Auditing Theory: Medibank Risk Analysis and Financial Ratio Comparison

VerifiedAdded on 2020/05/28

|13

|2312

|312

Report

AI Summary

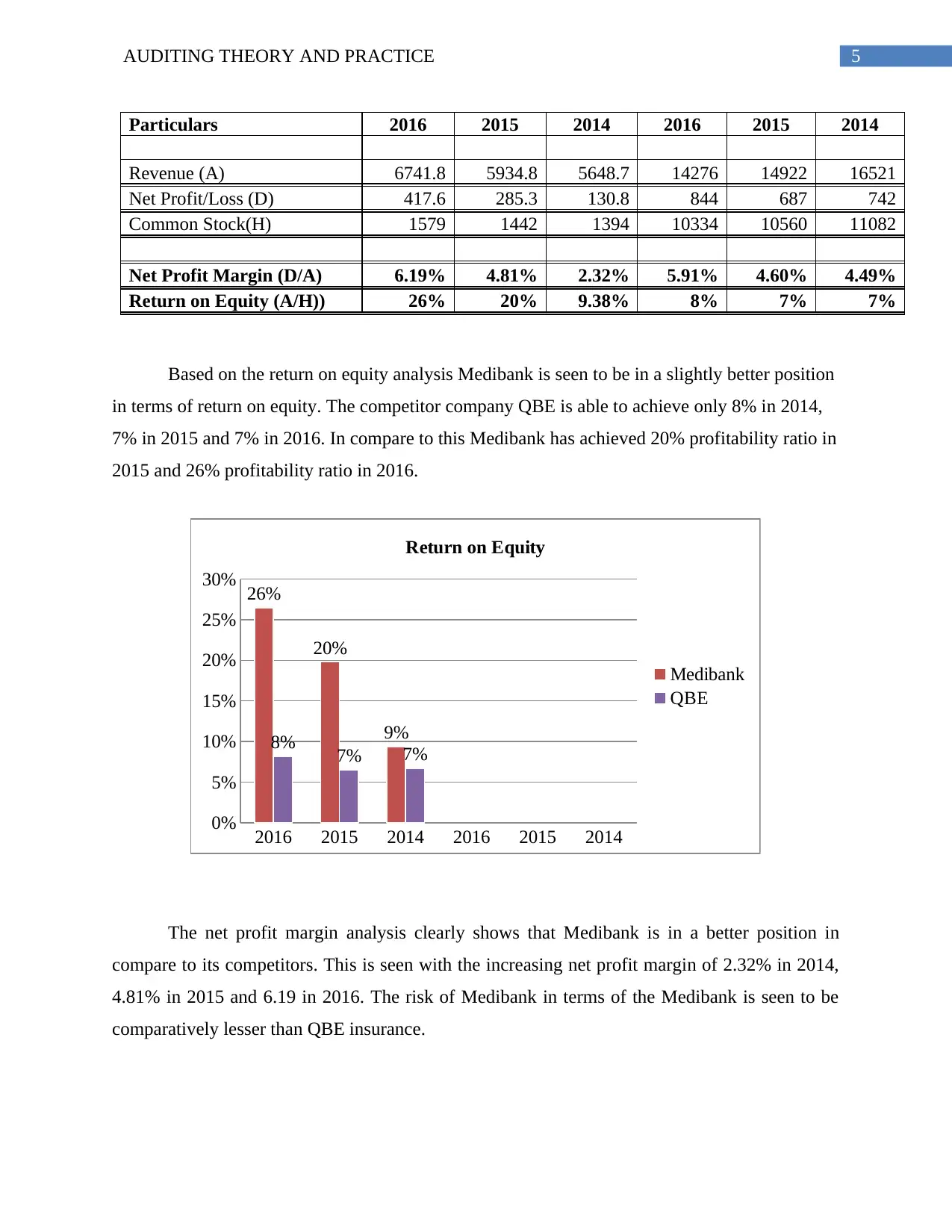

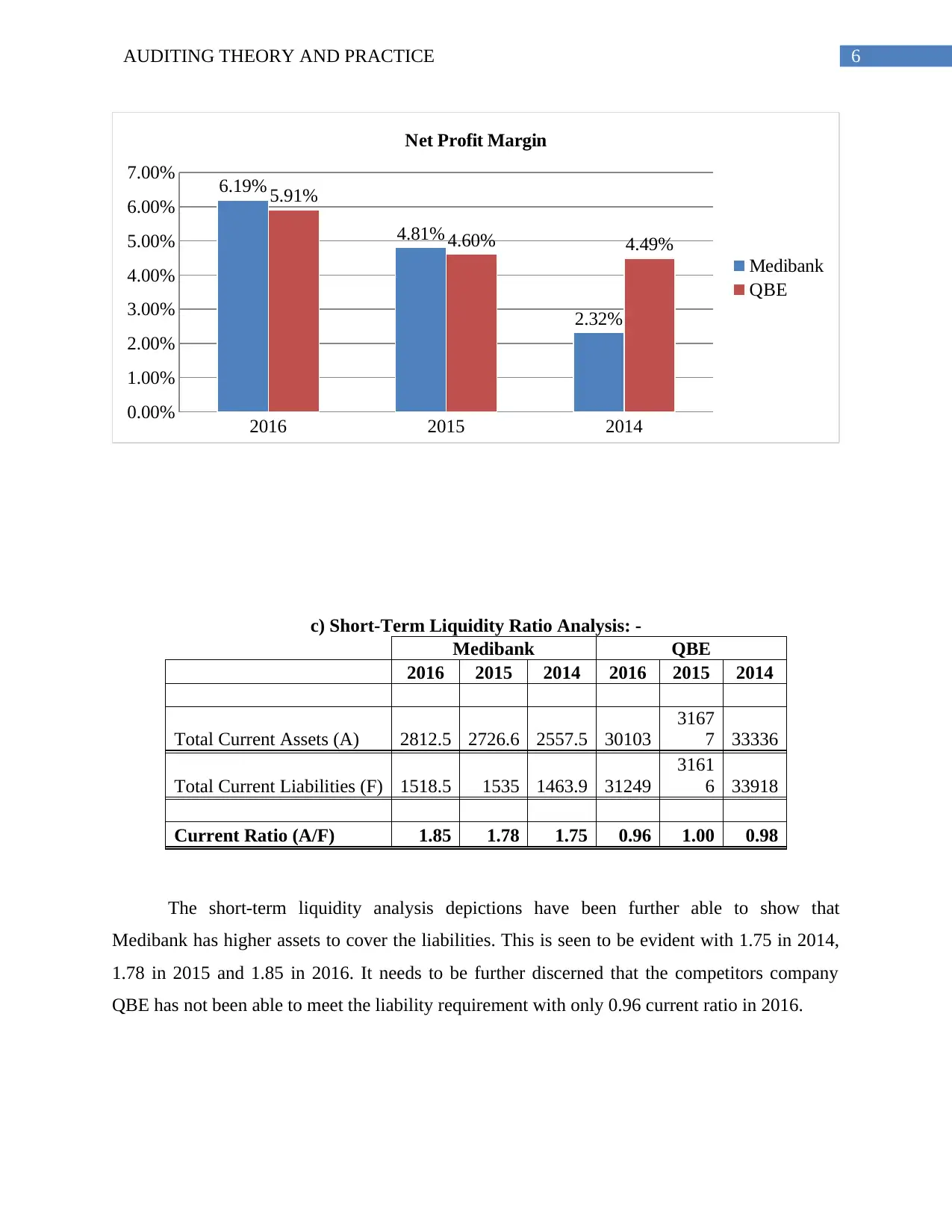

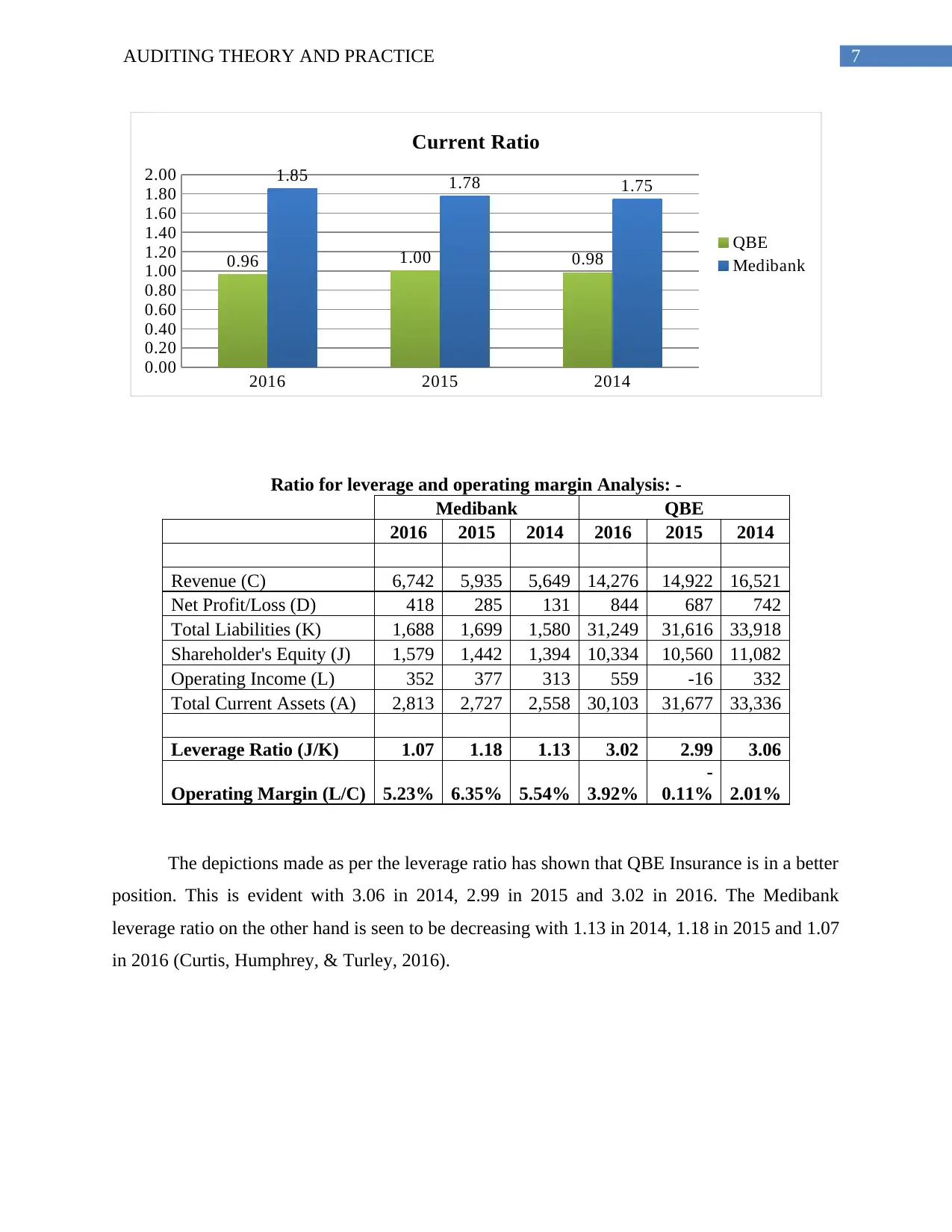

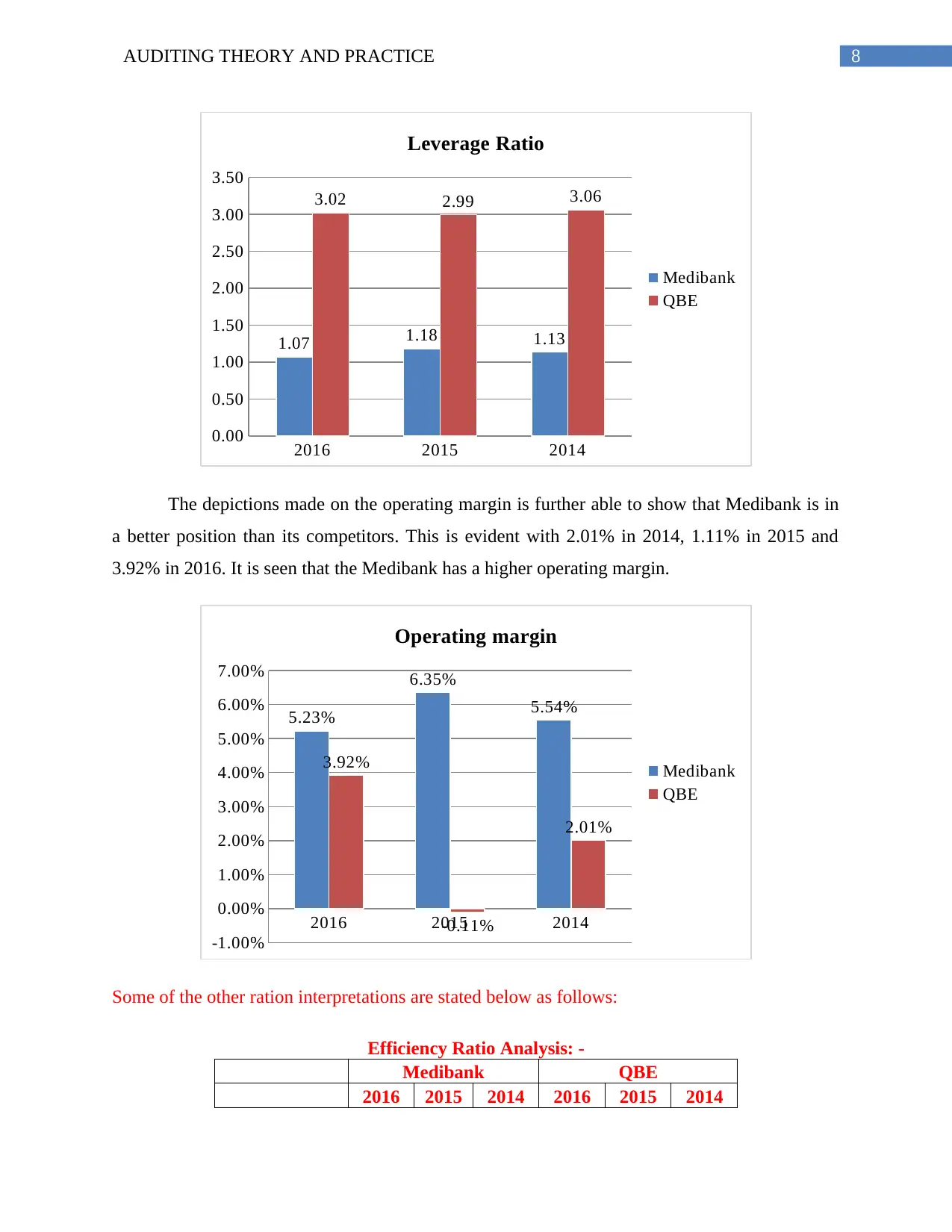

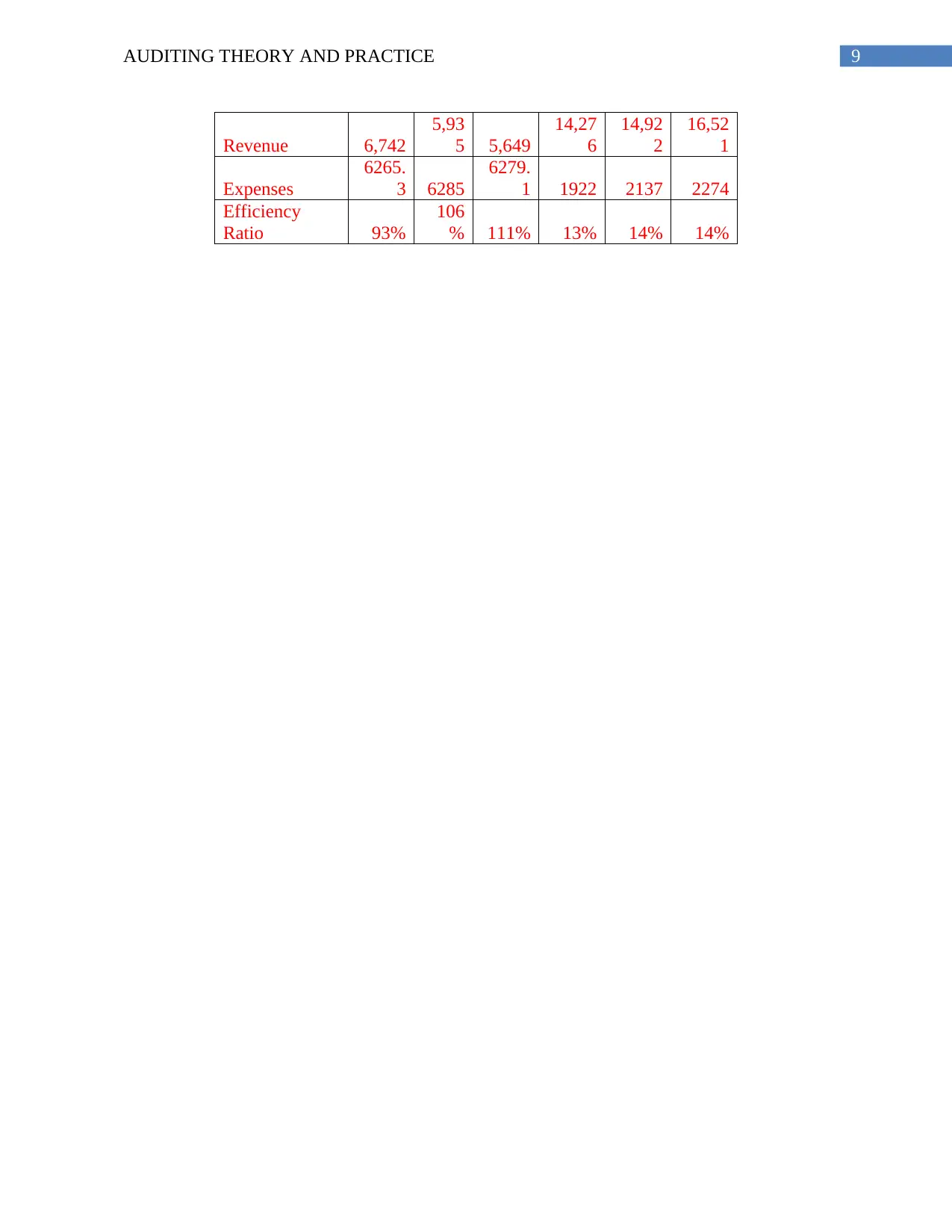

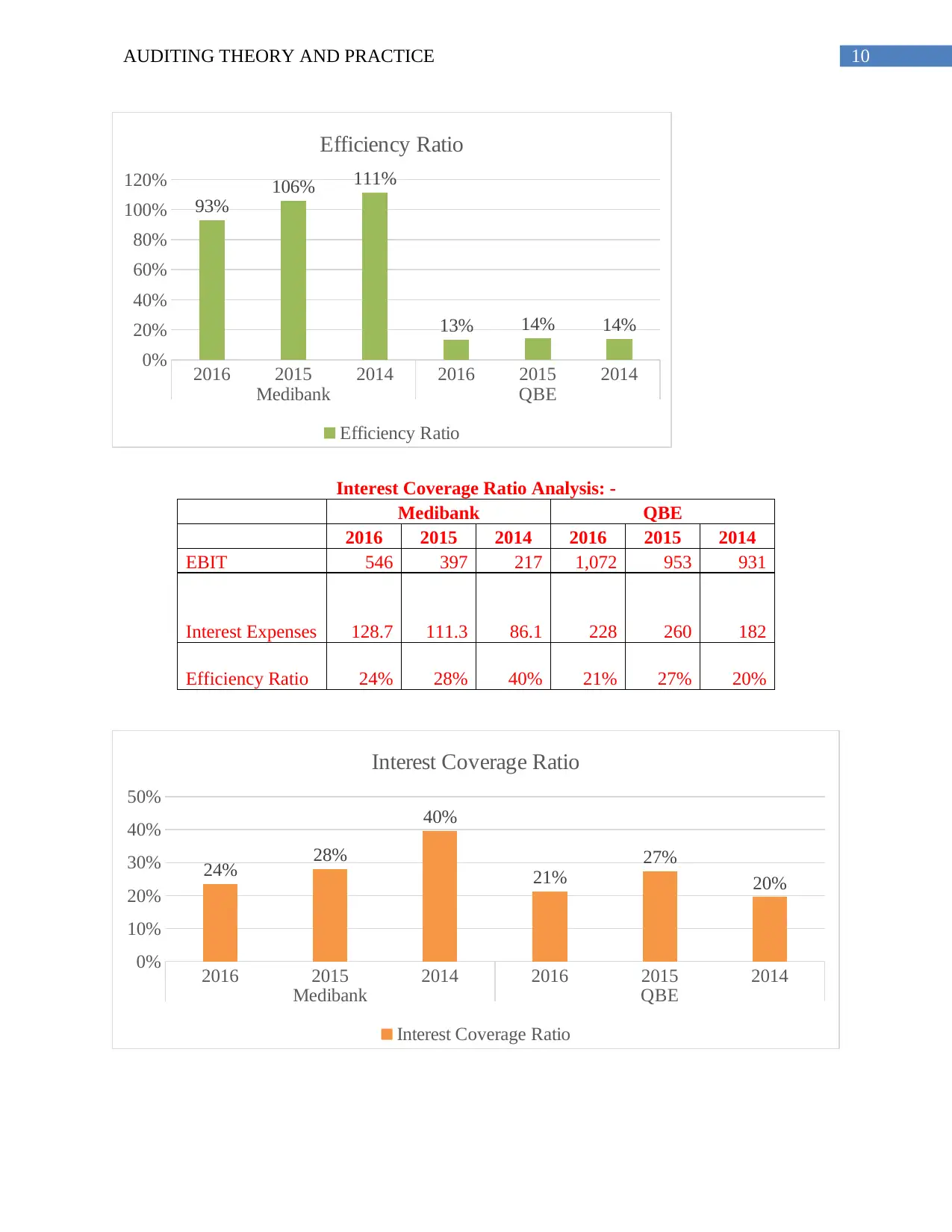

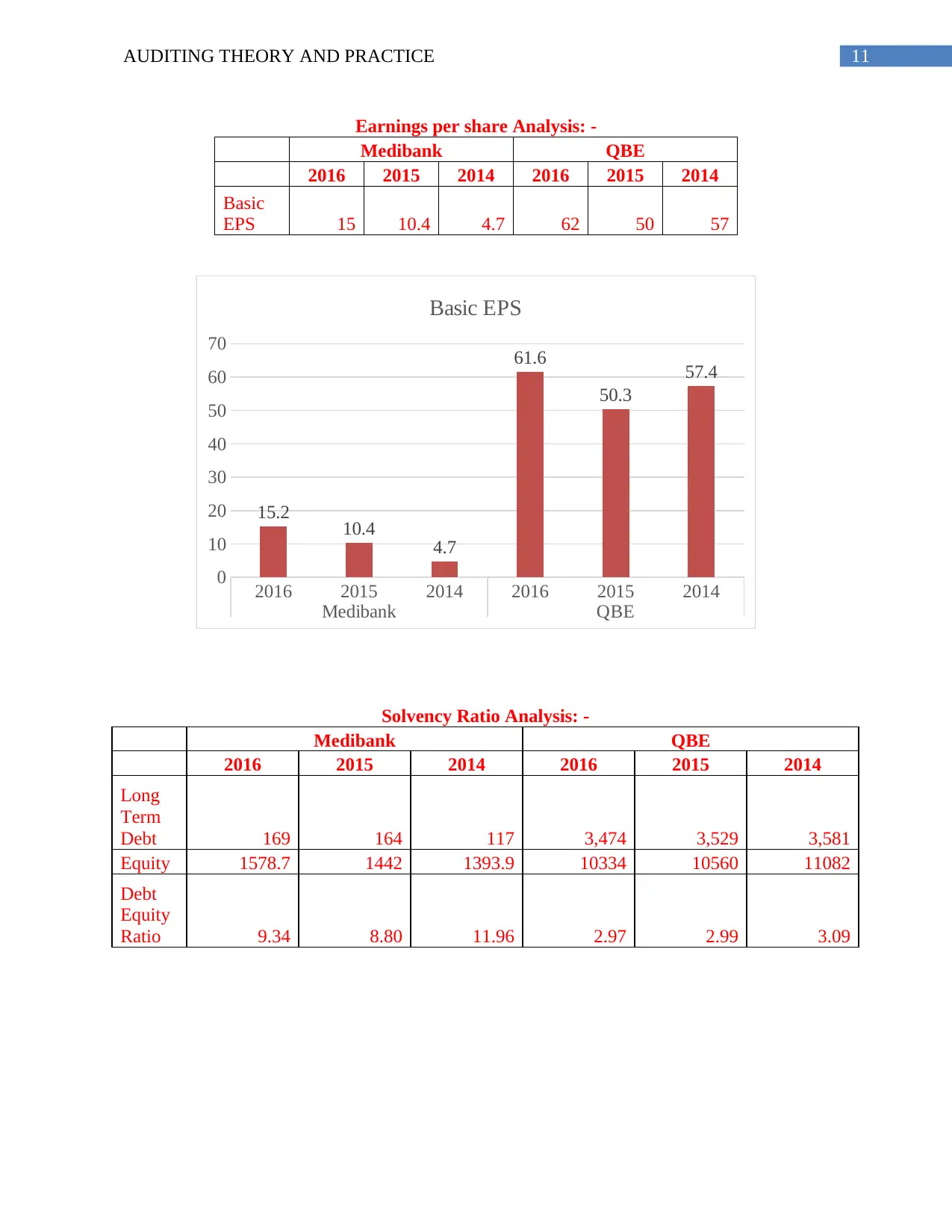

This report provides a comprehensive analysis of Medibank's auditing practices, focusing on risk analysis, evaluation of the control environment, and a comparison of its financial ratios with QBE Insurance Group. The report identifies key business risks, including healthcare costs, competition, product pricing, claims, capital management, and IT vulnerabilities. It examines the risk management framework and control measures implemented by Medibank to mitigate these risks. Furthermore, the report presents a detailed financial ratio analysis, comparing Medibank's profitability, liquidity, leverage, and operating margin with those of QBE Insurance, highlighting Medibank's stronger performance in profitability and liquidity. The conclusion emphasizes Medibank's proactive approach to addressing customer affordability and its efforts to manage risks effectively, supported by the financial data analysis.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.