction:....................................................................................................................2

2. Addressing conceptual framework objectives:................................................................2

3. Addressing conceptual framework-based recognition criteria:.......................................4

3.1. Assets........................................................................................................................4

3.2. Expenses...................................................................................................................5

3.3. Revenues...................................................................................................................6

3.4. Liabilities..................................................................................................................6

3.5. Equity........................................................................................................................7

4. Addressing qualitative aspects of conceptual framework:..............................................7

4.1. Relevance..................................................................................................................7

4.2. Verifiability...............................................................................................................8

4.3. Timeliness.................................................................................................................8

4.4. Comparability...........................................................................................................8

4.5. Understandability......................................................................................................9

4.6. Faithful Representation.............................................................................................9

5. Conclusion:......................................................................................................................9

References..........................................................................................................................11

Table of Contents

1. Introduction:....................................................................................................................2

2. Addressing conceptual framework objectives:................................................................2

3. Addressing conceptual framework-based recognition criteria:.......................................4

3.1. Assets........................................................................................................................4

3.2. Expenses...................................................................................................................5

3.3. Revenues...................................................................................................................6

3.4. Liabilities..................................................................................................................6

3.5. Equity........................................................................................................................7

4. Addressing qualitative aspects of conceptual framework:..............................................7

4.1. Relevance..................................................................................................................7

4.2. Verifiability...............................................................................................................8

4.3. Timeliness.................................................................................................................8

4.4. Comparability...........................................................................................................8

4.5. Understandability......................................................................................................9

4.6. Faithful Representation.............................................................................................9

5. Conclusion:......................................................................................................................9

References..........................................................................................................................11

2CONTEMPORARY ISSUES IN ACCOUNTING

1. Introduction:

In recent business surrounding, relevance of the conceptual framework in financial

reporting of the companies is necessary for financial statements preparation. The companies are

offered with all important action course in alignment with doctrines and techniques needed for

financial statements preparation (Bamber and McMeeking 2016). Along with that with the help

of the doctrines and techniques of the conception of the conceptual framework, it is possible to

deal with various business concerns. This also validates that the functions of the conceptual

framework are considered in the context of the financial activities of the business companies.

Considering the same, IASB (International Accounting Standards Board) has introduced such

framework for effective financial reporting purposes.

For this reason, the report is intended to analyze the compliance with criteria of

objectives, recognition along with qualitative aspects of conceptual framework on the behalf of

the organizations (Brusca and Martínez 2016). The organization that is selected within the report

is Medibank that is listed within top 100 listed ASX companies. Medibank is positioned as a

renowned health insurer that has more than 40 years of experience to offer health cover needs to

more than 3.7 million consumers by means of Medibank services such as ahm brands and life

insurance.

2. Addressing conceptual framework objectives:

It is gathered that financial reporting based conceptual framework is an important

requirement for financial management of the business companies. All the vital information is

present within the annual report of Medibank Company regarding the compliance with various

1. Introduction:

In recent business surrounding, relevance of the conceptual framework in financial

reporting of the companies is necessary for financial statements preparation. The companies are

offered with all important action course in alignment with doctrines and techniques needed for

financial statements preparation (Bamber and McMeeking 2016). Along with that with the help

of the doctrines and techniques of the conception of the conceptual framework, it is possible to

deal with various business concerns. This also validates that the functions of the conceptual

framework are considered in the context of the financial activities of the business companies.

Considering the same, IASB (International Accounting Standards Board) has introduced such

framework for effective financial reporting purposes.

For this reason, the report is intended to analyze the compliance with criteria of

objectives, recognition along with qualitative aspects of conceptual framework on the behalf of

the organizations (Brusca and Martínez 2016). The organization that is selected within the report

is Medibank that is listed within top 100 listed ASX companies. Medibank is positioned as a

renowned health insurer that has more than 40 years of experience to offer health cover needs to

more than 3.7 million consumers by means of Medibank services such as ahm brands and life

insurance.

2. Addressing conceptual framework objectives:

It is gathered that financial reporting based conceptual framework is an important

requirement for financial management of the business companies. All the vital information is

present within the annual report of Medibank Company regarding the compliance with various

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CONTEMPORARY ISSUES IN ACCOUNTING

aspects mentioned within the financial reporting conceptual framework (Bryce, Ali and Mather

2015). This is the reason for which all the corporate organizations totally comply with the norms

set by the conceptual framework of IFRS for better financial reporting. However, this framework

is deemed to have three specific objectives and it is vital for Medibank Company to satisfy all of

them. The 2017 annual report of Medibank indicates that all the doctrines along with regulations

of the “Corporations Act 2001’ and “Australian Accounting Standards Board (AASB)” are

implemented within general purpose financial reporting.

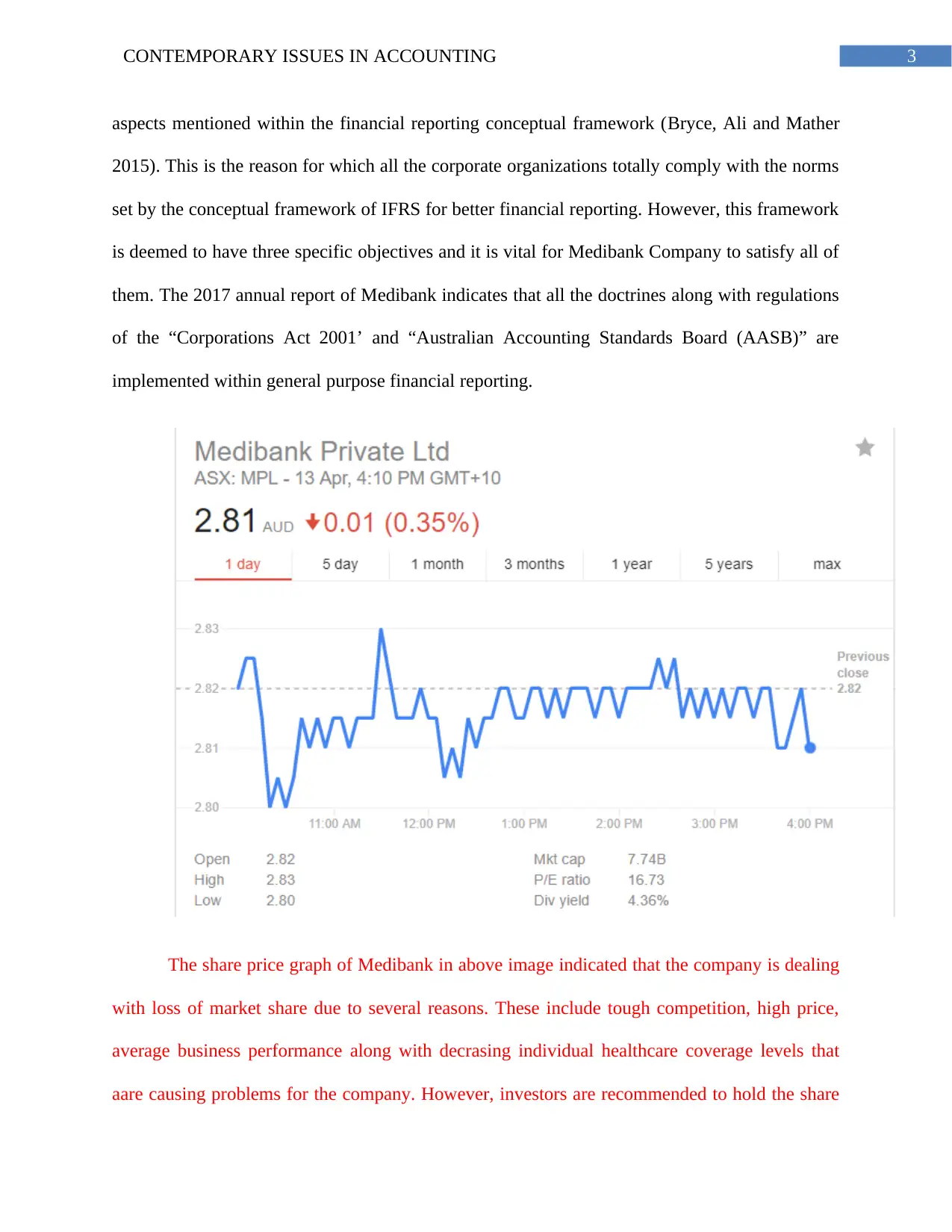

The share price graph of Medibank in above image indicated that the company is dealing

with loss of market share due to several reasons. These include tough competition, high price,

average business performance along with decrasing individual healthcare coverage levels that

aare causing problems for the company. However, investors are recommended to hold the share

aspects mentioned within the financial reporting conceptual framework (Bryce, Ali and Mather

2015). This is the reason for which all the corporate organizations totally comply with the norms

set by the conceptual framework of IFRS for better financial reporting. However, this framework

is deemed to have three specific objectives and it is vital for Medibank Company to satisfy all of

them. The 2017 annual report of Medibank indicates that all the doctrines along with regulations

of the “Corporations Act 2001’ and “Australian Accounting Standards Board (AASB)” are

implemented within general purpose financial reporting.

The share price graph of Medibank in above image indicated that the company is dealing

with loss of market share due to several reasons. These include tough competition, high price,

average business performance along with decrasing individual healthcare coverage levels that

aare causing problems for the company. However, investors are recommended to hold the share

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CONTEMPORARY ISSUES IN ACCOUNTING

of Medibank in the long term as government legislated boots in premium per year that causes

revenue of the organization to maintain its market share. There are three objectives based on

which a company can abide by the conceptual financial reporting framework that are explained

below:

Offering Helpful Financial Information

Based on the conceptual framework it can be stated that all the companies are responsible

for offering meaningful and valuable financial information to its investors that can facilitate them

in better decision making (Camfferman and Zeff 2015). Through analyzing the annual report of

Medibank Company, it is gathered that vital information is offered to its investors through timely

publishing financial statements. The financial statements of all the listed companies in Australian

stock exchange must include the balance sheet statement along with the cash flow statements in

its finical statements. Along with the same, accounting notes are explained within the annual

report that facilitates the users in gathering necessary information.

Evaluating Amount, Uncertainties and Timing

Another conceptual framework objective is that all the companies is responsible for

offering important and reliable financial information to its investors in analyzing amount, timing

along with uncertainties related with the company’s cash flow position (Di Pietr, Ay, Art and

Ronen 2016). Evaluation of the annual report of Medibank validates the company’s statement of

cash flow in a timely manner and it offers important information to the investors related with the

financial statements.

Organizational Resource Based Information

of Medibank in the long term as government legislated boots in premium per year that causes

revenue of the organization to maintain its market share. There are three objectives based on

which a company can abide by the conceptual financial reporting framework that are explained

below:

Offering Helpful Financial Information

Based on the conceptual framework it can be stated that all the companies are responsible

for offering meaningful and valuable financial information to its investors that can facilitate them

in better decision making (Camfferman and Zeff 2015). Through analyzing the annual report of

Medibank Company, it is gathered that vital information is offered to its investors through timely

publishing financial statements. The financial statements of all the listed companies in Australian

stock exchange must include the balance sheet statement along with the cash flow statements in

its finical statements. Along with the same, accounting notes are explained within the annual

report that facilitates the users in gathering necessary information.

Evaluating Amount, Uncertainties and Timing

Another conceptual framework objective is that all the companies is responsible for

offering important and reliable financial information to its investors in analyzing amount, timing

along with uncertainties related with the company’s cash flow position (Di Pietr, Ay, Art and

Ronen 2016). Evaluation of the annual report of Medibank validates the company’s statement of

cash flow in a timely manner and it offers important information to the investors related with the

financial statements.

Organizational Resource Based Information

5CONTEMPORARY ISSUES IN ACCOUNTING

As per the third objective of financial reporting conceptual framework, companies require

reporting all important information concerning its resources that assists Medibank Company’s

process of financial decision making. Medibank Company develops its financial position

statement in a manner so that it is in adherence with the AASB regulations (Henderson, Peirson,

Herbohn, and Howieson 2015). The company also offers important information concerning

economic resources is disclosed.

3. Addressing conceptual framework-based recognition criteria:

It is necessitated by the financial reporting conceptual framework that all the corporate

organizations must address the criteria of recognition that is related with the assets, liabilities,

revenues, equity as well as expenses. In addition to that, it also requires to company with three

major needs (James and Prout 2015). The first need is focused on the financial factors that is to

be represented with important information. The second requirement necessitates ensuring faithful

representation of all the financial factors. Finally, the requirement is related with such factors

those are advantageous for the company’s investors. The evaluation carried out in this section

will indicate representation of recognition criteria fulfillment on the behalf of the Medibank

Company.

3.1. Assets

A company is considered to attain different asset groups. In consideration to the property,

plant and equipment aspect it us disclosed through deducting depreciation from the expenses of

assets. The expenses associated with these assets are realized in a situation where the future

advantages are transferred within the company (Junior, Best and Cotter 2014). For the intangible

assets maintained by the company, impairment is observed to be imposed on it. Realization of

As per the third objective of financial reporting conceptual framework, companies require

reporting all important information concerning its resources that assists Medibank Company’s

process of financial decision making. Medibank Company develops its financial position

statement in a manner so that it is in adherence with the AASB regulations (Henderson, Peirson,

Herbohn, and Howieson 2015). The company also offers important information concerning

economic resources is disclosed.

3. Addressing conceptual framework-based recognition criteria:

It is necessitated by the financial reporting conceptual framework that all the corporate

organizations must address the criteria of recognition that is related with the assets, liabilities,

revenues, equity as well as expenses. In addition to that, it also requires to company with three

major needs (James and Prout 2015). The first need is focused on the financial factors that is to

be represented with important information. The second requirement necessitates ensuring faithful

representation of all the financial factors. Finally, the requirement is related with such factors

those are advantageous for the company’s investors. The evaluation carried out in this section

will indicate representation of recognition criteria fulfillment on the behalf of the Medibank

Company.

3.1. Assets

A company is considered to attain different asset groups. In consideration to the property,

plant and equipment aspect it us disclosed through deducting depreciation from the expenses of

assets. The expenses associated with these assets are realized in a situation where the future

advantages are transferred within the company (Junior, Best and Cotter 2014). For the intangible

assets maintained by the company, impairment is observed to be imposed on it. Realization of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CONTEMPORARY ISSUES IN ACCOUNTING

the impairment loss is conducted on the carrying amount of such certain asset classes mentioned

within the financial statements of the company. In case of Medibank Company, there are specific

useful lives for all the tangible assets and for such reasons no amortization is deemed to be

applicable on them (James and Prout 2015). Certain issues have been faced by the company in

maintaining compliance with the division 131 of health benefits fund act that did not consider

disclosing any relevant information about benefits in addition to those payable within public

hospital cover. This also did not cover regaining the ways in which the company maintains

adequate control over all its assets in its custody.

3.2. Expenses

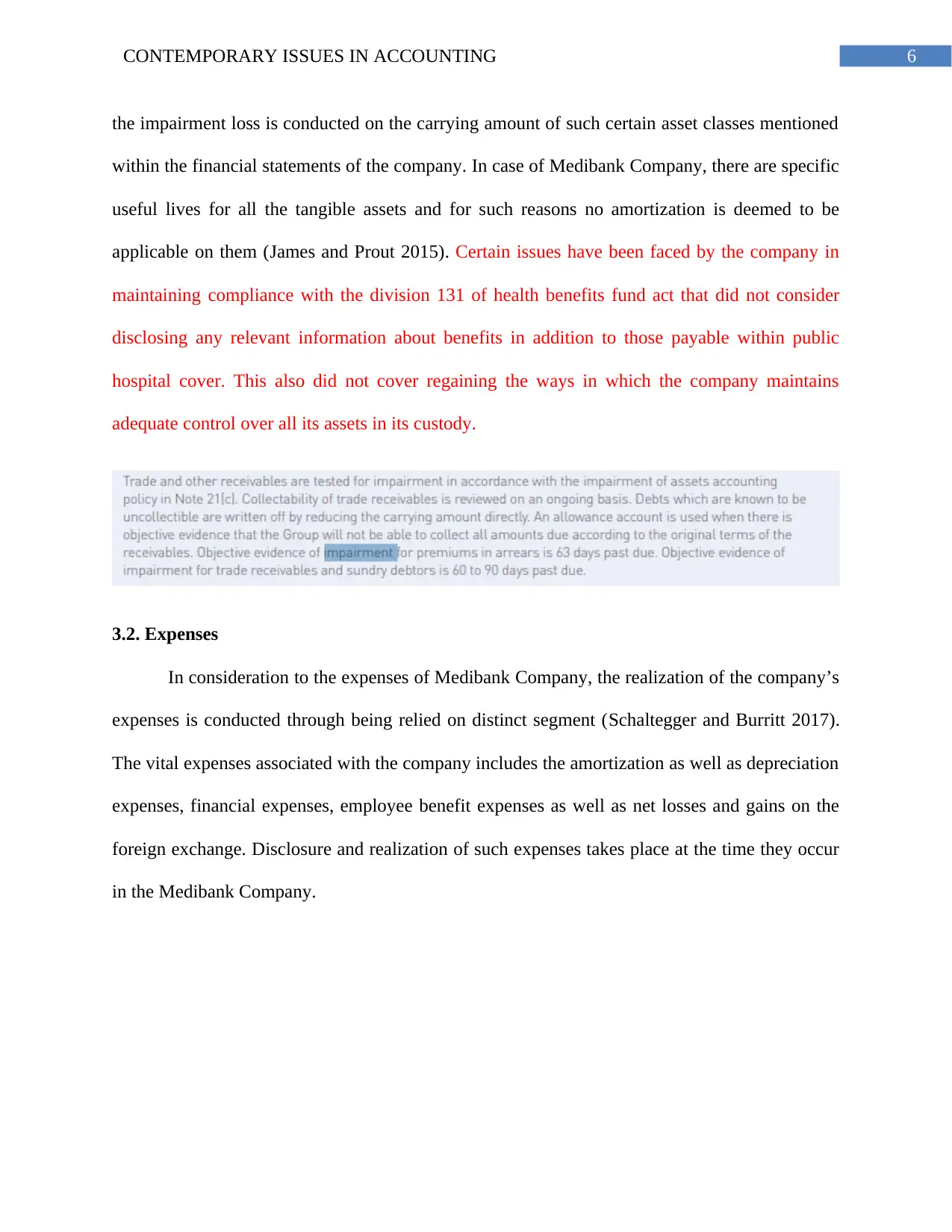

In consideration to the expenses of Medibank Company, the realization of the company’s

expenses is conducted through being relied on distinct segment (Schaltegger and Burritt 2017).

The vital expenses associated with the company includes the amortization as well as depreciation

expenses, financial expenses, employee benefit expenses as well as net losses and gains on the

foreign exchange. Disclosure and realization of such expenses takes place at the time they occur

in the Medibank Company.

the impairment loss is conducted on the carrying amount of such certain asset classes mentioned

within the financial statements of the company. In case of Medibank Company, there are specific

useful lives for all the tangible assets and for such reasons no amortization is deemed to be

applicable on them (James and Prout 2015). Certain issues have been faced by the company in

maintaining compliance with the division 131 of health benefits fund act that did not consider

disclosing any relevant information about benefits in addition to those payable within public

hospital cover. This also did not cover regaining the ways in which the company maintains

adequate control over all its assets in its custody.

3.2. Expenses

In consideration to the expenses of Medibank Company, the realization of the company’s

expenses is conducted through being relied on distinct segment (Schaltegger and Burritt 2017).

The vital expenses associated with the company includes the amortization as well as depreciation

expenses, financial expenses, employee benefit expenses as well as net losses and gains on the

foreign exchange. Disclosure and realization of such expenses takes place at the time they occur

in the Medibank Company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CONTEMPORARY ISSUES IN ACCOUNTING

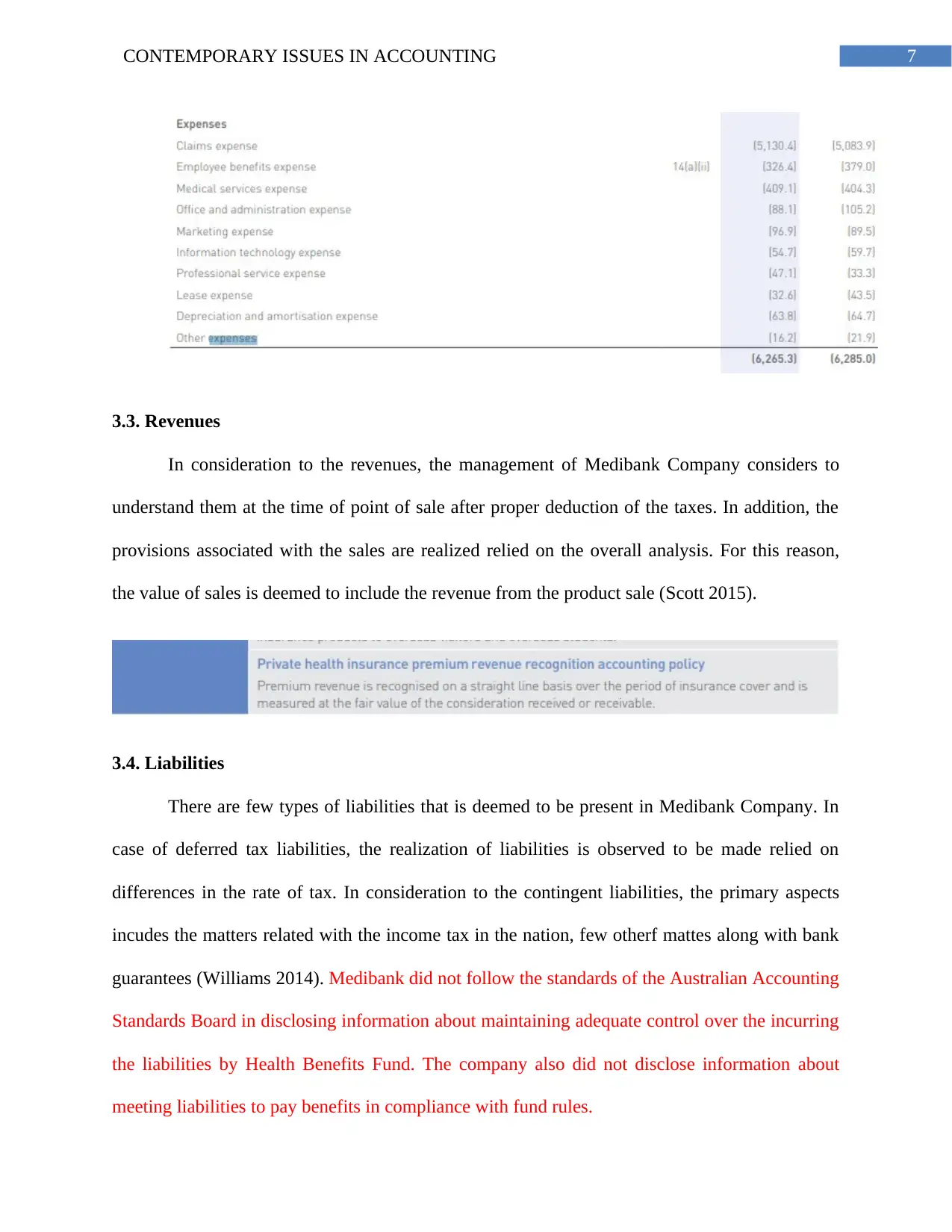

3.3. Revenues

In consideration to the revenues, the management of Medibank Company considers to

understand them at the time of point of sale after proper deduction of the taxes. In addition, the

provisions associated with the sales are realized relied on the overall analysis. For this reason,

the value of sales is deemed to include the revenue from the product sale (Scott 2015).

3.4. Liabilities

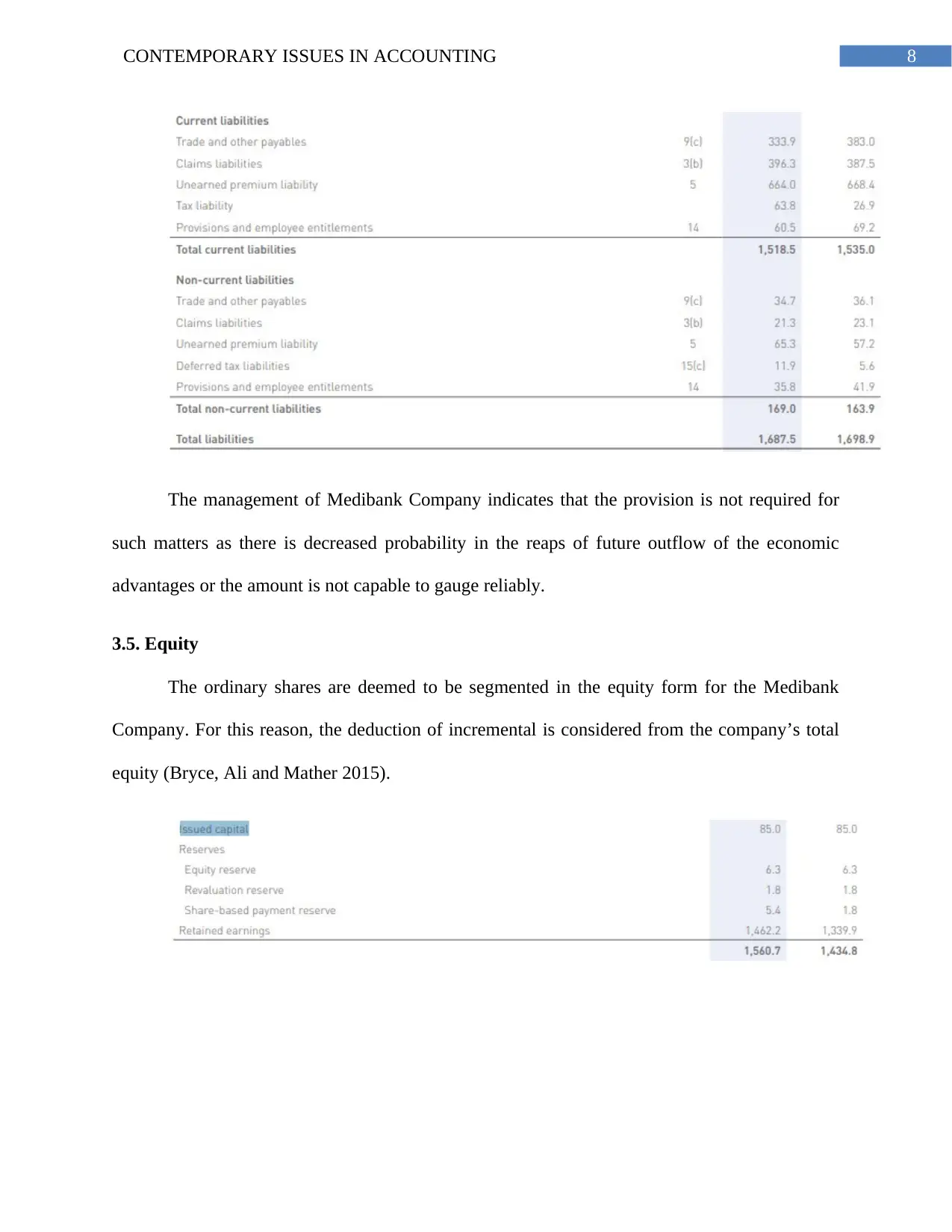

There are few types of liabilities that is deemed to be present in Medibank Company. In

case of deferred tax liabilities, the realization of liabilities is observed to be made relied on

differences in the rate of tax. In consideration to the contingent liabilities, the primary aspects

incudes the matters related with the income tax in the nation, few otherf mattes along with bank

guarantees (Williams 2014). Medibank did not follow the standards of the Australian Accounting

Standards Board in disclosing information about maintaining adequate control over the incurring

the liabilities by Health Benefits Fund. The company also did not disclose information about

meeting liabilities to pay benefits in compliance with fund rules.

3.3. Revenues

In consideration to the revenues, the management of Medibank Company considers to

understand them at the time of point of sale after proper deduction of the taxes. In addition, the

provisions associated with the sales are realized relied on the overall analysis. For this reason,

the value of sales is deemed to include the revenue from the product sale (Scott 2015).

3.4. Liabilities

There are few types of liabilities that is deemed to be present in Medibank Company. In

case of deferred tax liabilities, the realization of liabilities is observed to be made relied on

differences in the rate of tax. In consideration to the contingent liabilities, the primary aspects

incudes the matters related with the income tax in the nation, few otherf mattes along with bank

guarantees (Williams 2014). Medibank did not follow the standards of the Australian Accounting

Standards Board in disclosing information about maintaining adequate control over the incurring

the liabilities by Health Benefits Fund. The company also did not disclose information about

meeting liabilities to pay benefits in compliance with fund rules.

8CONTEMPORARY ISSUES IN ACCOUNTING

The management of Medibank Company indicates that the provision is not required for

such matters as there is decreased probability in the reaps of future outflow of the economic

advantages or the amount is not capable to gauge reliably.

3.5. Equity

The ordinary shares are deemed to be segmented in the equity form for the Medibank

Company. For this reason, the deduction of incremental is considered from the company’s total

equity (Bryce, Ali and Mather 2015).

The management of Medibank Company indicates that the provision is not required for

such matters as there is decreased probability in the reaps of future outflow of the economic

advantages or the amount is not capable to gauge reliably.

3.5. Equity

The ordinary shares are deemed to be segmented in the equity form for the Medibank

Company. For this reason, the deduction of incremental is considered from the company’s total

equity (Bryce, Ali and Mather 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CONTEMPORARY ISSUES IN ACCOUNTING

4. Addressing qualitative aspects of conceptual framework:

Different qualitative characteristics related with the financial reporting conceptual

framework are there for enhancing the overall quality associated with the company’s financial

reporting. It is vital for Medibank Company in addressing al the qualitative characteristics. The

below-stated explanation indicates the extent of conformance with these qualitative features of

the financial reporting conceptual framework on the behalf of the company.

4.1. Relevance

This aspect indicates that relevance must be signified in the company’s financial

statements that can facilitate effective decision making of the company’s investors. Medibank

Company remains aligned with all the recent doctrines and regulations elated to AASB, IFRS

along with Corporations Act 2001 (Bryce, Ali and Mather 2015). In addition to the same, the

company also considers the present rates that is associated with depreciation, tax and few more

aspects. For this reason, the disclosed financial information within the yearly report of Medibank

Company is important for effective investment decisions.

4.2. Verifiability

This factor indicates that the investors of the financial reports are needed to be able to

verify all the reported financial statements on the part of the company. In order to address the

same purpose, Medibank Company offers the segmentation of all the accounting aspects within

the notes of its financial statements (James and Prout 2015).

4.3. Timeliness

This factor indicates that financial information requires to be offered in this particular

schedule. For Medibank Company it is also been observed that the company represents all its

4. Addressing qualitative aspects of conceptual framework:

Different qualitative characteristics related with the financial reporting conceptual

framework are there for enhancing the overall quality associated with the company’s financial

reporting. It is vital for Medibank Company in addressing al the qualitative characteristics. The

below-stated explanation indicates the extent of conformance with these qualitative features of

the financial reporting conceptual framework on the behalf of the company.

4.1. Relevance

This aspect indicates that relevance must be signified in the company’s financial

statements that can facilitate effective decision making of the company’s investors. Medibank

Company remains aligned with all the recent doctrines and regulations elated to AASB, IFRS

along with Corporations Act 2001 (Bryce, Ali and Mather 2015). In addition to the same, the

company also considers the present rates that is associated with depreciation, tax and few more

aspects. For this reason, the disclosed financial information within the yearly report of Medibank

Company is important for effective investment decisions.

4.2. Verifiability

This factor indicates that the investors of the financial reports are needed to be able to

verify all the reported financial statements on the part of the company. In order to address the

same purpose, Medibank Company offers the segmentation of all the accounting aspects within

the notes of its financial statements (James and Prout 2015).

4.3. Timeliness

This factor indicates that financial information requires to be offered in this particular

schedule. For Medibank Company it is also been observed that the company represents all its

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CONTEMPORARY ISSUES IN ACCOUNTING

financial statements within a decided timeframe to all its investors to take effective investment

decision (Bryce, Ali and Mather 2015).

4.4. Comparability

With the support of this particular part of the financial reporting conceptual framework,

the stakeholders are capable to obtain a viewpoint regarding the differences and similarities

within the provided financial information among district financial statements. It is highly

important to explain that Medibank Company has represented its financial position statements in

graphical manner and through tables (James and Prout 2015). This can facilitate its investors to

understand financial position of the company in a clarified manner. For this reason, the investors

and the creditors might compare the financial situation and performance of Medibank Company

with its competitors in the industry.

4.5. Understandability

In adherence to this feature, the corporate organizations are required to disclosure their

financial information in a way that becomes simple for all its investors to analyze their financial

statements. Medibank Company discloses all its financial statements in definite format for better

understanding for its investors.

4.6. Faithful Representation

Relied on this aspect, it ca be indicated that it is vital for all the corporate organizations to

report their financial statements in a transparent and fair manner. This also indicates that

attaining the trust of all its stakeholders is of great relevance (Bryce, Ali and Mather 2015). As

per analysis of the audit report of Ernst and Young, the financial statements of the corporate firm

are represented faithfully that compiles with all the required accounting standards. Portfolio

financial statements within a decided timeframe to all its investors to take effective investment

decision (Bryce, Ali and Mather 2015).

4.4. Comparability

With the support of this particular part of the financial reporting conceptual framework,

the stakeholders are capable to obtain a viewpoint regarding the differences and similarities

within the provided financial information among district financial statements. It is highly

important to explain that Medibank Company has represented its financial position statements in

graphical manner and through tables (James and Prout 2015). This can facilitate its investors to

understand financial position of the company in a clarified manner. For this reason, the investors

and the creditors might compare the financial situation and performance of Medibank Company

with its competitors in the industry.

4.5. Understandability

In adherence to this feature, the corporate organizations are required to disclosure their

financial information in a way that becomes simple for all its investors to analyze their financial

statements. Medibank Company discloses all its financial statements in definite format for better

understanding for its investors.

4.6. Faithful Representation

Relied on this aspect, it ca be indicated that it is vital for all the corporate organizations to

report their financial statements in a transparent and fair manner. This also indicates that

attaining the trust of all its stakeholders is of great relevance (Bryce, Ali and Mather 2015). As

per analysis of the audit report of Ernst and Young, the financial statements of the corporate firm

are represented faithfully that compiles with all the required accounting standards. Portfolio

11CONTEMPORARY ISSUES IN ACCOUNTING

offers liquidity to cover the insurance liabilities associated with health insurance businesses.

Moreover, in such scenario, non-compliance with the faithful representation of extraordinary

items, revaluation of plant, property and equipment and valuation of inventories is observed in

case of Medibank Company. For this reason, it could also be revealed that Medibank Company

has not represented its financial statements faithfully and adequately.

5. Conclusion:

The report is intended to analyze the compliance with criteria of objectives, recognition

along with qualitative aspects of conceptual framework on the behalf of the organizations. It is

gathered from the paper that All the vital information is present within the annual report of

Medibank Company regarding the compliance with various aspects mentioned within the

financial reporting conceptual framework. Moreover, through analyzing the annual report of

Medibank Company, it is gathered that vital information is offered to its investors through timely

publishing financial statements. It is also gathered that another conceptual framework objective

is that all the companies is responsible for offering important and reliable financial information

to its investors. This is ensured by Medibank to analyze amount, timing along with uncertainties

related with the company’s cash flow position.

offers liquidity to cover the insurance liabilities associated with health insurance businesses.

Moreover, in such scenario, non-compliance with the faithful representation of extraordinary

items, revaluation of plant, property and equipment and valuation of inventories is observed in

case of Medibank Company. For this reason, it could also be revealed that Medibank Company

has not represented its financial statements faithfully and adequately.

5. Conclusion:

The report is intended to analyze the compliance with criteria of objectives, recognition

along with qualitative aspects of conceptual framework on the behalf of the organizations. It is

gathered from the paper that All the vital information is present within the annual report of

Medibank Company regarding the compliance with various aspects mentioned within the

financial reporting conceptual framework. Moreover, through analyzing the annual report of

Medibank Company, it is gathered that vital information is offered to its investors through timely

publishing financial statements. It is also gathered that another conceptual framework objective

is that all the companies is responsible for offering important and reliable financial information

to its investors. This is ensured by Medibank to analyze amount, timing along with uncertainties

related with the company’s cash flow position.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.