Analysis of the Mercedes Benz Audit Report: Financial Review

VerifiedAdded on 2020/05/11

|5

|782

|41

Report

AI Summary

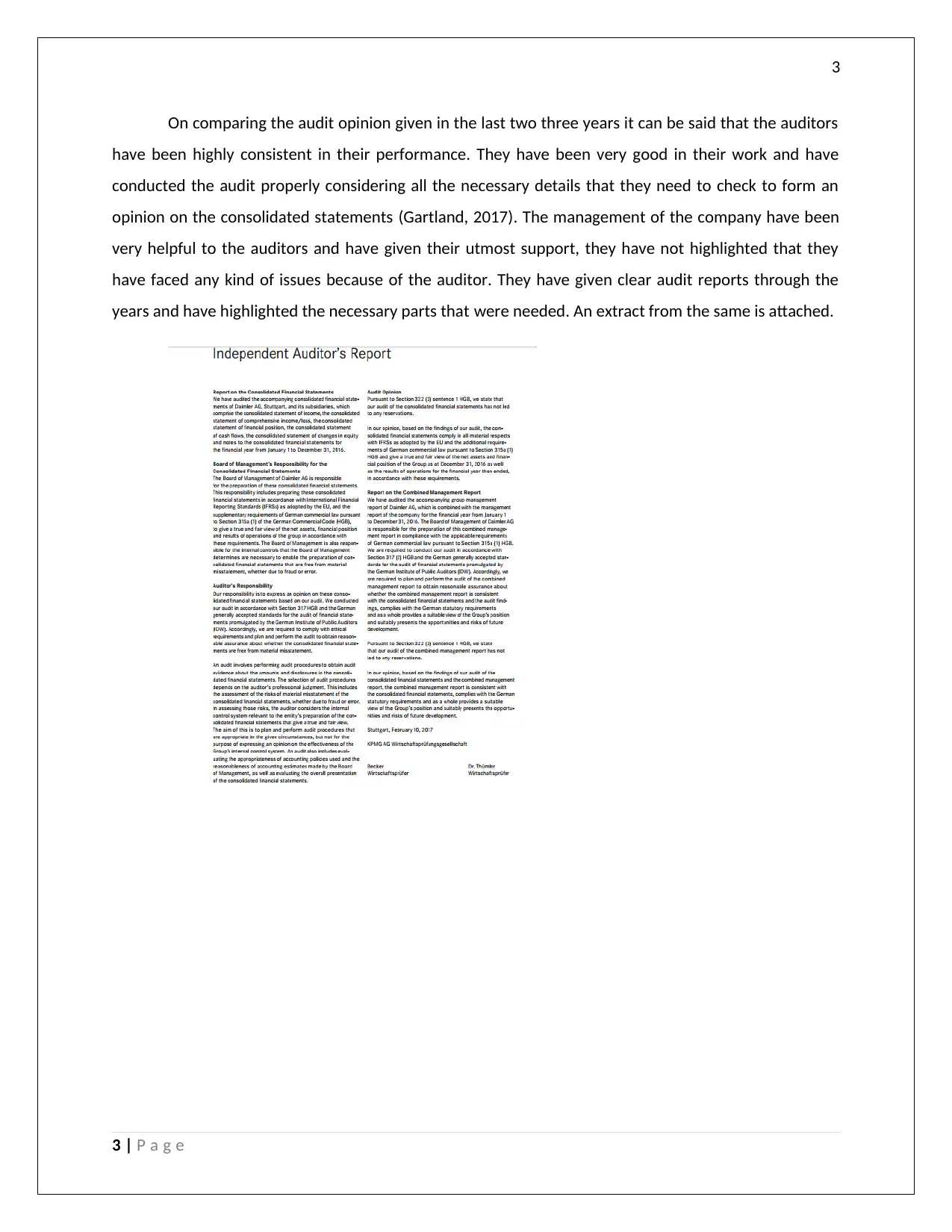

This report provides an analysis of the audit report for Mercedes Benz, a major division of Daimler AG, focusing on the role of the auditor, KPMG Global Services. The audit assesses the company's financial statements to ensure they meet the necessary standards and present a fair view, crucial for stakeholders' decision-making. The report highlights the auditor's independent opinion, which is included in Daimler's annual reports, and confirms the accuracy and lack of errors in the financial statements. It also discusses the importance of internal controls and the auditor's adherence to German generally accepted standards, as per section 317 (2) HGB. The auditors have consistently delivered positive opinions, indicating the company's strong financial reporting practices and management's cooperation. The report concludes by referencing key sources related to audit planning and competitive strategy.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.