Financial Analysis and Budgeting for Mediterranean Delights Ltd (MDL)

VerifiedAdded on 2023/01/12

|10

|2510

|97

Report

AI Summary

This report provides a comprehensive financial analysis of Mediterranean Delights Ltd (MDL). It begins by defining key financial terms such as cash flow, profit, working capital, receivables, stocks, and payables, highlighting the differences between profit and cash flow. The analysis then explores the impact of changes in working capital on cash flow, examining MDL's specific situation, including its increased debt, investment in an Italian company, and fluctuations in turnover and receivables. The report also addresses the adverse effects of issues with creditors and working capital management. Recommendations are provided to improve MDL's financial performance, including formulating effective policies to address customer disputes, identifying high-quality suppliers, and implementing customer-attracting policies. Part 2 of the report focuses on budgeting, defining budget and exploring different budgetary approaches, including traditional, rolling, zero-based, and activity-based budgeting, with their respective advantages and disadvantages. The report concludes with a discussion of how Second Sight plc could utilize these budgeting methods for cost management and business expansion, considering their revenue, capitalization, and potential adoption of modern budgeting techniques.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of cointent

INTRODUCTION

Question 1

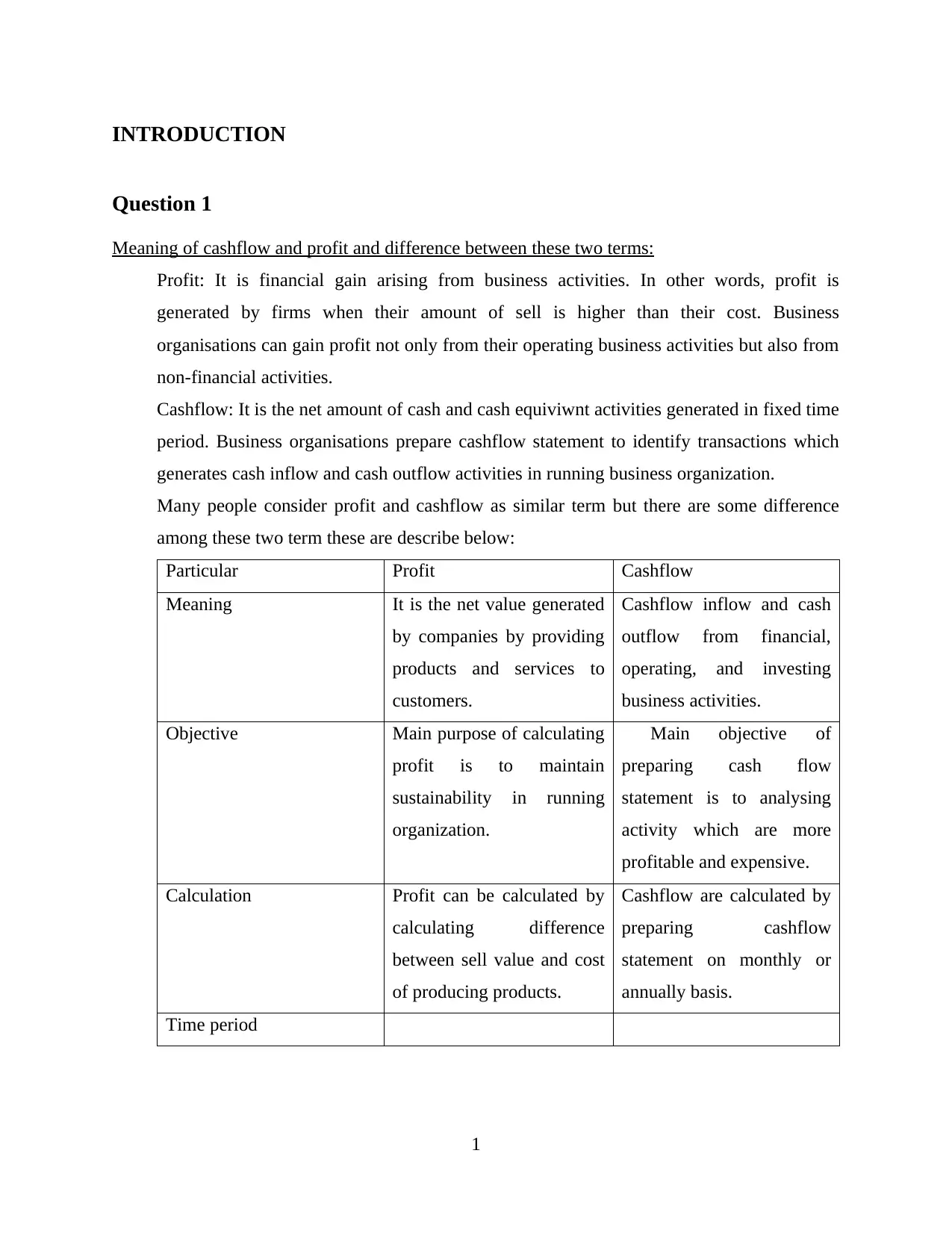

Meaning of cashflow and profit and difference between these two terms:

Profit: It is financial gain arising from business activities. In other words, profit is

generated by firms when their amount of sell is higher than their cost. Business

organisations can gain profit not only from their operating business activities but also from

non-financial activities.

Cashflow: It is the net amount of cash and cash equiviwnt activities generated in fixed time

period. Business organisations prepare cashflow statement to identify transactions which

generates cash inflow and cash outflow activities in running business organization.

Many people consider profit and cashflow as similar term but there are some difference

among these two term these are describe below:

Particular Profit Cashflow

Meaning It is the net value generated

by companies by providing

products and services to

customers.

Cashflow inflow and cash

outflow from financial,

operating, and investing

business activities.

Objective Main purpose of calculating

profit is to maintain

sustainability in running

organization.

Main objective of

preparing cash flow

statement is to analysing

activity which are more

profitable and expensive.

Calculation Profit can be calculated by

calculating difference

between sell value and cost

of producing products.

Cashflow are calculated by

preparing cashflow

statement on monthly or

annually basis.

Time period

1

Question 1

Meaning of cashflow and profit and difference between these two terms:

Profit: It is financial gain arising from business activities. In other words, profit is

generated by firms when their amount of sell is higher than their cost. Business

organisations can gain profit not only from their operating business activities but also from

non-financial activities.

Cashflow: It is the net amount of cash and cash equiviwnt activities generated in fixed time

period. Business organisations prepare cashflow statement to identify transactions which

generates cash inflow and cash outflow activities in running business organization.

Many people consider profit and cashflow as similar term but there are some difference

among these two term these are describe below:

Particular Profit Cashflow

Meaning It is the net value generated

by companies by providing

products and services to

customers.

Cashflow inflow and cash

outflow from financial,

operating, and investing

business activities.

Objective Main purpose of calculating

profit is to maintain

sustainability in running

organization.

Main objective of

preparing cash flow

statement is to analysing

activity which are more

profitable and expensive.

Calculation Profit can be calculated by

calculating difference

between sell value and cost

of producing products.

Cashflow are calculated by

preparing cashflow

statement on monthly or

annually basis.

Time period

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

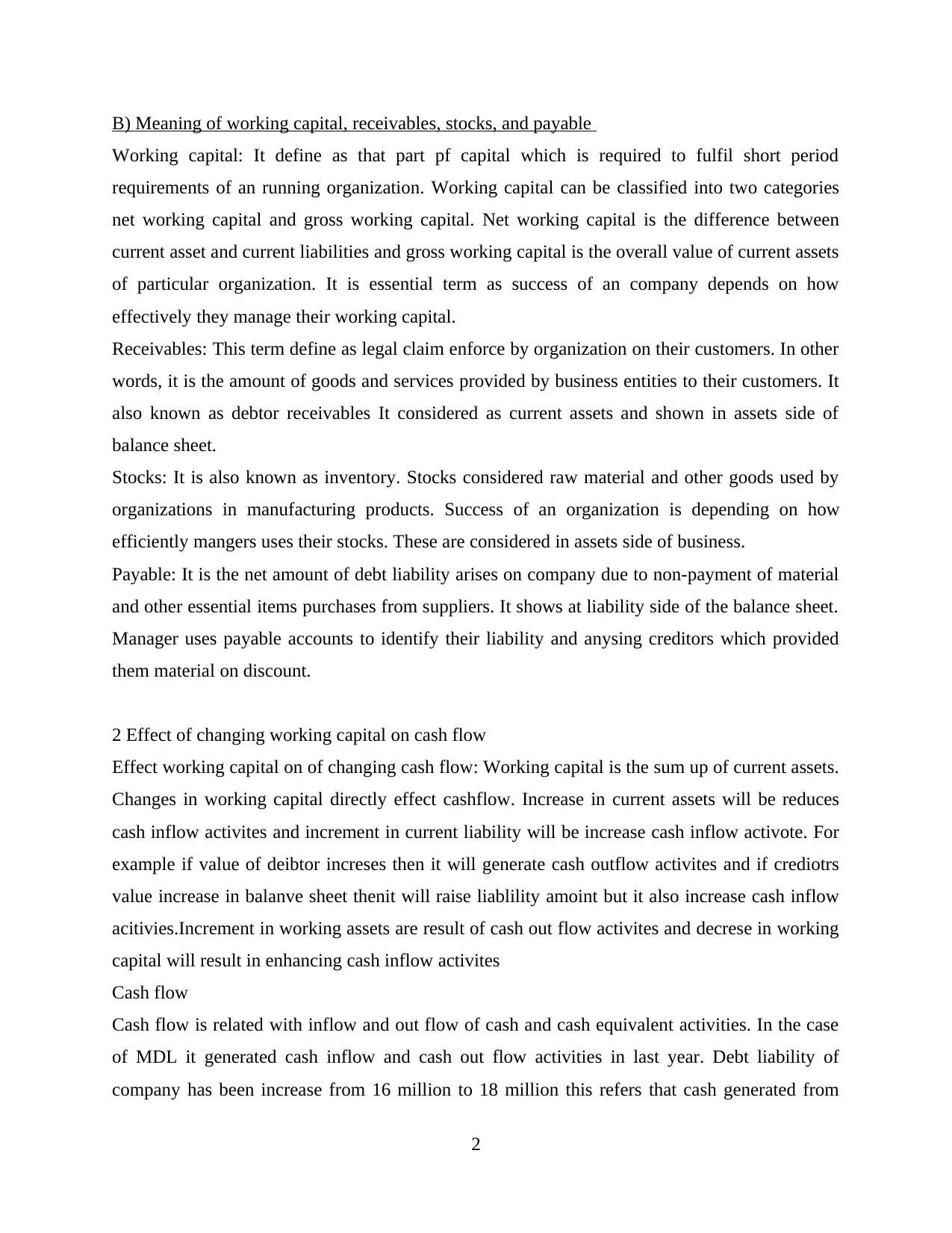

B) Meaning of working capital, receivables, stocks, and payable

Working capital: It define as that part pf capital which is required to fulfil short period

requirements of an running organization. Working capital can be classified into two categories

net working capital and gross working capital. Net working capital is the difference between

current asset and current liabilities and gross working capital is the overall value of current assets

of particular organization. It is essential term as success of an company depends on how

effectively they manage their working capital.

Receivables: This term define as legal claim enforce by organization on their customers. In other

words, it is the amount of goods and services provided by business entities to their customers. It

also known as debtor receivables It considered as current assets and shown in assets side of

balance sheet.

Stocks: It is also known as inventory. Stocks considered raw material and other goods used by

organizations in manufacturing products. Success of an organization is depending on how

efficiently mangers uses their stocks. These are considered in assets side of business.

Payable: It is the net amount of debt liability arises on company due to non-payment of material

and other essential items purchases from suppliers. It shows at liability side of the balance sheet.

Manager uses payable accounts to identify their liability and anysing creditors which provided

them material on discount.

2 Effect of changing working capital on cash flow

Effect working capital on of changing cash flow: Working capital is the sum up of current assets.

Changes in working capital directly effect cashflow. Increase in current assets will be reduces

cash inflow activites and increment in current liability will be increase cash inflow activote. For

example if value of deibtor increses then it will generate cash outflow activites and if crediotrs

value increase in balanve sheet thenit will raise liablility amoint but it also increase cash inflow

acitivies.Increment in working assets are result of cash out flow activites and decrese in working

capital will result in enhancing cash inflow activites

Cash flow

Cash flow is related with inflow and out flow of cash and cash equivalent activities. In the case

of MDL it generated cash inflow and cash out flow activities in last year. Debt liability of

company has been increase from 16 million to 18 million this refers that cash generated from

2

Working capital: It define as that part pf capital which is required to fulfil short period

requirements of an running organization. Working capital can be classified into two categories

net working capital and gross working capital. Net working capital is the difference between

current asset and current liabilities and gross working capital is the overall value of current assets

of particular organization. It is essential term as success of an company depends on how

effectively they manage their working capital.

Receivables: This term define as legal claim enforce by organization on their customers. In other

words, it is the amount of goods and services provided by business entities to their customers. It

also known as debtor receivables It considered as current assets and shown in assets side of

balance sheet.

Stocks: It is also known as inventory. Stocks considered raw material and other goods used by

organizations in manufacturing products. Success of an organization is depending on how

efficiently mangers uses their stocks. These are considered in assets side of business.

Payable: It is the net amount of debt liability arises on company due to non-payment of material

and other essential items purchases from suppliers. It shows at liability side of the balance sheet.

Manager uses payable accounts to identify their liability and anysing creditors which provided

them material on discount.

2 Effect of changing working capital on cash flow

Effect working capital on of changing cash flow: Working capital is the sum up of current assets.

Changes in working capital directly effect cashflow. Increase in current assets will be reduces

cash inflow activites and increment in current liability will be increase cash inflow activote. For

example if value of deibtor increses then it will generate cash outflow activites and if crediotrs

value increase in balanve sheet thenit will raise liablility amoint but it also increase cash inflow

acitivies.Increment in working assets are result of cash out flow activites and decrese in working

capital will result in enhancing cash inflow activites

Cash flow

Cash flow is related with inflow and out flow of cash and cash equivalent activities. In the case

of MDL it generated cash inflow and cash out flow activities in last year. Debt liability of

company has been increase from 16 million to 18 million this refers that cash generated from

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

increment of liabilities of the business organization. MDL also invested in Italian company worth

10 million the organization paid advance amount of 8 million to the Italian business organization

for purchasing pasta food produced of their company .t will reduce cash side balance. MDL ‘S

turnover also increase in past year which will increment in their cash flow activities.

Receivables:

MDL is Multinational Corporation and turnover of this company is increase from past

years but in last year their due to dispute with their potential customers. Company’s receivable

ratio is turned down and it will negatively effect on their account. Company is own 1.5 million

pound from Delios it will adversely effect on their account balance

Payables:

Creditor’s situation is also adversely effect of organization conditions. As company claim on

Maltese they supply low variety of material to the company and due to low quality of material

potential customers are claim on the business.

Working capital:

Working capital is differences between current assets and current liabilities. Due to lack of

managerial policies it will adversely effect on working capital. Ratio of working capital goes

down his will imply that company’s current liability increase. But due to last year’s profits and

high turnover rate manager of MDL will be handle all situation efficiently to cover up problem

and issue related to working capital.

Ratio of debtor, creditors turnover are provided adversely effect on the company’s performance.

For changes in current situation and enhancing financial performance of the company Manager

of MDL needs to formulate ethos policies which will help them to solve issues between their

potential customers. They will also needed to identify those creditors in market place which will

provided them material at discount and good quality of material. It will help in providing those

goods and service to their potential customers by they can satisfy their wants Manager of this

company also implements d policies which will attracted their customers.

3) Recommendation:

As per the above analysis it has been identified that financial condition of MDL

organization is not good form. Die to managerial polices and lack of working capital system their

Activity based budgeting

3

10 million the organization paid advance amount of 8 million to the Italian business organization

for purchasing pasta food produced of their company .t will reduce cash side balance. MDL ‘S

turnover also increase in past year which will increment in their cash flow activities.

Receivables:

MDL is Multinational Corporation and turnover of this company is increase from past

years but in last year their due to dispute with their potential customers. Company’s receivable

ratio is turned down and it will negatively effect on their account. Company is own 1.5 million

pound from Delios it will adversely effect on their account balance

Payables:

Creditor’s situation is also adversely effect of organization conditions. As company claim on

Maltese they supply low variety of material to the company and due to low quality of material

potential customers are claim on the business.

Working capital:

Working capital is differences between current assets and current liabilities. Due to lack of

managerial policies it will adversely effect on working capital. Ratio of working capital goes

down his will imply that company’s current liability increase. But due to last year’s profits and

high turnover rate manager of MDL will be handle all situation efficiently to cover up problem

and issue related to working capital.

Ratio of debtor, creditors turnover are provided adversely effect on the company’s performance.

For changes in current situation and enhancing financial performance of the company Manager

of MDL needs to formulate ethos policies which will help them to solve issues between their

potential customers. They will also needed to identify those creditors in market place which will

provided them material at discount and good quality of material. It will help in providing those

goods and service to their potential customers by they can satisfy their wants Manager of this

company also implements d policies which will attracted their customers.

3) Recommendation:

As per the above analysis it has been identified that financial condition of MDL

organization is not good form. Die to managerial polices and lack of working capital system their

Activity based budgeting

3

In this method mangers prepare budgets on the basis is of identify activity incurred in a running

business organization. In other words in this method budgets are prepared on the basis of

allocation of cost according to their activities. Following are the advantages and disadvantages of

this budgeting method

Part2:

PART 2

EXECUTIVE SUMMARY

Budget is a numerical statement which are used by organizations to identify future

earnings. It plays essential part in business finance and decision making process. To understand

the use of budget approach in an organisation Second Sight plc has been taken. The business

entity is run their business in Manchester and provides sunglasses products to their customer. In

this segment essential requirements of budget and uses of various approaches of preparing

budget has been identified.

Explanation of budget and advantages and disadvantages of various budgetary approaches

Budget: It is a numerical financial framework which is prepared by business entities to

estimate their future earnings and expenditure. In other words Budget is a tool of financial

management techniques which are used for decision making process in an organisation. Process

of preparing budget is known as budgeting. Business entities uses various method for preparing

budget statement. Manager also use budget for performance evaluation process of their

workforce. Budgeting methods can be classified into two techniques. Traditional and modern

methods of preparing budget.

Traditional approach: this method is one of the oldest method of preparation of budget. In this

method budgets are prepared on the basis of past year data. Usually budgets are formulated for

last 3 years data. It is most useful in small size organisation as it is easy to formulated budget

from this method. Following are the advantages and disadvantage of this method:

Advantages: Preparation of budget statement is very easy process.

4

business organization. In other words in this method budgets are prepared on the basis of

allocation of cost according to their activities. Following are the advantages and disadvantages of

this budgeting method

Part2:

PART 2

EXECUTIVE SUMMARY

Budget is a numerical statement which are used by organizations to identify future

earnings. It plays essential part in business finance and decision making process. To understand

the use of budget approach in an organisation Second Sight plc has been taken. The business

entity is run their business in Manchester and provides sunglasses products to their customer. In

this segment essential requirements of budget and uses of various approaches of preparing

budget has been identified.

Explanation of budget and advantages and disadvantages of various budgetary approaches

Budget: It is a numerical financial framework which is prepared by business entities to

estimate their future earnings and expenditure. In other words Budget is a tool of financial

management techniques which are used for decision making process in an organisation. Process

of preparing budget is known as budgeting. Business entities uses various method for preparing

budget statement. Manager also use budget for performance evaluation process of their

workforce. Budgeting methods can be classified into two techniques. Traditional and modern

methods of preparing budget.

Traditional approach: this method is one of the oldest method of preparation of budget. In this

method budgets are prepared on the basis of past year data. Usually budgets are formulated for

last 3 years data. It is most useful in small size organisation as it is easy to formulated budget

from this method. Following are the advantages and disadvantage of this method:

Advantages: Preparation of budget statement is very easy process.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It is cost beneficial process as organization does not need any expertise for formulation of

budget their manger can prepare it by analysing past year data.

Disadvantages: Data forecasting from traditional methods are not reliable there will be chances

of errors as in this dynamic environment budgets formulated by this method are n

Alternative budget methods:

Modern methods of prepration of budget:

With changes of time and technlologies various tools are implement for the purpose of prrpartion

of budget. In modern merhod of budgeting budgets are praperd on the baisis of analysing current

market situation. Modern methods included,rolling budget, activity budget, zero ba techniquesed

budgeting. Following are the benefits and drabacks of modern methods of budgeting

Rolling budget: Budgets are prepared for short term period in this mehod of

budgeting.Managers changes their policies after analysing short term period performance of

business. It is most flexible technique of prepration of budgets as busin ibess organization will

be chnge and foermulated new police for achinivg predertmind objective.

Advantages:

This tool of budget help in overcome inefficeinecies of business organizations.

Mangers enjoy flexibility power of changing polices as they can chnge rukles and opliies which

are not suitable foer business

Disadvantage:

Prepration of budget from this merod is vwry expensive and time consuming process as

managers need to supervise budgets within short term period.

Due to changesw of poloces and sturctre sempyers of organization get frustrated and

demotivated as they can not adopt changing policies in work place area.

Zero based budting: It is one of the most useful method adopt by organizations to prepare

budget.In this type of budgeting technique managers prepar budget without using past data they

start serchnig ,formulating strategies from scratch level . In other words in this technique budgets

are prepared from initial level. Following are the benefits and drawback of using zero bsed

budgeting technique: Activity based budgeting

5

budget their manger can prepare it by analysing past year data.

Disadvantages: Data forecasting from traditional methods are not reliable there will be chances

of errors as in this dynamic environment budgets formulated by this method are n

Alternative budget methods:

Modern methods of prepration of budget:

With changes of time and technlologies various tools are implement for the purpose of prrpartion

of budget. In modern merhod of budgeting budgets are praperd on the baisis of analysing current

market situation. Modern methods included,rolling budget, activity budget, zero ba techniquesed

budgeting. Following are the benefits and drabacks of modern methods of budgeting

Rolling budget: Budgets are prepared for short term period in this mehod of

budgeting.Managers changes their policies after analysing short term period performance of

business. It is most flexible technique of prepration of budgets as busin ibess organization will

be chnge and foermulated new police for achinivg predertmind objective.

Advantages:

This tool of budget help in overcome inefficeinecies of business organizations.

Mangers enjoy flexibility power of changing polices as they can chnge rukles and opliies which

are not suitable foer business

Disadvantage:

Prepration of budget from this merod is vwry expensive and time consuming process as

managers need to supervise budgets within short term period.

Due to changesw of poloces and sturctre sempyers of organization get frustrated and

demotivated as they can not adopt changing policies in work place area.

Zero based budting: It is one of the most useful method adopt by organizations to prepare

budget.In this type of budgeting technique managers prepar budget without using past data they

start serchnig ,formulating strategies from scratch level . In other words in this technique budgets

are prepared from initial level. Following are the benefits and drawback of using zero bsed

budgeting technique: Activity based budgeting

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

In this method mangers prepare budgets on the basis is of identify activity incurred in a running

business organization. In other words in this method budgets are prepared on the basis of

allocation of cost according to their activities. Following are the advantages and disadvantages of

this budgeting method

Advantage:

It will help in cutting wastage and expenses incurred activities`

Those method is useful for manufacturing industry as will help in proper utilization of resources.

Disadvantage:

It is hard and complicated process of preparation of budget from this method.

This method is not applicable for all type of business organization`

Rolling budget: In this method budgets are prepared FOR SHORT TIME PERIOD. Manger

Compare analysis their short budget activities and then prepared another budget for short term

period. The sequences of preparation of budget run continues until company achieved their

desired goal

Advantages

This is most flexible method and manager change policies according to the need and situation of

the organization

I provides accurate result in forecasting income and expenditure of company.

Disadvantage

Preparation of budget by this method incurred high cost as budgets are prepared after

competition of short time period

It will not applicable and suitable for all type of organizations

2

Second sight is well established corporation since last 10 years. Budgeting methods

Will effectively help them in cost management and expenshion of their business branch

Second sight PLC earn 250 million revenue in last year and had capitalization value over 300

Million. The business organization will be use traditional budgeting method for prepration of

budgets

As it will help them in identity expected revenue and expenses related to their new project.

They use past year daya for prepration of budgets. It will help them to save cost related to

Research and other expenses of formulated business’s. Manager of Second sight also adopt

6

business organization. In other words in this method budgets are prepared on the basis of

allocation of cost according to their activities. Following are the advantages and disadvantages of

this budgeting method

Advantage:

It will help in cutting wastage and expenses incurred activities`

Those method is useful for manufacturing industry as will help in proper utilization of resources.

Disadvantage:

It is hard and complicated process of preparation of budget from this method.

This method is not applicable for all type of business organization`

Rolling budget: In this method budgets are prepared FOR SHORT TIME PERIOD. Manger

Compare analysis their short budget activities and then prepared another budget for short term

period. The sequences of preparation of budget run continues until company achieved their

desired goal

Advantages

This is most flexible method and manager change policies according to the need and situation of

the organization

I provides accurate result in forecasting income and expenditure of company.

Disadvantage

Preparation of budget by this method incurred high cost as budgets are prepared after

competition of short time period

It will not applicable and suitable for all type of organizations

2

Second sight is well established corporation since last 10 years. Budgeting methods

Will effectively help them in cost management and expenshion of their business branch

Second sight PLC earn 250 million revenue in last year and had capitalization value over 300

Million. The business organization will be use traditional budgeting method for prepration of

budgets

As it will help them in identity expected revenue and expenses related to their new project.

They use past year daya for prepration of budgets. It will help them to save cost related to

Research and other expenses of formulated business’s. Manager of Second sight also adopt

6

Alterative ways of preparing budgets as they can prepare budgets from rolling method or

Activity based method . these methods will be manage their allocation of cost in various

Activities of manufacturing and selling Sunglasses to in target market of india and Netherland

Manager will be used modern techniques of formulating budget as budget prepare from these

methods are provide accurate data related to future income and exoenses. Manager of Second

Sight PLC will be used alternative methods az they have large sirve of income and they will

Be easily bear cost of preparing budgets.Second sight PLC will be manufacture glasses

In india after identifying demand of sunglasses in particular time period. For this purpose they

Will prepare rolling based budget . It will also be oficial in reducing extra curricular expense

Incurred in setting up and manufacturing process of producing sunglasses.

3

Second sight is medium size corporation and they want to expand their business units

In india and Netherland. Manager of Second sight uses budget method to take decision regarding

Formulation of policies . For this purpose they will traditional as well as alternative methods

Of formulation of budget statement. Both methods has their own benefits and drawback.

Business organization apply thoda method of prepration of budget which eill br suitable and

more beneficial from other alternative. Manager of Second sight PLC can be use traditional

method of budgeting for Netherlands project .

Of their business in India .For this new startup they need to prepare budget from rolling method.

As Target market of India is very complicated and demands and preferences of their customers

are not similar due to diversity. Thus rolling method is most useful and appropriate method for

Indian project. Traditional method of budgeting cannot be suitable on this project as Indian

market is very large. Managers may use zero budgeting method because Indian market is new

and they can benefit For Netherland project the manager will be used traditional budgeting

method as geographical conditions are similar of Manchester’s. Customer’s preferences are also

similar in Netherland and Manchester. Thus traditional method provides accurate data related to

future income of their projects. In Netherland project manager cannot use activity based

budgeting method as it will incurred more cost on calculation of each activity task. For this

project manager cannot apply zero based budgeting method as it will hire more cost on

researching of each and every element of production of products. Manager can adopt method of

preparation of budget as it will help in analysis of their profitability rate of future but not all

7

Activity based method . these methods will be manage their allocation of cost in various

Activities of manufacturing and selling Sunglasses to in target market of india and Netherland

Manager will be used modern techniques of formulating budget as budget prepare from these

methods are provide accurate data related to future income and exoenses. Manager of Second

Sight PLC will be used alternative methods az they have large sirve of income and they will

Be easily bear cost of preparing budgets.Second sight PLC will be manufacture glasses

In india after identifying demand of sunglasses in particular time period. For this purpose they

Will prepare rolling based budget . It will also be oficial in reducing extra curricular expense

Incurred in setting up and manufacturing process of producing sunglasses.

3

Second sight is medium size corporation and they want to expand their business units

In india and Netherland. Manager of Second sight uses budget method to take decision regarding

Formulation of policies . For this purpose they will traditional as well as alternative methods

Of formulation of budget statement. Both methods has their own benefits and drawback.

Business organization apply thoda method of prepration of budget which eill br suitable and

more beneficial from other alternative. Manager of Second sight PLC can be use traditional

method of budgeting for Netherlands project .

Of their business in India .For this new startup they need to prepare budget from rolling method.

As Target market of India is very complicated and demands and preferences of their customers

are not similar due to diversity. Thus rolling method is most useful and appropriate method for

Indian project. Traditional method of budgeting cannot be suitable on this project as Indian

market is very large. Managers may use zero budgeting method because Indian market is new

and they can benefit For Netherland project the manager will be used traditional budgeting

method as geographical conditions are similar of Manchester’s. Customer’s preferences are also

similar in Netherland and Manchester. Thus traditional method provides accurate data related to

future income of their projects. In Netherland project manager cannot use activity based

budgeting method as it will incurred more cost on calculation of each activity task. For this

project manager cannot apply zero based budgeting method as it will hire more cost on

researching of each and every element of production of products. Manager can adopt method of

preparation of budget as it will help in analysis of their profitability rate of future but not all

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

methods are useful and applied in running business organization Success of an entity totally

depends upon the decision of preparation of budget and how effectively they worth on their

budget.

8

depends upon the decision of preparation of budget and how effectively they worth on their

budget.

8

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.