Mel's Business: Journal Entries, Ledger, Trial Balance, Financials

VerifiedAdded on 2021/01/02

|12

|3472

|152

Homework Assignment

AI Summary

This assignment presents a detailed financial analysis of Mel's business transactions. It begins with the recording of transactions in journal entries, followed by posting these entries to the general ledger. The assignment then progresses to the preparation of a trial balance, income statement, and statement of financial position. Furthermore, the report includes the calculation of various financial ratios to provide a comparative analysis of Mel's financial performance. The content covers the entire accounting cycle, from initial transaction recording to the final preparation of financial statements, offering a comprehensive understanding of financial accounting principles. The report also includes a comparative analysis using financial ratios.

RECORDING BUSINESS

TRANSACTION

TRANSACTION

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

(a) Journal Entries of Mel...........................................................................................................3

(b) General Ledger of Mel..........................................................................................................5

(c) Trial Balance of Mel..............................................................................................................7

(d) Income Statement of Mel......................................................................................................8

(e) Statement of Financial Position of Mel.................................................................................8

PART B............................................................................................................................................9

Ratios calculation for Mel :.........................................................................................................9

Systematic comparison of various ratios of Mel with competitors average:............................10

CONCLUSION..............................................................................................................................11

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

(a) Journal Entries of Mel...........................................................................................................3

(b) General Ledger of Mel..........................................................................................................5

(c) Trial Balance of Mel..............................................................................................................7

(d) Income Statement of Mel......................................................................................................8

(e) Statement of Financial Position of Mel.................................................................................8

PART B............................................................................................................................................9

Ratios calculation for Mel :.........................................................................................................9

Systematic comparison of various ratios of Mel with competitors average:............................10

CONCLUSION..............................................................................................................................11

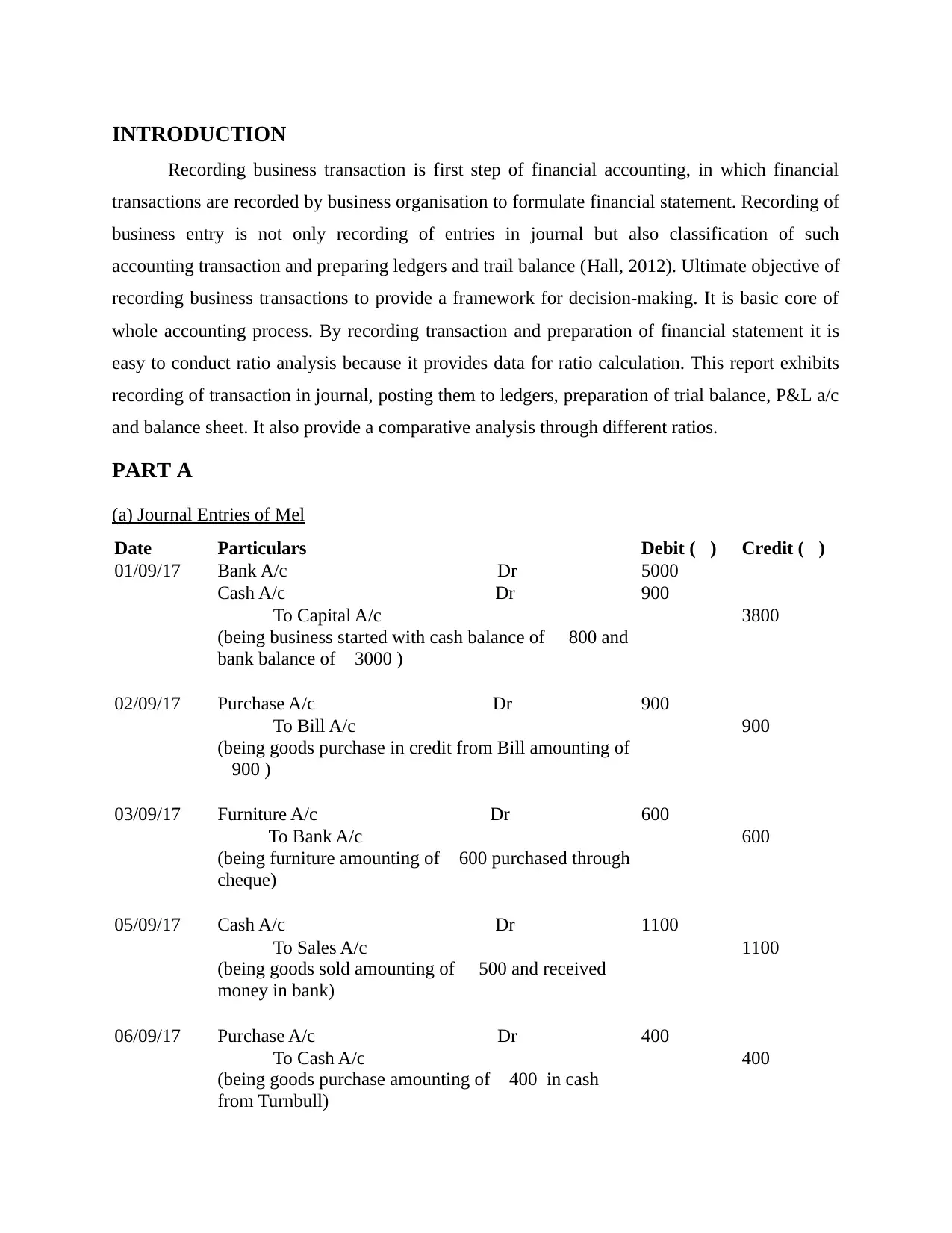

INTRODUCTION

Recording business transaction is first step of financial accounting, in which financial

transactions are recorded by business organisation to formulate financial statement. Recording of

business entry is not only recording of entries in journal but also classification of such

accounting transaction and preparing ledgers and trail balance (Hall, 2012). Ultimate objective of

recording business transactions to provide a framework for decision-making. It is basic core of

whole accounting process. By recording transaction and preparation of financial statement it is

easy to conduct ratio analysis because it provides data for ratio calculation. This report exhibits

recording of transaction in journal, posting them to ledgers, preparation of trial balance, P&L a/c

and balance sheet. It also provide a comparative analysis through different ratios.

PART A

(a) Journal Entries of Mel

Date Particulars Debit (£) Credit (£)

01/09/17 Bank A/c Dr 5000

Cash A/c Dr 900

To Capital A/c 3800

(being business started with cash balance of £ 800 and

bank balance of £3000 )

02/09/17 Purchase A/c Dr 900

To Bill A/c 900

(being goods purchase in credit from Bill amounting of

£900 )

03/09/17 Furniture A/c Dr 600

To Bank A/c 600

(being furniture amounting of £600 purchased through

cheque)

05/09/17 Cash A/c Dr 1100

To Sales A/c 1100

(being goods sold amounting of £ 500 and received

money in bank)

06/09/17 Purchase A/c Dr 400

To Cash A/c 400

(being goods purchase amounting of £400 in cash

from Turnbull)

Recording business transaction is first step of financial accounting, in which financial

transactions are recorded by business organisation to formulate financial statement. Recording of

business entry is not only recording of entries in journal but also classification of such

accounting transaction and preparing ledgers and trail balance (Hall, 2012). Ultimate objective of

recording business transactions to provide a framework for decision-making. It is basic core of

whole accounting process. By recording transaction and preparation of financial statement it is

easy to conduct ratio analysis because it provides data for ratio calculation. This report exhibits

recording of transaction in journal, posting them to ledgers, preparation of trial balance, P&L a/c

and balance sheet. It also provide a comparative analysis through different ratios.

PART A

(a) Journal Entries of Mel

Date Particulars Debit (£) Credit (£)

01/09/17 Bank A/c Dr 5000

Cash A/c Dr 900

To Capital A/c 3800

(being business started with cash balance of £ 800 and

bank balance of £3000 )

02/09/17 Purchase A/c Dr 900

To Bill A/c 900

(being goods purchase in credit from Bill amounting of

£900 )

03/09/17 Furniture A/c Dr 600

To Bank A/c 600

(being furniture amounting of £600 purchased through

cheque)

05/09/17 Cash A/c Dr 1100

To Sales A/c 1100

(being goods sold amounting of £ 500 and received

money in bank)

06/09/17 Purchase A/c Dr 400

To Cash A/c 400

(being goods purchase amounting of £400 in cash

from Turnbull)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10/09/17 Rent Paid A/c Dr 400

To Cash A/c 400

(being rent amounting of £400 paid in cash)

12/09/17 Stationery A/c Dr 200

To Bank A/c 200

(being stationery amounting of £200 purchase through

cheque )

18/09/17 Bill A/c Dr. 500

To Bank A/c 500

(being amount paid to Bill for previous due£500 from

bank )

21/09/17 Purchase A/c Dr 100

To Bill A/c 100

(being goods purchase in credit from Bill amounting of

£100 )

23/09/17 Till A/c Dr 400

To Sales A/c 400

(Being goods amounting of £400 sold to Till on credit)

23/09/17 Cash A/c Dr 1000

Rob Dr 500

To Sales A/c 1500

(Being goods amounting of £ 1500 sold to Rob and

only 1000 received in cash)

24/09/17 Car A/c Dr 1500

To Bank A/c 1500

(being car amounting of £1500 purchase in cheque for

business use)

30/09/17 Wages A/c Dr 800

To Cash A/c 800

(being wages amounting of £ 800 paid in cash)

30/09/17 Capital A/c Dr 400

To Cash A/c 400

(being cash amounting of £550 withdraw by Jill in

cash)

30/09/17 Office Computer A/c Dr 400

To Cash A/c 400

To Cash A/c 400

(being rent amounting of £400 paid in cash)

12/09/17 Stationery A/c Dr 200

To Bank A/c 200

(being stationery amounting of £200 purchase through

cheque )

18/09/17 Bill A/c Dr. 500

To Bank A/c 500

(being amount paid to Bill for previous due£500 from

bank )

21/09/17 Purchase A/c Dr 100

To Bill A/c 100

(being goods purchase in credit from Bill amounting of

£100 )

23/09/17 Till A/c Dr 400

To Sales A/c 400

(Being goods amounting of £400 sold to Till on credit)

23/09/17 Cash A/c Dr 1000

Rob Dr 500

To Sales A/c 1500

(Being goods amounting of £ 1500 sold to Rob and

only 1000 received in cash)

24/09/17 Car A/c Dr 1500

To Bank A/c 1500

(being car amounting of £1500 purchase in cheque for

business use)

30/09/17 Wages A/c Dr 800

To Cash A/c 800

(being wages amounting of £ 800 paid in cash)

30/09/17 Capital A/c Dr 400

To Cash A/c 400

(being cash amounting of £550 withdraw by Jill in

cash)

30/09/17 Office Computer A/c Dr 400

To Cash A/c 400

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(Being amount paid for office computer)

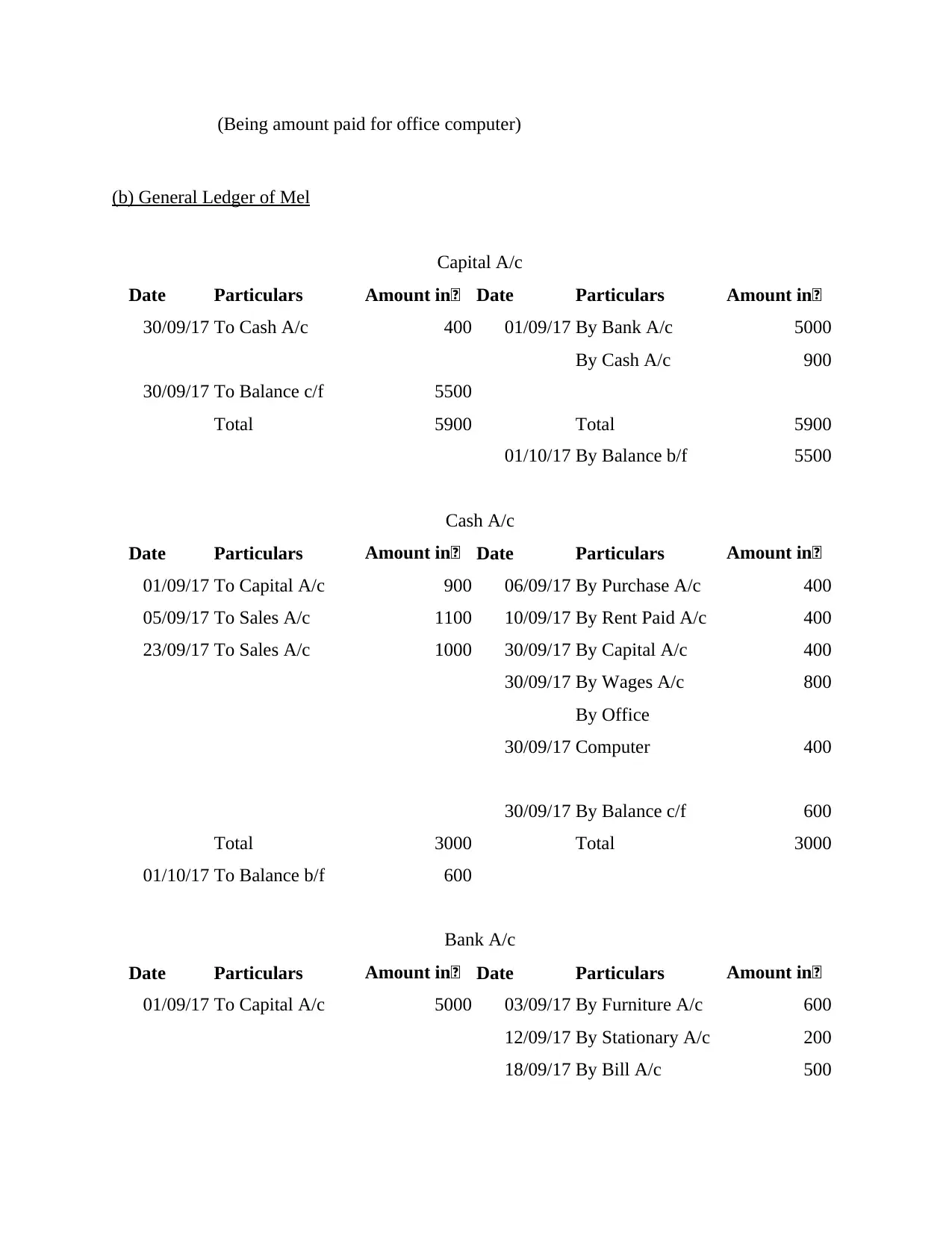

(b) General Ledger of Mel

Capital A/c

Date Particulars Amount in£ Date Particulars Amount in£

30/09/17 To Cash A/c 400 01/09/17 By Bank A/c 5000

By Cash A/c 900

30/09/17 To Balance c/f 5500

Total 5900 Total 5900

01/10/17 By Balance b/f 5500

Cash A/c

Date Particulars Amount in£ Date Particulars Amount in£

01/09/17 To Capital A/c 900 06/09/17 By Purchase A/c 400

05/09/17 To Sales A/c 1100 10/09/17 By Rent Paid A/c 400

23/09/17 To Sales A/c 1000 30/09/17 By Capital A/c 400

30/09/17 By Wages A/c 800

30/09/17

By Office

Computer 400

30/09/17 By Balance c/f 600

Total 3000 Total 3000

01/10/17 To Balance b/f 600

Bank A/c

Date Particulars Amount in£ Date Particulars Amount in£

01/09/17 To Capital A/c 5000 03/09/17 By Furniture A/c 600

12/09/17 By Stationary A/c 200

18/09/17 By Bill A/c 500

(b) General Ledger of Mel

Capital A/c

Date Particulars Amount in£ Date Particulars Amount in£

30/09/17 To Cash A/c 400 01/09/17 By Bank A/c 5000

By Cash A/c 900

30/09/17 To Balance c/f 5500

Total 5900 Total 5900

01/10/17 By Balance b/f 5500

Cash A/c

Date Particulars Amount in£ Date Particulars Amount in£

01/09/17 To Capital A/c 900 06/09/17 By Purchase A/c 400

05/09/17 To Sales A/c 1100 10/09/17 By Rent Paid A/c 400

23/09/17 To Sales A/c 1000 30/09/17 By Capital A/c 400

30/09/17 By Wages A/c 800

30/09/17

By Office

Computer 400

30/09/17 By Balance c/f 600

Total 3000 Total 3000

01/10/17 To Balance b/f 600

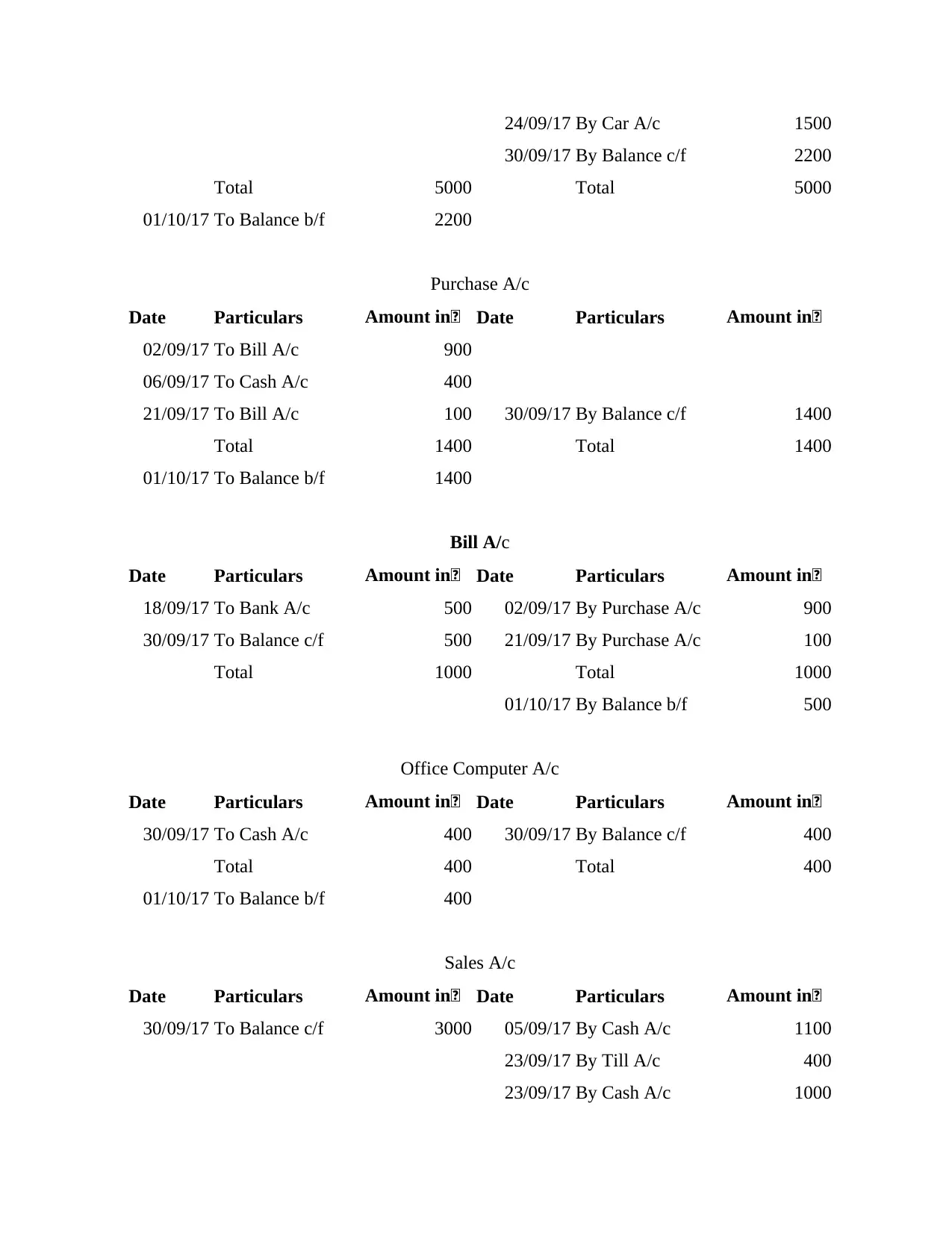

Bank A/c

Date Particulars Amount in£ Date Particulars Amount in£

01/09/17 To Capital A/c 5000 03/09/17 By Furniture A/c 600

12/09/17 By Stationary A/c 200

18/09/17 By Bill A/c 500

24/09/17 By Car A/c 1500

30/09/17 By Balance c/f 2200

Total 5000 Total 5000

01/10/17 To Balance b/f 2200

Purchase A/c

Date Particulars Amount in£ Date Particulars Amount in£

02/09/17 To Bill A/c 900

06/09/17 To Cash A/c 400

21/09/17 To Bill A/c 100 30/09/17 By Balance c/f 1400

Total 1400 Total 1400

01/10/17 To Balance b/f 1400

Bill A/c

Date Particulars Amount in£ Date Particulars Amount in£

18/09/17 To Bank A/c 500 02/09/17 By Purchase A/c 900

30/09/17 To Balance c/f 500 21/09/17 By Purchase A/c 100

Total 1000 Total 1000

01/10/17 By Balance b/f 500

Office Computer A/c

Date Particulars Amount in£ Date Particulars Amount in£

30/09/17 To Cash A/c 400 30/09/17 By Balance c/f 400

Total 400 Total 400

01/10/17 To Balance b/f 400

Sales A/c

Date Particulars Amount in£ Date Particulars Amount in£

30/09/17 To Balance c/f 3000 05/09/17 By Cash A/c 1100

23/09/17 By Till A/c 400

23/09/17 By Cash A/c 1000

30/09/17 By Balance c/f 2200

Total 5000 Total 5000

01/10/17 To Balance b/f 2200

Purchase A/c

Date Particulars Amount in£ Date Particulars Amount in£

02/09/17 To Bill A/c 900

06/09/17 To Cash A/c 400

21/09/17 To Bill A/c 100 30/09/17 By Balance c/f 1400

Total 1400 Total 1400

01/10/17 To Balance b/f 1400

Bill A/c

Date Particulars Amount in£ Date Particulars Amount in£

18/09/17 To Bank A/c 500 02/09/17 By Purchase A/c 900

30/09/17 To Balance c/f 500 21/09/17 By Purchase A/c 100

Total 1000 Total 1000

01/10/17 By Balance b/f 500

Office Computer A/c

Date Particulars Amount in£ Date Particulars Amount in£

30/09/17 To Cash A/c 400 30/09/17 By Balance c/f 400

Total 400 Total 400

01/10/17 To Balance b/f 400

Sales A/c

Date Particulars Amount in£ Date Particulars Amount in£

30/09/17 To Balance c/f 3000 05/09/17 By Cash A/c 1100

23/09/17 By Till A/c 400

23/09/17 By Cash A/c 1000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

23/09/17 By Rob A/c 500

Total 3000 Total 3000

01/10/17 By Balance b/f 3000

Stationery A/c

Date Particulars Amount in£ Date Particulars Amount in£

12/09/17 To Bank A/c 200 30/09/17 By Balance c/f 200

Total 200 Total 200

01/10/17 To Balance b/f 200

Furniture A/c

Date Particulars Amount in£ Date Particulars Amount in£

03/09/17 To Bank A/c 600 30/09/17 By Balance c/f 600

Total 600 Total 600

01/10/17 To Balance b/f 600

Rent Paid A/c

Date Particulars £Amount in£ Date Particulars Amount in£

10/09/17 To Cash A/c 400 30/09/17 By Balance c/f 400

Total 400 Total 400

01/10/17 To Balance b/f 400

Rob A/c

Date Particulars Amount in£ Date Particulars Amount in£

23/09/17 To Sales A/c 500 30/09/17 By Balance c/f 500

Total 500 Total 500

01/10/17 To Balance b/f 500

Car A/c

Date Particulars Amount in£ Date Particulars Amount in£

Total 3000 Total 3000

01/10/17 By Balance b/f 3000

Stationery A/c

Date Particulars Amount in£ Date Particulars Amount in£

12/09/17 To Bank A/c 200 30/09/17 By Balance c/f 200

Total 200 Total 200

01/10/17 To Balance b/f 200

Furniture A/c

Date Particulars Amount in£ Date Particulars Amount in£

03/09/17 To Bank A/c 600 30/09/17 By Balance c/f 600

Total 600 Total 600

01/10/17 To Balance b/f 600

Rent Paid A/c

Date Particulars £Amount in£ Date Particulars Amount in£

10/09/17 To Cash A/c 400 30/09/17 By Balance c/f 400

Total 400 Total 400

01/10/17 To Balance b/f 400

Rob A/c

Date Particulars Amount in£ Date Particulars Amount in£

23/09/17 To Sales A/c 500 30/09/17 By Balance c/f 500

Total 500 Total 500

01/10/17 To Balance b/f 500

Car A/c

Date Particulars Amount in£ Date Particulars Amount in£

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

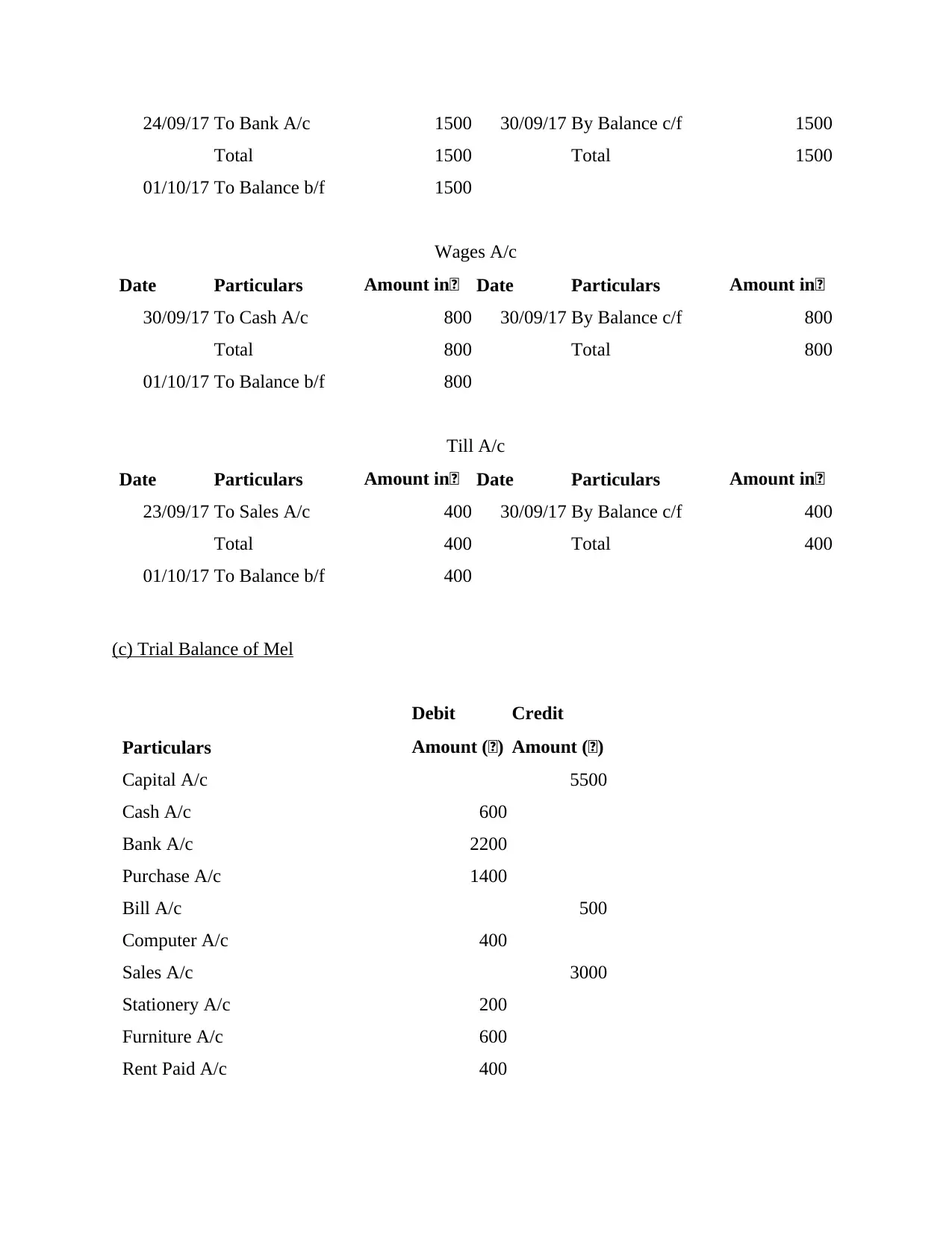

24/09/17 To Bank A/c 1500 30/09/17 By Balance c/f 1500

Total 1500 Total 1500

01/10/17 To Balance b/f 1500

Wages A/c

Date Particulars Amount in£ Date Particulars Amount in£

30/09/17 To Cash A/c 800 30/09/17 By Balance c/f 800

Total 800 Total 800

01/10/17 To Balance b/f 800

Till A/c

Date Particulars Amount in£ Date Particulars Amount in£

23/09/17 To Sales A/c 400 30/09/17 By Balance c/f 400

Total 400 Total 400

01/10/17 To Balance b/f 400

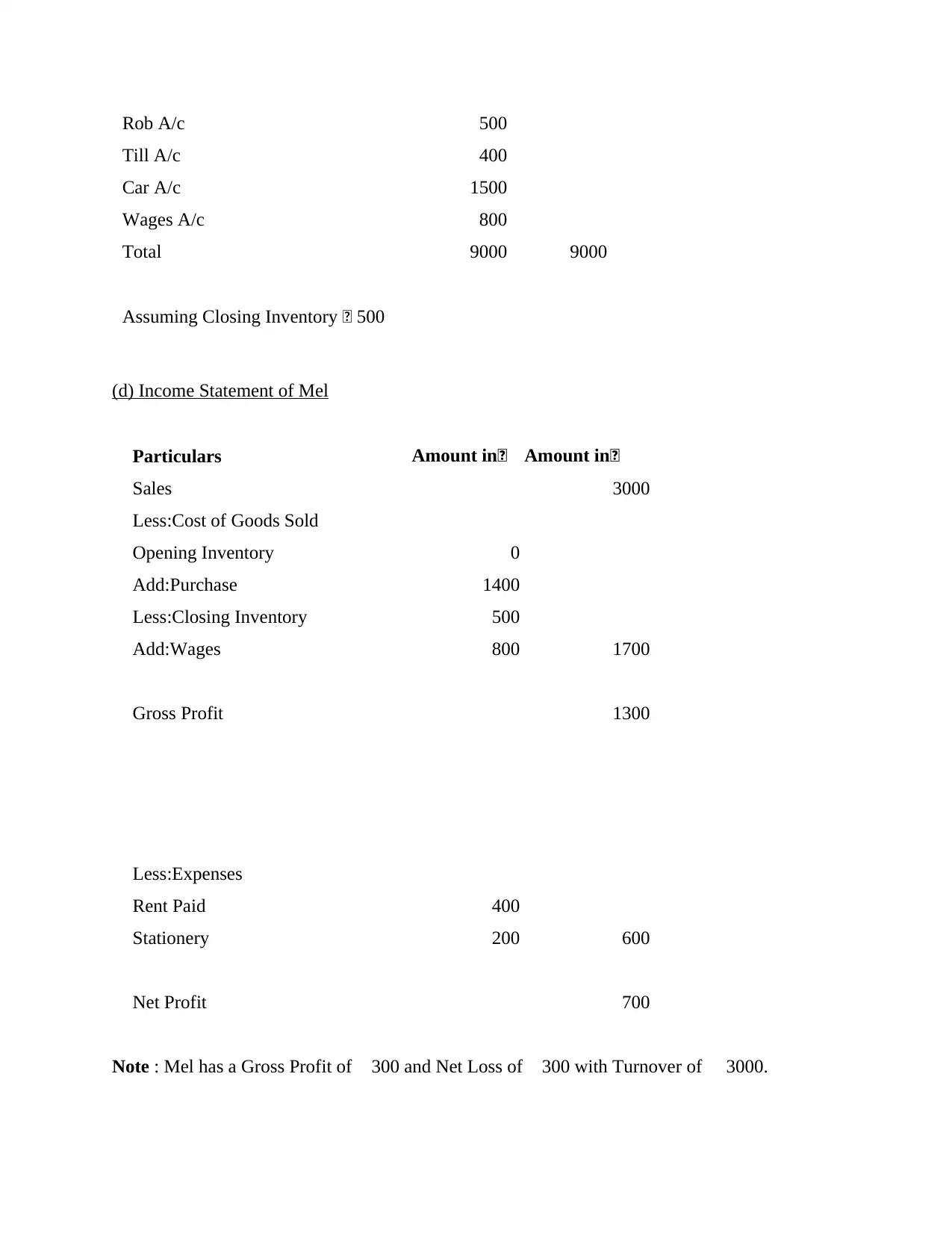

(c) Trial Balance of Mel

Particulars

Debit

Amount (£)

Credit

Amount (£)

Capital A/c 5500

Cash A/c 600

Bank A/c 2200

Purchase A/c 1400

Bill A/c 500

Computer A/c 400

Sales A/c 3000

Stationery A/c 200

Furniture A/c 600

Rent Paid A/c 400

Total 1500 Total 1500

01/10/17 To Balance b/f 1500

Wages A/c

Date Particulars Amount in£ Date Particulars Amount in£

30/09/17 To Cash A/c 800 30/09/17 By Balance c/f 800

Total 800 Total 800

01/10/17 To Balance b/f 800

Till A/c

Date Particulars Amount in£ Date Particulars Amount in£

23/09/17 To Sales A/c 400 30/09/17 By Balance c/f 400

Total 400 Total 400

01/10/17 To Balance b/f 400

(c) Trial Balance of Mel

Particulars

Debit

Amount (£)

Credit

Amount (£)

Capital A/c 5500

Cash A/c 600

Bank A/c 2200

Purchase A/c 1400

Bill A/c 500

Computer A/c 400

Sales A/c 3000

Stationery A/c 200

Furniture A/c 600

Rent Paid A/c 400

Rob A/c 500

Till A/c 400

Car A/c 1500

Wages A/c 800

Total 9000 9000

Assuming Closing Inventory £ 500

(d) Income Statement of Mel

Particulars Amount in£ Amount in£

Sales 3000

Less:Cost of Goods Sold

Opening Inventory 0

Add:Purchase 1400

Less:Closing Inventory 500

Add:Wages 800 1700

Gross Profit 1300

Less:Expenses

Rent Paid 400

Stationery 200 600

Net Profit 700

Note : Mel has a Gross Profit of £300 and Net Loss of £300 with Turnover of £ 3000.

Till A/c 400

Car A/c 1500

Wages A/c 800

Total 9000 9000

Assuming Closing Inventory £ 500

(d) Income Statement of Mel

Particulars Amount in£ Amount in£

Sales 3000

Less:Cost of Goods Sold

Opening Inventory 0

Add:Purchase 1400

Less:Closing Inventory 500

Add:Wages 800 1700

Gross Profit 1300

Less:Expenses

Rent Paid 400

Stationery 200 600

Net Profit 700

Note : Mel has a Gross Profit of £300 and Net Loss of £300 with Turnover of £ 3000.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

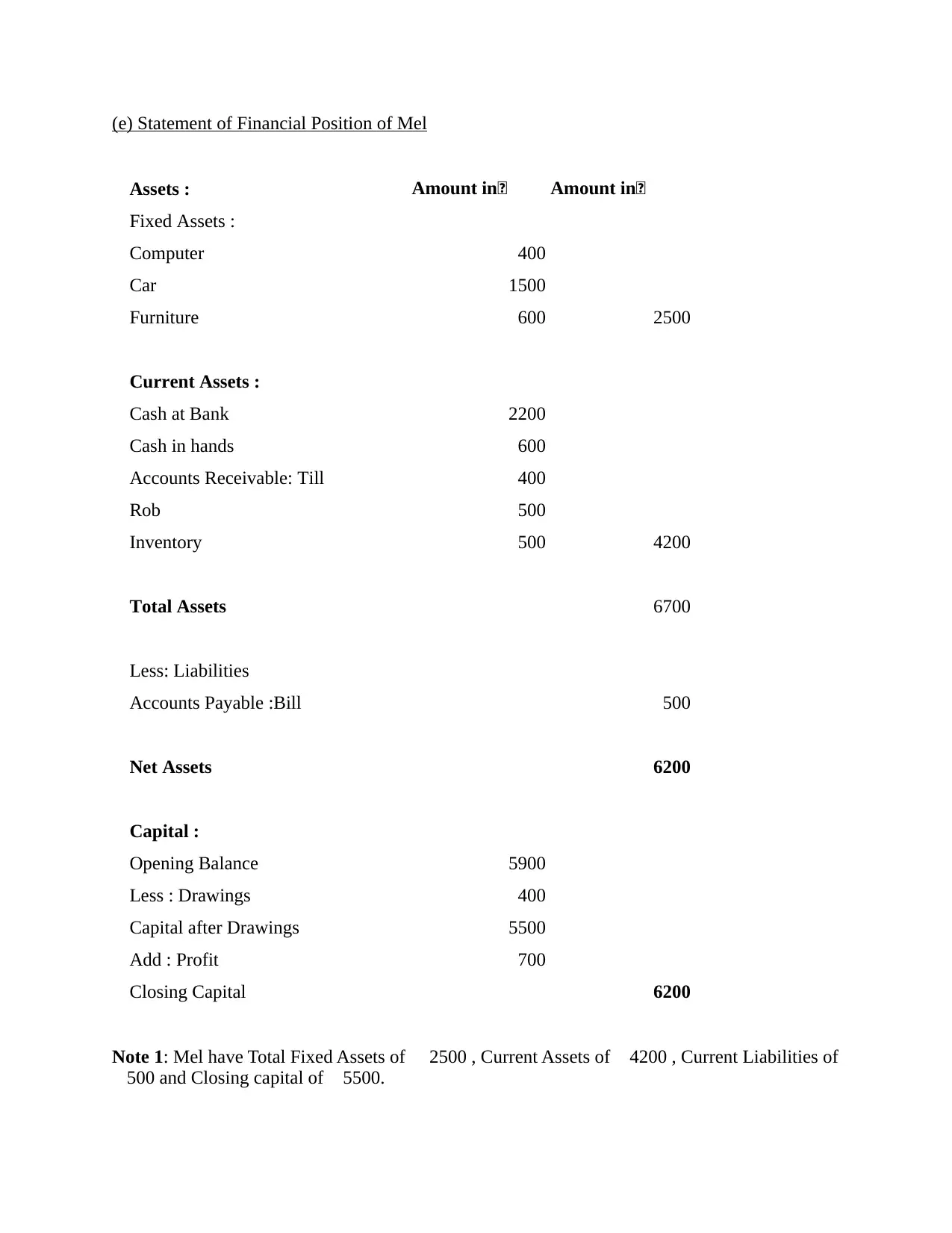

(e) Statement of Financial Position of Mel

Assets : Amount in£ Amount in£

Fixed Assets :

Computer 400

Car 1500

Furniture 600 2500

Current Assets :

Cash at Bank 2200

Cash in hands 600

Accounts Receivable: Till 400

Rob 500

Inventory 500 4200

Total Assets 6700

Less: Liabilities

Accounts Payable :Bill 500

Net Assets 6200

Capital :

Opening Balance 5900

Less : Drawings 400

Capital after Drawings 5500

Add : Profit 700

Closing Capital 6200

Note 1: Mel have Total Fixed Assets of £ 2500 , Current Assets of £4200 , Current Liabilities of

£500 and Closing capital of £5500.

Assets : Amount in£ Amount in£

Fixed Assets :

Computer 400

Car 1500

Furniture 600 2500

Current Assets :

Cash at Bank 2200

Cash in hands 600

Accounts Receivable: Till 400

Rob 500

Inventory 500 4200

Total Assets 6700

Less: Liabilities

Accounts Payable :Bill 500

Net Assets 6200

Capital :

Opening Balance 5900

Less : Drawings 400

Capital after Drawings 5500

Add : Profit 700

Closing Capital 6200

Note 1: Mel have Total Fixed Assets of £ 2500 , Current Assets of £4200 , Current Liabilities of

£500 and Closing capital of £5500.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Note 2: Working Capital means Current Assets – Current Liabilities. Therefore, working capital

of Mel is £ 3700 ( 4200 – 500 )

PART B

Ratios calculation for Mel :

(a) Net Profit Margin Ratio (%) = Net Profit / Sales *100

700 / 3000 * 100

23.33 %

This ratio exhibits company's efficiency to generate net income after providing of all

expenses. It point out towards profitability of a business organisation and it consider net profit

after deducting all expenses. Generally it is shown as percentage (Simkin, Norman and Rose,

2014).

(b) Gross Profit Margin Ratio (%) = Gross Profit / Sales *100

1300 / 3000 * 100

43.33 %

This ratio is provide a measure to evaluate company's efficiency to produce profit after

cost of goods sold. It is similar to net profit margin but in this ratio gross profit is considered to

calculate margin. Gross profit is profit after deducting all direct expenses. It also act as a measure

to evaluate company's efficiency to optimise its direct expenses.

(c) Current Ratio (Times) = Current Assets / Current Liabilities

4200 / 500

8.4 Times

Current Ratio is used by business organisation to measure its ability to use current assets like

cash, bank. Trade receivables etc. for payment of its current obligation or liabilities. It assist in

analysis of an organisation's liquidity position. A higher current ratio represents that company is

able to pay its current obligation more effectively. Where a lower ratio act as early warning

system of liquidity position of company.

(d) Acid Test Ratio (Times) = Current Assets – Inventory / Current Liabilities

(4200 - 500) / 500

7.4 Times

It points out towards an organisation's efficiency to utilise its quick assets or highly assets

to pay out its current liabilities or obligation. This ratio also known as quick asset ratio. In

calculation of this ratio quick assets are used. Quick assets refers to current assets less inventory

amount. It helps to analyse liquidity position of firm more efficiently as compared to current

asset ratio. It clearly points out towards short therm liquidity position of firm (Worrell, Di Gangi

and Bush, 2013).

of Mel is £ 3700 ( 4200 – 500 )

PART B

Ratios calculation for Mel :

(a) Net Profit Margin Ratio (%) = Net Profit / Sales *100

700 / 3000 * 100

23.33 %

This ratio exhibits company's efficiency to generate net income after providing of all

expenses. It point out towards profitability of a business organisation and it consider net profit

after deducting all expenses. Generally it is shown as percentage (Simkin, Norman and Rose,

2014).

(b) Gross Profit Margin Ratio (%) = Gross Profit / Sales *100

1300 / 3000 * 100

43.33 %

This ratio is provide a measure to evaluate company's efficiency to produce profit after

cost of goods sold. It is similar to net profit margin but in this ratio gross profit is considered to

calculate margin. Gross profit is profit after deducting all direct expenses. It also act as a measure

to evaluate company's efficiency to optimise its direct expenses.

(c) Current Ratio (Times) = Current Assets / Current Liabilities

4200 / 500

8.4 Times

Current Ratio is used by business organisation to measure its ability to use current assets like

cash, bank. Trade receivables etc. for payment of its current obligation or liabilities. It assist in

analysis of an organisation's liquidity position. A higher current ratio represents that company is

able to pay its current obligation more effectively. Where a lower ratio act as early warning

system of liquidity position of company.

(d) Acid Test Ratio (Times) = Current Assets – Inventory / Current Liabilities

(4200 - 500) / 500

7.4 Times

It points out towards an organisation's efficiency to utilise its quick assets or highly assets

to pay out its current liabilities or obligation. This ratio also known as quick asset ratio. In

calculation of this ratio quick assets are used. Quick assets refers to current assets less inventory

amount. It helps to analyse liquidity position of firm more efficiently as compared to current

asset ratio. It clearly points out towards short therm liquidity position of firm (Worrell, Di Gangi

and Bush, 2013).

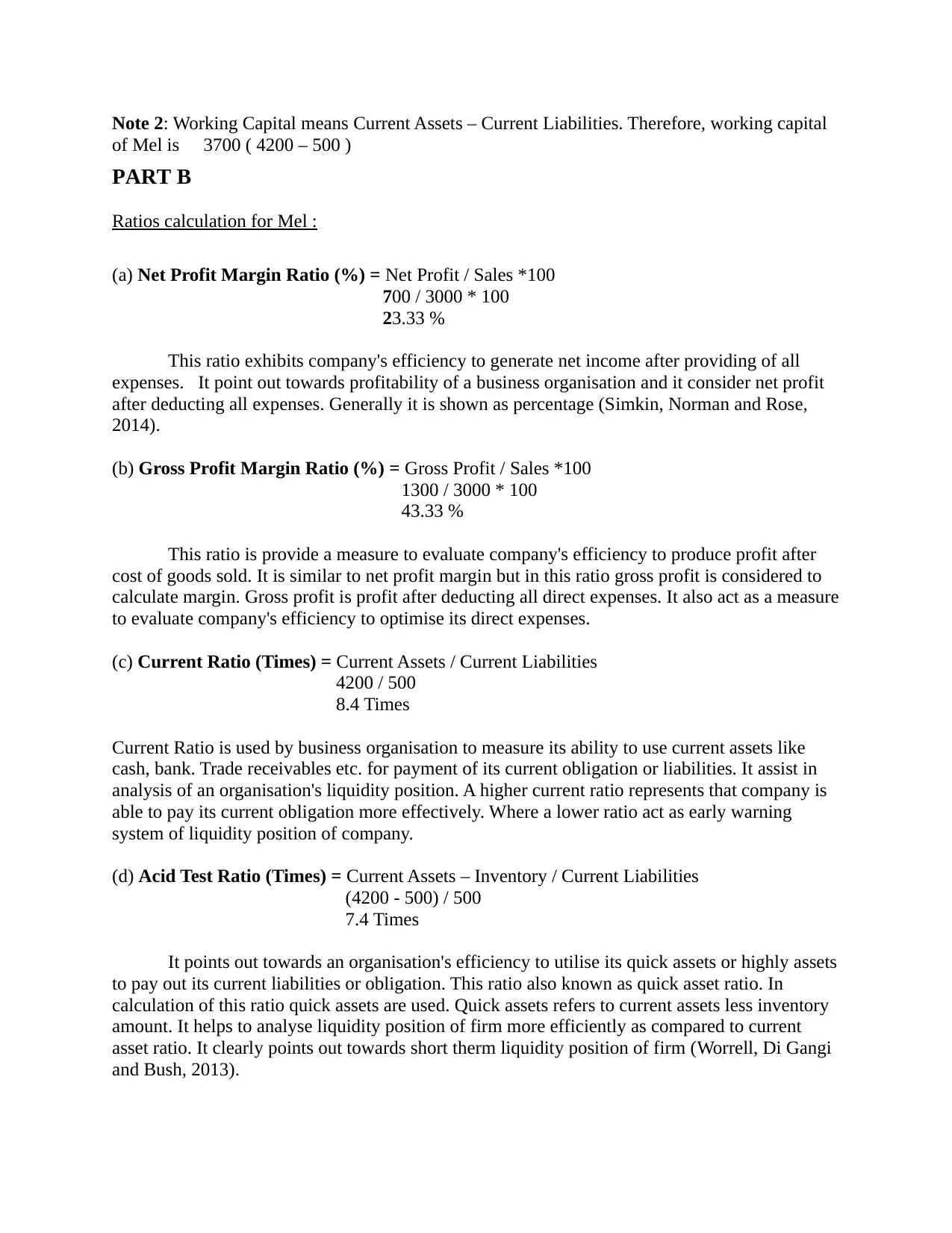

(e) Accounts receivable collection period (Days)= Accounts Receivable / Sales * 365

900 / 3000 * 365

109.5 Days

This ratio helps to compute days required for conversion of credit sales into cash. Out put

of this ratio provides average days interval in which a amount involved in credit sales is received

by organisation. It indicates company's ability to receive cash from its credit sales. Lower

accounts receivable collection period is better.

(f) Accounts payable payment period (Days)= Accounts Payable / Purchase * 365

500 / 1200 * 365

152.08 Days

It used to calculate average days that an organisation take to pay its suppliers or creditors.

It indicates how much time company took to pay amount of credit purchase. Shortly payment of

credit purchases by an organisation indicates its better liquidity position.

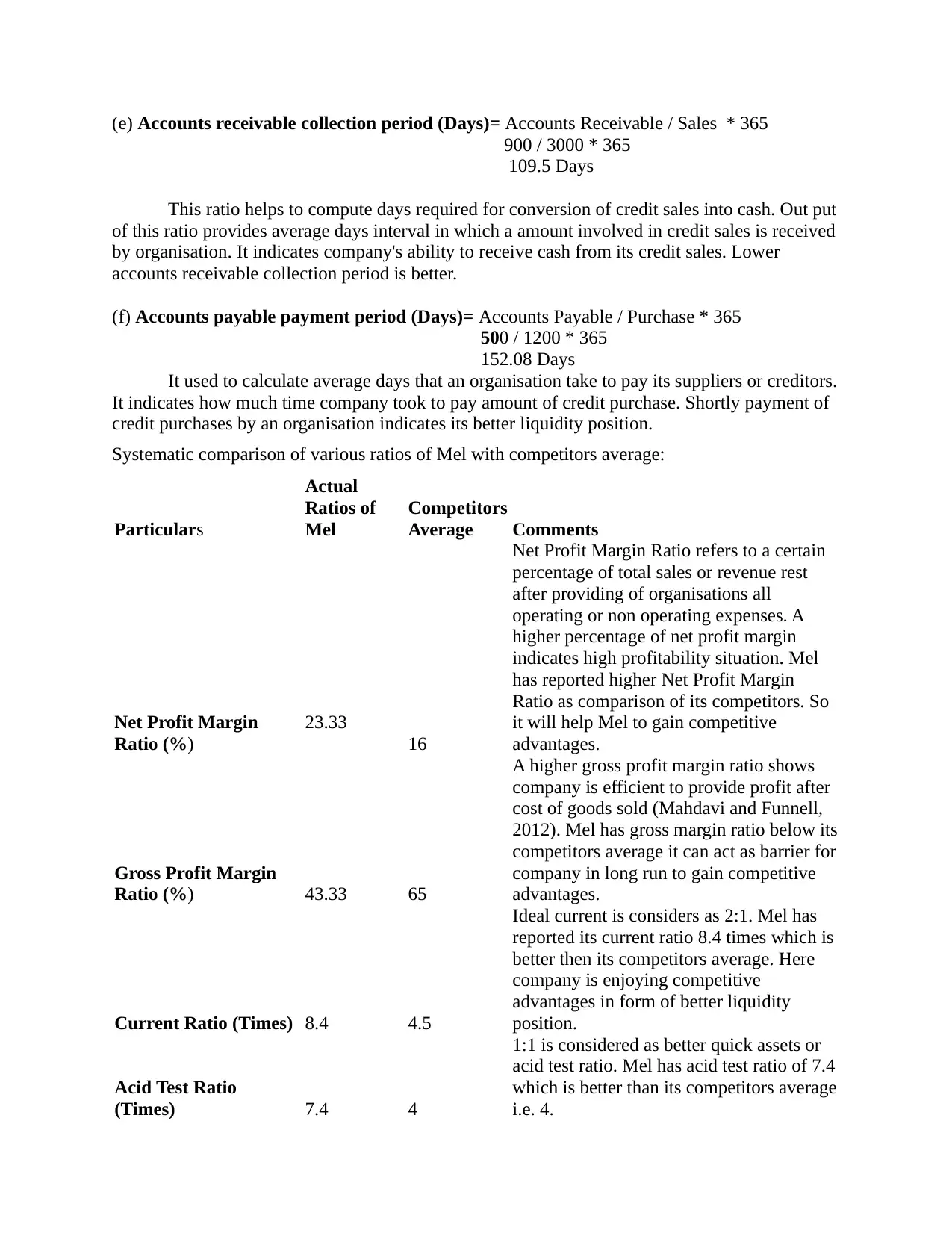

Systematic comparison of various ratios of Mel with competitors average:

Particulars

Actual

Ratios of

Mel

Competitors

Average Comments

Net Profit Margin

Ratio (%)

23.33

16

Net Profit Margin Ratio refers to a certain

percentage of total sales or revenue rest

after providing of organisations all

operating or non operating expenses. A

higher percentage of net profit margin

indicates high profitability situation. Mel

has reported higher Net Profit Margin

Ratio as comparison of its competitors. So

it will help Mel to gain competitive

advantages.

Gross Profit Margin

Ratio (%) 43.33 65

A higher gross profit margin ratio shows

company is efficient to provide profit after

cost of goods sold (Mahdavi and Funnell,

2012). Mel has gross margin ratio below its

competitors average it can act as barrier for

company in long run to gain competitive

advantages.

Current Ratio (Times) 8.4 4.5

Ideal current is considers as 2:1. Mel has

reported its current ratio 8.4 times which is

better then its competitors average. Here

company is enjoying competitive

advantages in form of better liquidity

position.

Acid Test Ratio

(Times) 7.4 4

1:1 is considered as better quick assets or

acid test ratio. Mel has acid test ratio of 7.4

which is better than its competitors average

i.e. 4.

900 / 3000 * 365

109.5 Days

This ratio helps to compute days required for conversion of credit sales into cash. Out put

of this ratio provides average days interval in which a amount involved in credit sales is received

by organisation. It indicates company's ability to receive cash from its credit sales. Lower

accounts receivable collection period is better.

(f) Accounts payable payment period (Days)= Accounts Payable / Purchase * 365

500 / 1200 * 365

152.08 Days

It used to calculate average days that an organisation take to pay its suppliers or creditors.

It indicates how much time company took to pay amount of credit purchase. Shortly payment of

credit purchases by an organisation indicates its better liquidity position.

Systematic comparison of various ratios of Mel with competitors average:

Particulars

Actual

Ratios of

Mel

Competitors

Average Comments

Net Profit Margin

Ratio (%)

23.33

16

Net Profit Margin Ratio refers to a certain

percentage of total sales or revenue rest

after providing of organisations all

operating or non operating expenses. A

higher percentage of net profit margin

indicates high profitability situation. Mel

has reported higher Net Profit Margin

Ratio as comparison of its competitors. So

it will help Mel to gain competitive

advantages.

Gross Profit Margin

Ratio (%) 43.33 65

A higher gross profit margin ratio shows

company is efficient to provide profit after

cost of goods sold (Mahdavi and Funnell,

2012). Mel has gross margin ratio below its

competitors average it can act as barrier for

company in long run to gain competitive

advantages.

Current Ratio (Times) 8.4 4.5

Ideal current is considers as 2:1. Mel has

reported its current ratio 8.4 times which is

better then its competitors average. Here

company is enjoying competitive

advantages in form of better liquidity

position.

Acid Test Ratio

(Times) 7.4 4

1:1 is considered as better quick assets or

acid test ratio. Mel has acid test ratio of 7.4

which is better than its competitors average

i.e. 4.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.