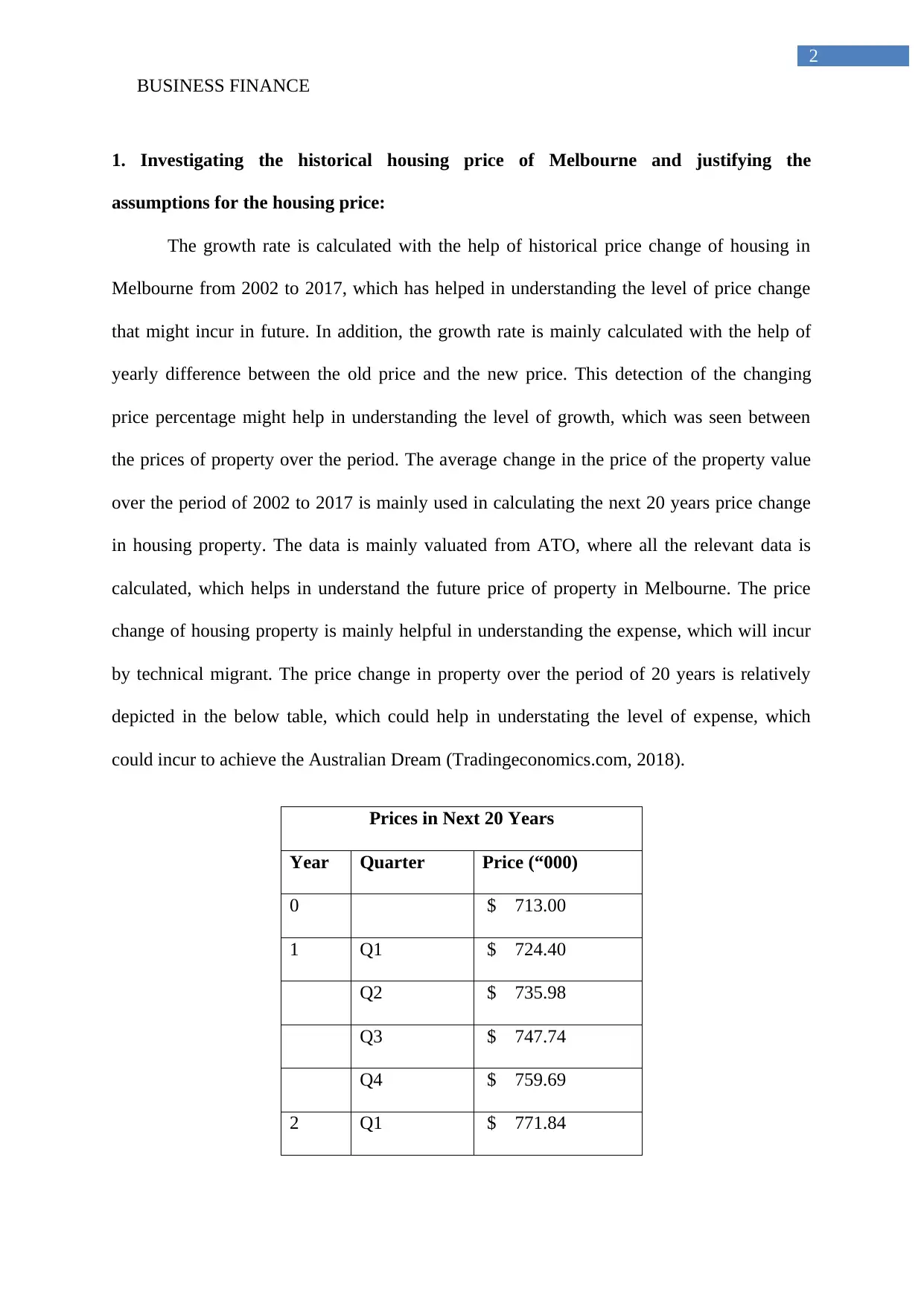

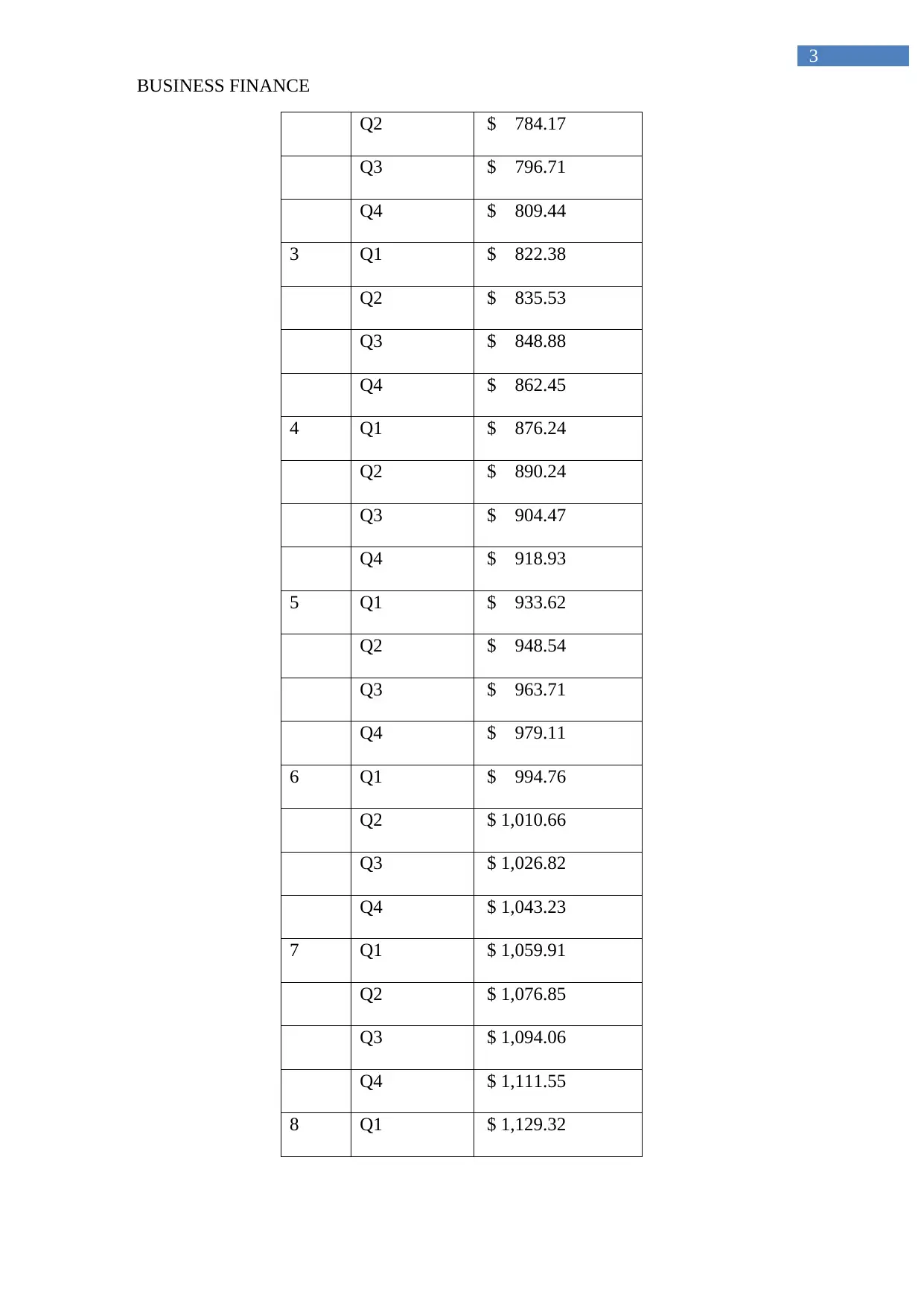

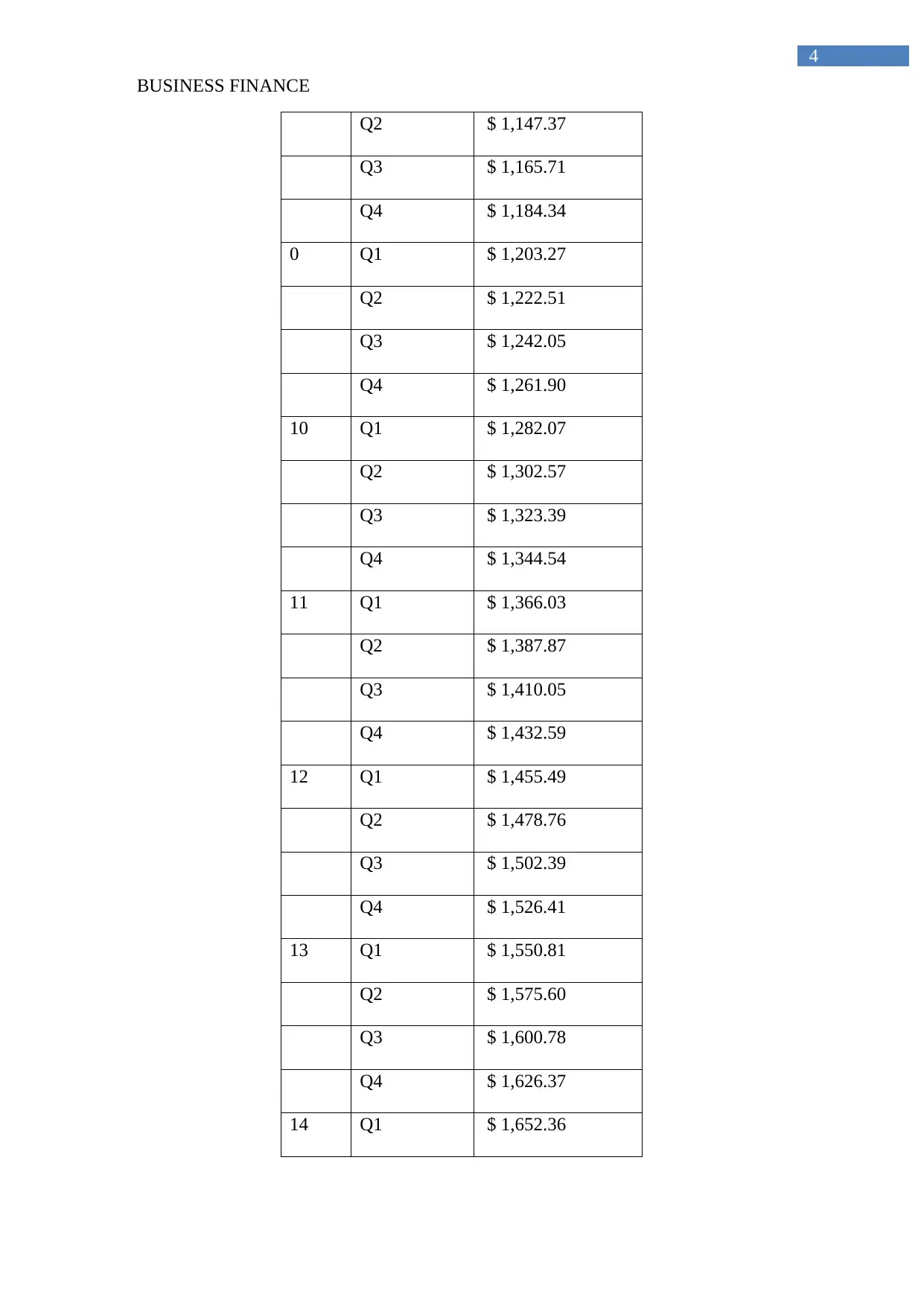

Business Finance Plan: Melbourne Housing Price and Income Analysis

VerifiedAdded on 2021/06/16

|13

|2791

|41

Project

AI Summary

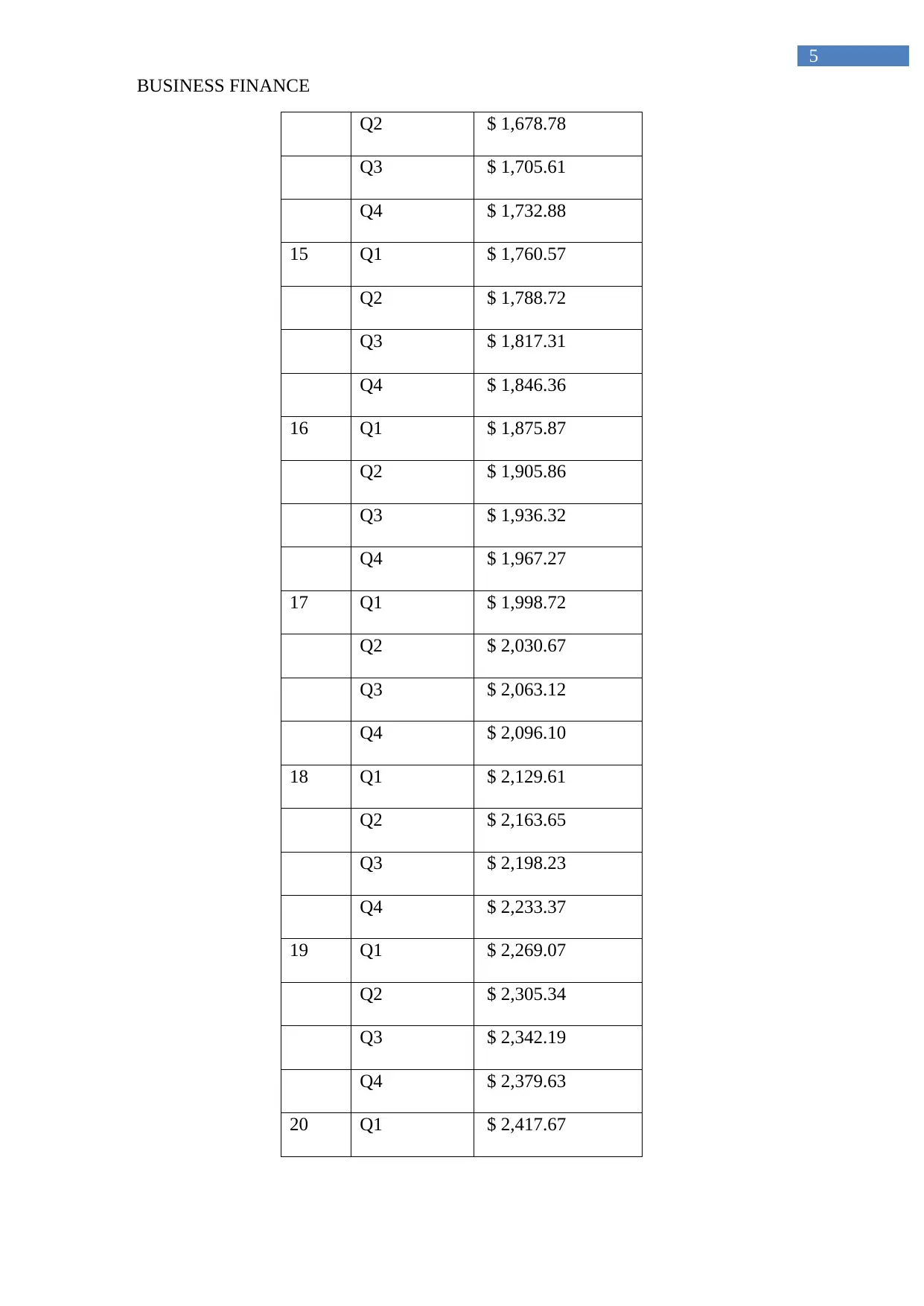

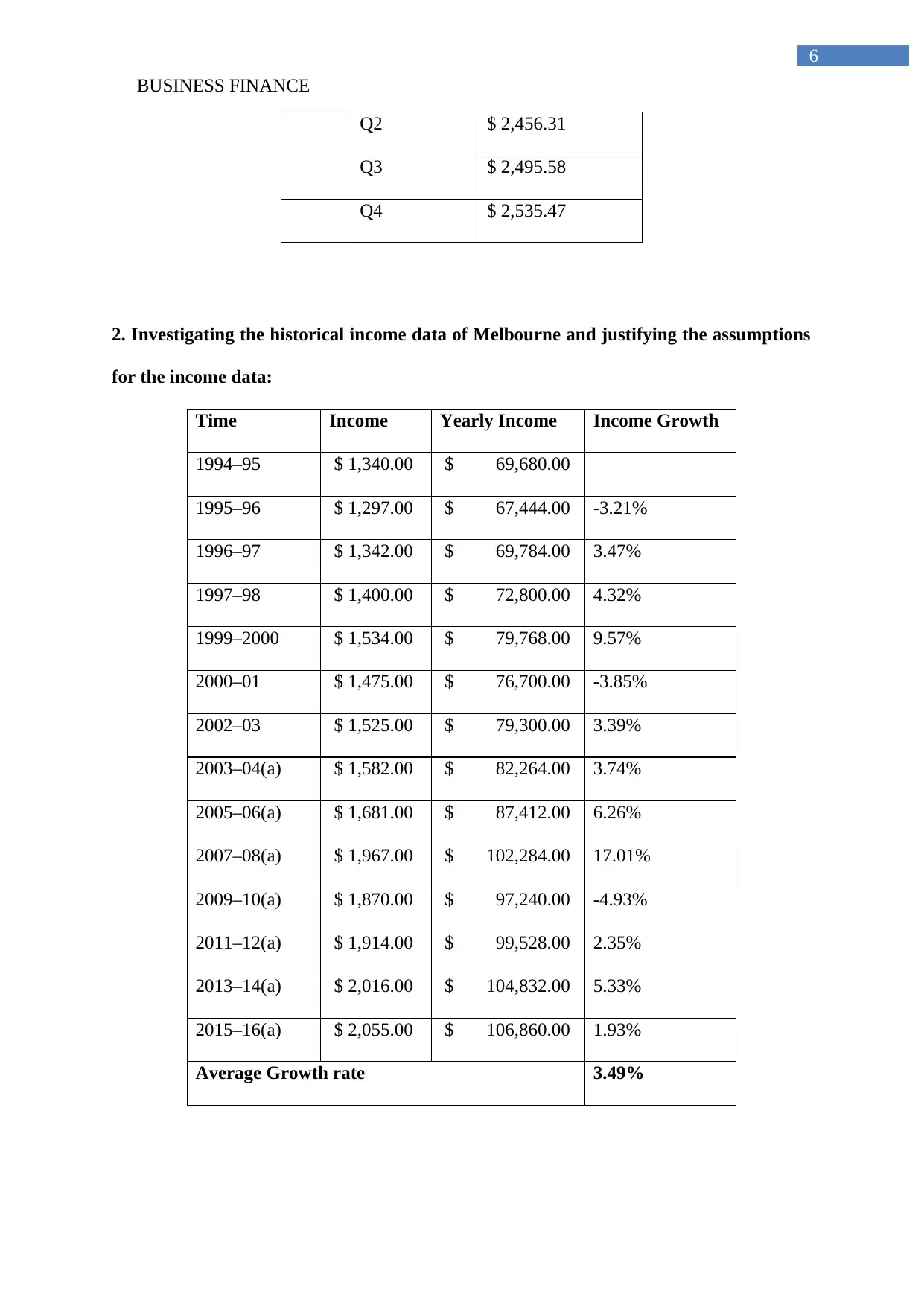

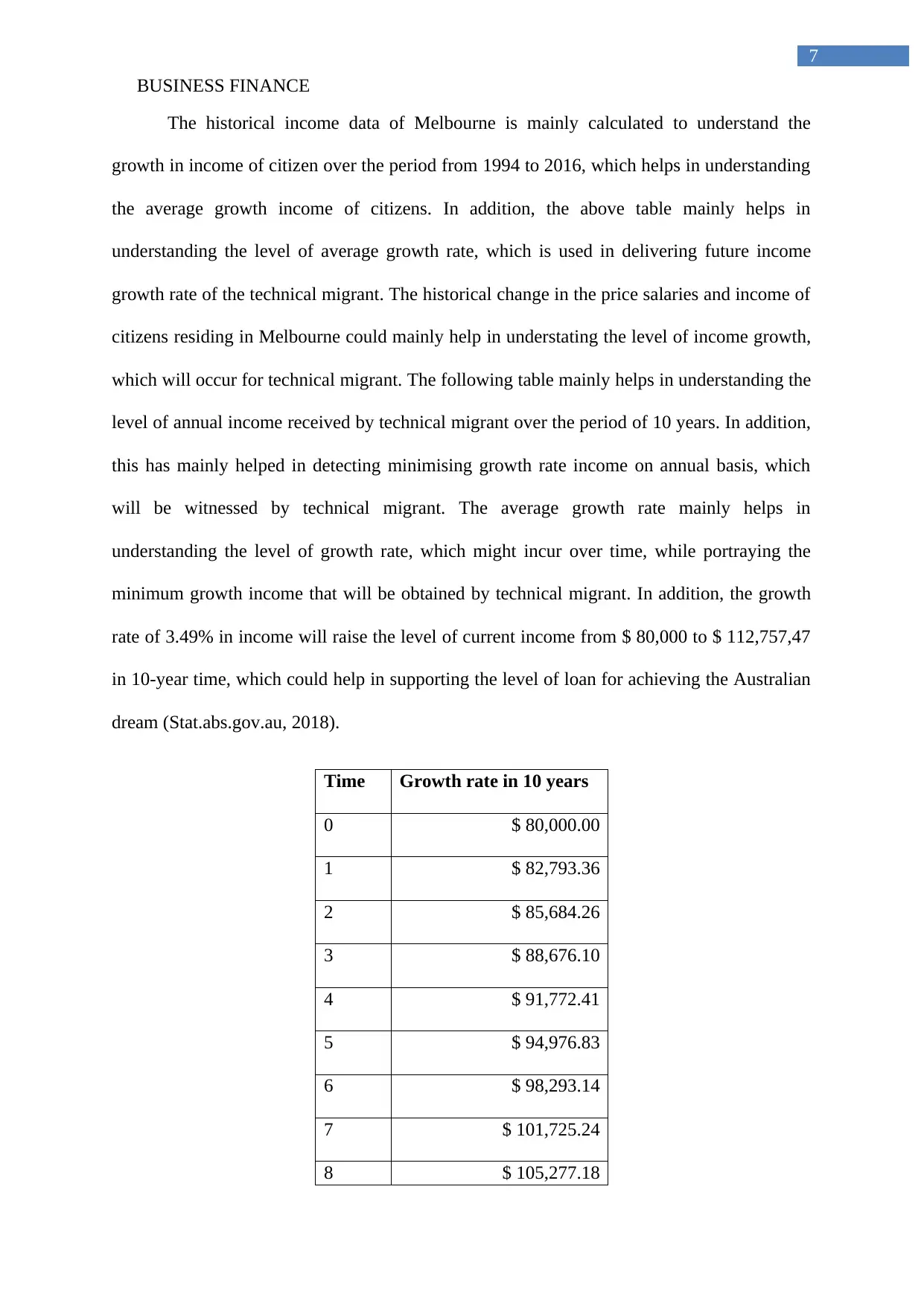

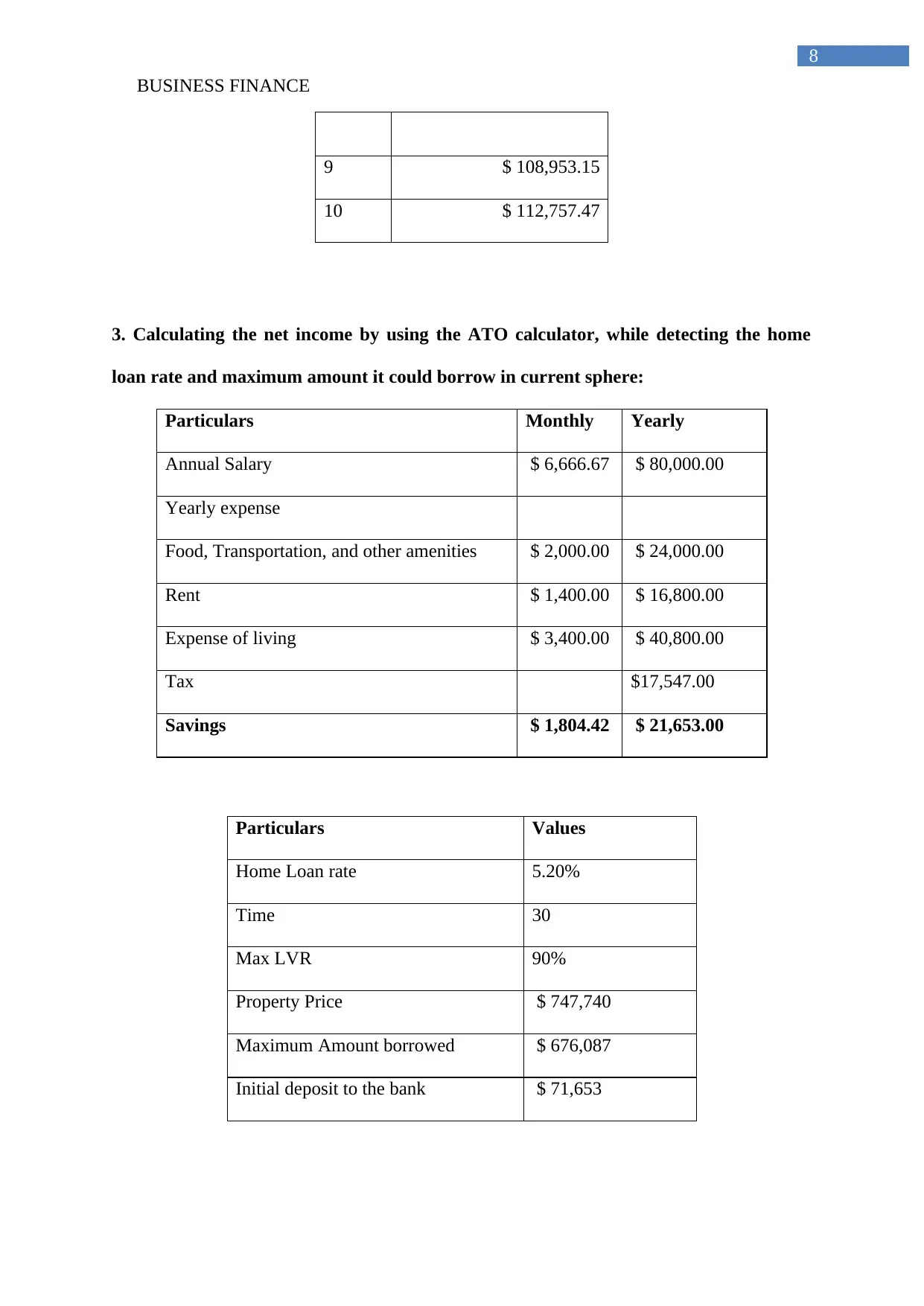

This project presents a business finance plan focused on the Melbourne housing market. It begins by investigating historical housing prices and income data, justifying assumptions made for future projections. The analysis includes calculating net income using the ATO calculator, determining home loan rates and maximum borrowing amounts. It further examines stamp duty calculations and affordability based on property prices. A detailed financial plan is drafted, considering upfront payments and loan scenarios, including the impact of interest rate changes on repayment capabilities. The project concludes with a risk assessment of the assumptions made, demonstrating the feasibility of achieving the 'Australian Dream' through property investment in Melbourne. The student utilized data from various sources to support the analysis.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.